Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- GE testing of giant GE9X engine aims for maturity at entry into service June 30, 2025

- Bjorn’s Corner: Air Transport’s route to 2050. Part 28. June 27, 2025

- Parent agency, FAA often at odds as politics outweighs safety June 26, 2025

- Electric Flight and the Ugly Duckling June 25, 2025

- Engine makers tout “Plan A” but have “Plan B” backups in R&D June 23, 2025

Pontifications: Dissecting Boeing’s 2016 delivery guidance

By Scott Hamilton

Feb. 8, 2016, © Leeham Co.: Boeing’s surprise guidance for 2016 for fewer deliveries on the 737 and 767 lines raised as many questions as officials answered on the Jan. 27 earnings call.

The lower guidance led to about a 9% drop in stock, from $128 to $115. As of Friday, the stock had recovered some, trading in the low $120s.

Boeing’s explanation about the lower guidance for 737 deliveries—12 fewer this year than in 2015—seemed, on the surface, reasonable. As the 737 MAX entered production, both with test aircraft and the first production airplanes, officials said this will lead to fewer deliveries of the NG.

But as stock analysts digested the information, skepticism arose. David Strauss of UBS issued a note last week in which he concluded the real reason for the lower deliveries is a likely production gap—not enough NG sales were achieved to bridge the gap from the NG to the MAX.

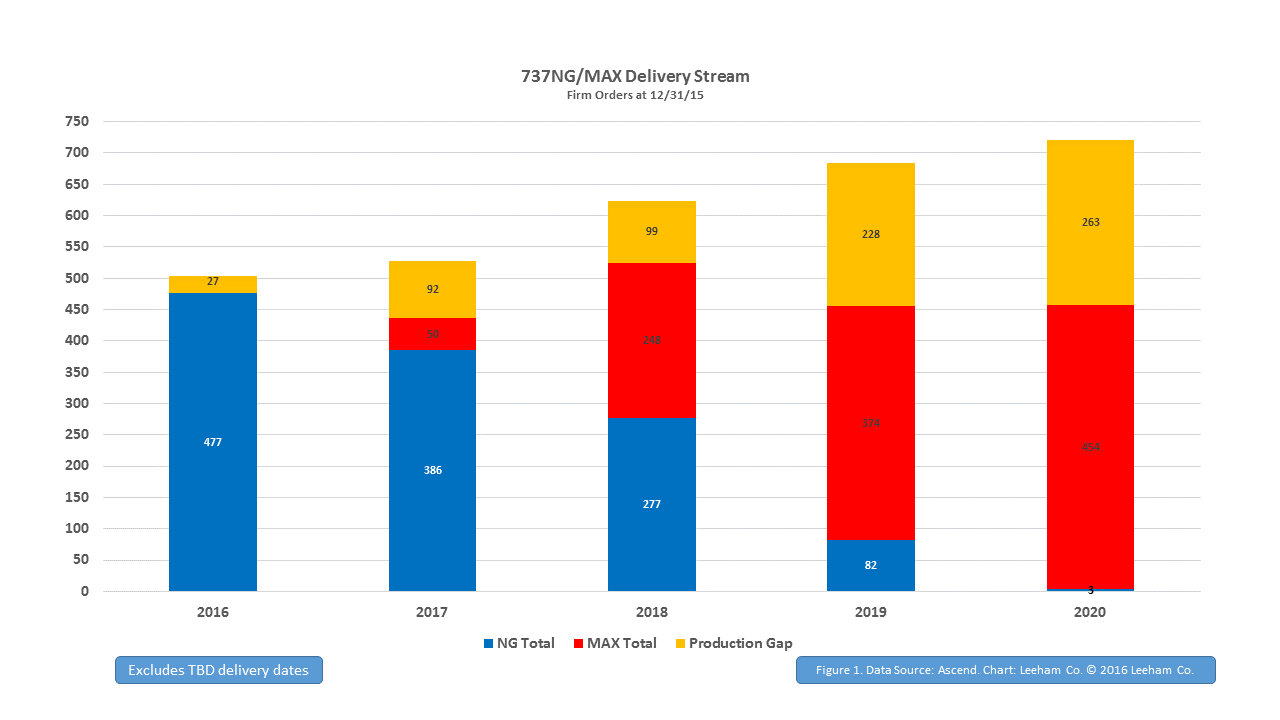

Figure 1. Boeing 737 production gap. Click on image to enlarge.

The production rate is 42/mo or 504/yr. According to the Ascend data base, only 477 NGs were scheduled to be produced this year. Deliveries are estimated at 493—the difference may be in Unidentified customers for which delivery dates are not identified in the Ascend data base, or late 2015 builds scheduled to 2016 deliveries.

