Leeham News and Analysis

There's more to real news than a news release.

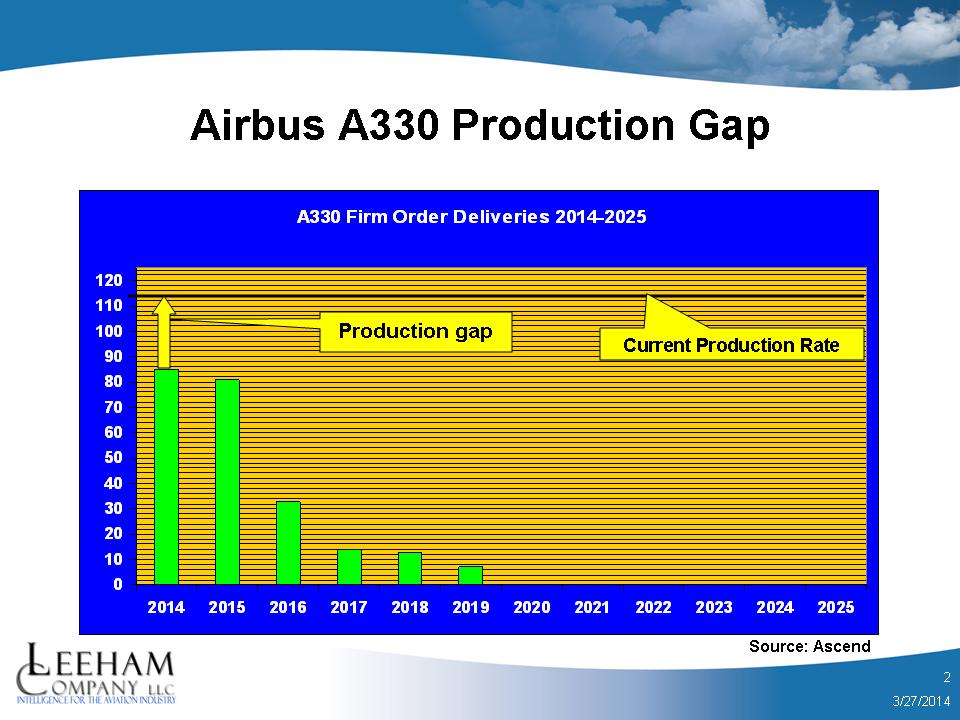

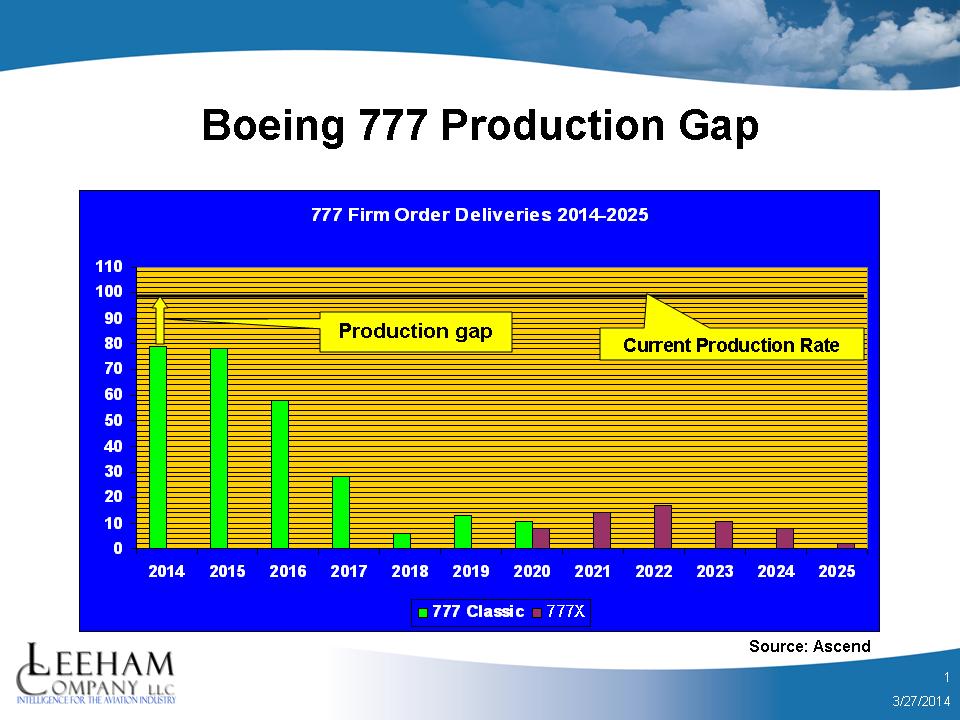

Filling the production gap for A330 and 777 Classic: huge challenge ahead

Two orders were announced this week for the Airbus A330 and Boeing 777-300ER, important for filling the production gaps of each airplane. In the aggregate, the current backlogs go through 2016, though in reality, they stream beyond that date. See our charts below.

Airbus announced an order for 27 A330s from China, but these were the airplanes long frozen in the push-back by China against Europe in the emissions trading scheme objected to by China and a number of other countries. China routinely freezes airplane orders (among other commercial deals) to express its political displeasure.

At current production rates for the A330 or 10/mo, this adds 2.7 months to the Airbus backlog, but offset with deliveries, the aggregate backlog (i.e., if all deliveries were bunched together) means the backlog ends in 2016. With the Chinese order, Airbus announced 31 sales year-to-date.

But the Chinese order didn’t include any A330 Regionals, which had been expected. Airbus announced the Regional at the Paris Air Show and the airplane is intended for the Chinese domestic market. An order for 150 was expected to be announced during the Chinese state visit to France this week. Boeing is aggressively promoting the counter-offer of two 737s for every A330 as more economical. The absence of the A330 order must mean Boeing is making a strong case.

Boeing announced an order for six 777-300ERs, 20 777-9s and 14 787s. Boeing faces a substantial production gap for the 777 Classic.

The two charts only are for firm orders, and do not include options or letters of intent. The 777X data does not include most of the commitments announced at the Dubai Air Show, because only some 30 were actually firmed up last year. The balance of the firm orders are those for Lufthansa Airlines, for 66 in total.

The data in the charts are through February.

The 777 Classic production rate is 8.3 per month, or 100 per year. The A330 production rate is 10 per month, or 115 on an 11.5 month year. Neither company has any scheduled deliveries beyond 2019/2020 of the current in-production models. The A330 includes the A330 MRTT.

Airbus has stated it wants to continue production of the A330 to at least 2022 if not beyond.

As we have written previously, neither company has sold enough of these airplanes to provide a book:bill rate of 1:1 in many years, with one exception for Boeing when Emirates splurged on 777 orders.

We don’t believe either company will be able to match orders to production, based on history, and will inevitably be forced to reduce production rates.

This is an interesting analysis but only a problem if the current production rates are maintained.

Any good business will adjust output to demand…

Precisely the point: rates are going to have to be adjusted down.

….. but to a degree the business case for buying the current generation 777 will be based upon delivery of the plane years before the 777X arrives. The closer we get to 777X deliveries the less compelling the current 777 becomes. So for Boeing to sell as many 777 classics as possible they need to maintain the current relatively high production rates.

Could be a case of who blinks first!

The recent ANA order includes some 777-300ER. Obviously those were only ordered because of availability. In growing markets there may still be some demand for delivery of A330-300s and 777-300ERs in the next years.

Those charts shows 20-25 open delivery slots in each program in 2014 (!)

How likely is filling that 20% gap in 2014 with last minute orders for immediate delivery? Time to grow desparate enough to offer rock bottom prices for Ryanair ?

How long is the required lead time for production/production rate decreases?

You won’t fill the production gap this year.

12-18 months notice on changing rates.

Build in 2014, deliver in 2015 (since you can’t stop the train fast enough). But it makes the gap even bigger for 2015.

That’s an awful long lead time for decisions. 18 months effectivly means the production rate for 2014 and 2015 is aready locked. 40 white tail widebodies? That would be a huge financial sinkhole and a risk for the whole programm.

What do you do if you’ve already produced so much ahead of time in 2014-15 that you could send your production crew on holidays for most of 2016?

You mention that Boeing must be making a strong point on 2 737s instead of a 330 since we didn’t see any regional 330 orders. How confident are you in that statement? Do you think the 330 regional orders were a done deal and supposed to be announced yesterday? Thanks.

Didn’t Airbus and Chinese sign for long term A320 production continuation at the same occasion? I think A330 vs 737 is a strange apple to oranges comparison. Bringing in the president, nucleair technology and trade deficits probably will be a more effective tactic selling aircraft to the Chinese.

Scott, what would the graph look like with the Dubai and Cathay Pacific and ANA orders and all 777x options put in place? Are there many open slots in 2020-23 for 777 sales? I know that nothing is final until the planes are delivered and cash is exchanged, but it would be interesting to see what A and B are dealing with.

Also, if the rumored 200 330regional or 330ceo aircraft order from China does not materialize do you think that pushes A to do the 330 neo?

The 777X orders/options/LOIs are, of course, from 2020–six years hence–and string out to 2035. This is so far out as to be meaningless with respect to today’s production capacity. Furthermore, Boeing, in its RFP for X, wants 10/mo capacity (vs the current 8.3/mo actual). But to answer your question directly, the highest “commitments” for orders, options and LOIs for the 777X is 40 in 2024, declining to 7 in 2035.

