Leeham News and Analysis

There's more to real news than a news release.

HOTR: With MAX nearing recertification, Boeing has bigger problem

By the Leeham News team

Oct. 27, 2020, © Leeham News: Boeing’s 737 MAX may be nearing recertification and airlines worry about passenger acceptance.

But Boeing’s larger MAX problem is its general product line-up.

But Boeing’s larger MAX problem is its general product line-up.

LNA pointed out the poor sales of the 7 MAX in the past. We’ve also compared the lagging sales of the 9 MAX and 10 MAX compared with the A321neo.

As a result of the MAX grounding and now COVID-19’s disastrous financial impact on airlines around the world, more than 1,000 orders have been canceled or reclassified as iffy under the ASC 606 accounting rule.

Airbus doesn’t publicly reclassify the European equivalent of ASC 606. But LNA in July estimated how many A320s would be similarly classified. At that time, about 425 appeared to be similarly subject to ASC 606 if this accounting rule was applied to Airbus.

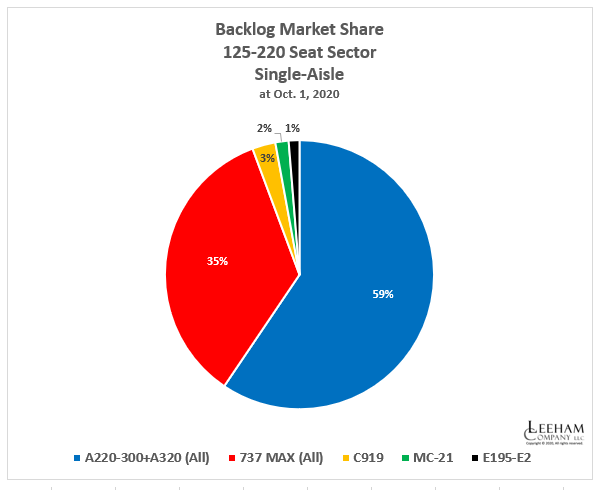

Backlog Market Share

Adjusting for ASC 606 and indefinitely deferred orders, based on data obtained by LNA as of Oct. 1, Airbus now has a 61% share vs the Boeing 39% in the competition between the A320 and 737 families.

Airbus also continued deliveries of the A320 throughout the MAX grounding. There are reduced deliveries through the COVID pandemic.

The MAX backlog market share declines to 35% when all current and planned aircraft in the 125-220 seat single-aisle sector are included. The additional aircraft are the Airbus A220-300, COMAC C919, United Aircraft Corp. MC-21 and the Embraer E195-E2.

The erosion of Boeing’s position in the 125-220-seat sector is an alarming, long-term problem that can only be remedied with two new airplane families: one in the 125-165 seat sector and another for the 180-240 seat market.

With the collapse of the Embraer joint venture in April, there isn’t an obvious solution for the smaller sector. Embraer was to be responsible for this segment.

MAX RTS

Southwest Airlines said on its earnings call this month it will take 3-4 months to return its 737 MAXes to service after the plane is recertified.

The airline must train 7,000 pilots for the MAX. It has 34 MAXes that were flying when grounding was ordered. These must have maintenance performed to bring out of long-term storage. There are also 34 MAXes that have been built but not yet delivered. The latter will replace 737-700s.

Southwest, which exclusively operated the 737 since inception in 1971, is evaluating the Airbus A220 and 737-7 for a large, future order, probably from 2025. The airline has 30 7 MAXes on order and rescheduled 23 of them into the future well before COVID. The need to replace 737-700s is huge. Southwest sees eventually splitting the replacement about half with 737-8s and the rest with a 150-seat airplane.

Except commonality, the 7 MAX stands no chance against the A220, so availability will be the determining factor for how many of the 700 replacements will switch brands.

As an entrepreneur you learn one thing above all else: It is better to make a false decision than to make none. But this is what is happening with Boeing apparently. They don’t buy Embraer, they don’t develop a 737 successor (with CFRP wings), they don’t develop a hydrogen fueled plane,… All they do is study and talk and think and dally and try to survive short-term.

With the 747 they were betting the company and there were no guarantees that it would ever recoup its cost. It appears that today the C-suits are lacking the guts to settle on a product strategy. Doing nothing will wreck the company.

I don’t know about the true financial situation and the strength of the research and development department, but they should have launched at least one serious development project, if not two long since. Maybe it’s not too late now, but it will be soon.

While South West fleet is sort of common, there is a major differences between the 700 (built lighter) and the -7 (shorter). So the A220 has a larger advantage.

the 700 and -7 have totally different engines.

South West runs point to point so the mixing and the advantages of a common hub/type are not there.

The A220-300 is a natural fit

Actually, what Boeing DID do, is extract $70 billion in cash for stock repurchases. By that measure, the last 10-20 years have been a huge success.

Boeing made a decision to prioritize investors over investment in new products. The consequence was predictable and here we are.

Ain’t that the truth!

D0n’t forget management pay tied to stock share and bonus for doing your job.

