Leeham News and Analysis

There's more to real news than a news release.

Airbus 1Q2026 Results: First quarter “suffering”

By Karl Sinclair

April 28, 2026, © Leeham News: An abnormally downbeat Guillaume Faury, CEO of Airbus, was clearly not pleased with how things progressed in the first quarter of 2026.

April 28, 2026, © Leeham News: An abnormally downbeat Guillaume Faury, CEO of Airbus, was clearly not pleased with how things progressed in the first quarter of 2026.

When asked when commercial aircraft delivery rates will converge with production rates, he said, “We don’t like to guide or to give rates when it comes to monthly production rates or even quarterly production rates. It’s non-linear and tends to be backloaded in Q2 and Q4 in most years. That’s something that we are suffering from probably more this year than I remember we’ve ever suffered in the first quarter. But we believe, we hope, we believe we should be reasonably back to where we should have been by the end of H1.”

Faury outlined a series of issues plaguing the company, calling it a “desynchronization between production and delivery,” which includes panel quality issues, an “administrative delay” that affected the delivery of nearly 20 aircraft to China, the Pratt & Whitney engine problems, ongoing seating shortfalls, the continuing tariff war, and the recently started Iranian War. The latter two were launched by President Donald Trump.

Faury outlined a series of issues plaguing the company, calling it a “desynchronization between production and delivery,” which includes panel quality issues, an “administrative delay” that affected the delivery of nearly 20 aircraft to China, the Pratt & Whitney engine problems, ongoing seating shortfalls, the continuing tariff war, and the recently started Iranian War. The latter two were launched by President Donald Trump.

While he was detailing the current travails of the company, Faury said, “As the basis for its 2026 guidance, the company assumes no additional disruptions to global trade or the world economy, air traffic, the supply chain, its internal operations, and ability to deliver products and services.”

The tenor of the earnings call is somewhat surprising. But Airbus underperformed in its first quarter results. However, this is hardly a “It’s time to sell the silverware” moment.

Company-wide results

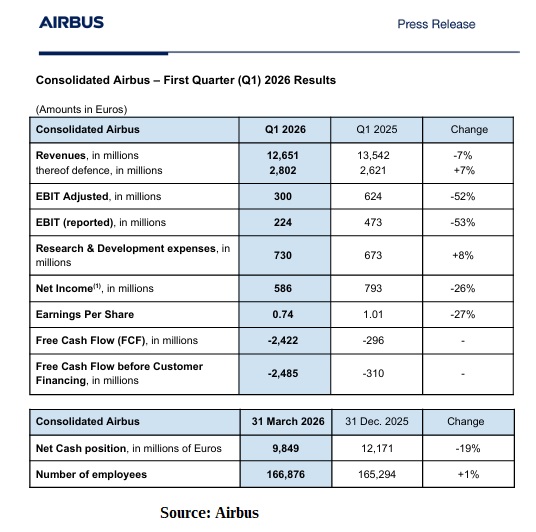

In what can be described as a difficult quarter for the corporation, by Airbus’ standards, the company earned a modest €300m (EBIT adjusted) on revenues of €12.651bn (€624m earned on revenues of €13.542bn in 1Q2025). This is a decline of €891m in sales and €324m in earnings, a whopping year-over-year drop-off of 7% and 52%, respectively.

The gulf widens even further compared with the results of the previous quarter, when the company earned €2.982bn on revenues of €25.984bn. While across the industry, Q4 is habitually the strongest period of the year (when deliveries are backloaded), Airbus expected to perform better in the current quarter than it did. This is highlighted even further, when compared to a strong FY2025, when it delivered 793 aircraft to customers and grossed €73.42bn in revenues and €7.128bn in earnings.

