Leeham News and Analysis

There's more to real news than a news release.

Etihad clears the decks

By Bjorn Fehrm

August 2, 2017, ©. Leeham Co: “Etihad, where to now?” was our headline on our May review of the Gulf airline. The 2016 revenue and earnings were not clear at the time.

Etihad group has now released the results, with a group loss of $1.9bn on revenues of $8.4bn. This is a shortfall of almost a quarter of the turnover, a dramatic change from a profit of $259m the year before. .

.

Clearing the decks

Etihad group says the trouble areas during 2016 were the valuation of its fleet and its investments in partner airlines. We wrote about the latter in the May article. Let’s look closer at the main 2016 problem according to Etihad, the fleet values.

Here are Etihad’s words in its results release from 27th of July:

“Total impairments of US$ 1.9 billion included a US$ 1.06 billion charge on aircraft, reflecting lower market values and the early phase out of certain aircraft types. There was also a US$808 million charge on certain assets and financial exposures to equity partners, mainly related to Alitalia and airberlin.”

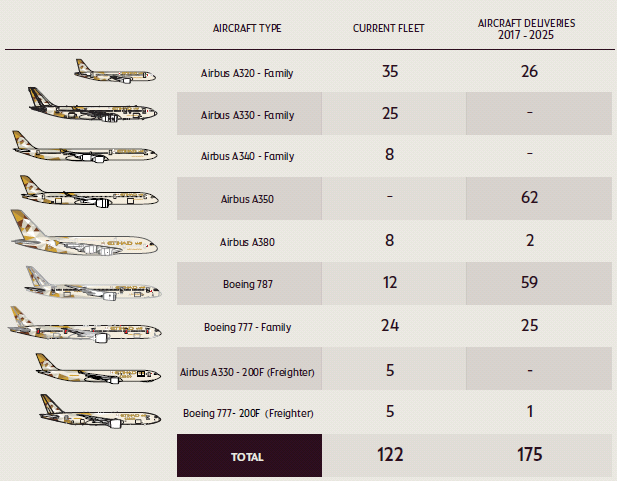

The airline’s fleet consisted of 122 aircraft during 2016, Figure 1.

Figure 1. Fleet on December 2016. Source: Etihad Airways.

If one looks at fleet developments in the ATDB database, Figure 2, one can see (click on the bars in our active diagram to see pop-ups with the details):

Figure 2. ATDB fleet timeline for Etihad airways, see here for active version. Source: AeroTransport Data Bank.

- There were not many aircraft leaving the fleet in 2016:

- One A340-500 from 2006 was stored in Spain;

- Four A330-200s were leased out or returned to lessors; and

- one A320 was returned to its lessor.

So, the talk about more aircraft leaving the fleet is strange. It’s more the previous management masking years of bad results by gradually not depreciating the fleet to market values.

This is a classical tactic if the business is not running as expected and one doesn’t want to show the problems, especially when one is owned by a government and there is no public auditing.

The old management is now gone, so it’s time to “clear the decks” from whatever was done previously. The problems were not restricted to ailing partner airlines. There were homemade problems as well, buried in fleet values.