So SWA recently released their 3rd qtr filings. Buried in the notes, is this gem;

Sale-Leaseback of Aircraft

In second quarter 2020, the Company entered into transactions with third parties, involving ten of the Company’s Boeing 737-800 aircraft and ten of the Company’s Boeing 737 MAX 8 aircraft that qualified as sale-leaseback arrangements under applicable accounting guidance. The Company sold the ten 737-800 aircraft to a third party for $405 million, then immediately leased the aircraft back for approximately ten years. The Company sold the ten 737 MAX 8 aircraft to a third party for $410 million, then immediately leased the aircraft back for approximately 13 years. As such, the aircraft were de-recognized from Property and equipment at their remaining net book values. All of the leases from the sale-leasebacks are accounted for as operating leases, and thus are now reflected as part of the Company’s Operating lease right-of-use assets and operating lease liabilities in the accompanying unaudited Condensed Consolidated Balance Sheet. The 737-800 and 737 MAX 8 sale-leaseback transactions resulted in a recognized gain of $153 million and $69 million, respectively, reflected within Other operating expenses, net in the accompanying unaudited Condensed Consolidated Statement of Comprehensive Income. The 737-800 and 737 MAX 8 sale-leaseback transactions have increased the Company’s future operating lease obligations by $18 million remaining in 2020, $71 million in each of the years from 2021 through 2025, and approximately $440 million thereafter.

https://seekingalpha.com/filing/5206107

What stands out to me is:

– Market value for a new Max is almost the same as a 737-800

– LUV recorded a GAIN of $153 & $69 million on the transactions

Boeing has a huge mountain to climb. If the Max is valued at some $41 million an airframe (which is in line what other airlines have gotten in recent sale/leaseback transactions) and they have to recoup $8 million per plane to cover the grounding costs (~$30 billion over 3500 units), they have a task ahead of them.

Secondly, LUV recognised a gain of $15 million/737-800 and ~$7 million/Max, which means we can infer they paid some $34 million for a Max 8.

Large quantity discount, indeed.

And then there’s the big, black cloud called “China”…and the question as to if/when it will ever re-certify the MAX and/or to what extent Chinese carriers will take their orders. The relationship between China and the USA gets worse by the day.

That trend may be reversed soon, we’ll have to see what happens with the election. If there is a new administration, there will be a bounce in relations.

CAAC has said the MAX is very much on their minds, which I think means they are working to bring it back but only under circumstances for which they are satisfied. Much like EASA did last year, they spelled out conditions for RTS.

In the meantime Chinese airlines are updating their MAX’s and Boeing is active in that process. That means that CAAC is likely to uphold the FAA RTS AD, although they may add other conditions of their own. They are unlikely to act before the ET302 final report is released in March, which is one of their conditions for RTS.

Rob, you should not forget that COMAC 919 will be certified one day, in China at least.

then selling MAXes to the chinese will become extremely tough

You are so right! You know, all this great demand for new airplanes from Boeing and Airbus in the narrow body sector is predicated upon the demand from countries like China and India. The elephant in the room nobody talks about is COMAC 919. If China mandates that its airlines buy COMAC 919 (even if it is somewhat less fuel efficient than the A320neos and B737Maxes), that part of the demand for Airbus and Boeing narrow bodies goes away. That is ominous. And if Russia and China do manage to produce their own twin-aisle aircraft, that takes away orders from Boeing and Airbus in that sector. May not happen tomorrow but certainly sometime in the next decade. Then where will Boeing be? Unless it comes up with a block buster design such as a hydrogen powered narrow body … …

Actually is the C919 is discused a lot.

However, it can only operate to internal China, any country that requires a recognized aircraft certification will not let it fly there. (US/EU/Brazil/Canada are the big certification countries)

So yes they could foist it on internal only.

Then the Chinese carriers use as few as possible and fly as many A320/737 as they can.

TW: I have little doubt China is not rushing to fly a NB (whether it’s 737 MAX/ 321 neo/ COMAC 919) to US/EU/Brazil/Canada anytime soon.

If when someday ….

Just another volatility factor, aviation is full of those.

Perhaps, but China has just announced sanctions against Boeing for arms sales to Taiwan. Those sales will go ahead even if there is a change of Gov. in the US.

In theory those only apply to the military side but they don’t need formal sanctions to mess with the commercial side of Boing, they just need to tip orders more to Airbus.

And to make matters worse: this morning, it was announced that the US will mount joint naval exercises with Japan, as part of its defense of an island group that China is also claiming. That won’t improve the relationship between the US and China…no matter who is in the White House.

https://www.msn.com/en-us/news/world/senkaku-islands-japan-and-china-both-claim-these-islands-as-their-own-now-the-us-is-showing-tokyo-how-it-can-help-defend-them/ar-BB1aqB65?scrlybrkr=20e64c03

Those tensions have existed for a long time and are not related to the US conflict with China over trade and arms sales. That area is rife with competing territorial claims. The US protects the sovereignty of those rights when they can be established, and freedom of navigation when they can’t.

China still has large numbers of Boeing aircraft so commercial activity with Boeing will continue, with conditions likely improving after the election. Chine sanctioned companies instead of the US, because the present US government ignores them.

If Chinese commercial aircraft become viable and produced in large numbers, then that market will dry up for both Boeing and Airbus. First for NB, and then perhaps much later, WB.

