Leeham News and Analysis

There's more to real news than a news release.

Pontifications: 787 production rate remains a question

By Scott Hamilton

April 10, 2017, © Leeham Co.: Boeing’s first quarter earnings call is scheduled for April 26, two weeks and two days from today. Officials said on the January earnings call, for year-end 2016, that they will decide this year whether to increase the 787 production rate to 14/mo by the end of the decade.

LNC has long believed this won’t happen. In fact, we predicted last September Boeing will have to lower the production rate from 2020.

The question of the rate is sure to come up on the 26th. I doubt CEO Dennis Muilenburg will be prepared to announce a decision one way or the other. It’s Boeing’s pattern to put off announcements like this until the very last minute, so a go-no go on rate 14 probably won’t be announced until toward the end of the year.

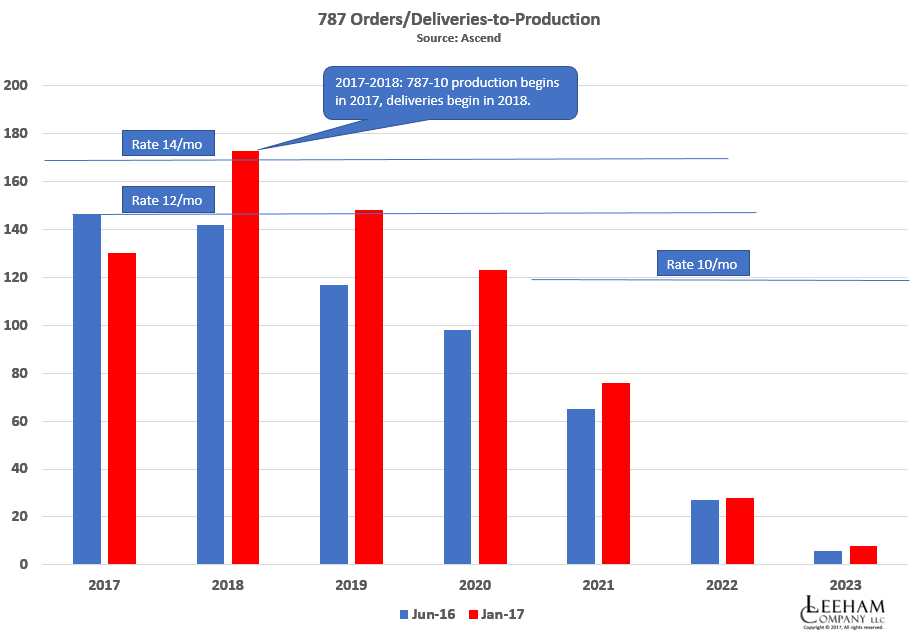

Struggling for orders

There were 80 firm orders for the 787 placed last year and 11 through last Thursday so far this year.

Figure 1. Click on image for a crisp view.

These orders helped fill the near-term production through 2019, according to an analysis of the Ascend data base. Figure 1 compares Ascend data from June(blue) and January (red). The current rate of 12/mo appears solid through 2019.

The fall in deliveries in 2017 and spike in 2018 reflects production of the 787-10, which reduces deliveries this year but spikes next year as accumulated inventory is delivered.

But so far, it’s clear visions of rate 14 aren’t supported.

Rate 12 a struggle

On the January earnings call, Muilenburg said Boeing sees no scenario in which the current rate of 12/mo can’t be sustained. A new cycle of replacement orders is coming around 2020, he says.

That may be, but the 787 competes with the Airbus A330neo and A350. The former is up to $30m cheaper to buy, market sources tell LNC, and Airbus appears on the cusp of adding more maximum takeoff weight to the A330-900, increasing its range to more than 7,000nm.

With Boeing all but abandoning the 787-8 (virtually none are ordered past 2020 and production of this sub-type is expected to decline to 1/mo in 2018), the new Middle of the Market aircraft (“7M7”) will effectively replace the 787-8.

Even the 787-9 is beginning to show some strain, says one lessor. Deferrals are popping up and lease rates–once routinely in the $1.2m-$1.25m range–have, on occasion, broken the $800k/mo level. It’s more common to see rates in the $900k-$1m/mo range, this lessor says (and so does an advisor to the industry).

Rate 10 seems likely

We still see a production rate of 10/mo on the horizon, as do some Wall Street analysts. One—Buckingham Research—forecasts a rate of 7/mo early next decade. We think this is a little aggressive, however.

I don’t expect Muilenburg to make any announcements on the April 26 earnings call. But I do expect questions.

Any rate reduction will come at the expense of Washington State, and not South Carolina.

With -8 basically disappearing, and all -10’s being produced in Charleston, that leaves only a portion of the -9’s for Everett.

7M7 fight will be tough to win for Washington, as will any new small aircraft. Will the price be to high for Washington taxpayers and the Unions?

IMO, MAX-10 will not be popular, if even sell-able. MAX-9 not competitive. 747 on life support. 777X not a big seller so far. Amazon may extend the 767-200F’s life. Perhaps.

Not looking good for the Evergreen State. The legislature had best wake up, and show some love for non aerospace related businesses, especially small ones.

Good points. As for the MAX10 they won’t build it unless they have enough guaranteed orders for a profit. It’s a stopgap measure anyway. 777X is a victim of a soft wide body market for sure (as is the smaller 330neo) but with over 300 orders already there is time for the market to rebound. I think Washington still has a Boeing future even with the hard bargaining coming up.

BTW Thanks Scott for putting this very informative post out for free! It’s nice to see data normally not accessible to the average plane fan.

Of these 25 airlines, 3 airlines have orders for the A330, whilst 24 airlines have orders / lease agreements for the 787. Half (12) of these airlines (reportedly) will migrate to an all 787 fleet.

Of the 120 A330 customers, only 29 customers currently have orders for the aircraft. This compares to the 787 where 57 customers still have orders for the aircraft.

Of these 29 A330 customer orders, lessors represent 23% of the backlog or 7 customers. Of the 57 787 order customer, lessors only represent 16% or 6 customers.

Approximately 23 airline customers (both A330 & 787) will have a requirement to place orders for the A330 / 787 in the immediate future. Of these 23 customers it is expected 15 will trend towards the 787, whilst 8 will trend towards the A330. Total orders could be as high as 600 aircraft, suggesting 400 new orders for the 787.

For reference, of the 57 customers who have orders for the 787, it could be argued many of these airlines have under ordered. For example, QANTAS mainline currently have orders for 8 787’s (which will be used to replace 747’s), whilst still having a requirement to replace 28 A330’s (2020-2025 period).

From 2019 onwards there will be a requirement to replace approximately 40 (20 yo) A330’s, 60 (22 yo) 777-200’s and 50 (23 yo) 767’s per year. Whilst some of these aircraft will be replaced by the A350, the majority will need to be replaced with an aircraft of a similar type.

Current 777-200 route trends suggest many of these aircraft can be replaced with an aircraft like the 787-10. For this market the A330-800/900 and 787-9 are too small and the A350/777 too large. Using an average retirement age of 22 years there will be a requirement for 499 replacement 777 aircraft up till 2025.

As such, orders for the 787 should pick up in the coming years. I just can’t see a situation where airlines would want to operate a fleet of 10-15 787 aircraft, when there is opportunity for them to simplify their fleets by operating 20-30 aircraft.

@ Travel

A very interesting and detailed post indeed but I feel you are being slightly bullish both in terms of the market as a whole and also Boeing within that market. The most fundamental issue is whether the replacement cycles will be met as the long haul market seems to be in a state of flux.

I am concerned that when we look at the market for 772/333 replacement there could easily be an element of double counting. The LCC move into the more tasty medium to long haul routes will chip away at the flag carriers core income meaning that replacements will be deferred and deferred. Further there are a lot of young, cheap lease aircraft available to take up the slack.

I agree that Boeing has had a very strong year against Airbus in widebody sales (comparative not absolute) but Airbus will have to respond and have the means to undercut all Boeing products quite significantly due to an advantageous exchange rate.

