Leeham News and Analysis

There's more to real news than a news release.

757 replacement not in the cards any time soon

The unexpected attention earlier this month on the prospect of a Boeing 757 replacement, possibly in the form of a 777X-style concept of composite wings and wingbox, new engines and some system upgrades, brings into focus the Boeing 737-9 and the Airbus A321neo.

- Aspire Aviation has its analysis of the next New Small Airplane here.

Boeing quickly denied, in an unusually firm manner, that it was planning on a “757 MAX” and reiterated it doesn’t currently plan to bring another new airplane to market until the middle of the next decade. We’ve previously reported that based on our information, Boeing will wait until the 777X enters flight testing, estimated for 2018, before launching a new family of airplanes to replace the 757 and 737 MAX—with entry-into-service of the 757 replacement around 2025 and the MAX replacement about two years later.

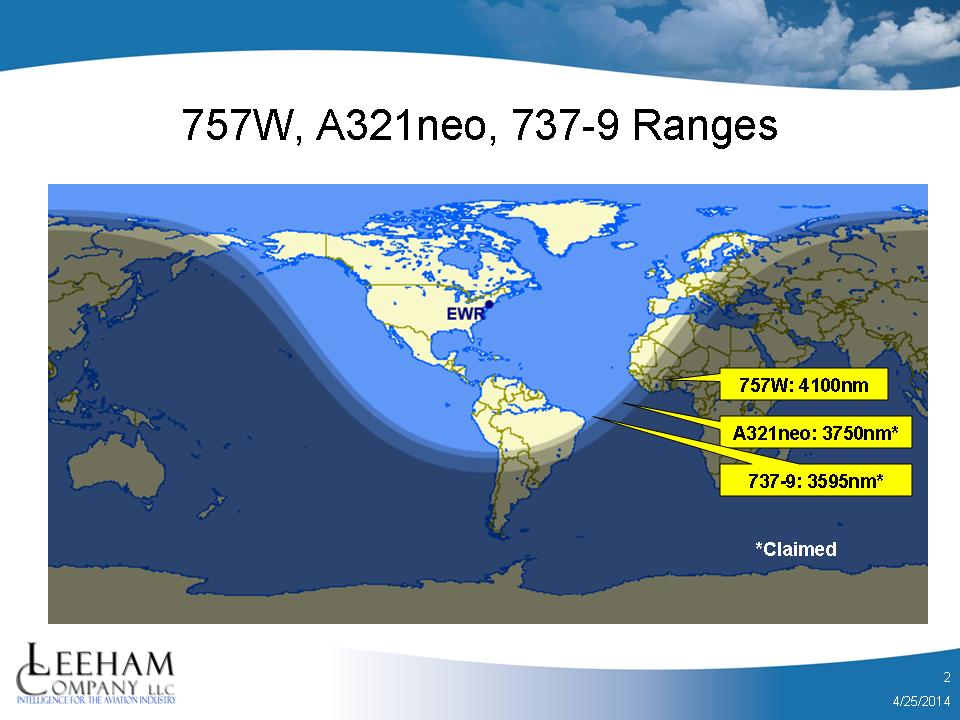

We expect the low-end airplane to start around the 162 seat mark, which is the 737-8/800 size today, and the high end to be around the 240 passenger size in dual class configuration. Top range would probably be around 4,100nm, about that of today’s 757W.

Today’s “757 replacements,” as touted by Airbus and Boeing, are the A321neo and the 737-9. However, neither matches up to the 757W. Airbus and Boeing officials each acknowledge the next generation of the venerable A321 and 737 families will cover only 90%-95% of the 757’s missions today. (Airbus claims the A321neo can go 98% of the 757W’s missions.) This goes to the heart of a recurring dilemma: do the OEMs design a plane for that last 5%-10% or are they satisfied with the heart of the market?

According to our sourcing, Boeing believes the “true” 757 market potential is about 1,200 airplanes—not enough to split evenly with the competition to provide a reasonable return on investment. Thus, this means a 757 replacement needs to be part of a family of airplanes.

