Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Balance shareholder value with product development and strategy

April 26, 2021 © Leeham News: Balance shareholder value with the long-term strategy of The Boeing Co.

By Scott Hamilton

This is what Boeing needs to do. But there were conflicting signals from the 2020 annual shareholders meeting held April 20 via virtual webcast and dial-in participation.

“We want to get back to a dividend policy. I can’t give you a date and we need a return in our commercial aviation department to support that.” So said David Calhoun, CEO.

Yet Calhoun was circumspect about a new airplane program.

When asked about developing a new airplane, Calhoun said—as he has before—that Boeing’s current research and development focus is on refining engineering modeling and production methods. These will be the “real differentiators” for the next new airplane.

“Calhoun vowed to return Boeing to its engineering roots,” reported Bloomberg News.

History favors shareholders

Boeing’s history during nearly the last quarter century favors shareholder value over airplane development.

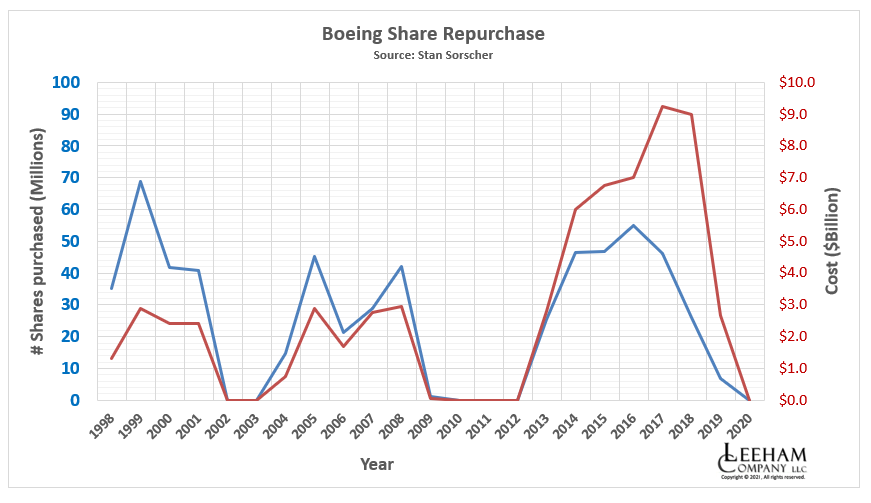

Dividends. Stock buybacks. Shareholder value. This has been the mantra since the 1997 McDonnell Douglas merger that, in retrospect, dramatically changed Boeing for the worse.

From 1998, the year after the merger was effective, through suspension of the share repurchases in 2020, Boeing spent $63.5bn. This is, at today’s costs, equivalent of about four widebody and 5-6 narrowbody programs. Dividends paid are in addition of this figure.

Nobody I know suggests that Boeing’s executives and Board of Directors not boost shareholder value via stock buybacks or dividend payouts. However, the Board had a policy of returning nearly 100% of free cash flow to shareholders. Certainly 50% of this could have gone to new airplane development.

There is a conundrum of launching a new or derivative airplane program, to be sure. But Boeing fiddled over the Middle of the Market Airplane from 2012, when a replacement for the 757 was first discussed, to January 2020, when Calhoun killed the New Midmarket Airplane.

In the meantime, Airbus took advantage of the weakness of the MAX 9 and later the MAX 10 lines by step-change improvements to the A321neo to develop the A321LR and A321XLR.

The A321neo outsells the MAX 9/10 by about 4:1, depending on the measuring point.

Boeing’s status quo is a spiral into oblivion

While Wall Street analysts fret about the dividend, shareholder value and profits (even before the MAX grounding and COVID pandemic), Boeing’s strategy of maintaining the status quo is a spiral into oblivion.

“We struggle to see how the business case for a new airplane closes favorably these days, especially when the eventual cannibalization of 737 profits is considered,” Melius Research wrote April 21, the day after the AGM.

“Any launch below 220 seats would cannibalize the MAX at a time when Boeing needs the cash from the MAX, especially since a new launch would likely cost more than $15bn,” Bernstein Research wrote in an April 22 note.

These are typical Wall Street views. Today’s profits at the cost of the future of the company. It’s the McDonnell Douglas approach of the 1990s. We know what happened to MDC as it fiddled while Airbus grew. By the time Boeing and MDC agreed in 1996 to merge, MDC was down to a pitiful 7% global market share.

I wrote in February: The Future is a New Airplane, Not Status Quo.

The MAX 9 and MAX 10 were the wrong airplanes when conceived and they are the wrong airplanes today. Period. Boeing doesn’t break out the MAX sub-type orders, but based on some known numbers and extrapolating them to variants TBD, LNA estimates the current sub-type market share. The conclusion is consistent with market data previously confirmed by Boeing shortly after the launch of the MAX 10 in 2017.

Boeing needs to move forward. The status quo, followed by McDonnell Douglas, is just plane wrong. (Pun intended.)

Next Boeing Airplane

Wall Street analysts fret about the Next Boeing Airplane (NBA) (whatever it is, single- or twin-aisle) cannibalizing the MAX 9/10. The MAX 9 is now the proverbial pimple. The MAX 10 has an estimated 15% share of Boeing’s MAX backlog, but the airplane isn’t certified, it hasn’t begun flight testing and new certification requirements were imposed because of the Lion Air and Ethiopian crisis. Entry into service is now targeted for 2023.

LNA sees 2023 as the year Boeing must launch a new airplane program if it is to enter service by 2030. Some analysts suggest the next step change in aircraft development will be by 2035.

Well, yes and no.

Electrically-powered airplanes and hydrogen-fueled airplanes may well have real potential by then—but not necessarily on the missions for which the MAX 9/10, A321neo and NMA/NBA will serve. A fully sustainable aviation fuel approach by the 2030 decade for these airplanes is more likely. Boeing already plans to have 100% SAF-capable airplanes across the fleet by 2030. Airbus will match.

Boeing must balance shareholder value with product commitment and product strategy if it wants to stay as a member of the Duopoly. Otherwise, “McBoeing” is its future.

Related article:

Boeing has a history of making (huge) net loses on (all) its recent programs; so, if we extend that trend to a new program, then such a program only becomes a strain on finances, thus reducing what could otherwise be distributed to shareholders. Hardly surprising, therefore, that Calhoun isn’t too enthusiastic about the idea — it would interfere too much with his desire to return to dividend payment.

If a relatively straightforward “re-hash” like the MAX turned into a dog’s dinner with $20B losses and a decimated order book, and the clean-sheet 787 is just off out of months-long “open heart surgery” on a stalled production line after its second grounding and a program loss of $32B, what hope is there that a new program will ever generate profit? In the recent LNA discussion with Richard Aboulafia, we learned that engineering staff levels at BA have been cut by 25% — so the chances of producing a reliable plane have gone down even further compared to past programs.

@Bryce

You know (sigh) there is a way for Boeing to get out of this. Problem is – it requires everyone to put on their big boy pants and let the adults in the room make the tough decisions.

