Leeham News and Analysis

There's more to real news than a news release.

Airbus, Boeing production gaps for the A330, 777

Airbus last week announced it will reduce production on the A330ceo from 10 per month to nine per month, beginning in 4Q2015. We predicted in 1Q2014 that the rate would have to come down, due to the sharp decline in the backlog beginning in 2016.

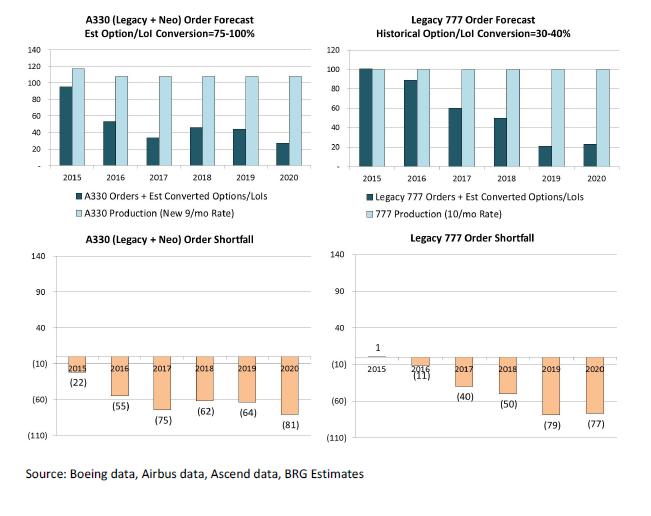

Buckingham Research Group included this chart in its note Friday about the Airbus A330 production rate cut announcement from 10/mo to 9/mo in 4Q2015. BRG predicts a 777 cut from 8.3/mo to 4.3/mo in 2017. We think the rate will step down, first to seven and then to five, before production of the 777X begins. Click image to enlarge.

We also predicted then that Boeing will have to reduce the production rate on the 777 Classic due to its sharp decline beginning in 2017.

Boeing so far continues to claim that it can maintain its production rate at 8.3/mo right through the introduction of the 777X into service in 2020. We don’t believe it can. We’ve illustrated why we believe a rate cut is inevitable. Buckingham Research Group, in a note issued Friday following the Airbus announcement, neatly encapsulates the data in a single chart.

What’s important here is that BRG (as did we) includes orders, options and Letters of Intent for both the A330 and the 777 Classic–and there still are significant gaps between the current 777 and revised A330 production rates.

- Airbus needs 337 orders (assuming 100% conversion of all options and LOIs, an unlikely prospect) to fill its order gap even at a reduced rate of nine per month.

- Boeing needs 257 orders (assuming 100% conversation of all options and LOIs, an unlikely prospect) to fill its order gap at the current production rate.

Airbus still hopes to land an order for as many as 200 A330ceo “Regionals” from China, which would go a long way toward filling its order gap–if it happens. There is an air show next month in Beijing that would be a natural forum to make an announcement, but these opportunities have come and gone in the past.

Boeing currently has 25 777s Unidentified, which are factored into our analysis and into BRG’s. President Obama will attend a pan-Asian regional conference held in Beijing concurrent with the air show, and we expect a Boeing order announcement that probably will come out of the 930 Unidentified 737 orders, the 777 backlog and maybe some of the 25 Unidentified 787 orders.

The number of 337 A330’s seems to match almost precisely the rumoured Chinese order of 200 frames, plus the Farnborough commitments for A330neo’s. I actually interpreted Airbus’s very modest A330 rate decrease, from 10/mo to 9/mo, as a statement of confidence in new orders in the near term.

I also believe Boeing has a reasonably good chance of filling the 777 slots; they have had good margins heretofore, and could probably offer better prices to offset the lower fuel burn of the A350 and 777X. Falling oil prices, as well as the limited availability of other products, may play right into Boeing’s hands. Boeing can also intermittently offer some heavily discounted 777 frames to sweeten offers in large narrow-body competitions. These large OEMs seem to be so good at what they do.

Boeing can also intermittently offer some heavily discounted 777 frames to sweeten offers in large narrow-body competitions.

Afair reading here in an earlier post Boeing has already been doing this to an astonishingly high degree. How does 50++% discount translate into reduced profits? 80% ?

