Leeham News and Analysis

There's more to real news than a news release.

Airbus A330-800 and -900neo, first analysis, part 3: performance

In our first two parts of the analysis of the Airbus A330neo launch at the Farnborough Air Show, we have gone through the information provided by Airbus and Rolls Royce and provided comments on what these really mean from a practical point of view.

Areas we wanted to verify with our independent model have been how the A330neo would perform versus the A330ceo, especially on shorter ranges, than the Airbus example of 4,000nm and how it would stack up against the Boeing 787.

We give the first answer to these questions with data from our proprietary, independent model. This is first-cut data and we bring it forward in time as there is some confusion on what Airbus has said about the shorter range performance of the A330neo.

The performance information provided by Airbus has been dissected and we have done a first independent modeling to verify the validity of Airbus launch presentation claims (given below) but also to clarify the muddled picture of what happens when the range flown gets shorter than the 4000nm example given by Airbus at the FAS. This is important since many sectors flown for a long haul airliner are still 1,000nm to 2000nm intra-Asia and some within Europe. The 4,000nm Airbus is using as reference is a mission which is equivalent to a Trans-Atlantic or a Europe – Asia flight (London to Delhi for example), with typical flight times of 8-9 hours.

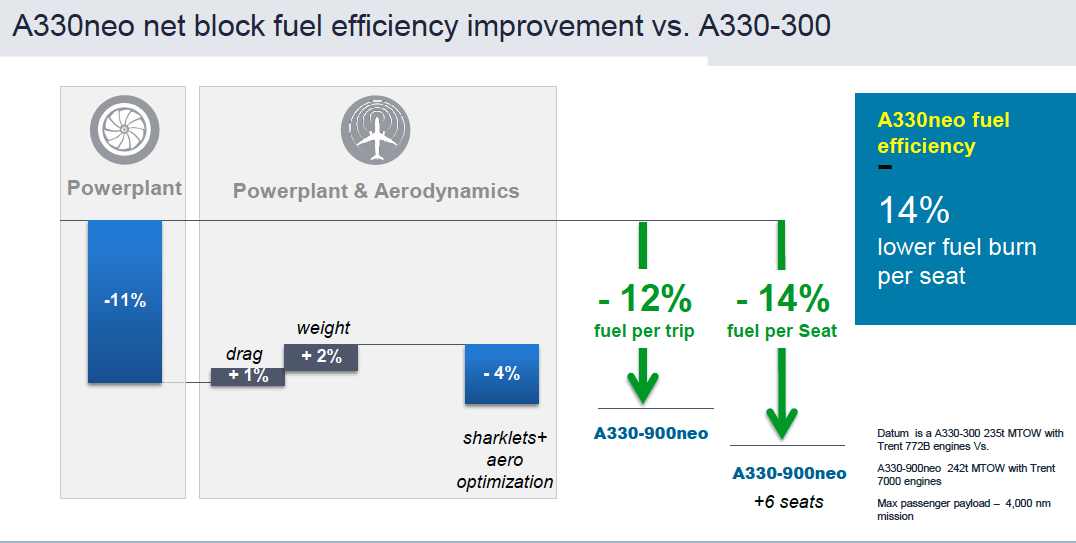

Airbus performance claims from launch presentation

Overall performance claim

We have modeled the main changes as presented for the final A330neo, comprising changes for engines, nacelles/pylons and A350-style winglets in addition to the weight changes. We have not had time to dissect and model the aerodynamic improvements Airbus will do to the inner wing. Further we have also not modeled the “Powerplant 11%” in full as the Trent 7000 gives 10% TSFC improvement and we do not understand where Airbus finds the last 1%.

Importantly, we wanted to understand the decline in efficiency improvement when the flown range gets shorter; 4,000nm is about 2,000nm above today’s average stage length for the in service A330 fleet, which is the stage length example used by Airbus since about 2010 to compare the A330-200/300 with the 787-8/9. We don’t think that the A330neo’s average stage length will be 2,000nm, but it will definitely be below 4,000nm. Therefore the performance at shorter flights is important to understand.

With the caution that this is a first run of our model on incomplete data, we can say the following:

- We focus this check on the trip improvement of 12%. We will explain why below.

- We have initial, more detailed information on what Airbus does to improve cabin utilization but it is too early to say if this shall be counted as a four or six seats increase in a normalized cabin configuration. Airbus has counted the performance numbers with a six seat increase, not the advertised 10 seat increase.

- We therefore only look at the trip fuel differences. To further make apples-to- apples comparisons of the aircraft, we configure them with identically loaded cabins of 245 and 295 respectively for ceo and neo variants.

- The 12% trip improvement is between a 235t A330-300 and a 242t A330-900neo. To us this means the 330ceo does not have the improvement that the 242t variant will have from changes in flap gondola shapes. In our comparison we compare aircraft with identical shapes.

- Our initial analysis says the A330-200 and A330-800neo tracks the difference of the -300/-900 models.

- Under these circumstances, we find an improvement of about 10%. We have not modeled the improvement for the inner wing aerodynamics,which involves changes to the slat and the upper wing faring and we have not modeled the 1% powerplant improvement over and above the Trent 7000 10% TSFC improvement, as we are not sure what Airbus means with this 1% gain on top of TSFC.

- With both those factors contributing around 1% each (which Airbus says the powerplant improvement does), 12% seems plausible.

- Perhaps more interesting at this first analysis is the decline in fuel efficiency gain when shorter ranges are flown. We have a decline of 20%-30% from 4,000nm to 1,000nm. We can thereby conclude that Kiran Rao, Airbus EVP of Strategy and Marketing, meant something else with the quote “for 2-3 hour missions, the A330ceos are still more efficient than a neo,” (from this discussion with Aviation Week).

The A330R for regional

In Thursday’s Farnborough wrap-up press conference, Airbus clarified the role and configuration of the A330R or regional. This model is in the price-list and is subject to ongoing sales campaigns, mainly for intra-China routes. Airbus also clarified that this de-papered and de-rated aircraft is a ceo model. It will not be raised to a neo specification, as this makes no sense. When calculating the total operational costs for the regional, the ceo is the better choice as it has a lower price (the engines are cheaper, as is the airframe), a lower weight and engines which consume 10% more fuel but fuel is a less important factor in the total cost equation for dedicated short-haul. For the discussion above we talk about the average stage length being shorter than 4,000nm, not all flights being shorter.

