Leeham News and Analysis

There's more to real news than a news release.

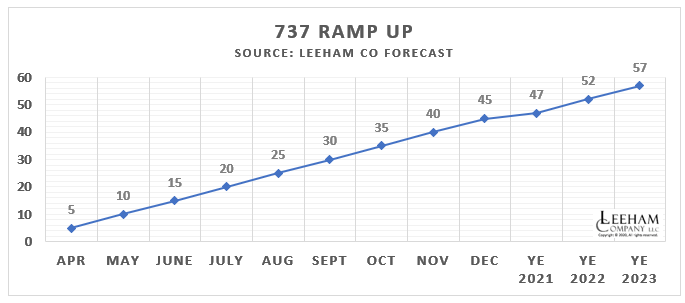

Boeing 737 production rate boost to 57/mo delayed by four years

- Plan called for 737 rate to go to 57/mo YE 2019.

- This rate won’t be achieved until 2023.

- Rate reduction considered for 777.

By Scott Hamilton

Feb. 5, 2020, © Leeham News, Lynnwood (WA): Suppliers attending the annual conference of the Pacific Northwest Aerospace Alliance say they gained some clarity from Boeing last week about future production plans for the 737 MAX.

But they still face a multi-year challenge that puts strain on everyone.

Boeing’s plans to return to the pre-grounding production rate of 52/mo will take until 2022. Plans to boost the rate won’t be fulfilled until 2023—four years later than planned.

Restarting production

Boeing last week said it expects to restart production soon, in advance of recertification of the MAX by the Federal Aviation Administration.

The best guess is that production may resume in April. Boeing EVP and CFO Greg Smith said the restart will be slow, deliberate and not add to the inventory of about 400 MAXes stored across Washington State and in Texas.

The production line is empty now.

Boeing CEO David Calhoun said it will take 18 months for Boeing to clear the inventory, or an average of 22 airplanes a month.

Last week, Spirit Aerosystems said it will deliver 220 fuselages this year to Boeing. This includes 116 737 fuselages it already produced but which are in storage.

- Update: Spirit advised this morning that the fuselages to be delivered will be 216 new-builds, not including the stored ones.

Spirit also said it won’t reach a production rate of 52/mo until late 2022.

Based on this and other information, LNA projected backwards to Boeing’s start up and ramp up rate. Boeing’s rate breaks historically are in increments of five.

Assuming an April restart (which may slip),using 220 as a starting point and Boeing’s announcement that restart will be low and slow, the production rate will start in the single digits. The average monthly production should be about 20 through year end, period of nine months. This is slightly below the average delivery projection of 22, over 18 months.

LNA expects initial delivery rates to be low and build throughout the year.

The FAA announced previously it will assume plane-by-plane certification of the inventory delivery. LNA believes this also to be true of the new production aircraft.