Finally, the issue is bridging the gap for the 777 Classic–not what the X delivery stream looks like.

WRT neo, we believe the current status of the A330 Classic, with or without the China Regional order, mandates Airbus proceeding with the neo, for any number of reasons but on fuel burn per seat the neo (by our analysis) comes within a few percentage points of the 788 and 789. Other costs have to be factored in, of course (such as maintenance, landing fees, etc) but Airbus can overcome these deficits with pricing in a meaningful way, not by assuming the absolute best in today’s Airbus presentations.

A330 NEO would do to A330 CEO what 777-X does to 777 Classic : a shot into one’s own foot. Strategic planners quite understand/accept that they can’t lay their hands anymore upon early slots for A350 so they say “too bad, we’ll take A330 CEO early up instead”. The trade-in is of crystal clarity, no need to think twice, it’s a clear-cut liberating “here and now” vs a frustrating “there and then”, the strong sales point of A330 being that there just isn’t any better alternative available before long …

Let’s now assume the A330 NEO is added to the picture … what happens ? : where before there was only two alternatives, one being out of timely reach, presently Airbus introduces a “third element” rewriting the equation to : A330 CEO vs A330 NEO vs A350 ? The middle solution is double attractive : fuel-efficient yet available early … This offering combination hypnotizes any Strategic Planner’s eyes away from the present, which as a result is made tasteless/inattractive.

Conclusion : A330 NEO will deepen the order gap in the period 2014-2018, ie, Airbus will achieve an effect OPPOSITE to the primary sales target, ie, maintaining the current throughput of the A330 CEO FAL until the A350 FAL reaches maturity.

Solution : an A330 NEO launch to be preceded necessarily by the announcement of a Chinese A330R batch, absorbing two to three full years of A330 FAL throughput ; in addition, intensify sales emphasis upon prior sales of A330F and/or A330 MRTT.

Rationale : if by the time of an A330 NEO announcement the order gap in 2014-18 has been brought down below 120 uncommitted slots, a NEO launch will be a total success, setting off a tsunami of A330 CEO ‘ricochet’ orders closing the gap to Zero

Morale for A330 NEO : it is urgent to wait !

Boeing is promoting two 737s for every A330 as more economical. The absence of the A330 order must mean Boeing is making a strong case.

Maybe China wants to find out what’s happening with the A330 Neo before ordering lots of a model that might be obsolete before it’s delivered.

That’s my thinking as well. What if they want to include A330neos instead of going all out on A330ceos. For Airbus, it would also mean a good order to back the re-engining program.

I would guess the Chinese bureaucracy is at play here and they tend to be very slow, to just behind the power curve (same with Max and NEO single aisle orders). Not in our 5 year plan, well wait for the next one (darn slots, but we have hp and can get them.

Also it may not make any difference. A bargain light A330 on the proposed short route may be more than whats needed with no real gain and delay in getting them.

And then there is the 767 light and the 777 light and the new 747-8 light.

With the Chinese I would say its a wait 5 years and the last issue will be certified and the current issue will be murky.

Really curious as to why ANA have skipped the 787-10 with this order. They were one of the first airlines pushing Boeing to launch it back in 2011.

“While Boeing has yet to commit to a launch, the Japanese airline’s vice president, Keisuke Okada told Reuters on the flight “the dash 10 is very attractive for us”. ANA, he added, encouraged Boeing to go ahead with a launch.”

http://www.reuters.com/article/2011/10/26/us-dreamliner-idUSTRE79P02Q20111026

So what’s the big deal?

There is no gap filling for the A340. Is it really a problem? I do not think so.

Therefore A330 can leave a void before the next version (A350 or A330neo) and 777 can do it too.

It seems the A340 slots were replaced with A330s on the FAL with out put steadily growing. Not a very traumatic conversion/ void it seems, unless one wants it to be.

keesje,

Are you telling us that the A330 is the a340-500/600 replacement?

That’s a very interesting concept.

Let me explain for you VV, if the gap / void is a market not served, but the production line which makes / made the aircraft in question is running at record production rates (e.g A330/340 FAL), few people will loose sleep or their jobs. If a line/ supply chain is idle for years waiting for a next version under development (e.g. 767/747 lines ‘2-’10) that is a different story.

So the “drama” of the A340 being stopped after just 400 a/c is unfortunate, but few people give it the continued attention you do for some reason. The “A340” line is spitting out 10 WB’s a month. That’s why.

That’s a bit of hairsplitting, isn’t it ?

In terms of production – yes, you could say the A340 is sort of replaced by the A330. It was a shared production line with common tooling and airbus is now using the excess capacity that resulted in the end of production for the A340 to simply build more A330s.

In terms of product clearly the A330 has not enough range to be an a340-500/600 replacement for the airlines.

In effect airbus has now splitted production from one shared (A330+A340) into two unrelated production lines (A330 vs A350) with completly different tooling. Will be interesting to see if they find a way to merge that back together or if it’s just not feasible anymore. A A330 successor that can be produced on each of two identical A350 lines would mean much more flexibility for airbus.

nofly,

That really is an interesting concept. So why did they do all the effort launching the A340-500/600?

Why did they bother to launch a new A340 model?

I would suppose because the older A340 models were growing incompetitive and they thought the new models would be the most appropriate option to counter that.

With hindsight that strategy didn’t work out, the 777-300ER effectivly killed the A340.

Same story as with the 747-8: expensive rework of an existing model, but dead on arrival because not competitive enough.

I mean, why should they surrender that market segment to Boeeing ?

More orders are alyways better, even if you could utilize the roduction line with other models.

Just because some airlines that pushed for the B-7810 and A-3510, and have yet to order any, does not mean they are no longer interested in those models. If they need a large capacity twin in the next several years, then the B-77W and A-333 are really the only games in town. The B-77X and A-330NEO will be more efficient than the B-77W and A-330CEO, but that will not make these older designs obsolete. After all they are more efficient than the B-744 and A-340 models.

And also more efficient than the 767. The 767-2C development is not so well off – 1$ billion over budget:

http://www.bizjournals.com/chicago/news/2014/03/25/boeing-tanker-project-could-be-1b-over-budget.html

On the other side Airbus did add 2 more A330-MRTT sales to Qatar.

http://www.flightglobal.com/news/articles/qatar-air-force-selects-airbus-to-supply-a330-mrtts-397536/

I also expect orders from India, France and Spain – another 20 A330.

India is in the final talks with Airbus about price for the A-330MRTTs they want to order. The competition for the Indian tanker was between the A-330MRTT and the Il-78. Boeing did not compete the KC-46.

France has already said the will order the A-330 tanker-without any competition against any other tanker.

Spain may, or may not order the Airbus tanker, but for now and the next several years they cannot afford it.

To date the A-330MRTT has only got 34 orders.

The KC-46 potentially can get orders from Israel, Poland, Brazil, South Africa, Germany, South Korea, and Canada, as well as a few others.

Actually the development of the B-767-2C/KC-46 is going well. The program is ‘on time’ or even slightly ahead of schedule and just slightly over budget. Boeing has to ‘eat’ most of the overrun costs. The total program costs of $5.85B is less than the costs Airbus and the RAAF spent t develop the A-330 tanker, and the Airbus Boom still doesn’t work. The RAAF and other Air Forces who ordered the Boom version still have not declared the tanker fully IOC. They can refuel with the WARPs but not the Boom.

You are partially right about the A-333 and B-77W being more efficient than the B-767-300ER/-400ER. But on missions of 5000 nm or less, and pax loads less than 300 the B-767 is actually more efficient. New build B-767-300ER/-400ER can still be ordered, and at bargain prices.

According to your potential KC-46 costumers:

Brazil: IAI won the Brazil tanker competition with two 767-300ER tanker conversions.

Israel: IAI will build them or the US present the KC-46 to Israel.

South Africa: SAS operates a fleet of A330/A340. The MRTT is a far better troop mover. Conversion possible.

Canada: Possibly a conversions like last time with A310 from Air Canada.

South Korea: KAL also operates A330, maybe conversions.

Germany: Lufthansa operates A330, conversions like last time.

Poland: Needs also new VIP aircraft. Only A330 MRTT offers airline seating and a cargo capability at once.

“[…] the Airbus Boom still doesn’t work”. I think Airbus will get full OC before Boeing. Singapore seems to be certain that the boom will work.

“The KC-46 potentially can get orders from Israel, Poland, Brazil, South Africa, Germany, South Korea, and Canada, as well as a few others.”

Equally, couldn’t these orders go to Airbus instead? Germany and Canada, for example , already operate A310s.

SAS does fly A-340s, but that doesn’t mean the SAAF will fly them. The SAAF is still PO’d at Airbus after the A-400M deal and it took years to get their deposit back.

The ROKAF is a long time US and Boeing customer.

It is possible the IDF orders the B-767-2C and has IAI complete them as tankers.

Thanks for the update on the B-763 tankers for Brazil.

Germany does fly two A-343s for troop transport and VIP roles. The A-310MRTTs do carry about 85 more pax than the KC-46 will, but it also carries a lot less cargo. The max fuel load of the GAF A-310MRTT is 140,000 lbs, leaving at most 70,000 lbs available for off-load.

