Leeham News and Analysis

There's more to real news than a news release.

Norwegian, from regional to mainline competitor

By Bjorn Fehrm

Introduction

February 8, 2017, ©. Leeham Co: When SAS (Scandinavian Airlines Systems) canceled Norwegian Air Shuttle’s (NAS) contract to feed its Norwegian network 2002, it had no idea the former feeder would almost run it out of business 10 years later.

The cancellation forced NAS to change tack. Subcontracting as a feeder to a mainline was no longer possible; SAS was the only mainline in Norway after buying Braathens (NAS’ original contractor). NAS decided to become a Low Cost Carrier (LCC).

Ten years later, Norwegian (as we call NAS from now) had taken over a large part of SAS’ European business. SAS was fighting for its life. Another five years and Norwegian’s expansion on LCC long-haul is forcing IAG (BA, IBERIA, Air Lingus, Vueling), Air France-KLM and Lufthansa to react.

How strong a threat to other LCCs and the majors’ long haul operation is Norwegian? We will answer the questions in a series of future articles. We start with Norwegian’s roots and its development til now.

Discussion

Norwegian’s journey

Norwegian’s expansion from a regional airline in Norway to a top three European LCC and the leading long haul LCC world-wide is described in Figures 1 and 2.

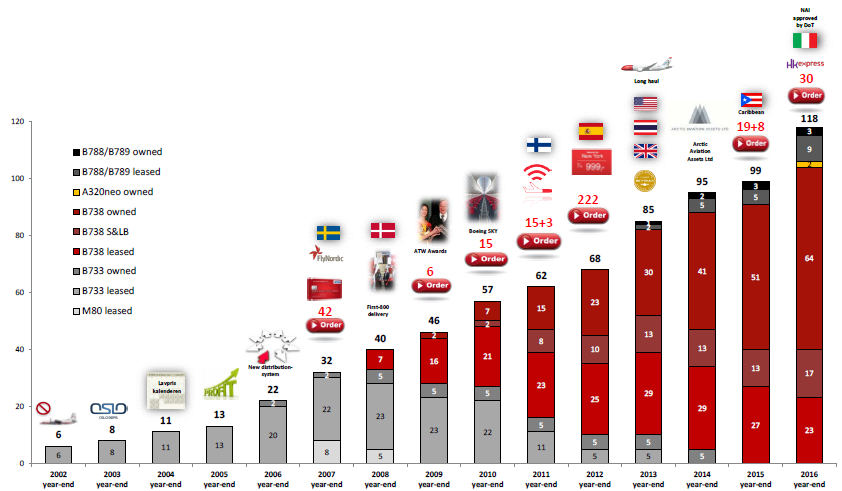

Figure 1 shows the overall fleet expansion from the formation of the LCC from 2002 to the last year’s expansion with Boeing 737-800s and 787s. Norwegian goes from six aircraft to 118 in the time.

Figure 1. Growth of the fleet of Norwegian. Source: NAS.

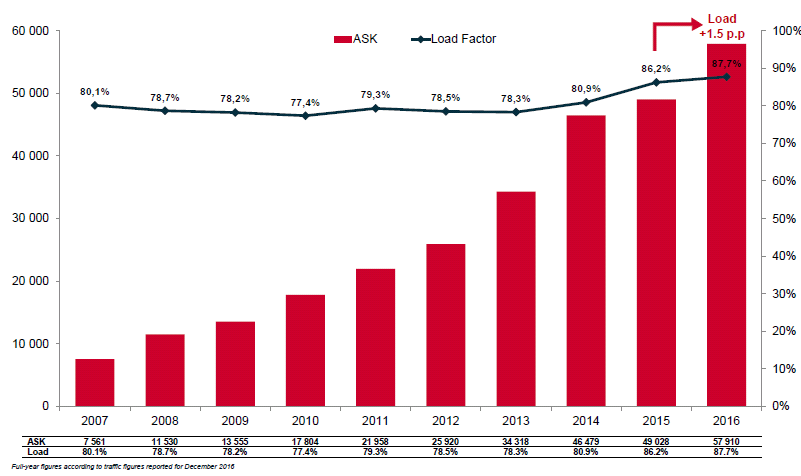

Figure 2 shows the expansion of Available Seat Kilometers (ASK) and the cabin load factor over the last 10 years. The offered passenger capacity has expanded eight times in these years. Load factors of 88% are typical for an LCC but about 3%-5% below the larger easyJet and Ryanair.

