Leeham News and Analysis

There's more to real news than a news release.

Airbus, Boeing freighter demand forecasts optimistic, says P2F company

Special to Leeham News

By Cliff Duke

LCF Freighter Conversions

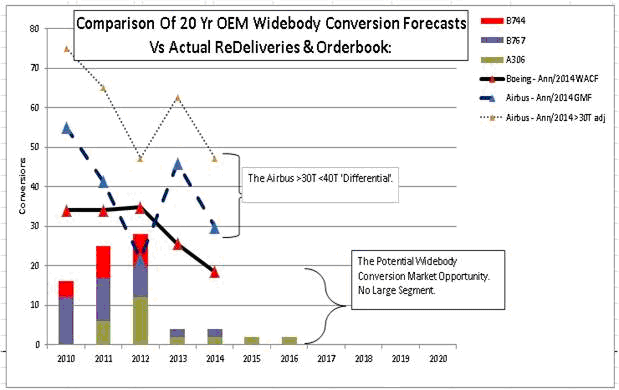

I have mapped out below the last five years of OEM forecasts (Boeing World Air Cargo Forecasts and Airbus Global Market Forecast data) on widebody conversions calibrated against the actual widebody aircraft conversions redelivered and the current respective order books. If this is half right, it suggests that if in 2010 you were a widebody aficionado and you set your stall out on the Boeing or Airbus 20 year forecasts published that year, you would, reading their 2014 forecasts, now be looking at a 46% reduction in that forecast and your 2010 business plan might be developing cracks.

In terms of performance to date, a quarter the way through the 20 year 2010 forecast (assuming an equal spread of conversions across the 20 years of the forecast) we are currently some 70 conversions behind the Boeing 2010 forecast, a 50% drop off from where we thought we would be. It looks unlikely that the variance can be recovered in the remaining 15 years of the 2010 forecast. In the meantime Boeing and Airbus have updated their 20 year forecasts, and the overall drop off forecast is significant.

One question is, have the OEMs now updated their outlooks enough? Could both forecasts still be too optimistic and could our 2010 investor be looking at a further 50% drop off when revisiting the OEM forecasts in five years’ time (2020)?

Figure 1. LCF Conversions says the Airbus and Boeing 20 year freighter demand forecast have been substantially over-optimistic. Click on image to enlarge for crisp image. Source: LCF

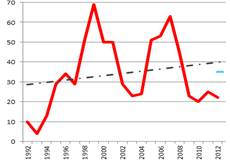

Figure 2. Wild swings in the wide-body P2F conversions during the past 20 years. Source: LCF. Click on image to enlarge and for crisp view.

Before launching into answering the question, a couple of comments on the methodology applied. The 20 year forecast is broken down to an annualized average. I know we will end up with wild swings (Figure 2: wild swings experienced in the last 20 year in the widebody conversion market) but it’s a snapshot of how we have done and are doing in the current decade (2010-20).

A note on how I have arrived at the Airbus widebody numbers. In order to create an all-widebody picture out of the Airbus forecast, I strip out the Airbus ‘anomaly’ of including >30T conversions in its forecast by assuming the Boeing single aisle forecast is a good datum. By assuming the Airbus and Boeing forecast agree on the single aisle numbers, this means the balance of numbers in the Airbus forecast are what they assume are widebody conversion opportunities. If the A321 is a 27.5T payload freighter, it’s difficult to understand why Airbus skew their forecasts this way and don’t line up with the Boeing single aisle/widebody categories. Other than the 757, I am wonder what is in the Airbus forecast in the >30T category).

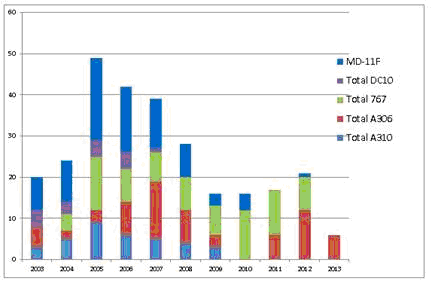

Figure 3. LCF’s own view of the 20 year P2F demand. Source: LCF. Click on image to enlarge and for a crisp view.

To try and answer the question, it seems to me that the >100T is dead for conversion opportunities and the jury is out how the <100T widebody conversion opportunities will pan out. Assuming the future will replicate the past, then after taking into account that the >100T conversions are now out of the picture; there is no feedstock and good, new long range products exist (the 777F & 747-8F). Assuming Boeing launches the 777-200ER P2F (it’s a straight MD11 replacement (82T payload) and key potential target operators are currently FedEx and UPS)), will the 777-200ER BCF fit in future fleet plans? If so, then the picture that would develop (assuming the past 10 years were replicated in the next 20) would reflect approx. 300+ conversions over 10 years or 600 over 20 years and nearer the Airbus forecast, or what we think the Airbus widebody forecast is. (Figure 3.)

The problem is that the future may not replicate the past. The leakage from the medium widebody conversion heartland could be significant. Key factors here are:

- OEM desire to focus on new builds. Boeing and Airbus now have control of the conversion programmes (which programmes, when launched and at what price). The cost of adapting passenger third-generation aircraft to conventional P2F configurations is expensive. There are two new-build freighter options looking in trouble (747-8F and A332F – backlog: 19 and 11 aircraft respectively) neither need perceived cannibalization from conversion options.