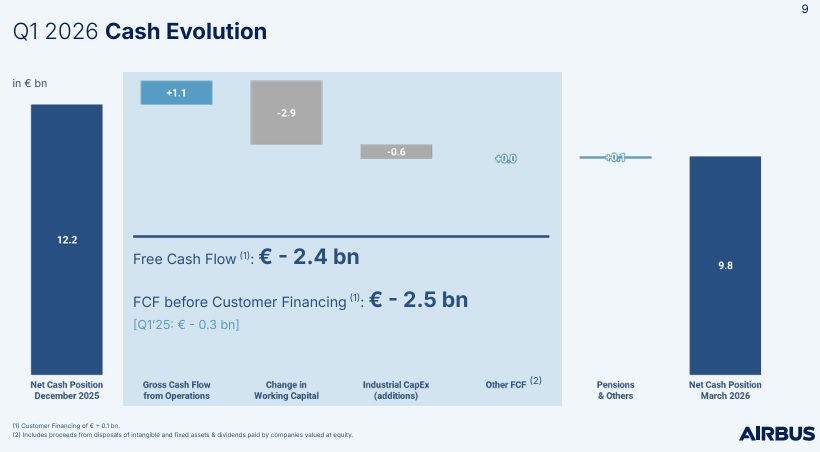

Airbus used €2.422bn in free-cash-flow (FCF) during 1Q2026.

“We built $5bn of inventory. That is significantly more than the build-up of last year, almost $1.5bn more build-up…that explains, obviously, the free capital development,” explained CFO Thomas Toepfer.

“We built $5bn of inventory. That is significantly more than the build-up of last year, almost $1.5bn more build-up…that explains, obviously, the free capital development,” explained CFO Thomas Toepfer.

Expectations are that the inventory will unwind in the coming months, reflecting in an improved financial performance in the near future. The silver-lining to the 1Q2026 results is that company earnings were still (modestly) in the black and full-year guidance remains unchanged.

Commercial Aircraft

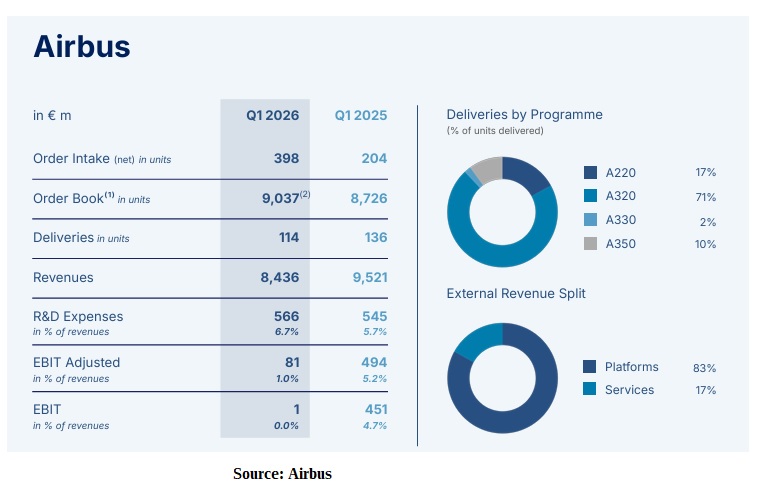

Revenues at Airbus Commercial declined €1.085bn in 1Q2026, year-over-year. This was driven by the “de-synchronization” between production and delivery, with the company unable to handover aircraft to customers and the resulting build-up of inventory waiting for delivery.

EBIT Adjusted plummeted to a paltry €81m, or less than a 1% margin on the €8.426bn generated in sales.

A total of 114 commercial aircraft were delivered (136 aircraft in 1Q2025), including 19 A220s, 81 A320 Family, 3 A330s and 11 A350s.

When asked about any updates on the Pratt & Whitney engine situation, CFO Toepfer said, “The shortage is the same shortage that we were talking about in our full year call. The situation in terms of what they told us they would deliver for 2026 has since then not changed.”

Airbus has also approached CFM, which markets the LEAP engine (which also flies on the A320 family of aircraft), to request help in ameliorating the engine shortage problem.