But that is still some ways off, I don’t think China wants to cut off growth so that they can mature an industry. They will continue to use other products for many years yet, and in all probability that will include the MAX.

Don’t be so sure that a new admin will change things as far a dealing with China goes.

Its not the China issue right now, its the chaos surrounding it (erratic, impulsive etc) – that will become stable formalized policy.

The Co Prosperity y Sphere has just gone across the Sea of Japan.

The difference is that the new administration will be willing to discuss issues like adults. Not saying they will be resolved, just that there will be communication and dialog. Most of the issues have existed for a very long time, but the poor relationship is a recent development.

Rob:

It does not change the facts on the ground.

I don’t see how you discuss away the South China sea, moves on the Indian Border or the Uhgers, Hong Kong, Taiwan.

What you are not taking into account is its not old issues, its the new aspect of China having the military power to push the issues.

Shades of Japan in 1941. In 1935 they did not have the power, by 1941 they did. We saw what happened.

Also massively more vest in nationalism and rhetoric on China part.

Its only going to get worse.

As I said, yo don’t discuss them away, but you do discuss, and discussion wards off drastic actions and creates stability, even if the stable solution is a stand-off. I think discussion can only make it better.

Hard to compare the MAX-9 with the A321 because the A321 is a different class in size. The MAX-9 needs higher MTOW to get more range otherwise it’s kind of restricted.

For 150 seats A220-300 and A319 burn less fuel but MAX-7 could have more range with an additional fuel tank. The MAX-7 would have more seat pitch than the -700, while A220-300 and A319 would have less seatch pitch than the -700 and there is a reason SW is using the -700 with 143 seats and not 149.

If it could be 144 or even 140 seats for SW and range is not important then the MAX-7 might not be the best choice. But more range could be interesting, the MAX-7 has even higher MTOW than A320, so this better range is special.

Maybe SW will choose MAX-7 for range and A220 for shorter trips. MAX-8 is not better for range, so for shorter trips with more pax the MAX-9 should be the better choice.

A220-300 and A319 for less fuel burn,

A220-300 and MAX-9 for shorter trips,

MAX-7 for range,

A320 for much more leg room and wide seats 🙂

But maybe SW is thinking more about quality after they learnt that Boeing didn’t do QC on the 787 for years?

I’m not sure Southwest needs more range than the A220. According to https://thepointsguy.com/news/longest-shortest-southwest-airlines-flights/ in 2019 the longest route SW flew was under 2500nm. Well within the A220’s capabilities. More-over the high MTOW version of the A220 will give it a bit of a range bump. And if that is not enough Breeze is planning on ordering a version with auxiliary fuel tanks that will take it out to about 38000nm.

Oh and the A220 for even wider seats 🙂

There is no doubt the A220 is the best smaller single aisle aircraft for SW. The question is can they bring themselves to make the leap.

https://www.flightglobal.com/strategy/southwest-flirts-with-airbus-in-fleet-renewal/140797.article

If Southwest orders, say, 200 A220-300s, why wouldn’t they just ask Airbus to develop a 180 seat plus A220-500 in order to replace their 737-800s and the few MAX aircraft that they have received?

As Garry Kelly indicated, now is the time for Southwest to be looking at other options than the MAX. IMJ, Southwest might be considering to jump ship entiely on the MAX.

By operating an all A220 fleet by 2030 would enable Southwest to return to their “roots” of only operating one major aircraft type.

Also, the A220 can be neoed and is therefore future proofed, while the MAX is maxed-out. Hence, it would make sense for Southwest to cancell their 737 MAX order alltogether and go for the A220-300 and a stretched A220-500.

“Also, the A220 can be neo-ed and is therefore future proofed, while the MAX is maxed-out. Hence, it would make sense for Southwest to cancel their 737 MAX order altogether and go for the A220-300 and a stretched A220-500.”

The same applies to Ryanair.

Add to that mix the A321(XLR), to give a super-versatile fleet of modern FBW aircraft, with a whole palette of range and capacity abilities.

All we need now is for Michael O’Leary to have a “burning bush moment”.

Bryce:

Why would you even think NEO on an A220?

The GTF has lots of upside and no one else is going to offer an engine in that size.

PW keeps refining the GTF in pips once every 5 years and you have your NEO.

@TW

“Why would you even think NEO on an A220?”

I was quoting OV-099

@TransWorld @Bryce

A22oneo?

Should be able to EIS by 2030.

The UltraFan, which will start ground tests in 2021 and be available towards the end of this decade, is a scalable design from 25,000lbf of thrust all the way up to 100,000lbf.

The PW1500G engine on the A220 has a thrust rating of between 19,000–23,300 lbf, so the lowest scalable UltraFan design would seem to fit the A220 nicely.

given RR’s current track record, why would anyone even consider the UltraVaporwareFan? especially a gen0 version?

not only has the GTF on the A220 been very solid, but it has enormous room for tech insertion as the core is fairly basic without all of the extreme tech GE needed to get equivalent performance out of a non geared architecture.

The cost of doing this would be very large, pilot retraining or turnover, simulators, maintenance facilities, etc. It’s more likely Southwest might dip a toe in the Airbus water with a few wet-leased A220’s for which they can contract out pilots and maintenance, as a trial.