Canada’s CC-150T (they only have two of the tanker versions) is less capable than the GAF A-310MRTTs carrying about 130,000 lbs of max fuel and a max off-load capability of 62,000 lbs.

Both the CC-150Ts and A-310MRTTs are getting old. They were already middle aged (years, hours, cycles) when they were converted.

Poland’s LOT never operated an Airbus airplane, but they did fly the B-767-300ER up until very recently. The Polish Air Force at one time wanted IAI to convert two B-767-300ERs to tankers for them, but the deal was lost because of budget reasons. Now with the problems in the Ukraine, I could see them wanting tankers again, either converted B-767s or new build KC-46s bought through the FMS program.

Yes, eventually Airbus will get the bugs worked out of their air refueling Boom. But it is not going to happen today, or even this year.

Airbus currently offers A-330MRTT new builds in two different configurations, and a sub configuration (a centerline drogue) as an option for both versions. They also offer the A-310MRTT conversion with and without a Boom. But I just don’t understand why Airbus has not considered offering a MRTT conversion to their A-340-500/-500HGW. Such a tanker could carry up to 383,500 lbs of fuel, with the current fuel system. That is about 155,000 lbs more fuel than the A-330MRTT. They could also offer conversions for the A-340-600/-600HGW that would carry more troops than the A-345 tanker, but less fuel. That would give a meaningful life for these airplanes, since they are a failure in the airline world. There are more A-345/6s available on the market than A-332s.

I expect nearly all countries you mentioned to do conversions except for South Korea. Israel is interested in KC-135R!

http://www.flightglobal.com/news/articles/israel-seeks-r-model-kc-135s-from-usa-390082/

“Both the CC-150Ts and A-310MRTTs are getting old.” That is the good thing about buying old aircraft instead of new tanker. I don’t know how much the 2 Canadian Polaris tankers are used but the German A310MRTT are still in good shape. I expect both types of aircraft to be around for 10 to 20 years more. The German A340VIP offers just 116 normal seats while the A310 offers 214.

I doubt we will see an A340MRTT conversion. Airbus would need to design a new place to fix the refueling pods. So only centerline refueling? Also far to much aircraft for most Air Forces. Maybe a good aircraft to lead a big wave of fighter aircraft other the Pacific.

Ironic that Australia axked the US for an aerial tank when they have the A330MRT.

“The 767-2C development is not so well off – 1$ billion over budget”

Huh?

The same report says Boeing continues to meet all program milestones and that the tanker program is worth north of 52 billion. Reuters also states that “Including maintenance, spare parts and replacing even more of the ancient KC-135 fleet, the value of the contract to Boeing could exceed $100 billion.” In this scheme of things, what is an extra billion in development costs, really?

Furthermore, “The total number of planes Boeing plans to build under the contract is 179.” 17 will be delivered in 2017 alone. And yet here we are looking at 2 A330-MRTT sales to Quatar and concluding that “the 767-2c development is not so well off.”

Again, huh?

The $1 billion is loss and the other figures are revenue and not gain. The other problem is called interest. Boeing offered one KC-46 for about $162 million to undercut EADS. That is less than $30 billion for all aircraft. Boeing makes profit maintaining KC-135!

https://leehamnews.com/2011/02/28/pricing-the-kc-x/

Until today the 767-2C was not in the air. I hope Boeing learned something through the refueling pod problems with Italian KC-767. The 767-2C is a minor problem. The far bigger problem is the KC-46 with all the military installations. Boeing will have no problem to deliver 17 B767-2C in 2017. I doubt you can call them KC-46.

Even the KC-46 just as a freighter would be a big relief for the C-17 fleet.

First, Boeing will not deliver 17 B-767-2Cs to the USAF by 2017. The USAF ordered the KC-46A, not the B-767-2C. They will be tankers.

Second, Boeing did learn a lot from building and testing the Italian KC-767A and the Japanese KC-767J. This experience will be worked into the KC-46A.

Third, When the USAF selected the Boeing KC-46 over the Airbus KC-45, they said the price difference “was not even close”.

Fourth, the C-17 fleet does not need relief in its cargo mission. The USAF still has more C-17s than it originally wanted. The C-17 is just one cargo airplane types in the USAF, the others are the C-5A/B/C/M, C-130H/J, KC-135R/T, and KC-10A. The USAF also has access to numerous commercial freighters for surge ops when needed. These include commercial B-747-400F/-400ERF/-8F/BCF, B-777-200LRF, MD-11F/CF, MD/DC-10-30F, B-767-300ERF, DC-8F, B-727F, B-737CF, A-300-600F, A-330-200F, etc. The KC-46A will add to this mix. But in major deployments or redeployments the KC-46 will be used as an air bridge tanker to refuel other cargo aircraft enroute, just as the KC-135 is famous for.

Finally, the USAF determined the Airbus KC-45 could not refuel the MV/CV-22, something the USAF determined the Boeing KC-46 could do. So, the KC-45 did not meet the RFP requirement to be able to “refuel all fixed winged aircraft”.

What you have not mentioned, mhalblaud, is if the KC-45 had been selected, it would not be any further along in development today than the KC-46 is. The KC-45 was a very different tanker than the KC-30, Voyager, or A-330MRTT. The USAF would have been highly critical of the Boom design and development due to its two separations and other failure modes that were not correctable inflight. The KC-45 would have had difficulty making it through the CDR.

“Finally, the USAF determined the Airbus KC-45 could not refuel the MV/CV-22, something the USAF determined the Boeing KC-46 could do.”

Lets not repeat the legendary way in which congress changed the selection criteria after the USAF fairly selected the KC-45 & the US politics exploded. What is the reason a KC-45 couldn’t refill something the KC-46. A technical reason or a smart lawyer working the documentation piles?

It was actual KC-135 and KC-10 aircrew member who determined the KC-45 cannot refuel the MV-22, not the Congress. If you are referring to the flawed 2008 competition for the KC-X, it was the GAO who determined the USAF did illegal actions in selecting the KC-45. They treated Boeing unfairly, and Gen. Lichte, who personally selected the KC-45 after he secured a post retirement employment first with NG in 2008, then with EADS-NA in 2012.

So, please stop trying to rewrite history to make your preferred OEM look like they are the victim. The only way the KC-45 beat the then KC-767AT was to cheat and offer the retiring AMC Commander a post retirement job.

http://en.wikipedia.org/wiki/KC-X#Initial_competition

“On 3 January 2008, the competitors submitted final revisions of their proposals to the U.S. Air Force.[28] On 29 February 2008, the DoD announced the selection of the Northrop Grumman/EADS’s KC-30.[29]

On 11 March 2008, Boeing filed a protest with the Government Accountability Office (GAO) of the award of the contract to the Northrop Grumman/EADS team. Boeing stated that there are certain aspects of the USAF evaluation process that have given it grounds to appeal.[30][31] The protest was upheld by the GAO on 18 June 2008, which recommended that the Air Force rebid the contract.[4][5]”

Boeing had never filed a contract protest before the 2008 KC-X program. The Congress had no input into writing the RFP for the 2011 KC-X program. There were many Boeing supporters AND Airbus supporters in the Congress. Senator Shelby of Alabama had lobbied hard for Airbus, who promised to build an A-330 FAL in Mobile, Alabama.

I think everybody followed the 3 round tanker selection, how executives had to go after round 1, how happy everybody was about the transperancy and openess of round 2, until NG/Eads won and how congress and its GOA made sure the decision was overturned. At that point NG concluded that EADS was not allowed to win. EADS stayed in to keep long term relation intact. Congress customized the requirements: cheapest offer to fullfil min. (767) requirements and extra capabilities are no more allowed to be taken into account. Everybody saw, laughed and moved on. Boeing sponsoring someone to rewrite history when details are forgotten is almost a given IMO. Not that the KC 767 is a bad aircraft, I think it will provide good value. The selection process is something folks involved are trying to forget.

With regards to the ANA A321 order, it’s a perfect fit & won’t be the last. The 737-900/ER/9 not being up to par is a closely documented example of Management by Denial on the part of the Boeing MT during the last 5 years. They obvious need to take a beating before believing.

The “757 replacement” discussion that keeps coming up is a “how to stop the A321 GTF” really. Airlines everywhere, but specially operating from hot places, are at risk ordering / converting large numbers with margins typically for a monopoly position.

http://4.bp.blogspot.com/-zakgxXZq5zE/UoOASIYsP-I/AAAAAAAAcds/9Lrncj6EIwQ/s1600/A321_DAVZU_131113gl.JPG

The Chinese today basically committed to 1000 A320s from Tianjin and I wouldn’t be surprised if most of them will be A321s.

A321 is the 80% solution to the 757, it still suffers in thrust to fill the 757 unless lightly loaded. 737-9 is too small to fill the gap, a 60% or so solution. 787-8 may or may not turn out to be the 757 replacement, but on paper looks like overkill. It may be the 20% hot/high solution on the other side of the A321 to fill the 757 niche.