Figure 2. Norwegian’s growth in passenger traffic in the last 10 years. Source: NAS.

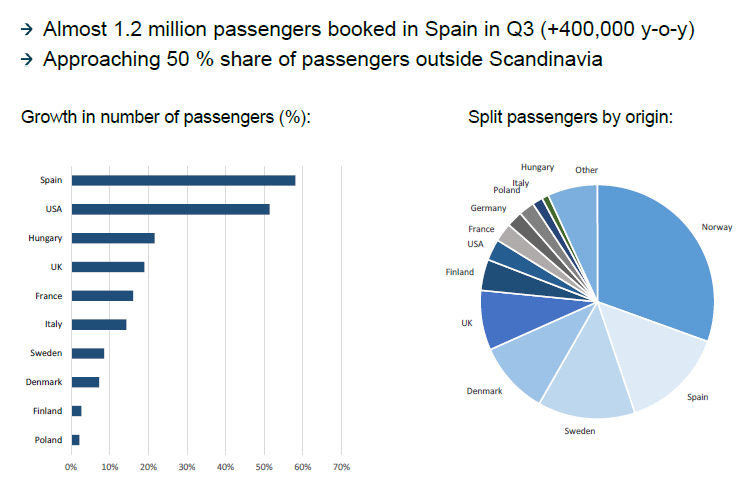

Figure 3 shows where Norwegian’s main markets are (right hand side) and where the growth is focused (left hand side). After a start to bring Scandinavians to more sunny places, the expansion focused on flying tourists to Spain and long haul to USA from Scandinavia, the UK and France in recent years.

Figure 3. Norwegian’s markets and their growth. Source: NAS.

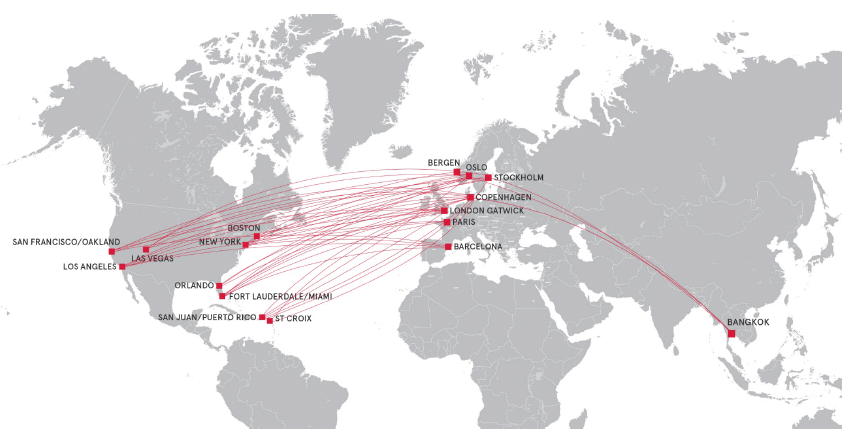

Figure 4 shows the growing long haul network. Focus is US and Caribbean destinations from Scandinavia, London/Gatwick, Paris and, during 2017, Barcelona.

Figure 4. Norwegian’s long haul network 2017. Source: NAS.

Figure 5 gives an understanding of the proportions of the short/mid-haul European network, operated with 737-800 (Red bars), and the long haul network (Orange, Grey and Black bars). Note that the Grey and Black bars contain aircraft with almost double the seating capacity (296 seat 787-8 and 344 seat 787-9) versus the 186 seat 737 MAX 8 and 737-800 fleet.

Figure 5. Fleet development up to end 2018. Source: NAS.

The fast expansion of Norwegian’s long haul made several players in the market take notice. All competing LCCs must decide if they will join Norwegian and launch long-haul operations, or, like Ryanair, feed the Norwegian network.

Legacy carriers must also react. Their long-haul operation is often the profit generator. Carriers like IAG, Air France-KLM and Lufthansa all announced that they will launch competing operations.