The A330 versus the 787

It is clear the A330neo forms a competitive proposition versus the 787 and that the competition between the two variants in the 250-300 seat segment will be fierce going forward. We have gained more understanding of the cabin modifications that Airbus has included in the A330neo, and this together with our knowledge from our normalized cabin work for our A330neo study makes it possible to position which models are competing in the market place:

- For the 300 seats segment, it is A330-900neo which is competing with 787-9. They are virtually identical in size with the seat gains the neo has. We see that the 787-9 would still hold a very slight advantage in fuel burn of 1-2% for 4,000nm sectors.

- For the 250 seat segment, it is the A330-800neo which is competing with a 3%-4% smaller 787-8. The 787-8 is clearly lighter and will show a larger margin to the neo than for the 300 seat segment, and we see that there is still a fuel consumption gap of about 3%-4% between them at 4,000nm.

Why the difference in what we see and what Airbus claims (they claim equal fuel consumption performance)? We don’t know how it configure the 787. We, for instance, use identical -10% TSFC Trent 1000TEN engines on the 787 with identically configured cabins, crew rests etc.

Finally we can point out that Boeing’s insistence of the 787-10 as the -900neo’s competitor is tactics and shall be discarded as such. The 787-10 is about 25-30 seats larger than the A330-900neo. The 787-10, then, shows better per seat efficiency but the model is rather a competitor to a A350-900 regional than a competitor to the 330neo.

As more information becomes available, we will further refine our model and re-analyze the economics of the airplanes. The results will be incorporated into an updated version of our A330neo Business Case Study, which is only a for-purchase item. These additional results will not be posted in this column.

By Leeham Co EU

Thanks for the analysis! Great read, and rich food for flight performance nerds like me!

Short question:

The “20-30% loss of efficiency” can be interpreted like this:

4000nm: NEO 10% better than CEO

1000nm: NEO 7% better than CEO

Is that correct?

Your analysis indicates that the A330-NEO is especially strong as B787-9 competitor (as -900). I think this is supported by the fact that Boeing will not give away the -9 at such discounts as the early -8s.

That is correctly interpreted.

Thanks Leeham Eu !

Number in the 787 vs a330 section are in block fuel or per seat ?

You are using pre FARN2014 seat count is that it ?

By the way, the 787-10 is more 30-40 PAX bigger than 25 – 30 I guess

Indeed it’s bigger than A350-900

Block fuel.

We do not accept any OEM LOPA (Layout Of Passenger Accommodations) without knowing it in detail (this is where the OEM wiggle the truth to a large extent) therefore we use our own LOPA, otherwise we might compare apples and oranges.

If the ceo remains more economic than the neo for short sectors, if there turns out to be a demand for a 330 sized aircraft for these sectors and if there is no alternative aircraft (ie in the gap pre 737/32x replacement), why would Airbus drop the ceo?

used aircraft will be abundant from 787 caused retirements, A330NEO retirement and A350 replacements

Whilst what you say is true, it’s also the case that demand in this sector is rising, so supply is still likely to be lagging behind demand.

I expect the 767 and 757 to leave pax service in droves.

I wouldn’t be so sure about 757s. Remaining aircraft are getting old an no replacement in sight so I guess a couple of hundred of them will soldier on in airline service until they go for scrap.

Imu 757 are misused today for TATL because US airlines have them. Not because

they are in any way efficient for the task.

The NEOs will step the 757 ( and the 767 ) by another 15..20% away from achieveable fuel numbers.

” Finally we can point out that Boeing’s insistence of the 787-10 as the -900neo’s competitor is tactics and shall be discarded as such. The 787-10 is about 25-30 seats larger than the A330-900neo. ”

I must agree with Boeing the 787-10 will compete with the A330-900 more then with the A350-900. Not because of cabin size but because of payload range. 787-10 have weak payload range to fly to/from Asia, where the A350 and 777 are specified for. Passengers and bags only isn’t a real market to/from Asia.

…that’s why Leeham stated:

The 787-10, then, shows better per seat efficiency but the model is rather a competitor to a A350-900 regional

Frankly I do not see the A350-900R as a realistic option for any market. How many regional 777s have been sold lately. Those frames are build to do hard landings at MLW, do ETOPS 300, take tons of LD3’s from hot Asian runways.

http://www.airvectors.net/ava320_01.jpg

Nothing regional about these aircraft IMO. Leahy will not mention the A350R anymore after this weeks launch.

“Frankly I do not see the A350-900R as a realistic option for any market.”

And yet SQ, EI, EY and probably more have selected the A350-900R.

“Nothing regional about these aircraft IMO”

Regional is a bit of a wrong name because it won’t have a regional cabin like the A330R. It’s just a de-rated aircraft.

Nothing new here, Airbus has dozens of de-rated A330s:

http://www.airbus.com/fileadmin/media_gallery/files/tech_data/AC/Airbus-AC-A330-20140101.pdf (page 60 onward)

The A350 won’t be different.

I agree with Keesje and believe that the 787-10 will eventually kill the A330-900neo. Assuming the trip costs of the 787-10 are not much more than the the -9 and the A330, the extra 30 seats are pure gravy. The only things in favor of the A330 are availability of the A330 and the extra capital cost of the 787-10 (higher than the -9, which in turn is higher than the A330). Once Boeing starts competing on price in a buyers’ market sometime around 2025 the A330 will struggle I believe

The exception are airlines that put 9 economy seats across in an A330. The cabin isn’t a lot narrower than the 787, which commonly has nine seats, but for most airlines it’s a squeeze too far – for now…

Airbus talked about sculpting a couple of inches of additional cabin width in their Mark I A350. Is any chance of them doing doing this for the new A330?

Irrespective of whether or not I agree with the premise that “787-10 will eventually kill the A330-900neo” (still somewhat on the fence on that one, to be honest), I have to say – and I have said this before – that Boeing trying to compete on price on the 787 sounds like a really bad idea. The A330-900 is allegedly ~25% cheaper than the 787-9, which in turn is, at list prices, ~15% cheaper than the 787-10. Really, trying to bridge that price difference doesn’t sound like a good idea (even before considering that Boeing’s accounting block for the 787 is already at 1,300 frames, and that assumes a certain margin over production cost per frame.

