Leeham News and Analysis

There's more to real news than a news release.

Airbus, Boeing split YTD orders leads

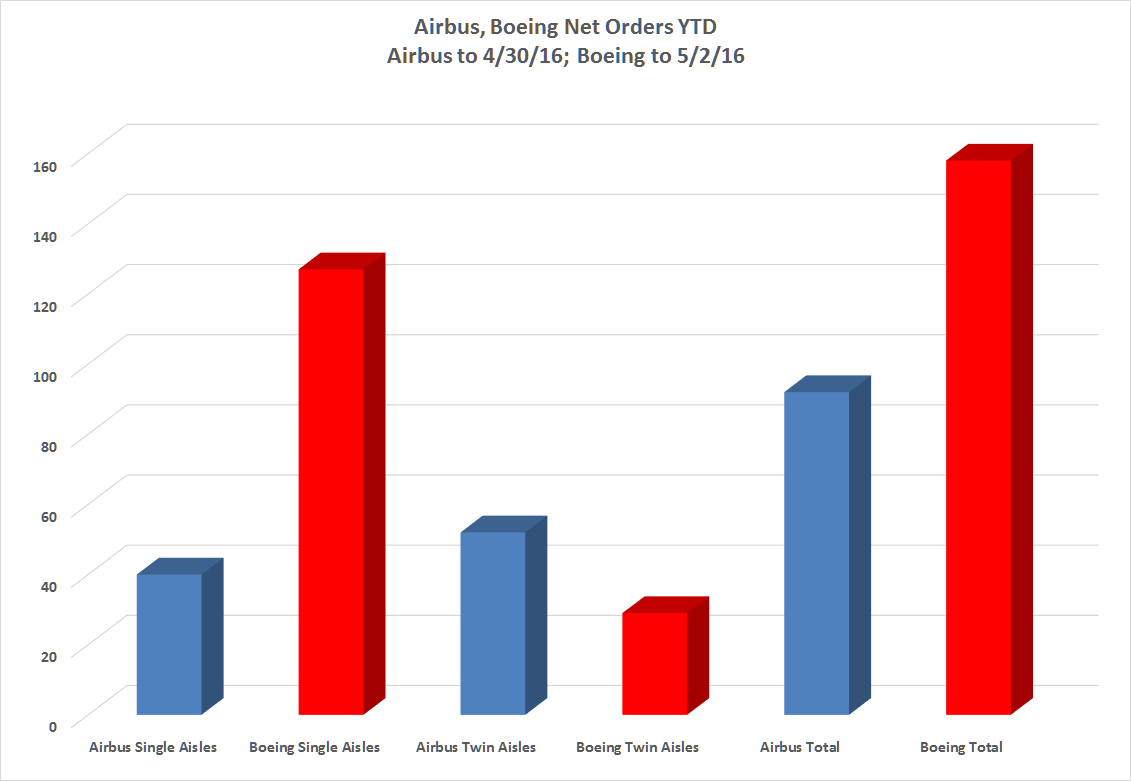

May 10, 2016: Airbus and Boeing split the leads for orders year-to-date through April 30 (May 2), following the monthly total released today by Airbus. Airbus led in wide-body orders by a wide margin. Boeing thumped Airbus in narrow-body orders.

Sources: Airbus, Boeing. Click on image to enlarge.

Through April, Airbus had 52 net orders for the A330 and A350 families. (The A380 netted out to zero after orders and cancellations.) Boeing had 29 net orders for its wide-body family: four 747-8Fs (which were white tails), one 767, and 12 each for the 777 and 787, through May 2. (Airbus reports monthly, Boeing weekly.)

For Airbus, receiving more orders for wide-bodies than narrow-bodies is unusual. It’s also unusual to so widely lead Boeing n wide-body sales.

On the narrow-body sales, Boeing is just cleaning Airbus’ clock YTD.

It’s still early in the year. The leads could easily shift in both categories.

We’re still waiting for Emirates Airlines to decide on a large order between the A350-900 and the 787-10. This order was expected last year, but was put off to this year, probably the fourth quarter–which is when the Dubai Air Show is scheduled.

I know its only a snapshot in time….