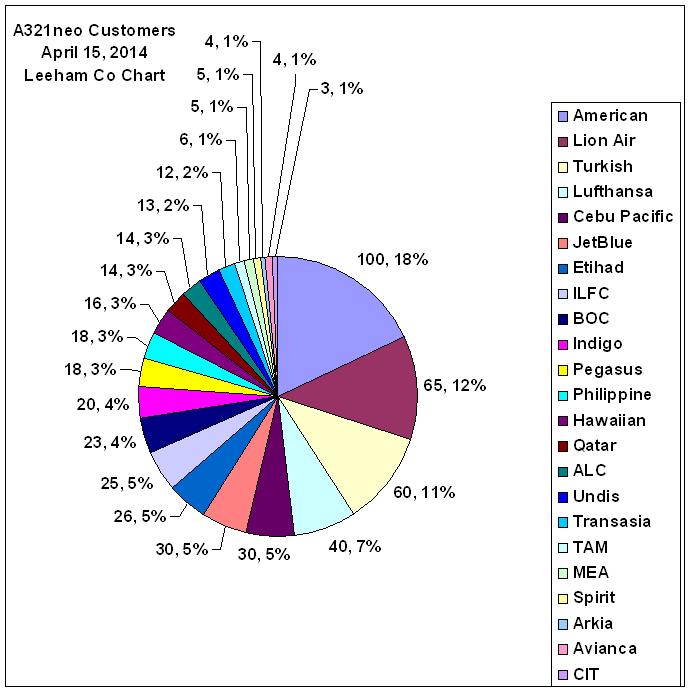

Airbus and Boeing have already sold roughly 1,000 A321neos and 737-9s (see charts). We pumped up the 737-9 order by assigning all 201 Series TBD of the 737 MAX order for Lion Air to the 737-9. All but a handful of the 737NG Lion Air orders are for the -900ER, with the others for the -800, so we believe the LionAir order will largely be for the -9.

However, the customer base for the 737-9 is highly concentrated. 73% of the orders are from just two customers: LionAir and United Airlines; another 7% are with lessors. There are just 10 identified customers for the -9. (Bombardier has twice as many for its CSeries, though only half the firm orders.) Boeing’s Unidentified 737 customers are presumed to include 737-9s, but absent information we can’t assign the sub-types.

Airbus has 22 identified customers, plus an unknown number of Unidentifieds, for more than 500 A321neo. Customers often are listed as ordering the A320 and later upgauge to the A321, and we expect this to be true for Airbus just as Boeing has “hidden” -9 orders. But for the moment, Airbus has a 53% market share of the A321neo/737-9 sector (including the 201 Lion Air assignment).

There are undelivered A321ceos and 737-900ERs plus aging in-service members of these subtypes. This leads us to believe the market it somewhat larger than the 1,200 Boeing suggests.

The issue for the airlines is that many of the 757s begin coming off lease or approach retirement age by 2019, needing replacement then. So what do Airbus and Boeing do to meet demand before a new airplane can be designed and put into service?

There’s little that Boeing can do with the 737-9. It’s already stretched as far as it can go, and the additional weight of the MAX design isn’t fully offset by the thrust-bump of CFM’s LEAP-1B engine. Field performance is worse than the 737-900ER, a 737-9 customer tells us, based on today’s design. Boeing still has time to improve the performance before EIS. But payload/range and baggage is still not only less than the 757, it’s less than the A321neo. And Airbus plans further improvements to the A321neo.

The Space Flex and other changes will enable a maximum, one-class configuration of 240 passengers by 2018, the same maximum capacity of the 757-200 and 20 more than the maximum capacity of the 737-9. However, range today is forecast to be about 450nm short of the 757W. Can Airbus squeeze more range out of the A321neo? It’s working to cut weight and improve aerodynamics—but another 10%+ in range out of the projected range is a tall order and probably unachievable.

