Leeham News and Analysis

There's more to real news than a news release.

Latest twin-aisle orders shift market share; Plus Odds and Ends

The flurry of orders in September and this month from Lufthansa Airlines and Japan Air Lines tightens the wide body race between Airbus and Boeing.

Airbus and JAL on Monday announced a firm order for 31 A350s and options for 25 more. Last month, Lufthansa announced a firm order for 34 777-9Xs and 25 A350-900s.

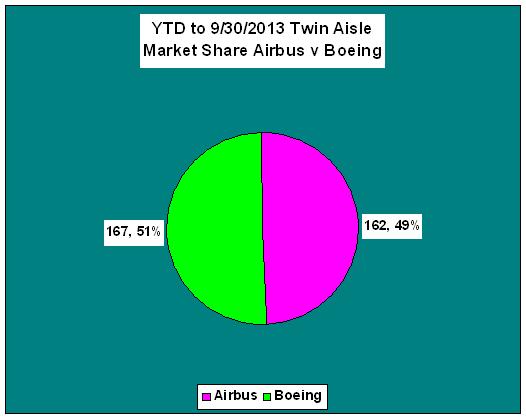

Sources: Airbus and Boeing

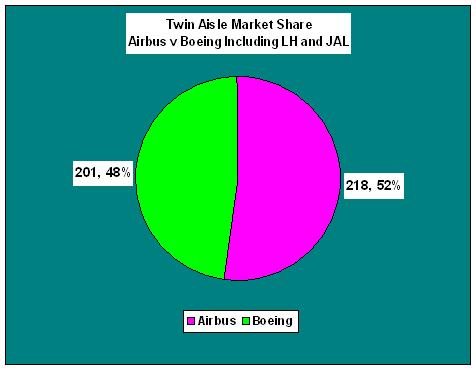

Sources: Airbus and Boeing

Airbus traditionally has significantly trailed Boeing in the twin-aisle sector, but so far this year the race is running about even through September. The Lufthansa orders for the Boeing 777-9X and the Airbus A350-900, announced in September, are not reflected yet, nor is the Japan Air Lines order for A350-900s and -1000s. None of these orders has been booked yet by either OEM. Airbus would take the lead.

Adding the new orders, Airbus has 218 twin-aisle orders and Boeing 201, essentially reversing the market share (below) from the chart above.

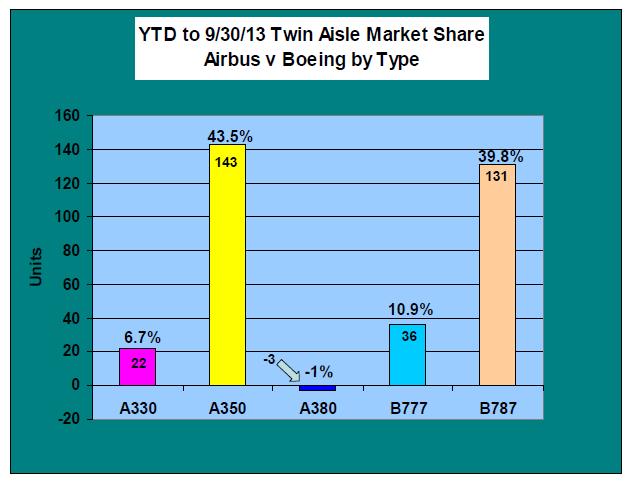

By equipment type (Bar Chart, below), sales of the A330 and 777 have slowed from the previous two years, while orders for the A350 and 787 continue to pick up despite meaningful quantities of production slots being unavailable until 2020.

Sources: Airbus, Boeing data

Sources: Airbus, Boeing data. Excludes Lufthansa and Japan Air Lines orders, not yet booked through 9/30/13. There were no orders for the Boeing 767 during the first nine months of the year and a net change of zero for the 747-8, following five orders and five cancellations.