Either way, UBS’ Strauss wrote last week:

While BA’s explanation seems straightforward, we find it unusual that BA hadn’t indicated any impact on 2016 NG deliveries from MAX prior to this (it also doesn’t appear there was any impact in 2015 when BA mostly built four flight test aircraft). By building more MAX’s in 2016 than expected, BA is partially pulling what we had expected would be a 2017 working capital hit into 2016.

Gap in bridge to MAX

We believe lower 737NG deliveries could be attributable to a gap in the bridge to MAX and therefore BA is diverting available capacity from the NG to the MAX earlier than expected. While BA has ~1,300 737NG’s in backlog currently, examining the most recent Ascend data would indicate unfilled NG slots during the bridge period.

LNC first raised the prospect of a production gap in the 737 line last September.

Furthermore, our Market Intelligence continued to indicate worries at Boeing that bridging the gap was a challenge. We understand that United Airlines’ recent order for 40 737-700s had a connection to bridging the gap and that a low sales price was, among other things, one of the incentives for Boeing to order this airplane.

We also learned late last year that because of worries over the gap, Boeing wanted to accelerate MAX deliveries as much as possible into 2017 and 2018.

Last week, Jon Ostrower of The Wall Street Journal reported Boeing eyes a six month early EIS. Boeing CFO Greg Smith later downplayed this timeline, but didn’t outright deny it. But this is consistent with the thesis we heard last year.

767 Guidance

Boeing also said it will deliver six fewer 767s this year than last. This, too, was a negative surprise for analysts. Officials said ramp up of the KC-46A refueling tanker was the reason. Again, skepticism emerged on Wall Street. One analyst I talked with noted that production is going up yet deliveries are going down. He wasn’t buying into Boeing’s argument.

777 Guidance

On the earnings call, Boeing said the 777 Classic delivery slots for 2017 are 80% committed. This leaves 20 slots unfilled. Given that Buyer Furnished Equipment needs about an 18 month lead to buy the interiors for passenger airplanes, time is getting short. Freighters don’t need this lead time, but the weak cargo market remains a challenge.

If you look at Boeing’s Unfilled order website, there were 33 Unidentifieds at year-end. It’s certainly possible a few of these are scheduled for 2017 delivery, but it’s unlikely that some 20 are.

LNC continues to believe another production rate cut below the seven confirmed by Boeing last month will be needed.

Boeing sales people are WILLING the market to respond to 737NG, 767-2c and 777 Classic throughput maxima, but unfortunately at little avail … till the beancounters – more prosaic – ring the bell and say ‘Gentlemen, let’s take the bull by the horns …’. The stock market reacts, not to the factual situation itself, which isn’t alarming, but rather to the way Boeing are communicating, which creates distrust in the ability of Boeing management to cope with said situation … a rather unnecessary boomerang effect that could have been averted ?!

The 767-2C is not a commercial aircraft. Despite labeled by Boeing as one only the US Air Force will order this updated 767-200. All the parcel movers will stay with the longer 767-300F.

Whatever you say, MHalblaub, feel free to change ‘767-2C’ with ‘767F’ in my comment and – thus amended – my comment stands, oder ?

And yes the 2C is a commercial aircraft certified to commercial standards.

No one may buy it, but that does not change what it is.

The 767-2C is more accurately described as a ‘short body 767-300F’, as when you have the wings , empennage, and reinforced floor from the in production 300F model, thats where the lineage points to.

Would this mean that the P-8 Poseidon have an internal Boeing designation of 737-8P ( the Clipper being the 737-7C)?

Re 737 Part of the gap can be built up by

– lower sales than Airbus and

-although Boeing decided to build the MAX about 6 month after Airbus announced NEO Max will appear 18 months after the NEO

Are changes to the NG so important that they cannot produce earlier ?? Thus creating a gap

Quite Interesting / amusing after the “_deliveries_ are the relevant metric in computing market share” meme was released (pushed ) into the wild recently.

Noteworthy is the low quality of the explanations.

Used to be more inventive ( and found a more gullible reception back in the times ..)

The 767 might be a different story. I guess it will take Boeing much longer to produce a full equipt KC-46 than a 767-300F.

On the other side the final delivery date to US Air Force might not so important. It is far more important when the USAF pays for something.

It looks like analysts are punishing BA for suspected past misdemeanours. There seems to be a certain lack of trust in the explanations given by senior management.

The much heralded increases in production rates of the 737 in whatever guise and whenever it will happens seems to gloss over the impact of NG/MAX transition in the short to medium term. Together with the 767/777 obfuscation you can understand certain skepticism in some quarters.

