Leeham News and Analysis

There's more to real news than a news release.

Boeing investors day: Smith: becoming a global industrial champion

May 11, 2016: Boeing strives to be a global industrial champion, not just against its peer group, says Greg Smith, the chief financial officer of The Boeing Co. Boeing has a continuing commitment to returning cash to shareholders, repurchasing 150 million shares, he said.

Note: Boeing is holding its annual investors’ day (really a half-day) today, with presentations by: Dennis Muilenburg , Chairman, President and Chief![]() Executive Officer, Greg Smith , Chief Financial Officer and Executive Vice President of Corporate Development & Strategy, Ray Conner , Vice Chairman and Commercial Airplanes President and Chief Executive Officer and Leanne Caret , Executive Vice President and Defense Space & Security President and Chief Executive Officer. We’ll report on the presentations by Muilenburg, Smith and Conner, but not the DSS unit.

Executive Officer, Greg Smith , Chief Financial Officer and Executive Vice President of Corporate Development & Strategy, Ray Conner , Vice Chairman and Commercial Airplanes President and Chief Executive Officer and Leanne Caret , Executive Vice President and Defense Space & Security President and Chief Executive Officer. We’ll report on the presentations by Muilenburg, Smith and Conner, but not the DSS unit.

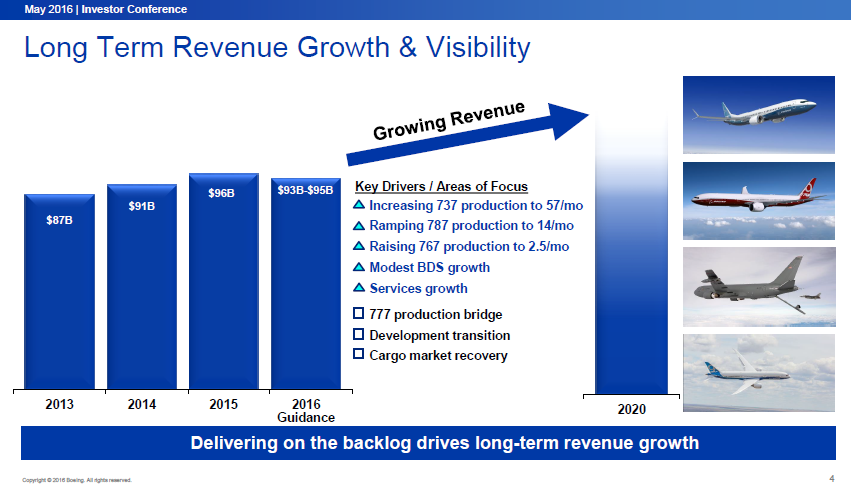

Boeing has had 17 production rate increases in recent year, with five more on the way.

Boeing has had 17 production rate increases in the past six years and plans five more in the coming years. Source: Boeing.

Boeing has 12 orders for the 777 Classic this year, out of a target of 40-50, needed to help build the bridge to the 777X.

“We’re not satisfied with our current segment margins,” Smith said. Boeing achieved a 10% margin last year but wants to grow to the mid-teens in the near future. Cutting costs, improving productivity and achieving favorable pricing on its aircraft and other products are necessary to reach this goal.

Smith said Boeing is working to reduce risk in production, transitioning its pension plans to a less risky structure, achieving labor contract stability through 2022 and transition carefully between current and new products are elements of this focus.

“We expect earnings to grow over the next decade. We expect cash flow to grow at even a faster pace,” he said.

Recovering the 787 deferred production costs will be achieved by shifting to the deliveries of -9s and -10s, and improving pricing for the currently remainging 900+ aircraft in the backlog. This will account for about 70% of the deferred production recovery, Smith said. Ramping production rates and supply chain costs will account for about 25% of the recovery. Cost cutting will account for the rest, he said.

- Boeing’s presentations at the Investors Day may be found here.

Improving pricing for the current remaining 900+ in the backlog. How are they going to do that, if they’ve signed contracts which would state price per plane? Did anyone ask that?

Presumably he means that the pricing offered to customers later in the production queue was not as aggressive as for “launch” customers who have been getting their deliveries early on. In others words most of that improved pricing should already be baked in – if not, he would be delivering materially false information to the markets, which is a big no-no.

What he may not be taking into account is that as a product line ages, one needs to start discounting to keep the line humming – as can be seen with Boeing’s 737-700 order for United and aggressive pricing to fill slots on the 777 line.

