Leeham News and Analysis

There's more to real news than a news release.

Pontifications: “The need for radical fuel improvements will only increase over time.”

By Scott Hamilton

May 30, 2023, © Leeham News: “The need for radical fuel improvements will only increase over time.”

That’s the definitive conclusion of Arjan Hegeman, GE Aerospace’s general manager of advanced technology.

GE is working on Performance Improvement Packages (PIPs) of its current engine lineup used on Airbus and Boeing airliners. It’s also developing the GE9X, now in testing on the Boeing 777X, and concepts of a hybrid-electric and hydrogen-fueled engine.

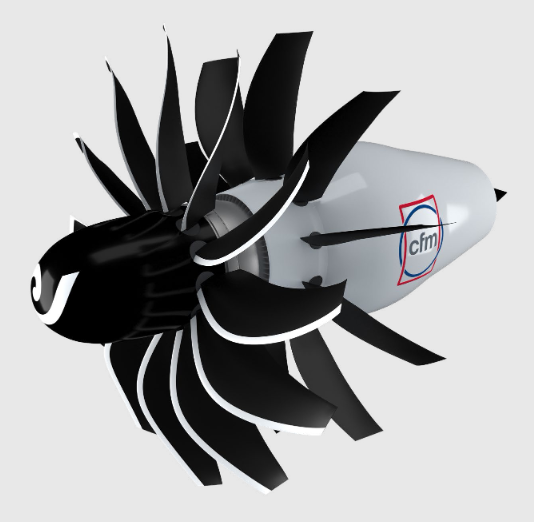

But the big bet is on the Open Fan “RISE” (Revolutionary Innovation for Sustainable Engines). “The Open Fan technology—it’s a go,” Hegeman declared earlier this month at a press briefing in advance of the Paris Air Show next month.

CFM RISE Open Fan engine. Credit: CFM.

The Open Fan is an evolution of the Open Rotor engine tested in the 1980s. The concept shows a dramatic reduction in fuel consumption compared with the engines of the day. But the counter-rotating rotor design was very noisy. Coupled with other technical challenges and a sudden drop in fuel prices, GE (and rival Pratt & Whitney) dropped the concepts.

But research and development continued. Today, PW thinks its Geared Turbo Fan engine will suffice for the future. Rolls-Royce is also pursuing traditional engine designs. But GE believes the problems of the Open Rotor have been solved for the Open Fan.

How?

It comes down to supercomputing, said Mohamed Ali, GE Aerospace vice president of engineering.

Supercomputing is the key

Supercomputing is going to be key to improving engine designs and working toward greener aviation, Ali said during the same press briefing. “We have access to supercomputing capabilities and we are privileged to be working with the Department of Energy. It’s by invitation only. We are designing RISE using that.”

Using Supercomputing power is advancing shape, fuel efficiency, and acoustics, Hegeman said. Whereas the Open Rotor was too noisy for use on an airplane even under the less stringent regulations then in place, the Open Fan has a lower decibel level than the LEAP engine. “The single fan was a design breakthrough. It’s better for weight, better for costs.” The RISE has only a single whirling fan instead of the counter-rotating fans of the Open Rotor. There are fixed blades aft of the rotating fan that helps dissipate noise. Supercomputing led to this breakthrough.

There was a second big breakthrough Hegeman wasn’t authorized to reveal.

The Open Fan is the most recognizable feature of the new narrowbody concepts, said Hegeman. “There’s a laundry list of technologies that will be in RISE. It’s how do we get that core smaller and smaller to burn less and less fuel, whatever that fuel is, whether it’s Jet A, SAF, or hydrogen.

“We have a narrowbody engine that has a fan similar to the size of the GE9X.” It’s a narrowbody engine able to move the air the size of an engine on the 777. But there is no casing around it, so it’s not that much bigger in diameter than today’s LEAP, Hegeman said. If you combine it with a core that is the size of a business jet engine, moving the amount of air of a 9X engine but very efficiently with narrowbody level-type thrust. “That is what RISE is.”

Past advances are no longer enough

In the past decade, GE replaced all its commercial airliner engines. The CFM 56 was replaced with the LEAP, the CF6 with GEnx, the GE90 with GE9X, and the CF34 with the Passport, Hegeman said.

“All had one thing in common: the fuel improvement was 10-15%. That’s been the name of the game in the industry. Each generation gets better fuel efficiency. It wasn’t so much for emissions in the past but for pure economics for the operator. Pratt and Rolls have been doing the exact same thing. When we started the LEAP 1B in 2011, the price of oil was at an all-time high. We had to meet or beat the 15%.”

But, oil prices fluctuate, at times relieving immediate pressure for changes. Today, Hegeman said, “We are convinced that with climate change, and the price of fuel, whether it’s carbon-based, synthetic, bio-mass or completely alternative fuels like hydrogen, the cost of carbon emissions and the cost of fuel will increase over time. It is no longer tied to the price of a barrel of oil.”

Hegeman said that investing in fuel efficiency is not only the right thing to do for the planet, but for following generations. It’s also going to be a much more economic differentiator for the operators compared to what it was.

