Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Certification timing may push EIS for 777X

Nov. 2, 2020, © Leeham News: Throughout the 737 MAX investigations and recertification process, former Boeing CEO Dennis Muilenburg said there would be no delay on 777X certification.

By Scott Hamilton

On Boeing’s earnings call last week, Muilenburg’s successor, David Calhoun, said there could be.

“On the 777X, we continue to work with the regulators on certification work scope, including reflecting the learnings from the 737 cert process,” Calhoun said. “As with any development program, there are inherent risks that can affect schedule. And while we continue to drive toward entry into service in 2022, this timing will ultimately be influenced by certification requirements defined by the regulators.”

Boeing is certifying the 777X under the Changed Product Rule, the same process used for the MAX. Certification is being pursued as a derivative of the 777, a point of scrutiny on the MAX.

Changing demand

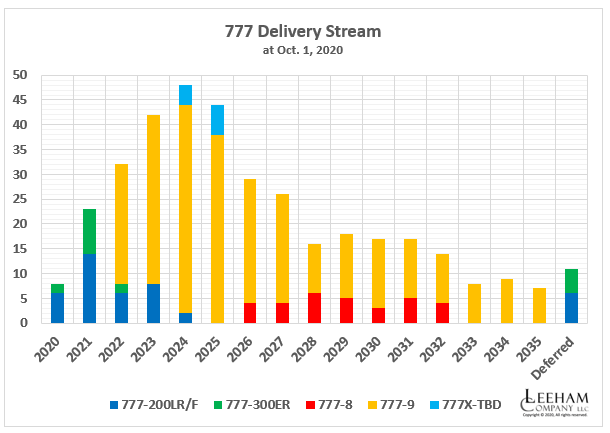

Changing demand due to the COVID-19 pushed EIS from 2021 to 2022.

Cathay Pacific Airways deferred its order for 21 777-9s until 2025 and beyond. Market intelligence indicates CX wants to cancel this order in exchange for the 787-10.

Even before COVID, some of the 309 orders listed on the Boeing web site were soft.

Boeing 777 delivery stream at Oct. 1, 2020. Recent adjustments may not be reflected.

Emirates Airline already reduced its order from 150 to 115 Xs. President Tim Clark indicated he may swap some of the remaining orders for the 787, but a number hasn’t been expressed publicly. This sentiment occurred before the COVID pandemic.

Etihad Airways is listed by Boeing with 25 orders. But long ago, as Etihad’s finances deteriorated and a fleet restructuring began, officials said they wouldn’t take more than six. Even this is soft. As a result of COVID, market intelligence indicates Etihad wants to swap these for the 787-10.

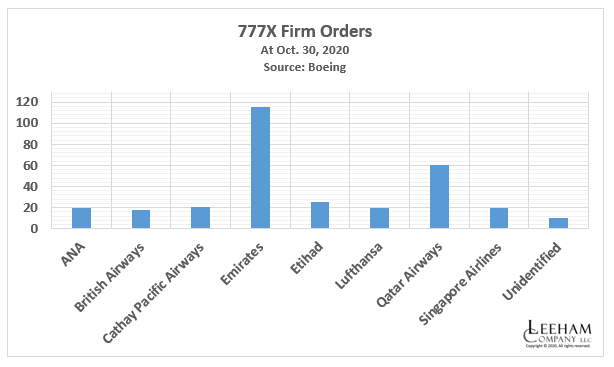

The third Big Three Middle East carrier, Qatar Airways, said in September it remains committed to accept all 60 of its orders between 2022-2029. The Big Three account for 65% of the 777X order book. Emirates has 37% of the backlog.

Lufthansa also cooled to its order for 20 777-9s, both pre- and post-COVID.

Boeing already produced the first 777-9s for Lufthansa and Emirates. There are about two dozen -9s stored at Everett Paine Field, where the airplanes are assembled. The production rate for the 777 Classic and X goes to two a month shortly.