Low costs the key

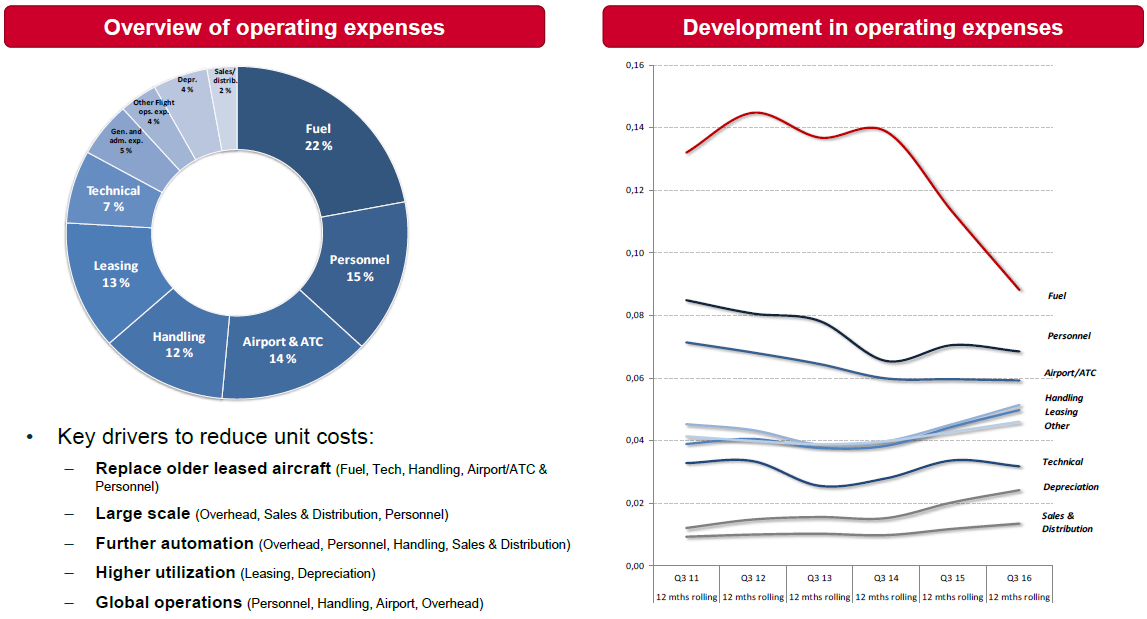

A key metric for an LCC is the cost level. Norwegian’s cost composition and development is shown in Figure 6 and the cost level compared with its competition in Figure 7.

Figure 6. Cost composition and development for Norwegian. Source: NAS.

The Figures show the dramatic shift in fuel costs as proportion of total operating expenses. It also shows how the young expanding fleet has increased depreciation and leasing costs in recent years.

Figure 7 shows Norwegian’s Cost per Available Seat Kilometer (CASK) compared with direct competitors (in NOK. There are 8.25NOK to a US $). Norwegian expects to get the CASK to NOK 0.38-0.39 during 2017. The cost base is competitive, with only Ryanair and Wizz air (which operates east Europe) with a lower cost base.

Figure 7. Norwegian’s operating costs (CASK) compared to competition. Source: NAS.

Rocky start

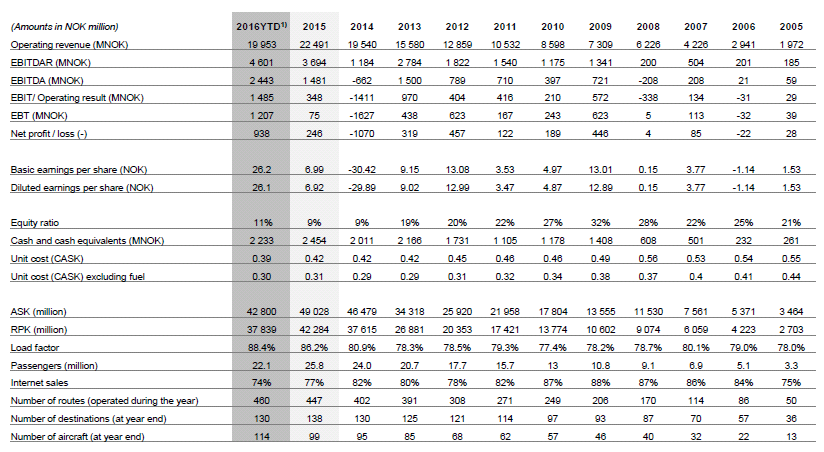

The move to LCC long-haul started badly with several problems with the 787-based fleet during 2013 and 2014. The operating results for 2014 suffered as a result, Figure 8.