BA spent $43 billion on share buybacks since 2013, when shares were around $100. I haven’t checked the average price they spent on all those shares, but I’m guessing they could get around $30 billion for them, maybe more.

That would go a long way to giving them a chance to do a reset and fix their problems, without raising debt servicing costs.

It makes me wonder; with the recent departure of the CFO, was their a voice(s) that proposed just such a solution? Was (is there) a faction in the company who is advocating for just this type of medicine?

You know there is a percentage of decision makers who are quite happy for the company to limp along from crisis to crisis, as long as they get paid with a waiting golden parachute when things get too bad.

Is there a camp in there who wants to do what it takes to make things right?

I think Smith was as bad and maybe worse than Calhoun.

You can count on bean counters never to change their stripes. There is a reason they are bean counters. Teaching an elephant to play the piano would be a high possibility vs a bean counter changing to thoughtful.

That is why when Scott etc talk about Calhoun being transformative its not going to happen. The Zebra can’t change its stripes either.

As for bought back shares, that (in theory) takes the stock price down and that is not going to happen. Management lucre is based on shares and it would kill them to see a single penny lost to them.

note: That is the same lucre package that gets you tens millions when you get fired like Mullenberg etc.

@Trans

I can’t really disagree with anything you’ve said here. So is there no eureka moment, once they see the hopelessness of the situation to say:

All hands to the pumps

Desperate times call for desperate measures

A drowning man grabs even for the point of a sword

and do what is necessary?

Or are they just going to ride it all the way down?

Disagree! TW

Some accountants are big picture thinkers, in tune with the whole enterprise.

I have worked with a couple, one old one young – and with some stupids. Yes, a minority – but many engineers are not sharp. Decades ago the saying ‘Lazy B’ described them, not hard workers. OTOH some sharp people, like Dick Peale and Harty Stoll on the 767 program – they had perspective (high level managers with decades of experience. The 787 program had some twits who should have been turfed, some good experienced engineers who had to be reminded of the big picture some times, some dedicated experienced managers, and some devious managers.

Leadership challenge is to enunciate principles and the big picture, and ‘coach’ those who stray.

Do remember that someone has to watch the money and ensure the company stays solvent.

(And this forum has the same variety as the 787 program did. I miss Rob.)

I agree entirely with your sentiments, it reflects my own experience.

In any tech company there is often a tendancy for engineers, accountants, sales/marketing etc. to loose sight of what each other needs to balance, to make the enterprise function as a whole.

The trick is to get the various disciplines to understand the basics of each others constraints, so they can work together, towards the shared goal. This inevitably requires some degree of compromise on all sides.

That said, I don’t think there is any fundamental conflict between the roles of engineering, finance and management. Engineering is after all the process of working out how to deliver the requirement using the minimum resources, be that weight, materials, fuel or work hours etc. The issue, is where to best draw the lines, between financial, product & manufacturing efficiencies (i.e. investments Vs operational costs)

An optimal balance of these can only be established, by complex iterative study of markets Vs technological & operational possibly Vs costs & available finance. This requires engineering, finance, sales/marketing and management to work very closely together, not against each other.

Culturally, I think AB have a distinct advantage here – the organisation having been founded on international collaboration; everyone in AB has to learn to rub along with many people with different outlooks and agendas.

@Keith Sketchley

@Rob retailed the corporate point of view, somewhat distinct from most comments on this site

This was interesting up to a point only –

– corporate comments lack attribution and are, as the planes, derivative copies one of the other intended to hide more than reveal (ditto BA dealings with FAA/WS)

– tedious when expressing the current corporate attribution of any difference & dissidence to deviant conspiracy theories

@Sonik

Unfortunately BA’s bean counters are not good with numbers.

See my post at bottom.

Boeing management is very good with numbers, numbers are a tool.

If you use the tool to get your lucre and gut the company future, then the numbers are spot on for that purpose .

Its been highly successful, strangling the golden goose until its dead. But as long as management gets theirs they don’t care.

To make a company successful long term you have to address several key fields. In order of their importance:

1) Happy customers

2) Happy crew

3) Unhappy competition

4) Happy shareholders and banks

Boeing has got this completely the wrong way round, and as they apparently don’t have and intention of putting it right again, they will fail.

When you mentioned delivering 100% of free cash flow back to shareholders, you stated that some of the cash could go to product development. My understanding is that cash R&D spend is taken out before you get to free cash flow. The meaning of free cash flow is that it is a post-reinvestment in the business figure, so you cannot allocate free cash to product development, because product development would be considered reinvestment in the business.

I think you’re right that there hasn’t been enough cash allocated to product development, I just am not sure if you’re looking at the right metric.

But that is the rub. Sure, some of that pre-free cash flow revenue gets allocated to R & D, but Boeing’s own numbers indicate pre-pandemic most of their spending in this bucket was on derivatives and investment in current production programs. If Boeing were serious about long term sustainability in the marketplace they would have higher allocation of free cash flow into R & D since this would indicate they want to actually reinvest into their company.

@Burk: Left pocket, right pocket.

@Burk

There is R&D spending (Hey! Look at the nice design the engineering boys came up with! Color prints, too!) and then there is an aircraft launch (OK, send $500 million to Spirit for the first 10 fuselages. Send $100 million to Collins for the avionics. Wire $750 million to the tooling people, so we can set that up in the building #5).

It’s all smoke and mirrors, until you gotta scratch a check.

@Burk

BA’s “FCF” in recent years is inflated by “PFS” (more like “Pilfering from Suppliers” in substance): extending payment terms from 30 days to up to 120 days. Not real free cash flow in traditional sense.

Boeing has a long history of calling future trends right – much more so than the competition – but seem to have now lost the willingness to take the risks necessary to convert that vision into a competitive product set.

Where did it all go wrong? It seems to me that 787 was the tipping point. But despite the obvious failure of execution, it was still the right airplane at the right time.

It’s very odd that having called several

emerging trends right, BA seem to have snatched defeat from the jaws of victory.

Meanwhile most all of AB recent program successes – A350, A32xNeo, A220 – seem to have been rather more reactive and opportunistic.

Sonik, this is really a funny way at looking at the past generation of planes. Since Airbus invented the widebody twin-engine airliner (A300) and thus started a megatrend, Boeing has been on the back foot most of the time. The next huge innovation and trendsetter was the A320 as the first FBW airliner. Airbus was also very early in the application of composites: The vertical stabilizer of the A310 was the first major carbon fiber component in an airliner.

So no, for the last 25 years Boeing did not call the future trends better than Airbus.

I don’t disagree; it depends how far back you go – I wasn’t specifically refering to Airbus when I said “the competition”.

One could equally argue that Airbus owes its very existence, to the inability of Europe to compete with the US industry earlier.

Europe has also had its fair share of spectacular commercialy failed projects, but those were mostly due to hubris and national pride. Concord and A380 being notable examples.

But I think it’s fair to say that Airbus has done a much better job of using the experience gained from those – both good and bad – and feeding the lessons learned into subsequent programs.

