Leeham News and Analysis

There's more to real news than a news release.

Is Norwegian in trouble? Part 2

By Bjorn Fehrm

July 19, 2017, © Leeham Co.: Last week we raised the question if Norwegian Air Shuttle was in trouble. The CFO, Frode Foss, left a few days earlier. Analysts were worried and the stock dived 8%.

Last Friday, the airline presented its 2Q2017 result. An optimistic report. New destinations, increasing revenue and a profit of NOK 861m ($107m). But the stock tanked further, now down 11%. What’s behind the increased worry?

The good stuff

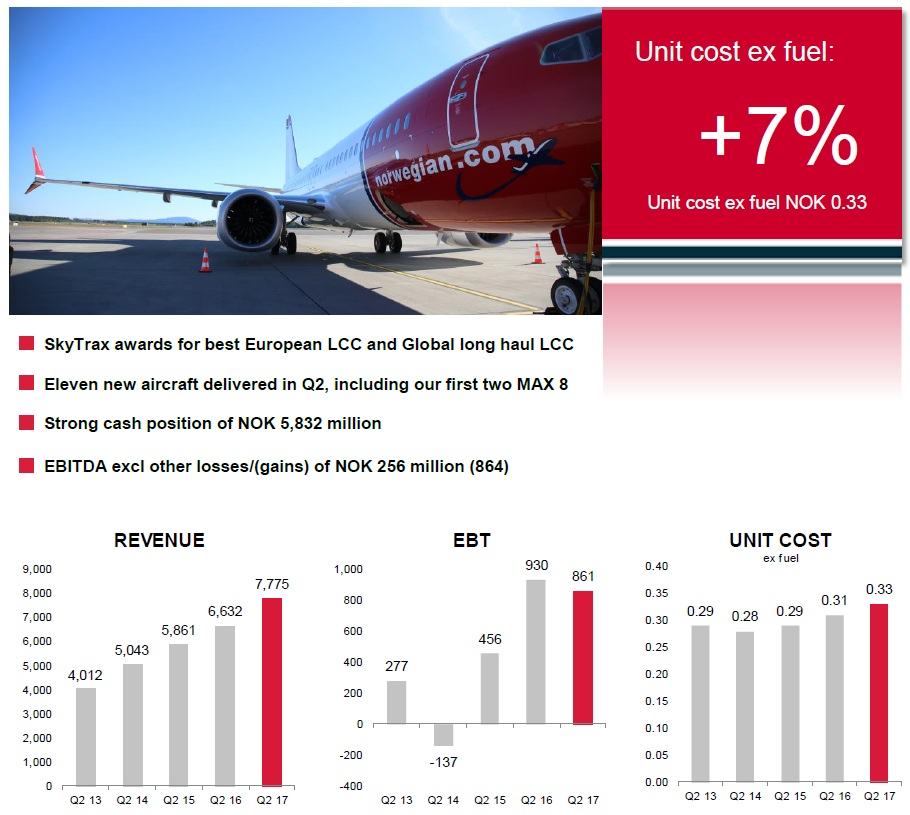

The first page of the 2Q2017 report from Norwegian has several good news items amid a 7% increase in unit costs, Figure 1.

The report describes quality awards received, the delivery of new aircraft (including Boeing’s 737 MAX 8 to fly new transatlantic routes) and more cash than in a longtime. Revenue is up, net profit (EBT, Earnings Before Tax) is healthy and unit cost is only slightly up.

The airline’s headline on the report is: “Norwegian reports a pretax result of 861 million NOK and a high load factor.” All good stuff. So what’s missing?

Figure 1. Summary of 2Q2017 report for Norwegian. Source: Norwegian 2Q2017 report