The 787-8 is “too much” airplane, with a range of 7,800nm. So is the A330-200 at 7,200nm and the proposed A330 Regional doesn’t have enough range at 3,000nm, though it could easily encompass 4,000nm. But at 246 passengers in typical international business class/coach configuration, it far exceeds the 169 passengers in United Airlines’ international 757 configuration—and the operating costs.

So far, there is no answer for a 757 replacement—at least not any time soon.

Boeing had a possible B-757-200/-300, B-767-200, A-321, A-310, B-737-900/ER replacement. That was the B-787-3, but its range was close to that of the B-737-9MAX, short of what was needed for a true B-757 replacement.

Perhaps Boeing can dust off that design and add a little more range? The B-787-3 had a range of about 3000 nm with 290 pax and a full cargo load. It also had a wingspan that was about 26′ shorter than the wingspan of the B-787-8, but used the same fuselage. Maybe the solution is to make the B-787-3 fuselage about 162.5′ (about 50m) long, which is about 7m shorter than the -8?

The 787-3 empty weight would have been more then twice that of the 737. And costs too.

This is exactly why you will not see a 787-3. The economics would be terrible.

Maybe Boeing made the wrong choice for the 737max – if it had based it on the 757-200 frame it would have had the ground clearance for the engines and a fuselage that could have been stretched and shrunk as required, using the 737 wing. Would have been a much more expensive option though, I guess.

There would have been a few problems with basing the 737MAX on the 757.

Off the top of my head:

a) The 757 line was decommissioned in 2005, i.e. over five years before Airbus launched NEO, which triggered Boeing into committing to MAX another six/seven months later.

b) For the bulk of the market – A320/737-8 size – a 757MAX would not have been a great fit at all. Engines and wings would have been way overengineered for 737-8/A320 missions. It would have meant delivering too much airplane for the bulk of the market, in order to satisfy a market niche that can be ~90% covered by A321neo and 737-9 as it is.

I did have my tongue firmly in my cheek when suggesting this, but on the other hand, would it be so big a challenge to modify 737 tooling to accept the 757 frame, given that the fuselages have very similar origins, also I would expect the designs for the tooling to remain even if the physical item does not, and that must represent a large part of the cost of producing it. Clearly the best option for Boeing longer term is the NSA, but the ensuing product will probably look more like the 757 than the 737, I suspect!

Pretty useless to guess what Bopeing should have done. Hindsight always helps 😉 In 2010 I suggested a more radical 737 upgrade for EIS in 2014 but being realistic a year later AA/SQ/DL didn’t give them any more time.

http://i191.photobucket.com/albums/z160/keesje_pics/Radical4Bill737Upgrade737-900XG.jpg

Reading back Boeing comments from the 2008-2011 period, they were convinced the 737 would hold it own against the A320 this decade and after that the new NSA will sweep the market.

McNerney April 2011:

“As you know, most of the data and customer feedback is suggesting to us that the new airplane option is the most favorable, but we’ll — we’ll get to that decision on a timely basis. We’re 2019, 2020, that’s the timeframe that the market seems to want this new airplane and where we can deliver technologies that can make a meaningful difference.”

https://leehamnews.com/2011/04/29/mcnerneys-interesting-comments-on-the-new-airplane/

A few weeks later Albaugh has AA on his cell & the rest is history, including a serious 757 replacement.

Sorry, didn’t spot that 😀

As for 757/737 commonality: As Keesje pointed out a couple of weeks ago, the 757’s fuselage is more similar to the 727, in that it changes profile aft of the wings.

I also wouldn’t underestimate the cost of producing tooling, converting all 757 tooling and design documentation up to modern-day standards… and then still doing the necessary modifications. That’s a lot of pre-work…

Anyway – that’s neither here nor there now. The 757 replacement is going to be part of the NSA line-up some time in the 2020s.

I.e. they should have based the NG on the 757 and they would have had something.

