Leeham News and Analysis

There's more to real news than a news release.

Pontifications: No rate increase on Boeing 787 predicted

Jan. 30, 2017, © Leeham Co.: Boeing will decide this year whether to boost 787 production to 14/mo from 12/mo by the end of the decade.

I don’t see how this can happen. Neither do several aerospace analysts.

Book:bill sales were just 0.36 in 2014, 0.53 in 2015 and 0.42 in 2016. The last three years saw a book:bill rate average of just 0.43, or an average of 57 airplanes per year.

Boeing is burning off the backlog, not adding to it. At this rate, Boeing won’t be able to sustain rate 12 beyond 2020, let alone boost the rate in 2019.

Not unless there is a plethora of sales this year. This doesn’t seem likely.

Securing more orders

Dennis Muilenburg, CEO of The Boeing Co., said on the third quarter earnings call the company doesn’t see a recovery in wide-body orders until the start of the next decade.

Yet more orders are needed this year to support rate 14. He had this to say last week on the fourth quarter/year-end earnings call:

“Our 787 Dreamliner program also stands on a strong foundation for long-term production with 700 firm orders in our year-end backlog. Securing additional 787 orders to solidify the 14 per month production rate at the end of the decade remains a priority. We’ve booked several new orders in 2016, but there’s still more work to do.”

Muilenburg said the 700 backlog orders is five years’ production at rate 12, which is true if all 144 airplanes were delivered per year. But deliveries stretch beyond 2020, tapering off beginning in 2020 and increasing each year thereafter. This is based on identified orders. There are more than 100 unidentified orders for which delivery dates are unknown.

Analysts doubt rate hike

Morgan Stanley, in a note issued after the earnings call, doubted there will be substantial 787 sales this year.

- “From a book-to-bill standpoint, the company’s expectation is for a year of similar orders vs. 2016 and implies a ~0.8x level, consistent with our forecast of 0.7-0.9x. In our opinion, the activity will be skewed to the narrow-body side given wide-body pressures associated with low oil and moderated (albeit healthy) traffic trends,” the aerospace analyst wrote.

- “We do not believe BA will ultimately hit 14/month, and believe there could be incremental pricing pressure on the 787-9s and -10s to be delivered in 2018-2020,” wrote Canaccord Genuity in its post-earnings call note. “We continue to believe there will ultimately be a charge on the 787 program….”

- “787 production decision coming this year; 14/month unlikely to us,” JP Morgan wrote in its note.

- “We believe a move to 14/mo from 12/mo is not likely,” wrote Wells Fargo.