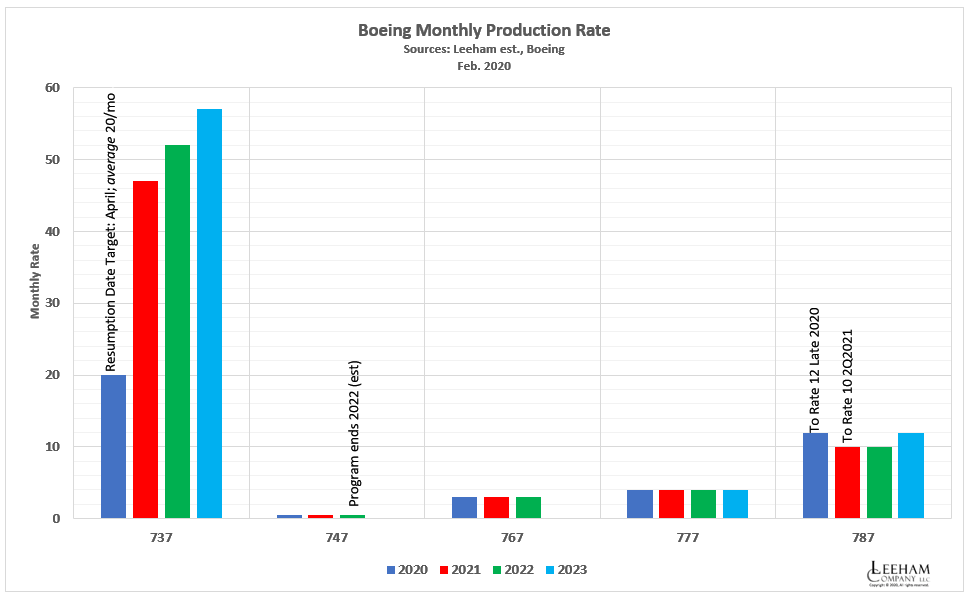

Rate reduction for 787

Even as Boeing resumes and ramps up 737 production, it’s facing rate reductions for the 787 and, LNA learned, for the 777.

Last year, Boeing announced the production rate for the 787 will decline late this year from 14/mo to 12/mo.

Boeing last week confirmed reports that the rate will fall from 12/mo to 10/mo in 2021 and 2022. Officials hope it will return to 12/mo in 2023.

Officials have not said if the 787 final assembly lines in Everett, just up the road from here in Lynnwood, or Charleston (SC) will share the rate reductions equally.

LNA notes that the overhead cost allocation in Charleston is borne almost exclusively by the 787. (There is some minor work for the 737 in Charleston.)

On the other hand, Everett has the 747, 767 and 777 lines in addition to the 787 FAL to absorb costs added from a rate reduction of the 787.

Rate reduction for 777

But the 777 line may also be looking at a rate reduction.

With slow sales of the 777X and a shifting market trend down-sizing and further fragmenting, the 425-seat 777-9 may face the challenges the A380 and 747-8 had competing against smaller airplanes providing more point-to-point service.

LNA learned that Boeing is considering dropped the current rate of 5/mo (with a delivery rate of 3.5/mo) to 4/mo. Cargo traffic is softening, in part due to trade wars. Shifting economics also contribute to softer demand. Orders for the 777X have been canceled and deferred, creating a softer skyline than planned. The 777X is also running a year behind schedule.

“LNA notes that the overhead cost allocation in Charleston is borne almost exclusively by the 787.”

Makes one wonder, which production line for the Dreamliner is more efficient? Especially, when all considerations including quality are factored in…

Boeing should have had the time to improve the FAL’s in Renton to produce 737MAX more efficiently, so in theory with the same staff numbers the ramp up could go very quick or they plan for fewer staff building 737MAX’s.

“the current rate of 5/mo (with a delivery rate of 3.5/mo) to 4/mo.”

I don’t understand the difference between production rate that delivery rate. The 777 program has had difference is these two rates for a long time. The difference amounts to 18 aircraft per year. Where does the aircraft that is produced, but aren’t delivered go? They have mot build that many test frames, and this isn’t the 737 MAX.

Meg: 777-9s being produced right now are going into inventory since the plane is not certified. 777 Classics are being delivered at 3.5/mo, with the 777-9 the other 1.5/mo.

Isn’t 220/9 equates to 24.4. So based on 220 fuselage and start up in April doesnt it average out to 24 737 a month. Where are you getting the 20 from? So once the full 24 a month is getting produced and 22 getting delivered from parked 737 Boeing at some point in 2020 expect to be delivering 46 MAX a month. No?

assuming a linear ramp over the next 3.5 years the delivery stream of the 737MAX will be ~1200..1300 frames behind what was initially planned and accepted by customers.

That then will continue for the foreseeable future ?

Good comment Uwe.It suggests they envisage a long and high production future for the 737MAX.So no replacement on the horizon based on their future manufacturing projections.Perhaps no surprise.