I am concerned that both OEMs are going to have a very uncertain couple of years with deferrals, cancellations and lack of significant orders being the main theme. I am changing my name to Voice of Doom btw

In the last 10 years the A330 have received more orders than the 787. For simplicity, let us round out the numbers and say that there has been a 50/50 division of this market segment in last decade.

Currently the production is 6 A330 per month and 12 787 per month, a 33/67 percent market split in production (not orders). While Boeing is very quickly burning of its backlog, Airbus has a reasonable production rate (balance between orders and deliveries).

Airbus has announced that it will produce the A330 at a rate of 7 per month from 2018. If the market split in the coming decade will be 40/60 in Boeings favor, and given Airbus’ rate per month, then Boeing should lower the 787 production to 10 per month. A rate for 12 787s per month (or even higher) seems to be unsustainable, unless the MOM aircraft will be a 787 derivative. 🙂

Concerning aircraft cabin size, the 787-10 and A350-900 are very similar, but have different capabilities. The former is a medium haul aircraft, while the latter is an ultra-long haul aircraft. The A350-900 have more powerful engines, larger wingspan and significantly higher MTOW. It will be interesting to see if the 787-10 will be more efficient on medium haul than the A350-900. Both will be excellent 777-200 replacement aircraft.

A few comparisons as a remark to your last paragraph:

Specification // 787-10 // 350-900

OEM // 136,9 t*// 134.7–145.1 t

MZFM // 192,8 t // 195.7 t

Fuel cap. // 126,372 l // 140,795 l

MTOM // 254,0 t // 280 t

Spec-wise the 350-900 is simply a 787-10 that can carry more fuel, if needed, so I don’t think the -10 will outperform the -900 on shorter routes.

* not yet released, so I extrapolated

= OEM[787-9] + (

(OEM[787-9] – OEM[787-8]) /

(Length[787-9] – Length[787-8]) *

(Length[787-10] – Length[787-9]) )

Just don’t know what is happening to the A330-900, no signs of the Trent 7000’s. This may play in favour of the 787’s.

If Airbus could offer a lighter A350-900 with lower thrust engines and 7000/7500Nm comfortable max range it, will beat the 787-10 in range and 787-9 in capacity. The current 350-900 being the “ultra long range specialist” (8500+Nm).

There is a market for a much lighter A330ceo with updated Engines, smaller slender wings with 4500nm range. Like a A330Re MkII.

It may not be that easy just to lower the 787 rate per month. Delivery dates have already been given to airlines and fleet planning depends on these dates. Remember when the 787 was late to EIS and airlines had to scramble to change fleet plans.

I feel the -10 will be the best seller so more orders will come soon.

Travel,

“Current 777-200 route trends suggest many of these aircraft can be replaced with an aircraft like the 787-10. For this market the A330-800/900 and 787-9 are too small ”

You neglected to mention the A359 above as you know it competes with the 787-10 directly and can fly further. Still though, I accept the premises of your argument. I think the 787-10 will win most of the routes in the future. I dont see how any of this is really relevant ro Boeing backlogs though.

You compare an airframe with shorter term deliveries ( A330) to one that was massively delayed and customers had ordered the bulk of outstanding orders a decade ago.

For a useful metric compare new A330 NEO orders with NEW 787 orders.

Hello Sowerbob,

I missed the first paragraph of my post when I copied and pasted from word.

This paragraph noted there are approximately 123 A330 and 63 787 customers, with 25 customers being both A330 and 787 operators.

This puts the rest of the post in context.

The intent of my analysis was to find trends rather than hard numbers. The reality is the numbers are suggesting airlines are trending towards the 787. I think this in part has to do with the versatility of the 787-9 and the economics of the 787-10, which should be the cheapest aircraft to operate on 3500-5500nm routes. These two aircraft are probably going to be a good combination for airlines.

As you noted the replacement cycle is a little hard to read. The US carriers are currently refurbishing 777-200 aircraft that are near the end of their 20 year economic lives, so as you suggest these aircraft could be retained longer than expected. I have used 20 years for A330’s as aircraft delivered prior to 2002 have a lower specification and are not suitable for upgrading.

As the A330 market is relatively fluid, I’d suggest the lessors / owners of these aircraft will have quite a few options in the secondary / part-out markets for aircraft coming of lease / becoming redundant to requirements. I would expect the lessors to part out the older aircraft and re-lease the new A330’s to ensure a neutral supply and demand situation.

The Boeing 20-year forecast for the small narrow body market suggests the market can sustain a production rate at 14 787’s and 6.5 A330’s per month from 2022 onwards. This would result in both OEM’s producing close to 100% of the total forecasted market. I still see a requirement for Boeing to raise production to 14/month prior to this period because there are just too many aircraft coming close to the end of their economic lives. For instance ANA and JAL have close to 70 passenger 767’s in service. Some of these aircraft have been earmarked for replacement by 787-9’s and A321NEO’s (already on order), but there is still a good forty aircraft that will need to be replaced by aircraft yet to be ordered. The US carriers 767 fleets are in a similar position.

To be honest I am really suspect on the A330NEO. I’d suggest Airbus is trying to increase its MTOW as it simply can’t compete with the 787. For instance China Southern and China Eastern, the two largest Chinese airlines have large A330 fleets, but only have 787’s on order. I think these two airlines prefer versatility and base aircraft economics over purchase price.

Even with the current volatility in the market there are quite a few airlines capable of placing new 787 orders. In contrast the majority of the major A330 customers have either ordered the 787 or A350 or currently aren’t in a position to order new aircraft (TK). Of the 29 customers with the A330 on order half of them only have orders for less than 5 aircraft (The majority around 1-3 aircraft).

@ Travel

Thank you again for your input, a lot to digest. It will certainly be interesting to see how the A330neo/B787 competition in China will pan out. One final thought in the absence of a NMA I was looking at the A330neo as the natural heir apparent at the top end to replace the large 767 fleets that must be coming to the end of their useful economic lives. You seem to be suggesting that these will be replaced by much more capable B787 variants.

This is a difficult one. Both 330 NEO’s are not really selling well, wonder if Airbus is working on a NMA/MoM as it appears they are also losing interest in their own product?

My suggestion would have been to keep the 330-900 as is with 242T MTOW (6500Nm).

Replace the current “800” with a stretch (2.42m/5 panels) that is between the 330-200 and -300 (330-“850”). Increase its MTOW to ~250T and give it a range of ~7500-8000Nm? (Landing gear upgrades and potentially 75K-lb engines will most likely be required).

That will give a 300 seater with 6500Nm range (with high density shorter range options) and a 270 seat aircraft with 7500+Nm range.

This pairing could be serious competition to the 787-9.

Even with the current volatility in the market there are quite a few airlines capable of placing new 787 orders. In contrast the majority of the major A330 customers have either ordered the 787 or A350 or currently aren’t in a position to order new aircraft (TK).

I think that perspective sort of ommits two key points.

1) 787/A350/A330neo are *not* mutually exclusive. DL is a prime example – they ordered A350 and A330-900 at the same time, when they already had 787s on order.

2) The A330ceo is still very much selling, i.e. the transition from CEO to NEO is a relatively soft one – not one where CEO sales suddenly fall off a cliff.

As a result of 1) and 2), the 787/A350/A330ceo/A330neo are not necessarily mutually exclusive.

Cases in point: China Eastern and Southern (the very same airlines you mentioned), as well as Delta Air Lines.

CZ ordered additional A330ceo and 787 at pretty much the same time in late 2015. MU ordered 15 A330ceos in late 2015, followed by 15 787 and 20 A350 in early 2016. If new or existing 787s at these two carriers don’t even preclude more A330ceos, it seems unlikely they would preclude A330neos at some point.

DL went from being an all-Boeing operator to inheriting 18 787 orders and over 30 A330s from NW – eventually ordering more A330ceo in 2013, A330neo/A350 in 2014, and cancelling their 787s in 2016. Those A330neo/A350 are “only” for replacing 747 and 767, plus additional capacity – i.e. A330ceo replacement isn’t even factored in yet.

Total orders could be as high as 600 aircraft, suggesting 400 new orders for the 787.

As I’ve tried to explain above, I don’t think it’s quite as simple as that.