- Integrators (FedEx and UPS et al) dominate the potential customer base (~60%). They are not capital-constrained and have expressed a preference to buy new as have oil-rich Middle East operators currently moving the cargo centre of gravity to the Gulf.

- The finance community has little if any appetite for financing widebody conversions (unless underwritten by gold-plated credits). The experience in recent conversion activity (747-400 conversion programme being a good example–Cathay Pacific Airways having scrapped or disposed of almost all their converted aircraft within six years of conversion, suggesting life expectancy for widebody conversions may need to be re-thought) has not been good and the overhang of regulatory threats such as age limitations and noise regulations, remains.

- The size of the third generation fleets (with a few exceptions) are so significant that part-out of passenger aircraft and resale of cannibalized parts (specifically the engine after-market potential) is a lucrative proposition that competes with (in many cases undermines) the case for the alternative-use conversion option on potential donor aircraft.

- The shelf life of the status quo has shortened, meaning the need for affordable, flexible solutions in all areas including the freighter platform format. The ‘profound change’ (says Fred Smith, CEO of FedEx) in the freighter environment is putting operators under constant pressure to develop more cost effective work-around solutions such as extending planned fleet retirements and the increased move to belly capacity (even FedEx now does this). Boeing recognizes the belly cargo threat. Airbus is more sanguine about the potential impact. A threat not yet recognized comes from the fourth generation passenger aircraft (B787, A350, B777X). All have significant range and freight capability, which means that these can carry a sizeable amount of cargo much farther, such as Northeast Asia to US west coast (LAX or SFO) with 20T per flight. One daily flight equals a 747-8F load over the week; twice daily equals two 747Fs. Over time, on the longer haul sectors (in particular trans-Pacific), these could turn into belly only markets just like the Atlantic is now – all cargo carried configured to the diameter of the Lower Deck Cargo Door.

LCF is a conversion solution for all the third and fourth generation widebody passenger aircraft fleets. The LCF proposition is that there will be demand in some markets for an alternative approach that reduces the engineering challenge and the cost associated with undertaking conventional P2F conversions on third and fourth generation widebody aircraft. The underlying demand for low capital cost, low utilization widebody lift will remain, but we need to recognize that the appeal for widebody conversions is being eroded and this demands cheaper and more flexible conversion solutions on fuel-efficient platforms. In time, this could leave the flexible, low cost LCF solution well placed to compete with high capital cost OEM conversion solutions.

LCF conversion options will eventually cover the 777-200, 777-200ER and 777-300 variants with the GMF (General Market Freighter); and the Airbus A330 variants.

Quote/In time, this could leave the flexible, low cost LCF solution well placed to compete with high capital cost OEM conversion solutions./Unquote ??

In my understanding, no such things exist as are dubbed hereover “high capital cost OEM conversion solutions”, simply because all (P2F or LCF) conversion solutions are low cost solutions, based as they are upon fully amortized end-of-useful-life paxliners. In comparison, paxliner-F newbuilds or “dedicated freighters” deserve better the “high capital cost” distinction. However, as the acquisition price is impacted upon by the airfreighters’ residual “economic life”, which is typically no more than 7-12 years for P2F/LCF conversions whereas for -F newbuilds it is a full 35 years or more, at the end of the day the ownership costs of P2F, LCF or -F newbuilds (if the latter -F variants exist) turn out to be # kif kif ? And by-the-way, whichever (of P2F, LCF or factory-new -F) are all underbid by belly-freight onboard WB paxliners, the offerings of which are based upon a cost of around or below 18 cents of an € per FTK ! No P2F nor LCF nor -F can beat that !

UPS and FedEx seem to be holding good with the MD11s (UPS no 777F oif course, FedEx shifting the priority to 767s and UPS holding pat right now (UPS probably got a real good real on the last of the 747-400Fs)

If that MD11 capability suits them then a 777PCF might work well with its better economics.

That assumes feed stock and so far that does not seem to be happening though a few years back there seemed to be a very active program (I think it was Singapore that was going to retire the early 777s and provide the impetus for it that did not occur)

Interesting dilemma and as noted, past does not count if future is rapidly changing.

With the intensification of ULD flows onboard long range WB paxliner underdeck (belly-freight), the need for dedicated freighters (or their P2F companions) are shifting from WB LR to NB SMR, meaning that the converters shouldn’t be out of business, but rather that they should concentrate on converting NB class aircraft : 757, 737 but preferably A32x Series. These are now indeed needed to collect/redeliver feed flows of cargoes to/from WB paxliner hubs to secondary airfreight centers all over the world. There are good reasons for Airbus to consider launching the F20QR + F21QR “Quick Rotation” feeder freighters family, today unreasonably still considered the “5th wheel” of the A32x Family by Airbus Strategists, obnubilated by the competitive Sporty Game in the passenger feeder market, impeached as they are to serve both markets from a limited throughput capacity, arbitrating to abandone the A32X-F.

http://www.aircargoworld.com/Air-Cargo-World-News/2014/10/narrow-body-freighter-conversion-market-rolls/6851