The A330 charts and numbers are not entirely correct. Airbus produces A330s on an 11-month basis, thus 11 x 10 = 110 for today’s production and 11 x 9 = 99 A330s per month from 2016.

* per year of course.

It is not clear to me how many A350s will be transfered to A330NEOs within the next years?

AirAsiaX is “deferring” their A350s? So AirAsiaX will need some A330NEO earlier. How many other A350 customers are out there who would be satisfied with the range of the NEO and also like the cheaper price?

I think Buckingham Research Group made a small but significant error. According to their chart Airbus produces clearly more 100 aircraft per year at 9 aircraft per month. The Airbus year just has 10.5 or 11 months and peak delivery rate for A330 was in 2013 with 108 aircraft.

With “just” 99 A330 the picture looks better. Instead of 278 missing orders for the next 5 years I “calculate” just 233. Did BRG considered the possible few aerial tankers for India (~6), Spain (> 2), Qatar (2) and France (14) (South Korea~?) and the already exiting orders for Saudi Arabia and Singapore (12)? With about 200 A330R for China Airbus has would have no big gap.

I doubt the A330neo has anything to do with the A350 deferral. AirAsia has postponed European expansion plans due to slow growth in Europe. Therefore no A350s nor more A330neo’s are required in the nearby future.

Regarding the A330 production numbers, I agree.

The first A330NEO is scheduled to enter service Q4 2017.

http://www.airbus.com.cn/cn-aircraft-families/passengeraircraft/a330/a330-200/specifications/?type=100&tx_airbusbanner_pi1%5Bcontent%5D=videos

The first B777-9X is scheduled to enter service during 2020.

http://www.boeing.com/boeing/commercial/777X/index.page

That is an additional is 2+ years of slots to be filled by Boeing, and not by Airbus; ~ 200+ aircraft.

Airbus has 250 firm orders for the A330-200/300s

http://www.airbus.com/company/market/orders-deliveries/?eID=maglisting_push&tx_maglisting_pi1%5BdocID%5D=40940

Boeing 280 firm for the 777-200/300s

http://active.boeing.com/commercial/orders/index.cfm?content=modelselection.cfm&pageid=m15525

-> The impression Airbus needs far more new orders to keep the A330 line going then Boeing the 777 line is beyond me.

The “trick” is to continue A330 statistics 3 years beyond EIS ( 2020) of its NEO sibling while closing the 777 window at the same time ( and EIS of the 777X.

But ramp up of the 777X will be (much?) slower than the A330 transition.

777-300ER/-F production will have to continue well beyond 2020 for Boeing to keep up Widebody deliveries. ( Any numbers around re 777X ramp up? )

There is no “trick” because the chart for the A330 is for CEO and NEO together.

It is not obvious from the pure order count when Airbus and Boeing had to deliver the A330 or B777. Maybe Boeing has a lot of 777 orders after 2020.

One manufacturer offers a new engine option (NEO) version while the other one offers a new wing with folding wingtips, new engines option and a different interior fuselage structure to fit in X-abreast more comfortable (NWwFWTNEOaDIFS). The question for further gaps will be delays of EIS.

How will FAA certify folding wing tips after the 787 lithium certification disaster?

How will FAA certify folding wing tips after the 787 lithium certification disaster?

The same way they will certify new A330 engines after the A380 wing cracks disaster.

The undesirable behavior of the ribfeet in the A380 weren’t really a certification issue, were they? An expensive blunder, obviously, but not a Swiss111 waiting to happen.

In contrast FAA decidedly appeared rather undesirably exposed in the batteries bruhaha. All the kings horses and all the kings men can’t take away from the dangers of a fire on board.

Something goes wrong in the BRG graphs. Where are the 121 A330 NEO for AirAsiaX, Transaero, ALS, Avolon and CIT, from 2017? BRG left the NEO’s out all A330NEO slots 2017-2020, didn’t they? Why? It’s distorting the picture.

http://airchive.com/blog/wp-content/uploads/2014/07/A330neoAirAsiaX-1.jpg

We can’t speak for BRG but having looked ourselves these orders aren’t booked yet so delivery dates aren’t in Ascend. Therefore we, in our own analysis, can’t assign timelines for the airplanes from 2018 (the first neo is slated for delivery in 12/2017). The neo commitments don’t affect delivery dates of the ceo in 2015-17 and as yet we don’t have visibility of the DDs or production ramp-up for the neo. We presume BRG to be in the same position.