Further fragmentation of long haul routes with the introduction of the 737-8 MAX and A321LR/XRL, capable of flying routes of 8-10 hours, demand of the 777X is further undermined. It’s the same fragmentation theory Boeing expanded with the 787 vs the Airbus A380 and Boeing 747-8. Fragmentation of the Very Large Aircraft began with the ETOPS Boeing 767, growing with the A330, 777 Classic and A350.

Many, including LNA believe the 777-9 is now too big for the market and the 777-8, if it is built (there is a backlog of just 30+), is too niche.

Soft skyline

With about one-third of the backlog orders considered by some to be soft, a few Wall Street aerospace analysts wonder whether Boeing will cancel the program. Even a few lessors believe the program is in jeopardy.

Boeing has a small customer base for the 777X. Source: Boeing.

Even in the radical restructuring now underway at Boeing, I think it unlikely the X program will be canceled. Boeing warned that a forward loss may be in the program’s future. (The 787 program also faces a possible forward loss, Boeing warned, due to the impacts of the pandemic.)

But with some two dozen airplanes already built, at least 60 firm orders (and probably scores more) appearing solid, for now, I just don’t see Boeing tanking the program. Boeing proceeded with the 747-8, for which only 153 orders were received. It also took a multi-billion dollar write off early in the program.

However, the longevity for the X probably will be vastly truncated. Boeing counted on retiring 777-300ERs as a source for new sales. But only one unidentified and eight identified customers signed up for the airplane. The market clearly indicated that smaller is better before the pandemic.

After the pandemic is over, smaller most like remains better.

This is looking like the very definition of DOA

Somewhere I missed they had actually made 777X aircraft.

I do think the -9 is too big (and the -8 is not competitive unless its in a -9 fleet)

Like the 747-8/A380 its going to limp along but its not going to be the wild success the 777-200/300 and all the varinets of LR and ER etc were.

That slot at best is moving to the A350-1000. The hot spot is the 787/A350-900 (A330NEO limps along)

That leaves Boeing with a two aircraft fleet (MAX and 787) and the MAX is not going to do that great.

Airbus is in good shape for the near and mid term.

If your weren’t paying attention enough to know they have been producing the 777x for 3yrs now, I’m not sure you are the most informed to be giving predictions on future commercial demand. Aviation will rebound, if it weren’t for government and political mettling, people would be flying right now in larger numbers. The 777x-8 was really only going to be a good option for project sunrise, and Qantas went with the 350. The 777x-9 would have killed the 380, but obviously current world events expedited that. Operators love the 777 and 787. The x is no different. The efficiency, killer Ife/wifi, big comfortable cabin will make it a long haul success. Boeing already has a higher fleet utilization rate than AB given the amount of freighters produced. Once the Max can be delivered again and airlines can’t contractually charge Boeing for missed revenue we will see a bottom in commercial production.

Government meddling? Like responding to a global pandemic?

John:

Its not paying attention, its seeing information like that and I have simply not come across it.

I haunt a lot of site and daily scan for what is going on in the Aviation world, as well defense and space.

I have recently bucked up and picked up Av Week again.

I hope that meets your approval.

John – did you mean ‘dying right now in larger numbers…’?

Let’s hope the re-certification is handled in an ambitious pro-active way rather than the defensive evasive process we saw on the 737 MAX.

In my opinion for the 737MAX it made a lot of sense to certify it under the changed product rule (grandfathered design and requirements), but they should have updated the requirements & executed it right.

The 777X is a different ball game, it has so many major changes (new wing, engine, fuselage, landing gear, cockpit, tail) that from the start it amazed many the FAA went along. They were probably under a lot of pressure.

For the current 777X customer base it is remarkable that all but ANA are introducing A350s. Only 170 -1000s are on order, but theys seems to do well & probably hundreds of conversions rights are baked into contracts.

The 777X still uses the same diameter aluminium fuselage from the earlier model 777.

They tried a new production process with automated riveting but it wasnt a success- would probably need a riveted fuselage designed in for automation from the beginning That wouldnt make sense in this size as they have moved to carbon fibre panels and barrels.