Today’s technology leap

Boeing CEO David Calhoun publicly stated several times that the next generation of airplanes and engines must be a 25% to 30% improvement over today’s aging airframe and modern engines. When GE announced the RISE in June 2021, it said the goal for fuel reduction was 20%. There are skeptics in Boeing who think this might fall to 10% once the engines are installed. But last week, GE’s target fuel reduction is more than 20% (without specifying what “more” is). And Hegeman reaffirmed that this is after installation.

“A new engine has to get at least 20% or more fuel efficiency, which ties directly to the amount of carbon you emit,” Hegeman said. “The overall integration of the next airplane with engine and airframe needs to be 25%-30% better than today’s airplanes. We’re looking at the aircraft level, what do we achieve? We don’t worry too much about what is on the aircraft side and what is on the engine side. It’s got to work as a system.”

GE is working with Airbus and Boeing and their engineering teams on future concepts. “We know the numbers they are coming up with for the aircraft,” he said.

“We also need to look at alternative fuels. SAF, synthetic. A whole new era is the electrification of flight. In the past, we always got our efficiencies through propulsive efficiencies—how efficient does the propeller, the forward fan, provide thrust? And thermal efficiency—the core—how little fuel can you burn?”

GE is doing studies in these areas. We’ll have more reporting in future articles.

Some recent background news regarding pricing of alternative fuels — pricing does, after all, act as a driver for this type of engine innovation:

***

(1) LH2 production (and SAF production) requires green electricity.

“Electricity Prices Plunge By 75% As Finland Opens New Nuclear Power Plant”

https://oilprice.com/Alternative-Energy/Nuclear-Power/Electricity-Prices-Plunge-By-75-As-Finland-Opens-New-Nuclear-Power-Plant.html#:~:text=The%20commencement%20of%20regular%20output%20from%20a%20much-delayed,new%20nuclear%20plant%20in%20more%20than%20four%20decades.

Just a few days after that article was written, electricity prices in Finland went negative, and output from the nuclear plant had to be cut so as to push the price into positive territory again.

***

(2) Relative pricing of LH2 and JetA in 2035:

“Running a hydrogen plane could be cheaper than traditional aircraft by 2035”

“Hydrogen jets could be cheaper to run than fossil fuel planes from 2035 provided kerosene is taxed adequately, a new study shows. In 2035, running planes on hydrogen could be 8% more expensive than using kerosene. But with a tax on fossil jet fuel and a price on carbon, hydrogen planes could become 2% cheaper to operate than their kerosene counterparts. These pricing measures are key to the deployment of green technologies like hydrogen planes, T&E says.”

https://www.transportenvironment.org/discover/running-a-hydrogen-plane-could-be-cheaper-than-traditional-aircraft-by-2035/

“The single fan was a design breakthrough. It’s better for weight, better for costs.”

😀

The next design breakthrough will probably be a high wing.

GE obsiously is the PR spout for CFM

with the base model of sentence building being “we, GE have..”

I do wonder how work and innovations distribute

between GE and Safran?

Yes, I’m also very curious about that.

In particular, I’d like to know if the LEAP-1As are manufactured solely by Safran, with the LEAP-1Bs being manufactured by GE…or is it a mixed affair?

And who does the LEAP-1Cs for China?

In the CFM partnership, GE designs and builds the core and Safran the LP system. Then each ships their half to the other partner. This allows both GE and Safran to do final assembly, test and delivery. The split between LEAP A,B,C final assembly and test is chosen so that the total engines built by each partner are approximately equal.

Thank you.

But, since Safran is close to AB and GE is close to BA, wouldn’t it make sense to have Safran do (predominantly) the As and GE do (predominantly) the Bs?

Also, with an eye to the (non-insignificant) differences between the two engines, wouldn’t it be more efficient from a tooling point of view to have such a split?

@bryce

At the moment the CFM partnership seems to be in a perfect balance. Airbus has a second assembly site in mobile, and Boeing’s production rate is lower than what airbus produces in EU.

At the end of the day, the split nicely works out to be approximately 50-50.

Back during the max groundings, Boeing didn’t significantly lower the production rate until later on. Then it was only a small window period before the pandemic hit, hence we couldn’t see how the partnership works with the unbalanced demand on both sides of the Atlantic.

@bryce Yes the starting point is to prefer A deliveries from Safran and B deliveries from GE and then balance as needed. In any given year the numbers are rebalanced. It is important to note that both partners maintain Production Certificates and tooling for all models. This is essential to ensure flexibility.

Airbus has 4 different assembly sites for its A320/321 series. It has no bearing on the engine production.

And no Safran isnt *close to* Airbus at all, their own engine production is largely geared to helicopters

@DoU

(1) Ever checked to see which AB A320/321 FALs churn out the most planes? Hint: think Europe.

(2) Safran is in Europe. Airbus is also predominantly in Europe. See now how close they are?