Etihad Airways operations

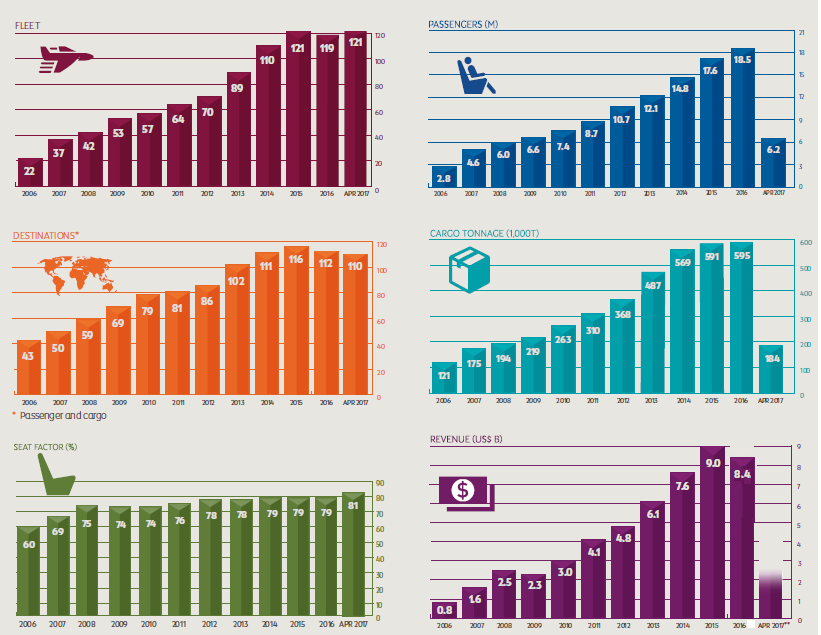

The core airline business should still be running OK, according Etihad. The diagrams in Figure 3 speak of a business that still grows in passengers flown, but all diagrams are tapering off or trending down (2017 data shall be ignored, work in progress):

Figure 3. Key data for Etihad Airways. Source: Etihad Group.

Peter Baumgartner, the new Chief Executive Officer of Etihad Airways, states:

“Operationally, we performed well in 2016. We maintained load factor levels even as we increased capacity. Yields were under pressure in all cabins, with Business Class impacted particularly as corporate travel policies continued to encourage flyers to downgrade to Economy.”

The yield declined 8% last year. Etihad is cutting costs to cope, -11% last year, through personnel reductions and other measures.

Summary

Etihad speaks of a tough market climate in its 2016 report. IATA reports that “three quarters of word-wide airlines” saw increased revenue and profits during 2016 and first half 2017.

The Gulf three have met tougher times, as other low-cost airlines compete on their routes and travel patterns change. For Etihad, the largest problem is the failure of its partnership strategy.

Alitalia, its largest airlines partner, is in bankruptcy and no one wants to buy the remains. What happens with Alitalia will eventually affect Etihad. The partner pains are not over.

“One A350-500 from 2006 was stored in Spain;”

This aircraft does not exist.

tortugamon

Obviously Bjorn meant A340-500.

I think it is abundantly clear that it is a typo and should read A340-500.

Yup, thanks.

With almost 150 widebody aircraft on order we can expect some deferrals and/or cancellations. The choice is wide: A380, A350, 787 and 777.

Perhaps the A380 and 777 would be the first ones to be sacrificed because they are the largest and most expensive. On the other hand the 787 and A350 would give more flexibility to Etihad by replacing older high-capacity aircraft like the 777-200/300.

The most obvious one to defer is the A350: There are zero in the fleet and no trained pilots, avoid the expense of introducing a new model, and the routes can be filled with 777’s or 787’s. That said the next question is which of the other orders do you cut back? 777 and 787 are the obvious ones. Based on load factors they may not take the A380’s or 777F. Either way, both A and B are likely hard hit.

All the A380s are already delivered. The list in the article is the state from December 2016.

Certainly an a340-500…

One just wonders what the management thought while investing into the “BLACK HOLE” – Alitalia and in smaller measure AirBerlin. To get at least something back they would have to do HUGE changes there and …. nothing did happen.

“The Gulf three have met tougher times, as other low-cost airlines compete on their routes and travel patterns change. For Etihad, the largest problem is the failure of its partnership strategy.”

To my very poor estimate there are about 200 new twins (787/350) in Eastern Asia. I wonder how much these planes are eating Gulf lunch of routes between Europe and Asia.

I also wonder how much the fleet impairment value results from the requirements of the accounting standard rather than the aircraft market value itself. That is how much negative results of an identified CGU (cash generating unit) and the forecasted cash flow from the markets an aircraft (or an aircraft category) flies impact its value based on the accounting standard (IAS 36). From this point of view, it is not about the aircraft value, it is about forecasted unprofitable markets the aircraft serves.

The text says ..” US$ 1.06 billion charge on aircraft, reflecting lower market values and the early phase out of certain aircraft types.”

So two parts: phasing out the type means those planes have mostly scrap value only, and the rest of market value may mean ‘used market value’. When you have big new aircraft orders, the planes you want to get rid of have to have used or scrap value at some stage, so its likely a process of getting there from ‘revenue making value’.