“Airbus has a 53% market share of the A321neo/737-9 sector”

IMO this doesn’t sketch a realistic picture about what is taking place in the 200+ seat short/medium range segment.

Airbus has 2000 firm orders from 95 customers for the A321, many commitments (CEO+NEO). The past has shown that a good part of the 3000 A320’s in then backlog will also be converted to A321. Airbus says in 2013 alone they got over 600 A321 orders, commitments and type conversions. The A321 outselling the 757 threefold is the next few years isn’t a farfetched scenario any more.

Apart form the fact that the 757 can do thing the A321 can not, the A321 does things the 757 cannot. E.g. carry cargo containers, meet the strictest noise requirements and offer 18 inch seat comfort in the back.

US carriers, Delta, American and Jetblue will make the A321 their Transcon working horses, replacing more then 757’s, And what can / will United do? Ignore the GTF powered A321 NEO’s?

Far more then replacing the 757, the main driver for Boeing developing a “757 successor” would be a “A321 stopper” taking over key customers such as AA, Delta, ANA, Hawaiian, TAM, the Chinese

http://www.airplane-pictures.net/images/uploaded-images/2008-11/14/28923.jpg

I presume the cargo containers help reduce the turnaround times, but adds weight. Do you know which US airlines use them/ plan to use them?

Not sure at all about US, but I know Air Canada uses containers at least on some flights.

In Europe (where I’m based) I don’t think I’ve ever been on a flight that didn’t have containers loaded. Flights without containers seem to be very few and far between.

(Note: I’m talking about flights using 737/A320 equipment here.)

Hmmm, Air Canada have now 737s. I guess that means no more containers for them at some point in time.

Let me try that again. Air Canada will have new 737s…..

Not for much longer now they are changing to 737max – it can’t have been that big a consideration in the decision.

I have the feeling AC will be flying on A321s for a long time. Because of network capacity, payload and cargo requirements on long flights. The 737-9 has different capabilities. http://www.airplane-pictures.net/images/uploaded-images/2009-4/14/42480.jpg

AC has strong links with Boeing since 2003 and benefits from cooperation in the areas of financing and asset management that make choices rational and beneficial, but I do not see any exclusivity demands included in the cooperation.

NYX I do not think any US carrier uses it yet. The rest of the world do. It this time it seems about 400- 500 out of 2000 A321 ordered are used/ earmarked for US Transcon service. I think slow US adaption has to do with fleet commonality / airport infrastructure. Most A320 operators also have 757, 737, MD80 fleets without container capability.

Daniel Tsang also took a shot at the Topic, with a mostly different approach but nice insights, like Scotts articlle. Aspire concludes Boeing needs to advance NSA to regain lost ground in the narrowbody sector. http://www.aspireaviation.com/2014/04/28/boeing-nsa-game-changing-technologies/

It seems the marriage of the Pratt PW1100G and Airbus A321 will be a crusial factor in Boeing NSA specification and time schedule. The value gap between the largest 737 and A321 seems too large and broad (capacity, engine choice, cargo, comfort, noise, runway performance, payload) to sustain.

CFM is in a squeeze, but (in its fierce battle with Pratt) will be forced to communicate that yes, a LEAP with a 79 inch bigger fan sfc is about 5% better then a LEAP with a 69 inch fan.

Meanwhile Airbus is already openly claiming victory (slides 17 & 18).:

http://www.airbus-group.com/dms/airbusgroup/int/en/investor-relations/documents/2014/presentations/JP-Morgan-Commercial-Update/JP%20Morgan%20Commercial%20Update.pdf

I wonder if the A320 NEO/B737 MAX competition has meaning anymore? Both are booked up so far into the future I imagine discounts must be at a near all-time low.

The B757 can be used for ranges beyond 3000nm. Only few operators do that, and these operators do other strange things, too. So why get fixated on this 4000nm mission?