Boeing should take note.

I don’t think the A380 was a failure due to hubris and national pride. After all, Boeing also tried to make a 747-8.

The market for TATL travel was very much of the hub and spoke model, with much slot congestion at airports like JFK, LHR, CDG et al. The thinking was a bigger aircraft would cut down on the number of flights needed to supply the demand. Take a look at Emirates – they were one of the only ones asking for an A380Neo, using the hub and spoke model (pre-covid).

Then airlines started flying long and thin, city pair routes with cheaper aircraft and less connections for pax. The paradigm shifted. Kinda like it has for the 777X.

Congestion was/is a genuine issue, but it seems it’s not a problem in enough places, to generate a viable market for VLA.

VLA relies on high load factor to be economic. So it doesn’t take much displaced demand to put a dent the hub and spoke business model.

This goes back to my original point – Boeing correctly foresaw the long haul fragmentation coming it’s why they built the 787. But 777x is really just a knee jerk response because A350 (itself built in response to 787) displaced the original 777.

That’s what I find ironic – BA originally called the market right with 787, which despite the various issues has sold well, and AB called it wrong with A380 which wasn’t viable.

But the two now end up with their original positions reversed, at the larger end of the WB market. Neither side planned it that way, it’s just how it’s all played out.

Gundolf:

Airbus did not develop the wide body, Boeing did.

Nice trying to split that hair.

Airbus came out with two engines widebody vs 3 (you also should be advised that the FAA would not allow 2). Airbus sold the A300 into the Asian market that did not adhere to ETOPS requirement for 3 engines. I flew one back in the day and no, I was not happy.

Boeing in those days was not stupid. Airbus was then able to leverage the two engine ops into increasingly longer ranges.

Boeing in turn flipped Airbus on its back with the 767 (careful when y9ou re-write history, some of us old farts lived it and remember it)

You forget that Airbus was the one that reverted to the 4 Engine (count em) A340.

The A330 was successful response to the 767.

In turn, Boeing came out with the very successful 777.

The 787 is very successful as well, no question Boeing tried to cripple it with Management screw ups.

The market research for the slot is still spot on and Airbus has not actually competed with it (other than the horror of horrors, a DERIVATIVE (attempt to compete)

Is that the Boeing of today? No. But how about not trying to re-write history to conform to your bias?

Boeing has a huge amount of legitimate criticism, Airbus does not walk on water as we have seen with the ego driven A380, the A340 and the A400 (which was developed under Airbus commercial not Airbus military by the way)

Airbus got both the A340 wrong and the A380 . They were valid choices for the time they were developed but wrong choices were made AFTER they went into service.

The later A340 bigger derivative with new engines and expanded wing area wasnt the right choice when a much heavier A330 longer range would have been. ( and earlier than they eventually did go)

An A380 neo with 12% SFC improvement might have gone towards keeping it production – but the over complicated delivery of prebuilt sections and maybe a guarantee on used values for existing model meant there was no more money or such a risker venture.

@Sonik

…and the 747-8 was?

Transworld a couple of misses there.

The A300 came out way ahead of the B767 -Oct 72 compared to Sept 81. The short fuselage A310 was the 767 competitor. And a close to fit to ‘NMA requirements’ with 200-230 seats and 5000nm range.

The A330 effectively ended the 767 when it came out in 1992, ahead of the 777 which was Boeings answer to DC-10.

ICAO rules allowed a bit longer range than ETOPS and FAA changed them when it suited Boeing ER series.

And no The A400 was Airbus Military plane , the issues were primarily with the engines – not made by Airbus , but they foolishly became lead contractor for.

Duke,

they were not misses.

The 767 was in response to the A300.

The A310 was a counter that was not successful.

The A330 was a sort of counter but moved it up a class that turned out to be a popular area (made more so by the 787 failures and subsequent delays)

767-400 was the attempted counter to the A330 that failed.

The first major certificated composite primary structure actually was conducted by Boeing with the 737 Horizontal Stabilizer under the NASA ACEE (Aircraft Energy Efficiency) program. The stabilizer was certificated in 1982. Five (5) shipsets were installed with deliveries to MarkAir and Delta airlines in 1984. One of the shipsets was damaged after six years in-service in non-fatality crash on approach to Unalakleet Alaska. The longest in-service stabilizer was at least 18 years, although I have not confirmed that number. The program was instrumental in establishing the path to certification for composite primary structure, which the Beech Lear Fan and Airbus A320 benefited from.

Huh?

Boeing invented he high capacity long range airliner, called the 747.

Boeing developed the 757 and 767 almost simultaneously, providing a middle capacity airliner in choice of narrow or wide fuselage (which could serve as a 707 replacement).

Boeing developed the 777 and improved it.

Airbus spent on the A340, smartly using same wing structure as A330, same fuselage of course, I suppose a modest success with 377 delivered., but being retired earlier than expected. (Compared to 561 of A300 and over 1500 of A330.)

Boeing’s customers wanted improved 737s for fleet commonality, I repeat that SWA was not forward thinking on that.

Airbus spent big on the A380, which did not sell well. Boeing improved the 747 but that did not sell well, too little change on an awkward fuselage configuration. (Configured as a freighter with second deck to facilitate nose loading, the arrangement was the losing bid for what Lockheed won with the C-5, sales of nose loading commercial freighter were disappointing. Apparently Boeing looked ahead to converting some 747 airliners to cargo. But the side cargo door does facilitate much cargo loading.).

Pontificators need to keep perspective, many in this forum do not want to IMJ.

> Since Airbus invented the widebody twin-engine airliner (A300) and thus started a megatrend <

Please point to the part of that statement that's incorrect. Thank you!

I think maybe we are talking cross purposes here.

BA did invent the long range WB category with the 747.

AB did also invent the widebody twin category with the A300, but it was originally conceived as a short haul concept. Hence the name “Airbus”. As TW pointed out the A300 then steadily evolved into a long haul airliner as deregulation allowed.

This wasn’t something AB originally predicted (as evidenced by their later A340), it just happened. The distinction therefore being intent, since the thread from OP is about AB vs BA calling the market right.

So both viewpoints are perfectly valid, depending on the context, IMO.

Irrelevant, you quote out of context.

My point is that Boeing ‘invented’ several airliner configurations, I recite successes and failures and point to some of each from Airbus.

I try to provide perspective rather than misleading headlines.

On the subject of “new” airline programs, there are more order cancellations for the 777X.

“Cathay Pacific Airways plans to shrink its order of Boeing’s newest marquee aircraft, the 777X, as the long-lasting effects of the Covid-19 pandemic trigger a rethink on the top-of-the-range commercial jets.

The airline would “optimise” its order, two sources briefed on the matter said, slashing it from 21 planes – worth some HK$58 billion (US$7.4 billion) – to between 10 and 15.”

“In the short term, Cathay’s existing 68-strong Boeing 777 fleet is mostly in long-term storage abroad, with the airline favoring smaller and more efficient jets such as the A350 to maintain its skeletal passenger flight schedule.”