Then build on that over time, if found to be successful and preferable to the MAX. I think that might be more like what Kelly has in mind.

Uh oh: 737 MAX pilots will need extensive simulator training.

This is one of the reasons why Southwest might jump ship entirely on the MAX.

One of the things that made the 737 MAX attractive for airlines when Boeing launched the programme, was that no separate simulator training was required for pilots flying the plane, assuming they were already rated on the 737.

MAX customers are going to be really unhappy about this, at least in comparison to what they were first promised by Boeing when they ordered the 737 MAX.

–

https://www.forbes.com/sites/benbaldanza/2020/10/12/proposed-737max-pilot-training-requirements-creates-advantage-for-airbus/#3d78d7e58c4b

WN will not abandon MAX.

The pilot training was a function of the errors that were made, not of the MAX. That became apparent during the pilot testing. Airlines understand this.

Making this claim is a reflection of the mindset that training is a cost to be avoided rather than a benefit. Hopefully the industry will move away from that now.

Also Boeing will assist with the training and make its simulators available. Much of it can be done in NG simulators. About 3 hours per pair of pilots, 2 hours in NG/MAX and 1 hour in MAX simulator. It’s a manageable cost and problem, and the airlines know they will be better and safer for it.

@Scott Hamilton

Exceptional circumstances call for extraordinary measures. It appears that Southwest is not in a good position to take delivery of new aircraft now and for the next couple of years. If the industry recovers by 2025 and if Southwest survives the crisis, the industry might look quite different in 2025; a world in which loyal long-standing customers of a particular OEM may no longer feel compelled to buy new aircraft from their long-standing supplier of new aircraft.

–

https://www.boston.com/travel/travel/2020/10/26/southwest-ceo-coronavirus-update/amp

@Rob

The fact of the matter is that extra training means more costs for airlines and — at the margin — makes the MAX less competitive versus the A320neo.

In addition, with Airbus’ Crew-Crew-Qualification concept, fly-by-wire qualified pilots are positioned for an easy transition between the A320 Family and Airbus’ wide-body aircraft through straightforward and rapid differential training. Another advantage of Airbus commonality is Mixed Fleet Flying, which is a pilot’s ability to be current on more than one Airbus fly-by-wire aircraft type at a time. For example, this capability enables a pilot rated on an A380 to switch from very long-haul operations to short- or medium-haul flights at the controls of the A320 Family.

Each of these components of Airbus commonality leads to lower training costs for airlines and considerably increased crew productivity.

I would assume that you’re talking about Boeing aircraft only.

Although the A320neo is a new type of aircraft, there isn’t any major noticeable differences compared to the A320ceo. The A320neo has over 95 percent airframe commonality with the Airbus A320ceo, meaning sitting in the flight deck of a neo will have no real difference than in a A320ceo (Compare that to the hopelessly outdated 737 MAX cockpit with different procedures and different displays than the 737NG cockpit).

Although, the operating philosophy of the A320ceo and A320neo is the same, some of the systems and procedures change in relation to the new engines, but overall the differences are not enough to require the operator to roll out a full training program for the new type. Thus, an A320ceo pilot has to undergo the computer-based type difference training, to qualify for flying the A320neo.

My thinking was along the lines of including sim time for every new aircraft, and stop trying to avoid that cost by the mechanism of type similarity. That reasoning is really poor from the standpoint of safety. It should be an expected airline cost at the introduction of any new aircraft.

As we saw in Pakistan, the A320 (or any other Airbus aircraft) is not immune to pilot error. We should ensure that acquired training departure habits in the pilot workforce don’t survive into any new or amended type that is introduced. Such training would have avoided the MAX accidents, even with the MCAS flaws.

The MAX will need 2 or 3 hours of sim time and 2 pilots can be trained at once. So it’s not a huge amount of time. It could also be merged with routine pilot check training so as to provide additional benefit. If that is done as aircraft are acquired, the cost and sim access could be spread out over time.

**Trolling Alarm**

“”Such training would have avoided the MAX accidents, even with the MCAS flaws”

NO NO NO

Boeing was hiding MCAS.

Boeing faked the sims.

Even with knowledge what would happen, Sullenberger crashed and not only once.

Do they train “landing with spoilers only”? (hidden somewhere in the documents!!!)

Do they train to advise pax to hurry to the back to change CG?

If Boeing did a better bulletin after JT610, the ET302 crash could have been prevented. The three pilot crew of ET043 needed over 220 seconds to get a clue.

South West got a 1 million dollar discount for not having to have pilot training.

A lot more to it than just a couple of hours.

Vastly more than an error, in the gun world its called a Negligent Discharge.

This verges into criminal if not criminal (that is still in the investigation stages)

There can be an intermediate stage of simulator training between full for new type and none for amended type

If 3 hours would have prevented the MAX accidents, it’s well worthwhile.

Criminal is an allegation at this point, no evidence presented as of yet for that case. We should wait for the investigation to conclude.

Its an interesting idea.

South West has been moving up in size though, so a 737-9/10 or an A321NEO might well be part of the mix.

A220-300 would be a start and maybe a hold, but certainly a great choice with upside.