Also, I’m not sure how you actually arrive at a market split of 66:33 in the 787’s favour with regard to the 767/772/A330ceo replacement campaigns over the next few years.

Overall, since the 787’s launch in 2004 the A330 and 787 have split sales almost exactly 50:50. However, that gives you a slightly skewered picture, because since 2008, the A330 has usually (with the exception of and 2013) outsold the 787. With a pretty healthy 65:35 ratio in most years. That’s also the total ratio you see from 2007 to 2017: 893 vs. 411 net. Even if you consider 2007 as well (the single best-selling year for the 787), you end up with a 57:43 split in favour of the A330.

Which begs the question why you think this long-running trend, which has been more than upheld in the last three years, is going to reverse in the future?

To be honest I am really suspect on the A330neo. I’d suggest Airbus is trying to increase its MTOW as it simply can’t compete with the 787.

As above, you might want to look at the orders sheets, though. Since its launch in mid-2014, the A330neo received 210 net firm orders. Since Janaury 2014, the 787 got 181 net firm orders. Even if it was the other way round, it would seem a bit far-fetched that the “[A330neo] simply can’t compete with the 787.”

Sure, bringing up the MTOW of the A330neo is a way of making it more competitive. It would basically bring the range of the A330-900 on par with the 787-9, while the -900 actually sits between the -9 and the -10 in terms of capacity. But that doesn’t mean the A330neo isn’t competitive already.

At ~30m cheaper per frame, the A330-900 actually seems like a pretty attractive proposition even before the rumoured MTOW increase that also brings its range within less than 10% difference to the 787-9.

“since the 787’s launch in 2004 the A330 and 787 have split sales almost exactly 50:50. However, that gives you a slightly skewered picture, because since 2008, the A330 has usually (with the exception of and 2013) outsold the 787. With a pretty healthy 65:35 ratio in most years. That’s also the total ratio you see from 2007 to 2017: 893 vs. 411 net. Even if you consider 2007 as well (the single best-selling year for the 787), you end up with a 57:43 split in favour of the A330”

Man that is statistical torture! Considering the monster order years 2005-07 and 2013it’s not surprising the 330 has the advantage in off years. There are only so many planes airlines need…

“Man that is statistical torture! Considering the monster order years 2005-07 and 2013it’s not surprising the 330 has the advantage in off years. There are only so many planes airlines need…”

Geo,

You hit the nail on the head.

In the A330 / 787 space (alone) the trends suggest there will eventually be 22 major airline A330 dedicated operators, 29 787 dedicated operators and 12-13 airlines who will operate both types.

Some airlines (Cathay Pacific) will migrate from the A330 to the A350. A different category again.

I know you love Airbus product so your analysis will always fight the Boeing order book. The A330-9NEO was a play to get as much as Airbus could from sales. Also, they wanted to get the big order of A330-300s from China for the completion center.

Biggest customer is AirAsia -66 frames, next Iran Air -28 (which is the newest order), then Delta -25, Air Lease-25, Avolon -15, CIT-15, Grauda-14 (who just canceled 6), TAP-14. The A330-800 has 6 orders. If Iran had not bought their 28, the A330-9 has not had much of a play in demand. Are you really sure AirAsia is going to take all of their 66? They have pushed A330-300s into -900s, so I would say that the customer base needs to grow. That has not happened in the past few years, and again without Iran there would have been nothing.

As Travel has said the demand seems to remain on the 787 side. When China places their next round of 787 orders, which will be in the next few years, those orders will be for 787-9s and -10s. They will not be coming to the A330-900 side, but will certainly move toward the A350-900 and some A350-1000s. The reason why Airbus is not picking up the output of the A330-900, there is no demand to justify an increase. An increas would mean the end of the program sooner.

Ever wonder why the price is so cheap for the A330 program? Because Airbus cannot sell the frame at higher prices. Scott has shared the soft market for the 787 and that is driven by the low price of the A330. I wish Airbus had ditched the A330 and went all in with the A350 and we would have a real competition in the wide body space. The 210 A330 sales in the A350 bucket would have made the A350 a real player. Airbus is really boxed in because the 787-10 is going to mop up the medium range space. It’s bigger than the A330-900, carries more than the A350-900, and there is nothing Airbus can do expect drop the price of A330 to stay in the space. Airbus killed Boeing with a strategy that has Boeing dead in the narrow body space. The A321 went to a place where an airline can address growth. Boeing is doing that with the 787-10, and airlines will go up to that frame for the extra seats. The A350 is too heavy to compete and the A330 is going up to fight the 787-9? Not a good move because the 787-9 now owns that space. That leaves the 787-10 alone in the medium space. So when China comes in for their medium demand where are they going? To the A321 and 787-10. Next play for Boeing will be to put the bigger wing on the 787-10 and make it an ER. If that can be done within tight weight restriction the 787-10 will be the frame to watch. The A330 has 5 good years left and it will be done.

“Next play for Boeing will be to put the bigger wing on the 787-10 and make it an ER.”

That would be a major revamp and expensive.

After 5 years in service a bit early.

On the tech side up against a wall. The 787 airframe is more “growth limited” than any Airbus frame.

First the market will be MOMified ( or not 🙂

I think your analysis underestimates the impact of long haul low cost travel. AirAsia X ordered 66 A330neos, Wow Air will lease four A33oneos from CIT and Air Berlin (soon to be Eurowings, ergo Lufthansa) will renew it’s fleet with neos leased from ALC.

From the LCC perspective, the Airbus looks like the better choice. The economics of the -900neo and the 787-9 won’t differ that much, they have similar specs and basically the same engine, but the neo is $30m cheaper. As a comparison: the Scoot 787-9 has a capacity of 375 Pax, the A330neo of Wow will seat 365 Pax.

Travle: Well done.

Anecdotally I had the same feeling myself, a bity of a edge to 787, not huge but kind of like the Constitution pulling away form the British fleet a slow but steady increase in distance.

Exactly what drives this I am not sure, some seems to be running dated technology though A330 obviously is competitive on certain routs and ranges.

It may be the flexibility hits it on the head.

One thing I have learned is that there is no exact right aircraft, its a balance between a whole route structure and a whole fleet and perfect is never accomplished.

You get as close as you can to efficient as possible but at best you may get 80 0- 85%.

We see United shuffling its fleet around now to do that.

You can likely add Aer Lingus in there in the medium term. Their ordered A350s will likely go to BA/IB as the a330ceo and neos are perfect for them, along with the a31lrs.

Too much aircraft/range, and too expensive comes into play with the new-gen air frames, and reliability/spares/know-how/MRO on current gen helps a lot.

I REALLY think Boeing is going have $$$ problems in the future. The 787 will take an age to make back it’s dev/prod costs, the necessary MOM is another huge cost with little income for a long time… and unknown final cost/market… the 737 is in it’s last iteration I would assume… the 777ceo~X transition is painful and the X market is fragile at the moment [but that could change by 2020]. Just seems like a lot of $$$ draws coming.

Aer Lingus is quite cunning…

I couldn’t agree more. They really need to hit the sweet spot with a MoM clean sheet design and then do their homework on the 737 and 777 replacements. Luckily for Boeing, the A380 and A400M constrain Airbus’ financial scope effectively.

CAPA recently had an article about the different business strategies of TAP Portugal and Finnair. TAP Portugal will operate a dedicated A330NEO fleet for the South American market, whereas Finnair will operate a dedicated A350-900 fleet to Asia. What is unique about this comparison is the strategies of both airlines revolve around a single long haul market.

In this example (both dedicated Airbus operators) the airlines have chosen the aircraft that best suits their needs. We could argue the A350 would be too much aircraft for TAP to fly to South America and the A330NEO not enough aircraft to fly to Asia (Via the North Pole).

Using the fleet plans and business models of these airlines for a basis to expand on the merits of the A330NEO, we can come to a conclusion the A330NEO may not be enough aircraft (range) for the route structures of other airlines where they serve multiple markets. On the flip side we already know the 787-9 is a very capable aircraft having good economics and capabilities on both medium and long haul flights.

For airlines like AirAsiaX their substantial A330NEO order is based upon a relatively large pan-Asian market. The aircraft are destined to fly from the out reaches of India, the Middle East and Australia/New Zealand, so there is a fairly large space for these aircraft to fill. They have A350’s on order, which have been earmarked for Europe.