Which is why I would tend to agree with Leeham that the 787-10 and A330-900 aren’t really competitors. The 787 has a bit more range and more capacity – all of which, however, come at a hefty premium over the A330-900.

I agree that competing on price makes no sense now, while supply is so tight. It’s not sensible for Boeing to price down their 787’s as they won’t be able to sell any more planes as a result. Come 2015 however, there will be a plentiful supply of 787s, A350s and A330s. The relevant backlogs will have burnt down and the current boom will probably have turned. Airframe manufacturers will be chasing sales. If the 787-10 can carry more passengers at a similar trip cost to the A330 that means Boeing can charge more for its plane. If the manufacturing costs are similar, Boeing will always win because it can price its plane so that it makes a profit while forcing a loss on Airbus

Which implies a replacement for the A330 sometime around 2025. I know we repeat ourselves. The great advantage that the 787 and the A350 have over the A330 has nothing to do with new materials, systems or aerodynamics. It’s the ability to accommodate 9 across seats, which transforms the per seat economics. This replacement will be based on the A350 fuselage, but won’t be the A350-800 in its current form.

>> If the 787-10 can carry more passengers at a similar trip cost to the A330 that means Boeing can charge more for its plane. If the manufacturing costs are similar, Boeing will always win because it can price its plane so that it makes a profit while forcing a loss on Airbus <<

If the manufacturing costs are similar? What in the world makes you think the manufacturing costs would be similar? I mean, you are aware that Boeing is taking staggering losses on each 787 delivered…Right?

>> It’s not sensible for Boeing to price down their 787′s as they won’t be able to sell any more planes as a result. <<

Or…maybe it's mot sensible for Boeing to price their 787s down because they are losing Gobs of money on every 787 they produce? In fact, I am starting to believe that Boeing no longer wants to sell its 787-8 because its such a money loser. As a result, this leaves the market wide open for the A330-800. And sooner, or later, I think Boeing is going to tire of losing money on the 787-9, too – and jack the prices up. As a result, I think Airbus made a good move with the A330 NEO.

Jimmy, the development and industrialization costs are sunk. Boeing, indeed any commercial operation, will try to maximize its profits over its cost to manufacture. Those costs will come down as the 787 ramps up and Boeing get more efficient at making the planes. The situation in 2025 will be very different from the one now.

>> Jimmy, the development and industrialization costs are sunk. <<

So? I'm not talking about Development and Industrialization Costs: I'm talking about Productions Costs. You know, the Production Costs that are at $23 Billion and climbing. And it makes me wonder…when is Boeing going to start making money from producing the 787? You know, that magical stage of the program where they can actually sell a plane for more money than it costs to build it. That is called "Profit" stage. And Profit is good, and generally understood to be necessary in the business world and is said to be the "Secret of Success" for those companies that succeed. Seriously…look at those companies that have failed compared to those that have succeeded, and in almost every case "Profit" or a lack of "Profit" has been involved. Thus, "Profit", though ignored by many, is a important business concept that must be at the forefront of business planning and assessment.

For example, let's consider the Lockheed L-1011. According to some aviation Fan Boyz, this was the "Bestest Jetliner" ever produced: it was high-tech and cutting edge and sleek and…just really cool. But…it is a little known Secret that Lockheed quit producing the L-1011 because they couldn't achieve the state of Jetliner Program Nirvana known as "Profit". So…like Kurt Cobain when he couldn't achieve Nirvana, they knew what to do to their L-1011 Jetliner Program once they knew "Profit" could not be achieved – they terminated it real hard. As a result, Lockheed is burned out on Jetliners and doesn't make them any more.

Yeah…I'd say "Profit" is important. Maybe even more important than "Return on Net Assets" (RONA). But, that is another story about another Jetliner Company for another day.

“Regional” always means low utilization (in terms of flight hours), high cycles, fuel being less important, capital cost very important. Such an airframe is easily ruined after 15 years, and I guess that’s what Kiran Rao meant with hier statement towards AW.

787-8:

If I understand the numbers correct the A330-800 will have the same seat mile cost as the 787-8. But the Airbus will be 3-4% larger.

I think that’s a slight advantage for the A330-800. Its cheaper and can hold some more passengers for the same seat mile costs.

787-9:

The A330-900 has the same size, 1-2% higher fuel burn but lower purchase price.

That will be certainly a fierce competition and all depends on pricing. How low can Airbus price the plane?

787-10: The 787-10 has 1000nm more range than the A330-900 and has more seats. Not exactly a direct 1:1 competitor. But how are the trip costs in comparison to a A330-900 at same sector length?

What interests me about the A330NEO is that it has been the lessors who have been the main players stepping up to the plate to buy this plane. I am not sure why this is!

From where I sit the A330NEO is going to run out of legs around the 2025 year mark. If it is a highly optimised aircraft that cannot maintain the 3-4% efficiency delta between itself and the 787 for a full range of mission profiles, demand for the aircraft is going to be less in the secondary market. Lessors don’t like this as it limits their ability to place the aeroplanes when they come off lease!

If we also consider early build 787’s (8’s) will be coming on stream into the secondary market during this time, second hand 10 year old 787’s are still going to have a fuel efficiency advantage over new build A330NEO’s. Again, if this is the case, the business case for buying/leasing a new build A330NEO versus buying/leasing a second hand 787 (even with higher maintenance costs) will be very hard to justify.

I am afraid some of the lessors are chasing a medium wide body bubble based upon pent up demand from the Asian LCC’s. JL has been talking up these LCC’s for quite a while and the lessors have been leasing plenty of aircraft to them. Are they getting ahead of themselves?

On the same point there could be some fundamental changes in the finance markets (cost of capital) that influence the optimum capital /operational cost ratios. If this is the case a lower capital requirement business model could be more advantages going forward. If we also throw into the mix that growth in the Asian market is going to be exponential going forward, using capital to maximise revenues rather than minimising costs might work out to give the best ROI.

Using Boeing’s latest CMO and known or announced production capacities, both OEM’s currently have enough capacity to supply 120% of the market over the next twenty years. If we throw in a 757MAX in the 2020-2025 year period this production capacity could increase to 150%. Will the OEMS’s eventually paint themselves into a corner if they keep chasing every niche within the market?