“We have worked with CFM to the maximum extent possible. They’ve supported us to the extent they can to offset part of the missing engines. But we also must deal with a mix of engines and the flow in the contract. So, it’s something we are trying to leverage as much as we can, but it’s not enough to offset the significant number of missing engines,” said Faury. “Pratt & Whitney remains the key pacer of our A320 ramp-up trajectory and deliveries for this year and for next year, impacting both 2026 and 2027.”

Seats and interiors

Seats and interiors are also in short supply. They are buyer-furnished equipment (BFE), which is ordered and paid for by the owner of the aircraft. There is a draconian solution in that regard, one which Airbus is reluctant to use.

“They impact the way we deliver–the completeness of the aircraft, especially when it comes to seats. You might remember that we’ve delivered, and we are entitled to deliver by contract, aircraft without the seats when the seats are buyer furnished equipment and they are late or very late. We don’t like to be doing this. We like to find solutions with customers. But that’s something sometimes we must do,” explained Faury.

This is the second earnings call in a row (the first being the P&W agreement), that enforcement of contractual rights has been mentioned, regarding equipment from suppliers.

Airlines, lessors and aircraft OEM’s traditionally work together to overcome the myriad of issues that arises over the life of a contractual order without the public ever knowing.

This is a troubling development, if it continues.

The bright spot of the quarter was the addition of 398 net orders to the backlog, which is now more than 9,000 aircraft, including a much-needed order for 20 jets in the A220 program. There was also a record freighter order by Atlas Air Worldwide, for 20 A350 freighters. This was a major win for Airbus, winning out over the Boeing 777-8F. Atlas has been an exclusive Boeing customer and operator.

Despite the plethora of headwinds, all guidance regarding yearly deliveries of 870 aircraft and all planned production rates remain unchanged.

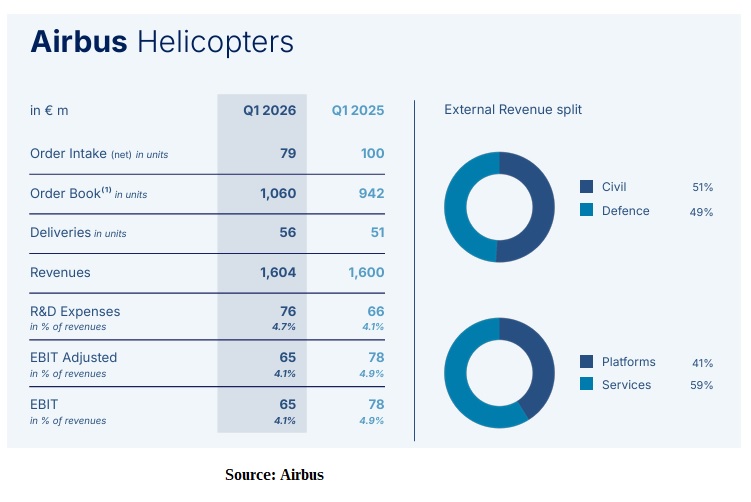

Airbus Helicopters

Revenues at Helicopters leveled out through the first quarter (€1.604bn vs €1.6bn in 1Q2025), with EBIT adjusted dipping to €65m and a 4.1% margin (€78m and 4.9% in 1Q2025).

“In Q1 of this year, we delivered 56 helicopters, five more than in the first quarter of 2025. Revenues stayed flat at €1.6bn, reflecting a less favorable delivery mix in the first quarter. As a result, EBIT adjusted to the 65 million euros, reflecting a solid performance from programs offset by higher R&D expenses,” explained Faury.

