Leeham News and Analysis

There's more to real news than a news release.

IAG’s low-cost airlines.

By Bjorn Fehrm

September 06, 2016, ©. Leeham Co: We continue our series about the European legacy carriers’ LCC arms. Now we cover International Airlines Group or IAG.

The LCC approach of IAG has a more local focus than for Lufthansa Group. Europe’s leading LCCs are based in UK/Ireland. Yet IAG, with its main brands, British Airways and IBERIA, only has a Spain-centric LCC, Vueling, and since June a Spain-centric long-haul LCC brand, LEVEL.

IAG’s LCC strategy

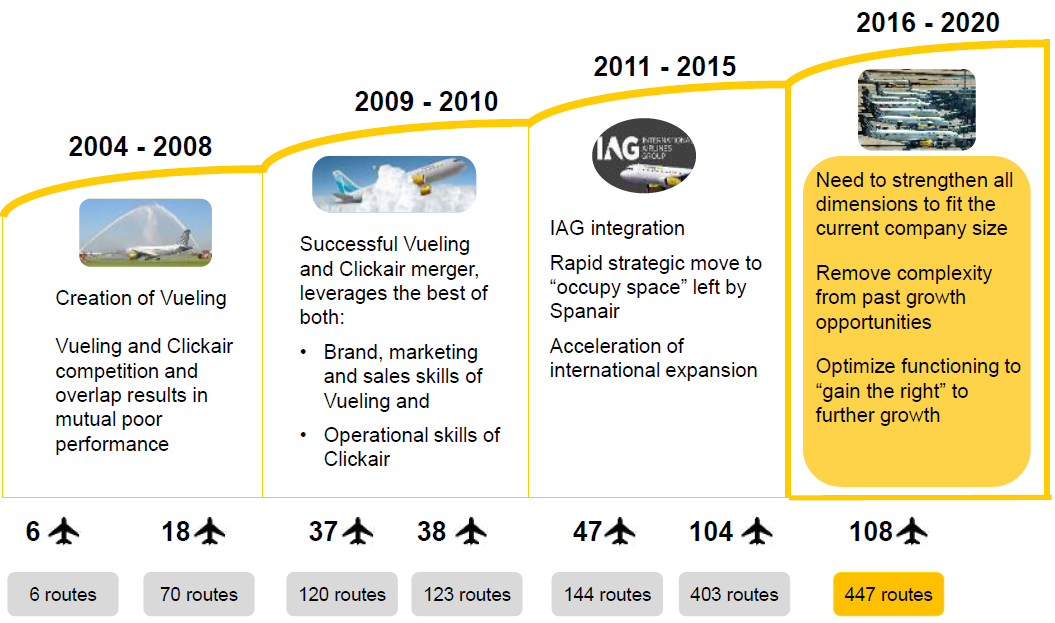

IAG, with British Airways as leading airline, has avoided a direct confrontation with the strong LCCs on its home market, Ryanair and easyJet. Instead, it gradually acquired Vueling with IBERIA, figure 1.

Figure 1. History and development of Vueling. Source: IAG

Vueling was started in 2004 by investors with a Barcelona base. It merged with the competing IBERIA-controlled Click-Air in 2009 after some tough years for both. IBERIA was then minority owner with 45.85% of shares.

The merged airline under Vueling brand grew to 150 routes by 2011 operated with Airbus A320 series aircraft. Then IAG bought 44.66% of Vueling shares, giving the IAG group a 90.51% share of Vueling.