Indeed Scorsch : some Operators have tried 757s for feeder, LCC or charter type operations, over ranges below 2,500 nm, with single class high density accomodation … as a result, they experience the infamed ‘757 syndrome’, meaning one up to two less flights/24h (before curfew) due to markedly slower ground rotations. For long cabins, of 35 or more rows, it is high time to switch to the twin aisle configuration. The same syndrome also affects the A321, the more so with 240 pax/40 rows ! Therefore, the idea to accomodate an A322 (a +7 rows/+42 pax/+210″ stretch beyond A321, aimed for the 753 replacement market ?) with [3+3] seating would seem antagonistic/far-fetched ?

I really do not think the market is for the 757-200 replacement. The 737-900/900ER/MAX 9, along with the A321/A321NEO have the domestic and west coast-hawaii portion of the 752 market covered. The TATL 757W market is a very small niche.

The real opportunity is in the 757-300 class of aircraft, which, if it were still in production, might garner orders today to replace domestic 767-300s, and the 767-300ER. Except for a handful of 753s, there are no new domestic aircraft larger than the 739 and A321 class. Similarly, there are no new international aircraft smaller than the A330-200 or 787-8.

Instead of a 757-X, perhaps a 767-8 or a 767-MAX or a 767-X would be worth considering. Using existing aerodynamic improvements (blended winglets, etc.) the 747-8 GEnx engines, new flight deck avionics (from the KC-46 tanker) aluminum-lithium alloys, and other possible weight saving improvements. The goal should be an airplane which could replace existing 767-300ERs with a measurable improvement in seat mile costs with a much lower capital cost than a net-new airplane.

This should be possible because the KC-46 production line will continue for many more years.

Alternatively, building a net-new airplane to cover the gamut between a domestic 757-200 and an international 767-300 is a big challenge.

I also agree that a 767MAX 200 series with new engines, but no composites might fill the need for a 757 type and then some. With a range of 5000 miles, it would be a good replacement for the 757 and the 767-200ER, carry 200-220 passengers and take up the long thin routes that still need a fuel efficient replacement.

With the 767 line still running, just an engine upgrade might keep RD costs down and with some weight shaving and new generation wing tips, it could be a good seller,not in great numbers, but enough to warrant production along with the tanker versions.

If the fuel savings can be at least 5-8 percent with a low acquisition cost, it might be attractive to some carriers.

Concurred, mehl30 :

The 757 is at its best when applied Medium Range (flight time > 3.5h). ln-flight service ease plus Product Differentiation demand translate into convivial 3-class LOPA (Premium/E+/YC), realistically seating typically 180 pax (752, cabin length 118.4ft) resp. 225 pax (753, cabin length 141.8ft), both with a cabin density = 7.2 – 7.9 sq.ft/pax.

When referring to the ‘757 niche’, keep in mind these numbers, not to be mixed with the single-class certification ‘Exit Limits’ of same aircraft, of 239 pax, resp. 289 pax.

A parallel assessment of A321 as “757 replacement”, given its cabin length of 112.9ft, equates to a capacity – in similar “Medium Range” applications – of more or less 170 pax. So whereas the A321 tallies closely short of the 752, there is a difference of # 50-55 seats vs 753. The pax density however improves to 7.8 – 8.3 pax/sq.ft in the A321, due to the 6.2″ wider cabin, enabling 1″ wider seats.

So when Airbus refers to the new Exit Limit (A321 = 240 pax ?) in forums focusing “757 Replacement”, the bias is evident, caricatural, long-nosed. In aeroreality A321 = # 175 pax when used on proper 757 routes, which is OK if we make a careful distinction : you actually DO REPLACE the 752, and to an advantage ! You have the NEO plus the leaner OWE plus 3 ACT (auxiliary container tanks = +3h additional flight time) for the cost and range pictures, plus 2 or more AKH for payfreight (each worth # 10 full fare paying Y-class pax) to boost yields vs 752 … but “it takes a 753 to replace a 753” (paraphrasing John Leahy) !