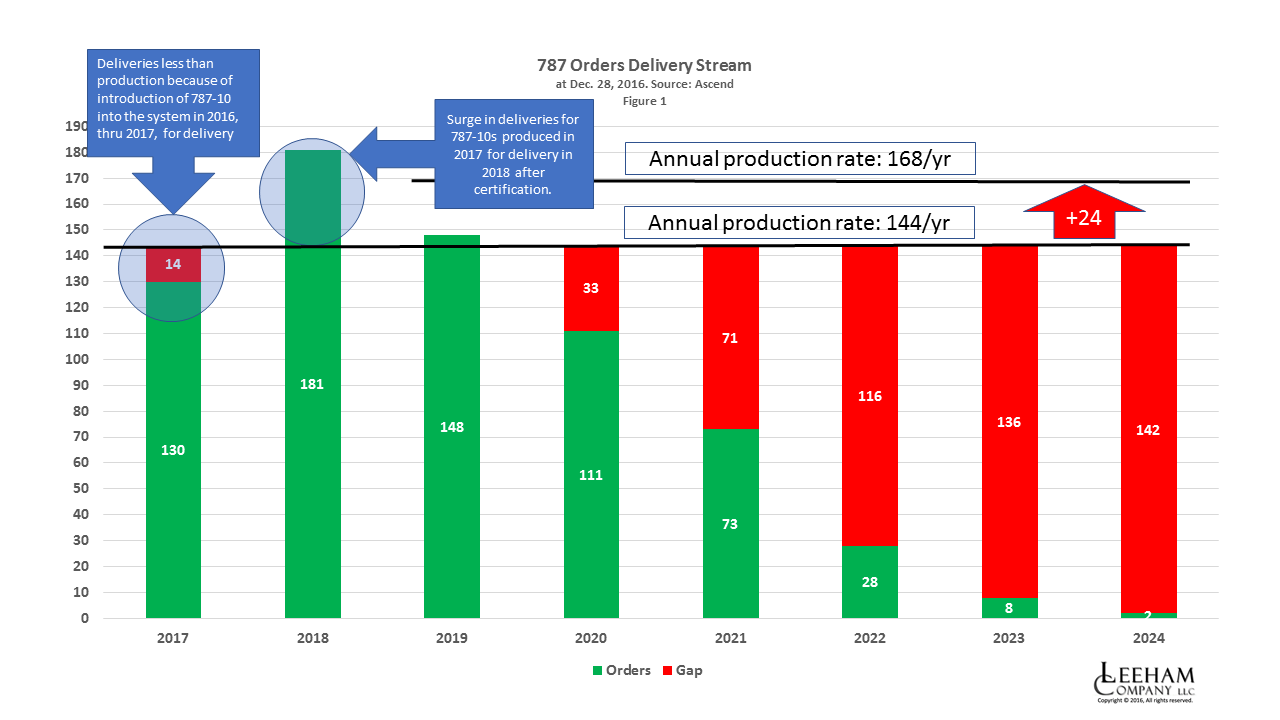

Filling the production gap

If we assume 2020 is full at the current rate, with 33 derived from those 100 Unidentified orders, Boeing needs to sell another 24 airplanes for delivery in 2020 to support rate 14.

From 2021, the challenge becomes much greater. Ninety-five sales for delivery in 2021 are needed, minus whatever is allocated from the Unidentifieds. (Note that the farther out, the more the deliveries taper off.) The number increases to 140 in 2022. There are virtually no delivery positions in 2023/24 in the identified orders.

Muilenburg points to a pending bubble (my word) of retirements coming from 2020. True enough, but Airbus will be competing for the same business. The required sales to support 14/mo just don’t seem realistic to me–nor to the analysts quoted above. Even Bernstein Research, which rates Boeing Outperform and remains one of the most bullish of analysts, forecasts rate 12 for 2019 and 2020.

I was surprised by you comment that I had overestimated A330NEO prices last post on this subject. Always knew that my estimates were going to be guesses. I assume that means that both sides are already fighting for every order in the longer range “small” twin isle segment, margin is pressed, and both A+B will be lucky to record the same 787/330NEO sales this year as last year.

It seems that the decision is more decreasing rate than increasing it.

Will that be 10 a month?

Scott, at the end of January, baccklog of 787 is not 100 but 76 aircraft for “unidentified customers”

Moving 24 aircrafts from unidentified to identified in January is not recorded in Boeing order book … only new sales to Arik (2 aircraft)

Or 9 a month. W’ll see.

Muilenburg points to a pending bubble (my word) of retirements coming from 2020.

Airbus will aggressively push to keep the A330 line alive, maybe launching family enhancements. Stretches, engines, cargo / tanker variants.

They are not going to stretch the A330.

The certainly will look at cargo, tankers a given (but that requires recertification)

They also are not going to change engines.

A stretch would make it a 787-10 competitor. Judging by sales there doesn’t seem to be room for two in that space. I guess Airbus can find better uses for their money.

Given the suggested stasis or reduction in output Is there rationale for Boeing to consolidate 787 FAL on one site or is that a step too far. Any reduction in numbers would play havoc with the admirable production efficiency/learning curve gains made in the past 3 years. Better one line going flat out than two lines working spasmodically

Its a question I have been asking myself.

They have a production over capacity.