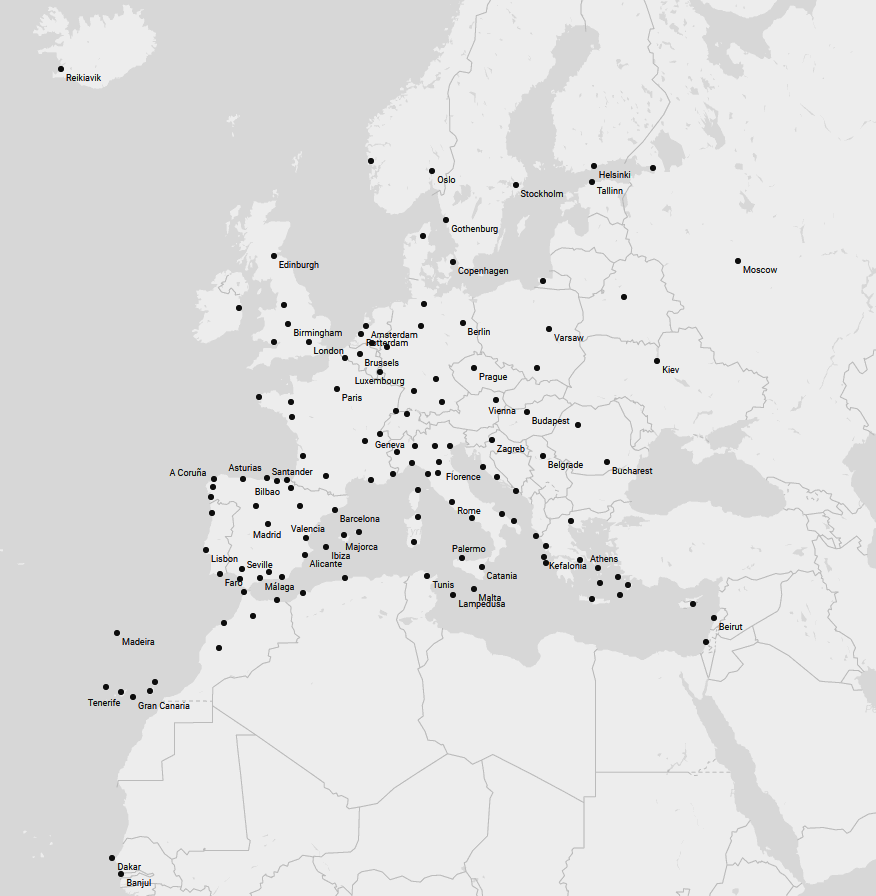

The early growth was centered on Spain and south Europe, with Rome and Toulouse as new bases. Today the Vueling network covers a large part of Europe, Figure 2. Largest hubs are Barcelona and Rome.

Figure 2. Vueling destinations as of 2017. Source: Vueling.

The growth has been steady, with about 20%-30% additional passengers transported each year, Figure 3.

Figure 3. Vueling’s growth over the years. Source: Wikipedia.

Vueling is today an airline about the size of Lufthansa Group’s Eurowings before the merger with Brussels Airlines. Vueling is, since January 2017, about half the size of Eurowings Group and lack long-haul operations.

IAG long-haul LCC

IAG has launched its long-haul LCC counter against Norwegian/WOW Air as LEVEL, a separate brand operation, reporting direct to the IAG mother.

LEVEL is also Barcelona based and is operating since June 2017 with two new Airbus A330-200 with 314 seats (21 Premium Economy and 293 Economy), Figure 4.

Figure 4. LEVEL A330-200 with 314 seats. Source: Wikipedia.

Initial destinations are San Francisco, Los Angeles (US), Buenos Aires (Argentina) and Punta Cana (Dominican Republic). These are all Spanish-speaking, long-haul destinations, with flight times of eight to 12 hours. They can therefore not be operated with single aisle aircraft.

A further three A330-200s are on order, allowing a future expansion of the route network from other European cities like Rome, Paris and Milan.

The aircraft are operated by IBERIA, with IBERIA crews. As the operation grows, the intent is to set up a company based on LEVEL, with headquarters in Spain.

Why a separate company and not a new arm of Vueling?

We will complement the review of IAG’s LCC arms with an economic review tomorrow. It will show that Vueling has a long way to go before being cost competitive with easyJet, Norwegian or Ryanair.

LEVEL was therefore started as a new entity to allow costs structures to be optimized for the long-haul LCC model. Vueling will act as LEVEL’s feed though, tickets can be booked with Vueling and LEVEL, which continue with the other airline to final destination.

Thanks Bjorn, the LCC’s are an interesting topic. Not want to criticize IAG/Vuelling but the 29″ pitch on their A320’s is not great, was forced to fly one trip with them due to circumstances. Read somewhere Ryanair is going 31″ on the MAX200’s?

Lots of “luxuries” are taken away when you fly LCC’s, as they are moving longer haul competition will be tugher. How much will Level for example gain in reality (as most others, including legacy airlines) flying their A330-200’s (for example) at 30″ pitch vs an airline flying 32″ pitch.

Flights over 4 hours are different than 1 and 2 hour hops. The difference in price for slightly more legroom could be less than the taxi/bus fare on the other side?

@Anton:

“How much will Level…gain in reality flying their A330-200’s at 30″ pitch vs an airline flying 32″ pitch.”

The math is actually pretty straight forward fm total cabin space consumption perspective. At every 480″ of usable cabin length:

FSC generates 15 rows of Y seat @ 32″ pitch.

vs

LCC(e.g. Level) generates 16 rows of Y seat @ 30″ pitch

i.e. in the same cabin space on a 332, LCC is 6.7% more productive than FSC. Out the gate @ the start just by playing with seat pitch alone, Level has a 6.7% op cost per seat advantage over anyone using legacy seat pitch set-up. At the low-end Y segment shopping for flights mostly by price comparison across all airlines on booking websites, it’s not uncommon for consumers to choose an airline based on just 3-4% fare diff….let alone 6.7%. Most of them hv received an avg of 1-2% or less per yr in terms of pay rise for nearly a decade anyway.

