Leeham News and Analysis

There's more to real news than a news release.

Pontifications: A deeper hole for the Boeing 737 MAX market share

By Scott Hamilton

Aug. 9, 2021, © Leeham News: Boeing’s 737 MAX market share vs Airbus is in a deeper hole than may be generally realized.

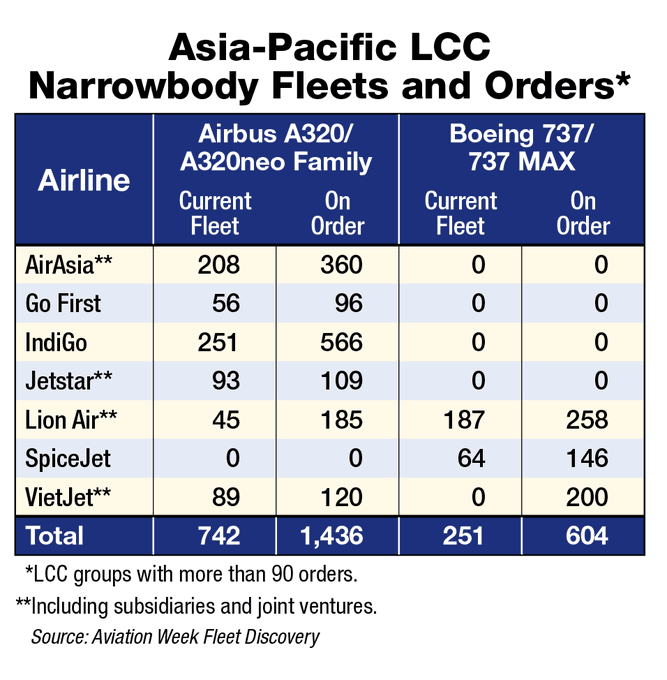

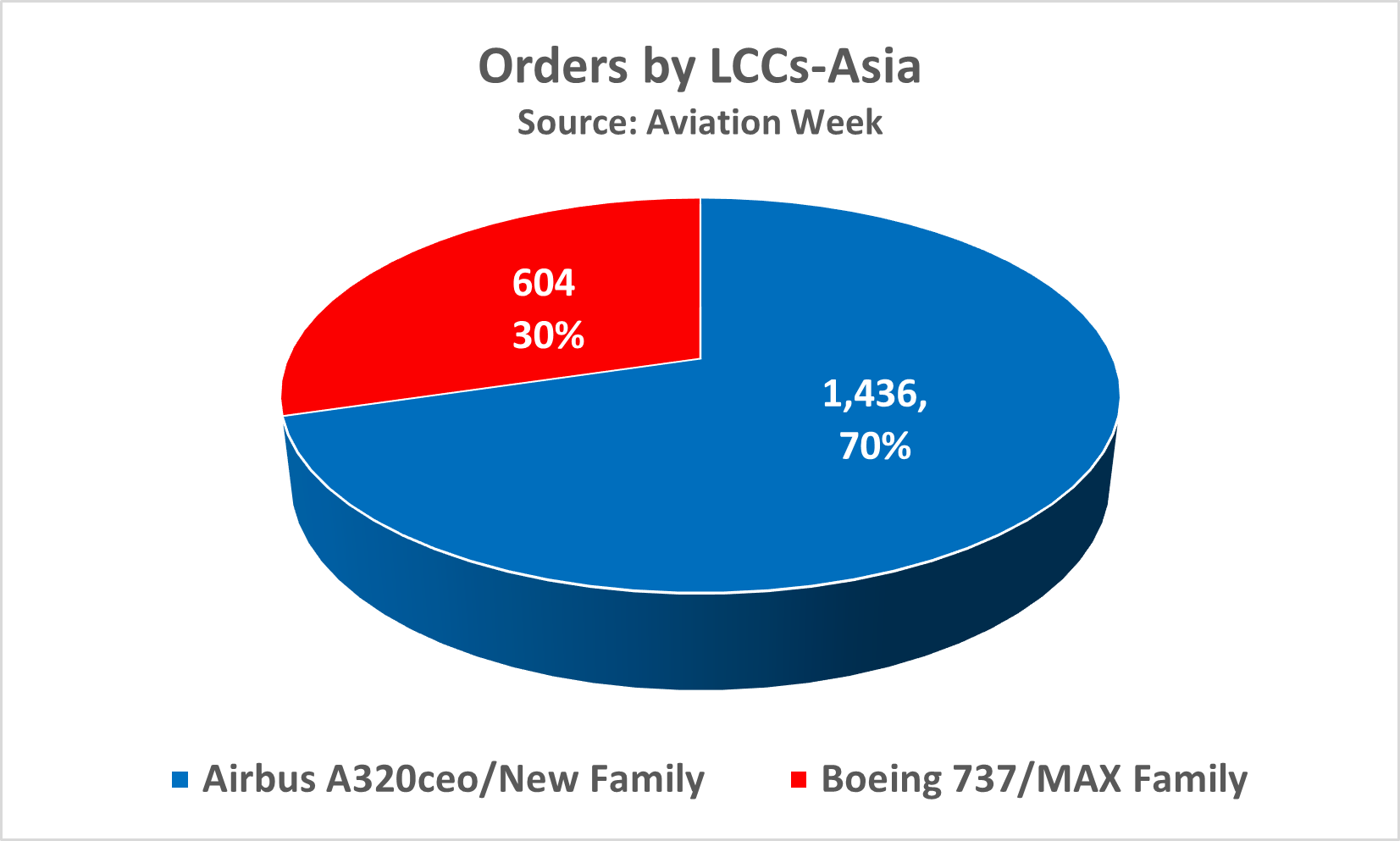

Aviation Week last week complied a list of the top seven low-cost carrier airlines in Asia with orders for 90 or more A320s or 737 family members.

The data illustrates just how deep a hole Boeing is in.

LNA created market-share pie charts based on the numbers above to better illustrate the challenge. It’s not a pretty picture for Boeing.

Sliver of a share

A major driver of this Asia gap is Boeing backing the wrong horses in India. It thought SpiceJet and Jet Airways would be the big winners, while IndiGo was dismissed as a too-cheap, slow-growth player. Jet Airways collapsed, removing its capacity from the Current Fleet—and its orders from the backlog. There are several 737-8s that were produced for Jet that joined the 450 MAXes produced but stored during the 21-month grounding.

Another factor: Boeing tries to back what it thinks will be the “winning” players in high-growth markets, with Boeing Capital often providing financing (or at least backing export credit guarantees). “They’ve been repeatedly seduced by overambitious growth plans like Norwegian, Lion, and VietJet – and are shocked every time a supposed protégé morphs into a rival arms dealer,” a former Boeing employee says.

Airbus was far more willing to place bets on start-ups and low-cost carriers than Boeing at crucial times. In my forthcoming book, Air Wars: The Global Combat Between Airbus and Boeing (due out next month), I describe how Airbus’s John Leahy was far more aggressive in placing large bets on emerging markets than Boeing. Boeing Commercial Airplanes CEO Ray Conner, now (like Leahy) retired, agreed this was the case.

No MAX replacement on the horizon

Despite Boeing’s dramatic loss of market share that pre-dates the MAX crisis, don’t look for any replacement airplane soon.

In recent months, Boeing CEO David Calhoun suggested a new airplane would rely on production cost reduction more than engine advances to give customers a less-expensive aircraft. Engine technology could only achieve 10% better economy today.

Some press coverage suggested the new airplane would be a single-aisle, two-member family roughly the size of the 757-200 and 757-300. But LNA understands that today, the prospects of any new airplane (1) appear to be taking a back seat to the more immediate need to respond to the Airbus A350F threat; and (2) Boeing may well be leaning toward waiting on a step-change in engine technology after all.

The recent announcement by CFM and Safran that the development of an open rotor engine, called RISE, suggests Boeing may be finding new interest in this powerplant. RISE stands for Revolutionary Innovation for Sustainable Engines. While Boeing’s legendary designer Joe Sutter once said an Open Rotor will never appear on a Boeing airplane, there may be little choice. Electrically- and hydrogen-powered airplanes are years away for mainline jets. The only way to make a step-change in fuel economy and reduced emissions seems to be an Open Rotor.

Airbus seems much more amenable to an Open Rotor than Boeing has been. Christian Scherer, now the chief commercial officer, previously served in a strategic planning position. He liked the Open Rotor as far back as 2010 when Airbus was debating the re-engining of the A320.

No move until 2023-2024

Boeing was unlikely to launch a new airplane until 2023-24 at the earliest. The timing is driven by clearing the MAX inventory, returning to a high rate of production, and recovery of its cash flow. By most forecasts, full recovery in the wide-body market isn’t expected until 2024-2025. But even then, the added flexibility of the service mission by the 737-8 and A321LR/XLR cuts into the lower end of long-haul routes. Demand for twin-aisle, long-haul airplanes will suffer as a result.

