Leeham News and Analysis

There's more to real news than a news release.

Eurowings, Lufthansa Group’s LCC

By Bjorn Fehrm

August 30, 2016, ©. Leeham Co: The European leading legacy carriers are all forming LCC arms. First for short-haul and now for long-haul. For Lufthansa, the LCC operations are gradually consolidated under its Eurowings brand.

The route there has been a roller coaster of airlines and brands. In the end, the regional Eurowings brand became the umbrella under which all Lufthansa Group low cost airlines consolidate.

The checkered history of Eurowings

Eurowings started operations in Germany in 1994, formed from two smaller regional airlines. Its bases were at first Dortmund and Nuremberg. Gradually this changed to Dusseldorf. Lufthansa was a shareholder in the airline since 2001 with 25%, increasing to 49% by 2006. It then also had the right to buy the rest of the shares, with it effectively controlling the airline. By 2011 Eurowings was 100% owned by Lufthansa.

The airline grew over the years and became an important part of Lufthansa regional. Eurowings’ low cost part, Germanwings, was formed into a subsidiary airline in 2002.

In 2008, Lufthansa wanted to merge Eurowings, Germanwings and TUIfly (owned by TUI Travel) into an LCC, to compete with Air Berlin and Ryanair/easyJet. The merger didn’t come about; instead Lufthansa took over Germanwings and developed it as the group’s LCC.

Gradually Lufthansa transferred all European and international flights to Germanwings that did not start from its Frankfurt and Munich hubs. Eurowings, meanwhile, was operated as a regional airline until 2014, when it started to operate flights for Germanwings with its fleet of 23 Bombardier CRJ900s.

Eurowings was developed as a sister LCC to Germanwings during 2015, exchanging the 23 CRJ900s for 23 Airbus A319s and A320s. The regional aircraft and routes were transferred to Lufthansa Regional.

After the Germanwings suicide crash in the French Alps March 2015, Lufthansa transferred all Germanwings flights to the Eurowings brand and closed the Germanwings brand in January 2016.

Eurowings of 2016

Eurowings of 2016 was the merger of Eurowings and Germanwings. The company wet-leased routes, aircraft and crews from an ailing Air Berlin from mid-2016, the more modern Air Berlin A320s replacing the older A320 from Germanwings.

Its European network had 80 destinations which were operated with 60 aircraft from hubs at Düsseldorf, Cologne, Berlin, Hamburg and Vienna.

The long-haul operations were based on breaking out a subsidiary of the Lufthansa-Turkish Airline joint venture, SunExpress, as SunExpress Germany. This airline, established in 2011, is now the operator of Eurowings’ leisure oriented long-haul flights.

The original 11 SunExpress Germany Boeing 737-800s have been complemented with six leased Airbus A330-200s to operate flights to the US, South Africa and Mauritius.