Charleston is the only one that is building the -10.

It also looks like it could ramp up and maybe do rate 8. I don’t know about 10.

But I think long term historical rate 8 is probably where it goes to.

So by by Everett as they have too much in Charleston to give it up now .

Boeing might want to ensure that if older airframes are retired in large amounts, it can cover the majority of the market. Otherwise, surplus demand may move to the A330NEO.

If Boeing had introduced the B787 on time (and hence had created 200-300 additional production slots until 2020), there would not have been A330NEO in the first place.

The interesting thing is that the A330Neo seems to have somewhat killed off the 787-10 model. Almost all of these were sold prior to the introduction of the A330Neo. I guess it’s a price play. The range of both planes are similar but it looks like the lower capital cost of the A330 beats the CASM improvement of the 787-10. The 787-9 may be less affected because it has more range. If so, Boeing will at some point reduce the price of the 787-10 and clean up.

I would say this is a case of correlation but not causation. Almost all of the 787-10s were sold at the time the model launched (or already under negotiation at that point).

Of the 204 A330-900s sold, 80 went to all-Airbus operators (I’m excluding the E-Jets at TAP) and another 55 went to lessors. Then you have Iran Air’s order for 28; who knows how that was decided? Maybe with no A330neo, Boeing would have had a better shot at orders from Delta and Garuda. But I would say the main impact has been on pricing, not actual sales.

Agreed. A330NEO is not selling either. 777X is in hiatus.

A350 is in hiatus.

That’s a long wait for an Aircraft so you begin to see where it hits first, new Aircraft that are long term (777X) and orders just stop.

Its the near-term and dealing with what they have and even pushing deliveries out when there is too much capacity.

They created a bubble and bubbles while they last longer than you8 thing and people start to say its the new normal, just like Prime Mortgage, when it comes to a screeching halt with the associated damage is worse than they ever thought.

@TW

Not sure if the OEMs created the bubble, the perfect storm of free money, unlimited credit and superhigh fuel prices created the bubble. The OEMs can simply generate as much cash out of the good times and hope for the best.

It is naive to think that either OEM will falter to a significant degree over time. The production rates can only be massaged so far and given the heavy and direct competition across almost all sectors the split is likely to end up near 50:50. That is why the fundamental risk to both OEMs is ongoing global demand.

No I don’t believe the OEMs created the bubble.

But a CEO and the boards job should be to live in reality and reality says that bubbles don’t last.

There were a lot of comments that this was not a bubble but the new norm.

Having a few years under the belt, when new norms are established with sudden peaks, they are bubbles.

Amongst other things you put as much cash in reserve so you have the money to get through the down turn, not squander it on stock buy backs.

Years back I was involved in an engine class, the company (Cummins) and the industry was involved in one of the recessions.

They had found a piece of info they needed to pursue, it took them far too long because their test cells were full of new development engines.

In the midst of a nasty downturn they continued R&D and investment in new products.

Having see Boeing drop what were going to be good aircraft for the future because of the downturn its the opposite story.

The waiting for Airbus to declare themselves instead of gong for it, more of the same.

We know what works, if there is going to be an industry, it needs R&D, money and management of bubbles and the dips.

Not sure how much of this is a bubble, as I see it operators are placing all there orders in one deal, ie 50 at once and not ten here and ten there, in order to secure good pricing. Note they are also securing plenty of options to cover growth. Looking at EKs current fleet I have no doubt that they can use 150 777-Xs at some time or another, and 150 options pretty well ensures that they will never have to negociate 777-Xs ever again. It also allowed the ME-3 to specify their own plane, even though it has limited appeal to anybody else.

I agree that a move to 14/month isn’t the most likely outcome, but it’s not completely impossible. Seems to me that the main determining factor is whether Emirates finally makes its 787/A350 decision this year and chooses the 787.