With South West type numbers there is leverage for the -500 there.

“”in 2019 the longest route SW flew was under 2500nm””

If only 2500nm are needed and as TW said that SW could grow, I would look at the A320. There is a payload-range curve for the 73.5t/62.8t MTOW/MZFW version, but the 73.5t/64.3t version would be better. With 150 pax it would give 4 inch more seat pitch than the -700. Even the 71.5t version could work and might be more fuel efficient than the 70t A220 because of bigger fan.

The A319 has an equal cabin as the -700. There is a 70t/60.3t version which could work too, but no room to grow.

Or if SW wants to stay Boeing they could use a 74.8t MAX-8 with 5-abreast for 150 seats. That would be really special and a way to attract pax.

Pre-pandemic, the market for less than 150 seats was very small. Max7 sold poorly, but so did the A319. Bombardier nearly went bankrupt trying to sell the C Series, now the A220. Airbus got half the program for a dollar, so that tells what the market was like. This was not much of a Boeing weakness.

All the airlines were up gauging. Southwest had five hundred -700s in their fleet compared to 200 -800s, but orders show where they are going: 280 for the Max8 vs 30 for the Max7. The Max7 is no worse compared to the Max8 than the -700 was to the -800. The market moved.

Boeings real weakness is the lack of any aircraft to compete with the A321. The Max9 and 10 work on shorter routes, but are range limited at full capacity. Backlogs are 3000 for A321 vs 500 Max9/10 combined.

The industry is in turmoil now, so who knows what will happen. I think attention on the A220 is misplaced. You don’t make 20 year capital decisions based on the trough of a one year downturn. A321 size is where Boeing needs to focus.

I think the market has split between the two segments.

200-240 and 180.

With the 500 model, the A220 would eat the MAX-8 market which is all that is really left (given the -9 is more MAX8). The -10 is no A321 competitor and even more limited.

If the A220 can challenge the -8, then it can replace the A320NEO for those who want to get the efficiency or is worth the more than one fleet type (Delta)

Reality is that the A320 is heavy for the segment and the A321 is optimal.

The very best you could do as a 737 Replacement is a bit too heavy -9 area.

The A320/-8 will continue to be a large segment.

Airbus can easily stretch the A320neo by 7 frames (i.e. A320-500) and the 101 metric tonne MTOW A321XLR also by 7 frames (i.e. A322).

In comparison the A321 is stretched by 13 frames over that of the A320. A 7 frame stretch is roughly equivalent to two extra LD3-45 containers in the lower hold — one aft and one forward — and 30 additional economy class seats (i.e. 5 rows) on the main deck.

There is no natural split between 180 and 200-240. All the big carriers want 200 seats and more, maybe not exclusively but at least the capability. Commonality means an A220-500 would be at a significant disadvantage because it can’t go bigger. The A320/321 covers those capacities well, particularly if they added a 320.5 that split the somewhat large gap between the two.

Look at Ryanair cramming 200 into a max8. Southwest might like a better max7, but they are transitioning to the 8 after which they’ll want more. Incidentally, Southwest could likely use the Max9/10. They don’t fly many long routes.

240 in a single aisle is a rehash of the 757. Everyone seems to forget all the problems that caused its demise. Boeing tried to magically get single aisle economics in a twin aisle, and couldn’t make it work.

I think Boeings position in the 125-220-seat sector has been eroding for some time, only accelerated by the MAX grounding. The decline startet when Boeing reduced their product lineup, from several narrowbody families, to only producing the 737NG.

I wish LNA could run a story on OEM market share in the 125-220-seat sector over the last 50 years, looking at deliveries from the different OEMs, from the very first 737 delivery.

All aircraft families have a lifespan. I think it is a smart move from Airbus to have two narrowbody families, one brand new and one middle-aged. Boeing should launch a new narrowbody family and at the same time continue to manufacture the 737 MAX. They should not wait until their market share is close to 0%. By then it is to late.

Apparently Boeing is leaning that way too. First priority is to resume cash flow from the MAX and take care of those customers, then second priority should be development, consistent with the new post-COVID market.

The issue is Boeing waited until it was way too late and then is stuck with a single product vs two that Airbus has.

Now Boeing needs two different lines.

Probably the A321 area is the first (if they do it at all) and that leaves them loosing the -7/-8 area to the A220.

Boeing is shot in both arms and at best can staunch the bleeding with one hand.

A much diminished Boeing is the only foreseeable future.

Like Lockheed, maybe no BAC.

TW, we know this is your long-standing position that arises whenever someone has something good to say about Boeing. But there is no evidence of this happening, now or in the near future.

Boeing still has a major presence in the world commercial market and that is not about to change. They have a lot of work to do in future, but no reason to believe it can’t be done, or won’t happen.

Boeing is reducing headcount left and right, with serious bloodletting in WA. By the time, the co. is ready to launch the next shiny new toy, all the institutional memory would have mostly gone.

Boeing is looking at a worldwide reduction from 160,000 to 130,000 employees. That is driven mostly by COVID, prior to that Boeing make a substantial effort to maintain workforce during the MAX grounding.

That’s not enough to lose institutional memory or the ability to design & build new aircraft.