The missing piece

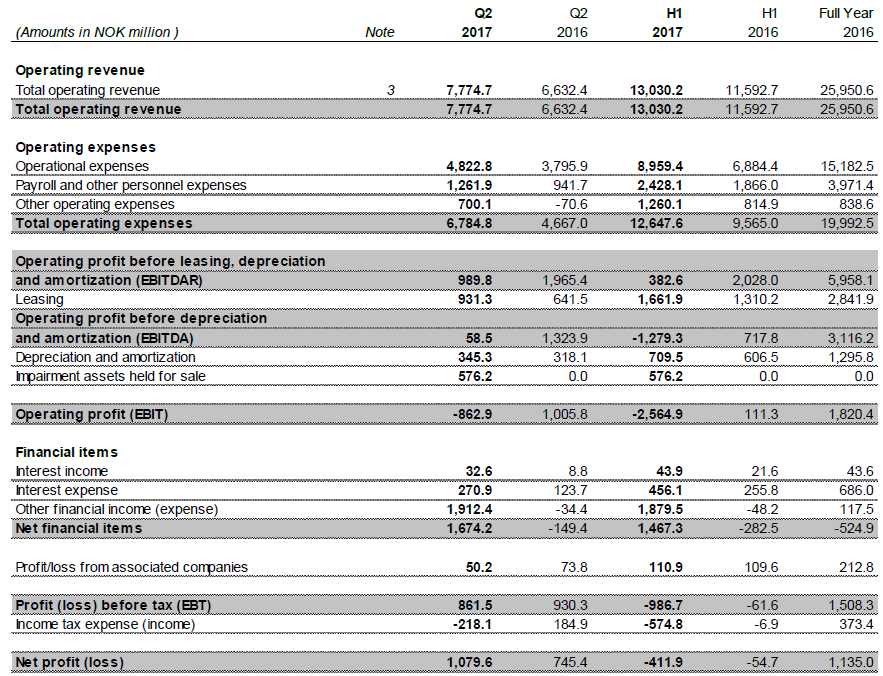

What’s missing is the operating result or EBIT (Earnings Before Interest and Taxes). The operational result for the quarter was NOK -863m, Figure 2.

The Before “I” in EBIT, stands for more than Interest. It represents all capital transactions of the company. The next section in Figure 2 describes what happens as Capital transactions are added.

Figure 2. Norwegian’s detailed 2Q2017 results. Source: Norwegian 2Q2017 report.

The important lines are “Financial items.” Normally this whole part is negative. The costs for financing the company’s operation and fleet is shown here. But now there is an extra line. Other financial income, NOK 1912.4m ($+237m).

Table silver

This is the gain from selling the company’s table silver. In this case, it’s 2.5% of its shares in Norwegian’s external finance company, Bank Norwegian. The bank manages Norwegian’s bonus card program (Norwegian reward) and offers customers and consumers credits. The Bank was listed on the Oslo stock exchange 17 June 2016.

The bank has 900,000 customers and manages five million reward cardholders. Norwegian was the largest shareholder with 20% of shares. This is now reduced by 4.7 million shares valued at NOK 2,047m.

Without the extra cash from sale of the company’s assets, the quarterly result would have been NOK-1,100m ($-137m) and half year results NOK-2949m ($-356m)– substantial loss, clearly worse than the company’s guidance.

Where’s the trouble?

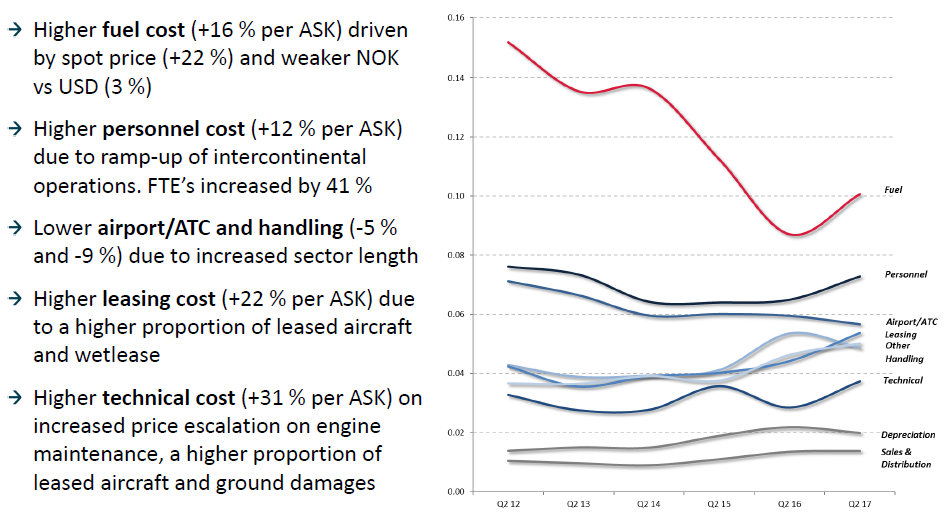

What forces Norwegian to sell assets to save face and keep a good liquidity? The trouble is mounting costs in several areas, Figure 3.

Figure 3. Norwegian’s cost development to 2Q2017. Source: Norwegian 2Q2017 presentation.

Several are natural for a fast expanding airline:

- Fuel costs. This is the same for all airlines and fuel is still cheap. It’s just less cheap than second quarter of 2016.