On the other hand the cost/ revenue balance of the 787 appears to be progressing amazingly well. Has Boeing really managed to drive down costs and increase pricing so much as to hit near unit breakeven? Or should we be skeptical of that as well…….

I think Boeing has made great progress with the 787 costs in the last year, or so, as the 787-9s have started rolling off the production line. Not only is the 787-9 priced higher (reportedly ~$140M as opposed to ~$120m for 787-8) , it probably probably does not also suffer the low selling prices that the initial 787-8s. Boeing seems to be able to produce the 787-9 at a slight profit, but the 787-8 seems to be hopeless as far as profit is concerned (I’m guessing based on a greatly reduced deffered costs as 787-9s are introduced). Nevertheless, the backlogs of 787-8s are not large and Boeing has more-or-less quit selling this plane (just a few terrible teens and specialty orders have been logged over the last couple of years). Once Boeing is free of the 787-8 backlog, it should be relatively smooth sailing (i.e., they should be consistently profitable on the 787 line).

Of course, the prices for the 787-9 will always be pressured by the A350-900 and the A330-900, but at least the deferred costs will stop accruing. Meanwhile, Airbus will very busy trying to produce the A350-900 at a profit. I’ve seen Airbus chart pitches that indicate a 2019 Break-even for the A350 (that’s on a “per unit” basis). OMG: what a task they have before them! I hope they are being pessimistic (i.e., under promise and over deliver).

Yes I was guessing the 787-9 was the fundamental reason. The costs can’t have fallen that much so it had to be about pricing more than anything else. Now the long haul to paying back the deferred costs. I was being slightly facetious……

increasing production will have been some help too.

Pricing info:

https://www.flightglobal.com/news/articles/analysis-boeing-787-historic-pricing-discounts-put-pressure-on-programmes-351323/

IMHO there are actually some little bombs in the production pricing info from the FG article.

To the host:

Do the risk sharing partners work under a gag order in respect to pricing/profits ?

Does this mean that Boeing will end up with a backlog of airframes/inventory waiting for engines or is Leap-1B as far ahead as well?

“price was, among other things, one of the incentives for Boeing to order this airplane”

Scot: Nit noid police believe you meant to say United in that statement not Boeing.

Based on the chart, BA will delivery roughly 750 737NGs through 2019, and after that, production will end.

But there are about 1300 firm orders listed by BA, so what will happen to the other 550? There are almost 300 for unidentified customers, but that leaves 250 for identified customers, with no set delivery dates. Will these aircraft actually get built?

And has there been a similar transition analysis for the A320 series?

750 NG ??

477 + 386 + 277 + 82

= 1222

planned NG deliveries! 2016 through 2019

Math problem! All that education for naught! Thanks for correcting that, Uwe. So actually only about 120 NG aircraft don’t fit into that production schedule ((1300 backlog as of 2016-02-01 plus 42 January production) – 1222 production for 2016-2019).

Sorry, a math problem, all that education all for naught! It seems only 120 aircraft are unaccounted for: 42 for January production plus the remaining 1300 orders for 1342 total, less 1222 planned deliveries based on the charts.

Thanks, Uwe.

I need to have my wife check the bills I write.

I never get the cents right 🙂

Hey Scott what about the GTF story? I went long again, but I just got to know!!!

You got anything about what is being done to address that issue? Has the s/w mod worked? Has LH been flying the NEO and has the startup issue been an issue during LH evaluations? Airbus is flying the LEAP A321 and not the PW GTF? What is going with that issue, and could that issue have an impact on the NEO delivery schedule for the year? What gives and will that have an impact on the number of A320NEO sitting around the plant waiting to be delivered? I see some stories and rumblings going on about that. I know the Boeing shortfall was hot last week, but can you get us some info about the more current GTF issues? Can you tell us what is going on with MAX performance post first, second and third flight? There has been mention the LEAP-1B was missing its marks early in testing on the 747 testbed, were there any comments about what the first frame saw, and were those same concerns seen in flight test? Guess at this point, if MAX comes out the box performing better than NEO/GTF we might see a much larger shortfall in the NEO deliveries and sales, and that might be a story of import? Boeing says they will deliver early, what does early look like? Can the industry accept early because if what you say is true, if MAX is early will the current config end sooner? I know Boeing is going to miss its numbers and I know the stock will be hit by that, but UT and Airbus could be slammed by the GTF not hitting its marks also. Would think that might be a story the entire industry might find concerning considering the large lead Airbus has in single aisle? And, if the NEO numbers on the A321 GTF engine are not as earth changing as once assumed, maybe all those A321NEO sales might be of concern also?