If this keeps going I suppose we can throw the Boeing Yellowstone project in the bin (I suspect Boeing already has).

There is more to this. We will have to wait and see how this pans out!

Could you please provide another reliable source for this claim:

“[…] second hand 10 year old 787’s are still going to have a fuel efficiency advantage over new build A330NEO’s.”

As I remember the Airbus NEO press conference someone told that the fuel burn would be equal to the 787 but then another person said that this would be just the rather conservative view of the sales department and the NEO would even be better.

I am well aware of the predictions made above within this article but they look very conservative. I guess the assumption was “even with worse fuel consumption the A330NEO with far less capital costs […]”

I guess lessors have done the calculation that early lease rates for the A330 NEO will be near enough to the 787, particularly if they are unable to get their hands on enough 787s to satisfy demand for leases. Depreciation will be similar – cheaper acquisition costs for the A330 will balance out against lower residual values?

With regard to a new aircraft (A338 or otherwise) in 2025 vs a 10yo one (788 or otherwise), you need to assume some level of PIPs for the new aircraft. Unless you retrofit the PIPs onto the old airframe, this will tilt the playing field in favour of the new one.

I’d suggest the analysis so far has been based upon the Trent-1000 787 and the A330NEO trent-100-TEN. The 787 will have the option of the 1000-Ten engine from 2016 onwards.

From Rolls Royce website the TEN will be up to 3% more efficient than the current Trent 1000.

I’d suggest this engine will be highly optimised (the 3rd PIP) and as such I don’t think we should expect any further major PIPS going forward.

Our analysis is done with the Trent 1000TEN for the 787 and the Trent 7000 for the 330neo, i.e. the same engine revision and TSFC for both. We don’t have that clarity for Airbus numbers.

Assuming no PIPs, for either engine or airframe, for 10 years, seems extremely conservative to me.

If I were a financier, I would be worried about the poor prospects for the residual value of the A330-800 and -900. Airbus is fragmenting the A330/A350 market and this will hurt residuals for the A350 as well. Bad move in my humble opinion. The A330-800 makes sense but A350-900 doesn’t as it will cannibalize market for the A350-900.

Having many lessors as launch customers is a bad sign. They may have wiggle room in their contracts that allows them to switch or cancel orders. Remember the ILFC A380s that were ultimately cancelled.

http://www.reuters.com/article/2011/03/08/us-ilfc-idUSTRE7275S120110308

Airplanes are first order aquired for enabling airlines to transport pax and things and not to make leasers ( or other financial entities ) rich.

Financing arrangements diminish the profit potential for airlines.

( One reason why LH performs better than comentators like to allow for.)

Moving profits back to airlines ( i.e. the productive market participants ) would be a good thing (TM) imho.

As you note residuals are more an issue for leasers than for users.

I am not sure I understand the 787-10 vs 330-900 issue. If the option is a larger plane with similar trip costs and slightly better range then would you not like the more capable aircraft?

The 330-800 and -900 are going to compete in the under 4500nm market for 10-15 years and allow some cash flow. It’s better then ceding the market to Boeing. It does say the 350-800 is done for until it can be optimized (after the 900, 1000, and 380-neo?).

Why do you think the 787-10 and 330-900 would have similar trip costs?

I think that’s the case for the 787-9 vs A330-900. The 787-10 trip cost would be higher.

The 787-10 has more seats but similar or better CASM. If cou can’t fill it, I think it is too expensive to operate, still.

“I am not sure I understand the 787-10 vs 330-900 issue. If the option is a larger plane with similar trip costs and slightly better range then would you not like the more capable aircraft?”

– You’re forgetting that Airbus is aiming to make up for the disadvantage using pricing. If you cannot fill all those extra seats in the 787-10, you run the risk of losing money compared to the A330-900.

>>> I am not sure I understand the 787-10 vs 330-900 issue. <<<

It was just thrown out there to obscure the fact that the 787-9 will now have to compete against the A330-900 – it's a smokescreen.

The 787-10 and A330-900 are much different in Pax capacity and, as a result, don't compete against one another.

I scratch my head about the A350-800 being done for.

Airbus has been trying to do it in for a very long time. They twisted arms, made deal etc to get people out of that version as they decided it was a dog.

They may resurrect something called a -800 (now called a stretch with is a stretch in all senses of the term) but its been a dead dog for a long time.

The original buyers did not do it in, Airbus did (but then the orignal buyers may have also had ideas it was optimized and not a -900 shrink with the full airframe weight issues.

I would not count on Alabama to solve Airbus A320 backlog. Thestate ranks 50th in literacy and math skills and #1 in obesity. They will be more of a headache than S Carolina has been for Boeing…..a state of dim bulbs.

For shorter flights, regional use, Airbus will probably promote and adjust the cabin to 9 abreast. Operators will revisit the economics, CASM after that. AirAsia already did so, even for longer flights.

http://www.airliners.net/photo/AirAsia-X/Airbus-A330-343/1577465/L/

How would a 9 abreast neo stack up against the 787 in terms of CASM? Anyone?

Very roughly, going 9 abreast adds 12% seating capacity and reduces per-seat costs by 11%. You’ll be able to carry less cargo due to the increased number of pax and more luggage. But almost certainly it would be lower CASM than a 788/789.

I sure wouldn’t want to sit in a 9-abreast A330 for very long, though!

“I sure wouldn’t want to sit in a 9-abreast A330 for very long, though!”

Me neither. I’ve tried a 9 abreast once, or make it twice since it was on a return trip, 7-8 hours long. It was 30% cheaper than the nearest available fare. Barring extreme or unavoidable circumstances, I wouldn’t do it again.

But somehow, Air Asia thinks they’ll be successful with it. We’ll see.