Figure 8. Key financials over the last 10 years and Q1-Q3 2016 . Source: NAS.

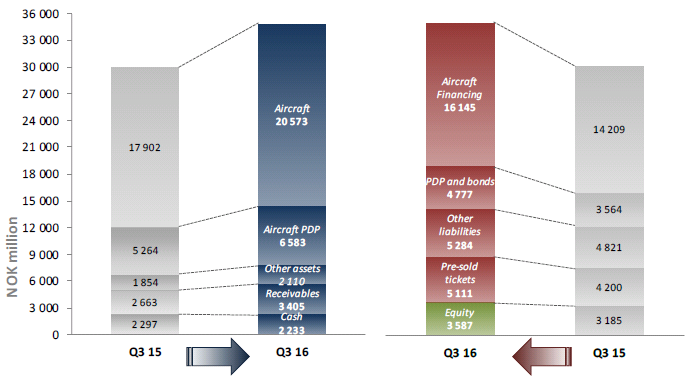

The 2014 losses of 5% of turnover (1070 million NOK) halved the balance sheets equity ratio to 11%, a low ratio. EasyJet’s ratio is close to 50% and Ryanair’s is still higher. Figure 9 shows the composition of the balance sheet in 3Q of 2015 and 2016.

Figure 9. Norwegian’s balance sheet. Source: NAS.

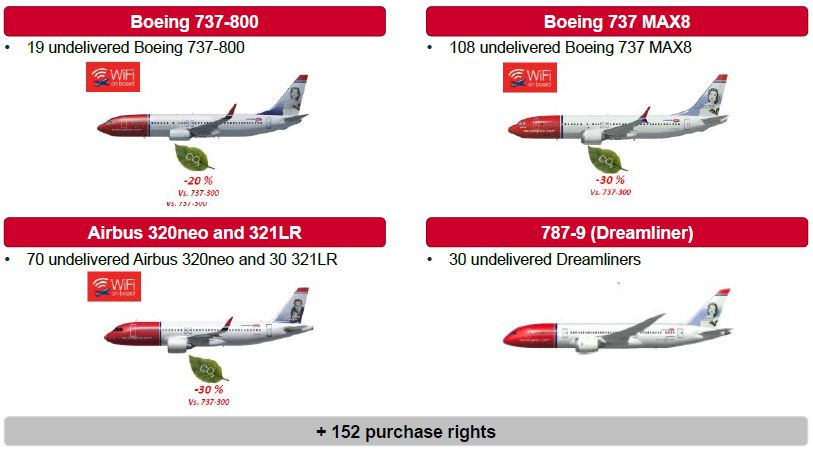

The strength of the balance sheet is a key factor in weathering any headwinds going forward. Norwegian’s large aircraft orders (Figure 10) makes them sensitive to any weakening in the air travel market.

Figure 10. Norwegian’s outstanding orders. Source: NAS.

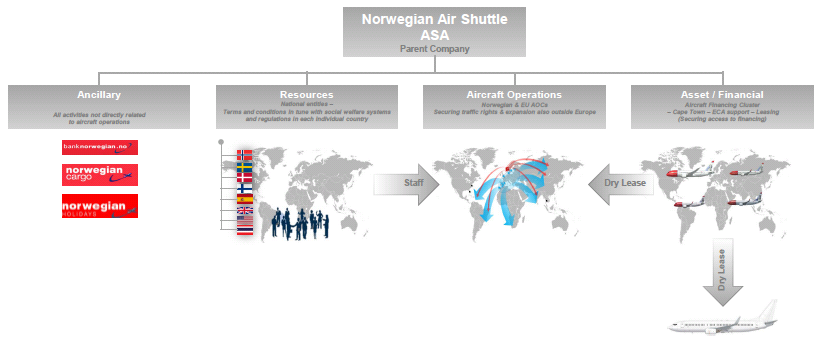

Affiliated lessor

Norwegian is holding the aircraft fleet in a special asset company (Arctic Aviation Assets Ltd) which is leasing the aircraft to Norwegian and other operators, Figure 11.