With the need to defend its freighter position, launching a 777-XF may be Boeing’s more pressing need. Boeing’s Calhoun thinks the MAX can recover market share going forward. (If Airbus boosts A320 family production to 70 or more a month, this may be wishful thinking.) But a moon shot is needed for Boeing to return to its glory days as the world’s leading airplane provider.

“But a moo shot is needed for Boeing to return to its glory” – possibly “moon shot”

@Mark: There are times I really hate Microsoft Editor. Grammarly, too. Fixed. Thanks.

Hamilton

I think Moo shot says it all. Sometimes a typo is a wondrous thing

Really, coming out with a new product is a moon shot?

How about just plain bad management? Nah, divert the subject and avoid the accountability.

> I think Moo shot says it all. Sometimes a typo is a wondrous thing <

I liked "Moo shot" too, finding it somehow fitting for the particular situation.

"Aircart" was good as well (not a dig)- will have staying power, I think.

Bill7:

One thing I learned lo many years ago, you can try to slather over mistakes and look stupid or take the ding for it.

So no, I don’t take it as a knock. It can be funny.

I thought Bryce was unusual in that he repeated GM 3 times maybe 4.

Equally I was having fun with it. Equal opportunity of course, have to be able to take it if you send it out.

Bizarrely, new product is what an mfg lives and dies on.

The so called moonshot was just management BS for we screwed up big time and we want to point at something else.

I had some aircart (grin) mechanics try to do that one time. They made a mistake and busted an MD-11 tail rail.

So they came up with this story about how noble they were to have been working in the horrid heat at that tail engine level and dying of CO poisoning but carried on!

What they failed to observe was I was working in an Air Handling Unit in the Hangar at the same level that day (inside). I was fine and there was no CO.

I wrote up my report to management and we heard no more of the heroic sacrifices made.

Reality is an engine removal from an MD-10/11 tail is tricky as you have very little latitude for out of level. Sometimes mistakes happen.

I had seen those same crews change out engine outside in sub zero temperatures successfully. They really had an outstanding record that they could be proud of and one mistake did not define them.

The 767 program had good management.

777 I wasn’t as close to but the result was successful.

787 OTOH was the poster bunch for botching.

Last I heard Boeing and unions still did not grasp what went wrong. For example, claiming that outsourcing was the cause – false, Boeing has outsourced from very early days, the question is choice of supplier and how you deal with deficient/devious ones such as Smiths Yakima/Cheltenham.

TW said:

“Really, coming out with a new product is a moon shot?”

Overused buzzpeak these days, but remember Boeing developing the 747.

Huge undertaking, had to construct new plant, may have looked chancy when crews were fortunate to get each new 747 from Everett plant to Boeing field flight test centre with all four P&Ws burning and turning.

Pratt and Whitney had botched stiffness of engine, a yoke had to be added around the engine to stiffen it.

Gee, if the US government had not broken the conglomerate of Boeing, P&W, and United Airlines up then engine would not have been outsourced thus the botch would not have occurred? Dream on…..

It’s the Bill Gates/Elon Musk method of developing products.

Try, revise, …..

Took Gates several iterations to get Windows halfway usable, now he takes the same approach to his health charity.

Wouldn’t want to suggest aging: https://www.saanichnews.com/opinion/schisler-try-actually-walking-a-mile-in-an-elders-shoes/

Boeing has done similar – dressing engineers in bulky clothing that restricts movement of joints, then having them board as passengers.

Now if we could just do that to pontificators who lack experience in business…. :-o)

Keith Sketchley

August 11, 2021

Wouldn’t want to suggest aging:”

I was tweaking Scott. 😉

Lots of mooing by media and pontificators. :-o)

It’s interesting to ask what near-term market there will be for any new-build widebody freighter — not to mind for a pair of them from different OEMs.

The P2F market is currently buzzing. EFW in Dresden was initially planning on doing 15 conversions per year, but has now upped this estimate to 20-25 per year, necessitating the use of ancillary lines in the USA and China (and, perhaps, also Singapore); the increased capacity was driven by complaints that freight operators had to wait too long for slots. Even though the factory-build A330-200F was not a success (38 units delivered), the A330-300P2F from EFW is selling like hot cakes. The EFW A330P2F features motorized loading tracks, which overcome the slight tilt of the A330 — thus eliminating the need for the nosegear blister on the factory-build A330-200 — and also speeding up loading/unloading operations.

It seems that these conversions are being used to replace aging A300s and 767s, as well as to provide additional network capacity.

An A321F sounds like a seller — there certainly is plenty of interest for P2F conversions of the A321ceo.

What happens to a nascent 777XF if the 777X passenger program suffers a severe loss of orders before the freighter version’s EIS? Does BA go ahead anyway, and end up with a repeat of the 747-8? Or does it pull the plug and cut its losses?

I suspect that an A321F will be based on the A321LR as this model offers not only an increased MTOW but the possibility with 3 ACT tanks a range similar to B757 freighter.

I don’t think so.

The basic freighter rules should be valid for the A321nef too. No ACT, empty center wing box. MTOW and range is not that important, even if there is much competition from pax aircraft in this range.

The 89.4t MTOW A321neo has the max MZFW of 75.6t, good for 5 hours flight. This MZFW should be increased for a freighter and then a higher MTOW is needed to carry all the fuel in the wings, 93.5t MTOW might be enough.

The XLR without RCT should have a much higher MZFW. The freighter would take advantage of this and that’s why Airbus is introducing a freighter.

Bryce, the 777X is a different situation than 747-8 – I’ve pointed that out before. Note that BA and the loudmouth from the Middle East still think the A380 is viable. But of course that depends on demand, which is still harmed by the SARS2 panicdemic and may be further harmed by climate catastrophists.

As for freighters, conversions of old airliners have low capital cost at expense of higher fuel and maintenance costs. If

The 777 and A330 and variants like A350 are for high-volume routes, A321s for lower volume routes, Cessnas for last-200-km courier routes.

The reason why so many freighters can be older aircraft, is that when used by traditional shippers (Fedex, UPS & DHL) they sit on the ground for long periods of the day. They fly into the hub, make the sort, then fly back out to destination and wait until nightfall.

Spending $50 million to have a cutting edge aircraft doesn’t make sense, when you can spend a couple million, save on Capex and deal with the increased fuel and maintenance costs an older aircraft comes with.

The exception is the long, overwater flights – where utilization is greater.

I’m not sure that a new narrowbody for cargo, is the way to go. Widebody – yes.

Frank:

That mirrors my thoughts. I saw a lot stops as well as gas and go wide body F ops in and through Anchorage.

It would seem for UPS and FedEx and maybe the heavy F operators as well they rival or exceed the Pax Wide Body flights.

Flip is that the 757F or conversion is really a big deal with UPS (dedicated F) and FedEx had to buy pax and convert them when they suddenly realized the 727 was totally obsolete (always wondered why they did not see it coming and act sooner).

Still would be a lot of 757s you could convert vs a new buy A321. As noted those do park and sit a lot.

I see a lot of the moves but long term they had excess capacity on the Wide body flights, unless Covd sets in and a prolonged siege that will change (no predictions)

IIRC, FedEx targeted to reduce aircraft emissions 30% by 2020. I believe they missed that by a wide margin.

Its all PR spin.

The problem with being green is you have to put money into the green equipment that takes serious technical background to set it up right and keep it running at optimum.

So you hire janitors to maintain it and it gets kludged and patched and spiral down to worse than the old stuff.

Sleep walking in yesterday’s world?

FedEx to take delivery of 120 medium duty EV in 2021/22.

@Pedro

…and DHL recently ordered 12 electrically powered aircraft from Eviation:

https://www.dhl.com/global-en/home/press/press-archive/2021/dhl-express-shapes-future-for-sustainable-aviation-with-the-order-of-first-ever-all-electric-cargo-planes-from-eviation.html

The problem with Electric Aircraft is that every dollar spent on them is a dollar not available to Electric Vehicles, Solar, Wind, Utility Batteries more efficient aircraft and SAF fuel development. To that we can add that valuable capital is best spent on producing carbon free Iron, Steel and Cement. The aforementioned are all vastly more cost effective methods of reducing emisions.

Electric Aircraft have a huge opportunity cost and are a negative. The Eviation Alice is probably the best conceived Electric Aircraft out there. However compared to the 40 year old Cessna Grand Caravan it has twice the take off weight, carries 2/3rds the cargo and has 40% of the range and needs 50% more run way. Apply the moulded CFRP concepts of the Alice to a conventional aircraft we get a dramatic improvements.

Electric Vehicles are improving and will be useful . They will likely be affordable in 5 years but could be 10. In 5 years time the bulk of electricity generation will still not be ‘carbon emissions free’

Electrical Aviation has a huge potential in the eVTOL where it adds something unique. Outside of self launch gliders and training aircraft they are a very bad diversion of resources.