“difference in price for slightly more legroom could be less than the taxi/bus fare.”

That’s exactly the kind of Y mkt segment LCCs are targeting AND in fact growing globally. Yes, these consumers will accept(or not even notice) 2″ less legroom in order to use the savings to help pay for the taxi/bus ride on the other hand…..every cent/penny counts toward their very small trip budget.

Many consumers notice. They even complain bitterly on travel review and seat map sites, with threats to “never fly this airline again”, only to be back in the 29″ pitch misery the next time a needed sun break arises.

Such is the lower-end leisure market, and I don’t see that changing since the flight is just to be endured so that the destination can be enjoyed.

As long as these ULCCs offer a tolerable Y+ product up front, the option to hop one for people on a more discretionary travel budget does have some appeal!

@RaflW:

But far more pax @ the low-end segment do not noticed because those who do complain @ online reviews anywhere are vastly out-numbered by the mass across the globe flying in 28-29″ Y seat pitch and continuing to do so….in fact, more than ever before as shown by the pax traffic growth date practically for every LCC on earth.

In any case, complaining dissatisfaction re seat pitch is 1 thing. How these pax react in terms of their future purchase decision is clearly another matter. Consumer mkt statistics clearly show vast majority of these ‘complainers’ may react by switching carriers but they simply continued to fly in the same/similar Y seat pitch @ similar fare level.

“As long as these ULCCs offer a tolerable Y+ product up front, the option….does have some appeal!”

Y+ likely hv sufficient appeal for some pax to actually commit a purchase but sales volume is clearly in the minority relative to sales volume for std Y or even Y-. The most amazing paradox is that if the majority of Y pax are indeed avoiding 28-29″ pitch and many operators are already offering Y+ alternative, why these pax don’t choose to buy more Y+ but choose to continue complaining more instead? IMHO, pretty econ logical for operators, FSCs or LCCs, to plan cabin/seat pitch set-up based on actual sales data across Y+, Y and Y- instead of relying on negative seat reviews against 28-29″ Y seat pitch by even millions of Y consumers….

I don’t know whether there are or aren’t, but maybe there are currently restrictions on UK and/or German basing of IAG LCCs going back to pre-IAG BA’s sale of its own LCC units Go (to Easyjet) and Deutsche BA/DBA (to Air Berlin) last decade.

I’d say that BA (especially their LGW 777s) are more and more becoming an LCC product in economy…

Sad but all too true…

BA is operating an aging A319/A320 fleet of ~110, they only have orders for 25 A320NEO’s, the 10 A321NEO orders appears to be intended to replace older A321’s.

Question/conclusion, is BA in the process to scale down its short haul operations and leave more routes to Vuelling/LCC’s?

This brings me to another question, are there really a future for short haul routes operated by legacy airlines in Europe in the typical format? Flights are seldom more than two hours (excluding the time spend in a holding pattern!!).

Maybe that’s why BA is going premium in the front and LCC in the back?

Could this result in a demand for smaller aircraft such as the CS100/300 operated in a “premium” layout and also faster check-ins while the bulk of passengers are carried by LCC’s?

@Nick:

Re all these comments about BA’s Y product becoming more LCC-like especially the 10 abreast in Y on a few 772s based in LGW, I found these comments very amusing as an outsider because:

1. Most BA customers in Y complaining are based in Europe /U.K.

2. AFKLM has been doing 10abreast in Y on almost ALL of their 777s for nearly a decade and their combined 777 fleets easily out-number BA’s.

3. AFKLM is also based in Europe and AMS hub is especially popular for non-London UK customers connecting for intercon flights.

4. We rarely heard complains about ‘AFKLM becoming more and more LCC like’ over the past 10yrs yet it suddenly became a massive consumer uproar when BA start copying AFKLM on a few BA 777s.

May be BA customers are more special/deserve better Y products than other major EU airline customers?

It is true that AF/KLM isn’t much better but:

British Airways A320, 180 seats (new/refurbished)

KLM 737-900 (Yes, the -900, 178 seats)

AF A320, 148 seats (EU variant)

AF / KLM has 20 kg bag, seats reservation, meals onboard etc. at no additional cost.

BA charges (more than the LCCs) for seat reservations, check-in luggage and charges for meals onboard. BA has the same seat pitch onboard their new/refurbished A320 as Easyjet.