***

@ Gareth Richards

Thanks for the additional explanation. 👍

“There was a second big breakthrough Hegeman wasn’t authorized to reveal”

My guess for this is the toroidal fan design.

Must be the recuperating heat recovery system, which CFM has mentioned consistently but hasn’t been too forthcoming with other details so far.

https://www.faa.gov/sites/faa.gov/files/2022-02/phase3_ge.pdf#page=4

Combining the open rotor and the recuperator technologies could yield a 30-40% fuel burn reduction, in my estimation.

Recuperating modern aircraft engines is not that easy as the work extracted out of the LPT lowers temperatures to below compressor exit temperatures of a modern high pressure compressor, hence to add heat before the burner you need a heat pump. If you have LH2 available it is better to cool the compressor and the turbine cooling air.

Regarding the “supercomputing” to which Mohamed Ali refers:

(he’d probably have preferred to use the term “AI’, since that’s the new buzzword these days — but that’s (nominally) a different concept):

A computer in such circumstances just calculates the outcome of a physics model for different scenarios.

A supercomputer just does it more quickly, allowing more detail to be used and/or allowing the outcome to be acquired more rapidly.

In all cases, the quality of the outcome is going to be determined by the quality of the model — there’s no magic involved that can compensate for shortcuts in the applied physics.

When ASML calculates vibrational modes and fluidics phenomena in its lithography machines, the models that it employs go right up to sixth-order effects. I’m wondering if GE’s models are that sophisticated — I somehow doubt it.

It will, indeed, be interesting to see the “on aircraft” performance of the RISE compared to the theoretical performance.

They combine the supercomputing of detailed FEM and CFD models with the LEAP-1 series woven fan blade technology to get the fuel efficiency and noise numbers I suspect.

GE’s subsidiary Dowty was involved in some high-powered computer analysis of propeller blades almost a decade ago, so their models should be even more advanced by now:

https://www.scientificamerican.com/article/the-return-of-the-propeller/

GE says (https://www.ge.com/news/reports/gaining-altitude-airbus-a380-to-test-cfms-open-fan-architecture-in-flight)

“…In the second half of this decade, the aircraft manufacturer will partner with CFM to carry out a flight test demonstrator program on an Airbus A380 to validate the open-fan engine architecture….”

As Scott reported, noise was an unsolved problem with the 7J7 open rotor design in the ’80’s, including sonic fatigue in the adjoining structure. Does GE have a working prototype with static testing to validate their claim to have “solved” the noise problem?

I share your skepticism: although the engine itself — in isolation — might eventually operate within spec, one can expect problems when such an engine is mounted on/near aircraft structures. I don’t accept that all such effects are being adequately modeled — particularly as we don’t even definitively know where/how such engines are going to be mounted on the aircraft.

I also suspect that noise will cause unforeseen long-term issues within the engine itself.

I think that trying to impress with the “supercomputing card” at this juncture has a bit of a smell about it.

Boeing chose to go with a composite vertical stabilizer to address the sonic environment of the open rotor design in the 1980s because composite structure is inherently more fatigue resistant.

Sonic fatigue though is dependent upon the frequencies at which the noise is generated with lower frequencies, on the order of 100-150 Hz or less, having more energy to drive a structural response. Detail design can consider and remove resonant structural modes which might be excited by the sonic field of the adjacent engine.

An example of how the field has advanced is the use and understanding of the chevrons on 787 nacelles which serve to shift turbulent mixing low frequency noise, which carry far distances, to higher frequencies which do not. One will note that the 777X GE9X engine does not require the use of chevrons to meet its community noise requirements.

As a consequence of these advancements, there is a good understanding as to why the 7J7 open rotor design was particularly noisey with a very simple and almost intuitive design change addressing much of the issue.

Chevrons were a known solution that come at cost : ~1%sfc degrade.

Getting the noise stuff right without chevrons is what produces a winner.

Open rotor was assessed unde the EU’s Clean Sky SAGE, both Safran and RR taking part. Safran ground tested.

That is why I raised my question further up.

Over recent years there were seen quite a lot of media snippets from especially Safran on various OpenRotor testing.

Now GE pops up with PR that seems to indicate that _they_ own OR. Strange.

Bjorn reported on GE and Safran’s separate open rotor development projects in January 2020, about a year and a half before the public CFM RISE announcement in mid-2021. Safran was working on a 1980s-style contra-rotating open rotor architecture, while GE was developing its more unique “Unducted Single Fan” (USF) architecture at the time. The CFM RISE’s Open Fan framework clearly resembles the GE’s USF more than Safran’s CROR engine.

https://leehamnews.com/2020/01/03/bjorns-corner-why-e-in-eplane-shall-stand-for-environment-part-3/

OK, understood now.

Remember GE and CFM both studied open rotor with NASA (ERA) a decade or so ago and had a ground demonstrator looking at blade designs much improved over the GE36. Seems reasonable to assume GE cottoned on to the possibility of a stator during that work.

Safran with EU partners/money did an counter rotating UDF from a M88 engine that was ground tested a few years ago and most likely had the fan designed similar to the RISE. Noise numbers was of cause of high interest. The RISE is much simpler and cheaper to build and with longer life limits on rotating parts.