If Boeing had ~70 orders in hand from Emirates, it doesn’t seem like it would be hard to get to 100 or more for the full year. It’s still not a book-to-bill of 1, but I’m not sure that’s the determining factor. We’ve already seen Boeing go up to an unsustainable 8.3/month rate on the 777 to offset cash flow problems on the 787. So we could now see Boeing go to rate 14 on the 787 from 2019 to 2021 to burn off a bunch of the deferred balance and offset the cash flow decline from 777.

Looking at the chart, Boeing has ~100 open slots in the 2019-2021 period at rate 12. (That doesn’t count any existing orders that haven’t made it into the Ascend database.) But it’s apparently oversold by a wide margin in 2018. If 20 orders from 2018 get deferred into the 2019-2021 window, then Boeing only needs 80 more orders at rate 12, or 152 if it goes to rate 14 for those three years. The vast majority of the open slots are in 2021. Selling 150 planes for delivery by 2021 over the next 2-3 years won’t be a cakewalk, but it’s not an insurmountable task, either.

That’s my two cents.

I not only think its impossible, I think rate 12 is also impossible

Scott says 10, I think 8, but it sure is not 12 or 14 long term.

As Scott noted, its not just orders, its when they are scheduled to be delivered.

If you make 200 in year 2020, and there is only 100 in 2019, 2020, and 2021 you have a problem (gross example)

You build white tails or you cut production. Sometimes you can feather a bit but there is a sharp limit.

I don’t think I understand your example.

In any case, I agree that it’s impossible for rate 14 to be sustainable. But if Boeing just wants to cushion the 777 cash flow headwind (I’m estimating 777 program cash flow at <$1 billion annually in 2018 and 2019 — and maybe more like breakeven — down from perhaps $3-$4 billion annually recently) it could ramp up 787 production in 2019 and then go back to 12/month in 2022 or something.

I also don't think rate 12 is sustainable long term. However, as Boeing management has mentioned, there is a wave of upcoming widebody retirements from the big production bubble of 1997-2001 (roughly speaking) that will provide a lot of replacement demand in the early-mid 2020s. A reduction below 12/month is more likely to happen after that replacement demand is met, although a significant global recession between now and then could obviously throw things off.

Additionally, I think a lot of people are starting to forget about the long-term impact of air travel growth. 4% annual growth works out to nearly 50% growth over the course of a decade. That's not showing up in order totals right now, because airlines are still working through the massive orders they placed a few years ago. But as those order books get whittled down, airlines will need to order more planes. There hasn't been a slowdown in air traffic growth in the past few years. http://www.iata.org/pressroom/pr/Pages/2016-10-18-02.aspx

The problem is that your suppliers ramp up, then would have to cut back.

They don’t want to do that, it hurts them badly.

So they try to make do with what they have at higher rates, people worked harder, morale drops, pressures mount and they get less productive.

People looking for jobs look at it and know its going to fall off and pass, or jump as soon as they get something longer term.

Boeing doesn’t want to put any skin in the game but wants the best of both worlds.

Is there any particular reason why airliners can only be manufactured in even numbers?

A330 is 7/mo. 777 currently is 7/mo, going to 5/mo (with actual delivery rate 3.5/mo). 737 going to 47/mo, then 52, then 57.

57 a month with Airbus wanting to go to 60. Think about that for a moment, that is incredible when you put perspective with the past.

Incredible times!

And Boeing is talking about it coming out of one factory not 4 for their end. Phew.

2 x 737 competed each day!

You do have to wonder about Boeing contingency planning. Airbus situation won’t be that much better, they’ll be in trouble with component parts. Obviously they’re not stupid but..

Unless Boeing is crazy, there’s no way they go to rate 14 – and there are some good reasons for this belief. First of all, the 787-10 is a loser. You can get the same plane with the Airbus A350-900 Regional (or whatever ya’ call it) with the additional capability to convert your A350-900 Regional back into a Super-Plane with the changing of software (and off ya’ go to flying 8000nm sectors). On the other hand,the 787-10 will never fly 8000nm no matter how much you mess with it’s software.