All I can say thanks heavens there are airlines flying A330’s and more A350’s to come!

Wonder if it will be possible to do a 3-5-3 squeeze on the 777X?

Are there enough emergency exits ?

Intriguingly, will Boeing have to demonstrate a full 10 across emergency evacuation on the 777X or will they be allowed to get way with a ‘modelled’ exit plan based on the plane using the 777 type number ?

@Anton:

“thanks heavens there are airlines flying A330’s..”

Yes, thanks heavens for the 9abreast in Y on every 330 in AirAsiaX fleet which is already flying 8-9hrs sectors such as KUL-NRT and KIX-HNL.

330 is the best human creation since slice bread and Boeing should shut-down the 787 assembly line to stop spreading the inhumane suffering by Y pax on the 9abreast Nightmareliner….

“thanks heavens….more A350’s to come!”

Why? 350 does not provide ‘good’ Y seat pitch by default. It’s the individual 350 operators who get to make that kinda of decision, isn’t it? It’s a bit strange/wishful thinking to automatically assume every 350 regardless of operators is a gift fm heaven for Y pax relative to other types….

“Wonder if it will be possible to do a 3-5-3 squeeze on the 777X?”

Likely. After all, it’s not only possible but in fact certified for 350 to do 3-4-3 layout complete with mkting/promo photos of a demo cabin in such layout published by Airbus a few yrs ago.

Max cabin width on 350 is 23cm and 35cm narrower than 777 and 77X respectively….

And BA’s 787 are significantly less comfortable than any LCCs A320 or B737….

Agree, 787 at 3-3-3 and 777 at 3-4-3 with 30″ pitch of legacy airlines are significantly less comfortable than 330’s with 2-4-2. Why bother with food on the legacy airlines, there are no elbow space to eat it?

Just hope Airbus can do something with the A330-200 (other than the -800) that it stays attractive to for LCC’s to operate.

Got a feeling Boeing could go 17″ on the 797 (2-3-2), at least just one middle seat then, or are they going to go 2-3-2 just wide enough that airlines can operate it 2-4-2 at 16.5″ seat widths?

Boeing will be blowing smoke on the 797 for a long time yet… look how long it took to ‘fully define’ the 737-10, it was almost a year to choose between articulated or levered undercarriage .

At this rate they will be dealing out scraps to fight over till 2025 on the winglets…. the cockpit design… the seats…

@dukeofurl:

“Boeing will be blowing smoke on the 797 for a long time..”

Probably will be as long as how long Airbus has been ‘blowing smoke’ about the 380Neo/Plus, 350-1100(i.e. that mythical 350 as large as a 779) and 322Neo(i.e. the beefed-up 321Neo)…

“look how long it took to ‘fully define’ the 737-10, it was almost a year to choose between articulated or levered undercarriage…”

If U truly understand the re-certification & supply chain readiness factors/considerations involved re that type of decision regardless of an Airbus or Boeing type, U wouldn’t be questioning why it took a yr…

“At this rate they will be dealing out scraps to fight over till 2025 on the winglets…. the cockpit design… the seats…”

Must be news for U that the winglets, cockpit, seats, etc. on the Max10 are 100% common with the Max9 design which has not only been built but also flew to the Paris show a few mths ago and scheduled for cert less than 0.5yr fm now….

Boeing is claiming that the 777-X will be able to accommodate 18″ wide seats in 10-abreast configuration.

https://skift.com/2014/07/23/boeings-new-777x-designs-intensify-the-race-for-space-on-airlines/#1

So 16.4″ seats in an 11-abreast configuration?

If you borrow an inch or so from the aisles you get to 16.5″. Sure someone will do it and I won’t fly in it.

@thysi:

16.4~16.5″ seat width already in operation for yrs onboard 330s in 9abreast.

s542:

“BA’s 787 are significantly less comfortable than any LCCs A320 or B737″

How so?

Y seat pitch on BA’s 787 is @ least 31in. In contrast, no 320 in any European LCC offers Y seat pitch beyond 29”.

In terms of seat width, Boeing specifically designed the Y seat on 9 abreast 787 to match the 6 abreast 737…..don’t take my word for it, go check the detail specs(e.g. ACAP on Boeing.com: http://www.boeing.com/assets/pdf/commercial/airports/acaps/787.pdf

It is easy

– the seat in 787 is much thicker than the one in most NB – i.e. less space left for legs.

– the seat in any A320 is wider than the seat in 787 in 3-3-3

s543:

“the seat in 787 is much thicker than the one in most NB”

The problems with your claim as above are that:

1. U started with saying “any LCCs” and now U shifted to “most NB” which implies inclusion of seat pitch on 320/737 operated by FSCs more generous than LCCs. U changed your premise/criteria and of course it becomes easy to explain.