I know Boeing is keeping the MAX numbers close to the vest but I bet cfm would certainly like to stick it to the UT guys if MAX is doing better than GTF NEO? Now that would be worth knowing about across the industry.

Production slow downs are coming, China is having major issues with their economy right now so, so Airbus is going to see a drop in production as well. How will the China plant function within the economic slowdown? All that shuffling Airbus used in the past to keep the 320 line going will certainly be needed, because everyone buys in consistent quantities. When I can get a NEO versus a classic, will I do it, and will that impact the cross over mix? Will it impact profitability? Do a comparison of the impacts to both companies, hey that stuff is some real mess for your readers!! Might shut the stupid fan crap down when you see both companies numbers!!!

A330s will be coming off lease and they are going to impact A330 sales, Iran can only take so many of those open slots so the holes will get bigger for both sides of the pond.

cfm just said their start up times were in line with current configs, which I assume to be a dig at UT? Is that true, and if it is will that mean that more current GTF customers might shift to LEAP, and can LEAP actually handle the stronger shift in demand? Compare the engine suppliers please, another set of stocks you can impact.

Guess I’m saying thanks for the pontification on Boeing but honestly that is a small story in aerospace right now. I mean from all of the write up that’s already been done by every analyst in the world. Everyone please move on!!! There is something bigger going on and it has to do with whether UT has solved its start up production issues for GTF. This is the second time they have tried to push into the single aisle commercial market, and the last time things did not go well (not the Rolls JV but directly through PW). Are we seeing those same concerns creeping into the GTF program? Does the past have a concern on Airbus and how are they dealing with the potential? There has to be some major hallway discussion going on right now at Airbus, and it has to be very interesting how and who is being beaten for this current issue. I don’t want to see it happen because I assume Boeing will be courting them for the MOM replacement? Considering PW was created to support Boeing programs, it might be good to see the two companies get back together?

Competition is always a good thing and the industry needs it, but it needs to be watched and it needs to be watched by someone with the bredth and depth of you. Something is happening and people are only nipping at the edges but no one has a clear picture of the story. Tell us oh great sage of aerospace what is happening in the world of GTF!!!

@L7 We’re on extended travel and on other commitments and unable to do justice to look into this right now.

L7, I see a lot of hopes and opinions disguised as questions.

What if PW solves the GTF within a few months and it is structurally better then the LEAP in terms of sfc, noise and MRO? What would it mean for CFM, and for the 737?

Not even unlikely scenarios. The LH NEO is used intensively and punctually as we speak.

http://cdn-www.airliners.net/aviation-photos/middle/7/7/2/2774277.jpg

I do think P&W will solve those issue.

Its other issues that crop up as time goes by.

One maybe, but 3 significant items that should have been caught in testing.

I am very interested in GTF succeeding, I am just not ready to jump on the bandwagon. A good years service should tell more than we know now and better will be 5 years.

“I see a lot of hopes and opinions disguised as questions.”

Yeah we NEVER see that in the comments!

Well put Keesje!

Still good discussable items

The second A320 neo for LH has F1 on Feb 3, so it’s due for delivery this month. The first frame is flying on FRA-MUC and FRA-HAM rotations like clockwork.

L7:

I don’t think one issue automatically drops another off the map. They run in parallel and are parelelellay (new word!) relevant.

While the GTF problem appear to be soluble, its a work in progress.

CFM is just getting going on testing so that’s also a work in progress.

Sadly a lot of the interesting stuff is behind the paywall (787 payback)

The most interesting one I thought came from Keesje, why not put a MAX LEAP on a A320NEO? Same thrust, lighter weight and less drag!

Boeing is not going to put P&W on the MOM if they can’t get their act together. This is the second program (F35) they had rubbing problems on.

Unwanted rubbing will get you in trouble!

Yea, they burned up and F35 on the ground as a result. Wonder if they paid for it?

https://youtu.be/5oUHtE55gWI

Very nice.

A new 737 would probably be similar to the A380neo, in that you’re basically looking at one airline who needs to shoulder the development cost.

How much to develop the 737 Midway? 200 passengers at about 145′ length, able to take off and land at Midway. With a wing root insert and new gear, maybe 3B. Whatever price Boeing would sell Southwest the 737-9, about a 5 to 10 million $ premium over that. The payoff, 200 passengers vs. 175 over a 20 year life. Maybe it pans out.

Southwest flys 17 mill passengers per year through Midway ( its busiest hub), but their operating model is homogenous fleet and high frequency to non stop destinations. I dont see they have a need for a bigger plane only for Midway as their capacity is well distributed over the top 10 routes there.

Pingback: Boeing’s Lower Q1 Deliveries Fits The Profile – Investor Maven