This suggests why Boeing is trying to figure out how to take 787 production to 14/mo by the time the 787-10 enters service in 2018; and why Airbus is evaluating the creation of another A350 production line to add to the currently planned capacity of 10-13/mo.

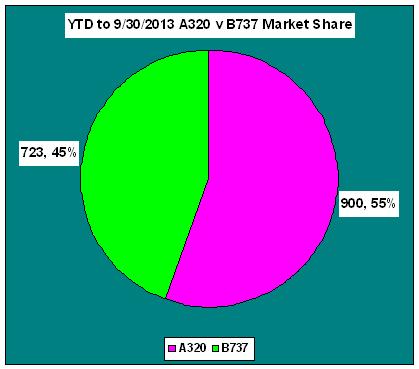

In the Single-Aisle sector, Airbus continues to maintain its market share lead. This chart reflects all single-aisle sub-types, including the current generation of A320s and 737NGs and their re-engined siblings.

In the Single-Aisle sector, Airbus continues to maintain its market share lead. This chart reflects all single-aisle sub-types, including the current generation of A320s and 737NGs and their re-engined siblings.

Sources: Airbus and Boeing

Odds and Ends

Stretch or no stretch for A350-1000? John Leahy, COO Customers said Airbus is studying whether to stretch the largest member of the A350 family to offer a plane closer in size to the forthcoming Boeing 777-9. But then he takes it back again. See this Aviation Week story.

Afterlife for A340s: Aviation Week reports that Airbus sees an active secondary market for the A340 family. Low capital costs and lease rates certainly can extend the life of airplanes, as history demonstrates. Airbus might not be wrong.

LIghting up: In another story we did for APEX, a German company has come up with a new lighting system that has been certified for the Airbus A320 family. This doesn’t sound exciting, but we found it more interesting than we thought when we stopped by the booth at the Aircraft Interiors show last week in Seattle. There is a composite photo showing the before-and-after and there really is quite a difference.

Silver lining in Delays: Seems hard to believe, but Aviation Week’s story on the Mitsubishi MRJ suggests there might be one.

Regarding A340: if you are cash-strapped airline, the 340 is the most potent aircraft you can get for small money. The 340 is better suited for hot’n high or short runways. Challenging conditions for a B777-200ER, especially if flown with dense seating layouts.

Actually, the A340-200/300 are not at all very good hot & high performers. The installed thrust is quite low: 600kn for 275tons of MTOW vs 800kn for 300tons on the 777-200ER. Captains complain they take for ever to reach cruising altitude!

The A340-500/600 is a different story of course.

Which A340 does Air France fly to St Maartin? This short runway, with mountains at one end, is difficult and the AF A340 operates much better out of there than the Boeing 747-400.

Re: St. Martin. AF uses A340-300. According to Airbus docs, the 343 could take off SXM (7500ft runway) with a reduced max take off weight of around 250tons which is fine for the required range to CDG. However, the situation changes radically with altitude. Same conditions at 6000feet and the max take off weight goes down to about 210 tons (of max 275). My info is based on ISA conditions (15celcius) so actual performance at SXM would be lower still.

It’s not 600kN/275t against 800kN/300t but

3/4th of 600kN/275t against 1/2 of 800kn/300t ( i.e. 1 engine out conditions )

normalised this is 1.64kN/t for your example A340 and 1.33kN/t for the 772.

This is reflected in required take off runway length: A340/747-400 : 3100m 777-200ER : 3350m

You’re correct Uwe, the one engine out requirements limit the higher thrust performance of the b777-200er. Checking Boeing docs reveals a MTOW of just around 255 for SXM , a much higher penalty (-45tons) compared to the (-25tons) on the 343. It also gets worse with altitude, so you’re totally right Schorsch! I was too influenced by the bad climb reputation the 342 had at the airline I worked for.

I think during the last 18 months Airbus managed to capture a good part of the 777 replacement market.

http://i191.photobucket.com/albums/z160/keesje_pics/A350orders777operators_zpsf8017683.jpg

Everybody is looking at Emirates as the cavalary coming in to ave to kick start the 777x. I think we have to realize EK are in the books for 70 XWB’s and have options on 50 more.