I recently suggested the mooted Malaysia Airlines order for aircraft to replace their existing A330 fleet will be a strong indicator of how airlines will order in the future. They could order A330NEO aircraft like their competitor AirAsiaX, but in reality if they want to cover all markets (Asia/Europe/USA) the 787 is going to be a better choice.

Some have argued the lower price of the A330NEO to be an advantage. We have to remember, the 787 is capable of economically flying a combination of long and medium haul flights. This has the potential to increase the aircrafts utilisation rates (by combing long and medium haul flights in the aircrafts itinerary) to a level where the lower cost A330NEO advantage is partly nullified. In other words a 787-9 flying a long haul route from Europe to Asia and then a short haul from Asia to Australia will probably have higher aircraft utilisation than an aircraft simply flying medium haul routes.

The -900neo has a range of 12,130 km (6550 nmi), which is sufficient for most routes between Europe and Asia or Europe and North America. AirAsia X, for example, will use the neo to resume it’s London route (10.568,22 km air distance). I assume that Finnair simply needed more capacity because their asia business is running well.

Malaysia Airlines will order at Airbus. They leased six A350-900 from ALC already and have an option for two early A330-900. Since the A330 and A350 share a common type rating and their long haul fleet mix covers all distances needed, I see no sales potential for Boeing at MH.

China Eastern odered 35 A350’s last April. China Southern ordered 12 A333’s at the end of ’15. Smells like Boeing marketing.

I replied in another post that I have not analysed the A350 situation. I mentioned CX will transition from an A330 to A350 fleet, meaning even though Airbus lose an A330 customer, they will equally gain an A350 customer.

I have used the Airbus O&D sheet for my numbers. I just checked and China Southern doesn’t have a direct order for A330’s with Airbus. The orders could be listed with CASC which have an order for thirty aircraft.

If these aircraft are ordered through CASC than they would be, from memory be for the “Regional” A330(R).

“Current 777-200 route trends suggest many of these aircraft can be replaced with an aircraft like the 787-10. For this market the A330-800/900 and 787-9 are too small and the A350/777 too large. ”

The A350-900 proves the most popular replacement for 777-200’s so far. Hundreds being ordered as 777-200ER replacement.

“For instance China Southern and China Eastern, the two largest Chinese airlines have large A330 fleets, but only have 787’s on order.”

China Southern has 16 outstanding A330 orders, China Southern 15.

“To be honest I am really suspect on the A330NEO. I’d suggest Airbus is trying to increase its MTOW as it simply can’t compete with the 787. ”

The A330 proves an unexpectedly successful 787 competitor.

https://ffmbbg-ch3302.files.1drv.com/y3mFlxttaAV4zcVNCLGJpRI-RT79M3O3g89ePgu0mZ2xQqxA01qdpJfeB2T4n3qnB06VCo2y6nZyou65tL3JfaM2Eny9aHsgEMx17M5O4OalUosZeLbV9UZxFODNfjHpd_M30YnT3UaYNWz8O2BB9wtZNe74mpSIH5s8kp-q_Sa8Qk?width=780&height=462&cropmode=none

That has to be the longest link ever posted here. 🙂

Yes, the orders race does indicate the A330 is winning……but, we have to put this into a context.

We know from market intelligence there is a valid space for aircraft in the A330 / 787 size categories. We also know the market, largely has been able to absorb deliveries of these aircraft, which in recent years has maxed around the 170 deliveries per year mark. It is only recently that the market has come to a point of saturation.

We also know Boeing has delivered every 787 they can possibly could during the 2011-current time period.

From this perspective, if airlines (or probably more correctly the market) required aircraft in the A330 / 787 size category (2003 – current period), for many airlines the only real option would have been the A330. This is demonstrated by QANTAS who ordered / leased additional A330’s due to 787 delays even though they were committed to operate a single 787 fleet.

It is pretty obvious to see what the advantages for Boeing would be if they get a majority of these replacement orders in a new cycle starting around 2020.

On the other hand, what would be the consequences be if this cycle doesn’t happen, or it comes a year or two later than expected or what if they don’t get the number of orders for the 787 they anticipate?

“What would be the consequences be if this cycle doesn’t happen, or it comes a year or two later than expected or what if they don’t get the number of orders for the 787 they anticipate?”

If the 787 had a troubled past it certainly has a bright future now. But between these two positions there will be a plateau, where the B:B will be less than 1. As things stand right now we can expect production to stay at 12 for a little while, and then will likely have to be brought down to 10 or less. And the longer the order drought will last the lower the production rate will have to be.

When the 787 programme was in trouble the 777 and 737 were there to bring Boeing the cash it needed to get through this difficult period. But we are now entering a period when the 777 will burn more cash than it will make. Since the 777 is subjected to the same widebody drought as the 787 this may leave the old and partially incapacitated 737 as the sole money provider for what could turn out to be a long period of time.

But apparently there is nothing to worry about because Boeing thinks it has a solution: the NMA. They say it will address the middle of the market where there is a gap. Indeed there is a gap there, but I don’t think that gap is large enough to justify the expense. In my opinion there are much bigger gaps in Boeing’s portfolio.

The 777 is an impressive machine and it has no competition in its category. But we said the exact same thing for the 747 in its glory days. Then came the 777, which slowly, but surely, killed it. The same thing that happened to the 747 could also happen to the 777 itself with the newer A350. The 777 offered less capacity than the 747 but had a similar CASM and was less costly to operate. More or less the same thing could be said of the A350 versus the 777.

If they wait too long to plug those gaps they may become too big for Boeing to be able to do anything about them. We may actually already be there. That is how I would answer your question “What would be the consequences be if this cycle doesn’t happen.”

Well “the old and partially incapacitated 737” has over 4,300 orders yet filled so I would say that’s a pretty long term cash cow.

Many would debate your prediction your pessimism about the cash the 787 would bring in…

https://tinyurl.com/ltfpgpc

http://www.industryweek.com/finance/boeing-profit-gets-boost-787-goes-drag-rainmaker

If the 350 is going to kill the 777 it’s sure taking it’s time.

You also omit several sources of income….

The 767 is still bringing in cash and 68 models to go at least (not counting military derivatives).

The quite lucrative military and space sales, the defense division brought in 2.8$ billion in the last Q of 2016 alone.

Maintenance contracts is also a big and growing part of their portfolio.

If the 350 is going to kill the 777 it’s sure taking it’s time helped no doubt by the nibbling of sales the 330 is taking from it.

Overall yes wide body sales could bottom out if they haven’t already but Boeing still has plenty of other cash makers.

IMHO it’s not that bad of an outlook cashflow wise.

Sorry about the poor editing of my previous post!

I retire in great shame..

The 2.8 billion refers to cash flow BTW.

I thought you were displaying link envy

“If the 350 is going to kill the 777 it’s sure taking it’s time.”

Very little real detail has come out about the 777X, but we do know the lightweight carbon wing is heavier than the wing it replaces. The advantages seem to come from aerodynamics ( L/D and increased span) and higher seating density.

Maybe some airlines will want a genuinely lighter new generation plane?

“If the 350 is going to kill the 777 it’s sure taking it’s time.”

Isn’t that paraphrasing, “If the 787 is going to kill the A330, it sure is taking its time!”?

Just wondering if Boeing shouldn’t have started with the 777-8 instead of the 777-9 due to the slowing down in demand for very large aircraft?

This will give you an 777-300ER with “real” range.

Even though defense spending remains subdued in US, the Trump administration is anticipated to increase US spending on defense. Plus, on the 787 program, supplier pricing step-downs are getting underway. The fact that the 787-10 is a pricier model and many productivity/cost-reduction initiatives are being implemented will help Boeing’s margins in the medium turn. The 787 deferred production equilibrium is improving and will offer Boeing a tailwind on cash flow.

I guess much will depend on how well Boeing succeeds in reducing its costs on the 787. If they continue being as slow as now and are intending to make money on that line one day, the 787-9 will really only be sold to those that need the range and the rest will be 330neo.