By the time the accounting block for the 787 has been delivered T-1000 and GEn 1 will be getting old and it might well need re-engining to compete with an A330 NEO mk II with a 70 klb GTF or new RR. I doubt that the 787 mk 1 will ever recover costs.

The current accounting block will be delivered by early 2022. I feel quite confident saying Airbus won’t be re-re-engining the A330 before then.

In fact, I don’t see anything new coming in the small-medium widebody segment until 2030. That gives Boeing plenty of time to pay back the deferred production, make some profit, and put a new engine on around 2030. And since the Dreamliner engines are already not-quite state of the art, it should be possible to improve fuel efficiency by at least 15% with a new engine by 2030.

I would not be so sure about that. The RR “Advance” will be on the test rack this year and shall enter service in 2020. The “Ultrafan” is planed for 2025. This is putting a lot of pressure on PW to go ahead with their plan for a larger GTF if they still mean to win market share in that category. Which again puts quite some pressure on GE to move beyond the GEnx.

So no, there will not be time until 2030.

Just in case you have missed it, here is a very nice article of what’s going on:

http://aviationweek.com/commercial-aviation/rolls-royce-details-advance-and-ultrafan-test-plan?NL=AW-05&Issue=AW-05_20140825_AW-05_683&YM_RID='email'&YM_MID='mmid'&sfvc4enews=42&cl=article_1

Advance is not that big a deal. Ultrafan? Maybe, but it’s a long way off. And there will probably be something even better than that five years later: that’s just how the engine market is, and it’s a good thing. Any aircraft design is going to have outdated engines 15 years after entry into service — it’s just a question of figuring out what the right timing is to invest the money for a new product.

Anyway, Boeing is the winner in any re-engining scenario, because the 787 has older engine designs than either the A350 or A330neo. Thus, it has more potential gains in fuel savings from a simple re-engine as opposed to a bigger development project.

The Trent-7000 engine on the A330neo is basically a bleed-air version of the significantly upgraded Trent-1000-TEN engine that will enter into service with the 787 in 2017:

http://www.rolls-royce.com/~/media/Files/R/Rolls-Royce/documents/customers/civil-aerospace/Trent-1000-TEN.pdf

@ Adam: You are missing the point here, it is not the question who profits more (787, A350, A330neo almost on the same level) but about the additional cost for the re-engining and its timing. It is easily possible that it will happen in about 10 years from now, with PW pushing for that class and GE and RR defending their position. By then the 787 will not have earned the deferred production cost, which will make the accounting look pretty ugly.

This is pure management double talk, Boeing is already a global industrial champion and as such gains the benefits and brickbats that go with it. Senior management appear to be fixated on the ‘sales message’ rather than giving a ‘balanced and understandable view of their current position and future prospects’. In my view they should be put back in their box by activist investors calling then on the stats in a far more rigorous manner than currently happens.

In summary Boeing is sitting pretty in relation to orders and short-term cash generation but they have difficult transitions to make on their two main cash cows. The one area they really struggle is in articulating what they are intending to do to create shareholder wealth in the medium to long-term. The cost cutting agenda is probably necessary as employee bloating is a constant problem in any company but is not a successful strategy in itself. If there is one issue I have with their product portfolio is that there appears to be little in their design philosophy that is carried from model to model any more. For example 787 to 777x appears to have minimal compatibility in production technique and aircraft architecture (electric vs hydraulic) and the MAX will relatively soon be the only offering out there which is not FBW. And as for future products? Delay and disarray.

This doesn’t stop Boeing being a company that I admire profoundly for the quality of their product but I do question the hand of senior management on strategic direction and vision

Very good comments Bob.

I second that.

Who’s interested in a “balanced and understandable view of their current position and future prospects” ?

– Stock holders ? No, unless it’s positive.

– Boeing executives ? No, unless it’s positive. Most salary is stock related)

– Press / analysts ? No, unless it’s positive.

Some are category 1 themselves & it hurts the above two groups in the wallet. You might not be invited for the next press event.. The home public & advertisers prefer hurray’s too.

It’s a win-win-win.

http://www.fool.com/investing/general/2016/05/08/boeing-co-is-ready-to-soar-the-skeptics-arent-payi.aspx

I don’t think the media and analysts are biased pro-Boeing. Did you see the range of comments following the analyst day (in a different post here on Leeham)? Did you see the WSJ piece that came out yesterday?