But 75 firm CSX00 for Delta, plus 7 firm CS300 for Air Baltic, plus an additional 45 “semi-firm” CSX00 for Air Canada puts BBD at 127 CSeries sold (assuming that AC order does firm up as all parties say it will) – outselling Airbus and Boeing over the first 1/3rd of the year.

Means nothing long term obviously, but who’d have seen that coming at the start of the year!?!

You can’t really compare, as some of these aircraft are so far CS100s that compete with Embraer, not Airbus or Boeing.

The Delta order was indeed announced as a CS100 order, but the reality is that out of the 75 firm aircraft Delta has an obligation to acquire only 35 CS100. The rest of the firm order could be converted at any time to CS300. In addition to this there are 50 options, for a grand total of 125 aircraft. We can therefore say that this is a significant order, one of the largest so far this year. It is true that Bombardier was competing with Embraer for this order, but it was also competing with Boeing and Airbus, because when Delta placed that order they had a larger view that could signal a significant shift in Delta’s strategy that would integrate various models of the C Series in the 110-160 segment. And that might include on the short to medium term the CS100 and CS300, and perhaps later on the CS500 as well. So if we take all this into account it certainly legitimizes the comparison.

What you say is broadly true; the CS100 doesn’t compete against anything from A&B, but the CS300 does. If the CS300 is a shot across the bows of A&B, a CS500* would be a missile aimed right at the bridge.

But if the big two intend to prevent BBD building a beach-head on the mainline market, on the evidence of this quarter, they’ll need to work a little bit harder at it.

*Talking about this elsewhere, conclusion we reached is BBD need to find the cash to stretch the 300 fuselage – as the saying goes, even if they have to beg, borrow or steal the money! Stretch by 4 rows and just keep MTOW the same for now and get the thing in the air ASAP. OK, range is sacrificed in the short term**, but the fuel tank volume is there for release in future MTOW steps – which would be largely a paper exercise which can be ongoing with improved cash position – that cash position ever improving through deliveries of the CS500 and the two smaller siblings.

**P&W talked about 4-5% fuel burn improvement prior to 2020, that’s already pushing range back up never mind increasing MTOW – and would mean current tank volume (which I believe isn’t fully utilised anyway) is sufficient for a ~3000nm range eventually.

“But if the big two intend to prevent BBD building a beach-head on the mainline market, on the evidence of this quarter, they’ll need to work a little bit harder at it.”

In order to have any hope of killing the C Series A&B had to do everything they could to prevent Bombardier from reaping an order like the one they got from Delta. But it’s too late now. I think the C Series is unstoppable at this point. But the road ahead will be long and difficult before the programme becomes profitable.

“P&W talked about 4-5% fuel burn improvement prior to 2020, that’s already pushing range back up never mind increasing MTOW – and would mean current tank volume (which I believe isn’t fully utilised anyway) is sufficient for a ~3000nm range eventually.”

Aerodynamic improvements alone will bring the CS100 to the same level as the current CS300 is. That is from 3100 to 3300 nm (@225 lbs per passenger). And because we are still on this side of EIS it is indeed possible that in the coming years the CS500 could benefit from further improvements and refinements of the CS300 base model in terms of weight, PIPs and aerodynamic refinements that when combined would give the CS500 a 3000 nm range. But right now apparently we can only expect the CS500 to have a range of somewhere between 2500 and 3000 nm. Still, I remain confident that they will be able to achieve 3000 nm in the near future with the existing wing. Of couse the number of additional seats that Bombardier will elect to put in the CS500 will determine what range it will have. But I have the impression more than ever that the market wants a CS500 with a 737-8 capacity even if that will likely limit its range. So BBD will first have to find out what kind of range the airlines would find acceptable, and from there determine what would be the maximum number of seats that would allow this kind of range.

One order does not always translate into success. MDD had a good plane in the MD95, 717 and Airtran made a large first order but only 156 frames were sold. It will take at least two more sizable orders from large carriers to be a success and the price per plane will have to be more than Delta paid.

While I don’t know or anybody else knows what Delta paid per plane, but talk is that it was a deal Delta could not refuse.

“One order does not always translate into success. MDD had a good plane in the MD95, 717 and Airtran made a large first order but only 156 frames were sold.”