2. Now my turn to ‘shift’ premise/criteria: Y seat has to be thicker on BA’s 787(in fact, any widebody type in modern longhaul cabin config @ any FSC) than on “most NB” because the former must accommodate a seat-back AVOD system while the latter rarely does.

3. Per 2. re FSC’s Y seat on WB are thicker than on NB. But the typical diff is more like 0.5~1″ and nowhere near 2~3″ as U claim.

“the seat in any A320 is wider than the seat in 787 in 3-3-3”

A factually & technically correct statement which I knew U would eventually bring up.

Unfortunately, the seat width diff is more like 0.6-0.7inch if U check the relevant official Airbus/Boeing specs published….just a tad more than the width of a std USB socket or 3-3.5% diff in seat width. “significantly less comfortable” due to that degree of diff? U must hv really sharp sensitivity(or a laser measuring equipment) to detect it…. 2mths ago I was flying 2 sectors back-to-back connection in Y 1st on a 9abreast 789 and then on a 320. Frankly, I couldn’t detect/feel any diff in their seat widths.

Firstly the A320 has ~1″ advantage on seat width, Wizz is flying their A320’s at pitches between 30″- 32″, not sure about easyJet.

I found Jetblue’s (US) 320/1’s very comfortable whatever it is, my airline of choice in the states if it is serving the route/s I am flying (if I am aloud to make such an statement).

@Anton:

“Firstly the A320 has ~1″ advantage on seat width”

Yes, in your dream…but not in reality such as aircraft cabin specs.

Give an example of ‘reality’, say from a carrier with both 737 and 320 flights

United does seem to have a 1 in difference ?

On the 320/1 there are the option of 17″ or 18″ depending on the aisle width which the airline selects, with the 737 its basically 17″.

The interior cabin width of the A320/1 is approximately 7″ wider than the 737 (146″ vs 139″).

I don’t know its an option but 17″-19″-17″-aisle could be an interesting option on the A320/1’s for the longer haul routes?

Aer Lingus have just launched a LCC ‘fare’ on their long haul operation called saver, whereby checked baggage, blankets, and headphones are not included (but can be added)… To compete and align more closely (but still ahead of) ULCCs.

I think existing carriers should use their fleets and differentiate their economy cabins better instead of setting up entirely new brands… Seems like such duplication and effort for little financial return.

BA’s densification is the idea (10-across a 777 or 9-across an a330)… But… It should be done ‘at the back’ of normal economy and sold as an ‘LCC’ seat… With a ‘saver’ fare (clearly identified). As this cabin sells out.., you move to (what EI calls) a ‘smart’ fare… And that features regular economy seats (9-across a 777, 8-across an a330) and spacing.

A few rows of premium or comfort economy… And ‘fares/seats/pitches/inclusions’ to match the price.

From the comments its apparent the the format of Legacy airlines Y-class is impacted due to the rise of the LCC’s.

Question/observation, why is “pure” LCC’s not flying medium-long haul such as Ryanair, EastJet, Wizz, Jetblue, Indigo. etc but mostly those with affiliation to Legacy airlines such as Eurowngs/Air Berlin, Level, Scoot.

Don’t know where to place Norweigan?

@Anton:

“Question/observation, why is “pure” LCC’s not flying medium-long haul..”

Read more about WestJet(Already serving LGW-Canada), AirAsiaX(Already flying 10h45m sector fm the U.S.), CebuPacific(Already flying 9h50m sector to DXB), LuckyAir(Already serving Moscow-China), none related to any FSC, then U’ll understand your question itself already started with the wrong assumption.

“…such as Ryanair, EastJet, Wizz, Jetblue”

A very U.S.+EU centric list…..no wonder U are unaware of the facts outside these regions contrary to the assumption in your question.

Claiming JetBlue is “pure” LCC is even more ironic when their super-premium(i.e. product specs on-par with the latest, best intercon J offered by US Big3 such as DLOne) Mint product is being expanded rapidly across JetBlue network right in front of our eyes while your presumably non-“pure” LCC Vueling does not hv a seat with more than 29″ seat pitch….

“such as…Indigo”

Must be news to U that Indigo is precisely planning to go longhaul right now. They’re just deciding which way is more feasible basically with:

a) Buying AI longhaul ops which is being prepared for sale by the Indian gov’t

or

b) Start fm scratch and build its own longhaul ops.

“Don’t know where to place Norweigan?”

If Norwegian is not “pure” and their 14h10m SIN-LGW sector is not longhaul by your definition, I don’t know what is your definition.