There are two aspects of this

1 By the end of 2017 it will no longer possible to sell an B767 or even B777F under the ICAO emissions rules.

2 The ICAO CORSIA “Carbon Offsetting and Reduction Scheme for International Aviation” rules require operators to wind back global emissions to 2019 levels either by flying more efficient aircraft or using more expensive SAF fuel or Carbon Offsets. It will cost. the airfreight companies dearly to operate old types. The same applies to passenger airlines.

3 The EU is applying the ICAO rules. It’ll be compulsory in important jurisdictions.

This may end the tendency to rely on aging freighters either P2F conversions or designs like the B767 at the end of design life. This is one reason the A350F is of such interest and I suspect the A321F based on the neo airframe.

It’s clear that the technology Airbus developed for the A321LR and A321XLR to increase MTOW and MZOW when applied without the permanent RCT tank will create a freighter of considerable flexibility and MTOW/MZW

It’s not just in Asia that AB has dominance among LCCs: it’s the same picture in Europe and the US.

Good bet by Leahy.

Europe AB: Easyjet, WizzAir, Vueling, Aer Lingus, Eurowings

Europe BA: Ryanair, Norwegian

US AB: Spirit, Frontier, Allegiant, Breeze, (Virgin America)

US BA: Southwest

The A321neo Is The Real Gamechanger For A ULCC

https://www.google.com/amp/s/simpleflying.com/a321neo-gamechanger-ulcc/amp/

Undoubtedly the max8-200 and max10 will probably boast the lowest CASM amongst the current narrowbody offerings. IMO, the reason why the A321neo will be a game changer is because of the XLR variant. It will offer the LCCs fleet commonality to operate medium haul transatlantic or intra-Asia flights without the need to operate widebodies.

Its the classic CASM vs flexibility and fleet commonality dilemma. For Ryanair and southwest, committing to the max implies that they will not be venturing into transatlantic operations in the short to mid-term. The only possibility to venture into transatlantic operations is to use a widebody like Norwegian, AirAsia X and we all know how that ended.

Of note with regard to your Ryanair longhaul comment is the fact that WizzAir has opened a hub in AbuDhabi, and is considering flights from there to India / southeast Asia. It can make such plans because of its A321LR/XLRs. If this actually materializes, then we’ll have the world’s first narrowbody longhaul LCC.

Not sure if Ryanair could made a success of transatlantic LCC, but it’s worth noting that nobody flies from Ireland directly to Asia / inland Africa, so they could potentially have made something out of such markets.

Ryan Air have Hubs in Malta, Dublin and potentially Shannon. They could certainly do Transatlantic with B737-7, -8, -9 at least to New York, Boston and also quite a large part of Africa.

@ William

Yes, they could — and also from Stansted.

But there’s lots of competition transatlantic (Aer Lingus, JetBlue, Virgin Atlantic, Norwegian (now Norse), Wow (now Play), as well as all the flag carriers). On the other hand, if Ryanair aircraft had the range (e.g. A321LR/XLR), they would have new Asian/African routes (from selected countries) essentially to themselves.

At least for Wizz Air, they claim lower cost thanks to more seats in A321. Can Ryanair’s B787 MAX 200 match a jet with 20% more seats??

According to Michael O’leary, the B737max8-200 requires the same number of crew as the A320 and 1 less cabin crew than the A321, hence the total crew cost of the max8-200 is a fraction lower than the A321 (200÷4 vs 239÷5).

On the other hand, O’leary also claims that the max10 has lower CASM than the A321neo as the max10 is a simple stretch of the max9 hence it offers an identical per trip cost of the max9 but featured an increased capacity close to the A321neo. He also claimed that the extra range of the A321LR/XLR is of no value to Ryanair as the range of the B737max8&10 is more than sufficient for their current network.

Vince:

All that argument on costs is truly nuts.

Does it work and are you making money?

Ryan Air may well not need A321 range, but it really does not matter, they will make do with the 737 as its what they have.

“””O’leary also claims that the max10 has lower CASM than the A321neo as the max10 is a simple stretch of the max9 hence it offers an identical per trip cost of the max9″””

Same trip cost is impossible.

The MAX-10 is heavier and will be used with the higher MTOW and this won’t be for free.

For sure the MAX-10 will have higher trip costs than the MAX-9.

Can’t be that O’Leary said that …

Since Mike is so eager to give BA a big order of the MAX 10, I think he realizes more seats are better for certain segments. Otherwise, how do you explain it?

Forgot to add: ATM almost a quarter of Wizz Air’s fleet are A321neo, it’ll take at least a couple more years for Ryanair to catch up.

Vince:

A thing called Norse Air is picking up some of Norwegian 787 lease and plan to start in again if you can believe that.

@ Pedro

My local airport is a hub for both Ryanair and WizzAir, and was slot-restricted before the current crisis. Every Wizz A321 at that airport can carry 25% more passengers than a Ryanair 737 MAX8200…a considerable advantage when slots are scarce. Only if/when Ryanair gets the MAX 10 (years from now) will it manage to nullify this seat-number advantage that WizzAir (and Easyjet) have…but it will still not have the same range potential.

Even during the covid crisis, Wizz continued to accept deliveries, add new routes and open at least 13 new bases.

ATM over 50% of Wizz’s fleet are A321ceo/neo, over 25% are A320/321neo.

When it takes delivery of all outstanding orders, over 70% of its fleet are A320/321neo and two-third are the larger A321.

OTOH Ryanair ordered 208 737 MAX, barely one-third of its fleet consist of more fuel efficient jet when all are delivered.

“A thing called Norse Air is picking up some of Norwegian 787 lease and plan to start in again if you can believe that.”

Like shale oil frackers over the previous decade.

“””the max8-200 and max10 will probably boast the lowest CASM amongst the current narrowbody offerings”””

Those MAX will be range restricted because they are MTOW restricted. But for smaller range the A321 can be used with less MTOW too.

I didn’t calculate how many seats on the A321 would be comparable to 197 seats on the 8-200, but I doubt that the CASM for the 8-200 would be better than for the A321 with less MTOW. Same with the MAX-10 too.

There are sectors where the MAX-8 can’t beat the A320neo too because the MAX-8 doesn’t have the payload to fill the seats.

The only advantage the MAX has is they are dirt cheap now. But as a passenger I would always choose to fly Airbus for safety reasons. Ryan would not earn a single cent from me. To me Ryan is a garbage airline because they prefer cheap over safety.

The 737-10 should weight less than an A321 and have a smaller body diameter causing less drag. The 737 wing might be slightly more efficent than the A321neo wing but its engines have a smaller fan so it evens out. Hence on the same routes the A321 need some more pax to give the same trip profit.

claes:

Agreed. It depends on if you need the range and if you are trading off passengers fore range (like the Singapore A350-900 was going to do, all of 172 pax from Singapore to NY – you better be able to collect the big bucks for those seats)

All reports I have seen say the A320/MAX are about dead equal for SFC. So the 800/-8 technically has a bit more revenue as it carries a few more passengers.

The one that looks to have a slight advantage is the A320 GTF.

But you also have to know the maint costs and longevity to come up with true costs. I have yet to see any data on that vs the LEAP.

Clearly the -10 can be efficient if its worked withing its capability as can the A321 on longer routes.

How many fleets have all NEO vs CEO, its a mix and there is an average and trade off for too big, too small and seldom just right.

They both work and its how an Airline operates that determines its gains or losses not slicing and dicing tiny ASM etc.

The A320 series has the advantage of under floor containers “Unit Load Devices”. In the case of of the A321 ten LD3-46 can be loaded. The LD3-46 is a version of the widebody LD3 chopped down from a height of 64 inches to 46. Two LD3-46 can fit in a widebody side by side just as two standard LD3 can.

If the carrier is flying their A321 less than about 2500nmi they have plenty of reserve for cargo and can carry substantial cargo.

No sure if this is a big factor for Wizz or Ryan.

About 3 at most 4 LD3-46 would be used by baggage. Jetstar (LCC of QANTAS) has fast turn around times due to the use of containers.

The fact that men keep getting back injuries and knee injuries loading 737 is one reason this practice of non containers has to stop.

There are after market solutions for the B737.

While I agree with your general point, it’s worth noting that Boeing did back the most successful players in the US (Southwest) and Europe. Ryanair’s fleet is approximately the size of EasyJet + Wizz Air together.

@Dave

SWest and Ryan are successful bullies, it’s better to pick the weaker to better bully cheaper (rock bottom negative margin) prices

They picked BA, not t’other way round

Correct me if I’m wrong, AB has more order backlog from Wizz + EasyJet combined than BA’s from Ryanair (over 60% more); furthermore, AB is not selling its NB jets at fire sale price.

Hence LUV and Ryanair get to bully Boeing when it comes to pricing on aircraft. Pyrrhic victory, no?