“”For the current 777X customer base it is remarkable that all but ANA are introducing A350s””

Wikipedia:

779=0+20 ANA

35k=7+11 779=0+18 BA

359=27+3 35k=13+5 779=0+21 Cathay

359=0+50 77X=0+115 Emirates

35k=6+? 779=0+6 Etihad

359=17+26 779=0+20 Lufthansa

359=34 35k=18+25 778=0+10 779=0+50 Qatar

359=50+17 779=0+20 SIA

Only Qatar makes no sense. The 778 cabin is only little bit smaller than the 35k, as if Qatar don’t know what they want.

If Emirates cancelled their 778 already, there are only 10 778 for Qatar.

There may be a certain amount of bet hedging going on. If an airline places an order, it kinda needs that order to be delivered. A lot of new aircraft programmes in recent years have been delayed. Splitting the orders means that, at least, the airline is no worse off than other airlines.

Though just at the moment, airlines with an all-Airbus order sheet are probably quite pleased with that (not counting COVID).

Another aspect at the moment is the question of whether the manufacturer will survive financially to deliver an order. Airbus seem pretty solid. Boeing less so. If Boeing’s situation declines too much then there’ll be a point where airlines won’t place orders, won’t take up options, etc.

In the current situation, I think it is best for Boeing to transfer as many orders as possible from the 777X to the 787 programme.

There is always introductory pricing and high initial production costs. All 777X, for the foreseeable future, will be delivered below cost, and if break even ever will be achieved, is out in the blue.

By transferring many orders to the 787, this program can archive the necessary volume to keep production costs low, thereby generating badly needed profit for Boeing.

Yep, almost keep the 777x as a marker but sell the 789 and make some money. Helps in two ways, gets the the 787 done the learning curve in order to burn off the remaining deferred fees and stops the massive costs associated with each unit of the 777x programme

typical acountant trap.

Switching sales to the now more profitable B787 doesn’t help the company with its overall B777x issue.

Because it’s a calculatory number. if you write over sales to the B789 you basically kill the B777x program and take the losses.

For a redesign as the B777x is, with existing FAL the learning curve is way more mellow, the cost of the early units not that much worse than later units.

If you follow that idea, you would never build a new aircraft, you would always write them down to the older one, as this is the one cheaper – on paper.

It wouldn’t help the company overall, as Boeing already has invested 6 or 7 bn. $ into the b777x

I agree though with a bit of a different take.

The 787 still has huge losses (20 billion?) though that money is long gone.

The 777X looks to be a big loss as well.

The reality is with forward accounting and management disaster that is Boeing now, its a mess and there is no silver lining.

777x dump also another arrow in the heart of Everett.

No happy faces here at all.

TW – there’s a guy over at the investing site that does a quarterly analysis of the 787 deferred production balance. IIRC it’s now down to ~$19 billion, with the accounting block moved down to 1500 units. He always clarifies that this does not mean 1500 is the break even point for the program, but at the margins that BA gets, they will almost certainly have a loss on the program.

The 777X has a del cost somewhere in the $5-7 billion region to make up and the Max grounding has been estimated to cost some $30 billion (back in early 2020 Boeing estimated it to be at least $19 billion). The Max will also never be profitable…

All three programs are in the red, with the future product cupboard bare – robbed by the C-suite boys and funnelled into stock buybacks & dividends.

This, from the division (BCA) that in the last full year prior to the grounding and covid, was responsible for 60% of the entire corp’s revenue AND 66% of the profits ($8 out of the $12 billion).

Defence and services is going to have to carry the company until Boeing launches a new jet and gets it act together.

Thanks, good info. I am not an accountant of any shape or form.

The 777X costs sound right, the 737MAX costs seems excessive.

Havn’t tracked those closely, more into the tech aspects. It seems 6 -10 billion and some may recover when deliveries start.

A lot of moving pieces involved in the MAX cost wise, infrastructure is not one of them (maybe some big buck returns for Renton site if they move to Everett)

As I understand the 787, at 1500 its paid back the lost costs.

Difference in revenue positive on delivered which now is????