Figure 11. Norwegian’s outstanding orders. Source: NAS.

The incoming aircraft which are’t needed in Norwegian’s own operations are leased to other operators. All A320neos, the first two which arrived 2016 and a further six in 2017, will be leased to the airline HongKong Express.

While the arrangement cares for excess aircraft in a growing market it does not solve the problem should the market turn. Should the demand for air travel go down, the placement of aircraft with other carriers will be more difficult at a time when its own operation doesn’t need the aircraft.

EXCELLENT WORK, BJORN!

In their ever more resolute quest for operating cost savings, Norwegian is bound to discover, understand and make full use of TAT savings (turn-around time) as the only still available lever to making further progress towards LCC maturity. With root in the feeder service cost split 45/20/35 for hourly/cyclic/fuel and cycles averaging 140’/90’/50′ (Trip/Flight/Turn-around), a 20′ saving in trip time from shortened ground turn-around time induces a trip cost saving of 0.45 x 20/140 = 6.43 % … compare this to savings achieved from better fuel consumption and we find we’d need 0.0643/0.35 = 18.4 % lower trip fuel costs to produce the same effect on trip costs. And anyway, the fuel picture has been corrected with EIS of MAX/NEO ! Conclusion : we anticipate that Kjos’ next step in his quest for better CASK will center upon slicing off another 20 minutes away from his feeder TAT statistics ? And if the solution may combine shorter TAT with boosted revenues from Product Differentiation, boosted payfreight, increased daily productivity, compressed cabin crew roster, more ancillaries, higher IFEC revenues a.s.o. … the strategy decision is straightforward … follow my eyes ?!

Deeper penetration into the U.S. interior (Midwest and Rockies) can be a “growth sustainer” for Norwegian. I can see, for example, Norwegian going into Denver, and really pulling “system” market share from UA for DUB and LON.

Norwegian could conceivably buy second hand A380s and operating them in a 700 seat-plus LCC mass transport configuration between LGW and JFK/LAX/MIA/MCO (etc.) + BKK/DEL (etc.).

Some very interesting numbers there, Bjorn.

More strangeness in the news, as Sean Spicer seems to be implying that purchasing Boeings gives an airline(Norwegian) an advantage when dealing with the US government.

Well, this is what Spicer said:

–

Now, Norwegian is planning to “open up” the US East Coast from Western Europe with the A321LR and US crews (50 percent). It remains to be seen if Trump/Spicer will be happy about that. Perhaps it will be OK if those A321LRs will be delivered from Mobile… 😉

Thats a good point. I think the Mobile plant is going to be much busier under this administration. Hopefully they will build the NEO in Alabama too.

I really wish they’d come to Houston/DFW. I assume load factors for widebodies/transatlantic routes would be necessarily lower than the typical LCC targets. Does WOW air compare similarly in that aspect?

Of serious interest is the “Leaving Arm”

That seems to be where the LCC are going, leasing aircraft they don’t need.

As those leases are at least 5 if not 10 years?

As that space is served, that becomes a pricing war.

It should be interesting when that single aisle bubble bursts.

I’ve read plenty of reassuring words from people who are much better at understanding the numbers than me, but LCCs shifting metal like that is showing all the signs of a familiar pattern to me.

Is it sad to say I follow Norwegian airlines news everyday? My wife and I have fallen in love with Norwegian and their plan to make transatlantic flights affordable for everyone! Thanks for the great article. Being from the US I wasnt sure how Norwegian Airlines had expanded and grown so quickly. Very good info above. Anyone know when they will be selling seats for the new Boeing plans they are expected to get in May? Thanks

Pingback: » Daily Aviation Brief – 14/02/2017