@Frank

The airlines infect BA with the ULCC mentality, but do not pass on the knowhow to operate this – they can not, as- basically – cheap airtravel (in EUUS) is subsidised

Cheap is best is a simple slogan when selling China imports, another when trying to compete against a much better planned and more efficient industrial base, one which benefits from the advantage of developed infrastructure, including an intelligent financial system

It looks like BA is dying from the cheapo mentality bug no vx

Wizz is part of Indigo Partners which operate Frontier Airlines in the USA, Jetsmart in Chille and Volaris in Mexico.

Clearly the know how Indigo have operating in the highly competitive US market has allowed them to go “ballistic” when this know how is applied in Central and in particular Eastern Europe where it can connect deep into the CIS and middle east. Obviously Ryan Air Own Lauda.

Further deepening Boeing’s hole in Asia:

“Preconditions remain in effect for Boeing 737 MAX to return to China market”

“The three mandatory prerequisites China has set for Boeing’s 737 MAX to be back in service in the country will remain in effect, aviation industry watchers said on Thursday, following reports of a 737 MAX test jet heading to China.

There’s still a way off for the flight ban to be lifted in China, the first to ground the narrow-body airliner in the aftermath of two MAX crashes in the world, they said.

Such test flights might continue for three to six months, while the flight evaluation and the test report writing and the approval of the results from both China and the US would be a lengthy process, he continued.

Progress on the re-certification test flights won’t automatically be translated into the lifting of the flight ban, analysts said, pointing to the three mandatory requirements as the conditions for a comeback of the aircraft in China.

“China’s civil aviation authorities always uphold three principles: First, aircraft alteration must be approved for airworthiness. Second, pilots must be fully and effectively retrained. Third, the conclusion of the investigation of the two fatal accidents must be clear and the improvement measures effective,” Chinese Foreign Ministry Spokesperson Zhao Lijian said at a press conference in mid-June.

Only when the plane manufacturer fulfills such prerequisites, will the country consider allowing it to fly again, Lin Zhijie, a market watcher, told the Global Times on Thursday.

China will also verify the qualification of the testing based on the flights and modifications having been made, said Wang.”

https://www.globaltimes.cn/page/202108/1230693.shtml

Meanwhile, back at the ranch, the C919 certification program is coming along just fine:

SF: “The Comac C919 – With 6 Made It’s On Track To Be Certified Soon”

I’ll wager a bet that the Chinese will use potential re-cert of the MAX as a carrot to obtain favors of some sort for the C919…such as a US guarantee that LEAP engines will (continue to) be supplied in sufficient quantities. And if no interesting favors are forthcoming, then I suspect that the MAX will stay firmly on the ground.

https://simpleflying.com/comac-c919-certified-soon/

The possibility of withholding LEAP engines to slow the military growth of China is a long passed opportunity . A coherent strategy from the US and Western Europe is simply lacking. Technology is transferred by building of factories in China by ‘western’ corporations and Europeans that turn a blind eye to human rights and territorial pressures.

China would simply turn to Russia and fit the PD-14 engine to the C919 with only a tiny loss in efficiency that will soon be made up.

I would add that the China-Russia allegiance is unnatural and was made by inept US (and European) policy that drove Russia into China’s arms. Appeasement for China and confrontation with Russia.

And another interesting article on this subject, this time from the South China Morning Post:

“Airbus’ edge over Boeing in China under threat as Comac’s new C919 jet readies for take off”

https://www.scmp.com/economy/global-economy/article/3144095/airbus-edge-over-boeing-china-under-threat-comacs-new-c919?module=perpetual_scroll&pgtype=article&campaign=3144095

I think the article overstates things. COMAC has a goal of 150 deliveries per year. Best case it will take till 2025 or later to reach this goal. Airbus has an actual final assembly line for the A320 in Tianjin. Boeing only has a finishing line (installs interiors, paints the plane) for the 737, as does Airbus for the A330/A350. The article mischaracterizes these as FALs. Airbus’ partnership with China is deeper than Boeing. While there will be some impact to the A320, sure, I think the 737 is more vulnerable.

Ergo, China starting to work on MAX recert, otherwise Airbus has the market (short of what China foists off on their Airlines )

They know Boeing is offering bargains. Get bargains and lower Airbus prices.

Case of self interest to get MAX back into China market.

> Case of self interest to get MAX back into China market. <

Yes, but whose? 😉

An interesting situation w/ the 737MAX

and the COMAC entrant.

Will be watching it with interest.

Clearly China self interest.

Boeing gains but China does not care about Boeing directly nor should they.

While not stated, clearly China has stated what they want to see and Boeing will comply with that.

As they are now officially talking (obvious they were before) MAX gets re-instated by the end of the year probably.

What impact there is, uncertain with the current Covd surge and questions on efficacy of the Chinese vaccines.

@TW

Dark clouds coming. How good is vaccine when only 50% is fully vaccinated?

Southwest Airlines is seeing a slowdown in bookings and a rise in cancellations in August amid a surge in Covid-19 cases

https://mobile.twitter.com/R_Wall/status/1425447073739018248

Apparently many reported breakthrough infections.

Looks worse than what’s in your mind.

@ TW

You recently chided others for discussing the C-word and/or the V-word…and yet here you are bringing them up unnecessarily.

You should tread more carefully so as not to draw The Wrath of Scott upon us all.

@Bryce

Haven’t we seen this before?

“All animals are equal but some are more equal than others”

Bryce:

Yes I expected that, and of course the answer is, there was nothing about Covd other than a neutrally stated factor in the business climate which affects China in this case as far as travel occurs or does not.

Its a fact like Jet Engine use Kerosene (technically Jet A-1 )

I did not delve into Vaccines and who is doing what.

Delta variant spreads, Southwest no longer sees profit in Q3

https://mobile.twitter.com/detroitnews/status/1425496170248515588

@TW

All Moo shots not work all over the world

When discussing externalities best to be objective

I hate to beat a dead horse, but lemme get my whip out again 🙂

This is the 2018 annual report from BA. I use this as the benchmark because a) It’s the last year before the grounding & pandemic and b) It’s their best year ever

https://s2.q4cdn.com/661678649/files/doc_financials/quarterly/2018/q4/4Q18-Earnings-Release.pdf

On page 3 you’ve got the summary for BCA – a record 806 deliveries and a margin of 13%. That margin is a combination of both wide and narrowbody aircraft and while the exact percentages are not given, it is a widely held assumption that twin aisles generate a greater profit.

This is the Planespotters production list for the Max:

https://www.planespotters.net/production-list/Boeing/737/737-MAX-8

China grounded the Max in March 2019 – over 2.5 years ago. Some of those still sitting in the employee car park are bound for China. Just like the 100 – 787’s, Boeing has tied up a substantial amount of capital in inventory, money which they have had to borrow.

Putting aside the costs incurred to keep those aircraft in stored condition, how much longer before BA is guaranteed to never get into the black on those airframes? Four Max’s easily equal the production cost of one 787 and if there are 400 of them in inventory, that is another $10 billion costing $3 million a day in financing costs.

Tighter narrowbody margins mean that every 2-3 days costs them the profit on one Max.

I guess one could say that China has a vested interest in keeping those planes in Washington as long as possible as each day that goes by weakens Boeings financial picture and strengthens theirs.

Nothing personal, it’s just business…

Your analyses are always illuminating 🙂

China currently has time on its side: the increasing crisis there is now eating into air travel (see my comment below; -32% in one week), so they certainly aren’t waiting for extra MAX capacity at this juncture. With the C919 approaching certification (it just needs to do icing tests in Canada once the weather cools enough), the Chinese can just sit back and calmly move the chess pieces on their board…they do, after all, have a historical reputation for being master strategists. And while they’re taking their time, Boeing is stuck at a relatively unprofitable production rate, and will continue to bleed cash.

Scott’s comments above are astute, but the link from the South China Morning Post is still valuable because it allows us to see how China views this whole situation; in particular, it is clear that the C919 is a matter of national pride/priority, and anything that gets in its way is (ultimately) going to be suppressed. As Scott states, this will almost certainly impact BA much more than AB — not least because AB has made more of an effort to establish a real manufacturing footprint in China (though there are, of course, other reasons also).

One thing is for sure: if a US attempt is made to curtail LEAP exports to COMAC, things are going to get really ugly for BA.

Frank:

If you exclude all other factors you can narrow it down to what you stated.

But equally clearly, China did not have to do anything other than just stay quiet, but they talked to Boeing and between them, the MAX was dispatched to China to demonstrate its corrections.

China can clear the MAX or they can impose conditions of their own to clear it (aka the -10 third synthetic speed and AOA system)

But the fact they are talking shows there is another or more than one factor in play that you did not list.

Clearly what Leeham amply demonstrated with the numbers China is short aircraft by a lot without the MAX.

So that is at least one factor, pricing is another one that may be fortuitous that they benefit from.

@TW

Did you learn a thing or two from Dave?? Don’t think so.