Boeing had estimated, back in Jan 2020 a cost of ~$19 billion;

“Boeing puts cost of 737 Max crashes at $19bn as it slumps to annual loss

Boeing set aside a further $9.2bn to cover the costs of airlines that have cancelled thousands of Max flights and towards higher costs related to compensation – doubling its estimate of the total financial hit from the crisis to $18.6bn.”

https://www.theguardian.com/business/2020/jan/29/boeing-puts-cost-of-737-max-crashes-at-19bn-as-it-slumps-to-annual-loss

This was 9 months ago. The Street has estimated $5 billion a quarter, which puts it in the $30 billion range.

The change in sim requirements is looking to cost $5 billion ALONE, with over $1.2 billion given to SWA.

“Boeing Co.’s costs would rise an estimated $5 billion if pilots need to get simulator training before flying the 737 Max, according to Bloomberg Intelligence.”

https://www.bloomberg.com/news/articles/2020-01-09/boeing-seen-facing-5-billion-tab-on-737-max-simulator-training

“In January 2020, Ron Epstein, aerospace analyst at Bank of America Merrill Lynch, estimates that groundings cost, excluding any settlements from lawsuits from crash victims’ families, could reach $20 billion, provided the MAX returns by June or July, 2020.”

Boeing is not going to make money on the program. Even at the low end that they estimate of $19 billion, way back in Jan – they will have to make a profit of ~$6 million an airframe just to cover the costs, given the current backlog of ~3500 jets.

A few points on this:

The financial loss of the MAX program has been tempered and merged with the impact of COVID. Compensation to airlines has tapered off due to lack of air travel and fleet groundings. Also the compensation has been negotiated into different forms. So I think the $20B mark is probably closer than $30B.

Second, even if a loss occurs in the initial sales program, there is value in the maintenance and support of a 3,500 aircraft fleet over a 20 year life. So together with write-downs of initial losses, it very likely will make a profit overall. If that were not true, Boeing would fold the program.

The same is true with the 787, which may have greater production numbers now, but in any case will have a long support life, as it’s not being retired.

One thing that has not been discussed much, is the loss of support revenue due to aircraft retirements brought on by COVID. If those aircraft are replaced by new, there is a net gain. But if the fleet shrinks overall, there is a net loss.

Rob,

Boeing is in too deep to can the 737 Max. What are they going to do – cede the entire segment from 100 seats up to their smallest 787 to Airbus for the 5-7 years it takes to bring a clean sheet to market? Cancel all the contracts and return billions of deposits to customers, who need the cash NOW?

The backlog is ~3500 units. Using LUV as the bottom of the revenue chart at ~$34 million a copy, and let’s conservatively say 25% of the aircraft is paid for, that would be $30 billion in deposits they need to return, for the backlog. That’s a conservative number. Not gonna happen.

Boeing doesn’t even have the $15 billion needed to launch the FSA to replace the Max. C-suite boys spent it all on buybacks.

As far as services go – let’s have a look at the financials to see how they fit in;

We start at Q4 2018, because that is the last year without the Max grounded and without covid. It is the benchmark:

https://s2.q4cdn.com/661678649/files/doc_financials/quarterly/2018/q4/4Q18-Earnings-Release.pdf

BA absolutely crushed it. Revenues of $101 billion, earnings of $12 billion – as a whole. BCA delivered over 800 aircraft, rev of $60 billion, earnings of $8 billion. The margin for the division was 13%.

Boeing is not going to tell us how much they make on each aircraft – the 787/777 margin is more, while the Max is less, but as a whole they made 13%. Up from 9.4% in 2017, and 3.4% in 2016. The best they’ve ever seen.

Let’s look at services:

For 2018, they had revenues of $17 billion and earnings on that of $2.5 billion, good margin of 14.8%.

But $17 billion and $2.5 billion are nowhere near $60 billion and $8 billion. And remember – this is when Boeing was flying high; services for this year are $11 billion, down $2 billion from last AND margins are down 85%, to $307 million, for the 9 months.

BCA drives the company; 60% of revenues, 66% of profits.

Another way: let’s take that best margin and apply it to the order book, to give us the best possible outcome that they could hope for.