RISE blade design also likely result of the NASA (ERA) tests. But yes, trade off some propulsive efficiency for a product that has a lower sticker price for CFM to get to market, lower sticker price for the airlines, and very importanty a much better chance of hitting the ground with adequate reliability.

So far, RISE sounds like smoke and mirrors to me.

We’ll see.

This is a very interesting interview. Thanks for making it available outside the paywall.

I’ve always found that making predictions about the future of technology is fairly hazardous. Small incremental changes that combine known materials and ideas are far more likely than big leaps. And even when a major change is well along in its presentation, the purveyors and users of the legacy incrementally improving solutions are very slow to recognize it. Major investment strategies require modification, and sometimes core market values are being restacked.

The history of aviation is full of examples of highly motivated institutions getting it wrong. Perhaps the three most dramatic examples are the rejection of the Caproni C.20 monoplane before WWI, the failure of railroads to initiate airline divisions in the 1930s, and the investments in new transatlantic ocean liners in the 1950s (i.e. the France, United States, and QEII).

What is fairly easy to do is to identify unmet value needs in various markets and line then up with technologies that look promising to satisfy them. For example, it’s trivially easy to map ignored internet RFCs dealing with security with market needs for solutions in this space. They have been around for over two decades, and yet languish almost completely unused. The need is real, the solutions are solid, but driving them into acceptance and use has proven to be a Herculean, if not impossible task.

So for all of these comments about the future of aviation fuel and energy needs, economics, and solutions, my first thought is maybe.

Fokker ( when he worked in Berlin for the Kaiser) Eindecker fighters were wire braced monoplane wings plus synchronisation of the gun to fire through the propeller arc. Maybe Caproni was a bit earlier but the braced monoplane wing was probably only suited to short span low performance fighters. The biplane larger span bombers went on to be the basis for early commercial aircraft.

Getting metal wings was the next stage which Dr Junkers pioneered with the J1 monoplane prototype in 1915- which is different to a surviving metal J.1 sesquiplane ( unrestored ) in the Canada Aviation Museum

The path to “passenger safe” commercial air transport was set by Junkers with the F13 : low wing full metal airplanes.

All the double decker, canvas covered and wire braced layouts were dead ends.

The Tri-motor metal aeroplane era , which began in 1924 with Fokker ( in Netherlands this time) Junkers G24 (1924) and Ford (1925) superseded the little F13 ( 4 pass only).

The next advance was the Boeing 247 of 1934

As well as the Caproni ( prototype only) and Fokker braced wire monoplane fighters mentioned above the Morane-Saulnier N and Bristol M.1 of 1916 also had same configuration.

Not sure why its thought the Caproni configuration was ‘rejected’ by the aviation community when it wasnt. Maybe the Seattle Museum of Flight where the original Caproni ( unrestored) is displayed needs to update its information.

The actual innovator for a wire braced monoplane plus monocoque type fuselage was the Deperdussin Monocoque of 1912

Funny how when you get free money for a specific technology how that becomes the Mantra of what future tech is going to be.

And of course if you are going to bet the bank on that tech you don’t want anyone else coming up with an aircraft that does not buy it, so you try to freeze the status in place.

Of interest is the note about the fan as big as a “Similar” top a Gen9X. That is one big fan no matter how much you try to diminish it. It can’t go on a low wing aircraft can it?

As I stated before, its free money and you get a new core and a gear system out of it (the basis of a GTF)

Flip the script, P&W worked for decades on the GTF, but they had a basis for that, it was in service in small versions. You had one tech issue to solve and that was the gears. The rest is advanced but proven tech.

And now RISE is the way to go though there is not running prototypes, computing which we have had form some time magically changed the world.

But this idea goes back to the 80s and it was only put in service in one engine and that had no track history to it.

In the meantime it keeps changing and now they have found the magic elixir.

I have seen that play out repeatedly over time only to see it founder on the rocks of history.

And none of that answers the issue of people not liking prop jobs and that is what it is, a prop job.

I couldnt follow the ‘size’ comparison either .

“Even with larger blades, the open fan is not much bigger than the nacelle we have around the CFM LEAP engine today. In fact, the blades for the RISE Program’s open fan are not much bigger than the GE9X fan blades.

Compared to both size of Leap ‘nacelle’ AND GE9X ‘fan blades’

“In fact, the blades for the RISE Program’s open fan are not much bigger than the GE9X fan blades.”

Similar area covered but decidedly different thrust class 100+klbf vs <50klbf

massflow ~= area * v * “specific mass air”

thrust ~= impulse ~= massflow * dv

propulsive efficiency is inversely linked to dv.

Doesnt match the other claim

“Even with larger blades, the open fan is not much bigger than the nacelle we have around the CFM LEAP engine ‘

Im convinced the actual full size is more like the diameter of nacelle of a Leap. The previous flying open rotor didnt have blades that werent all that long, ( in an era of smaller BPR fan size) and the new version is moved from rear to front.