“Boeing CEO David Calhoun says at the top of the company’s earnings’s call that remaining global regulators (read: China) are expected to approve the 737 Max for return in the first half of 2021.”

Reality:

The B737 MAX remains founded in three major markets: China, India and Russia, plus Singapore (flyover only), Malaysia, Vietnam (flyover only) and Indonesia.

*grounded*

@TWA

“But the fact they are talking shows there is another or more than one factor in play that you did not list.”

I was just stating the cold, hard financial facts of the case. But in any case, try this on for size, in reference to other factors;

There have been recent dialogues between the current admin and China. Perhaps the Boeing situation was brought up and as a goodwill gesture China said, “Sure – send the Max over. We’re not promising anything, but we’ll have a look”

Lip service, in other words.

“Clearly what Leeham amply demonstrated with the numbers China is short aircraft by a lot without the MAX.”

I’m not sure where Scott says that in his article about LCC’s in Asia. Could you please point out where he made that assertion?

@Frank

“I’m not sure where Scott says that in his article about LCC’s in Asia. Could you please point out where he made that assertion?”

I believe TW may have been trying to allude to an article written by Scott several weeks ago, in which he briefly looked at China’s fleet needs and concluded that capacity would fall short without the MAX in the equation. However, in the meantime, the aviation sector in China has undergone a collapse (-32% last week; -50% at China Southern) due to the evolving health crisis there, and that situation isn’t expected to improve any time soon.

I agree with your “lip service” comment. I think the Chinese are dangling a carrot on a loonnnnggg stick.

@Frank @Bryce

So as Frank mentioned, it can be a goodwill gesture. My question is what’s the reciprocal response from the other side?

@Frank @Bryce

Interesting observation

https://mobile.twitter.com/mcneal_wayne/status/1425324971593666563

OTOH

Flightradar showing air space above Shanghai

https://mobile.twitter.com/jonostrower/status/1425297117820510212

Time rewind

https://www.washingtonpost.com/world/as-trade-war-grinds-on-chinese-authorities-ready-the-populace-for-a-long-fight/2019/05/20/11997968-7b0d-11e9-a66c-d36e482aa873_story.html

https://qz.com/1614273/photos-anti-us-protests-after-bombing-of-belgrade-chinese-embassy-in-1999/

Frank:

Leeham did an excellent breakdown on China LCA market needs if the economy returns to previous.

COMAC is not going to be able to fulfill it even if they can figure out how to fly the C919 just in country.

But your stated case as Lip Service? They have gone beyond that.

There is a concrete process in place. How long it takes is up to China.

A carrot would be we might agree to talk about the MAX, not we are proceeding and will have critique of what you have done.

So yes, you certainly are welcome to disagree but I see the hook you are hanging your hat on as implausible.

Clearly in time we will see what occurs.

How much can past performance indicate future results?

The B737NG is one of the safest, but the MAX is regrettably not; BCA had a history of engineering excellence, but recent mis-steps show otherwise.

BA and its top management show they fail to grasp reality and naively optimistic (might be it’s necessary in order to maintain the stock price 😉).

@TW

Do you know how many jets over 15 year old AC have in service??

https://www.planespotters.net/airline/Air-China

Facts are best for rational discussion.

Oops

*CA*

Beside a possible A321nef, which new Airbus will come next?

Boeing then might jump to a different path, but only jumping while doing nothing. Sure Boeing is busy with repairing their mess and is still trying to find a way to cheat in the process. How can Boeing repair the 787 fuselage gaps, when they couldn’t fix it for 10 years.

A321P2F conversions make sense, a new A321nef not so much because the A320family backlog is so big.

OTOH how much cheaper could the A320family be if the production rate would increase to 80+.

Actually it doesn’t get any cheaper after a certain point. Its a diminishing effects. Its probably not worth tge efforts for airbus to push beyond a certain level as the other supply chain risk would outweigh the cost savings from the economies of scale.

Some analysts puts this number at 100 units/mth, while some go as low as 60/mth. Considering that they are talking about 75/month, that could very well be the optimal point. This only airbus knows.

Vince:

I keep seeing reports of suppliers warning on production and it was an impact before the Covd mess.

So yea, there was a limit where things were getting seriously iffy and ramp up with a smaller workforce?

What does history of mass production tell us??

“Assembly-line production allowed the price of the [Model T] touring car version to be lowered from $850 in 1908 (equivalent to about 18 months salary for an average wage) to less than $300 in 1925 (equivalent to about 4 months salary for an average wage)”

.. going from a tradesman’s approach to industrial manufacture.

Today it is detail improvement on established proceedings. no step changes visible afaics.

( And IMU the advantages of ever merging towards bigger participants in the market so much liked by Wallstreet usually don’t bring the cost effects visualized. What they bring is lever from size.)

In 2018, BA credited higher production rate of B787 gave it the advantage to drive down costs across its supply chain. In the fourth quarter, Boeing said its operating margin on commercial aircraft increased to 15.6 percent from 11.6 percent from a year ago, partially driven by higher margins on the 787 Dreamliner.

Frank:

I would agree on the sales numbers but I have a different take on some of the Airbus strategy.

Airbus felt that they could make gains in China with an FAL.

Alabama started out as A330 assembly in regards to the KC contract.

Airbus wants to sell not just airlines in the US but military equipment as well. Having a US presence was a means to that end and it clearly gets you political clout from the area the FAL was put into.

Alabama and the A220 FAL was clearly a fall back strategy that was no needed.

Airbus has stated the US is the single best place overall in the world for building aircraft.

They are in a position or culture situation where up front profits are no the sole drive and may well benefit in other ways.

I don’t think Boeing could put an FAL someplace else and not get serious blow back though it might well be they just pay their way tax wise instead of off the hook.

I do admire Airbus and what they have done.

Pedro:

Aircraft are not mass produced. Run the math on 30 Model T a month vs 60.

Look at Airbus. They have A320 lines scattered all over the planet, only the European ones are running at a high rate.

Alabama and China cost them a lot of money without a high rate return (that is just buildings and support)

Comparing auto build or smart phones vs aircraft is a huge error in what mas production is all about.

Equally profit margins are not a bench mark unless they are put in context.

Boeing made more money on the 787-9/10 as they sold them for more money.

And with the shim debacle, that was a false return at a huge cost.

And what did they pay for that ramp up only to drop down?

Hey, how much experience you have in large scale manufacturing and cost management?

@TWA

You’re right – aircraft are a very different animal.

“Alabama and China cost them a lot of money without a high rate return (that is just buildings and support)”

‘Bama secured the A220 sales to Delta, Jetblue and Breeze – a workaround the Trump 300% tariffs on the program. It’s only 180 aircraft, but it’s 180 less that Boeing can sell. Not to mention the A320’s that come off that line.

I’m guessing it’s the same for China, from which Airbus just delivered it’s 500th plane on late 2020.

With two thirds of the worldwide narrow body share, I’m guessing that Airbus knows what it’s doing, when it opens operations in countries it wants to sell aircraft in.

“Beside a possible A321nef, which new Airbus will come next?

The higher performance optimised single slotted flap developed for the A321XLR that replaces the double slotted flap on the standard A321neo to maintain take-off and landing performance may find its way on to standard A321neo and A320 neo. It will certainly improve take-off and landing performance, reducer tyre and brake wear and possibly MTOW at little.

Bryce, the criteria are almost ‘motherhood’, the same as most if not all regulatory authorities. But a good recitation to keep things in perspective.

I don’t know where the Ethiopian investigation is at – ‘preliminary’ report perhaps. Indonesia issued ‘final’ report.

Different scenarios. (Ethiopia was close to the ground and fast due ground altitude and temperature, crew had heard of the risk and procedure but ….)

Opinions may very on accuracy of the crash reports.

The big question is how much mainland China will duplicate work done by the four authorities with the most recent experience. (Brazil, Canada, Europe, US) I say time to get flying.

For operators of old A321’s they pretty easy to upgrade their aircrafts to late build A321ceo’s standard hence the supply of old A321’s might not be that big. Still the installed base is big enough and doing a P2F conversion when the aircraft is due for heavy check, landing gear and engine overhauls might be attractive for a buyer with money or good bank relations.

BA deferring the 737max replacement in favour of defending its 777 freighter market seems like fiddling while Rome burns. Can they really afford to do next to nothing in their most important market whilst focusing their efforts on defending a minor one?

Agree. Still the assumption the MAX will be ok after 2025 seems hard to break, regardless of overwhelming signals and writting on the wall. Nobody brave enough to pull the plug on a 5 decades old cash cow.

Last statement – ain’t it the truth… Also, at anytime in the next few years, there could be an economic reset. This could precipitate delays and cancelations of new programs. We are really seeing the fruits of Boeing’s leadership vacuum during the McNerny through 2019 era. Just atrocious…

Exactly what I was thinking: “fiddling while Rome burns” is a good way of putting it.