Last year everybody was amazed when Boeing slowed down 777X development and said they had time to first fully understand how the undefined A350-1000 would look and what the market really needed. Albaugh left etc.

I remember stating that the time had come to panic, when CX and SQ switched. But Boeing remained very self confident. http://seattletimes.com/html/businesstechnology/2018972134_boeing777x23.html

At least LH’s A350 has actually been booked already. Airbus’ September spreadsheet already shows 25x A350-900 for LH, as well as their cancellation of 3 A380s and BA’s order for 18x A350-1000.

http://www.airbus.com/fileadmin/backstage/orders_deliveries_table/Sept_2013_-_orders_deliveries_Airbus.xls

Here’s the twin-aisle order breakdown from Airbus for September, for completeness sake:

04-Sept: 10x A330-300 – Delta

20-Sept: 25x A350-900 – Lufthansa

26-Sept: 18x A350-1000 – British Airways

no date: -3x A380-900 (Lufthansa)

About a possible A350 further stretch, for fun I stretched the A350-900 into a A350-1000. Still a lot of wing it seems. And the -1000 wing is even a bit larger then the -900 wing.

http://i191.photobucket.com/albums/z160/keesje_pics/A350-1000studykeesje_zpseca1d6df.jpg

It seems Leahy is starting testing the water for a -1000 stretch. Soft enough to avoid formal repsonses, strong enough to create doubts among airlines that are both XWB customers and 777X prospects.

I do not see major technical constrains, the -1000 wing, landing gear and engines seem scale-able for e.g. ~10% growth.

Keesje, The key to a A350-1100 lies with the risk that RR is willing to take for a unique engine for that model. RR was willing to build a special engine for the 777X and now that they have been rebuffed by Boeing and for the moment are the only A350 engine supplier, it may be possible that RR use their engineers that would have been working on the 777X power-plant and point them to developing a 460 KN Trent XWB,

If you read wikipedia Rolls Royce were the first to reach 100,000lb thrust and subsequently115,000 ft lb thrust (510 KN)with engines Trent 8104 and 8115. So it depends if Airbus wants and has a customers requiring such a stretch on the A350-1000.I’m sure RR could achieve 450KN with XWB Engine.The thing is,Rolls Royce,made a point of not increasing the overall size of the engine,hence the overall size of the A350-1000 engine is no bigger than the 800/900.The main problem for Rolls royce

would be getting a quart into a pint pot so to speak,keeping the engine size down to the 97,000lb ft thrust but obtaining 115,00 lb ft from it.

NEO is moving further ahead…

The NEO is ahead because it will enter the market 2 years before the 737 Max. With a production rate of 42 units per month, Airbus has 42 * 12 * 2 = 1008 more delivery slots to offer. This figure is about the difference we see in the backlog (1500 vs 2400).

I understand that, and I may have been the first one to point this out on this blog. But nevertheless, the advantage including options is now closing in on 1,200, and on the other hand Airbus produces less than 12*42 a year, it appears to be more 11.5* that, so Airbus may now be 5 months of production ahead. The point I was making was rather that Boeing is not catching up, closing the gap, or even holding its position.

Sorry, not closing in on 1,200. 1,130 to be precise.

http://www.pdxlight.com/neomax.htm

Also, on average per day since launch, the NEO has sold 0.5 units more than the MAX (3.44 vs. 2.93) if you include MoUs and options.

So the additional available units due to earlier EIS are the last comfort Boeing has in the NB battle. It seems to grow colder.

I guess the total 737NG+MAX vs A320 CEO+NEO backlogs would provide be a better comparison.

Neither NEO nor MAX will do a full fledged step to 50 frames per month on EIS.

For Airbus the minimum they are comfortable with seems to be 2.5 years for the switchover.

Thus when the MAX debues not more than ~380 NEOs will have been made available to the market.