Second, the 787-8 is a total loser. Forget it. Boeing is throwing into the scrap heap and they don’t want to build any more.

The 787-9 is about to get squeezed between the A350-900 and the A330-900. It’s going to be ugly for Boeing. The A330-900 is a very profitable and amortized aircraft: so Airbus can use it to exert constant pricing pressure on the 787-9. On the upper side is the A350-900 which still has ready-made improvements (from the A350-1000) yet to be rolled into its design. Additionally, the supplier structure of the A350 Program will let Airbus more effectively reduce A350 build cost than whatever Boeing can do with the 787-9. In short, the 787-9 is going to get caught in price/capability squeeze (or so I foresee) with no end in sight.

As a result of all these events, I don’t think the financial future of the 787 is promising enough to go to rate 14. Of course, Boeing just might increase 787 production to try to offset losses of 777 Program Revenue. I think that would be crazy…but “Crazy” has never stopped Boeing before.

Jimmy:

Yeah let’s pack it all in and call it day!!! The 787-10 is a dog, the 787-9 is a mess when compared to the A330NEO, and the A350-900 is the world beater? Let’s not let facts get in the way of a good story. I think the A330NEO will be a wonderful plane, that I think was a bad idea for Airbus to pursue. Never called them “crazy” for shoosing to build it but I missed the opportunity I guess. I now understand the A330NEO was created to support a justficiation to build the widebody completion center in China. In exchange for that deal Airbus got orders that have kept the A330/A330NEO transition line open. Hey, why should we let facts step into postings? Thanks for an afternoon break of hard work with some light humor. Leeham News and comments gets better and better with time!!!!

I don’t know Vincent, maybe ya’ out to call it a day. Because that Light at the end of the 787 Financial Tunnel is an oncoming A350/A330 Freight Train. Now, I’m not saying the 787 won’t make Boeing some money – it certainly will – but it will never be enough to cover deferred production costs and never be enough to.ne considered a “Cash Cow” (a “Cash Goat”…maybe).

And that’s a shame for Boeing, for if Boeing is ever going to develop a 737 successor (and they need one really bad) then they are going to need another “Cash Cow” Program to keep bringing the money in while they develop and begin to produce the single-aisle successor. They don’t have that Program, and it doesn’t look like it will ever materialize in the future.

So, yeah…maybe ya’ ought to call it a day and enjoy the Fat Lady’s Finale Song.

Or quit buying back stock!

@Transworld,

You are right. You make sense. But to Boeing Executives you do not make sense. Their job is to loot the company for as much as they can get before Boeing crashes. The more they lot, the bigger the pay. And screw the the worker, the taxpayers and the local citizens.

Caveat Emptoriuum Unber Alles!

The Canaccord Genuity note is particularly ridiculous, in my opinion: “We … believe there could be incremental pricing pressure on the 787-9s and -10s to be delivered in 2018-2020.”

Given that Boeing is ~100% sold for the 2018-2020 period taken as a whole according to the Ascend data, there can’t be incremental pricing pressure (at least in any meaningful sense) until post-2020.

More broadly, the fact that 787 sales have been quite slow since the late 2014 decline of fuel prices and launch of the A330neo means that there will be very little pricing pressure reflected in Boeing’s deliveries for the next few years. Nearly all of the existing order book still reflects the high fuel price order rush of 2007-2008 and 2013.

You always seem to see a bright sight on everything Boeing. They should hire you 😀

Old orders don’t guarantee good prices. Delta e.g cancelled their old 787 order and bought A330NEOs instead. Little positive here, or..

Don’t worry lads, the DoD has never let us down in a situation like this

How many options and purchase rights are there that could be exercised in the coming years? Firm orders alone don’t tell the whole story…

That is true, but if the environment is not positive, then those options and purchase rights not only do not get exercised, existing order get kicked down the road.

It not easy and denial is not a way to work it.