The last time Boeing had a huge wide-body model changeover was when the 747-200 and -300 classics were replaced by their 747-400 equivalents. The -400’s were virtually all-new airplanes; P&WA, GE and RR all supplied engines. Anyone who was there at that time will tell you that certification of three new airframe-engine combinations was a huge challenge, but Boeing got ‘er done.

Although history never repeats in detail, there was an 18-month transition between the two 747 models. The first -400 passenger airplane was a 747-451 for Northwest, line number 696, January 1988 rollout. 747-400 EIS was a year later, in February 1989, also with Northwest. The last 747 classic passenger airplane was 18 months LATER, a Sabena 747-329 combi, line number 810, August 1990 rollout

During the transition, there were twenty-four -200 and -300 classics, scattered over fifteen customers. Seventeen customers took delivery of ninety-one new 747-400’s. Those twenty-four 747’s were probably the deals of the century.

Onward to the 777X.

Once an A330NEO is launched, I suspect that the gaps in 2017 to 2020 will be filled for Airbus on their A330 line. Alternatively, production could move to the A350 FAL from 2016 onwards if the A330 is not launched.

Boeing however, will have lean years from 2017 to 2020. One story is that they would use the spare capacity to convert 777 pax airframes to freighters. Frankly, given the different skill-sets and manufacturing facilities, I have doubts about the viability of this plan. Boeing would also have the B747 FAL to deal with as I doubt that there would be any orders left to fulfil from 2016 onwards. I can see some more jobs going at Boeing in two years time.

“Once an A330NEO is launched, I suspect that the gaps in 2017 to 2020 will be filled […] on their A330 line.”

How would the launch of the NEO make ordering A330-CEOs more attractive?

They would not, but the topic is A330 production slots, and the A330NEO definitely adds to the backlog (after 2017 when in prod.).

A330neo development is mentioned several times to be 3 years (EIS in 2017) whereas A320neo takes 5 years. Is that because there will be only one engine type on the A330neo? A320neo was considered as a derisked and simple development. It looks like A330neo is even simpler.

Does anybody know how the A330neo changes are (relative to current A330)? Thanks for the insight.

“Is that because there will be only one engine type on the A330neo?”

Most of the development work depends on the engine supplier. The A330neo with EIS in 2018 is supposed to get a GEnx2B or T1000 derivative; a derivative usually requires less work than a competently new engine as the A320neo. Additionally one engine supplier will also reduce risk.

“Does anybody know how the A330neo changes are (relative to current A330)?”

Nobody knows, we will have to wait until Airbus officially launch the program.

Yup. But bear in mind that Airbus wants to keep things as simple as possible for a potential A330neo, going by their public statements. Even sharklets aren’t a given.

Word is that the A330 Neo will also have an aluminum-magnesium-scandium frame which will reduce airframe weight by double digits percentage. Little investment will be necessary as its production will use the same tools used for the current aluminum frame. It is also mature technology used in Mig fighter jets. These re-skinned and re-engine A330-200 and 300 Neo’s will severely hurt the immature and problematic 787.

Are you sure you meant to say the “frame”? I would expect this would require some major validation and possibly re-certification work.

Now – replacing some or all of the skin panels with AlMgSc is probably way more doable; still not a purely quick-and-easy thing to do, but may just be worth the effort.

Actually, I’m not sure about the frame itself, but definitively the “skin”. I read last night that an aluminum -Mg-scandium skin A330 prototype is already being built. I will look for the source and post it later,

Apologies…see link. Aluminum- Mg-scandium A330 body panels are being built as demonstrator project. I saw the same on other links.

http://www.aviationweek.com/Article.aspx?id=/article-xml/AW_01_20_2014_p34-654795.xml&p=2

http://www.technology-licensing.com/etl/int/en/What-we-offer/Technologies-for-licensing/Metallics-and-related-manufacturing-technologies/Scalmalloy.html

A Scalmalloy, re-engined, A330 with sharklets and a few modifications here and there may just do the trick?

I can see one major difference between production of A330 and 777: the workforce. Airbus can shift the A330 workers to the A350 line. What will Boeing do? Lay off and hire again untrained workers?

I think you are missing the unique business opportunity for Boeing here.

As with the much shorter gap in need with the 787 fuselage in Charleston, they laid off the people that were gluing the operation together and created another mess.

So with the 777 gap, they could lay off thousands and then of course easily resume production the 777x came on line.

Think of it as an opportunity for Boeing management to once again show how brilliant they are. And the icing on the cake is that they can blame the union!

“whereas A320neo takes 5 years. Is that because there will be only one engine type on the A330neo? A320neo was considered as a derisked and simple development. It looks like A330neo is even simpler.”

Airbus having a 2000/5yrs A320 CEO backlog in 2010 played a role. And being extremely busy with the A350..

“Does anybody know how the A330neo changes are (relative to current A330)?”

That’s an interesting question. What can you do / what’s feasible when you have 4 yrs to EIS.. If that’s the case anyway, maybe 5 yrs is a better idea, or 3 yrs? Engines, wing pylons, sharklets, aero clean-ups (CFD motivated optimizations, belly) A340 related weight savings, A330F nose gear, new design cabin, etc. seem shoe-ins. For the rest I guess it will be case by case trade-off’s where time windows are crucial. Some ideas that were considered a decade ago..

http://www.flightglobal.com/assets/getasset.aspx?itemid=9994

keesje said om March 28, 2014 on why it takes so long to develop the A320neo, “Airbus having a 2000/5yrs A320 CEO backlog in 2010 played a role. And being extremely busy with the A350..”

I think the rationale is somewhat bizarre. Is keesje insinuating that the A320neo was launched too early?

The huge A320ceo did not require that a new version had to be launched. Secondly, if they had so much to do with the A350XWB then why on earth they launched the A320neo so early.

Basically Airbus’ rationale according to keesje was, “We have such a huge backlog for the A32ceo and we have so much work to do on the A350XWB, so let’s launch the A320neo.”

So what are those engineers doing during the first two years, turning their thumbs?

The reasoning is not very rational. So what is the irrational reason that pushed Airbus to launched the A320neo so early? We now know that a reengining can be done only in three years.

I sincerely think we still do not know exactly the real motivation behind the A320neo’s premature launch.

VV the A320 timing can IMO best be described as “BullsEye”. They have been selling 50% more and bigger NBs then Boeing since & made CSeries prospects doubt/switch. I believe anyone still claiming the NEO was launched premature is suspect to indications of adopting a very flat learning curve adjusting his/her vision to realities as they materialize.

They first deliver all the A320 CEO’s in the backlog, while certifying / ramping-up the A350 supply chain and switch to NEO certifications/ setting up the Alabama line.

“I sincerely think we still do not know exactly the real motivation behind the A320neo’s premature launch.”

Frankly I think the “we” group is limitted in size.

keesje MARCH 29, 2014 @ 1:40 AM

“Frankly I think the “we” group is limitted in size.

Well, yes I can say that I am the only one who expressed my confusion about the premature launch of the A320neo. Many people don’t even ask the question because they are hypnotized by the A320neo “order” number.

I noticed that if those order had generated predelivery initial deposit (“PDP”) of 3% it would have provided many billions of cashflow to Airbus, which I failed to trace in their quarterly earning reports. It is then easy to me to conclude that the PDP is very small, if any.

In addition, there should have been progressive PDP (based on the progression of the program) that should have been in the cashflow too. Again I failed to see the impact in their financial report. But it does not matter much, because it is not important to discuss here.

The most important point is that there are more and more conversion of the A320ceo to the A320neo when Airbus has been very clear in the beginning of the A320neo that they “would not allow” any conversion“.

The Tiger Air case is a good example for this cancellation and deferral trend. I can only suspect that the value of the A320neo resulting from the conversion would have not been very good. It looks like a mere “deferral” to me.

It looks like the rate of cancellation and conversion of the A320ceo will be increasing in the coming in the next three years. It is a clear manifestation that the A320neo was launched too prematurely, killing the attractiveness of the A320ceo when it is badly needed due to the lack of offering in the widebody long haul sector.

Today, the Boeing is delivering about 55% to 60% of the widebodies including freighters. The proportion might move again this year.

As far as narrowbody deliveries are concerned, people know that the suply chain is now under very high pressure to deliver. Those suppliers will need to invest in order to increase their production output. I am not sure that they will be able to provide enough products to Airbus even if Airbus now has four locations to assemble the A320 (Tiajin China, Mobile Alabama, Hamburg and Toulouse). The number of Final Assembly lines does not matter much if the supply chain does not produce te parts.

In addition, the unit cost of A320 assembled in four different locations could well be increaasing. It is certainly not easy to manage four assembly lines all over the world, when most of the major subassembly are built in Europe and the engines built mostly in the US. I am not saying it is not possible, but the overhead cost is certainly quite massive.

I still believe that the A320neo was prematurely launched when the A320ceo backlog was still too big. We need to monitor the trend of A320ceo cancellation and conversion (which is a disguised delivery deferral).

If A320neo cancellation and conversion rate increases in the coming months the it means that my suspicions about A320neo premature launch are correct.

Through 2013 Boeing converted 159 737 NGs from nine customers to MAX. Airbus converted 35 from two customers to neo.

leehamnet MARCH 29, 2014 @ 6:39 AM

Through 2013 Boeing converted 159 737 NGs from nine customers to MAX. Airbus converted 35 from two customers to neo.