@Rob: 1) the layoff is borne by BCA; 2) within BCA, WA would suffer the most, SC relatively minor; 3) in May Boeing chopped 12% of its engineers and 21% of its technical staff, those are staff with decades experience, cream of the crop.

Well, its not as though AirBus ending up with two single aisle planes was the result of strategic genius. More Boeing overplaying their hand. Boeing should have either let the c-series totter along, or made a serious offer for it when they were approached. It would not have been the deal AB got, but still at a substantial discount from the development cost. They could have then skipped the Max-7 certification costs and focused on a new aircraft.

Strategic genius?

5 across seating

6 across

8 across

9 across

10 across ( endof line)

See a pattern there?

Yes. Like making the 737 and 757 simultanuously, the next narrowbody might not be much better but made much quicker, cheaper and precise by robots

The story of the last 50 years is evident from the sales figures over that period. Up until Airbus launched the A320, Boeing had a dominant position in the market. What’s happened is that Airbus started gaining market share, but the market size increased.

So Boeing was making more sales and profit from those, and all looked good and rosy for Boeing. But in reality their % market share has been steadily declining ever since 1990. And they’ve roundly ignored that trend for those 30 years. Instead of focusing on preserving market share, they engaged in share buy backs.

Initially they got lucky with the MAX; the market grew again, and Airbus couldn’t fill it all themselves.

The grounding and now COVID has done terrible damage to the MAX’s prospects. Everyone now knows the 737 endgame has arrived.

How far up to and into the 125+ seat range could you stretch the Mitsubishi M90? Given that this program appears to be close to termination Boeing could potentially acquire this type relatively cheaply, leaving them to develop a new model larger and closer to their comfort zone and a clean sheet A321LR competitor. The natural cut over point to me seems to be how far you can push a 4 abreast design versus a 6 abreast cabin. Shrinking a 220 seat design into the 170-180 seat range would intuitively feel likely to retain a new generation’s design advantages over any legacy designs and be out of reach for any 4 abreast RJ.

@Andy: The SpaceJet would be a 130-seat airplane, or M300.

@ Scott – what do you think, would an M90 to M300 product range covering 76-130 seats and a new design A321LR killer shrunk to give a 6 abreast product range from 175-220 seats be a viable portfolio for Boeing?

If there had to be a gap in a product line up I’d judge the 150 seat segment to be the least important.

“The erosion of Boeing’s position in the 125-220-seat sector is an alarming, long-term problem that can only be remedied with two new airplane families: one in the 125-165 seat sector and another for the 180-240 seat market.”

– Boeing doesn’t have the resources to develop two new programs. Even for one, massive direct and indirect government support might be required.

– Creating a third option next to the new A220s and E2’s doesn’t sound like a profitable business case.

– By the time Boeing can come up with anything new (2027), the market is already stuffed with A321 & A220s and new variants.

https://groups.google.com/group/aviation_innovation/attach/57f1d448a2948/Airbus%20Future%20A320%20portfolio.jpg?part=0.1&view=1

Maybe Boeing better goes for a middle of the NB segment lean & mean, uncompromised & parks 220 seats ambitions. So:

> 150-200 seats

> OEW 30-32t

> Hybrid?

> Range up to 2500NM / 5 hours

> AKH container / pallet options

> 2040 high BPR engine ready

> Modular design, production, FAL’s all over the world possible

>> 8-10% more fuel efficient than the 30 yrs old A320 family

https://groups.google.com/group/aviation_innovation/attach/4fe98ff2ca66b/FSA%20on%20ICE%20Boeing.jpg?part=0.2&view=1

There is a new reality. Boeing are the #2 OEM, the US is the #2 passenger market and customer loyalty is low.

Exports are vital and Boeing are uphill from an unloved starting position (MAX, tradewars, Trump, Partnering for Success, Stock Buybacks, FAA bullying). I think realism / real listening is crucial for Boeing at this stage.

Plus: scrap the short term profit/stock driven executive bonuses ASAP. It brought the company to its knees. It’s a failing concept for long term success.

I think a valid question is, does Boeing have the resources to develop even just one new aircraft?

AFAIK they’ve made some changes to how the business is run, but until that’s demonstrated an ability to push a good new design out the door to schedule the answer to that question is “no”.

Basically, Boeing can’t even draw up a plan of campaign to get their product line up back in the game.

So I think they need to set their team running on, well, just about anything other than the plane that’s going to matter most. They need the practise, get back to being match fit.

I don’t know what that plane is, or whether the company can last long enough to see it through.

If the market for fewer seats is huge why don’t keep the present planes and take out the seats ? It will make passengers to pay a premium for leg space and save a tons of money to any airframe manufacturers !! Profit come from customer satisfaction not only fuel savings. !!!!!

If not all seats are sold or payload is still available, airlines could load cargo, but cargo pays less than pax and there are also weight restrictions for cargo. If airlines don’t use the full payload they earn less.

MTOW could be reduced and save money but the empty weight is always there. Better to use a smaller plane with less empty weight and use all the payload available.

Cargo is far less an aspect of single aisle ops than the wide bodies.

Alaska used to run combi setup but that is gone to dedicated now, it did not work all that well.