They already are successful

Heh, just look at weight/height distribution charts for current asian populations 😉

The seats will be slightly narrower then the 787s. But through the years many forum members told me a thumb doesn’t really matter, so half a thumb ..

http://airlines-lounge.com/wordpress/wp-content/uploads/2014/07/800x600_1405423294_A330-900neo_RR_Air_Asia_X_01.jpg

You are a laugh keesge. I read your comments in a forum having a fit between an 18″ airbus a350 seat width versus a 17.5″ Boeing 777 seat. But the difference between a 17.3″ 787 seat width and a 16.7″ airbus width in this case means “half a thumb” so who cares. The 787 vs. Neo width is greater than what you were whining about before. As you said back then “can we have some consistency please?” LMAO

With regards to value of a 10 year old 787 versus a 10 year old 330NEO – remember that a mature 787 is unknown territory while the 330 is well charted. It is too early to make any statements of long-term value.

The announcement of the 330NEO raises the possibility of a one plane airline. The regional for domestic flights, the CEO for longer regional flights up to 2500nm and of course the NEO for up to 6500nm flights. I suspect that if you crunch the numbers, the optimisation gains and route flexibility should be quite attractive.

Yes, I think you are right. Airlines already flying the A330 can transfer the CEO’s for domestic routes and use the NEO’s for longer haul. I think a large part of the A330NEO business case relies on this.

Most astute opinion in this blog. Airbus is safeguarding its A330 base for many years to come.

I believe Boeing will adjust the pricing of the 787. Some sources claim that the 787-8 typically is offered at around $116 million; rather likely Boeing will sharpen their offers to maybe around $108 million, despite publicly eschewing such suggestions. It’s good for airlines and ultimately the travelling public. In the long run, though, the sharpened competition will make entry for a third long-haul aircraft manufacturer even more difficult, thus also benefitting the A&B duopoly. I believe that both Airbus and Boeing will book an additional thousand orders for their small twin-aisle products very comfortably; the demand is tremendous.

Lessors are quicker to act because agility is at the heart of their business model. Airlines have much slower acquisition processes.

Airbus has especially huge one advantage, availability. The A330 line has been running for a while and Boeing lost a good number of sales with the 787 screw up. The waiting time for Boeing 787 wide bodies is too long and since they sat on their hands and let the chance to offer a 767MAX slip through their hands, Airbus has been the recipient of increased orders due to Boeing’s inept and slow management.

I know some here will discount the idea of the 767MAX, but it could have been a low price leader for Boeing in the 200-240 seat category and with the line running, new engines and some weight loss could be very attractive to some carriers. Not a huge number, but yet enough to produce along side the air force tankers.

I don’t discount it. I suspect its an option.

What I don’t know is how far you would have to go to make it a good regional competitor. New engines given, new wing maybe, lighten the fuselage with Al Li possibly (which would have been the dagger to the Airbus heart if they had done that on the 777X.

Someone way above my level has to crunch the numbers and figure out if there is a benefit or enough market there for which changes.

Scott (or someone), could you help dispel my confusion? I completely understand & agree that the A330-800neo will compete with the 787-8 (similar aircraft in terms of both pax count at 250-ish & range around 7,500 nm), but I’m puzzled by the assertion that the A330-900neo matches up with the 787-9. In Monday’s announcement, Airbus said the A330-900neo will seat 310 pax, or +10 pax vs. the A330-200ceo. Meanwhile, Boeing says the 787-9 seats 280 pax, while the 787-10 will seat 323 pax. Based on this, the 787-10 is only 13 seats larger than the A330-900neo, while the 787-9 is 30 seats smaller than the A330-900neo. Why is Boeing incorrect, then, in seeing the 787-10 as more the competitor to the A330-900neo than the 787-9, particularly when the range capabilities of the A330-900neo and 787-10 are closer to one another than the A330-900neo and 787-9 are? I certainly understand that truth is the first casualty in the seat-count wars, but what am I missing here?

Ignore the manufacturer seating claims-Airbus and Boeing use different standards when making them. Leeham Co EU normalizes seating to typical airline configuration across the board to have the same parameters, and it’s from that we draw our economic conclusions.

So are using 8 or 9 across seating in both the 787 and A330 models?

See this slide from the Airbus presentation,

http://oi61.tinypic.com/6537d1.jpg

They’ve basically taken the lighter and cheaper 787-9 (compared to the 787-10) and packed in extra 20+ seats to bring it closer to the A330-900 capacity (304 vs. 310). I’m not sure if the 787-10 would be at a better position than what’s been shown in the slide according to them. They’ve pretty much improved the CASM on the 787-9 in the analysis with the extra seats instead of keeping it at 280 as according to Boeing.

I question the seat count numbers being used by Airbus. The ANZ 787-9’s in a 3-class configuration have 302 seats where as QF’s current A330-300’s have 301 seats in a 2-class configuration. On the same point Boeing are saying we should be comparing the 787-10 with the A330-900. Go figure!

The 787-10 is way too much plane to be compared against the A330-900 then.

Also in the mix will be the continuing improvements on the 787 in weight reduction, aerodynamic improvements and PIP improvements on the engines.

You want to bet that Boeing is talking with P&W real hard now about an exclusive deal on a GTF?

How that all plays out gets into it as well and in what time frame.

Until 787-9 and -10’s are steadily rolling out the doors at targeted rates, the NEO will have some breathing room. Once that happens though, and with 5-10 years of further 1%/year improvements on the 787, it will have a quite tough go of it. Again the systematic/gradual improvements (as has happened over the years with the 737/777) are what make static analyses/projections particularly difficult in the comparisons. And what happens when Boeing suddenly does both re-engine and discover based on a decade of maintenance/inspections/experience it can significantly thin out some of the overbuilt CFRP components to save more weight?

Conversely, it’s the lack of any steady investment/improvements in the commercial passenger 767 that makes it a highly improbable candidate for a quick and cheap re-engine. That wing is closer to 30 years old I think now, and just doesn’t approach an A330 in efficiency. Sort of like McD trying desperately to get that final MD-11X stretch/tweak without an all new wing; it just didn’t work/fly.

787-9 is rolling out the door in “numbers” now.

It has (3 years) before an NEO is even in the air let alone being built in numbers (and which NEO goes first?)

I think Boeing has the main weight gains out of the 787, ergo the -9 being under weight (biggest gains, some incremental will continue). It will slowly add up.

Keep in mind the A330 is nothing more than an early 70s era airframe, the 767 should have a lot of possibility if Boeing chooses to (or is forced) to do something with it.

Yes it would need a new wing along with engines (my opinion). Other improvements?