If the dollar devaluates and Boeing reduces the costs, the 330 output will drop to today’s 767 levels soon.

It is clear that Boeing sold its first 200-500 787s much to cheap. Also, it is evident, that the 787 in the original configuration 2-4-2 is not competitive. The question is now, what is the real price tag for that plane.

Airbus can always go cheaper. Question that remains for me is: why does this game not work so well in 777 vs 350?

What I am struck by is the A330-900 increase range.

Hmm, didn’t we have all that in “original ” A350 Ver 1.0 or 2.0 before we got a whole new aircraft ?

Trying to compete with the 787 obviously and flailing.

And the -800 that looks to be toast.

Will Hawaii order 787-9 and or -10s?

Hawaiian , because of its position in the pacific doesnt need ultra long range. Thats why they have ordered A330 neos. ( to replace the discontinued A350-800)

They arent going to add 787 and mix up their fleet.

Well that is one take, but Airbus first forced the small A350 on them (the one they aren’t going to build) then it was, oh, here is the A330 you really wanted, but by the way, we aren’t going to build that small one either.

So in the end, maybe Hawaii just says the heck with you and buys the 787-10

Why would they go from A358/A338 to B78J? If they wanted a higher capacity they would have switched to the A339, and the B78J is even larger than that.

Airbus is busy messing with their clients, loyalty and fleet commonality only goes that far?

I can see a place for all three 787’s in the Hawaiian fleet in the long term.

Think they bargained that the 787-9 will have the same start-up problems as the Dash-8, and it didn’t.

I am more in line with rate 8 on the 787.

Help keep the prices up with a bit of a shortage.

For now it helps kill the A330NEO on availability alone, but once that is nailed then throttle them back to a real long term sustainability.

We saw what happened when they got carried away with the 777.

I don’t think 737/A320 rates are sustainable either.

@TW

Reduce the rate and the whole programme falls back into the red again. The cost base is heavily dependent on volume. So I guess the middle path of 12 will be chosen at end 2017 with a revision down (if needed) in mid 2019. Then they can concentrate on a single line in Charleston to the ire of many.

BTW $30m a plane seems quite a saving if you don’t need the range

Doesnt make sense to concentrate in Charleston, that limits your ability to increase the rate again when orders pick up. They might only happen at the end of the 787 life- that could be over 20 years away.

Charleston is under utilized. They have a second line they can open up.

What I think is going to happen is that the MOM is build in Everett and they shift the whole 787 line to Charleston.

Initially that was impossible as the Everett plant was teaching Charleston how to do it.

Not a single major piece is made in Everett, small stuff can be moved to Charleston with the 747 Guppies.

I could be wrong of course , they could make the MOM a competition with all the hulaalbaloo but it would be the best utilization of facilities they have.

That’s going to be the real test of Mullenberg and if he is sane or not and not taking vendettas out to the detriment of Boeing as a whole.

The 787 debacle should be heavy on their mind, if it had been an all new site and all the other issues it would never have made it (my opinion of course)

You don’t want to have an all new workforce and an all new aircraft.

Also a new aircraft is in line with what the far more experienced Everett facility can do without assembly issues (others are not site specific)

Sowerbob:

And if you have white tails?

You have to go with what is needed, there is no free lunch.

Charleston can handle any 787 needs into the far future. Its not used to its max (pun intended) and its a logical split.

@TW

Keep pumping the numbers and hope for an upturn, the traditional way of dealing with uncertainty. The volumes drives the cost base down and gives the sales team more scope on price going forward. I think it has been described as the sporty game for precisely this reason

A rate for 14 787 per month seems only sustainable if the MOM will be a 787 variant. With the 787-8 having few orders left I could envision a MOM as a 787-6 and 787-7 aircraft with a 52 meters wingspan.

7 per month for 787-9 and 787-10, and

7 per month for 787-6 and 787-7.

= 14 per month

@ meg

So a return to the 787-3 in some shape or form. It has always seemed the most obvious route to follow and you are presenting an additional compelling reason for developing it. Perhaps Boeing have to accept that the unit return on this model will be negligible but that by maintaining 12/14 a month production rate it marginalises a key reason for the A330’s existence and drives down the overall cost per unit of the programme as a whole. This would certainly force Airbus into a corner.

Limiting the MTOM and/or redesigning the wing is an option open to Airbus as well and might result in A330neo regional variants. Considering this, the MoM should be a clean sheet design.

Cant see that happening, the cost structure of the 787 has pushed it out of the -3 and -8 versions. A lower production rate of another different but lower priced version doesnt make sense.

Shorter range of MOM is even harder to produce advantages against an A330 type plane

Boeing essentially vacated its 757-767 market with no airliner sales there for the last 1o years, building for the US carriers isnt the be all it once was. [They keep their planes for too long- wouldnt you rather build for Asian carriers who change their planes from 5 to 15 years!]

I’m rooting for the A330-900 with 2-4-2 seating, as a validation that there’s inherent value in less middle seats, seat width, and aircraft comfort. 787 economy seating is LCC territory.

That does seem a sweet layout, especially if your sitting in the window seat.

Am I one of the few who think a 767MAX would do rather well? I don’t see the A321NEO being a true TATL plane meaning operating all year round with no fuel stops or sizable weight restrictions. The 767 at 220 seats and a 5000 mile range could fill smaller European and South American routes that will not support the large end twins.

I like the 2-3-2 seating and have always enjoyed the flights to Europe on the 767. Its still in production and with some weight shedding and new engines, it should have good appeal to many airlines.

I agree. The current 767 has these major design problems

1) lower fuselage lobe is too big, diameter could be reduced to decrease weight and surface drag and use the common narrow body baggage containers.

2) wing too big, could do with 757 sized wing and new engines

3) not fly by wire and all that goes with that, but could have ‘part FBW’ like the 737 max and 747-8

Advantages are it would use existing type certificate and just be a derivative.

Use of the existing front fuselage ( the most expensive part of fuselage to design and build) and the KC46 has paid for the new instrument layout- similar to 787?

My name for this blend of 767 and 757 is 767-5

It might not satisfy the purists, but airlines arent the most profitable business sectors and cost of planes is very very important.

But if you are going to spend a fortune on a B767MAX, something in the region of $7-10 bn doesn’t it make sense to evolve the B787 airframe instead? You get the front fuselage, FBW and the low weight for free. The fuselage length can be cut down and the single major expense would be the new wing. It would simplify the production needs at Boeing, retain capacity if necessary on the B787 line and could be sold at marginal cost plus.

This way the derivative is near state of the art rather than reworking yet another old frame. As the B787 technology matures this derivative would be a link to the future rather than revisiting the past.

What concerns me about the B767MAX idea is that Airbus would revamp their A330 sufficiently to compete and hence nullify it before it is out of the box

Steve:

I thought it would as well but there has been zero interest from Boeing end.

I have to assume its existing deficits for what is needed simply do not work for the MOM markets Boeing has identified .

I would think there is a bit of hope as it seems to have morphed into a larger MOM, ie the 767 replamcentment so many are after.

You have to weighty that with is it appealing not the ones who want it because it will be lower cost than the 767 MAX even with all its possible increased efficiencies (engine, winglets and some clean up?)

Once you do a new wing AND an engine you are into a new aircraft.

I do feel your frustration as I have not seen it laid out well as to why.

NOTE: UPS is now buying used 767s and doing a PTF conversion on them. They can’t get a 767 from Boeing as the production is too low and FedEx got in ahead of them.

That is ironic.

More likely theres cheap 767s parked in the desert and new 767Fs are relatively pricey. Its tough times for the air freight business so that have to look very hard at their capital expenditure.

You should read the news.

UPS is buying and converting JAL 767s. not picking some junk up out of the dessert.

While I doubt there are any 767Fs parked, this is a long term investment so you want the newest and best shape aircraft.

Also 767F is a hot commodity. Lot of demand.

You get that from JAL and ANA.

And yes I see them flying back through Anchorage all the time to the Stares.

UPS paid the price when they bought them for a reason as they did the 757F.

You can bet they aren’t going cheap.

They also are buying upwards of 28 new 747-8F when you can get 747-400 of various types all day long.