“In February, the manufacturer saw its orders for the 777X slashed by more than a third to 191 from 309. The adjustment is a reflection of provisions in purchasing contracts that allow for orders to be voided in the event of production and delivery delays.”

https://www.scmp.com/news/hong-kong/hong-kong-economy/article/3131000/battered-coronavirus-pandemic-hong-kongs-cathay

Hardly surprising: now that BA has delayed the 777 EIS even further, airlines can cancel without penalty.

Cathay Pacific has become surplus to needs and will be gone as it is a Hong Kong entity that is being rushed.

You can write all those orders off.

There is a risk that Boeing waits for the goverment to pay for a new plane to save US aerospace export sales of aircrafts, spares and support. One can understand that Boeing want to be very sure of production cost of a new NMA carbon widebody to make a good profit and deliver volumes. The cost for even these trails and prototypes Boeing might want NASA and Uncle Sam to pay. It is a moving target with materials, machining and robotic assembly constantly evolving and the board of Directors need to decide when it is good enough and when the progress is pretty flat so the competition cannot use much improved designs 5 years later.

The US does not run on the European model.

Boeing will not be allowed to fold any more than BAE, but the mechanisms are not the same.

You meant the $426 billion Wall Street bail-out in 2008-9??

A new aircraft hits free cash flow, buy back dividends and the executive bonuses based on them.

“Boeing CEO David Calhoun received more than $21 million in compensation last year while announcing plans to lay off about 30,000 workers.

…

Calhoun, who became CEO in January 2020, declined a salary and performance bonus for the majority of 2021, but he still received stock benefits worth some $20 million, according to a regulatory filing.”

https://www.businessinsider.com/boeing-ceo-took-home-millions-despite-mass-layoffs-2021-4?international=true&r=US&IR=T

The board gets way more cash if they avoid investment/ new programs that will only benefit the company long after they retired.

The mechanism stinks. Bu most influencers are complicit / beneficiaries.

And no, it doesn’t work the same everywhere. https://www.bloombergquint.com/business/airbus-ceo-donates-bonus-to-charity-amid-coronavirus-disruption

In case you’re all looking for Calhouns Full Quote:

“We anticipate a return to a very positive and healthy cash flow in the near- and medium-term future. And our priorities with respect to the use of that cash flow is, No. 1, to sustain the investments we’re making in our company with respect to both production stability and innovation. They are the keepers of our future. Secondly, we will turn toward the balance sheet and reduce debt as quickly as we can. That will be priority No. 1 for us. And get our capital structure back to a pre-pandemic level and a healthy place to prevent any issues in the future from creating any hurt. And then, we’ll turn our eyes sharply toward dividends. We want to get back to a dividend policy, and we want to get back to the relationship that we’ve enjoyed with shareholders for many, many, many years.“

When asked when return to dividend will be:

“I can’t give you a date, and we need a return in our commercial aviation market to support that”

Well, that explains a lot: it seems that planes are sold for the pure purpose of generating dividends.

Whether the planes can actually be used satisfactorily seems to be of secondary concern.

Actually the planes are sold to quote

“ No. 1, to sustain the investments we’re making in our company with respect to both production stability and innovation”

I don’t know why people can’t let Calhoun do his work. In my honest opinion, I can see where he wants to take the company and he is slowly but surely getting there. Like I’ve said Boeing is now doing things they ought to have done before all this started but that’s the price you have to pay.

This current 737 max issue with electricals, Boeing of 2018 might very well have kept quiet. They spotted the problem and acted quickly. 787 the problems with that aircraft did not start with Calhoun but he made the decision to stop deliveries for 6 MONTHS to carry out deep engineering analysis and fix the issues that they spotted, as well as quality control problems. They’ve resumed deliveries on those and have pushed out 6 this month.

Now a Boeing of 2018 will have never stopped those deliveries to sort out those problems.

Are these remarkable achievements, far from it but Boeing would not have done it before and we know that.

The point is the engineering problems that have come up recently, were birthed before Calhoun, but are being discovered under his tenure but it looks like oh he hasn’t done anything. The fact that it was even discovered and reported is evidence that something is working.

I don’t know why everybody is getting their knickers in a twist because he brought up paying of dividend. It’s an AGM what are the shareholders there for? What do you think they actually care about I can tell you it’s not about whether NMA is going to be twin aisle or single aisle. It’s what’s the cash flow looking like, what’s the debt load looking and Moreso. Dividends. Which is why Scott has said correctly they must balance out.

Anyway that’s just my opinion. A lot of people hate Boeing I don’t blame though

Shouldn’t shareholders want to know more about long term survival than dividend?? Just struggling to believe if there are many “long-term” shareholders present in the AGM.

Opus:

I was looking at that same info earlier today as well.

You are spot on to report it.

The issue is, Calhoun is a bean counter with a history of nothing but bean counting.

He was also on the board that left Boeing developed into the nightmare it is (as well as he voted to make the CEO and the COB the same person)

You see the consequences of the 787 program debacle as well as the MAX grounded again.

He also took a bonus for getting the MAX back in the air that was others work (and he will not be held to account for the wiring grounding failure)

In short, he has robbed the bank repeatedly and why would anyone give him any benefit of the doubt?

Unlike his misbegotten salary, he has to earn trust and that means he has to go break the rocks for a long time.

Expecting him to screw it up is the default now for valid reasons.

Opus:

Boeing has responded the way its supposed to with recent issues.

What most (I believe) do not trust is why its done it that way.

Is it to prevent a PR black eye or is it changing culture?

If a person robs a bank every 6 months, you have to wait over 5 months to find out if they are reformed.

Due to the long track record of Corporation robbery (of which Calhoun is a participation ) as well as throwing previous CEO/COB under the bus (for who he voted for as well as merging the position)

its going to be a long time before anyone would believe its reform.

He is getting (7 million) extra fro doing his job. 21 million a year regardless.

I love Boeing, I hate their management with a passion and what they have done to what was a fantastic company and an American Icon.

Huh? You can’t succeed by ignoring resources including capital.

Boeing is publicly traded, which does make its decisions more sensitive to investor perception but may temper crazy CEOs. Dividends are essential for many long-term investors. Financial condition is essential to obtaining loans on good terms – interest rates will vary with risk as evaluated by lenders.

Errors are made – read up on the Dassault Mercure, essentially a larger 737, Air Inter agreed to buy it but no one else stepped up. It wasn’t enough more than the 737 in capacity and its range was too little for many operators outside of shuttles within Europe, which it had been optimized for. (Whereas Brit airlines liked to not just fly within northern Europe but go to sun holiday places well south.) Over half of development cost came from the French government, motivated in part by nationalism I think. Perhaps a good machine technically, designed with some thought to be stretched and re-engined, Air Inter flew 11 of the 12 built for two decades.