I think the GE9X comparison is ‘mis spoken’.

“.. “The single fan was a design breakthrough. It’s better for weight, better for costs.”..”

Is the newly-vaunted “single fan” (formerly known as a ‘propeller’) superior in net efficiency to the previous, twin-propeller design? The phrasing is ambiguous, and with the continual *re-naming that’s a hallmark of our times*, one can wonder about many aspects of the provided framing. I won’t mention this time Jevons’s Paradox, setting aside the ever-increasing complexity..

Yea it all keeps morphing and I think its pretty clear they are trying to put a round peg in a square hole and hope no one notices.

In the meantime, P&W continues its upgrades with the GTF (tech inserts) and a Pip 2 is coming out. Clearly they have wear issues with various parts but it works and works really well. P&W has a history of that unfortunately but they have got it right in the end and they will solve this one as well. Keeping in mind they have 7 major engine building partners on this and they all will be working on the bits to get the longevity they should get out of it.

An all new one aka NMA would have major changes but for existing you need to maintain commonality that you can do tech inserts for and on.

@Vincent – So were you deliberately throwing out a bone to see if the dog in me would jump on it? The paradox applies to manufacturing resources as well, provided that the product being produced is also in demand. Quite specifically, if you drive down the efficiency of manufacturing labor by cutting its quality, productivity will decline while costs soar. A certain aerospace company experienced this in spades following an event on 8-1-97.

Your comments re: organizational dishonesty have likely influenced my thinking, and the rhetorical stuff I mentioned ties in well.

“What’s its name *this* week?”

Confucius talked about a Rectification of Names being necessary at some point, and I think we’re there.

“let’s all pretend to fool ourselves awhile longer..”

@Vincent – thanks. This was hard for all of the local Boeing “graduates” and those who are still there to see happen. To give you an idea of how bad it is, I was at a local marine store last fall getting some parts for a boat trailer that I’m rebuilding. I got to chatting with one of the guys working there who turned out to be a good friend of a retired senior VP and division head. I asked if his friend had made any comments about the current leadership culture, and he immediately said: “Yes, that they are ‘quote’ a bunch of g** d**** liars.” You hear similar sentiments expressed everyplace you go around the area.

Another friend with whom I am working to start a not-for-profit dedicated to teaching music instrument mastery to the blind had a self-defined career in Boeing as what one might call the chief proselytizer on the importance of trust in any organization. The troops loved what he had to say but he was in constant running battles with managers who simply did not want to talk about it.

It really makes all of us quite sad to see what has happened.

So.. sail, or power? I was just down at the back bay this early morning, myself.

😉

@Vincent The fleet consists of two Edyline kayaks, one wood and canvas Atkinson Traveler canoe that I built, one 1933/35 Old Town 50 pounder that needs a little work, and a 1979 Lund 12 that I went a bit overboard restoring and improving as a crab pot tender (all teak seats, a lazarette, and a bunch of aluminum brazing mods to clean up the hidden sloppiness covered by the wood, repainting, etc.). The trailer is on its third life. I’m modifying it so it can haul the Lund back and forth to the beach from the Lopez house, and haul the paddle boats to other launching points around the island. It’s having all of its welds redone, new lights with metal guards, new coupler, and so on.

single stage propeller is not what this represents.

this new layout may still be seen as

coaxial counterrotating “thingies”

with the rear set of blades running at ZERO rpm 🙂

( where before rear rpm was the ~~negative of front rpm.)

one lossy feature of single stage propellers is that the exit airflow has a vortex component.

If you can fully rectify that with a set of guide vanes …

Or that since the fixed blades are downstream of the rotating blades, unlike those rotating baldes in free air they don’t receive a purely 90 degree incident flow and so mathematically can be considered to have some rotation

I don’t expect the rear blade set to be fixed but variable incidence?

Both are variable, and it is a big risk with such big rotating fan blades with variable pitch. The DC-7 had a Hamilton standard 34E60 with 168″ dia variable 4 blade pitch prop. the Connie a slightly bigger prop of 181.312″ dia. The GE9X just 134″. But having 12ea variable pitch blades on a 30 000shp engine is not that easy.

My bad choice of words. I meant fixed reference point to the nacelle. Yes, variable incidence.

There’s a lot of skepticism here but with CFM they have access to both US and EU initiatives as well as a proven track record with LEAP and 56. Yes part of what they’re doing is PR but if there’s a partnership I wouldn’t bet against it’s them. I’m excited to see what the end product is and also what it goes on. The hardest part I think will be “customer acceptance”

The word “partnership” in present-day parlance gives me the creeps. Too many tentacles.. as we will be seeing.

All the current jet engines and most of the previous ones are partnerships between the majors and minnows , usually in different countries.

Who is RR currently partnering with…?

MHI, ITP, Kawasaki and some key suppliers like GKN. The heavy Japanese partners might then caused ANA to be launch customer for 787-8,-9,-10…

@ Claes

They’re supplier partnerships –not co-production partnerships à la CFM, Engine Alliance, IEA,…

There are currently 17 humans in orbit, a new record.