However, it seems that the non-availability of a new engine for the near future will impede any move to replace the MAX, and one can question the size of any forecast market for the NMA in view of the ongoing crisis in longhaul travel. Trying to salvage a slice of the freighter market — particularly in the midst if such a flurry of P2F conversions — seems like trivial pursuit.

I don’t see how they can do anything but wait. They are boxed in by the open rotor announcement and its timing (EIS early/mid 2030’s). RISE is to be hydrogen and SAF compatible, have a hybrid electric capability and is expected to result in 20+% better fuel burn.

If Boeing moves now they will need to use a PIPed version of current engines, giving at most 5% improvement. Then Airbus will move in 5 years announcing a new single aisle optimized for the open rotor and with all electric systems. Boeing will again be snookered.

I sometimes wonder if CFM was given encouragement or even promises by the EU knowing how problematic it will be for Boeing.

Open Rotor is just pie in the sky free research money.

It keeps morphing around and its basic flaws are still there.

People don’t like spinning propellers even if they managed to mount it on the wing.

Tail location is heavy structure and you can’t mount different mfgs (even if there are two mfgs which there are not)

I don’t know if it’s exactly pie-in-the-sky, but it does make

a convenient excuse for a certain aircraft mfr to not do anything..

There’s something else Going On with that company.

Perhaps so, but this time it is not all research funding and signs are it has un-nerved Boeing.

jbeeko:

Well Boeing Management has been unnerved for so long its now a way of life!

How much money can we still suck out of the carcass?

I don’t think that’s any longer true. If it ever was it was from the time when aircraft were rapidly developing from piston engines to turbo-prop to jets and each implementation was associated with progress and modernity. Factor in the accident rate for aircraft of those times, the late ‘40’s to the ‘60’s and how they made people regard flying then the antipathy to the (perceived) old style of aircraft can be understood. However, that was a long time ago, those people are fewer and fewer and if you “greenwash” a product, say a ‘plane with spinning props then this current woke generation will applaud.

Fastship:

I grew up with props and Alaska is hugely aviation ordiented, boht the main networks, regaionl operates to excusions on the bussiness end.

Private aircraft vastly exceed anywhere else in the US (I toured Washignton State once and wass asonished at how few aircraft there were, Western Washington is a flying dream)

That said, most passengers on the Anchorage Fairbanks run were unhappy with the BBD Dash 8 Boeing replaced the common 737 flight between the two.

It was enough unhappy they put an Embraer Jet on it.

While 10% of the serious Greenies might weight green in, most people will not, its cost and they don’t like props.

If you cant sell it in Alaska I don’t believe you can sell it anywhere.

As I follow the so called open rotor, its not a advanced fixed blade Turboprop Prop as its geared.

Its free research money and cores apply to both type engines.

Interesting to note a new restriction by FAA on all 737 (NG & MAX) regarding cargo hold fire precautions.

One more worry for B to deal with, and perhaps a killer for PtoF conversions.

There is really nothing to see here

… operators may not “dispatch or release an airplane with cargo in the aft cargo compartment with failed electric flow control of air conditioning packs,”…

Essentially the electric flow control of air conditioning packs is now part of the mandatory equipment if the aft hold is used.

Yea, the blossom affect of anything MAX is the sky is falling.

Standard AD stuff.

For those who think its only Boeing they should look at Tarom Flight 371 with a very MAX MCAS like behind the scenes failure.

The Tarom Flight 371 crash was *twenty-six years ago*.

https://mentourpilot.com/tarom-flight-371-a-complicated-tragedy/

Bill7:

Agreed but do you not think it was a severely ignored well known issue that only got fixed after the crash?

737 Rudder issue is what 30 years back but you saw Boeing denial on that one as well as FAA go along.

Partly the point is that people being disappointed with how far the FAA has fallen don’t know it fell a long time ago, the MAX tragedy was a logical outcome of what had gone before.

Equally Boeing denial was no different.

It puts thing into perspective and ADs and adjustment to MEL etc go on all the time.

Some like the most recent one is innocuous, some like the A310 throttle and the MCAS are lethal.

You need to be able to tell the difference for an informed discussion.

@ Doubting Thomas

This AD — just like various ones that have preceded it in the past few months — is interesting in that it shows that, while it was grounded, the MAX certainly was NOT “gone through with a fine-tooth comb”. BA seems to like to project that image of a plane undergoing historic levels of scrutiny — but, if such scrutiny had indeed occurred, then ADs wouldn’t be cropping up every few weeks (often relating to systems that were also already on the NG). Instead, one can surmise that — just like the 787 today — the MAX was just sitting passively waiting for the FAA to suggest/approve a bandaid for the grounding problem. Indeed, this seems to have become the new BA modus operandi: if a problem occurs, then just freeze and wait passively — for as long as it takes — until the FAA gives a green light. Meanwhile, airlines are delighted with this approach because, as deliveries become more and more delayed, more and more orders can be canceled without penalty.

Bryce:

Lets look at the pickle fork issue. How long has that been there?

Unless it reveals itself, you don’t know its going to fail.

Its pure nonsense that the wire grounding failure was a band-aid. Nothing more than in uninformed opinion (much lie the flat earth proposition ) You site no sources nor exhibit the technical knowledge required to assess.

I worked with grounding equipment, the proposal to remedy was thorough and coherent .

The fact it got to that point is a real issue and problem.

Equally, the system did work like it should. Boeing found the issue, reported it to the FAA and proposed remedies.

The FAA looked over the proposed corrections carefully (read that as it takes some time) and then concurred with them.

In the case of the 787 shims, the FAA did not like Boeing’s proposed approach and told them to try again.

In the tech world that is not unusual. Once you identify a problem you come up with a trial solution. Often that does not work the way you hoped, so you keep working it until you come up with what does work.

Clearly the FAA is now doing its job.

You ignore the issue with the cabin pressure switches. Another AD that recognized that the time between tests was too long and you could wind up with dual failure (called MTBF)

That was adjusted to a very safe and conservative number to ensure it did not happen.

Engine TBO goes through that same process. You do an initial estimate of what TBO should be, then you watch it and see what it actually is.

It may get shortened or as time shows, longer as the durability was higher.

The flip is sometimes you find a single component in the engine that fails sooner despite the rest of the engine is fine.

You then replace that component with one that has proven itself durability wise.

I know of one that you just did the TBO and you had to get to the guts of the engine to replace the one bad part.

At that point the time clock restarts and you assess the new part to ensure that it safely reaches the TBO of the engine.

Aircraft have hundreds if not thousands of these process going on all the time and its not a Boeing exclusive, it common and standard to all aircraft and their engines.

Indeed, thanks.

MTBF = Mean Time Between Failures, notice that is akin to average but not quite the same. (There’s also Median, important to understand difference among the three.)

That’s useful for parts that do not wearout in the normal sense, but beware that electronics do age.

To establish TBO, you start somewhat low then slowly increase based on experience.

But you may also do monitoring – common with engine parameters, use oil plugs that collect chips/fuzz, and analysis of oil for wear particles.

And do inspections – common with turbine engines to do a ‘hot section inspection’ partway to TBO, as the combustor and turbine end of the engine is more sensitive.

(TBO = Time Between Overhaul)

(The chip collecting plugs whose o-rings were left off in the L-1011 that almost became a glider in Florida. A real lesson in paying attention.

A mechanic was assigned to replace the plugs. Three came in a kit. He did not realize that the o-rings were supplied separately and overlooked absence of them. Presto! rapid oil leak, at least one engine not producing thrust.

A practice where extra high reliability is needed, such as in ETOPS, is to not work on all engines at the same time.

@TW

C’mon what does cabin pressure switches failure have anything to do with faulty air conditioning flow control??

Fortunately this failure is not found after another crash!!

@ Pedro

Some people just don’t (want to) get the point.

They prefer to ramble on about the details of a particular AD rather than realize that, if a plane had really spent two years undergoing historic levels of scrutiny, then failures such as these would have been discovered pre-emptively rather than cropping up now after re-cert.

All these ADs do is demonstrate that there was no “historic scrutiny” at all applied to this plane: we can surmise that it was just sitting on the ground corroding while the FAA took its time to approve an MCAS bandaid.

> (2) Boeing may well be leaning toward waiting on a step-change in engine technology after all. <

It's looking ever more to me like Boeing is "waiting" themselves right out of the commercial passenger aircraft market.

Agreed

Perfect is the enemy of good enough.

William said:

“1 By the end of 2017 it will no longer possible…”

Another failed prediction?

😮

Greens are good at FAIL.

😉

I’d meant 2027. However it suspect it won’t be a fail since they airlines will be compelled to purchase SAF. If there isn’t enough SAF I would expect carbon taxes or compulsory offset.

Certainly is an ‘offset’ scam about.

But who needs people meeting people, who needs transporting people out of harms way, who needs getting aid to people quickly, who needs people?

Not the publisher of the inaugural issue of The Ecologist magazine which called humans ‘parasites’/.