Does Boeing tend to sugar-coat things? Yes. And they also have a reputation for freezing out analysts that criticize the company, which is not an ethical policy, in my view. Unfortunately, it’s all too common in the corporate world.

As the author of the article you cited, I would note that I’m not really an “everything’s-perfect!” cheerleader for Boeing, as you imply. Things I’m worried about:

1) How much will Boeing have to compromise on margin to fill out the 777 production bridge?

2) The 777X seems awfully heavy. It makes sense if you need the plane’s full capabilities, but is there enough demand for that segment?

3) How much of a pricing premium can the 787 sustain over the A330neo?

To a much smaller extent, I’m concerned that the MAX 9 isn’t really a match for the A321neo. But MAX 8 demand (and NB demand overall) is strong enough that this is a much smaller worry.

The reason why I come off as so optimistic on Boeing is simply because so many other people — and the stock market — appear to have such a negative view of the company. Boeing is in MUCH better shape than it was 5, 10, or 15 years ago, but gets no credit.

Fun fact I just discovered: In the late 1990s, the total Airbus+Boeing backlog across ALL models was about 3,100 planes. In other words, equivalent to the current backlog for the 737 MAX alone, despite its performance compromises.

@Adam Levine-Weinberg

I’d say that it’s only during the last couple of years that analysts/stock-market etc. have started to take notice that Boeing’s mid- to long-term future outlook may look rather dim. IMJ, things started to change after the 787 was grounded for 4 months in 2013. Before that, to many it seems were caught up in the “drug-like-rush” of the 787 programme. When the 787 was grounded, the promised dream of a revolutionary aircraft and hefty financial returns, started to look more like a nightmare.

I understand Boeing lost an average of $5 million per 787 produced in the first quarter of this year. The mix consisted of mostly -9 models that were sold or renegotiated from -8 models after 2010. So they are already benefiting from enhanced pricing. They are already at 12 planes a month so ramp up will have a diminishing effect on unit cost. First tier suppliers have considerable clout. They are not going to accept losses just so Boeing gets more profits. In other words they can be squeezed a bit, but only so far.

Going forward, the A330 which is being sold on price, will put a ceiling on how much Boeing can up the prices on the 787.

I have no doubt Boeing will sell the rest of the backlog at a profit with the steps with the steps outlined by Greg Smith. But at a cumulative profit of $30 billion?

3 Years ago Boeing stated deferred cost would top slightly above $20 billion and the 787 would become profitable in 2014. Stocks jumped, executives / stockholders cashed.

They have been repeating the “soon profitable” message ever since and get away with it.

Everyone wants to forget, looks forward & Boeing knows. Sharing positive developments that are (predictably) unrealistic & skip the rest doesn’t hurt, contrary..

The difference is that now the Dreamliner actually is cash positive. And if you look at the trend in the deferred balance, the 787 is clearly on track for unit cost profitability by Q3 or Q4.

Most of the orders in the production block are already sold, so pricing is locked in at much better rates than the average of what’s been delivered so far. I have my doubts about Boeing paying off the deferred balance in 1300 units. But if it takes an extra year or two, that’s no big deal. There will still be plenty of years ahead for Boeing to make a profit on the 787.

@Adam Levine-Weinberg

According to the International Institute for Strategic Leadership, the 787 programme will not break even until approximately 2,700 airplanes are built — development costs well in excess of $20 billion, not included.

http://ii-sl.org/ii-sl/Experience___Learning_Curves.html

But not, I think, at much better rates than what was delivered in the first quarter of this year, when Boeing was borderline breaking even. They will certainly squeeze more margin out but the easy wins have already happened IMJ. We will need to see how quickly the unit profit increases in the next year or so.

Another potential worry is how many 787’s they can sell in the next ten years. The book to bill ratio has been quite low in the past couple of years and Boeing are burning through the backlog fast. If they have to reduce production rates at the point where they are producing their most profitable planes, that will affect their ability to pay off the deferred costs.

30 Dreamliners delivered, of which 24 or 80% were -9 models. That’s a higher percentage of -9 models than in the backlog, I expect Boeing will convert a number of 8’s to 9’s. As I say I think the easy win on margins (adjusting the 8/9 mix) has already happened.

Thanks FF

Apologies for misquoting you, a fundamental issue re cost, learning curve and reality