Airbus intends to deliver the last CEOs before 2020 ?

What kind of timeline is Boeing planning for the 777 to 777X transition?

The line will fully switch to NEO in 2019.

That would amount to about 500 A330CEO slated for delivery.

Requiring another 250 hard sales?

Apropos, the A330 regional is said to be a CEO derivative.

Will it be sold beyond 2019 then?

Airbus would indeed need another +- 250 CEO sales if they want to hold the announced production rate of 9 aircraft per month.

Achieving this target will be challenging but it’s not impossible. On average Airbus seems to be selling 60 A330s annually. They are only 19 short for 2014. I suppose there will be less sales in the coming years, say we make the following prediction:

– 2015: 50 net

– 2016: 40 net

– 2017: 30 net

– 2018: 20 net

Total: 140

– Chinese order: 150

Total: 290

That should be enough CEO orders to bridge the NEO. Please note, unlike BRG claims, Airbus does not need 337 new orders (Airbus produces A330s during 11 months a year, not 12).

Bottom line: bridging the NEO will be challenging but it’s not impossible. It all depends on the Chinese order for a large chuck of (regional) A330 jets. If the deal fails to materialize, a further cut will be necessary.

BRG mentions: “estimations, CEO’s, NEO’s, forecast, conversions, LOI’s” and but nonetheless leaves out all NEO’s for 2018-20. That’s what I would call smart perception management.

Adding 30 A330 NEO’s to each 2018, 2019 and 2020, plus 5-10 777-9s to 2020 would IMO paint a far more realistic picture. Because the A330 launching customers say so.

http://aviationweek.com/site-files/aviationweek.com/files/uploads/2014/07/AW_07_21_2014_2560L.jpg

That’s still well below the current and announced production rates, and that’s the underlying point. They aren’t sustainable.

True, very true. As mentioned below, Airbus needs the big Chinese A330 order if they want to hold this rate.

An A330 NEO is 25% cheaper than a 787, I recon Airbus and RR will want a $20 mil premium for the A330, so A330~$100 mil=A330 NEO~$120mil=787~$160 mil. $60 mil price difference=$600,000 USD month capital difference=600MT A1, or more, can´t see why Airbus can´t shift A330 CEOs if they want to, oil isn´t going up in the near future.

Over 5 years Airbus will nearly double wide body production and must be nearing the point where they need to send people to Alabama to help set up a greenfields A320 line. Are you sure they have enough experienced people for all that and 10x330s month? I recon it might be planned to slow down the A330 line as needed to keep everything else on track.

Secondly can suppliers meet demand for all this, esp as a thousand or so A320s have or are going to be upsized, requiring another 40000 seats more than has been planned for?

The native workers for Mobile are already building A320s since January 2014:

http://www.airbus.com/presscentre/pressreleases/press-release-detail/detail/first-manufacturing-employees-for-airbus-assembly-line-in-mobile-alabama-start-training-in-hamburg/

I guess down there in Alabama they speak much better English than in Tianjin.

The US is stuffed with skilled aerospace workers from Wichita, Washington state, Long Beach and the defense industry. They’ll move over if the prospects are good.

If we assume:

– Airbus will deliver first A330 NEO late 2017

– Boeing will deliver first 777-9 in 2020

– Airbus fully converts A330 line to NEO in 2019

– Boeing starts converting FAL in 2019 & delivers 15 777-9s in 2020

Deliveries look like this: http://i191.photobucket.com/albums/z160/keesje_pics/A330B777gap_zpsc7e0ba66.jpg

The A330 line looks pretty OK this decade, even without too much further orders. Not the record level of 2014, but that’s probably not a rock solid requirement with the A350/A321NEOs ramping up.

I expect Boeing pulling all stops to start delivering 777-9s by 2020, because at that time long time 777 customers like JAL, BA, UA, AF/KL, AA, QR, SQ, CX are well underway growing their A350(-1000) fleets.

While you’re on it, you might want to reduce the A330 rates as well (9x 11 = 99 per year).

Boeing sees demand for 40 to 60 current model 777s per year to bridge the gap with the 777X.

http://twitter.com/R_Wall/status/524933047532421120