- Personnel costs. With seven Boeing 787 Dreamliners joining the fleet, the flight crews must be increased fast (25 pilots per aircraft is needed) and in remote places. This is never cheap. But this is nothing unexpected.

- Higher leasing costs. More aircraft are leased today because the weak balance sheet makes owning the ever-increasing fleet difficult. Leasing is costlier than owning aircraft. If your own capital is at 8% of total balance, there is not much choice. Lending you money to buy more aircraft is risky and risk equals cost of aircraft finance.

- Higher technical costs. This is aircraft maintenance costs. Norwegian has returned five leased aircraft during the year. If reserves (especially for engines) for their use have not been deposited in sync with use, then return fees are heavy. Leasing contracts define return conditions. If the aircraft are worn beyond the agreed condition, the lessee (Norwegian) pays. The extra fees end up as maintenance.

So a big portion of the mounting costs are because of costly leases of a larger portion of Norwegian’s fleet. Indirectly, this is the cost of one of the weakest balance sheets of all LCCs. To this shall be added the mounting costs for not having the most recent Airbus A320neo’s at customers, earning their leases.

Together, the costs changes increased operating expenses by 45% (Figure 4) on a revenue increase of 17%.

Figure 4. Operating expenses for Norwegian’s 2Q2017 vs. 2Q2016. Source: Norwegian 2Q2017 results.

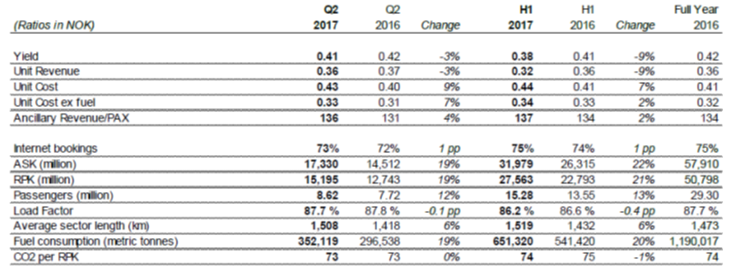

The result of the softening yield (ticket price for sold seat) described in last week’s article and the increasing costs, is a difference between Unit Revenue and Unit Cost of -0.07NOK for the quarter (0.36NOK-0.43NOK in Figure 5).

Norwegian’s first two quarters are weaker than the third and fourth. But it will need good further quarters to avoid selling off more of the silver.

Figure 5. Norwegian traffic figures and ratios. Source: Norwegian’s 2Q2017 report.

In my opinion, the A320neo issue cannot be a major driver of second quarter costs at Norwegian. Should the problems persist beyond Q3, alongside mounting deliveries of the type, my assessment may change. Norwegian themselves mentioned the 787 as a major contributor, but that aircraft type is not mentioned anywhere in this article.

Hi Tsa,

re the A320neo you are correct. But if non acceptance of the lessee drags on it will get expensive. Re what Norwegian says and not. They mentioned the NOK2b cash injection with one sentence in the 2Q report. All analysts I’ve checked missed it . They just saw the quarterly profit. So why should Norwegian point to the real problem in leasing costs?

The 787 leasing costs are planned, therefore they should have been in the Unit Cost guidance Norwegian gave as NOK 0.39-0.40 per ASK. Lease factors (what you pay for your lease) are the lowest since decades so this is not the reason, and the ASK lease costs are not higher for the 787 than the MAX 8 when both are used to their capability.

Like for the real reasons around the result one has to dig a bit deeper to understand the real reasons behind the higher costs. The cost increase is per Available Seat kilometer (ASK) and compared to guidance, not absolute costs.

Agreed with Bjorn 100%. The increasing lease cost re the expanding 787 fleet today is projected/planned/expected quite a while ago.

In contrast, the increasing lease cost re 320Neo fleet today is unexpected mainly because Norwegian didn’t expect lease customers for 320Neo either deferring deliveries or unwilling to lease them in the near term thx to PW1100G tech issues still not completely resolved permanently until nex yr…..it’s very costly for Norwegian to hv even a small fleet of 320Neo today sitting on the ground without generating any leasing income.

I am also aligned with both of you, perhaps it is just the magnitude and timing that we disagree upon. I appreciate the 2bn NOK which was not picked upon by the mass media.

The A320 lease costs may be unexpected, but they don’t explain the magnitude of the loss ($137M in Q2) once the financials are pulled out.

It looks like Norwegian has leveraged itself too much, and is getting hit with the combination of not only A320 leases, but also a dropping yield and increasing costs (operating costs went up far faster than revenues).