Brussels Airlines merges into Eurowings group during 2017

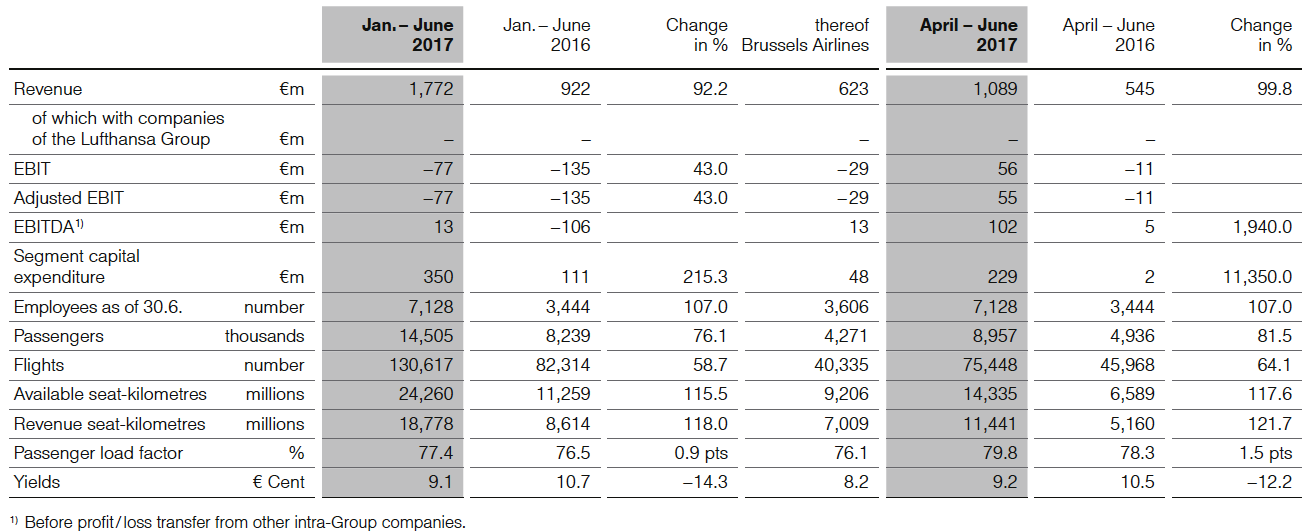

Lufthansa bought the remaining 55% of Brussels Airlines on Jan 7, 2017. The airline, the size of Eurowings, is consolidated into Eurowings financials for 1H2017, Figure 1. It will be operationally integrated into Eurowings, now called Eurowings Group, during 2017.

Figure 1. Eurowings group with Brussels airlines. Source: Lufthansa Group.

Brussels Airlines adds short and long-haul operations to Eurowings Group. In total, the Eurowings Group now serves 192 destinations in 62 countries from its 11 bases in Europe. North American destinations have grown to 10, with more being added.

The non-long-haul part is the dominant part, with 66% of the ASK (Available Seat Kilometers) and 78% of revenue, Figure 2.

Figure 2. Eurowings groups traffic data 1H2017. Source: Lufthansa group.

The combined fleet with Brussels Airlines comprise 160 aircraft, of which 144 are A320 series, 10 A330-200s and six A330-300s.

Lufthansa group’s long-term LCC strategy

Lufthansa calls its low cost segment the Point-to-Point segment and its legacy airlines Network Carriers, Figure 3. Its target is to be number 1 in its home markets, which for LCC means Germany, Austria, Switzerland and Belgium.

Figure 3. Lufthansa group strategy as of 2017. Source: Lufthansa Group.

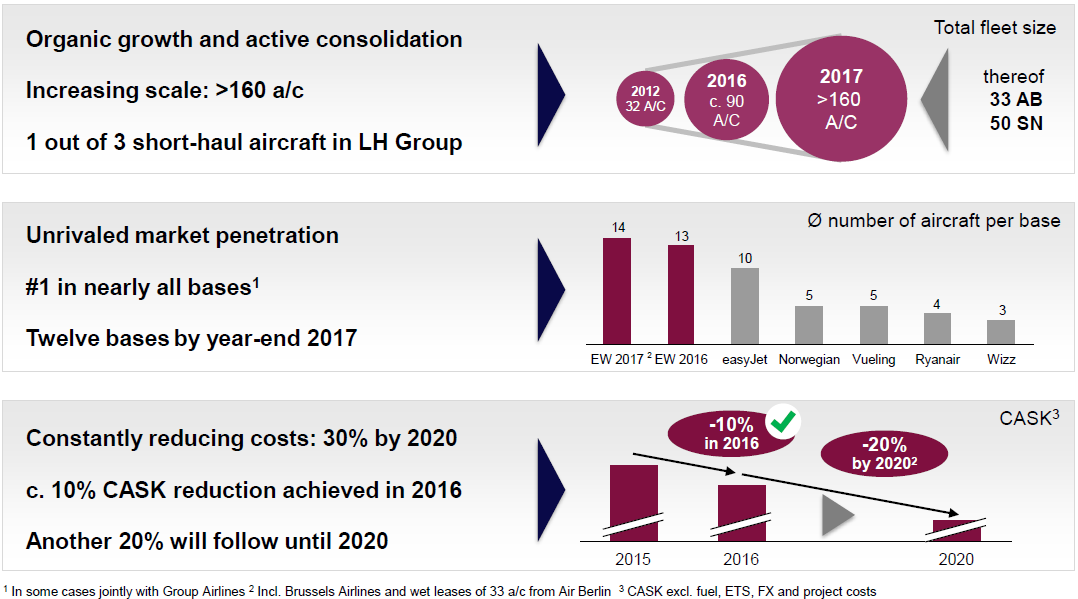

The Eurowings Group will from its Dusseldorf headquarters consolidate all LCC operations of Lufthansa. It integrates the operations of merged airlines first “as is,” with marketing and sales quickly changed to the Eurowings brand.