Today a fundamental question is when to risk the huge cost of developing a new airliner design, given Boeing’s tight financial situation with recovery from the 737MAX debacle and the uncertain future of the airline industry which is under attack from eco-activist politicians and suffering from the effects of the SARS-CoV-2 panicdemic.

Some of the posts in this thread remind me of conspiracy theories, I just happened across another as to the fate of MH370 – claim US shot it down to prevent sensitive electronic equipment reaching Communist China, author piles up supposed facts and speculative extrapolations from actual facts.

Wait, what? Which one is now their No. 1 priority? Sustaining the investments or reducing debt? Or do they have TWO No. 1 priorities?

If the big boss can’t get his priorities right, how can anyone else?

A little off topic, but interesting:

Breeze Airways (David Neeleman’s new startup) has ordered another 20 A220-300s, which brings his total to 80.

“…the deal would make Breeze the second-biggest customer for the Canadian-designed A220 family after Delta Air Airlines DAL.N, leapfrogging JetBlue JBLU.O which Neeleman also founded.”

https://www.nasdaq.com/articles/u.s.-startup-breeze-airways-boosts-airbus-a220-jet-order-sources-2021-04-26

Like I’ve noted, Southwest Airlines is going to find all them B737Max-7s up against those A220-300s in next three to five years or so. Kelly may be able to squeeze in another 3 or 5 seats, but those carbon fiber winged Bombardiers might be hauling folks around for 10-15% less per seat. I wonder if he paid Boeing less than what Delta paid for that initial order of the CSeries? I’m guessing when you factor in the Max problem, he did. And I wonder if there is a lawsuit somewhere in the future for selling a 60 year old plane at below cost, to entice people to buy it.

First that assumes A220-300 are on direct competitive routes.

No there are no lawsuits, dumping products into the US market is under a law that has nothign to do with domestic.

Boeing in its stupidity attempted to use that law where it does not apply. They have been kicked out of the Canadian tanker market as well as the fighter market (not official yet but Canada bought used F-18s and will not be buying any US aircraft).

Will South West be able to compete? Yes, but South West may wind up buying A320-300s or 500s in the ends as well. Business is business.

TW, technically you mean SWA might buy A220-300 or -500? You said A320.

Boeing hurt itself with its stooped trade complaint. We’ll see what happens in Canada with fighters, the used F-18s are a stopgap, Canada is part of the international F-35 effort.

It is stealthy and would support Canada exchanging surveillance data with F-22s out of Alaska, that would facilitate each force having only one airplane in a given area instead of two for redundancy (the area near Alaska of course, I don’t know about near Greenland where USAF has a base in Thule).

Canada goes in circles on Arctic sovereignty, has for several decades. At one time it pushed Inuit to settlements further north because they were not doing well at present location and for sovereignty presence. Resolute Bay worked out OK, the other location did not because of constipated bureaucrats, the RCMPolice helped on the ground despite bureaucrats in Ottawa.

Canada’s basing of fighters in the Arctic is poor, for example at Yellowknife (which is like Fairbanks but the US does not have big islands north of Alaska as Canada does), I always vote for basing interceptors at CYRB.

Also, just in the news, Canada looks to Airbus’s MRTT A330-200 for tanker, and government VIP transport.

@Sam

Delta, JetBlue and Breeze. About 250 of them.

They will be head-to-head against a number of SW -7s and American and United A319Ceos. I can’t imagine that the A220s were sold for much more than the -7s or the used A319s (figure in maintenance on these.) Airbus has whined incessantly on the fact that the 220s were sold to cheap.

SWA apparently paid $23-30 mln for the 737-7’s. List price is $99.7mln. Not saying it not the right decision, or price dumping, but the nett profit will probably not be high, if at all.

@ keesje

Analysts estimate that Boeing has a margin of about $12M on a 737-7 when it is sold at “customary” 50% discount.

Simple math:

– 50% of $100M is $50M.

– $50M – $12M = $38M.

If it’s sold for less, it almost certainly represents a loss.

@Bryce

That’s 24% on a narrow body. Does it not seem a little high to you?

I go back to the 2018 financials, when BCA delivered over 800 aircraft, when fixed costs were spread out over a huge number of units sold and the company made a record profit margin of 13%.

That 13% represents both narrow and wide bodies – which have a higher margin.

Colour me skeptical

@ Frank

It does seem high, but it depends on what is included in the concept of “margin”. Importantly, are development/start-up costs included, or just per-unit manufacturing costs? And what production rate was assumed to underlie that margin?

Moreover, I think we can assume that the big customers will get more than 50% discounts, which thus cuts further into margin.

The point here was to demonstrate that the margin on the SWA sales was zero/negative.

Boeing wants to accomplish 3 very expensive things, at once:

1) Pay down debt. Interest payments for Q4 2020 amounted to $700 million. That is $2.8 billion a year which is some $25 billion (at 2018 margins) of revenue. Borrowing any more drives this number up and might push them into junk status, which probably adds between $1-2 billion extra to the bill.

2) Revamp the BCA product lineup. I’m betting that there are various factions inside pulling for different solutions. At the top are the money guys who are hoping that they will not spend a bundle on development as it will cut into their compensation. Guys who have a 5 year horizon (and get out) will want the company to limp along, keeping share price high, out of Chapter 11 and could care less about the long term viability of the entity.

3) Keep The Street satisfied. If investors are happy, they keep the people making them happy, in place. That means dividends and buybacks.

Boeing can’t launch anything without borrowing more. Perhaps they can use the revolver that they paid down, to fund some portions of a new plane. but people will see this as interest expense goes up. They just don’t have the $15 -20 billion to do it.

There is also a matter of where to go with a new aircraft. Anything new they roll out will have an additional $15-20 million per aircraft price tag (assuming 1000 units sold) saddled on it, to cover capital costs. Airbus has already spent their money (and was gifted some $7 billion from Bombardier) in capex, so BA is at a disadvantage. A new design will have to be very attractive to customers, in order to compensate for the added cost they will need to pay to cover Boeing’s design costs to launch it.

At what price point will airlines say, “Thanks, but no thanks – we can make do with the current lineup, instead of saving 5% in fuel costs”.

Also, the market has changed and BA got caught looking the wrong way with the 777X. In the future, is the biggest aircraft customers are willing to operate an A350 sized aircraft? The 777X is looking to be Boeing A380. Wrong plane, wrong time.

The way the market has shifted and how Boeing’s lineup matches up against Airbus (not to mention customer needs) lends itself to those in the company arguing for the status quo, to be heard loudest.

“Guys, we don’t have money for a new plane. Borrowing will drive up interest rates and could drive us into junk status. Our planes match up horribly with the market now and we can’t launch the two planes needed to do it right. All three programs are bleeding and need to be fixed. Let’s just do that, tiptoe the line, get paid – and leave the mess for the next guys to worry about (Like the previous guys did to us…)”

You think Calhoun et al. are airplane guys who worry about the ‘legacy’ they leave behind? Just take a look at Muilenberg who was parachuted out and is jumping into a SPAC launch… I’m guessing some guys who stayed behind are looking at him and going “Lucky bastard”

Not anywhere near my arena but somewhere there should be a analysis run as to what happens with no new programs to collect money and kick the accounting can down the runway.