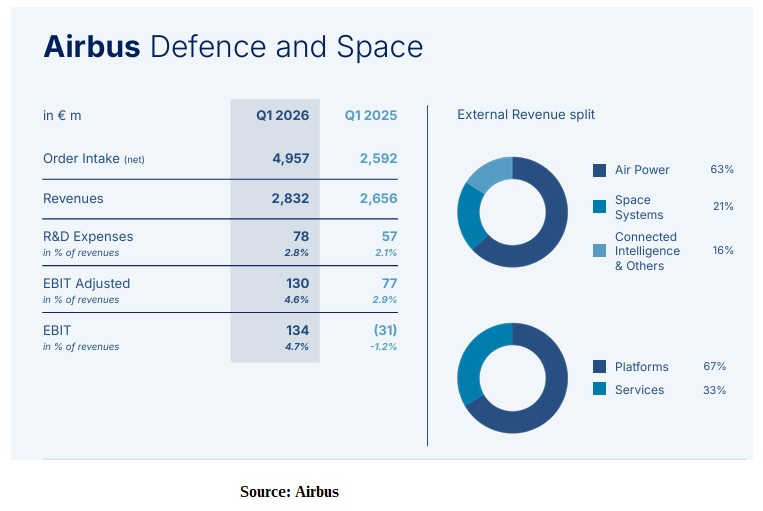

Defence and Space

The bright spot of the quarter was Defence and Space, with increased revenues and EBIT adjusted. This is undoubtedly driven by the Iran War and mounting tensions between Europe and the United States.

“We finished Q1 with a very strong order intake of €5bn, mostly on the air power side, reflecting the need from our customers for military aircraft and services,” detailed Faury.

Revenues were up €176m, EBIT adjusted gained €53m and the margin grew from 2.9% to 4.6%, during 1Q2026.

This is a welcome change for the division (and for all of Airbus), which had been a drag on the company’s financial results, in previous quarters.

Maintaining guidance for now

Despite all the headwinds that Airbus faced in the first quarter, it is holding firm to the guidance issued at the beginning of the year for 870 commercial aircraft deliveries, EBIT adjusted to ~€7.5bn, and free cash flow before customer financing of ~€4.5bn.

Interesting rhetoric from AB, who for some reason appear to be sandbagging. “We doing so bad!” Mmm..

The Other Outfit / their nominal competitor would be lucky to have such “problems”.

“…the company assumes no additional disruptions to global trade or the world economy…”

Good luck with that!

On top of everything else going on at the moment, the world is facing a worsening shortfall in supply of aluminium, plastics and rubber.

Also, with jet fuel prices staying elevated, it’s only a matter of time before airlines start to fail — with attendant effects on order books at the OEMs. One wonders if the first order deferrals — or even cancellations — are already going on behind the scenes…

***

Apart from all that, it’s notable that:

– BA had a record good quarter in terms of deliveries, and still reported a gaping loss (especially using unit accounting);

– AB had a very poor quarter in terms of deliveries, and still managed to make a profit.

Strange that Airbus commercial aircraft deliveries loose tempo after each new year. One would think each FAL should run its monthly tempo and stores should be stocked well ahead of time of all components needed for aircraft installation, roll out and paint. Somebody might have the answer. One would think that with 2 new FAL that deliveries should scale up.

Production of the frames doesn’t appear to be an issue. At the moment Airbus have over 210 A320 family frames that have come off the FAL at the various sites but haven’t been delivered yet. That includes around 80 that have had at least one test flight.

There are about 40 A350s that have rolled out as well. I don’t know about A220/A330s.

I’d assume apart from engines and seats, stores are well stocked.

One would think Airbus could make 2 classes of seats already certified and just install them and deliver the aircraft. Then the airliners just return them serviceable once finally they get theirs certified and delivered.

The seats for the Douglas DC-3 were produced by the Douglas Aircraft Company as part of the overall aircraft manufacturing process in Santa Monica, California. These seats were designed to be comfortable and, in the case of the Douglas Sleeper Transport (DST) variant, convertible into berths.