The detail is that Boeing had not said that it would “not allow” conversion from NG to MAX.

Airbus was very clear about not-allowing airlines to convert ceo to neo, although we all knew that it was a big joke. There has always been conversion since the beginning of the industry. For the A320 it can’t be otherwise.

Now, it is indeed interesting to evaluate both Airbus and Boeing narrowbody backlog. A very simle aarithmetic was presented here http://wp.me/piMZI-3uK

VV I agree there always is a trend of converting to newer, larger versions, for a fee. Its normal. It explains why Airbus seems to be overbooking CEO slots after the NEO ramps up. I can see customers converting from CS100 to CS300 too. Wonder if that’s bad news caused by premature EIS of the CS300 too..

What is still in the air is the real EIS of the A321NEO. Maybe a similar internal discussion as around the A350-800/1000 is going on. Shouldn’t they pull forward the larger version.

I can see a similar discussion emerging in a few yrs around a 777-8X a yet to be confirmed -10X. option. The basic 777-9X is a bit heavy too. http://i191.photobucket.com/albums/z160/keesje_pics/Boeing777-10XConceptfeb14_zpsdf3d7445.jpg

“Now, it is indeed interesting to evaluate both Airbus and Boeing narrowbody backlog.”

“The detail is that Boeing had not said that it would “not allow” conversion from NG to MAX.”

The marketing department of a company can tell you a lot of stuff. IMO the real interesting case to monitor is how both OEM’s will fill the production gap during the transition to the new generation jets. The A320ceo is currently overbooked. There will be more cancellations, but airlines are still ordering new ones as well because availability is a key factor for fleet purchase decisions. I’m sure Airbus does allow conversions but we only saw 35 of them last year. Whatever the reason may be, there is not a sign yet that airlines are massively converting their CEO’s to NEO’s. As of today, it seems Airbus has secured the bridge.

Boeing on the other hand still needs to sell hundreds of 737 NG aircraft to fill the production gap, and I’m not sure how they will manage it if they keep moving 100+ NG to MAX aircraft on an annual basis.

For 2014, we already have 28 NG conversions and I bet they will end the year with another 100 conversions.

Of course, everything can change rapidly in aviation…

Seems the “GE pushing for A330NEO” story has been busted by…..GE.

http://www.google.com/url?sa=t&rct=j&q=&esrc=s&source=web&cd=1&ved=0CCgQFjAA&url=http%3A%2F%2Fwww.flightglobal.com%2Fnews%2Farticles%2FGE-reluctant-to-launch-new-engine-for-A380-A330-397501%2F&ei=p2k1U7XJI4LHqQGl8oDwCA&usg=AFQjCNEpgkWYtAvLtfZlVjLTiDRUfc1oNg&bvm=bv.63808443,d.aWM&cad=rja

I wonder who/what website it was that said “GE pushing for A330NEO?”

“Bee in my bonnet”, eh?

That is a subscriber-only link. Perhaps you could post the relevant excerpts under the fair use doctrine.

In a 26 March interview, GE Aviation president and chief executive David Joyce came close to ruling out launching a new clean-sheet engine programme.“A whole new engine is a tough ‘put’ on an A380 or an A330neo. I’m just being blunt about it,” says Joyce. Joyce says that GE is now focusing on improving the existing engine.“I’ve got more than enough platforms to create the next generation of technologies,” he says.

Well, I don’t recall ever reading that GE wanted to put an all-new engine on the A330neo. In fact, Scott previously said explicitly:

GE Aviation and Rolls-Royce are encouraging Airbus to proceed with a neo as a platform for their GEnx and Trent 1000 TEN engines. The GEnx is used on the Boeing 747-8 and the 787; the Trent 1000 TEN is used on the 787.

From your quote, Joyce isn’t even ruling out a new engine for an A380neo/A330neo – he just rules out a “whole new engine”. I don’t think anybody expected a new clean-sheet design from them to begin with.

“After taking on a series of major engine development programmes, General Electric is adopting a more cautious approach as it evaluates proposals to re-engine the Airbus A330 and A380 and replace the Boeing 757.”

Not very clear what he indicated? (757?NSA?) In his statement, for new programs in next six years already anounced are the CFM Leap ,the Passport 20 and the GE9X.

My screen saver was faster 😉 The article basically says GE (Allen Joyce) is not considering another all new engine for the A330/A380. With the GENX still young and GE9X under development that seems a bad idea anyway. Not even Airbus is suggesting / asking for it. The article suggest PW in the PW/GE AIE alliance wanted to go ahead even with a new engine, GE obviously not at this stage.

“Seems the “GE pushing for A330NEO” story has been busted by…..GE.”

Not at all. Just not an entirely new engine. They love to offer a GENX derivative.

The guy in the article says GE will not develop a new engine for the A330/A380 as they are too busy with other projects. The A330neo is however supposed to get a derivative of an existing engine, something completely different.

@Neutron73: might want to re-read the link you posted, maybe through clearer eyes this time?? Notice that he didn’t really rule out an engine for the A330neo like you’d want to believe

Regarding the NEO, word is on the street one of the nacelle vendors has been informed that Airbus is seeking bids for an A330neo nacelle. Scott, you might want to check this out.

Relative to nacelle question.

Let’s see it this way, no new engine without new nacelle, right?

On the other side of the equation, Airbus has two aircraft that badly need improvement. The first is the A330 and the other is the A380.

Is it reasonable to think that Airbus would launch a 400+seater new aircraft in the next three years? I do not think so.

In other words, the only remaining work to justify paying those design engineers during the next 4 years are: 1. A330neo, 2. A380neo and 3. new super-transporter. That’s it that’s all.

It is highly likely that the only reasonable project in the mid-term is the A330neo. Then the question is whether there is any engine manufacturer that wants to jump on board with a new dedicated engine considering the fact that the A330’s EIS was in 1994 or twenty years ago.

Someone here said that GE is reluctant to provide new engine for A380neo or A330neo. He is most probably right. However, GE would certainly willing to participate if Airbus accepts a GEnx-2B-ish engine on the A330 provided it becomes the sole engine on the A330neo both passenger and freighter versions.

For the A380neo, GE’s situation is even clearer. They can’t just get out from Engine Alliance (for the A380 application). So, it is easy to understand that GE is very reluctant to design new engine for the A380.

A brand new engine for the A380 will most likely be a Rolls Royce engine.

How can a new engine nacelle be designed for the A-330 and/or A-380 without knowing the size and thrust of the new engine? Also, keep in mind that two new nacelles designs are needed for the A-380, one for the inboard engines with thrust reversers and one for the outboard engines without the thrust reversers.

kc135topboom MARCH 29, 2014 @ 12:55 AM

How can a new engine nacelle be designed for the A-330 and/or A-380 without knowing the size and thrust of the new engine?

Maybe somebody already knows the exact specification of the engine. If the rumoured EIS in 2017/2018 proves to be true then in is obvious that they already have the engine definition now, including the size and the thrust specification.

If there is not massive order intake int he coming months and f the current production rate is maintained then the last aircraft of the current backlog will be delivered around 2016.

If my memory serves me well Kingfisher still has 15 A330 in the orderbook and there are still 39 A330 to be delivered to AirAsia X. A specific lessor, Intrepid Aviation Group, might also change its mind.

So, there are three interesting points to look at here:

1. the current A330 real backlog is about 250 units including the recent Chinese orders

2. at current production rate, the whole backlog will be delivered in two years, up to 2016.

3. An A330neo must enter into service in 2017/2018 if Airbus does not want to see its widebody deliveries part fall below 40% of the total widebody deliveries starting in 2017.

http://wp.me/piMZI-3zr

Perhaps the request is more of a ‘heads up’, so that the nacelle mfr can get back to Airbus with a portfolio of technologies that they could apply before iterating through with the engine mfr & Airbus to a finalised design. Also would help with getting some long lead operational planning and supply chain issues worked out.

VV mostly agree. The only wildcart IMO is Pratt. I don’t have a clear view of what is exactly in the GP alliance contract or how far they are with a 60-80klbs GTF engine.

BTW how is the GTF doing, is it really as quiet as hoped, how is realibility? I think in busy, small and noise restricted Western Europe this could become a strong selling point of GTF powered Aircraft. If you can fly more with GTF ‘s that’s irresistable.

Word is that the A330 Neo will also have an aluminum-magnesium-scandium frame which will reduce airframe weight by double digits percentage. Little investment will be necessary as its production will use the same tools used for the current aluminum frame. It is also mature technology used in Mig fighter jets. These re-skinned and re-engine A330-200 and 300 Neo’s will severely hurt the immature and problematic 787.

“These re-skinned and re-engine A330-200 and 300 Neo’s will severely hurt the immature and problematic 787.”

That’s a bit of a stretch, isn’t it? l can see it taking a slice of the pie but not “severely hurting” the 787.

“Word is that …”

Do you have any link for that? How much of the body structure is subject to replacement in that idea ?

If weight savings >10% really can be achieved, wouldn’t that allow to use engines optimized for much lower thrust and fuel burn?

I’ve seen a report about 3D printing to be used in the airospace industry for airodynamic improvements. Is any word about that in the street? Just wondering if that is already mature enough, or at the moment just marketing.