Then gradually, the operations are integrated and streamlined, to reduce overhead and costs, Figure 4.

Figure 4. Long term LCC strategy for Lufthansa Group. Source: Lufthansa Group.

Brussels Airlines is the new integration for 2017, following the induction of 33 A320 aircraft from Air Berlin from 2016 and the merger of Eurowings and Germanwings started in 2015.

Lufthansa is in negotiations with Air Berlin’s bankruptcy management to add further parts of Air Berlin to Eurowings, beyond the 33 wet leased aircraft and crews.

The Lufthansa Group has never really had a competitive LCC airline as they constantly transfer high cost operations to the LCC brand. So technically speaking, they have never really had a LCC airline. Germanwings never made money and I don’t see how Eurowings will ever make money either with Lufthansa constantly dumping high costs onto its balance sheets.

Is that done for tax reasons ? Is there a double Dutch sandwich or similar as its called for companies that use Netherlands/Luxembourg/Ireland as tax havens

Thanks Bjorn, will have to read this a few times to fully memorize the layout of things.

LLC competition on the Transatlantic is surely going to increase. For me there is however a void for medium-long haul LCC’s from Europe to Asia, sectors generally 3500-5000Nm.

Are these to long routes for LCC’s, pax comfort and they will require more expensive twin-aisles and/or are the ME-airlines to strong in that area?

The “797” (MoM) could however be an interesting future option for LCC’s from Europe to Asia?

I doubt medium-long haul could work in the Asian direction for anything below the B787/A350 aircraft. There are a lot more countries to fly over than the Atlantic and you need more seats to make it viable and to offer walk-in fares like we see on the Atlantic.

Had a similar “feeling”, the India-Europe market is potential lucrative but think Qatar has its eye on that one.

It’s possible more likely to see Asian LCC’s such as AirAsia-X feeding into European LCC airlines hubs? (On the other side Berlin, is “only” 4500Nm from Beijing).

With the US North-East coast under attack from LCC’s single-aisles the potential for airlines such as Eurowings with twin aisles are destinations that’s not in reach of the single aisles?

Shocked EU regulators have not stepped in, any time BA does anything they are on it like Trump at a beauty pageant.

Let have a Posting on the Houston Flood? I have been surprised at Leeham no mention at all.

I know its not Aviation beyond SW and United but its relevant.

And add in any thoughts or prayers to the victims of all this, pushing the comprehension limits severely.

LH’s strategy here is everything it appears to have been; a hot mess. It may not make sense right this second, or maybe it does, but it will be totally different in 6-18 months so it doesn’t make much of a difference.

Using CRJ900’s for a LCC arm is about as irrational as it could get, but they managed to one up themselves eventually, and once some Air Berlin assets are gobbled up into some quasi-integrated piece of Eurowings I bet it’s even more of a mess again. I don’t know where a German competitor to the Chinese/ME3 to asia competition would fit in as an LCC, but I bet LH tries a few different strategies eventually.

German immigration and economic vitality seem to indicate a disproportionately growing international air travel market though, I would think, relative to the rest of the EU.

To add to the current confusion/turmoil O’Leary says Ryanair are interested the Alitalia fleet, approximately 90 Airbuses (including 14 x A330-200’s) and 12 Boeing 777’s?

In figure 4, costs are to reduced by 30% by 2020. From my non aviation industry background, how is this achieved? Is it labour costs, or just a little bit of cost cutting every where?

Slightly cheaper fuel as part of Lufthansa,

Reducing airport costs?

And so on?

Seems LLC are trying to get their hands on A330-200’s for longer haul routes. The A330-800 is most likely not favoured due to its higher price while the 330-900 is to big and expensive?

Still believe Airbus could have a niche with an A330-200 Advanced/Enhanced with the NEO’s improvements but with CEO’s and low price.