As this is a Pyramid scheme (and tax cheating) at some point it has to crash.

It should be possible to calculate that.

@Trans

Yes. But I’m going to give you the quick and dirty version;

At the end of 2020, Boeing Commercial had a backlog of $281.5 billion.

The most optimistic, best case solution for determining the margin on these planes would be to take the y/e 2018 numbers – the year when BA delivered a record 806 aircraft for $60 billion in revenue and made almost $8 billion in profit from BCA, which breaks down to a 13% operating margin.

Now, if tomorrow, Boeing could snap their fingers and magically make, deliver & get paid for each and every plane in it’s backlog – they would make $36.5 billion (using the 2018 pre grounding, pre pandemic number).

$36.5 billion. Best case.

They have ~$62 billion in long term debt.

They must have some valuable assets to sell. Delta / Northwest had I think a hotel in downtown Tokyo; Bombardier had airport and downtown land. Boeing must have land in Long Beach, Texas or maybe around Seattle that must be worth Billions. I’d bet that Boeing Field is coveted real estate.

Boeing Field is owned by King County. Its actual name is King County International Airport.

Ok. I bet that land is worth a lot. Conceivably, Amazon and the big high tech expansion companies must be coveting other land and buildings owned by Boeing in your area.

Any enterprise that undertakes infrequent but regular, high cost, high risk product development to guarantee its future should have cash on had for at least one and ideally two development cycles. So Boeing should have set aside between 15 and 30 billion.

Otherwise the company can only develop new products funded by new investment, cash flow or by borrowing and if there is a substantial decline in its core business may find itself unable to fund the new product needed for recovery.

Well – there is all those shares they bought back for $43 billion which could be turned into the new aircraft you talk about.

Problem is – who’s got the balls to do this?

That would take a lot of courage. I suspect they may only get 20 billion for the shares they paid 40 billion for. Plus it would substantially depress share prices possibly attracting a share-holder law suite.

I agree.

It could be done but stay tuned. I severely doubt it.

@jbeeko

Boeing started the recent buyback spree in 2013, when share were ~$100. They are hovering around the $250 mark today, and did not get there until late 2017 – so depending on how many they bought, they could be at a dollar for dollar value…i.e. around the $43 billion they spent.

I am so not doing a year by year analysis to determine how much they spent vs what they are worth…

Frank – thank you. I should have checked.

Cutrent stock market rewards short-term thinking of established companies, but rewards hype of “start-ups”!

Start ups are short term as well.

Come in overpriced (Wall Street is happy) then go down like the Titanic, Wall Street is onto the next big thing.

“Nobody I know suggests that Boeing’s executives and Board of Directors not boost shareholder value via stock buybacks or dividend payouts”

Dividends are fine. Share buybacks are nothing but looting by the C class (raises the price for their stock options), and used to be illegal, as they are a form of price manipulation. That regulation was abolished under the Reagan administration.

Buybacks should be illegal once again.

> Dividends are fine. Share buybacks are nothing but looting by the C class (raises the price for their stock options), and used to be illegal, as they are a form of price manipulation. That regulation was abolished under the Reagan administration. <

A rousing "hear, hear!" to all that. jbeeko's comment above is apposite, too. Boeing is way behind in the point, and they

put themselves there; via buybacks, for one Big Thing.

Yes, yes, yes!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

Its also corrupting as shares are a big part of compensation.

+1 @Bill7.

Agree 100%!

“Dividends are fine.”

No they arent fine. The US system of double taxation of the company and the shareholder for any dividends means its flawed.

The majority of shares are held by funds that want share price growth, Boeing cant run its business like to suit a 1950s version of Wall St, it has live within the current system. A recent period of bad management has meant imbalances in the share buyback program and coincided with black swan events

Anyway dividends can be funded by borrowing as well.

Duke:

You miss the point. Dividends are the normal but they are supposed to come out of good profits after company is secure, R&D is paid for and future products are int he works.

Its how its been corrupted that is the issue. No sane board would approve that (which means Boeing board was insane when they tired to do that with the 13 billion that was borrowed to do so)

There should be mechanisms to can a whole board as well as not allow that attempted behavior.

All 1950s thinking…. no good company would these days ensure its all cash flow is taxed as company profits and again as dividends in hands of shareholders who would rather have capital gain in future years.

The current mechanism rewards risky corporate behaviors. More belly-ups!!

> The majority of shares are held by funds that want share price growth

I want a Pony, too..

How’s the present system working for the great majority of the Citizenry? If it’s not working well

for them/us, we need a Different System.

@DoU

You miss the point – the share price growth system is bankrupt – and has almost bankrupted BA – it works for one or two monopolies FB Ggle etc at the expense of the rest

Dividends do not double tax, the company pays taxes the shareholder pays taxes

To fund dividends other than from cash flow simply because a company can borrow – for the moment – cheaply – is also to bankrupt the company : once again BA is proof of this

@ Keith Sketchley – I was wrong you were right bring back @Rob

@DoU

You miss the point – the share price growth system is bankrupt – and has almost bankrupted BA – it works for one or two monopolies AMZ FB Ggle etc at the expense of the economy, the rest of the market

Dividends do not double tax, the company pays taxes the shareholder pays taxes

To fund dividends other than from cash flow simply because a company can borrow – for the moment – cheaply – is also to bankrupt the company : once again BA is proof of this

@ Keith Sketchley – I was wrong you were right bring back @Rob

I see you have no knowledge about financial affairs to add to your zero knowledge about aviation….can you even drive a car ?

@ DoU

Actually, in most posts here, you’re the one who continually has to be corrected for your lack of real-world financial knowledge 😉

Most financial analysts would categorize Boeing as a “value stock” rather than a “growth stock” — meaning that its price isn’t expected to outpace price development in the broader market. Value stocks are only interesting to investors when they pay out dividend. Even when taxed, dividend is a source of income. For growth stocks (with low to zero dividend), income can only be generated by progressively liquidating partial stock quotas, which incurs fees and capital gains tax.

Your attempt to profile yourself as a financial guru is pure “shanzhai”.

@DoU

Please moderate your language : you are sounding too corporate snarky

BA is the company which is bankrupt (almost) it is they who have mismanaged their finances

It appears you post to support management-but why, to what ends, support such mis management?

@Bryce

Exactly – routine BA disinformation

The can you drive… a car remark harks back to the Jedi insults

I don’t think the MAX 9 in the lineup is a mistake.

Its not an A321 Challenger, but it adds a variant that has sold to those who need a bit more carry capacity.

As the MAX 8 carries a bit more than the A320 and the 9 even a bit more, the economics are better.

Its the -10 that is a total flop (and more so as its a ticking time bomb for Boeing as they have to bring it fully up to snuff AND then change the -7/8/9.