I’m sitting here At Brisbane airport awaiting my domestic flight departure & observing the changes on the domestic apron since my previous visit some ten years previous the changes are significant & Brisbane is not alone in this change as I see similar examples worldwide.

My view of Airbus single aisles airframes in a previously held Boeing domain domain illustrates concerns that Boeing will have an accute awareness of from both a geographical & political bias a factor the Leeham 321 order distribution graphs blatantly illustrate.

Setting aside as yet unknown performance claim & counter claims the reality is Airbus is not only increasingly the more visible & but also offers the more flexible, economic & sadly the more acceptable political solution.

773 was a dud, how much of that was due to the turnaround times for a long narrow tube? I suspect that anything longer than an A321/B739 will need to load both ends.

I’m assuming you meant 753 instead of 773.

If the A321 seats were kept at the same width as those of the 757, it can have wider aisles, (by up to 6 inches). Can help improve the turnaround times.

My best guess if operators will adjust frequencies and types to cover B757 routes with existing types, scaling down to B737/A321 with slightly more frequency if needed or up to A332, and lower frequency. If operators ask for an A332/3R with 4000 mile in enough numbers they will get it, its not like it would be expensive. I guess Airbus have an advantage here where traffic is increasing.

753 indeed, I need new glasses.

Aspire Aviation predicts the sweet spot will move to near 200 passengers, and remain a single aisle. Will the primary boarding door be an L2 door at mid-cabin? Will the wingspan remain at 36m, or will it be optimized for fuelburn at 40 or 42m?

Maybe it’s time for a folding wingtip for the future narrow body it the 36m must be kept?

Back to the mini twin aisle Boeing as looking at real hard.

I gather you mean Boeing’s patented “Fattie” [2+3+2] ? With its horizontal-elliptic cross-section, it’s a ‘NO-GO’ : the idea was to optimise the fuselage around the seven-abreast concept, at 2010 Y-class standards, ie the 62″ triple, which sets the twin seat @ 42.5″, too narrow if you want to install a proper hatrack above it … the result being that a Fattie “as is” would fall short in terms of carry-on. Or Boeing pays Royalties to Airbus for the application to the Fattie of Airbus’ proprietary Wankel-shaped NSA cabin cross-section ?

2-3-2 is possible. It would fit LD3-45 and provide enough space for everything. The exact optimum shapes and sizes tbd, maybe circular is best after all.

Issue is if Airbus or Boeing makes it, that fuselage will be sub optimal for flights up to 200 seats / 1500NM. Guess where 90% of the market is.. The other guys will dive under it with a lighter / smaller single aisle, also offering LD3 capability, but being efficient around 160 seats / 700NMs too. And gain market dominance where the large fleets are.

Keesje, LD-3’s need a belly more than 5 ft high. Airbus’s first twin-aisle family [A300, A310, A330 & A340] had their circular cross section defined by the minimum diameter of a circle around a pair of LD-3’s. I’m not sure what kind of cross-section you would get with a single aisle above a single row of LD-3’s

LD3-45 is the flat variant for the A320, Comac, MS-21. Widely in use outside the US. http://cdn-www.airliners.net/aviation-photos/middle/6/7/6/0267676.jpg

One would expect at some point CFRP construction will allow greater flexibility (variability) in cross section design, beyond the slight nuances old aluminum tubes like the 757 had. It could make nitpicking more complicated too (“those 4 rows will be intolerable on that model.”)

Much greater efficiencies would be gained I think with mid-fuselage boarding, but airlines are loathe to invest in that gate infrastructure.

Like I’ve been saying Boeing/Airbus will not address the 757 replacement with a standalone plane in a few years like some have suggested. In the next narrowbody replacement programme though? Definitely. I can see that spanning from A320/738 sized aircraft at the bottom, up to the 753 sized plane at the upper end.

That the problem, if an airframe is good for 160-250 seats over 4000NM, it will automatically be outclassed in the center of the NB segment by something much lighter/ smaller/less capable around 150-170 seats.