Leeham News and Analysis

There's more to real news than a news release.

Asian airline market: overheated, balanced or just some spot troubles?

The Zhuhai Air Show, underway this week, comes against the backdrop of rising concerns–and large orders announced in recent weeks–of an over-ordered Asian market.

We’ve expressed concern about the large number of orders at Lion Air and AirAsia Group and AirAsia X–these two airlines alone have about 1,000 orders of various Airbus and Boeing types–and the proliferation of low cost airlines for which a shake out is inevitable. We also have expressed concern about India.

Two reports were issued in recent weeks, one arguing Asia is not over-ordered and the other taking a much deeper dive into the entire Asian market.

Lessor CIT Aerospace concludes not only is Asia not over-ordered but China is vastly under-ordered.

The Centre for Asia-Pacific Aviation (CAPA) issued a 72 page study that examines Southeast Asia, India and China. CAPA concludes the LCC market is only in its infancy in China, India continues to be a financial disaster and Asian airlines are struggling for profitability.

CIT Aerospace

CIT is one of the world’s largest lessors, with a sizable speculative order book comprised of narrow- and wide-bodies from Airbus, Boeing and Embraer. In its four-page report, CIT writes:

- Asian carriers are instituting more capacity discipline than in years past. Of the Top 50 airlines in Asia, 70% reduced their capacity growth rates in the third quarter of 2014 compared with the same quarter a year earlier. From a route perspective, of the top 50 intra-Asia routes, 25% had less capacity in the third quarter compared with a year earlier.

- CIT’s supply and demand model points to several sub-regions in Asia that are significantly under-ordered, including China and East Asia. This represents significant opportunity for leasing companies.

CIT acknowledges that a consolidation is inevitable and will “struggle” in the short term with excess capacity. But GDP growth will drive orders.

Tony Fernandes, CEO of AirAsia Group, told us a few years ago that the geography also drives demand. Asia has few highways, lots of mountains and thousands of islands, making air travel the most feasible method of transportation.

CAPA

The CAPA study, Market Analysis: Asia Pacific, begins on the front cover with the bold statement that “Asia’s full service airlines could become endangered unless they adopt new strategies for sustainability.”

Ten years ago, there were no LCCs; since then, that Asian airline industry has transformed “beyond recognition.”

Legacy carriers are struggling, with LCCs proliferating. Many have yet to achieve meaningful profitability, if at all, and some long-haul LCCs have been formed and are eating into legacy operations.

Liberalization across Asia is feeding the creation of LCCs.

“Only in this new and more relaxed regulatory atmosphere have the new pan-Asia LCCs been able to emerge and expand,” CAPA notes. “In China…there will soon be a host of…LCCs entering the market.” This is why most of the Asian order book is from LCCs, and it’s not limited to short-haul carriers. Most wide-body orders now are from long-haul LCCs, CAPA says. AirAsia X is a major Airbus A330/A350 customer. Scott and JetStar are Boeing 787 customers.

“The long-haul, low-cost model is, with the main exception of Norwegian, unique to Asia. It has prospered on north-south sectors of up to eight hours,” CAPA says. With more efficient planes entering service, longer ranges become more viable.

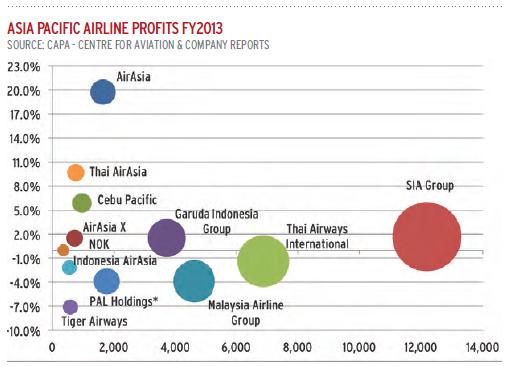

Profits remain elusive for many of Asia’s legacy and low cost carriers. Profit margin is on the left; the airline company’s size is represented by the size of the bubble. Source: CAPA. Click to enlarge.