Guess which country has the most?

And on that note:

“Boeing delays 1st Starliner astronaut mission again, targets July 21 liftoff”

https://www.space.com/boeing-starliner-first-crewed-flight-delayed-july-2023

pretty sad that 62 years after Gagarin and 54 years after Apollo 11 we, as a species, have never had more than 20 people in space at a given time.

I was promised moon bases and orbiting cities when I was a child. we went 4 wheeling on the moon.

at this point I would be surprised if we got back to the moon in my lifetime.

China is planning to land humans on the moon within a few years (2030) — and it’s looking at the plausibility of doing mining there.

https://spacenews.com/china-sets-sights-on-crewed-lunar-landing-before-2030/

Totally not on the main news stations because we don’t want to see / the Chinese tend to under-hype achievements, contrary to us.

Shenzhou 16 (three people) — Chinese taikonauts Jing Haipeng, Zhu Yangzhu and Gui Haichao, now aboard China’s Tiangong space station.

Shenzhou 15 (three people) — Fei Junlong, Deng Qingming and Zhang Lu, who have been aboard Tiangong since November 2022 and who are expected to return to Earth in early June.

Not any more. Four just came back down from the ISS.

Establishing a human spaceflight program is no joke. It is quite the technical achievement. China is one of only three countries on the planet that now have this capability. And with a recently (relatively) operational space station, China is making great progress.

Let’s keep things in perspective though. SpaceX has launched more people into orbit (38) than China (29).

I would like to recommend following a free newsletter called The Visual Capitalist, to this group. https://www.visualcapitalist.com/

If you go back and look at the many charts they have done over the past couple years that include a Chinese component, it is quite sobering. They are on a trajectory to reduce the west, including the U.S. into also-ran bit powers over the next century. And basically, we have done this to ourselves. It makes our lack of a coherent industrial policy that builds up our industrial capacity instead of constantly outsourcing it look absolutely stupid. Short term greed is destroying us from within.

Again, I am convinced that the solution to turning things around is to solve our “Delaware problem” with respect to the way we charter, and oversee the governance of our corporations. The Boeing situation is just one example, but a rather extreme one. We legally allow debtor stockholders to have a voice in governance so the decapitalization process that began with the merger can continue.

Our wounds are self inflicted.

Coincidentally, RR have recently run up their new Ultra Fan engine (i.e. one with all the tricks they’ve been working on recently all in one design) in their new test cell. Take a look at:

https://www.rolls-royce.com/media/press-releases/2023/18-05-2023-rr-announces-successful-first-tests-of-ultrafan-technology-demonstrator-in-derby-uk.aspx

Things I noticed were:

1) a suggestion of 10% better fuel burn than the Trent XWB. That’s quite a big improvement. XWB is a current generation engine too, so compared to older designs like the Trent 900, it’s going to be a much bigger step change.

2) they’re saying it can scale between 25,000lbs and 110,000lbs thrust. That encompasses pretty much every aircraft flying.

3) they’re saying that some of the tech will be retro-fittable to existing Trent engines. I don’t know what that means exactly, but that could mean that in the near term there’s an awful lot of RR powered aircraft that can get a useful performance boost. No idea if that’d amount to a typical PIP (a few 0.1% improvements) or something bigger.

Emirates A380s with ultrafan upgrades could be quite a thing in the market…

GE are doing PIP packages, and are betting on open rotor as the way forward for which they’ll probably need a new aircraft to put them on. Whereas RR are doing a new engine that can in principal be retrofitted, and don’t need to wait for a new aircraft design to come along. RR’s approach feels more immediately promising, less risky. GE’s approach will come with a ton of difficulty and may not really be any better than Ultrafan.

RR’s test was some weeks ago; by now, they’ve probably got a solid idea of what it’s actually achieving. I wonder if their sales team have hit the road yet?

The RR Ultrafan will not be cheap, still the biggest long range aircrafts would benefit the most, especially those with range problems (787-10) and very long ranges like A350-1000 Sunset version for Qantas. Tim Clark might want it for his A380’s. I would lock at just replace engine #2 and #3 if the wing can take it and derate engine 1 and 4 to increase life on wing.

Not mentioned in the RR press release but covered elsewhere in the media is the fact that RR plans an indefinite pause in Ultrafan development after this “initial phase” of testing, to be resumed when (IF) an airframe application develops. Retrofit of Ultrafans onto a current fleet of airplanes is not that application. Don’t hold your breath waiting to see an Ultrafan fly anytime soon.

Coincidentally or not, Andy Geer, the chief of the Ultrafan program for the past seven years, retired as of March.

Oh dear…that doesn’t sound good.

Time for AB to buy RR 😉

Sad but to be expected. RR needs to get its house in order, and are on their way to doing that with their new CEO.

Explains the transfer of Ultrafan technology talk to present products.

Hmmm, it would be a pity if after all this work they did just sit still waiting for a new airframe.