Geo: “Well “the old and partially incapacitated 737” has over 4,300 orders yet filled.”

Yes the 737 order book is full and will indeed provide Boeing with plenty of cash for a relatively long period of time. But my understanding is that the margins are not as high as those for the 777; reportedly less than 10 millions per plane, which is still pretty good though considering the number of aircraft on order. But you can’t deny that it is old, for it is turning 50 this year. And when I say that it is partially incapacitated it is a play on words that refers to the fact that the 737-9 is not doing that well and the 737-10 is not getting much traction either, and may in fact need a “walker” to get to the end of the runway. This is all double entendre of course.

Geo: “Many would debate your prediction your pessimism about the cash the 787 would bring in…”

It is not pessimism, although it is not optimism either, nor is it a prediction. The only figure I mentioned was the B:B ratio of less than 1. This may not be good news but it is no fake news.

Geo: “If the 350 is going to kill the 777 it’s sure taking it’s time.”

It took 10 years for the 777 to kill the 747 and this only started to happen when the 777-300ER was introduced.

“The 767 is still bringing in cash.”

If this was the case Boeing would not try to replace it with the NMA. The reality is that whatever is left in the order book was sold at a very good price for the buyer. As to the military version Boeing has already lost a few billion dollars on it, and like for the 787 it will probably take a very long time for Boeing to get a decent return on its investment.

Geo: “The quite lucrative military and space sales.”

Space I don’t know, because of the abundance of new players. As for the military things are indeed looking good right now. And this may bring Boeing back to the same situation it was in before it became the preeminent commercial aircraft manufacturer that it no longer is.

767 is a different story. They have a lot of FedEx orders and the KC46.

UPS may buy some as well latter on when they can get them.

Right now they need them so they are doing PTF.

It obviously has some future as a freighter.

The 767 just seems to be no what the airlines need (or want) for the 767 pax replacement. Cash is not the issue, its what they can sell them for and the pax market.

I think the 787 will be able to stand on its’ own two feet for many years to come. Boeing predicts orders for small wide body aircraft will represent 60% of the total wide body market over the next twenty years.

That’s a lot of aircraft. More than 5500 aircraft to be exact!

At this stage the MOM is the cat amongst the pigeons. If it can win success in the market for airlines wanting to fly 3500-5000nm routes, the A330NEO may end up having too narrow a market to justify its existence.

“Boeing predicts orders for small wide body aircraft will represent 60% of the total wide body market ”

They tend to say only things that are self serving. If they really believed that they wouldnt have done the 747-8 and unlikely they would have done the 777-9 as well. As they are niche products.

In reality they dont know the future all that well but have to cover eventualities and defend their market share.

I use the Boeing forecats as they have been proved (history) to be the more accurate of the forecasts out there.

As such if Boeing predict 60% of the wide body market will go to the small wide body sector, I stand up and listen!

If this prediction were so true and accurate, don’t you think Boeing would have launched something appropriate by now?

Not if they were waiting for the technology to catch up.

Prediction is very difficult, especially about the future.

— Niels Bohr

Not surprising coming from a guy who couldn’t decide if something is a wave or a particle! 🙂

Aero Ninja:

There is a vast difference in people performing (the predictors) and getting management to get their head out of the jet exhaust and do what they are supposed to.

US Intelligence was screaming at the Generals that the Germans were doing something serious in the Ardennes. Management ignored that, we know better. Nasty bit in the butt for the guys on the ground.

The best people and work are limited by the worst of management.

” use the Boeing forecats as they have been proved (history) to be the more accurate of the forecasts out there.”

Some people have graphed Boeings forecasts over time, there are some very surprising short term swings, which can be only explained as ‘aligning their prediction to what they will be building’

LNR put it much better

leehamnews.com/2017/02/20/pontifications-boeings-long-term-message-doesnt-resonate/

Yet still more accurate than Airbus has been in widebodies.

Travel: “The A330NEO may end up having too narrow a market to justify its existence.”

That is an interesting statement, for I had the exact same thought about the NMA. Since day one I saw it as a very interesting concept that actually answered a certain demand in the market. But at the same time I aways believed that “it may end up having too narrow a market to justify its existence.”

One thing we do know for sure is that the A330 already exists and the A330neo is fast becoming a realty as well. And the latter presents itself as an efficient straightforward evolution of the former. But who knows, Boeing could surprise us with the NMA. But the risk involved is in my judgment higher than for any other programme ever developed by Boeing, except for the SST, which was backed up by the government, and the Sonic Cruiser, which was promoted by a bunch of lunatics.

Travel: “I think the 787 will be able to stand on its’ own two feet for many years to come.”

I agree with you on that. Like I said in a previous post I believe the 787 has a bright future. But what worries me is what will happen between now and that future. What I do worry about is the immediate future, which in aviation can be defined as the coming years, because aviation cycles tend to be quite long. And right now we seem to have entered a down cycle in the widebody market.

The way I see the situation at Boeing I would be inclined to say that this could not be happening at a worse possible time. This has to do with the convergence I have been talking about for a couple of years now. What I always had in mind when discussing this convergence is that the Boeing portfolio was evolving in such a way that it would not take much in terms of the unexpected for Boeing’s business plans to collapse.

Well, the unexpected has now arrived. Perhaps it was not totally unexpected, but we had been used for a number of years now to a continuous stream of orders more spectacular than the previous ones, and for both manufacturers. Of course Airbus is also hit by the same invisible market forces, but the impact will likely be less damaging because it finds itself in a less vulnerable position. You can call this luck if you want but Airbus is arriving at the end of a costly development cycle whereas Boeing is at the beginning of such a cycle.

There is no question that however successful the 737 has been in the past, and still is to a very large extent today, that it is arriving at the end of its career and retirement is in sight. On the other hand the 787 is just starting its own career and its best years are probably ahead, and not behind, as I once thought. But right now it is more cashflow neutral than positive. In other words it is no longer hurting Boeing’s balance sheet, but unfortunately it is not at this time contributing that much either. This is why Boeing wants to go to 14 a month as soon as possible. But possible it is not. Not now anyway.

With the 777 the situation is totally different. On the one hand, like for the 737 it might turn out to be one iteration too many; but on the other hand it may not die as honourably as the 737 is now assured to do.

For me the problem with the NMA market is that it does require a plane in the 767 size and weight bracket. The A330 and 787 are both in a bracket a couple of notches larger than this.

If the MOM, as Boeing describes it goes ahead it will be a lot more economical than a 787 or A330 for its chosen route profile. Both of these planes won’t be able to compete.

We also know (this came from Airbus themselves) the A330CEO is more efficient at short haul flying than the NEO. This implies, if there is demand for the A330 (no MOM) in the short haul market, the space will largely be filled by existing A330CEO’s, not new A330NEO’s.

For instance I can see QANTAS using their existing fleet of A330’s for the domestic market, where I can only see QANTAS using their new 787’s on the international market.

I am not as pessimistic about wide body sales as you are. We are the start of a relatively large replacement cycle and as such new planes will be required. We are talking close to 150 planes per year.

Keeping older aircraft may give airlines a couple of years of grace, but at the end of the day these planes will need to be replaced. They can either spend money on new planes now to achieve an economic advantage in five years’ time or they keep flying older planes, pay for the extra fuel and maintenance and see that money disappear when the planes are finally replaced.

I think the fundamentals are there for new wide body sales.

Not only that. The MOM / NMA / 797 will be the first real option for LCC medium to long-range travel. This marked is HUGE and has nothing in common with the current 787/A330 market dominated by the old flag carriers.

The MOm will create it’s own marked independent of the current A332 – A330-800/787-8 situation. The market isn’t static.

First real option for LCC medium/long-haul? Airlines like Norwegian (787) and AirAsia X (A330) would disagree with you on that.

thysi is right, existing options are there, even including using the 757

Yes, you can always by a 787-9 or A330-900 as a LCC to do long haul. But that are very expensive large planes with massive capabilities many LCC Airlines don’t use.

The MOM will broaden the possibilitys for charter and LCCs regarding medium to long houl connections by a significant amount.

And it will be the number one option for high frequency intra-asia medium runs done by the A330-300 ATM.