Airbus can’t solve Norwegian’s problems, Norwegian must do that itself (maybe with a little help from Airbus).

100% agreed.

And at the end of the day I am lucky to get my Timing Belt changed and the failure prone chain driven oil pump/balance module changed to gear driven (GTF as it were!) .

Is this a sign of things to come?

http://c.newsnow.co.uk/A/894524843?-303:3665:0

And good luck to the A330NEO, dead on arrival?

http://c.newsnow.co.uk/A/894458172?-303:3665:3

@Anton

Saj Ahmad, the “chief analyst” at the one person operation; “Strategic Aero Research”, peddled the same story back in June, 2015:

http://www.postandcourier.com/business/emirates-airline-dangling–airplane-order-in-front-of-boeing/article_f2db8e96-6a07-5be9-8e66-eae36cb062ba.htm

–

It’s interesting to note that Charleston, SC based Post and Courier seems to be a client of Mr. Ahmad. The editors at the Post and Courier probably don’t mind publishing feel good Boeing news stories that are only supported by “insight” from the pompously self-important “chief analyst”.

http://sajahmadfactcheck.blogspot.no/p/who-is-saj-ahmad.html

I agree that Airbus have a slots issue with the A350. Boeing doesn’t have the same issue with the 787. Nothing else in the articles I agree with. Airbus must go to 13/month with the A350 or they will lose hundreds of ssles

Think airlines are starting to loose their sense of humor with Airbus’s production issues.

I think the 787 production issues were much worse, but please feel free to correct me!

I also predict GE won’t deliver on the GE9X. Five and a half years to develop a new engine hasn’t been done before. GENX and the Trent 1000 are the most recent proof of that, they were both very late in meeting specification

Can’t argue that, just a pity Airbus can’t get it right and it could cost them.

I feel that Anton’s hidden agenda is becoming more and more obvious.

“Airbus supporter” my ass.

No offense taken.

My point is that AB should have been building an A350-8xx with smaller and lighter wing as well as potential new centre section an wing box with ~75K-Lb XWB engines to compete with the 787-9.

Now they messing around with the 330NEO that is getting out dated and be “ancient” in 10 years when major A330 replacements start to kick in. An A350-8xx will be good for 20 years to come?

I do mean to offend though.

You’re not what you’re pretending to be. My guess is you’re being paid to throw mud and to spread FUD.

Eish, that’s rough.

@Bernardo, ratchet it back right now. This sort of personal attack violates our Reader Comment rules.

Hamilton

Thanks Scott.

I agree sith Scott. The A330neo is brilliant but not for reasons many will assume. So these are my reasons why its brilliant.

1. They won’t sell more thsn 500, but as the cost is only €2billion they will make a mint out of it. They will therefore replenish the bank balance in preparation for the A320 replacement, another A350 stretch or perhap an Airbus MOM.

2. Bleed Boeing. The 787-9 is a very, very good product. The -8 and -10 are not good products. But Airbus are forcing Boeing to cut margins on the 787-9 making it very, very difficult to recover costs never mind make a profit.

Airbus can make a very good A350-800 to match or beat the 787-9, but Boeing have got the market segment tied up for now. Translated, not much money in it at the moment. Wait for the next generation of carbon and engines, I say!

Thanks Philip. From a business angle very valid an good points.

Just hope they can get to 500.

Sorry, I agree with Scott about invective. The rest of the post is mine, not Scotts. Didn’t realise until I posted!

@Anton

“My point is that AB should have been building an A350-8xx with smaller and lighter wing as well as potential new centre section an wing box with ~75K-Lb XWB engines to compete with the 787-9”

IMJ, Airbus should develop an A350-400 (787-8, A338 replacement), A350-500 (A330-900 replecement) and A350-600 ( 787-10 replcement) -family of aircraft with an EIS, a decade hence. The smaller and lighter wing should have a wing area of up to 20 percent less than than the wing-areas of the A330/787 wings. With a wing span of 64.75m, you’d have a seriously high wing aspect ratio-of about 14. Outfitted with 2 x 55,000 lbf of thrust, RR UltraFan-type engines, MTOW could be reduced to as low as 200 tonnes.

The fact of the matter is that such an undertaking would be seriously premature at this point in time. With a smaller and much slender wing (i.e. significantly more efficient than the same-sized wings on the 787 and A330 and that would be fully optimised for use with a 10-plus more efficient UltraFan engine, an A354, A355 and A356 family would completely blow the current 787 out of the water.