Apologies…they are building an aluminum-mg- scandium A330 fuselage panel as part of this potential A330 Neo project. See last paragraph of link. http://www.aviationweek.com/Article.aspx?id=/article-xml/AW_01_20_2014_p34-654795.xml&p=2.. There are others on the web.

If significant weight savings can be achieved, this is of course an area where Boeing will find it hard to respond.

I think the problem with the article is it puts all the details before the concept. i.e. disuses the orders and current and then the implication.

More actually would be something along the lines of Boeing and Airbus are going to have to cut 777/A330 production in 201X (or fancier terms but thats the idea) unless they get more orders for that periods.

Then get into the produciton rate vs the orders.

Some readers will get it and some won’t. flip it and all can see what the issue is, back it up with details to support it.

Pingback: Any "Latest & Greatest" about Delta? - Page 15252 - Airline Pilot Central Forums

No conversion allowed

This article mentions the “blocking” of conversion from A320ceo to A320neo.

http://www.flightglobal.com/news/articles/airbus-stands-firm-over-a320neo-conversion-block-355217/

Selling 2500 NEOs and hundreds of CEOs it seems Airbus was successfull in preventing conversions. Able to back up its announcement better then some other OEMs, agree?

keesje MARCH 30, 2014 @ 10:40 AM

“Selling 2500 NEOs and hundreds of CEOs it seems Airbus was successfull in preventing conversions”

I do not know keejse. Perhaps the cancellations and conversions have just started.

Let us watch closely A320ceo cancellation and conversion rate in the next two years. There are more and more rumors that many of those orders are not as firm as they are supposed to be.

It really is a pity that Airbus does not differentiate the orders for the A320ceo and the A320neo in its orders and deliveries spreadsheet.

Fortunately, http://pdxlight.com provides a good bookkeeping of A320neo orders.

Deferring deliveries seems to be not that uncommon, generelly speaking. So ordering end of line models effectivly means loosing any flexibility to defer your deliveries. Is Boeing handling that any different? (I doubt it)

Deferral and cancellation are absolutely normal and it is a very healthy reaction.

However, the case of A320ceo is of particular interest. As we know, the A320neo was launched in 2010 when the A320ceo backlog was at a whopping 2,200 units.

The A320neo put an “upper bound” to the A320ceo’s life. Just think about it, the A320neo is supposed to provide at least 15% of fuel burn improvement realtive to the A320ceo. Fifteen percent of fuel burn economy is equivalent to about one million US$ per year and per aircraft. In an A320’s life time it would represent about fifteen million US$. So, it is obvious that the A320ceo will not be able to survive the assault of the A320neo. Any airline CEO who accepts to take delivery of an A320ceo starting in 2015 is simply irresponsible.

Obviously, many more A320ceo will be cancelled and some will be converted to A320neo despite the hopeless “no-conversion-allowed” request from Airbus. It is simple,if it can’t be converted then it will be cancelled.

The fact that Airbus have allowed some limited cancellations of CEOs with conversions to NEOs suggest to me that it is a way of keeping customers who are desperate for new aircraft, and willing to take CEOs, happy by freeing up earlier slots. The fact that there have been relatively few cancellations and continuing sales for CEOs suggests to me that availability is an important issue, and that anyone cancelling their CEO slots is looking probably six years beyond their CEO delivery date before they get their aircraft. So taking a CEO in 2015, if it is possible to make money with it, is not irresponsible, it is being pragmatic.

With Airbus launching the NEO when they did, they already had most of the orders to fill the production gap till the new version came out, but they must have been pleased by the seeming ease with which they have sold the remaining CEO slots. I imagine it’s a lot more of a problem for Boeing, who despite their similar backlog have a further year+ of NG production to sell.

Roger,

I regret that Airbus does not make any distinction between A320ceo and A320neo orders in their orders and deliveries spreadsheet.

Boeing has a specific entry for the 737 MAX, although it does not make the distinction between the different MAX versions. The distinction between NG orders from MAX orders is more than enough.

It would be interesting if Airbus starts to make the separation between A320ceo and A320neo in their spreadsheet. After all, the A320neo is so much better than the A320ceo.

Perhaps it is done on purpose to hide any “cooking” inside the backlog.

“Any airline CEO who accepts to take delivery of an A320ceo starting in 2015 is simply irresponsible.”

I guess you should inform the CEO of Delta Airlines, the airline ordered 30 A321ceo’s last year with delivery to start in 2016. Those guys are obviously deluded 😉

Some notes on nacelle commonality-

– The original A300 had CF6-50 engines; it used the same nacelle as the DC-10.

– the 747-8’s GEnx has bleed air, so it should be suitable for the A330NEO. 747 rating is 67,400 lb SLST

– the A330ceo’s GE CF6-80E1 is rated at 72,000 lb SLST. But the NEO will less fuel = lower MTOW so maybe the 747 engine’s lower rating might be enough. If not GE will have to adapt one of the larger fan diameter 787 engines for bleed air.

The 787-10 will need about 76 klbs, so I guess GE will come up with a GENX solution.. as will RR.

The 777-8X & -9X carry more passengers and fly farther than the 777-300ER with the same MTOW, 775,000 lb. Their GE9X engines are rated at 105,000 lb SLST vs the 777-300ER’s GE90-115B at 115,000 lbs.

Unlike the 777X, the A330NEO will not have a new wing. However, new engines plus sharklets may yet allow the same payload range at a lower thrust rating and MTOW. Let the Airbus aero weenies work their magic and we shall see.

Is that a fact? Last I read it was 102klbs. Is their an official GE/Boeing release that states otherwise? Otherwise, lets leave the guessing to the Fan-boy and amateurs.

VV in you latest blog I saw your analyses on the big twin market segment:

“As of today, the 787-8 and 787-9 don’t have any direct competitor and the recently launched 777-9 won’t have any competitor either. Clearly the A350 strategy has been a failure.

I repeat again that there is no way Boeing will become too dominant in the long haul segment. It is forbidden by the rules. In other words, Airbus can live in peace, they are protected.”

An interesting conclusion. Some have the opinion Boeing has been dominant in the long haul segment for ages. And it seems to me the A350 has done well. I think a backlog of 825+ before EIS among the big 777 operators seems nothing to sneeze at.

Yeap, 825 orders, including the 50 or so A-358s. We all know Airbus will not build them, and has been pressuring A-358 customers to buy the bigger A-359. Not all have taken that bait. US and Hawaiian are two hold-outs.

The B-787 had 900+ orders before EIS.

Boeing has dominated the WB and long haul market for decades. Airbus competes with the A-300/-310/-330/-340/-350/-380. Boeing has the B-747/-767/-777/-787. I’m not counting anything from the former MD. Boeing’s original long haul airliner was the B-707.

KCT agree, however it seems the US A350-800s have been converted & you’ll probably see them pass by in the near future.

http://3.bp.blogspot.com/-lKsoU1WC6PE/Ur4OV-1iMWI/AAAAAAAAKxg/XmZuFyOP0-w/s1600/image.jpg

Hawaiian is interesting, the A332 seems just right sized and the A350-900 on the large expensive side. They are in a good position it seems, they have got A330s / time, Airbus will bow deep to keep them and Boeing will bow even deeper to snoop them away with 787-9s..

I believe HA still has some 4-6 A-332s scheduled for delivery this year. They have about 6 options for the A-332. Their A-358 order is 6 firm plus 6-8 options, IIRC. The A-332s and A-358s are scheduled to replace the remaining 15 B-767-300/-300ERs still remaining in the HA fleet. What they are looking for is a 300 seat airplane. Both their B-767s and A-330s have about 300 seats.

If Airbus tells HA they will not build the A-358, HA has these options:

Firm up the 6 option A-332s, shifting the A-358 deposits to these A-332s

Find used A-332s on the open market for sale or lease

Order new build B-767-300ERs

Order new build B-788/9s

Find used B-767-300ERs on the market for sale or lease.

Order new build B-772/E/3/Ws (even though not offered, Boeing can still build the B-77E/2/3)

Find used B-777s on the market for sale or lease

Convert their A-358s to A-359s

HA only needs a 300 seat airplane with about 5,000-5,500 nm range.

Since HA has not taken any of the options, above, for Airbus products, I can only assume they are demanding price discounts and production slots for the A-359. I will not assume HA is PO’d at Airbus because HA has leverage to force Airbus into making a deal. Airbus either has to build the A-358, or break the contract, or make an offer that HA wants for new build A-332s or A-359s, even at a huge loss.

Thanks for the update on US converting their A-358 order to A-359s.

Topboom, haven’t you left out the A330 NEO option for HA?

That’s a strange coincidence.

I have just posted another entry that you will certainly appreciate.

http://wp.me/piMZI-3zX

Observer, it was not guesswork: the thrust ratings are from Wikipedia:

http://en.wikipedia.org/wiki/Boeing_777

Amateur? Not after 42 years in commercial aviation.

The pejorative “fanboy” – there are many more positive ways to express disagreement

105,000 lbs or 102,000 lbs? either way the 777X’s will have lower-rated engines than the -300ER

“Is their an official”. ???