The C Series is at the same level in its evolution as the DC-9 was when launched by the Douglas Aircraft Company. If the MD-95 and 717 were not very successful it is because they were end-of-line products. So to be fair to the the C Series you would have to compare it to the DC-9, not its derivatives.

“It will take at least two more sizable orders from large carriers to be a success and the price per plane will have to be more than Delta paid.”

I agree with that statement.

“While I don’t know or anybody else knows what Delta paid per plane, but talk is that it was a deal Delta could not refuse.”

My understanding is that they paid between 25 and 30 million dollars. But that is not really important at this stage, for this was a strategic sale. At the end of WW2 when the Allies were preparing to land in Normandy they knew they were going to loose many men in a short period of time, but that was the price to pay in order to gain access to the European theatre. In a similar fashion the Delta order allowed Bombardier to penetrate deep in the Big Two’s territory.

@Normand

The lower end of this is what you should consider. Left unsaid are MRO concessions for the airplane and the engines, and the benefit for Delta Technic.

I don’t know if it will continue like this for the rest of the year but something strikes me in those orders, especially if we take BBD into account: those OEMs will likely not make very big profits on those sales. In the case of Boeing many of the transactions were fire sales. As for BBD they were below-cost ‘strategic sales’. For Airbus I am not sure, but they are obviously starting to feel the heat at the lower end, and a bit worst at the very top where there might be no heat at all but no interest either and consequently no sales. My feeling is that 2016 could end up being a dull year overall. Except perhaps for Bombardier, which never had a more promising start.

Scott, there’s no Dubai Air Show this year. Next one is November 2017. We have Farnborough in July this year, maybe we’ll hear something then?

@Stealth: It’s tough to keep all the Air Shows straight. My info is that EK won’t be ready until 4Q.

I assume the Iran Air “provisional” is not an order.

http://www.businessinsider.com/airbus-sold-iran-25-billion-airliners-2016-1

Keeje:

I think we can agree its not. Shakiest pending order since Skymark!

I understand Emirates took two the Skymark whitetails.

I think there were two White Tails sans interiors as it became evident that one was going down the drain.

According to other sources Emirates will order about 50 more A380ceo.

This obviously vindicates Boeing strategy of not coming gout with a new single aisle (for a couple of hours anyway)

I recognize the 37 A321 in the graph. Apparently the BOC and Gulfair orders aren’t firm? Neither the ACJ’S.

http://www.airbus.com/newsevents/news-events-single/detail/gulf-air-orders-29-a320neo-family-aircraft/

Surprisingly the PAL A350 order is not included yet.

“We’re still waiting for Emirates Airlines to decide on a large order ”

I think we are also all waiting for that Iran order to get firmed up.

PAL and China Eastern A350s should be included in the graph.

http://www.airbus.com/newsevents/news-events-single/detail/china-eastern-airlines-orders-20-airbus-a350-xwb/

http://www.airbus.com/presscentre/pressreleases/press-release-detail/detail/philippine-airlines-finalises-order-for-the-a350-xwb/

These 4 should lift the A320 orders at least abobe 40 (Incl 37 Delta). And there’s Comlux. Gulfair was signed Jan 21st. Maybe BOC was 2015?

It’s ashame http://www.pdxlight.com/neomax.htm is no longer updated..

If Airbus sells A380s to ANA, EK, BA and Iran Air this year, I won’t be surprised. And maybe even 1 or 2 more from existing customers.

I would be stunned.

Doesn’t ANA have their order in?

Iran has made a big publication of the orders, in depth analysis says they could not handle anything more than a few aircraft a year.

Without delving into the political end, their system is melted down and you don’t start with 150 aircraft, you start with ground service, airports, and slowly work up.

BA has made no noise about needing more A380s.

Iran has 10 airlines operating hundreds of aircraft from a few dozen airports. The 80 million Iranians are not so poor or shy and tourist potential is enormous. The evil image is coming down fast as euros/dollars come in.

http://www.middenoostenreizen.com/files/IRAN/Teheran1.jpg

BA is in a price fight with Airbus as we speak.

http://www.bloomberg.com/news/articles/2016-01-18/iag-could-lease-used-a380s-as-walsh-says-new-aircraft-too-pricey.

Farnborough is in 2 months.