Per plane profits fall (if there are any )

Better off a new aircraft and dump the -10 and all it implies. Not that I have any hope mind you.

No doubt BA never imagine AB would pull LR /XLR out of its sleeve.

Why does LNA imagine that the vast 737 replacement program can be done in 7 years, when even the MAX took 6?

My strategy would be simultaneous development of A321 and A220 300 competitors with mostly the same systems. This would give Boeing a significant advantage over Airbus, whose products are actually fairly badly compromised by age and different operating and production systems and all the compromises associated with their birth. If Boeing waits until 2023, Airbus might as well jump Boeing just like they did with the NEO, knowing that they have at least 10 years with competitive incumbent products to work through the program properly.

> My strategy would be simultaneous development of A321 and A220 300 competitors with mostly the same systems. This would give Boeing a significant advantage over Airbus, whose products are actually fairly badly compromised by age <

Not seeing much that latter part, esp in relation to its

"competition". If I'm reading you accurately, Boing could eventually, somehow, someday be in a better

position than AB is *now*, with its current products and their long backlogs, and w/ the 321XLR coming online? Is the assumption that AB will be sitting still

during [all that] time?

Of course airbus will do something about it (assuming they’re awake and not blinded by short term cash), but if Boeing doesn’t act quickly they won’t have to.

> My strategy would be simultaneous development of A321 and A220 300 competitors with mostly the same systems. This would give Boeing a significant advantage over Airbus, whose products are actually fairly badly compromised by age <

Not seeing much that latter part, esp in relation to its

"competition". If I'm reading you accurately, Boing could eventually, somehow, someday be in a better

position than AB is *now*, with its current products and their long backlogs, and w/ the 321XLR coming online? Is the assumption that AB will be sitting still

during that long time?

Boeing is not going to use the same systems that Airbus developed.

They may not be able to do to terms of the contracts and they would not be optomised for a new aircraft and its new approach .

Boeing needs to make a hit out of the park and the A320 would be like the MAX, still competitive but no longer a long term prospect.

@Trans

Good thing they have the A220-500 sitting in the wings, waiting, as the A320Neo replacement. Then the lineup goes A220-100, -300, -500, A321Neo, LR, XLR.

Done on the cheap, too – since Bombardier has already flown it for them on their sim ‘puter program thingie, already.

“”the A220-500 sitting in the wings, waiting, as the A320Neo replacement. Then the lineup goes A220-100, -300, -500, A321Neo, LR, XLR.””

The A225 will come, it will be in competition with the A320, but not replace it, simply because of the needed production rate and price.

It could be that the A225 will come together with an A320plus because the gap between A320 and A321 is big.

If the A320 is kept, the A319 might still be there because of the price and the similarity with the A320.

I could see the lineup with A221, A223, A225, A319, A320, A320plus, A321, A322.

You have to consider that Boeing will not design a new plane and MAX orders will dry, so Airbus should offer more.

Southwest made more money per percentage than any airline in the world with 500 737-700. The max 7 is bigger than the -700, A319neo and the A220-300. Also Southwest do not cram seats into their aircraft. Just check out their seat pitch. Max seating for A220 is 160 @ 28 inches and Max seats for Max 7 is 172 at the same pitch.

Thank you, I had missed someplace the -7 is 6 feet longer than the 700

@Daveo

All that matters is how close you get to 150 seats on the Max 7/A220, because that’s all the SWA will put in there. After that, by law, they will need another flight attendant.

I’d go with Airbus’s present competencies and (esp) institutional memory over its competition’s, in a land

of free choice. Not to mention workforce and supplier

satisfaction (crucial and maybe decisive over the long term)..

Not seeing anything from the US company to make me

think otherwise, yet. “We’ll get ’em in 2037! ..”

B7

Apparently Southwest will configure the 737 Max 7 with 150 seats, seven more than the older 737 it replaces. Frequent short flights by WN favour a jet with lower weight i.e. A220-300 which happens to be more fuel efficient per seat, too.

@Pedro

They won’t go any higher then 150 because at 151 you need another stew

And the same story, its how an aircraft fits in overall to a company and South West has made a single one work for it.

A220 adds its own costs in startup, pilot training and no commonality, as well as maint training, spares parts.

Its a balancing job of how it all works out, but South West clearly has made its choice as to what they feel works for them.

I am not their accountant to so I am not going to have the Hubris to tell them what they should do. Respect their decision and see how it plays out.

@Trans

Absolutely. All you have to do is look at their balance sheet to know that are running their op the right way (all things being equal).

The question I have then, is imagine if you will, what would have happened to SWA had the grounding occurred in a couple of years (without the covid pandemic) and what shape they would have been in, had they had some 300 Max’s in their fleet?

I’m sure that was a subject that was kicked around the c-suite for quite a bit, with the guys deciding that it was better to be aggressive, then safe (fleet diversification).

I guess we’ll see how it plays out

You guys do not understand that A220-300 and 737 max7 @ 150 with three lavaratory are not the same comfort as the max have more floor space. Some people in this forum equate Southwest with spirit, frontier or European LCC. They configure their aircraft better than legacy carriers with regard to comfort.

“”the max have more floor space””

Lets do the easy floor math.

Length between the doors:

24.11m A223

22.3m MAX-7

Cabin width:

3.28m A223

3.53m MAX-7

Floor space:

24.11m x 3.28m = 79.08sqm A223

22.3m x 3.53m = 78.72sqm MAX-7

Then the MAX-7 needs 2 overwing exit pairs, the A223 only one. This will reduce the seat pitch on most seat rows of the MAX-7.

I’ve never heard anyone that says Delta or JetBlue is LCC. 🙂

The problem with the MAX is 2 x 3, with narrow seats (don’t get me started about the idiocy of the much hyped widest seat of WN

https://qz.com/386379/southwest-airlines-new-wider-seat-probably-isnt-wider-after-all/ ). Why should I concern if there is more space (wasted) at the front or rear??

Inside the A220, only 1/5th chance (in reality it’s even lower unless load factor reaches 100%) you are in the dreaded middle seat.

Most load factors are 100%

Take a look at JetBlue’s A220 inaugural flight (and why it’s so nice … see tweeter’s other tweets)

https://mobile.twitter.com/airchive/status/1386822908966735872

With the current hedge fund ownership of Boeing shares I don’t expect any new aeroplane. Their interest doesn’t lie in WASTING money on new aircraft, just spitting out derivatives of existing models. Since its an effective duopoly between Airbus and Boeing, the derivatives will always have a customer base and allow the hedge funds to milk the company dry through dividend payouts. But when a third capable manufacturer shows up on the market destroying the duopoly, expect Boeing to go down the path of MD.

Enjoy it while you can, Boeing has a used by date pinned on it.

Meanwhile pax misbehave about masks

Alaska Airlines has banned 500 people – yes five hundred.

Including an elected Alaskan official heading to the state capitol for a legislative session in which voting is only in person: https://www.fox10phoenix.com/news/alaska-senator-drives-takes-ferry-in-2-day-trip-to-work-after-airline-suspension-over-mask-policy.