VV

“The plan (the “A350 strategy”) was to compete against both the 787 and the 777. We today observe that the 787-8 and 787-9 are still without any credible contender. The 777-9 will virtually be in a monopoly in the 350-400 seater segment.”

787 with credible competitor? What about the 800 A330s sold since 787 launch? Replacing 787 orders with e.g. VS, DL and the Chinese? The A350-900 and A350-1000 are in the centre of the segment. Capacity /CASM wise the 787-10 is a good competitor but it simply lags payload-range. Payload-range wise the 777-8i fits the bill, it’s OEW/CASM hurts though.

So Boeing might be absolute right in claiming the A350 has been “boxed in at the top”, just not by competitive platforms. That’s an issue you need to monitor and sales confirm it.

LH, EK and QR have not been cheering the 787-10.

http://www.bloomberg.com/news/2013-06-18/emirates-chief-says-boeing-s-dreamliner-stretch-may-be-too-small.html

http://blogs.crikey.com.au/planetalking/2013/06/30/qatar-ceo-critiques-787-10-unfavourably-but-he-does-that-to-everyone/

LH: “The 787-9 is too small for our requirements and the 787-10 does not have the necessary range for around 40% of the destinations,” says Carsten Spohr, CEO of the passenger airline division.”

keesje MARCH 30, 2014 @ 1:58 PM

“LH, EK and QR have not been cheering the 787-10.”

Very true, but you forgot to mention that all three airlines ordered the 777-9/-8.

The situation is a little bt strange for the A350. The biggest “family” member will have to grow bigger and the smallest one is in limbo. Perhaps it is just a question of product positioning that has been properly done.

I do not think the 777-9 will sell as many as the 777-300ER have done so far (more than 7000 units ordered), but I do think both the 777-9/-8 will exceed easily 600 orders in the next twenty years. If my memory serves me well, it already got more orders and commitments in 2013 alone than the the total order tally for the A350-1000 since 2006.

As I mentioned in my last blog entry, I think the launch of 787-10, 777-9 and 777-8 in 2013 will slow down future A350’s sales.

In addition, there is not so many available slots left in the A350 production (unless if those orders are not all firm as they are supposed to be, meaning there will be many overbooking).

Will Airbus be able to ramp A350 production up quickly to ease the slot availability?

I do not know, but considering the fact Airbus thinks building three batches of A350 proves that there are some issues ramping the production up.

“LH, EK and QR have not been cheering the 787-10.”

Very true, but you forgot to mention that all three airlines ordered the 777-9/-8.

You forgot to mention they ordered A350s too, -1000s even. The EK “order” seems to have been a marketing “commitment” sofar.

“Will Airbus be able to ramp A350 production up quickly to ease the slot availability?”

I guess that will be a challenge, they stumbled there with the A380. An entirely new “black” supply chain / infrastructure has been set up. The program is moving ahead better then many analysts expected, so lets hope for the best.

IMO Boeing lacks a competitive 350 seat long haul aircraft, to replace the successful 777-300ER. Crushing 400 tiny seats in a heavy 2020 artist impression and say now you dominate long haul, just aint gonna cut it. The easiest solution for this gap IMO would be to re-wing / stretch the 787 to give it real 350 seat / 8000NM capability. Good chance Boeing is already working on it.

The A350 family is pretty much like an up-gauged A330 family to me, designed to sell well within its own space instead of going head on with a single competing family.

The A330 has been doing pretty well against the upper end of the 767s and the lower end of the 777s. Likewise, the A350 is positioned to go against the upper end of the 787s and the lower end of the 777X.

As to what happens to the A330? It could become the new A300! 🙂

So in a nutshell, I don’t see a major change in the widebody strategies. It’s just that they all moved upwards in capacity in unison.

Boeing needs three 787 models and two 777-x models to box in and compete with the A350. Now who has the best positioned aircraft?

Joe MARCH 30, 2014 @ 3:24 PM

“Boeing needs three 787 models and two 777-x models to box in and compete with the A350. Now who has the best positioned aircraft?”

That’s a very strange question. In reality, Boeing proposes those different versions to satisfy airlines’ needs. Airlines have different needs according to their business model.

I invite you to read one of my past posts in which I explained my suspicions on how Boeing would try to “lock the grid” using its very simple product strategy. The blog entry was posted in August 2009.

Please read the last paragraph, in which I wrote,

“Once the grid is locked, there will be many other things to do like the “Ultra Long Range” niche aircraft like the 787-8-ULR and the double-hypothetical 777-8-ULR. The 787-10 can also be built as a medium range high-density aircraft. But we won’t see these aircraft anytime soon.”

It seems that things happen much faster than I anticipated back then in 2009.

Here is the link: http://wp.me/piMZI-h6

I agree, but the same goes for Airbus. They can also extend range or derrate engines. Remember that the initial intent was to build an A350-900R with a range of 9500nm. Rolls Royce still lists this aircraft on their website with regard to engine development. Similarly, any of the other Airbus models can undergo the same the transformation as any Boeing aircraft and vice versa. The A380 can be stretched as can the A350-1000. To me it seems that the A350 as afamily of aircraft is positioned closer to the sweet spot.

“That’s a very strange question”.

I don’t think so. It doesn’t synchronize with Boeings slides though.

“In reality, Boeing proposes those different versions to satisfy airlines’ needs. Airlines have different needs according to their business model.”

In reality Boeing does not have a competitive 300-350 seat long haul offering. Boeing will never admit but reality in sinking in with sales telling the story & airline CEO’s being vocal about it.

Airbus grabbed UA, AA, JAL, BA, SQ, LH, AF/KL, EK, QR. -> panic.

The 787-9 seems an excellent spec but is on the small side. The 787-10 seems right sized (if 17″ seat / 14 hr flights are ok) but lacks the wing/range to carry heavy cargo from Asia. And the 777-8i seems the new 777-200LR, very capable, heavy, expensive and (too) late (2021) to the table.

There is a problem, 300-350 seat/ 8000nm is the center of the segment. I think Boeing is back to the drawing table. Or should be. Probably looking at a 350 seat / 8000NM 787->wing.

Airbus has excellent aircraft planned in the 315-350 space (350-900, 350-1000). They are optimized there. The issue is that the 787-9 (280) is optimized, the 777-9x (380+) is very competetitive/optimized (if you can fill it) and the 787-10 (323) is very competitive/optimized if you don’t need the range (as most routes do not). The 777-8x (350) is a niche aircraft.

So Boeing can compete in Airbu’s optimized space (315-350), but Airbus doesn’t compete very well in Boeings optimized spaces (375). Airbus will sell every 350 it can make to customers who are in that 315-350 seat area. It needs to look at the 280-300 seat and the 365-400 seat market. Hence the 330neo or the putative -1100…

You seem to agree Boeing can only offer the range restricted 787-10 and niche 777-8i were the bulk of the market is.. If an airline/its passengers think 17inch seat width is too narrow for 10+ hour flights redo the numbers..

The biggest 777-200ER/300ERs operators massively switched to A350-900/-1000s. A switch from B to A in the 300-350 seat long haul segment has already taken place. Chicago seems in denial, talking “boxing the A350” but what else can they say..

Many more 777-200ER’s and A340s up for replacement in the next 10 years. Will operators scale down to 787-9s? Introduce heavy 777-8i’s starting 2021? Take 787-10s and leave cargo behind at the platform?

Sorry, 365

It depends onif the 315-350 space is “the bulk” of the market. Again, Airbus will sell all their 350 aircraft. But if the airlines need a >350 or <315 seat aircraft then what can Airbus compete with in the future? The 330 neo is a short term solution.

The 787-10 is competitive with the 350-900 and will be long-term. Some airlines will need the range, others won't. Every one that Boeing sells is one less 350-900 for Airbus.

The 787-9 is optimized (280 seats) and will be for the foreseeable future. The 350-800 is not competitive (current iteration), hence it will not be built. The 777-9x is near optimized, but faces no challenge as Airbus has no entrant (as of right now).

IMHO, it makes sense for Airbus to:

1. Get the 350-900 out and ramped up (315 seats) (2015-2017)

2. Get the 350-1000 out (350 seats) 2017-2018

3. Optimize the 350-800 (275 seats) 2019-2020

4. Launch a 350-1100 (380-400 seats) 2021-2023

If they need more time, then neo the 330 but realize that you will have a shorter run than you would like (say 5-7 years) until the 787 backlog is worked through. Boeing's only response I think would be a 777-10x to go to 450 seats or so…

Airbus is going to be fine if you want 315-350… it's above and below that is empty. And Boeing has entrants in the 315-350 space that are competitive.

The A350-1000 is competing with the 2.7m longer 777-9X. Because it is yrs earlier in the market and 20t(!) lighter. The 2-3 extra seatrows on the 777-9X are payed for heavily.

McNerney, Conner and Tinseth looked each other deep in the eyes and decided the passenger will accept 12-16 hours in a 10 abreast 17 inch seat. Now for the real thing..

According to wikipedia all airline customers of the 777-X have ordered the A350-1000, too: Lufthansa, Cathay Pacific, Emirates, Qatar.

I think at the moment both aeroplanes are in fact complementary. If you need the range, you take a 77X. If not, the A350 will be more economic.

Will be interesting to see if 10 abreast will be widely accepted by airlines as the new standard on the 777X. For now I think for most pax best-price is really the only booking criteria.