The 777-9 situation seems a little more troubling,particularly if it is ( re the article) grouped in with the now two defunct VLA’s.Is it now too big for tomorrow’s market?

If so they better get planning on a 787-10ER.Perhaps the new RR geared fan will be a way forward for a late 2020’s EIS?

backlog is now reaching ~2 years further right into the future.

Up to now lesser sales for 737MAX enabled a shorter

delivery horizon. This is now gone.

Expect sales for the 737MAX to slump even more or rebates going through the roof.

I agree that a 787-10ER would be the obvious next move for Boeing’s portfolio. If I were Boeing, I would stay the heck away from RR for a next gen engine after the disaster their current engine has been. It’s 9 years after EIS and RR engined 787s are still grounded for engine problems.

GE had its major engine problems too for the 787 early on. The earlier production run had complete sections replaced, but as GE has better press it was called ‘durability enhancements’

Problems continued to more recent times

https://www.flightglobal.com/safety/faa-orders-airlines-to-replace-some-genx-turbine-cases/129099.article

“We learned from GE of a quality escape at one of their suppliers,” says the directive.

“Quality escape”… you have to marvel at the ingenuity of the spin doctors here. In a nut shell why GE has similar issues as RR but ‘manages it’ so much better

NickSJ.I wasn’t referring to the previous generation of 787 RR engines (Trent) or indeed comparison with GE.Neither engine would be suitable.

Indeed I only mentioned RR ( advance/ultra) as Airbus have openly spoken about a 350…neo and can only be referring to this engine development by Rolls.(It also has the same timeframe).

As such it may simply be lucky that Boeing need a new engine in this class size and it appears one may be available in the correct time horizon.( although it would need to be bleedless)

“… the delivery stream of the 737MAX will be ~1200..1300 frames behind what was initially planned and accepted by customers.? ”

Interesting to wonder what long term effects this might have. Suppose a global slowdown triggered by coronavirus or some other unexpected event, then the world might have enough single aisle aircraft, but some airlines will be in a better position than others to meet the reduced demand. The most obvious cause of concern would be WN and so other fast growing airlines around the world that only fly 737

Another effect might be to retain in service 1000 or more planes that would otherwise have been scrapped. More maintenance work than expected ? Good for some replacement parts suppliers ? More fuel consumption ?

Finally we think of Boeing now having a weak negotiating position, but usually having more demand for your product than your ability to produce it, puts the producer in the dominant position and able to extract premium prices (As I understand Airbus was able to do with A321 for a long time)

Ryanair seems to think the opposite, that they can reprice their existing orders and get a low price for a new order. The reality is the production rate is over committed and existing orders will have to be deferred. O’Leary will find the down side of having larger numbers of a single type now.

GE engine was not bad enough to be grounded or for ETOPS to be reduced to 180. Trent 1000 is on its third redesign and EASA just gave a directive to repaired new engine. The GENX has not been grounded like the trent1000.

After revelations on how industry worked shoulder to shoulder with rule makers to have authorities do the right thing for the nation, I’m looking back at those decisions uncomfortably.

Reader “Phil” has been banned from commenting on these pages.

This action was taken for habitual violation of Reader Comment Rules prohibiting personal attacks on others. Phil was previously suspended for the same thing and more recently edited for the same violation.

This “Phil” is not to be confused with another commenter who also used the screen name “Phil.” The second “Phil” effected a change to his screen name today (he is now “Philby”). With this change, this announcement is made.

Nearly all readers abide by the Rules willingly. Some violate and are either admonished through my public posts or through private emails. Compliance is usually followed, but sometimes not, in which case suspension follows for a period. (TransWorld is under such suspension right now.) In the 12 years this column has existed, only five people have been banned for habitual violation of the rules.

We had no quarrel with the substance of Phil’s posts, nor do we with others who have been identified as violating the rules.

We suggest you read these rules (on the drop down box under About This Blog).

Hamilton