A number of the test engines, and probably the one they’ve tested recently have looked to be within a whisker of something you could bolt underneath an A380. Even Leeham have previously mused over this point, pointing out the option of slapping four underneath an A380 and calling it a neo. Emirates would probably give (someone’s) hind teeth to get them on their fleet, I’d have thought. The Trent 900 is quite old; an assumed 15% fuel burn saving on A380 operations would surely soon pay for new engines, you’d think.

It’s possible that the key battle ground now between RR and GE is persuading the next airframe programme to design for their engine. It’s quite likely that an airframe designed for open rotor would be imcompatible with a conventional turbofan, and vice versa.

For example, one can see an open rotor engine having to be mounted up high, whereas keeping a shrouded turbofan low down makes a lot more sense. If the airframe manufacturer plumps for one, that might cut out the other completely. That’s be bad news for either GE or RR.

I’d have though that the very best insurance against that risk for RR would be to get Ultrafan into service and gaining hours and operational data ASAP. A new airframe programme would then have to choose between a low risk proven engine that has delivered good results, or a complex development program for open rotor that may end up being not much better.

Another way of looking at it is if RR could get Ultrafan on to existing aircraft by any means, that may effectively block new airframe programs for a long time. GE would find it very difficult to persuade anyone to design an aircraft just for the sake of open rotor, if RR have already delivered the same benefits to existing aircraft types. After all, it’s not like A350, 787 or even A380 are hideously inefficient airframes that left loads of performance on the drafting table.

It’s possible that RR are content that, having done a test on a stand, they’ve got adequate data to make Ultrafan a near certainty for any new airframe development. But, today’s data has a nasty habit of looking slightly tarnished, if left unimproved for a few years.

Besides that, given the supply issues surrounding P&W’s GTF and the LEAP engines on A320 / 737 / A220, one would think a small version of the engine would be something worth bringing to market ASAP. RR have said they want to get into that market, so offering a product for it sounds like a good idea? Okay, that’s not going to effect existing orders for those aircraft, but there seems to be no let up in the numbers of those aircraft Airbus and Boeing can sell. If RR want to be supplying that market segment in, say, 10 years’ time, they need to have one to sell quite soon!

Having said all that, it does feel like the industry is settling down for a bit of quiet, unexciting profit making. Boeing have said they’re doing nothing new for the foreseeable future. Airbus look content to churn out A320s and A350 plus the odd A220 for a few years, let the order book cool off a bit.

Between its inception in 1996 and its end when Mulally gave up and went to Ford, the 20xx program was considered to be a highly secretive project within Boeing – so much so, that I’m guessing that fewer than 400 people had been briefed on it, and most of those were senior technical people.

In the aftermath of JAL 123, and our timid first steps in moving toward true long range planning and continuous improvement, we made a pretty big misstep in the siting of the replacement 747 structures and S&I tooling. When we realized what a horrendous mistake had been made with respect to evolving the Everett factory layout, the long range planning part really came into focus. One of the outcomes of the studies that followed was a strong belief that by mid 21st century, the basic business model for the commercial side needed to change pretty drastically if Boeing was to survive.

In a nutshell the old model was pour about 25% of the company’s net worth into a dev effort, turn the crank for five years, and out the other end would come a shiny new wonder of aviation. It would then require a production run of a minimum of 1,000 units to justify the investment.

The studies suggested that my mid this century we need to change that such that if a customer wanted to place an order for a plane we didn’t have, to take the order we would need to be able to cut the dev time down to two years or less, and the dev costs down into the noise level of continuous development. Mulally coined the phrase the “1 in 10 airplane” meaning 10 months from program kickoff to first flight for $1 billion 1996 dollars.

We had a pretty good plan for all that had to change to make some serious progress in that direction.

For high performance aircraft such as fighters, the airframe is essentially designed around the engine(s). Propulsion is way way outside of my bailiwick, but it strikes me that this discussion is saying essentially that promising propulsion options are languishing due to the unacceptably long product cycles that the airframe manufacturers are requiring. If that’s right, this would seem to be some supporting evidence for the validity of the assumptions that went into Mulally’s 20xx program plan.

Today you easily spend $1-4bn on software that can be certified for a new airliner over 7 years… Just look at the 777-9X.

@ claes OK, so this is squarely within my wheelhouse. I keep harping on the importance of competency in managing complexity. That’s shorthand for a lot of things, and we could do a whole advanced degree’s worth of discussion and writing about this topic. It’s huge.

The natural thing for humans to do is to overuse our latest hot new technologies and not use them wisely. There is solid archaeological evidence for this behavior going back at least 9500 years. That we would be doing this with computer chips and software should not be surprising.

Why does it take so long to certify avionics systems (hardware and software combinations – it’s NOT just software!!!!! – hear me pounding the table on that point)?

On the defense side of things we have a process called Failure Mode Analysis. The commercial folks like to call the exact same process Failure Mode and Effects Analysis. What you do is go through a process of documenting exactly how something works, and analyze each step and thread of steps to identify everything that can go wrong. This starts with hardware failures which end up either or both just stop working, or feeding bad data into the software.