@Andreas

You’re right about the Airbus production rate. It’s more like 42 * 11 months per year if we include all the vacations in Europe.

The Trent XWB for the -1000 was significantly modified. You can be sure RR isn’t investing for a 97k lbs without any growth potential. RR has always boosted the scalability of their 3 spool designs in terms of thrust range.

Theoretically Airbus could aim for a A350-900, -1000 and -1100 family, without overlapping with any future A330 developments (unless they do a A330-400NEO 😉 )

http://i191.photobucket.com/albums/z160/keesje_pics/AirbusA330-400NEO-1.jpg

So the 777 will get a life extension, the 787 and A350 seem to be on the road to success (at least with sales, the jury is still out on the A350 flight test/certification program and the performance numbers).

I wonder what both OEMs have planned for after these aircraft. Airbus a A330 replacement or even perhaps a NEO after all? Boeing a new 757/new single aisle type of line? Or would Airbus go for the gap between the 777 and the 747-8?

Boeing seems to believe they have the whole widebody segment covered so I don’t see them doing anything but smaller aircraft post 2020, but is that a correct assumption?

Performance:

787 seems to have just now reached its 2008 ( EIS ) performance data

while the A350 seems to be very slightly ahead of its “2013” spec sheet.

“keesje

October 8, 2013 @ 4:31 am

I guess the total 737NG+MAX vs A320 CEO+NEO backlogs would provide be a better comparison.”

I agree, if someone has those, it would be very interesting.

Wikipedia says that at the end of 2012, the total backlogs were 3629 for the A320 family and 3074 for the 737 family.

Hmmm. Then you need to carve out OEOs/NGs from that. Halfway there. 🙂

So adding the new orders (900 and 723 for the A320 and 737) and subtracting the deliveries to date (353 for A320 and 325 for 737) we end up with a calculated backlog of 4176 for the A320 family and 3472 for the 737 family as of the end of September.

I think my math is right, but of course actual backlog numbers from A and B would be better.

Thanks!

Combining the two generations’ backlogs as the metric, A has about 55% of the narrow-body market share … coincidentally the same number as for the orders in 2013 to date.

I guess there’s also a question of when you ramp up production. If the 737 has a longer period to get the current model out of the system, Boeing doesn’t want to ramp up too soon – other wise it will be left with a bunch of empty or unprofitable slots to fill before the new model comes on stream.

What a meaningless topic when these trends are measured over years and not 9 months. Quite ridiculous really. And if Boeing garners 100+ 777X order by year’s end it will change it around completely. Maybe you can then do a month by month or week by week chart.

My thoughts exactly. Rather than order tallies, I think the widebody product mix would be the more accurate predictor of long-term market share. Boeing has or shortly will have two modern in-demand product families with solid current and future sales prospects (787, 777x) and one end of life product on its way out (747-8 – I’m not even counting the 767 anymore). Airbus has or will have just one modern WB product line – the A350 family. The A330 had a great run but it’s old and will eventually fade out sales-wise, while the A380, already showing its age, hasn’t been and will probably never be a hit – even if it manages to stick around somehow, it’s not going to significantly affect the numbers. So that’s two against one. Am I missing anything?

Well yes: The A330 and B777 are both ‘equally old’ or ‘modern in-demand’, having entered service within a year of each other, both once upgraded and both with planned upgrades. The sole difference is that the 777 planned upgrade is a very expensive proposition while that for the 330 is minimalist in comparison.

So as far as I can see in twin aisles both A and B have one new and one middling line, with B having one old VLR and A one new VLR line.

777X is not the first major upgrade for the type.

The changes towards the -200LR / -300ER subtypes were neither simple nor cheap. Then how much did the original basic -300 stretch cost ? It didn’t sell all that well which probably forced the -300ER.

Actually wondering how the Airbus “continuous detail twiddling” strategy compares to the Boeing “step enhancement” way of doing things.

I don’t believe you are missing anything. It is two against one.