Have to stay tuned, only Boeing really knows what they could wring out of that airframe let alone if they think its worth doing so.

I continue to find it funny that Airbus could have done this all along and put the bucks into a true 777 competitor but people like Hazy beat them over the head (and Hazy is the biggest advocate). Thee is a real twist to that and I don’t mean wings

I scratch my head when people talk about pricing. Forget R&D costs and the difference between them written off Airbus style or amortised Boeing style (this is not an A vs B issue but due to accounting rules differences). That cash is gone for both and it is now a paper exercise. The aircraft industry is still fundamentally a manufacturing industry.

The pricing difference is driven by the manufacturing costs. And fundamentally CRFP is an extremely expensive material from both a raw material perspective as well as an manufacturing perspective. Aluminium is effectively a very cheap material. So while CRFP is incredible strong and light and potentially is lower in maintenance cost, if the final structure ends up to be about the same weight, size and performance, then Al is the superior material from a cost perspective. So if the 787 and the A330neo are similar in weight (roughly), then the A330neo should be significantly cheaper to manufacture than the 787. Add up the fact that the A330 production is mature and most of the tooling has been written off, then the difference should be big. And due to the fundamental difference in manufacturing technologies, this difference will not go away even in about 5-10 years time. And today the 787 is still losing money (even without R&D amortisation) on every plane they deliver. Same will be for the A380 (finally about to break even next year) and the A350 (for the next 3-5 years). The 777 will turn from a cash cow into a money loser due to CRFP wing for the first 2-3 years after transition to the 777-8/9. But for the 777X wing CRFP makes sense because the end result is a fundamentally better and lighter wing.

Delta (whose business model it is to have low capital outlay) have many times hinted that the only thing they don’t like about the 787 is the price and that this is effectively a showstopper for them. Looking at the eagerness of the lessors signing up to the A330neo, I think that the difference in real world (not list) prices is very significant.

BTW: looking at comments from both Delta and Virgin Atlantic on the A330neo, am I the only one expecting a package deal where both Delta and Virgin sign off on the A330neo in exchange for cancelling the Virgin A380 order?

“BTW: looking at comments from both Delta and Virgin Atlantic on the A330neo, am I the only one expecting a package deal where both Delta and Virgin sign off on the A330neo in exchange for cancelling the Virgin A380 order?”

Interesting for sure.

To cancel some A380 I have the feeling they would have to swallow several A330CEO.

“But for the 777X wing CRFP makes sense because the end result is a fundamentally better and lighter wing.”

So we agree that CRFP weighs less and has better performance. Other than that I don’t disagree with anything you’ve said and in fact that is the Airbus bet on the A330NEO.

But I think the window of the A330 being a mature product able to compete on price is closing and the bargain basement price isn’t able to go on sale on a starting-point rather thin margin AS CRFP gets lighter and cheaper to produce.

This seems to me to be the same thinking out of Airbus that led to the A350-1000 targeting the 777-300ER rather than the obvious future (now in development) upgrade.

The core issue here is not materials (I will get to that), its Stage Length! We really need a chart not the verbiage, it would be easier to see.

787-9 is designed to carry full passenger load something around 8300 miles very efficiently.

A330-300 at 6100 miles and a fuel hog (grin)

A330-900 than above less fuel at 4000 miles

If Boeing designed the 787 to work at that distance then the A330NEO would not stand a chance (but they would not sell it to those who desire the long flights without refueling)

So, if Airbus can pick off a more common stage length (2 to 4k) the 787 supposedly burns more fuel (only if its fueled up all the way), then on that comparison as it carries far less fuel it can be more efficient with its newer engines. A330 does not need as much wing to carry fuel.

I am wondering if Boeing then uses a new system I call “auto stage length:” The program uses the programed flight distance, re-certifies the aircraft for that distance, adjusts the landing fees as well as supplementary payments (or deductions) to Boeing.

Materials:

The material cost is only part of it. An important part for sure.

Assembly is large part as well. To assemble an aluminum aircraft takes fabricators thousands of hours of cutting, forming and riveting items together to make a larger part and then to assemble that larger part into an even larger assembly.

CRFP allows the Boeing fuselage to be spun, then smaller reinforcing rings to be inserted. Overall a whole lot less assembly time.

Mechanics cost and time cost of course so the end product at least theory can be done quicker which offsets material cost.

Other advantages are lighter (smaller engine for the same size aircraft) and less fuel needed to carry the structure.

More efficient and accurate forms can be made and meet the ideal shape that gives better aerodynamics.

Boeing also claims its stronger (probably true) and part of that was touted as higher pressure (6k?) but the 777x with its aluminum fuselage supposedly will have the same pressure level so that seems to be ?

More ramp rash resistant which seems to be true but have seen no figures yet.

Also as aircraft produce enormous amounts of condensation, CRFP supposedly reduces the corrosion and the times between inspection increase which reduces overall costs (if true) While that’s true of CRFP that also means the fastenerss and non CRFP material have to be corrosion resistant which cost more (titanium a bit factor though they are reduction that at least somewhat with the new -9 window frame)

Final assembly is also a factor, how fast can you run one through the factory? How many people does it take to put it together.

Boeings model was to have the sections arrive and plug and play assembly which reduces time (and easier to stuff systems inside before its assembled). Note that the 737 fuselage sections are empty from Spirit and all that has to be done at the factory. Older system and maybe not worth changing?

So, its all a big balancing act, market, stage length, materials, engines

Most of the manufacturing and material advantages you enumerate are Boeing PR reurgitated and may have no equivalent in reality 😉

Laying fiber is automated but still rather limited volume work. ( Go back to the Airbus lessons learnt pdf that held usefull information about fiber laying capabilities and expected improvements over time )

Inserting tight fitting hoops ( aka frames ) into barrel sections is a major hassle.

Calibrating a spun and baked barrel section to tight tolerances will stay more difficult than via the “panelvan” route . Boeing used to even have issues with classic manufacture 777 section tolerances that needed strong hydraulic presses for assembly.

I would not expect them to perform significantly better on the 787.

My expectation is that Boeing will not do another clean sheet design using spun barrel sections in the longterm future. Though complex shapes like the tail section seem to have enough advantages to continue in this way.