Circa 1980 your typical least cost chips (we’re talking fab capacity, not chip type) would have up to just short of one million IC components, a little more than 25% of which would be transistors. They were arranged in similar arrays, so even though those are big numbers, it was possible for the average EE doing a design to get a pretty good handle on exactly how a given chip worked. By 1995 this ability had been lost. The number of really good top notch EEs that it took to fully understand a least cost chip was probably three or four, but you could still assemble a team in an aerospace company that could do this. By 2000 assembling such at team had become impossible for three reasons. One was the skyrocketing number of IC components (often referred to as Moore’s Law). Another was some of the amazing technologies that were built into some chips such as self healing and the still amazing Field Programmable Gate Array (FPGA). And the third was the rapid drain of top notch talent out of aerospace and into tech companies. And this is just the hardware.

The software was seeing the same thing – explosive complexity, crossing the threshold of comprehensibility by a team that can be assembled, and the talent drain out of aerospace into tech.

So the question that was squarely on the table in the mid-1990s as Condit was leading Boeing into first one really good M&A activity with North American Rockwell, and then a disastrous one with MD, was how do we manage this exploding complexity and declining talent problem in aerospace avionics? How do we even do our designs such that a competent FMA (aka FMEA) is even possible?

There is a way to do this, but it requires mature and insightful engineering leadership that understands the challenge and what needs to be done. And, that engineering leadership needs to be fully supported by the corporate and investment community. In Boeing’s case, neither of these happened, so new products didn’t work, and people got killed. It’s just that simple.

This next part will be a VAST oversimplification. What needs to be done is to use simpler IC fabs, in discrete functional modules, with tightly defined interactions with each other, so that people can isolate and understand what they are supposed to do and identify the risks that need special attention.

What has consistently happened in Boeing and in the mission avionics on the Lockheed fighter programs, is that the ability of the chip fabs to host unimaginably large numbers of functions, and software tools that can take advantage of those large numbers (we’re well into 9 orders of magnitude and more here) have been used without discretion. Thus, the engineering teams are nearly totally blind as to what is going on inside what is supposedly their own designs. And that is without adding generative AI tools into the mix.

The right answer is to work with the tech companies, probably on government funded programs, and develop a radically different set of chips and software development tools for control system applications.

As an aside, the Wikipedia definition of a control system went badly off course a few years back, so you have to be careful with it. It has a lot of good information in it, but the high level definition is just plain wrong. It talks about a relatively narrow case in which feedback loops are a defining part, and that is really only a small but important percentage of the whole topic.

Airbus is doing well with the A350 in the 777-size segment, but the A330 is not doing well vs the 787 in the one size smaller area. Perhaps the should be scope for a new “mom” WB, based on a shorter range and higher cycle design. The evidence seems to be that NB lengths are approaching the point where they at a practical limit, surely as passenger numbers continue to grow there ought to be scope for a modern-day, more capable A300 equivalent?

Some would say that A330neo’s real purpose is to depress the profit margin Boeing can get for 787s. Supposedly, if Boeing try for a fat, juicy margin on a 787 sale, the A330neo suddenly looks like the better deal overall (so the thinking goes). It’s a way for Airbus to limit Boeing’s ability to design other new airframes in an attempt to claw back market share lost to Airbus.

The counter argument is that A330neo was too little too late to retain the entirety of the A330 classic customer base when they come to refresh their fleets.

Well, time will tell. Regardless, A330neo is actually quite nice to ride on – it’s a good choice for an airline. A330neo didn’t cost much to launch either

@Matthew – Your comment almost wants to make me cry. The real revolution we were trying to create with 20xx airplane #1 (i.e. the 787) was in manufacturing and assembly. We had a plan to quite dramatically reduce the costs such that even if we sold it for the same price points as the 767, we would be making a bundle on it. But program execution was effectively sabotaged by the GE method resulting in cost soaring to a point that the dev costs will never be recovered. It really is pathetic and sad.

There is a deer in the headlights aspect to this. When you tell the folks on the current management team that they need to forget their budgets and stop worrying about making their numbers, and instead focus 100% on their quality and schedule performance they just don’t get it. It’s like you are talking a different language, which in many ways you are. That their way is exactly equivalent to institutionalized lying about performance, and that it makes profitable operations impossible, is something they can’t see, even though it is in front of them every second of every working day.

Another way of putting my previous argument is that technical improvements are just one way of effecting economies – an aircraft with greater capacity is another if the operating costs don’t increase commensurately – see A321 v A320 for example. But there must come a practical limit with NBs where loading and unloading times become excessive . With much of the industry in Europe moving to A321s, where do they go from there as traffic continues to grow? We seem to be seeing an increasing incidence of ground collisions by taxiing aircraft and I wonder if increasing aircraft lengths are a contributor to that.

“.. pause in Ultrafan development..”

that fits in badly with Airbus seemingly planning/working to reengine the A350

around the end of the decade.

That is quite a nice fleet, RTF. There are few things better than being on the water. Apologies for the non-inline reply.