787-10 vs 350-900 is a similar picture.

Now think 10 years ahead. The A330 grew over the years in range by PIPs. Could the 787-10 and the A350-1000 do the same? For the A350-900 and the 77X there is no headroom they could grow into with more range. Both already have all the range that’s realistically needed. That would effectivly kill the 77X. The A350 programm would be less impacted, demand would simply shift to the larger variants A350-1000 and (future) A350-1100.

The A330 was in a relatively unique position. It had a massive range boost built into it as it shared a common wing and structure with its longer range sister, the A340. I don’t think the 787-10 can get that kind of growth without significant design changes as its wings and structure is already at the very edge of its limits. Think how many other twins got the same kind of boosts in the manner that the A330 did. So, it’s not easy.

If, and I accept its a big if, the scandium and whatever panels offer a yield a significant weight saving and the A330 NEO gets engines to match the 787s then the A330/787 gap could be closed.

The best an A-330NEO can do would be to (possibly) narrow the gap between it and the CURRENT version of the B-787. The A-330NEO crowd does not seem to acknowledge Boeing is capable of PIP and aerodynamic improvements, as well as PIPs done by GE and RR to the GEnx and Trent-1000 engines.

Boeing is going to maintain the B-788/9’s economic operating advantage over any A-330NEO.

KCT agree the A330NEo will never have an engine advantage for long. IF GE or RR comes up with a better engine airlines will demand it for 787s too. Specially because 787 is dual source with a fierce competition between RR and GE. However the A330 is a 25 yrs old design & many improvement opportunities exist as technology has moved on & A340 was deactivated. The 787 design is just 10 yrs old so less opportunities at this stage.

The 787 “economic operating advantage” is a big question mark for me. Yes it was advertised and the 787 is 15 years newer design. But has maintenance proven cheap, I doubt it. The A330 has a world wide competing maintenance and support network with 1000 in service. Hard to beat IMO.

Many have claimed the 787 to be 10-12% more fuel efficient then the A330. Now that GE& RR claim they can offer 15% more efficient engines for the A330. Airbus can reduce weight, ad Sharklets, optimize fselage lenghts etc. it has been become very quiet at the analyst side.. Better avoid calculations if you feel you might not like the results. The more opportunistic ones quickly (will) move the goalposts stating the 787 is 20% better then the A330 really.. Did that with the MAX.

IMHO, the A350-1000 will end up replacing many more 300-ER’s than any 777-x model. If airbus does build the A350-900R as originally intended (R for range) with a range of 9500 nm, the 777-8 will have a fierce lighter competitor in that niche market. That ultra range A350-900 as previously described (wings and engines of the 1100) would be easy and quick to develop. Personally, I would love to see this aircraft be built.

That’s funny considering it hasn’t replaced too many as yet, and the 77X shows up and in less than 1 year, nearly beats A351 sales since 2006.

I think Airbus is considering a A350-1100 because the A351 has not turned into the “77W Killer” they claimed it to be, and the 77X has them covered on top end.

The super twin concept looks very interesting, though

The A350-1000 proved to be a 777 killer.

Ask BA, JAL, EK, CX, AF, UA, Qatar. LH, AA, SQ and ANA are not out sight either.

The Emirates 777X order has still not materialized after 5 months & nobody is asking questions. What going on?

Correct me if I’m wrong but if the A351 is killing the 777 program, why do 4 of the 6 carriers you mentioned who ordered the A351, still have 777’s coming off the assembly line AND have placed order for the 777x? (EK, CX, QR). More interesting is that LH chose the 777x over the A351 when they knew the -1000 has earlier delivery slots.

If AA doesn’t need anything bigger than the 77W for at least the next 12-16 years. SQ is rumored to be negotiating for 40 777x’s despite the 350’s they have on order and the 777’s they have coming to them. NH just opened up their checkbooks for Boeing widebody’s so the introduction of the A351 is unlikely but hey they still might order the A380 too right!?! Lol

In a nutshell, the A351 is not killing off anything. What can be said is that the 777x is slowing down the A351 in terms of momentum and order tally.

I wouldn’t be too concerned about the QR/EK order. It’s taking longer than usual. No biggie. China just freed up 330’s they ordered many moons ago. Airbus finally got the order. Both sides shake hands. All is well. Get it?

“In a nutshell, the A351 is not killing off anything”

“All is well. Get it?”

Wake up & smell the coffee.

http://i191.photobucket.com/albums/z160/keesje_pics/A350XWBcustomers_zps927fbabd.jpg

Hey sorry it took me so long to respond, I was too busy not taking comments from others personal and not getting my EADS bloomers in a bunch. Seriously Karel …. Back to topic though.

That link you posted contained graphics of airlines who ordered the -900 and the -1000. Since your statement was regarding the -1000 your graphic is off by 3 carriers. Those 3 being AA/US, LH, and AF. Also I’m not trying to be confrontational, just factual and unbiased. If you can present a better argument why and how the A351 is killing the 777 program I’d love to hear it.

Lufthansa says they have A350-1000 options, and have little doubts Airbus won’t be angry if AA or AF upgrades. Probably included in the contract. Must let know .. months before delivery. Rotate you are totally right pointing out the -1000 vs -900 commitments, even if they’re of limitted value.

http://www.reuters.com/article/2013/09/19/lufthansa-fleet-a-idUSL5N0HF1JU20130919

There’s no need to prove the A350 is taking over the market segment currently dominated by the 777. Just observe whats happening at the worlds biggest network carriers; EK, QR, Ethihad, AF/KL, BA, LH, SQ, CX, AA, UA. Watch Korean, DL and even ANA. What will they replace their 300 seat 772ER fleets with? 777-9Xs?

Chicago, we have a problem..

@Rotate: Weren’t you the one who said the A350 wouldn’t get more orders beyond what it had sometime ago, after which the plane has racked up a few orders? Clearly you speak from something, not sure if it’s from your nether regions or from your head. Still waiting to determine that.

Bryan,

[Edited] I said that the a majority of the carriers who already ordered it probably won’t place more than what they already have plus or minus few top up or option exercises(+,- 100). Furthermore this, ( your meaningless banter) has nothing to do with what Kesseje and I were conversing about. Good day.

No, you actually said it wouldn’t be getting more orders give or take a few the ones it already had, pity I can’t be bothered going back to find it. And yes you’re right, it does have nothing to do with what you’re saying, but it does show that your posts probably shouldn’t be taken more seriously than the inane ramblings it is.

Neutron73, can you prove your impression that 777-300ERs are replaced by 777-Xs with concrete orders?

Most 777-300ERs are still young (EIS 2004). I doubt any are up for replacement yet.

The A340 and 777-200(ER) are older and more likely to be replaced in the near future.

I believe Tim Clarke has mentioned that the 777-9x will replace earlier 777-300er aircraft in his fleet. Emirates turnsover aircraft at the 12 year mark I believe.

Correction, the A350-900 R (not regional) is estimated to have range of 10,300 nm. Awesome on paper but likely not needed.

10,300NM is an extreme city pair you wouldn’t develop an aircraft for. The interesting part of such an aircraft (777-8i also) is you can load a useful amount cargo on e.g. 14 hour / 7000NM flights with reserves.

Kessler wrote —>

Lufthansa says they have A350-1000 options, and have little doubts Airbus won’t be angry if AA or AF upgrades. Probably included in the contract.

While this is true, LH could exercise options on Boeing orders too. Say the 748? 777x? It goes both ways.

I doubt there is a problem in Chicago. I think you know like I know if a carrier wanted to replace a 772 ER it won’t be with a 777x. Perhaps the 787-9? I see your list of carriers in your reply and yes they are big network carrier’s but I don’t have time to go over each one and disect each one and expose where you may or may not be wrong. IE NH just ordered more 787-9’s and you think they’ll order an Airbus widebody to replace their 772’s? Come on.

http://airchive.com/blog/2014/03/28/ana-order-analysis/

ANA, we will have to wait. Do you think ANA will scale back and replace 777-200ERs with smaller 787-9s on Europe and US for the 2017-2037 period ?

“While this is true, LH could exercise options on Boeing orders too. Say the 748? 777x? It goes both ways.”

Except they say they will consider the A350-1000 and they won’t take more then 19 747-8i’s I wonder if they will take all 747-8i frankly. They had some negotiating power, Boeing badly needed them to order 777X’s.

http://www.aviationweek.com/Article.aspx?id=/article-xml/awx_06_03_2013_p0-584172.xml

Looking at the current portfolio’s and recent sales trend I see Boeing coming up with a (or two) bigger 787s). Probably with a 10-15% bigger wing to cater for more range and lift. To match the A350-900 and -1000 XWB.

The 787-10 and 777-8X aren’t capable/efficient enough for that.

http://i191.photobucket.com/albums/z160/keesje_pics/787-10.jpg

There is a little difference between these two options. Lufthansa has the option to decide either to buy the A350-900 or the -1000. The other option is to buy more aircraft. There are 9 B747-8i left for delivery to Lufthansa. The only option left is the 8F. Why should Lufthansa downsize from the 777-9X to the 777-8X?

The seat mile cost calculation in that link is interesting.

They claim a typical set count of 300 for the 77X.