@Keith, I’m a big sceptic of the environmental movement. Elements of them have important things to say but the movement has too many self righteous fanatics with more zeal than sense. Dr Patrick Moore, one of the Founding members of Greenpeace left the movement.

http://ecosense.me/2017/01/17/issues-68/

However sensible measures to reduce emissions should be taken. The problem is they are taken to an inane level.

All animals are parasites. The problem with some eco fanatics is they fail to see that they are also parasites in a sociobiological sense.

The EIS says that the Nett Present Worth of delivering nuclear electricity in the USA is only $0.03 per kW.Hr. This includes allowances for decommissioning and waste disposal. This is by far the lowest of energy sources. It is 1/3rd to 1/5th the cost of wind which is $0.08 (actually $0.14 when tax incentives are remove, the need for back is considered and transmission lines cost factored in)

At $0.03/KW.Hr it would be possible to produce PtL fuel at 50% efficiency (ie it would take 16kw.hr to produce 1Litre of gasoline containing 8kWhr). Cost including capital cost would be about $0.96/Litre for petrol.

You end up with costs around 4 times this using wind.

Waiting was their response to the C-Series followed by demanding the Government standup to progress. They literally said: We got this old plane and we make more money if there’s less competition.

It depends on whether or not they can raise money for that moonshot effort to get back in and match Airbus.

Meanwhile, Airbus is pretty much free to get fat on the vast number of A32xxxx sales that it will rack up in the meantime, and is guaranteed to have a large war chest at its disposal before it even begins to think about going to the money markets. Plus it’s likely to be in tip-top, match-fit, raring-to-go condition with a mature engineering team used to getting things right and doing them in predictable time with a minimum of slip-ups.

For me that means that Boeing’s future single aisle moonshot really needs to start right now, if it’s going to stand a chance of smoothly executing a program that actually matters. I can’t see their first effort even beginning to compete against every single aspect of a program that Airbus can deliver. They need to get one or two projects with modest goals under their belts, just so that they know how to do them, before they can even start to think about taking on Airbus.

Besides, it’s like Boeing are not learning from Airbus’s strategy. Airbus is doing a freighter, probably a pretty good one, and Boeing are feeling like they’ve got to at least defend against that move.

However, consider the scenario where Boeing right now set-to on a really big effort to deliver an A32xxxx killer (I dunno – CF fuselage / wing, the best engine out there right now, something really out there). Could Airbus afford to let Boeing go ahead with that, unchallenged?

No. They’d be forced to respond, and they might think twice about just how much resource to actually put into the A350F. Admittedly, the A350F likely doesn’t need a massive amount of resource, but they’d probably put their best on to ensuring Airbus get a level playing field against Boeing’s A32xxxx killer.

Attack is, quite often, the best form of defense.

Boeing will produce an NMA first. Something like the size of their successful

B767 about 35% bigger than an A321 and 70% the size of a B787-9. It will have an ovoid fuselage to reduce frontal area and be made of CFRP for weight reduction. Although nominally for ranges of around 3200nmi it will surely have an “ER: variant such as the B767-200ER with a range of 6500nmi.

Compared to the A321XLR it will have true intercontinental range while carrying cargo. It will probably cannibalize B787 sales.

…and where will the money for this NMA come from?

I was going thru’ its Q2 earnings call.

BCA is cut to the bone: its r&d spend is chopped by 50% comparing with corresponding period of 2019. Calhoun indicated there’d be no increase. As a result, no NMA, no FSA.

@ Pedro

Probably no 777XF either.

All available resources will probably need to be diverted to the new bridge tanker offering for the USAF.

After so much hype earlier about BA’s coming FSA, we’re back to square one: nothing.

So Dave is a reincarnation of Jim??

“But a moon shot is needed for Boeing to return to its glory days as the world’s leading airplane provider.” As a retired Boeing engineer who was there for the pinnacle of Boeing engineering excellence (the 777), I believe Boeing no longer has what it takes to pull off a moonshot. The brain drain is relentless, the executive bloat unending, the product strategy in shambles. There hasn’t been successful Boeing commercial program execution since before the 1997 merger with the failed airplane company from Long Beach. The defense and space side is hardly a litany of success stories either – JSF and B21 losses, KC46 debacle, Starliner, and so on.

I flew ORD to SEA last night, and watched several 747 cargo planes come and go. It saddens me every time I see that airplane – a reminder of what Boeing once was, and likely never again shall be.

I disagree on the Moo shot. They just need a consistent process for new products.

As predicted, the KC-46 is getting cleared for more missions and keeping in mind, the boom being to hard issue was a USAF spec that they are paying for. Clearly its been a mess but nothing says it won’t be corrected.

Starliner would not be military, its not BCA but its a NASA project. And yes you have to ponder why valves suddenly quit working and no, its not flying for a while because they not only have to get them working, they have to figure out why they aren’t and come up with a remedy.

Frankly I think Boeing was lucky to miss the JSF debacle and the T-7A may well be their best entry into the future vs a more challenging B-21.

My wonder is, is the F market in the 777 range really that big an income?

Its a nice supplement clearly. But take the total Boeing focus?

The 777X-F should be designed already, is Boeing so weak it can’t execute that work vs the work for a new A321 competitor?

You begin to see the waffling on the future and that in turn has legitimate question of BCA future period.

> My wonder is, is the F market in the 777 range really that big an income? Its a nice supplement clearly. But take the total Boeing focus? <

Good questions, and my layman's guess is 1) no, and 2) no.

Something else going on.

The article mentioned that Boeing needs to deliver the inventory first. That makes sense. So a 777XF should be on the schedule. But it won’t work because Boeing lost the self-certs and the Know How to do it right and doesn’t have the money. So they will only try to deliver the inventory while more aircarts will join the inventory.

“We at mcBoeing can’t deliver our Basic Stuff, so instead

we’ll show you new, trivial mindproducts of the Future!”

someday, baby

Prediction: there will be no 777XF.

I think more accurate Boeing can get the money but elects not to.

Av Week commented that the FAA reported it was not getting through to Boeing manager of 777 ODA that he had issues and it had to change.

Shades of if not short term fixes on MAX and 787 to get the cash flowing so they can spend it on dividends or stock buy backs.

There has got to be some level of alarm within the board at all this. But that same board also extended Calhoun so ???????????

– In SC, as recently as early 2020, BA allowed managers who were not part of ODA to oversee employees who were; ODA member was pressured to inspect a jet which had outstanding issues; managers push ODA employees to rush inspections and report a-okay faster; at times the senior managers would stand outside a jet to see how quickly ODA employees responded to inspection requests and how quickly those inspections were completed; BA managers pressured employees to sign off on a jet despite fixes still needed to be made.

– Long before the MAX disasters, Boeing had a history of failing to fix safety problems

– Boeing employees’ emails draw parallel between 737 MAX and 777X

“BA allowed managers who were not part of ODA to oversee employees who were.”

This is a recipe for disaster. It’s guaranteed that pressure will successfully be applied. I’ve seen it and have been a subject of it. If the ODA employee thinks it will take 1.5-2 weeks, even with an excellent plan, and the manager wants it in 4 days (to meet his own KPI) the manager and his gang can pressure can apply pressure, Personal & professional criticism etc, riding etc. Things that should double checked checked only once, arguments made that a previous check had already been done etc. The idea is to get the employee to signed off. It always comes to grief and creates quality issues down stream. In certain industries such people or mentalities don’t belong and need to be kept away.

Pedro, while behaviour of Boeing’s ODA honchos appears unacceptably bad, keep in mind that the individual engineers with delegated authority need to be quite involved with the work in order to have knowledge of it sufficient to do their job.

Halting delivery of B787 certainly doesn’t help. Over 100 waiting on the lot. Swings from a cash generator to a drain.

Pedro:

Not like Boeing had a choice, granted they found and reported the problem.

A good thing to keep in mind is Corporate culture, Charleston is not going to be the same as Everett (top maybe but under that….)

Probably one of those good and bad aspects.

My takeaway on the 777 article was that Everett was hidebound with having done it their own way that it is impossible for the ODA manager to adjust.

My reference is the L-1011 that crashed into the Florida Swamp when the entire crew (3 in those days) fixated on a burned out light and quit flying the airplane.

Like Ford, Boeing BCA is either going to turn the ship around of fail .

In some ways you see promise and others its enough to cause despair.

> A good thing to keep in mind is Corporate culture, Charleston is not going to be the same as Everett (top maybe but under that….) <

I'm not sure exactly what was meant in the quoted bit,

but I'm having a hard time imagining the consolidation

of production in Charleston as being a plus for quality

control, and workplace morale.

Its more how flexible the Charleston Culture is vs Everett in my mind.

Yes they clearly had quality problems there, but also with some of the changes that was reported and we see the correction is in the works.

That is a change.

The 777X seems to have run into a more problematic issue with FAA not being able to get the ODA managers attention and concurrence to correction.