All the benefits listed are to me the technical view. I am taking the bean-counter view. Forget performance, weight, fuel consumption, aerodynamic shape, corrosion and whatever else. I am of the opinion that the 787 will always be more expensive to manufacture than the A330neo and the carbon fibre fuselage is the main reason. Carbon is great for large sheets, wingspars etc but it is terrible for small components. Some of the airbus A350 delays were the need to build special tooling for every single carbonfiber bracket where before it was a single CNC machine with various software programs. Carbon fibre is not a magical material: it is difficult to manufacture, has lower tolerances than metals and as I said before the raw materials are expensive. Every material has benefit and tradeoffs – there is no perfect material. A simple example is GLARE. Technically it is a good material for its intended use, but it has not reduced in cost as was expected and as such it use is restricted to the A380. Another example where powerpoint met reality was the MRJ where the design was changed from majority carbon fibre to majority aluminium based on the experience from the 787.

A lot of benefits stated like lower labour cost, pre-stuffed barrels etc, I don’t see evidence that this is reality. Simplest evidence of all: the cost reduction curve on the 787 is the same as the 777. Also, Boeing factories are not significantly leaner than Airbus factories. Charleston had to fly in experienced workers from Seattle because the Lego brick concept turned out to need the same skills and experience as the 777 and 737.

So the 787 is higher performance but more expensive to manufacture while the A330neo is lower performance and cheaper to manufacture.

What also people don’t realise is the impact of Lehman Brothers. Before 2008 obtaining capital was much easier to get than it is now. Evidence is in the Exim banking articles posted earlier this month. Before 2008, the 20 years business case was more or less the deciding factor. That has changed as the risk appetite of the financial community is now far less. The implication of that is that less money going out today has a higher weighting than less money going out in the future. You can not bank 20 year fuel saving today, but you can bank a $10M discount on a new aircraft. It is not the airlines who control this, it is the financial community – there could be a case where an airline wants a 787 and the bankers are only willing to finance an A330 (and reverse…).

So the question becomes what is the difference in price and performance. I do not believe that Boeing has the ability to price the 787 at the same level as the A330neo due to the inherent difference in manufacturing cost. If the difference is 1-2% in fuel, I believe the A330neo can use pricing to win a lot of deals while maintaining profitability. If you really want bleeding edge long thin routes stretching the range limits of both aircraft, the 787 will come out on top. So the question is where the market is and how much the difference in operating costs is in real life.

Go to http://en.wikipedia.org/wiki/Airbus_A350_XWB; scroll down to “Early Development”. Airbus’s original 2004 concept for the A350 was the A330 fuselage with a new wing, empennage and engines. (The A330 fuselage is the same outside diameter and nominal cabin cross section as 1972’s A300.) This was rejected by prospective customers. They insisted on an all-new airplane with a wider (XWB) body

The A330-800/-900 are several steps back from 2004’s A350 concept; the wing is modified instead of replaced and the empennage is retained

As for the extra ten seats, use the A330-300 baseline in fig. 2-4-1 of the A330 airport planning document. 295 seats=12F+42C+241Y. One way (but certainly not the only way) to get the extra seats would be to re-pitch all the seats between the emergency exit and the aft entry door from 32 to 30 inches. That’s plus 8. Then remove the lav in front of the RH aft door. That’s plus 2. Voila = plus 10 seats.

I’ve asked the question before and no-one has really answered – how much scope is there for lightening the A300 by using new alloys for the skin, for example? Presumably this is something that Boeing will find difficult to match in the 787 and so could help to keep the A330 competitive.

Roger in terms of materials, systems, wings, LDG’s, engine related structure and systems the A330/340 shares little with the old A300s. Look e.g. at the percentage composites the A330 has versus the A300. Al Li is said to be a pretty straight forward option replacing some Al alloys. It has to have feasible implementation within a few years though.

You can do it, it costs and then becomes non competitive . Ergo, as little as needed to get the new engines and pick off the more common stage lengths so its competitive.

As the A330 is nothing more than a stretched A300 with 70s technology you had it right! (grin)

Do seriously believe that?

Notice the grin at the end?

Sorry, typo, I meant lightening the A330

Somehow I managed to upload the previous comment before finishing it! What I was going on to say is that there must be scope in an older frame for using newer materials (I think I read a mention somewhere of Aluminium/beryllium) but less in the CFRP frame because it is less well understood and there will be an inevitable tendency to err on the side of caution. So I don’t necessarily see the 787 pulling ahead in terms of efficiency if Airbus make a determined effort.

A330NEO works on minimal investment. Boeing faced the same thing on the 777X and did not do it (Li Al). Cost to re-design in their view was not worth it.

My take is it would have been as Airbus would not even come close with the A350-1000 or 1100. Current Boeing chicken management content to stay with status quo.

Also keep in mind the A330 is a 70s technically and you can only do so much with what you have. Its been tweaked as much as it can be and at that point you just need all new to get benefits.

While not as competitive a the spun fuselage, Airbus elected to use a frame and panel system on the A350 as that is supposedly better than Li aluminum. Hard telling, in their case they did not have the research done to do what Boeing did so they punted.

Downside is not only not as well done but also a lot more mixed metals and corrosion issues (nose is aluminium as they could not get that done at all with the frame and panel system).

You may well have to pull a special inspection just for the nose at a much shorter interval than the rest needs (no one is currently talking about the differences between the A350 and 787 in that regard but it’s a factor for purchases as it’s a life long cost item (or the lessors)

With the massive number of twins all competing for the same slots you have to wonder if the users will figure out when it’s the optimum time to return a leased plane of one type or another, let the lessor do all the maintenance in the meantime pickup up another one from someone else that is just through maintenance and they don’t have to worry about it. Could be quite the dog eat dog thing by the 2020 time frame.

Boeing putting 180 787s a year into the market (15 a month which is not unlikely and could be more) and an equal or large number of A350s and A330s a year from Airbus (and that does not count the 767NE-NWO offering!)

A330NEO works on minimal investment. Boeing faced the same thing on the 777X and did not do it (Li Al). Cost to re-design in their view was not worth it.

The 777(-300ER) as it stands lacks potential for just a NEOisation.

IMHO Boeing has to invest more to achieve probably less ( similar to the 737 MAX ?