Hence, the A330neo was a pretty smart move by Airbus IMJ — an ultra cheap development that is roughly on par with the 787-8/-9 performance-wise — and if MTOW is increased to some 250-plus metric tonnes (from the current 242 metric tonnes), the payload range capability of the A330-900 would pretty much match that of the 787-9, except for on ultra longe range sectors. With A330neo capital costs significantly lower, I’m not surprised that the folks Seattle is painfully feeling the downward pressure on 787 pricing going forward — all the while knowing that the 787 deferred costs picture is not a pleasant one, to say the least.

Thanks OV-099. Agree with the timing aspect, just hope they are working on it.

On the 330NEO, was the TRENT7000 the right option? The T1000 still seems to have problems.

Was using the XWB-75 with a 6″ inch smaller fan (112″) not an option? It would have given engine commonalities with the A350.

My concern is that airlines seems not to be interested in the 330NEO, some go to the 359 but most of them seems to go to the 787-9.

A 270 seat MoM could kill the 339 for airlines that do not need the range an the extra seat capacity (Delta for example?). It could have an OEW in the order of 40+% less than the 339 and be available in 10 years when “big” 330 replacements are due.

p.s. Think Boeing will start with the smaller (~230 seat?) MoM to support the MAX10 at the lower end as a ~270 seat variant could/will cannibalize 787 orders?

@Anton

The issue with the A350 is slots. To give you evidence

1. American Airlines deferred, the slots were taken up by China Southern Airlines

2 Delta deferred, the slots were taken up by Ethiopian Airlines

3 Vietnam Airlines signed for another 10 last summer. Still not confirmed but that may be because of slots. They may need to lease, if the lessors have any left.

4 China wants another 40. Where they are going to get them from, I don’t know

5 Aeroflot want another 14, where fron I don’t know

6 Lufthansa have said they bought too many 777X and too few A350s

The above is what we know. My view is there are lots more who want A350s and can’t get them.

I will address Qatar and United. Airbus released a very terse response to Al Baker. We will simply reallocate them. United’s deferral suggests they don’t know were their future lies. Thst’s true of Delta and American, for the majors in the USA are under pressure.

This then comes to stretching and shrinking the A350. What’s the point. There are no slots to build them. Airbus must increase production of the A350 to address the market. The same applies to the A320. Otherwise they will lose hundreds of sales to Boeing who do have the production capacity

The A330neo is easy profit and a spoiler. It has already sold over 200, thats enough for a proft, not much, selling 500 would be better

Just hope the A350-1000 is going to do well, for me its near to “perfect”.

The 777-9 could find itself in “no-man’s land” between the 777-300 and 747 size aircraft.

If one needs 25 pilots per aircraft, it seems like there is a good case for economy of scale, and using larger aircraft on routes wherever possible. How much of the transAtlantic market can single aisle aircraft capture, with their higher crew costs per passenger?

That’s why a 220-240 seat (2 class) “797” could change the face of airline business in 1000-5000Nm sectors. Boeing should just bite the bullet and not go “overboard” with high tech and risk.

The long term upside will come, “a leap of faith”?

Stock tanked because of something no one noticed?

Hello Grubbie,

Not to take anything away from Bjorn’s excellent article and analysis, but I doubt that it was the case that no one noticed. To anyone who reviewed the financial report line by line (some people regularly do this rather than taking investment advice from TV Shows or the internet), the change in “Financial Items” from -34.4 in Q2 2016, to +1912.4 in Q2 2017, slaps you in the face, especially if you know that this is normally a negative number. As far as I can tell, mass media coverage of earnings reports often consists of a re-write or condensation of a company press release written by someone who may not know how to review a financial statement line by line, or if they do know how to do so, may not have been allocated the time to closely review the pertinent financial statements by their employer, since they are employed to rapidly generate mass media articles by summarizing and condensing press releases, and not as a financial analyst or investment adviser.

Simple solution: Time to go all “Al Baker” on them. Refuse any more defective neo product deliveries, and sue the pants off AB!

AB needs a serious wake-up call.

Is filling up skies and airports going to slow down the boom of LCC’s? The answer could be larger aircraft such as the MoM.

As said a few few times the future of 180-200 seat single aisle aircraft (A321 size) could be the smaller twin aisle (~220-240 seats?).

http://c.newsnow.co.uk/A/894796745?-303:3665:0

Concerning the “SUPER 358” (slimmer i.e. different wings etc.) – you forgot to mention how much would it cost…. and how many pieces the market is and then will it ever (most probably NOT) recover the development cost…… forget some profit.

Can you write a blog post on why one new plane needs 25 pilots so interesting!