Thanks for the info FLX, I predominantly considered (U)LCC’s flying into Europe, I should have included WestJet.

Just read SpiceJet also want to join the Longhaul looking at the 787-10 and A330-1000, so real big volume stuff.

@Anton:

U are welcome.

“I predominantly considered (U)LCC’s flying into Europe..”

Pretty certain Europe is not the only place on earth blessed with short, medium or long haul (U)LCC services these days….especially when the 3 brands @ AirAsiaX already operate a total fleet size of 333 x30 with 339 x66 more scheduled to join later….

“SpiceJet also want to join the Longhaul looking at…A330-1000”

Pls educate me on what exactly is a “A330-1000”?

Finger problems, should have been A350-1000.

An conceptual A330-1000 has been mentioned a few times, ~4.8m stretched A330-900, +40 pax, 76Klb engines, range 5500 Nm range. (Tail strike limits?).

This could potentially have fitted in with what SpiceJet appears to be looking for?

The price should be good, maybe they could become a launch customer? There are future production line capacity for the A330’s.

@Anton:

Just read no widebody for SpiceJet due to acquisition cost. Enjoy:

https://www.flightglobal.com/news/articles/new-widebodies-costs-prevent-long-haul-low-cost-lau-440979/

Bjorn, in the following article you say the cash operating costs of the A332 don’t disdvantage Level vs the Norwegian B788s.

Would the increased cash cost of A338s be paid for by better operating costs ir not?

Can Level move on to A339s in the future and gain an advantage, or are the NEO upgrades insufficient to give the A339s enough range to take over the A332 routes?

Didn’t Norwegian take some of the terrible teens? Does this have an effect on B788 economics vs A332? I would have thought these airframes we’re capital light and no worse than new ones in our current cheap oil environment.

Some interesting points, the Trent 7000’s will have significant weight, drag and cost penalties compared to the Trent 700 but 10% lower fuel consumption and 50% longer “on-wing” times.

Maybe the A330-“800’s” day will come with the availability of the Ultrafan engine and laminar flow wing?

@Anton:

” the Trent 7000’s will have….compared to the Trent 700 but 10% lower fuel consumption.”

I recall Airbus has been claiming 14% improvement 330Ceo vs 330Neo so i guessing your “10%” is only about net SFC gain fm the engine swap alone.

“the A330-“800’s” day will come with the availability of the Ultrafan engine and laminar flow wing?”

1st of all, both features are currently in very early tech concept/demonstrator developmental phase not specifically linked to any aircraft program while the 338 is already a production-focused program(at least in theory even if sales data don’t support eventual production).

But the biggest question re your question is:

When UltraFan & Laminar flow are ready for integration into an aircraft development program, what’s stopping them fm being applied to non-338s and retaining advantages over an Ultra-Fan+Laminar Flow equipped 338?

Anyone knows what’s happening with A330-900, its mid-Sept 2017.

@Anton:

Basically delayed about a yr fm original Airbus schedule(2H2017). 1st flight won’t happen until End17 with 1st delivery to TAP not happening until @ least mid-2018. Earlier related news here:

https://www.flightglobal.com/news/articles/tap-a330neo-deliveries-at-least-a-year-away-pinto-437522/

Thanks, heard about September 2017, as long as its this year!

Hopefully AB used the delayed time well to work on increasing the MTOW to ~248T?

An 8000+Nm A330-800 variant could also make some airlines think twice about selecting the 787-8/9.

Such an aircraft will actually supplement the 350-900 and not compete with it. It could potentially serve the same routes as the 359 at times when lower seat capacities are required.

@Anton:

“Hopefully AB used the delayed time well to work on increasing the MTOW to ~248T?”

No such plan ever announced by Airbus and given Airbus history in developing higher MTOW 330 variants, they always announced such variants 2~3yrs in advance of cert/delivery….if for no other reason than to be able to start telling the mkt about such variant is coming so they can sell it in advance of cert/delivery?

In any case, the 1st 339 prototype(possibly the 2nd one too by now) had largely been built mths ago and sitting around @ Toulouse doing nothing but waiting for 1st set of T7000 to arrive. Luckily, latest news i’ve read is that Airbus has begun installation+integration+early system tests @ the assembly line….. power-up not yet achieved though. Somehow i feel Airbus’ effort on 330Neo program fm now till @ least 2019 will be 100% focused on ground test and then flight test+cert for 339 so delivery to TAP won’t be delayed too much nex yr and then move on to repeat the same for 338(if this thing ever gets to fly at all)…. not figuring out how to squeeze 6t more MTOW and go thru an additional cert cycle.