)

Agreed Boeing had to do a lot more than Airbus in the 737 vs A320 (covers all variants no matter what Airbus calls them) . I don’t think Boeing succeeded in even matching it despite the figures they throw out. Current operator say they current versions are dead even despite Boeings claim to 8% better. Boeing has done far ore (or had to) on the 737 to keep competitive. The A320 is simply better optimized (the turning nose wheel aside). Airbus can keep tweaking and getting better. 737 is beyond its limit.

The only reason Airbus can’t seize more of the market is they can only produce 42 a month right now, which is what Boeing is making (about 1-2 different between them depending on who is in what stage of ramp up). As Alabama comes on line that may change but Boeing is also ramping up a lot. Sold into the 2020s does not mean market share now.

Not so much due to the age of the 737 (A300 not much newer)

but the architecture of it being designed with tube engine and not fan engines. Boeing should have changed that at the 737NG but did not and lost a chance.

777 sees limited regional (or followed b y long distance) so the range has to stay up and cherry picking off a flight area with a lot of need not workable (my opinion, not hard fact). I admire Airbus for what they did. How successful remains to be see. I still go for 200-300. Also I don’t think Air Asia is a reliable customer, like Lyon I think they will run afoul of themselves and never take the planes and numbers they say.

It makes for an interesting dog fight and also puts a lot of kaput in Boeings claim to dominate the twin aisle segment (777 and 777X yes, the rest no). Boeing has not lost its arrogance. Not sure what that will take.

On the other hand I suspect Boeing has a slew of trick to pull yet as well. In this case you let Airbus launch the A330NEO before putting them out.

All Darned interesting.

70s design? I have a steel cocking knife. The design is somewhere around AC or AD. There are some really sharp ceramics blades available today. Did you ever tried to hone them? I use the wetted backside of my tea cup to hone my cocking knives.

Old design is not always a disadvantage.

BC instead of AC… DC…

http://www.youtube.com/watch?v=V5iTQf5PDyY&feature=youtube_gdata_player ??

I don’t disagree, I believe Airbus threw out how dated the 737 and 747 were and its no more valid than the A330, its my way of poking a hole in the Leahy airbag.

“On the other hand I suspect Boeing has a slew of trick to pull yet as well. In this case you let Airbus launch the A330NEO before putting them out.”

Expect something underhanded.

“All Darned interesting.”

For sure.

Like selective statistics? I am pretty keen on my “auto airframe re- certificate ” i.e re- paper the aircraft for each stage length system will see if they adopt it! (I am still working on a catchy tittle, thats the important part)

Maybe the answer is to let people beg you for a solution like the A330NEO (and Hazy, hmm)

Hopefully some interesting actual engineering work comes out into play

What about the Freighter and the MRTT versions of the A330 ?

Did Airbus announce something about NEO versions of them ?

Isn’t the MRTT just a certified option package for “any” A330 frame?

The freighter could be slightly more hassle.

I would guess a whole new certification required. Not all that many MRTTs in the works and you could use used A330 airframes as they are converted anyway (and making an NEO available would be an issue as all commited to commercial.

The KC45 will be the only logical choice as its still the same old 767 we know and love so Airbus won’t have to worry about it! (grin)

The KC45 will be the only logical choice ..

Don’t underestimate the complexity of that effort.

A.net already is at posting 275 just for following the assembly of a rather bog standard 767. they still haven’t fathomed were that additional tiny little increase in length will sit 😉

Add one and you will be a little more correct: KC-46

The KC-46 is not the “old 767” and that is the problem for Boeing:

http://www.businesstimes.com.sg/breaking-news/transport/boeing-may-face-higher-expected-costs-kc-46-tanker-20140714

The KC-46 is an enlarged 767-200, with -300 wing, -400 cockpit with 787 style displays and FBW and therefore not the “old 767” you may know.

The NEO option would give the MRTT more range/loiter time/fuel off load. Such aircraft are hardly used and therefore the better engines will not compensate the price difference for less fuel burn. I can imagine a MRTT with MTOW at 242 t version.

Used A330-200? Try to buy one.

Regarding the A330 size debate…here’s another weird chart from Boeing.

http://3.bp.blogspot.com/-1-V527uwjdQ/U8bpgFOGH-I/AAAAAAAASNQ/KpPG20gwyPk/s1600/image.jpg

Didn’t Boeing miss something on top? 747-8i or A380?

The timeline for EIS is missing…

Also the space you will get as a passenger on an 8-hour trip in tourist class.

How long can Boeing impress stock holders until they will realise what is going on:

747-8: 120 orders

787: production cost still high and output less than expected

777X: new wing like the 747-8i on the same airframe and expected for the next decade.

As long as the pimping ecology can keep up a closed, synergetic front….

At some point though, fractal degeneration will proceed at an accelerating pace.

The 737 is doing great too. Boeing stock holders / management earn money from good news. Everybody happy.

“Don’t mention the war!”

http://www.pdxlight.com/neomax.htm

“Don’t mention the War!”

If we time line orders against available delivery slots, both Airbus and Boeing are roughly running even.

The 737MAX’s entry into service is approximately two years behind the A320NEO. Boeing will be delivering NG’s during that time.

If we also look at order counts in comparison to underlying demand by region, we will see Airbus has more orders than expected demand. This will even itself out as time goes by (orders delayed, aircraft leased to other regions) and they do have a quality customer base, but something will eventually have to give.

In the 2016-2020 period, Airbus will be delivering up to 200 twin aisles per year.

Meanwhile Boeing is preparing the first 777-9X for 2020 and pushing seriously discounted 77W’s while finally trying to recoup 787 investments, competing against cheap A330NEOs.

Boeing dominates the twin aisles market. I do not think so. Boeing is trying to dismiss the A350-1000. Ignoring JAL, BA, UA, SQ, CX replacing their 777s with them.. It will be shockingly lighter and not as much smaller as Boeing likes to suggest.

http://www.aspireaviation.com/wp-content/uploads/2013/12/Screen-Shot-2013-12-31-at-15.08.43.png

Pingback: Half time 2014 for Boeing and Airbus | Leeham News and Comment

Pingback: Final A330neo analysis; cabin improvements gives the A330neo gains over today’s A330 | Leeham News and Comment