Where is the swap over in efficiency between a “MOM” style less capable airframe and the purportedly overranged more capable types? More fuel carrying capacity out in the wings is structure wise “cheap”. Even without fuel loaded the larger wings provide for an advantage.

@Uwe

Not when you’re looking at the root chord of the wing in order to determine the actual size of the wing.

Page 10: http://www.fzt.haw-hamburg.de/pers/Scholz/dglr/hh/text_2008_01_30_A380.pdf

For example, the root chord of the A330 wing is 10.6 m while the root chord of the A310 wing is 8.4 m. For an A330neo-derived “MOM-type” aircraft sized roughly between that of an A300-600 and an A332/A338, the wing could have about the same wing area as that of the A310 wing. However, it should be more slender than the A310 wing — i.e. wingspan increased towards 50 m and a reduction in root chord by one metre, or so. Hence, the structural weight of an all new composite wing box with those parameters should be almost half that of the structural weight of the A330 wing box — even with an aspect ratio higher (>11) than the aspect ratio of the A330 wing.

Travel: “For me the problem with the NMA market is that it does require a plane in the 767 size and weight bracket.”

I have identified the same problem, but I came to a different conclusion. You see, a plane can either be too big for its market or too small. And this is different for widebody aircraft than narrowbody ones. There seems to be a set of ideal sizes and ranges for each category. The trick is to find the perfect combination and you have a winner.

One good exemple is the 777. In its first iteration it was struggling to find its mark. Then Boeing decided to add capacity and range in a perfect combination that pleased the market. The magic formula had been found. This actually had for effect to pull the rug from under the 747’s feet.

In the narrowbody market we have this interesting duel between the A320 and 737. The latter’s most successful variant is the 737-8 and its predecessor. It is preventing the more modern A320 from taking the whole market to itself because it offers a slightly bigger capacity that can compensate for its deficiencies; especially in a market that seems to be moving up a little and which now makes the A320 look a bit small. And that’s why we now see the A321 gathering steam. Of course we would see the same phenomenon with the 737 if its genetic inheritance had given it longer legs. But dwarfs normally don’t give birth to long-legged children.

What I am getting at is that the 797 will be too small for its category. What is confusing everyone, including Boeing itself, is that its capacity and range combination appears to be perfect. It certainly does to me. But most people have forgotten why we moved up from the 767 to the A330 and 787. The same thing happened then that was simultaneously happening with the 777. These moves up in terms of capacity and range is what made those aircraft so popular.

That is one of the reasons why I think the 797 will falter in the market. The other reason is that it will certainly be too small for a widebody airplane to be structurally and aerodynamically as efficient as a narrowbody aircraft or a larger widebody. So I don’t expect it to make much of a dent on the A321 market and I believe the A330 won’t budge. That is my prediction anyway.

But there is not much risk for me with such a prediction. All that could happen is that I might be proven wrong. But for Boeing the risk involved is enormous.

I have to disagree (other than the long legged children, that had me choked up)

So lets step this back and look at the Iconic Ford Mustang.

Right car, right time. I am not talking about the hot rod versions, I am talking new mom and dad, first couple of kids, with a 6 cylinder engine and an auto trany.

Did that market ever go away? No, it was filled, but by better designed cars with a 4 cylinder engine and eventually that had 4 doors and you could fit 3 kids in the back.

My wife and I have ranged upwards as large as a F-250 pickup with a moderately ((for its size) economical engine (and still have it) Its way too big for the normal mission (one person to somewhere) but its paid for and most of the traffic can be shifted to the other vehicle.

But we also found that a Passat Station wagon did about t90% of what her limited two door Bronco did and vastly better fuel economics with some of the latter generation bennies.

Not unyutpicial sitaitons. If you can find that magic sweet spot as we did with the Passat, it works.

And that seems to be what its all about, a magic sweet spot tech wise that is reasonably low cost, economical and you are not going to upsize.

The Passat has gotten bigger, but they then shifted the Jetta into its spot as that market is not gone.

Where this splits really is car maker use marketing and the image to up size a care and get more money for it, but they always fill that slot with something else.

So what that tells you is that there always was (or did developed) a market above what your original Aircraft research identified, and they upgraded existing to fill it.

That still leave the market below it.

Now there are far more carriers,s various cost structure (fuel) and what worked in the past (too heavy is ok, it don’t cost that much) is now not working.

So, the MOM can come in, fit a market and not have to upsize as that upsized is well covered and the name thing is not the same as cars.

Again, this assumes Boeing can pull it off and get the right package put together. Its possible they can’t do it with what they have now.

But to just rule it out as that’s always the way its gone I think is a mistake.

“So, the MOM can come in, fit a market and not have to upsize as that upsized is well covered and the name thing is not the same as cars.”

Well, I don’t mean to insult your parents, but your MOM is anything but a POP (Perfectly Optimized Plane). 😉

I think another important aspect of the A330 / 787 discussion is the make-up of orders and how airlines plan to introduce the aircraft into their fleets.

From a historical / media perspective we have often focused on the large orders from the ME3, up and coming Asian LCC’s and the Chinese carriers. With the advent of the NEO and MAX and the subsequent order books, we probably have a perception on what should be normal when airlines place orders for aircraft (i.e. large orders) when what is normal is probably quite different to these perceptions.

If we consider the KLM / Air France Group for instance, these two airlines have placed orders for a total of 25 787 aircraft. They have also entered into agreements with leasing companies for the supply of additional aircraft.

The two airlines currently fly a total of 24 A330’s and 9 A340-300’s, meaning they probably have a requirement for a further 35 787 aircraft. They already have 9 787’s in their combined fleets (8 leased, 1 owned), meaning they could have a requirement for an aircraft in the 787 size category for approximately 45 aircraft. If we consider the group could use the 787 to replace other types (747, 777-300ER), as we have seen happen with other airlines, there could be a requirement for more than fifty 787 aircraft.

This doesn’t seem unreasonable for two airlines the size of Air France and KLM.

The question becomes, if these two airlines have a requirement for more than fifty 787’s than why have they only ordered 25 aircraft?

The reality is the two airlines have already made substantial commitments to existing (other) aircraft (types) and as such, regardless of the merits of the 787 they have to use these aircraft in the best possible economic way (They use them to fly passengers all over the place).

For instance, the Air France A340-300’s are coming very close to the end of their economic lives and as such it is not unreasonable to suggest these aircraft will start to be replaced over the next year or two. The Air France A330’s are a little younger, but again will be up for replacement over the next 4-8 years. In contrast the KLM A330 fleet is relatively young and will not need to be replaced for another 10 years.

For the fleet planers they could decide the 787 is the best aircraft to replace the Air France A340 and A330 fleets. How they retire all of these aircraft and introduce the 787 will be dependent on a number of factors. Training, spare parts, contract agreements with third parties (lessors, financiers) will all have a bearing on how old aircraft are retired and new aircraft introduced.

Where I can see the Air France / KLM group having a fleet of 35 787’s by year 2025, I can’t see them having a fleet of 45 or even 50 aircraft by this time. They just have too many young aircraft in their fleets that will need to be kept to ensure they obtain an economic advantage from owning them.

If we now consider QANTAS using the same system of thinking we have a very different situation. They currently have 11 787-8’s in the Jetstar fleet and are about to introduce 8 787-9s (replacing 747’s) into their QANTAS International fleet. They currently have 28 A330 aircraft that will be due for replacement from 2021 onwards. If we consider replacement, growth in new markets (North Asia markets currently experiencing exponential growth) and general growth, QANTAS could have a requirement for an additional 30-40 787’s over the next seven years. They currently do not have orders for any of these aircraft, even though they have made repeated commitments to the aircraft type.

As per my original posts there are quite a few airlines in similar positions to that of QANTAS.

My analysis suggests there are currently 29 airlines who will need to commit to new aircraft in the A330 / 787 size category over the next few years for a total of ~600 aircraft. I suspect 22 of these airlines will order the 787 over the A330, meaning Boeing could receive orders for an additional 400 aircraft (600×67%, my analysis suggests 470 aircraft).