The 330 platform entered service 23yrs ago roughly as a 228t MTOW frame. To reach yr hypothetical 248t MTOW, it’ll be squeezing 8.8% more fm the original design limit. Not impossible but becoming very tough loading on that main landing gear structural design that has remained largely unchanged for well over a quarter century since 330 launch in 1987.

“An 8000+Nm A330-800 variant could…”

If Airbus could do that without incurring too much cost+development/cert complexity+fuel burn disadvantage, they would’ve planned it that way back in 2014 upon 330Neo program launch….not suddenly in 2017 or beyond. 788 performance was already a known quantity and not a fuzzy target for Airbus to aim back in 2014.

“..could also make some airlines think twice about selecting the 787-8/9.”

U honestly believe any rational airline interested in 338, 788 or 789 has not asked Airbus whether a 8,000nm 338 has a reasonably good chance to appear(After all, that’s exactly the mkt process behind the genesis of 321LR)? Or those same airlines hv not already thought twice about 338 before committing to 788/789?

“It could potentially serve the same routes as the 359 at times when lower seat capacities are required.”

Very true…if op cost is no object. Do U honestly think a 338, with whatever range capability, will achieve a fuel burn per seat level anywhere remotely near a 359?

If it somehow does, sales prospect for 359 itself will actually be doomed.

That’s a comprehensive response. All I am trying to say is the the 359 and 338″LR” could form a good combination on routes where different capacities are required based on seasonal and/or weakly seat requirements.

The 338 (HGW) will never match 359’s seat mile cost at full capacity but it will have a lower DOC with 200pax than that of a 359 with 200pax?

Hope a competitively prized 330-200″E” could stay in production for some time with the NEO’s wing and interior updates but with CEO engines. I see a particular application for such an aircraft for GE operators and/or LCC’s such as LEVEL.

I copied this form Keesje (Thanks in advance).

On closer inspection the 330NEO wing let actually looks not bad.

https://leehamnews.com/wp-content/uploads/2014/07/screenshot-2014-07-14-19-01-43.png

Three recent articles relevant to the topic.

http://c.newsnow.co.uk/A/901281461?-303:3665:0

http://c.newsnow.co.uk/A/901278772?-303:3665:0

http://c.newsnow.co.uk/A/901275708?-303:3665:0

A “long-range” LCC destination from Europe to the US that I feel is under developed/exploited is to Seattle.

It could serve as a connection/hub to the US (South-) West, Alaska, Hawaii, Vancouver, etc. Flight distances from Europe will range from 4000-4500Nm depending on port of departure.

Seattle- London using great circle is 4800 miles/7700km. That doesnt allow much for margins, delays or winds if you are looking at a new longer range single aisle.

Rules out much of Western europe as they would be further.Its not in Boeings interest to undercut its 787 either.

The A321LR is 4000nm /7400km so is a bit too short for pacific coast destinations from Europe

This is why the delay for Boeing for a MoM. Too much range and it undercuts the future cash flow for the 787, too little and it runs into the A321LR territory. So its delay delay.

There must be some resistance from the big airlines who would say’ If we give you substantial launch orders, the LCC will then buy it and compete with us

I had twin aisles in mind for Europe to Seattle.

On the MoM front, there are lots of “catch2’s” out there, capacity and range combinations, that why Boeing battles to “freeze” a design.

For me its sometimes simple (always is when you a spectator), the 2-3-2 is ideal for quick turnaround times on the ground, so shorter haul (<2000Nm), high volume routes. But there is always the thinner routes and/or direct city pair model/use.

An aircraft with approximately the 787-8 seating capacity (~240), 2-3-2 cabin layout, OEW of around 65T, an efficient range of 5000Nm and 45Klb thrust engines is probably whats required? (Guess folding wingtips to put it in Cat-C is another head scratcher for Boeing?).

Such an aircraft should not impact on the 787-9, the 787-8 seems to be dead in Boeing's eyes in any case.

If you throw the 757, 767, and 787 in a pot and add 2020 herbs and spices to it you will probably get an 797?

@dukeofurl:

“This is why the delay for Boeing for a MoM. Too much range and it undercuts the future cash flow for the 787, too little and it runs into the A321LR territory. So its delay delay.”

Not exactly.

If U’ve been following various MoM/797 inside stories reported elsewhere and right here on leehamnews.com over 1-2yrs, U would know range being too close to 788 or 321LR hv little to do with Boeing’s long assessment re the program’s viability.

The biggest obstacle/dilemma to launch 797/MoM for Boeing is not its technical definition(i.e. potential customer sources who hv seen the concept described a single widebody family in 2 sizes/variants – 1 with seatcount being a bit larger than 321LR/752 but with nearly 763ER range while the other being 763ER size but with 321LR/752 range). It’s the targeted price range vs estimated production cost:

Most customers interested in 797/MoM=

Want to pay no more than a bit higher than the most expensive 321LR/Max10 for sale today.

vs

Boeing=

Development+production cost will be approaching the traditional low-end widebody territory.