(The twit had to drive from near Anchorage, through Canada then take a ferry to Juneau which is only accessible by air or water. Took her two days.

I don’t know why she couldn’t take a ferry from Anchorage to Juneau.

Juneau is near the top end of the panhandle, not accessible by road but close to Canada, perhaps there is a ferry from Haines or Skagway – both connected to Highway 37.

Nor why she didn’t charter a small airplane (if the airport didn’t ban her).

She’s trying to spin the situation – yeah, she’s a politician.

Conspiracy to defraud??

Isn’t BA under a deferred prosecution agreement?

Boeing quietly agreed to repay the U.S. $10.7 million after a 3-year investigation concluded it double-billed the military for taxes paid to foreign governments on overseas employees

https://mobile.twitter.com/ACapaccio/status/1387036907457101826

More evidence of the evaporating MAX order book:

FG: “GE Aviation lost 1,900 Leap 1B orders in 12 months”

https://www.flightglobal.com/ge-aviation-lost-1900-leap-orders-in-12-months/143476.article

@airbus remains far ahead of @BoeingAirplanes in terms of deliveries to APAC

APAC deliveries ramped up in March and contributed more than 30% of global market

https://mobile.twitter.com/MaxK_J/status/1386973995526930438

Summarizing (single aisle and twin aisle):

– BA has had zero deliveries in APAC since September last year.

– BA had zero deliveries in APAC in the period April-July last year.

“Gerrard White

April 26, 2021

@Keith Sketchley

@Rob retailed the corporate point of view, somewhat distinct from most comments on this site”

More of your typical sneer tactics that just suit your fantasies while revealing your ‘content of character’.

You use the standard collectivist scam of claiming to speak for everyone else.

Bad behaviour.

@Keith Sketchley

To distinguish corporate comments is not to ‘sneer’

The corporate use the ‘we’

What has collectivism to do with anything discussed?

The corporate do not like to debate or discuss, preferring, as BA demonstrates, to denigrate

Along with the corporate comes the morality police

Gerrard White:

Your view of life is collectivist, obviously, including your ‘corporate’ distinction and your evident beliefs from what you recommend as solutions.

Your posts often sneer, including that one, don’t evade “…retailed the corporate point of view.” which disparages an individual who calmly presented facts – FACTS Mr. White. You can add other information if you actually have any, but sneer/smear is shameful behaviour.

But hey! perhaps I should be glad you reveal your ethics to everyone,

Boeing is coming with its Q1 results today, before markets open.

Analysts are expecting another big loss.

Reuters: “Longer runway, daunting challenges ahead for Boeing CEO”

https://www.reuters.com/business/aerospace-defense/longer-runway-daunting-challenges-ahead-boeing-ceo-2021-04-27/

For those who can’t get behind the paywall, here’s an equivalent article on nasdaq.com:

“Boeing is expected to report a smaller first-quarter adjusted loss of $1.16 per share, compared with $1.70 per share a year earlier, helped by an improvement in aircraft deliveries as airline customers add flight capacity, anticipating a rebound in summer travel.”

https://www.nasdaq.com/articles/preview-longer-runway-daunting-challenges-ahead-for-boeing-ceo-2021-04-28

@Bryce

Here is another preview:

“”The consensus EPS Estimate is -$1.10 (+35.3% Y/Y) and the consensus Revenue Estimate is $15.08B (-10.8% Y/Y).

Analyst expects Free cash flow of -$3.94B.

Over the last 2 years, BA has beaten EPS estimates 25% of the time and has beaten revenue estimates 38% of the time.

Over the last 3 months, EPS estimates have seen 1 upward revision and 7 downward. Revenue estimates have seen 0 upward revisions and 6 downward.””

And another report on the 787 from Dhierin Bechai, as often torn between caution and prudence

https://seekingalpha.com/news/3686267-boeing-q1-2021-earnings-preview

https://seekingalpha.com/article/4421270-boeing-787-improvement-on-the-horizon

“Dreamliner inspections continue, increasing cost growth on the Boeing 787 program.

On unit level, the Boeing 787 should still generate significant cash flows.

Also for the deferred balance, reductions are still possible, but significant cost growth could trigger a forward loss on the current accounting quantity.

Uncertainty about the Boeing 787 financial performance is higher than ever.”

@Gerrard

They lump in the total backlog for the entire company. Breaking out the BCA numbers:

At the end of 2020, Boeing Commercial had a backlog of $281.5 billion. (from the Q4-2020)

‘Commercial Airplanes secured orders for 100 737 aircraft from Southwest Airlines, 25 737 aircraft from United Airlines, 23 737 aircraft from Alaska Airlines, and four 747 freighter aircraft from Atlas Air. Commercial Airplanes delivered 77 airplanes during the quarter and backlog included over 4,000 airplanes valued at $283 billion.’

‘Commercial Airplanes added 76 net orders’

So from Q4 to Q1, the value of the backlog increased $1.5 billion and the net order tally rose up 76 units – for an average increase of $19.7 million per airframe.

I’m guessing SWA really did get a sweetheart of a deal, after all.

Interest expense for the quarter was $679 million. That’s $2.7 billion a year. That’s a hefty borrowing cost number.

@ Frank, @ Gerrard

That debt servicing cost of $2.7B per year is crippling.

And, if a rating downgrade comes, it will increase even further.

Plus: doing debt rollovers in an era of increasing interest rates will only further the pain.

Interesting that there were zero 787 orders in Q1, and that 787 inspections are continuing.

I wonder what the running compensation tally is for all those 106 MAXs that are now languishing in their second extended grounding…at least several hundred million $?

@Frank

Thanks for this revealing analysis

This precedent will not help BA in the future – will bind them in mutual co dependence with a few anglo airlines

If ever India re certs, will not part of the deal be similar very low prices, ditto China ditto anywhere else

CNBC: “Boeing posts sixth consecutive quarterly loss, expects turning point in 2021”

“Here are the numbers:

– Loss per share: $1.53 adjusted. Analysts had expected a per-share loss of $1.16, according to Refinitiv, but it’s unclear if the numbers are comparable.

– Revenue: $15.22 billion vs. $15.02 billion expected by analysts surveyed by Refinitiv.

The plane manufacturer had a net loss of $561 million for the first three months of 2021 on revenue of $15.2 billion, 10% lower than last year but ahead of analysts’ estimates.

The company reported a $318 million pretax charge related to issues with a supplier in its modified 747 plane used as Air Force One.

Boeing shares were down more than 1% in premarket trading after it reported results.

https://www.cnbc.com/2021/04/28/boeing-ba-q1-2021-earnings.html

A minor news item:

https://www.heraldnet.com/business/fedex-said-to-be-in-talks-to-take-over-dreamlifter-center/

Few Dreamlifter flights to PAE any more, no surprise as 787 production is now in the eastern US. Still delivering some 767 noses, I don’t know how 777 pieces are transported (the Dreamlifter was built for handling 787 pieces).