If my assumptions on order cycles is correct, than airlines placing incremental orders for the 787 is going to be the new normal, but with the exception being there are going to be quite a few of them (5-10 orders per year).

Some additional information:

Air France-KLM has also 28 A350 on order.

Qantas ordered 14 B787 back in 2006 for a rather modest price. Only 5 more were ordered in 2015.

I expect many airlines to wait until the A330neo is in the air with robust information about fuel burn rates.

A330-900 is about 64 m long.

A340-600 was even longer than 75 m.

What about an A330-1000? Range about 5,000 nm. A big MOM?

I think that is a bit of a diversions.

The A330NEO is a pretty well known quantity.

Hesitation to order has nothing to do with the fuel burn down the .001 percentiles.

There are 3 airlines and one leaser that are hot for the A330NEO.

Delta , Air Asia and Hawaiian (and Hazy I )

Hawaiian has got to be ticked as they keep getting short changed.

Air Asia is extremely speculative.

We will see, there is far more long term upside to the 787 than there is to the A330.

I still think its long term is rate 8. That fits in historic norms.

@MHalblaub

An 11-13 frame stretched, 251-tonne A330-1000 is a no-brainer IMHO. However, while the A330-900 and an A330-1000 would be too large to be considered to be “MOM-type” aircraft, both an A300-sized and an A332/A338-sized aircraft would not be too large (IMHO). What is required, though, is both a significantly smaller A310-sized composite wing and an A310-sized horizontal tailplane (HTP). Hence, a cheap Airbus “MOM-type” wide-body family would have two members significantly larger than the A310 where both aircraft are optimised for intermediate range. MTOW should be similar to the MTOW of the A310 — some 100 tonnes lighter MTOW than the enhanced A330neo (i.e. 150 tonnes vs. 250 tonnes). In short, what I’m talking about is a significantly stretched, next-next-gen A310 (i.e. the A310 was shortened by 13 frames over that of the A300), that would use the existing A330neo cockpit, fuselage and empennage (minus HTP). Type designation could be either A310-800/900 or A330-500/-600.

Addendum

Rgds, OV-099

On reviewing my example of Air France / KLM, it looks like Air France will use 10 787’s to replace 10 A340-300, 5 787’s to replace 5 777-200ER and 21 A350-900 to replace 20 777-200ER which will be due replacement when these aircraft start to arrive.

The Air France A330’s have just recently had their interiors refurbished, so this would suggest they will be in the fleet for another 5 years.

For KLM the waters are somewhat less clear. Some suggest the 747’s will be kept longer (because of low fuel prices and ownership costs) and the A330’s (on lease) will be phased out. Last year 3 A330’s were returned to lessors.

It has also been suggested that KLM will transfer its A350 to Air France. This is based upon KLM statements about a fleet structured around the 787 / 777, which have similar type ratings.

If this is correct KLM will need to order / lease additional 787 / 777’s as they will have a shortage of aircraft.

As such, even though we can (almost) safely assume KLM will need substantially more 787’s over the longer term, it is currently difficult to define exactly how many 787 aircraft they will need over the shorter term.

Again, this is a situation of an airline that has an immediate need for 787 aircraft, but where the do’s and how’s of achieving their fleet goals is currently not known.

I see more 787 orders!

The Airbus twin aisle was killed when the original A350-800 program was canned by Mr. we know who.

He also don’t want spend money on upgrading the landing gear for a higher MTOW A330NEO.

On the NMA/MoM, “we have it covered”.

Burning money on the A350-2000 concept which is a born loser.

On the A320+, we are out selling Boeing on the single aisles and don’t want to wake them up to develop an NSA?

Airbus have a great future?

The A380 and 350-2000’s ego trips of some that is busy killing Airbus.

There is the 787-10 that is already flying.

Qantas 789s ( 236 seats) will be unlikely to replace the 747, which seat 371 in their operation.

Their long range A330-300 seat 297.

So far they have indicated 789s will be used on new routes, but of course could add frequencies on existing routes.

Eight 787-9’s (8 x 236= 1888) will replace 5 747-400’s (5 x 371 = 1855).

QANTAS are migrating from a P2H to P2P route strategy with the 787-9.

Or maybe just adding frequency on those same routes.

Will Qantas use 3-3-3 seating in economy for the 787-9’s for these ultra long haul flights?

Hi Travel,

What will the 787-10’s seating capacity and range be if they they do the equivalent outlay to it than the 236 seat 787-9?

I couldn’t agree more!

…but throw in a few 787-8’s and you would almost have the perfect the fleet. Good for long, medium and domestic routes with one plane type and pilot rating.

“QANTAS are migrating from a P2H to P2P route strategy with the 787-9.”

Thats not going to help them for their two largest hubs , Sydney and Melbourne.

Are they going to drop hub destinations like LAX, Singapore, Bangkok, Tokyo?

P2P is just marketing spiel from Boeing,[ very very few of the 787 routes are P2P] and its not even original, old Douglas hands will recognise as their marketing back in the 60s when they were trying to sell their offering against the 747. We know how that turned out.

Yes, Melbourne and Sydney are QANTAS’s two largest markets. With the 787-9 Brisbane just might become their third.

The 787-9 will allow QANTAS to fly their passengers directly to their final destination. New York, Dallas, Vancouver can all go P2P, whilst at the same time QANTAS can maintain its presence at Las Angeles. San Francisco as a direct flight could be back on the cards.

From this perspective, flying 8 smaller capacity 787-9’s using P2P route structures could be far more economical than flying 5 larger 744’s using P2H route structures.

To further illustrate I could be flying from Brisbane directly to San Francisco in the not too distant future. This would save me one stop over and at least 4 hours of flying.

From a passenger there would be a lot of appeal associated with such a flight.

After handing over their non SYD/MEL European Business to EK, SYD and MEL are about all they have left. It appears that A350-900 ULRs migh be in the frame. They can and just started doing Perth -London with B-789s but it is reported that evn if it had the legs they want something bigger. I havent seen anything about B778s yet, but Aus pax are screaming about being transferred to EKs 777s so that might not be an option.

Worth a read

https://www.bloomberg.com/news/articles/2017-04-12/delta-reviewing-14-billion-wide-body-jet-deal-in-blow-to-airbus

Any delay is only impact on Airbus as there are no Boeing jets in this mix.

And another possible hit to both A330 and A350

Regardless of the immediate impact, I think this should be a worrisome sign for both A and B, as cuts by DL will likely end up shrinking its twin-aisle capacity. It currently has 8 744s and 58 763ER (total seat capacity about 17,000) and 25 each of A339 and A359 on order (total seat capacity about 15,000).

Cuts in the orders would surely end up reducing DL’s long-haul pax capacity. Canary in the coalmine?

Delta appears to be worried about excess capacity that is starting to develop in the market.

They have 25 x A330-900’s and 25 x A350-900’s on order. What is more simple and flexible than replacing it with 50 x 787-9’s?

There could be. Delta cancelled the Northwest 787-9 orders (18) end last year.

Maybe they are reconsidering? At this stage the 330NEO is starting to look like a white elephant without legs (engines).

200 orders is not bad for an engine -less plane.

If you only want trans atlantic or intra asia , and you have the A330 in your fleet , this is your plane.

……….but, if you want intra Asia, Europe and the USA, than it (A330NEo) is going to be a plane with many short comings!

Don’t get me wrong, I really like the 330’s, from a passenger point of view it also much more comfortable to fly in than the “horrible” 3-3-3 of the 787’s.

But look at the orders, AirAsia-X 66, Iran 28, Delta 25, TAP and Garuda 14 each, and 40 from two leasing companies. That is about it. Think cancellations/reductions/deferrals are unfortunately also very likely?

But where is the engines, things has gone very quiet?

Get the “NEO” certified with GE CF6-8E1’s and get it flying. Sure there will be takers for such a variant!

If the cheap CASM at any price theory keeps eveloping opt for a 9 wide A330 NEO and beat everybody. God help us pax who have our tickets bought by the boss.

And for the doubter

http://www.bizjournals.com/atlanta/news/2017/04/12/ups-purchases-first-used-boeing-767s-with-new.html

Doubters of … what? 767 P2F is pretty common, given how inexpensive used 767s are.