Each time you change, you have to pull seats, power runs and then re-install latter.

Its man power intensive and you break things

Interesting that WN sees the capacity nodes at 150 and 175 passengers. The other majors operate on a feeder system of 75 and 150/175. What would be the optimal balance if starting from a clean slate? 100 and 175? If WN is to go into smaller cities, then why not an aircraft of 100 or 125? It looks like the E190 and CS100 share the same problem as the 737-7, they are overbuilt for their size, so the extra seats of the CS300 don’t have much extra relative cost in comparison.

Maybe India should enter into a joint venture with Embraer.

India has a developed aerospace program, and would probably love to be able to match China in some way as regards aircraft manufacture. India and Brazil have a good relationship, and are both BRIC countries.

How about MHI?

However, having watched India with their fighter program, man, what a train (err aircraft) wreck.

The A220-300 is not a 150 seat airplane in southwest configuration. The 737 -7 MAX is a very generous 150 seat for Southwest with 3 lavs. Southwest do not use those 28, 29 and 30 inch pitch like other airlines.

The A220-300 seems ok with 145 seats non low cost, 3 lavatories, 2 galleys and all seats, aisle significantly wider then on any 737.

https://www.seatguru.com/airlines/Swiss_Airlines/Swiss_Airlines_Bombardier_CS300.php#

You could adjust max seating to 145 or 140, and or the A220-500 could figure in.

At 150 pax in an A220-300 you get 30 inch pitch so you can play with numbers from there.

The 700 is 31 inches so you are very close. I believe the -7 is (or would ) the same

I’d bet that SW does order the A220-300 with 143 seats and then holds options for possibly the A220-100 with 124 seats. Probably 50-100 copies.

I really do not see SW with A220-100.

I can see a -500 replacing the MAX8

The reason they might go -100, is that SW does not work much with regional carriers. That, and the fact that Delta has -100. SW would put in 124 seats, and make money on certain routes at certain times.

The A220 has 19 inch seat width

https://runwaygirlnetwork.com/2020/01/17/a-curvy-girls-take-on-the-new-air-canada-a220-300/#:~:text=19%2Dinch%20wide%20economy%20class,armrests%20apparently%20aided%20this%20achievement).

“Air Canada’s A220 features two cabins – 12 seats in business class in a 2-2- layout, and 125 seats in economy class, with the latter measuring a glorious 19 inches of width each (slimline armrests apparently aided this achievement).

For comparison purposes, the standard seat size on the Boeing 737 is 17 inches, and on the Airbus A320 is 18 inches. A 19-inch width is akin to what is found on many premium economy class seats.”

Correction: The A220 has 19-inch middle seats and 18.5-inch window and aisle seats.

Off-topic, but very important:

Nearly 200 European airports are at risk of insolvency as a result of the CoViD travel hiatus.

https://www.reuters.com/article/idUSS8N2H501D

Governments will rescue them.

Ironically Anchorage is doing fine with the freighter market we wound up with (as opposed to the former Air Crossroads of the World before Pax bypassed us)

I saw that. If a significant number of those airports close that could be an issue for Ryan Air given its strategy of flying into secondary airports (some like Carcassonne are literally tents).

That said I don’t think governments will allow those airports to close.

Funny you should say that: Ryanair was the first airline that entered my mind. In fact, much of Ryanair’s business model / success is based on the fact that it uses secondary airports.

I hope that governments step in…but, concurrently, I’m not sure to what extent that’s feasible: the total bill for CoViD-related economic support is spiraling out of control, and choices will have to be made.

Note sure whether to call this desperate or embarrassing: how low the mighty have fallen.

“American Airlines plans customer tours of Boeing 737 Max and pilot calls to boost confidence in jets”

https://www.cnbc.com/2020/10/24/american-airlines-plans-customer-boeing-737-max-tours-to-build-confidence.html?&qsearchterm=737%20max

Just a recognition that people will believe pilots and mechanics over the media. I doubt many people will do this, but offering the opportunity demonstrates confidence, and that there is nothing to hide.

People don’t know which aircraft they board I was assured. Why would AA than do this?

Back in the day when McDonnell Douglas was doing a good job, I would think when a customer choose between the MD-83 and the Boeing 737-400 Classic, that their economics had to be with in of a percentage point depending on the length of flight? It would almost have to be with Robert Crandall ordering 200 of the McDonnell Douglas MD-80s? They both used similar technologies, granted different engines. This discussion I would think primarily takes place because Boeing has chosen to not use the latest and greatest advances in the industry, correct?

So recently, Leeham did an article adjusting the BA and Airbus order books using ASC 606 rules. Here it is:

https://leehamnews.com/2020/09/15/hotr-adjusting-airbus-and-boeing-orderbooks/

The adjusted single aisle backlog is as follows (from the graph)

A220: 456

A320 line: 5331

B737 Line: 3455

Total: 9242

The Max has a 37% market share, the A320 has a 58% share and the A220 has 5% of the market.

Anyway you cut it, Boeing is in tough with an older model that will cost them some $30 billion because of the grounding. They have to make a margin of some $8.5 million an airframe to cover the loss.