However, profitability remains elusive. Although AirAsia’s 2013 profit margin was around 20%, this year numbers are down and the airline has deferred a handful of airplanes. JetStar has deferred, Lion Air’s LCC subsidiary faced challenges and even some of AirAsia’s affiliates are struggling. AirAsia’s initial entry into Japan fell flat, with ANA buying out AirAsia’s interests.

In Japan, we note that Skymark’s grandiose ambitions, including the now-aborted order for six Airbus A380s, have brought this carrier to the brink of collapse. A major order from a Japanese lessor, announced in advance of this week’s Zhuhai Air Show, was exclusively for the airplane size in the heart of the LCC sector. Boeing announced a new order from SMBC Aviation Capital for 80 737-8s. This is incremental and not from the Unidentifieds and it brings the MAX orders to just over 2,800.

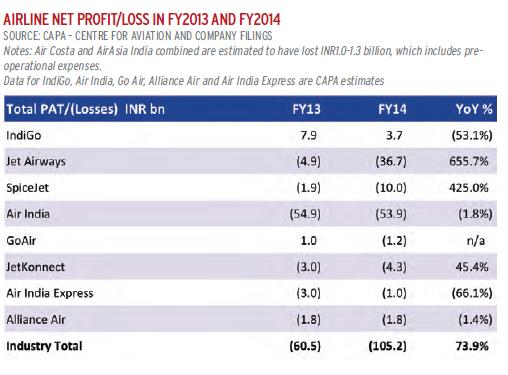

India’s airlines struggle to be profitable. Source: CAPA. Click to enlarge.

India is notoriously hostile toward airlines and profitability. Air India’s disarray is well known. But aside from Indigo, which has hundreds of A320s on order, the other airlines are losing money on a big scale, and even Indigo’s profits fell 53% YOY, according to the CAPA analysis.

CAPA believes India will have “significant” over-capacity in the next 12-18 months.

China continues to grow as a major force. Airbus and Boeing agree, in their 20-year forecasts, that China will emerge as the world’s leading market for airliner demand.

The Chinese market now accounts for about one quarter of Airbus and Boeing aircraft deliveries, according to an analysis by Flight Global. This is second to the US and it’s expected to surpass the US in the future.

But China has been slow to allow LCCs. This is changing. Honeywell, the supplier for avionics and other systems, believes that China’s move toward open skies at the end of 2013 provides great opportunities for the LCC market. Honeywell is a supplier on the COMAC C919.

I think the large Asian LCC orders for narrow bodies are basically large institutions securing slots to match foreseen growth for the next 10 years. When the frames will exactly be delivered and what airline brand they will end up with is tbd.

http://qf32.files.wordpress.com/2013/09/airbus-world-travel-by-region-2013.jpg

“The long-haul, low-cost model is, with the main exception of Norwegian, unique to Asia. It has prospered on north-south sectors of up to eight hours,”

I don’t consider what Scoot and AirAsiaX are doing “long-haul, low cost”. Living in Singapore, I don’t consider flying to Beijing, Shanghai, Seoul, Tokyo, Delhi, Melbourne and Sydney long-haul. 4 hours to Hongkong is short haul. I consider 6 hours to Tokyo not far. But a lot of these routes are just too much for a narrow body. Long haul in the local definition is 13 hours to Frankfurt, 14 to London and 18+ hours to the US.

Another factor to consider is that Asia is not a unified deregulated market like the EU or US. Someone like Scoot could be restricted to a single slot in a major market like Taipei. Frequency does not work, so you just go wide body.

I think the A330neo and 787 will sell well to in this region because they are perfect for a lot of these routes (LCC or not).

Even in Asia, true “long-haul, low cost” like AirAsiaX and Oasis Hong Kong failed.

I think in most of the world 6h counts as long haul. And as you say, for 6+ hours you need a wide-body aircraft — or an A321neo LR.