Claes

Expecting the addition of 2 FALS to ramp smoothly and efficiently produce aircraft makes sense, but isnt in the cards. Its not the wrong way to build aircraft, it just exposes you to a different set of risks. If you compare the 737 line to the distributed lines Airbus uses, the risk of distributed parts distribution is more problematic for Airbus. You can get behind 3 or 4 shipsets on a lifeline part like gear legs, and while thats bad, its worse when you try to cure the line stopper in 3 different locations rather than 1. The logistics of getting the correct part to the correct location is more work for your logistics people. The ability to recover thru the use of overtime is easier to do in a single place instead of 5 different factory’s. Conversely, there are offsets that make the distributed model a better choice. An accident, fire, earthquake or railroad derailment can shut down your entire production line. A bad process error such as the incorrect 787 shimming would be far easier to correct in a distributed model as the likelihood of the error being system wide is far lower. There is also the not so inconsequential issue of labor unrest by greedy Americans. This is one of those times where you choose between bag of problems A or B. I prefer to have 1 location, but maybe that’s because I have far more experience doing it that way. Airbuses’ distributed model definitely has things going for it in that a rate change, either an increase or decrease is spread over so many locations means far more stress than throttling 1 location. I hope this helps….

It’s interesting (to me) to see the different stages of production and delivery at the various Airbus sites.

I know things will never run strictly in MSN order but it gives you a rough idea as to where things are.

I’m assuming Airbus allocate production to the various lines so that they’re all supposed to be at roughly the same point.

At the moment it’s the Chinese production at TSN that’s ahead in MSN numbers for the A320 family. They’re test flying and delivering frames in the 13300 range. They’re not just doing Chinese airlines there – they also do some for EasyJet, Wizz Air and now Transavia France.

TLS is generally delivering in the 13100-13200 range with a few outliers.

BFM which at the moment is solely for aircraft for the Americas is in the 12900-13000s.

XFW appears to be a bit mixed. One one hand they’re delivering the 13100s but they also have a load of A321XLRs as well as standard frames in the backlog, some of which haven’t been assembled yet, in the 12500 -12900s. The current lowest MSN to be delivered is a Delta standard A321, MSN 12336, that has finally had test flights at XFW this week. It was seen painted in full colours last September. MSN 12337 was also a Delta frame and that was delivered from BFM in July 2025.

More (long-term) AB orders on the way from China:

“China’s Spring Airlines targets 300 aircraft by 2035”

“Spring Airlines (9C, Shanghai Hongqiao) is aiming for a fleet of 200 aircraft by 2031 and around 300 by 2035 as it maintains an all-Airbus narrowbody strategy, its vice president Zhang Wuan declared at the event Routes Asia 2026, as reported by industry outlet Aviation Week.

“Speaking during a keynote interview, Zhang pledged that the low-cost carrier would continue to operate only A320 family aircraft and avoid widebody acquisitions, citing current market conditions. The airline expects to add around 30 aircraft in 2026.

“The additional capacity will support international expansion, while maintaining a focus on medium-haul routes of about 1,200 kilometres, where the airline remains competitive against high-speed rail.”

https://www.ch-aviation.com/news/166578-chinas-spring-airlines-targets-300-aircraft-by-2035

“China Southern Airlines orders Airbus jets worth US$21b as Boeing deal remains rumour”

“Airbus secured an order for 137 A320neo jets from Chinese airlines, extending the European company’s edge in one of aviation’s most contested markets as US rival Boeing waits on a long-speculated deal with Beijing.

“China Southern Airlines, one of China’s three major state-owned carriers, announced the deal on Wednesday. The airline, based in the southern city of Guangzhou, will purchase 102 aircraft, while its subsidiary Xiamen Airlines will acquire the remaining 35.”

https://www.scmp.com/economy/china-economy/article/3351900/china-southern-airlines-orders-airbus-jets-worth-us21b-boeing-deal-remains-rumour

Of course. China under its party-state economic system will have the central buying agency for state owned carriers take the output of the Airbus Tianjin TWO A320 Family FALs

But under recent new rules, once you set up shop in China you cant leave. The 21st century Hotel California

Why people think they know better than those with many years’ of experience? Talk is cheap.

RTX CEO Greg Hayes stated that the company cannot decouple from China

Hayes explained that with thousands of suppliers in China, decoupling is impossible

Hayes suggested it could be difficult to produce without Chinese suppliers.

PEDRO

what prompted this. I haven’t seen any talk of decoupling. Do you have that reference at hand…..