“There must be some resistance from the big airlines who would say’ If we give you substantial launch orders, the LCC will then buy it and compete with us..”

Which is a very very shaky assumption to start with because:

1. When Airbus/Boeing were deciding to launch 320Neo/737Max, every potential customer in the biz knows everyone will buy them regardless of ‘big airlines’, FSCs, LCCs, etc. And they still bought them @ the end…with many of them in bulk.

2. To a lesser extent/scale, similar story to 1. re how longhaul LCC customers for 787 and 330Neo did not induced FSC customers/big airlines to deter Boeing/Airbus fm launching this pair.

3. U forgot @ least some ‘big airlines’ willing to commit substantial launch orders+options for a new type/variant in recent yrs ARE the LCCs such as:

QF Group committed big on 787 and gave some to JetStar.

SQ Group committed big on 787 and gave some to Scoot.

Norwegian will soon become Europe’s largest 787 operator on current delivery trajectory.

AirAsiaX is by far the biggest customer for 330Neo program.

4. U forgot in this day & age, huge leasing empires such as Avolon, GECAS, ALC, etc. buying in bulk can be more important to Airbus/Boeing to launch a new type than ‘big airlines’. Not only because leasing firms don’t really care whether their customers are LCCs or FSCs but also because over the past 2-3decades, I’m unaware of any commercial aircraft leasing company going into Ch11/BK and therefore failed to take aircraft delivery while plenty of so-called “big airlines” went bust.

@Anton:

“A “long-range” LCC destination from Europe to the US….is to Seattle.”

How do U ‘feel’ about Vancouver then which is only 200km away fm SEA and practically geog identical to SEA to function as a regional connecting hub?

Seasonal LGW-YVR by WS(WestJet) has been in op for about a yr and WS @ YVR hub already has an extensive Western U.S.+Hawaii network….not to mention connecting to Canada @ U.S. airports is much more ‘painful’ than connecting to U.S. @ Canadian airports.

Vancouver is a great place but it seems not to have the frequency and number of options as Seattle into the US South-West, Hawaii and Alaska.

@Anton:

“Vancouver….seems not to have the frequency and number of options as Seattle into the US South-West, Hawaii and Alaska.”

U must be joking re the above when we look @ how many LCC operators/frequency exist in SEA today linking the mkts U’ve listed:

1. Alaska? Zero.

2. Hawaii? Zero.

3. U.S. S.West? Probably more than YVR if talking about LAX, LAS and OAK but clearly not by much more.

The fact that no LCC is hubbed/based in SEA today while YVR has 2(i.e. WS and Rogue) give us a clue.

Some interesting valid points. LCC flights from the US and Canada into Hawaii and Alaska are few and far apart.

Will Alaska create a low fair company with the take over of Virgin America’s aircraft? It could potentially be a viable arm of Alaska connecting Hawaii, Alaska, the US Southwest and East Coast, including Miami, with Seattle?

If the European Legacy airlines could tap more into the Asian/India/China passenger pool their LCC arms could thrive on routes to North and South America as well as the greater Europe.

This could have serious implications for the ME airlines.

@Anton:

“If the European Legacy airlines could tap more into the Asian/India/China passenger pool…”

Biggest longhaul brands(i.e. LH, AF, KLM and BA) within the EU Big3 hv been tapping “into the Asian/India/China passenger pool” for @ least 2~3 decades….over half a century in the case of Asian/India pool. Pls kindly explain how they could suddenly, out of the blue, gain the ability to “tap more” in order to help their LCC arms to build North/South America traffic? All 40-50 Trans-Pcf carriers unrelated to EU Big3 and based in Asia/India/China suddenly decided to withdraw fm/not grow in N/S America mkts so EU Big3’s LCCs can move in AND ask pax to take a much longer routing via Europe?

Sorry, I don’t get the logic.

The “cut-off” is around Malaysia/Indonesia/Thailand/Vietnam in the East.

I see potential for scavenging passengers that are currently flying to Dubai/Doha and then onto the US. Instead the European Legacy airlines could fly those passengers into Europe and then the LCC can fly them onto the US?

When I read about Spicejet looking at the A350-1000 I was wondering if they are not considering flying directly from India to the US for example which should be well within range of the 350K?

Thanks FLX, was good to throw a few ideas around.

In light of 9/11, and Irma, lets take a moment to reflect.

Hope we can exchange views again at some time.