While there is talk about BA approaching airlines about the NMA, they just don’t have the $15-20 billion needed, right now.

Boeing has the resources to do this, but they need to be sure there is a market for whatever they produce. Right now they have offerings across the board, so there is not a sizable hole to fill, except possibly at the low end. Developing new is more a matter of competition and market share right now, and they will need travel to recover as well.

The PW1124G of the A319 has a bypass ratio of 12.5 and a fan diameter of 81 inch, 206cm. The PW1524G of the A220 has a bypass ratio of 12 and a fan diameter of only 73inch, 185cm.

Could it be that a 70t A319 is more fuel efficient than a 70t A220-300? It should be but the question is how much. If Delta, JetBlue and Breeze use A220, SW could beat them with A319.

A220-300 and A319 should have same seat pitch with 150 seats. For SW it should be 144 seats on the A319 and 145 on the A220-300.

A22o has a smaller diameter fuselage and a much more modern wing, so it should have significantly less drag.

engine diameter & weight aren’t the be-all end all of fuel efficiency (although they are certainly a factor)

the A320 NEO has about an 8T greater OEW than the A220. at 70T (the A220’s MTOW) the A220 is carrying 8T more pax/cargo than a 70T A320. fuel efficiency may be comparable at those weights, but the A220 is more capable.

Yes, 8t OEW between A320 and A220-300, but I thought about the more comparable A319, then it’s only 5.5t OEW difference.

If SW only needs 2500nm range, additional fuel is not needed, that’s why only the 70t A319, not the 75.5t, and it makes both planes better comparable.

The A319 wings have 124 m2 wing surface, A220 only 112 m2, so at the same MTOW this is a lot help.

I guess the A319 is even cheaper to buy. That would kick the A220 out of the race for SW if it’s about fuel efficiency.

wing area is is not a good metric for efficiency. the A220 wing has a much higher aspect ratio, which means (relatively speaking) it would product the required lift with less drag all other things being equal (airfoil shape, smoothness, interference drag from engines, flap actuators etc)

but all things are not equal, the A220 has a 25 year newer composite wing, so it has a better airfoil, better skin smoothness, lower interference drag etc in addition to a higher aspect ratio.

what you end up with is an aircraft that is right sized to the wing and engines at the A220-300 size, whereas the A319 is too much wing and structure for the size.

range of the 70t A220 is 3400 NMI, the 75.5T A319Neo only gets you another 350 NM and taking away 5.5T of fuel to get to 70T is going to cut that down to somewhere in the 2800 NMI range.

if you are now talking ok, I only need 2500 NMI, then the MTOW of the A220 doesn’t matter because you can hit full passenger capacity for that range and carry a lot less fuel, bringing you well under 70T mission weight, probably in the 65T range.

“”wing area is is not a good metric for efficiency. the A220 wing has a much higher aspect ratio””

Thanks Bilbo,

I agree, wing area is not only important, hard to get good infos. But AR is a poor metric too, especially when the wingspan is restricted by airport gates. So the A319 can’t get better AR, but the 10% more wing area still helps a lot.

I agree, the MTOW of the A220-300 could be reduced too, but not as much as the A319.

The A220 has other advantages too, but not to think about the A319 is wrong. I would choose the A320 because it gives room to grow. SW could choose the MAX-8 for the same reason. What would you choose?

As a general note, has the general A320/737 competitive landscape changed significantly during the Max grounding? I think conventional wisdom was that the Max was selling in part because delivery dates weren’t so far out, but as Airbus look as though they’ll have burnt off around 2 years of backlog whilst the 737 line has been at a virtual standstill will that affect future sales campaigns?

From another perspective: if Southwest or Ryanair said in the morning that they’d switch their entire orders from the MAX to the A320 family, but only if Airbus could give them early slots, would this be achievable? Well, with the A320 lines currently only operating at 2/3 capacity, and other airlines deferring rather than bringing forward, Airbus could potentially scale back up to full production and allocate all the extra capacity to the new orders. When back at full swing, they could give each operator 10 planes per month.

Sure, it’s not a standard way of working, but it’s not impossible.

Airbus has repeatedly refused to sell at what Ryanair wants to buy at. Ryanair talks a lot but in the end nada (remember they were going big on the C919?)

South West ?

I would only think so if the MAX was so out of competitive range (5%) and its not.

Huge infrastructure involved.

A gradual transition by SW into the A220 would make sense.

I think formally the 737 backlog is shaky at this stage. Meaning airlines have gained rights to cancel because of delays.

I think those with cancellation rights have already negotiated some outcome with Boeing. Future slots in the order book will also be negotiated, but those will be standard terms unrelated to the delay, more related to COVID impact.

cancellation rights are, my guess, more dependent on a customers delivery horizon than on RTS right now.

i.e. I expect a constant stream of orders coming up for cancellation due to delivery dates not being met.

ANA retires 22 B777s, JAL retires 24 B777s.

Um One Thing!

The Boeing 737 Max 7,8,200,9 & 10

Will gain Recertification you know something everybody at home watching TV’s so Boeing CEO Dave Calhoun and FAA Steve Dickson

Should go to Congress and Deliver the Speech Because This Will Help Passengers Regain Trust And Confidence.