So have to see what transpires there. Some of it seems MAX like in copy and paste 787 Control program when its a different aircraft and you have to use at least different values in your PID.

When is the next Olympics?? I don’t buy BA/Dave’s hot air.

Does anybody buy it?

Incidentally, this Dutch aviation link is indicating that the worsening situation in China has caused a 32% reduction in planned seats since last week, and China Southern has even reduced its scheduled seats by 50%. The article is referring to a “collapse” in Chinese aviation.

At present, the Chinese are in no need of extra MAX capacity.

https://www.luchtvaartnieuws.nl/nieuws/categorie/72/algemeen/chinese-luchtvaartsector-stort-in-door-maatregelen-tegen-corona-uitbraak

‘ Boeing scrubbed Starliner spacecraft’s launch after 13 valves failed to open

Boeing still doesn’t know the cause.

“Without a clue as to how this happened, ‘still hopes to launch in August’ is very much just a hope.” ‘

https://mobile.twitter.com/dominicgates/status/1424798114750222341

Just makes you want to slam your head against a concrete wall to make the pain go away.

Amazing.

Now its the rainstorm (how you muck up a valve with rainstorm is beyond me) and why your valves would be exposed to weather if they are not impervious is also beyond something.

He may be squirrely but Elton sure does better than the Corporate Suites.

I wouldn’t describe Elton John as “squirrely”.

One can only assume you’re bringing him into the discussion because he sang “Rocket Man” … though the exact relevance to the Starliner is obscure 😏

Elon? or was that Elton John?

Dan F:

Thank you, typo.

Earlier today

Aug 7 10:48 am

“Boeing is still looking to launch #OFT2 in August:

‘This weekend, Boeing restored functionality on more of the 13 CST-100 #Starliner propulsion system valves that did not open as designed during prelaunch system checks … 7 of the 13 valves are now operating as designed.’

*Aug 9* 10:48 am

Oops

This suggests a very optimistic design. Seems to have weak troubleshooting capability and hard to service. Seems like it will be tough to keep in service and maintain the needed launch cycle time.

https://mobile.twitter.com/KemClawson/status/1425506276398751747

WSJ: Boeing’s Starliner Launch Could Face Delay of Several Months

Boeing’s John Vollmer on launching Starliner in 2021: “It’s probably too early to say whether it’s this year, or not. I would certainly hope for as early as possible, and if we could fly this year it would be fantastic.”

Translation: Not 2021.

https://mobile.twitter.com/SciGuySpace/status/1426233069372067850

If Boeing were serious about commercial passenger aircraft they’d be working all-out on a *parity* single-aisle 321 competitor. Their excuses in the article for not doing so do not wash.

Show you can do something, mcBoeing [assuming they want to; not a safe assumption].

I suspect that, by the time such a “parity single aisle” were ready for EIS (at least 5-7 years from announcement), Airbus would already be working towards a next-step replacement, with a new engine. So BA would lose 5-7 years of the market, and then enter the market with a product that will be superseded shortly thereafter.

It seems they’ll just have to stick with the MAX until a new engine presents itself.

“He who burns his ass, will just have to sit on the blisters”.

Boeing vs SpaceX, major cultural issues resulting in quality problems, cost overruns and long delays at Boeing. Existentially critical issues.

Boeing vs Airbus, oh, look, same thing.

5 more years waiting to see what happens. Meanwhile the third party in the now Triopoly keeps catching up

I don’t see COMAC or UAC catching up soon.

The MC-21 is clearly a tech jump over A320 let alone MAX and its ability to compete is limited by the Russian system (see fate of Super Jet)

MC-21 will be certified into other major markets (Russia has gone through the process that make that possible and will get EASA certification in all probability)

Ironically the C919 will not be allowed to fly in Russia as it does not meet those certifications.

At best the C919 is going to me 150 a year (in the area of the A220). 15 a month? All those go into the China market (well they will give a few away)

Airbus is looking at 100 (not likely but its out there) and Boeing can return to 50 some at some point.

> I don’t see COMAC or UAC catching up soon. <

I think that they don't really need to: what they need to do in the near and middle term is present a modest alternative to

the duopoly (should it still be called that?), which can place

them in a nice strategic spot over time; even if only in their local markets, for now.

“I don’t see COMAC or UAC catching up soon”

Does anyone see Boeing “catching up” soon?

Not much point in having “technologically advanced” planes if they’re sitting on the ground. And what do you do when you’ve fallen seriously behind but don’t have enough cash to conjure up a meaningful new program?

***

“Ironically the C919 will not be allowed to fly in Russia as it does not meet those certifications.”

The MAX is also not allowed to fly in Russia…or in most of Asia-Pacific. It wasn’t even allowed to overfly Russia during its recent trip to Pudong.

“Boeing can return to 50 some at some point”

When?? Otherwise sounds more like wishful thinking. Again.

What’s the percentage of 737 MAX order came from China before grounding? How many BA plans to sell to them in its comm. market outlook?

Clearly Leeham aptly demonstrated BA’s 50+ /mo is unlikely, but I expect you to say otherwise.

Pedro:

A shame that you take it out of context. I did not say they will, just that they did.

Boeing may not get back to 50 a month, but they were delivering 50 some a month before the grounding.

Clearly they could work back up to that level if they get the orders for the MAX and or existing want them sooner.

Airbus was experiencing a lot of delivery issues at that same point. That was part of Welsh problem and the nebulous MAX order that never came to be (and man well never)

COMAC has never delivered aircraft in numbers and they would have to work through the same sort of ramp up Airbus is doing with the A220.

United Aircraft has not delivered in any monthly numbers either and I have yet to see MC-21 ramp up estimates. They too would have to work their way up to deliver any numbers.

United Aircraft has a vastly smaller market and has not sold any MC-21 to anyone other than internal Russia.

We do have some gauge of how it goes with the Superjet that is not getting any market penetration and has undergone a major revamp.

Its not an easy business like Auto where you crank up production easily and you still have the whole world of support to ensure that neither Russia or China has successfully done .

BBD made an outstanding aircraft in the C series but it was going to fail until Airbus took it over.

@TW The C-series was hardly a failure. BBD was forced to sell to a lower bidder thanks to i) BA’s failed dumping petition and ii) GC’s intervention. Time to stop your false claim.

I believe in karma, what comes around goes around.

It’s happening!! 🙂

Contrary to popular myth, EASA confirmed it has started its certification of the C919. Certification soon? Nope, it’ll take years.

Could I blindly base my expectation of what’s ahead on what happened in the past?

For over a century, parts of the U.S. were colonies of Britain. Based on that, is it logical to say the U.S. can be a colony of Britain again??? Everything is possible, it’s important to consider how probable it is for any rational discussion.

Can past performance guarantee the future?

Before the GFC, credit analysts built their financial models on a false assumption that there’s no nation-wide downturn in housing market because it hadn’t happened since the WW II. Reality proved how badly wrong that was. Well you can continue to *believe* whatever is going to happen, but don’t be surprised if it turns out you are badly wrong. Wisful thinking is not a plan, at least not in my mind.

If the COMAC C919 receives EASA certification, in 1926 (about 5 years after production starts and EIS into China) then COMAC will have a production line producing 13 aircraft/month with a certified product that can both fly and be sold internationally. It will also be a fully debugged and mature product.

No wonder Faury wants to push the A32x supply chain to 75/month. He must want to saturate the global markets before COMAC ramps up.

There are plenty of ‘poor’ nations that will find the prices of the C919 attractive.

Small typo: you meant 2026…not 1926.

In addition to the price aspect of the C919, there are plenty of countries that are not “western-centric” and that would welcome the opportunity to buy a Chinese plane. These countries will not be particularly concerned as to whether or not the Chinese plane is certified by the FAA/EASA — just as most of Asia-Pacific continues to keep the MAX on the ground, regardless of what the FAA/EASA thinks. US/EU airspace is just a tiny fraction of the globe’s area…there’s plenty of jetting around that can be done without ever entering it.

I agree with your statement about the Airbus ramp-up: Faury wants to get as much as possible delivered before the C919 comes online. Let’s see now if GE will pull the nationalistic card and impede a hike in LEAP production rates so as to help protect BA’s interests. I can see this turning into a dogfight.

“Fully debugged” in 2026 ? I believe thats wishful thinking, historically Boeing and Airbus needed longer to iron out even critical kinks.

Boeing can realistically only make their next move in the narrowbody area once the next gen of engines becomes available. It makes sense for Airbus to burn through their backlog while they still have a clear advantage and bank that money.

“””No wonder Faury wants to push the A32x supply chain to 75/month”””

The backlog of the A320family is simply too big. When customers place an order they should not have to wait so many years. 75 per month might not have to do anything with the C919.

@ Leon

Yes, the C919 is probably only part of the driver behind the increased production rate.

As you indicate, Faury also probably wants to be able to offer earlier slots to new start-ups / fleet expansions arising out of the ashes of the current crisis.

@ Jas