From the 10-Q of the last quarter:

‘Total backlog of $393 billion, including more than 4,300 commercial airplanes’

Let’s say Boeing makes all of them, delivers all of them and get paid all $393 billion, even the 777X’s. At 2018 margins (13%) that’s $51 billion in earnings, over the life of all 3 aircraft, without losing any orders.

Split the difference between $20 & $30 billion, for the Max grounding cost, there’s $25 billion, leaving $26.

787 is down some ~$19 billion still, leaving ~$7.

777X development cost, $5-7 billion, leaving $0 to $2 billion.

This is the best case scenario, with the best margin from 2018, with a full and complete order book built and delivered, without any loss of orders, any slip ups.

What are the realistic projections?

Oh…we haven’t figured in debt servicing yet, to account for all the money BA has borrowed and the annual interest payments that will be required to meet their obligations and the portion attributed to BCA.

Defence is defence, but services cannot compensate for the losses incurred by commercial aircraft.

Frank, I appreciate your points, but by your own numbers, if $10B a year in service, over 2o years that’s $200B. Having aircraft in the worldwide fleet is a significant source of revenue. That has dropped during COVID like everything else, but it will eventually resume.

Same is true on the military side, that’s why all the uproar over the KC-46 also misses this point. Their contract stipulates service and support contracts negotiated every 5 years, for 40 years, with an increasing number of aircraft entering service for the first 15 years. So together with write-downs, that program will eventually make a profit.

Please note I’m not claiming that these programs are not deeply troubled, or that BCA is itself not troubled. But to insist they can’t make a profit over the long run is not really right. They could not stay in business if that were true.

This is where many of the criticisms leveled here, although mostly factually correct, depart from the consensus of the business world.

Rob:

The aspect of support is not as slam dunk as it seems.

In fact, Bo0ein takes a loss on warranty for 5 years on each new aircraft. So a new sold MAX is still a cost and for sure not generating support revenue.

While an NG is making money for them.

There is now a slump period when non delivered MAX are not aging out on warranty either (and unknown on delivered and not able to fly)

You have to keep in mind its not about Boeing as a whole, its about management getting their bucks before they golden parachute out.

Calhoun get a bonus for doing his job. So he wants to get MAX into service for his own gain not for Boeing.

Granted its like a ballistic trajectory, you have to weigh the altitude (money gained from stock that are part of the package ) vs down range as it decreases altitude (stock seeks its real level of value) and you don’t get as much money but your bonus is in there.

What we do know is the existing management group will be gone when the pigeons come home to roost.

My younger brother saw that in BP. Their MO was to run an operation into the ground and then bail to a new one.

Ideally as they turned the thing over to another guppy buyer, it all fell apart.

As I recall there is an old tale about a Carriage that simply disintegrated at the end just like it was intended to do.

As long as you get out of Dodge with your bucks that is all that counts for management now.

TW, these are your opinions as ever, which are distinctly your own, and are repeated at every opportunity.

The fact remains that every manufacturer with high-value products understands that the principle of life-cycle revenue goes hand-in-hand with life-cycle costs. Warranty covers failures or defects in workmanship, but not normal wear & tear, damage, and required maintenance. Also service and support, in some cases.

Those are principle sources of revenue for many industries, not just aircraft or Boeing. Often they are greater than the initial sales. They are priced to help ensure the program makes a profit.

Rob:

Its not an opinion, between the MAX mess and Covd, there is a change in the previous reality of what revenue comes in from where.

Equally many flights are suspend for NG and those do not need work.

Short term yes that impact revenue and long term that gap will remain on the records of not earning money or the MAX not aging the way it would and you get revenue from support.

At a time Boeing needs all the money it can get (see selling off the Yacht) yes, its a factor.

Rob,

Boeing is too big to fail. They aren’t GM or some bank, they are Boeing.

The federal gov’t has back stopped their bonds, which I believe are rated just above junk status. Think about that for a sec. Ratings agencies have analysed their position and determined that the risk of those bonds being repaid is just above junk status – very high risk.

Based on Boeing’s financial statement as of July 29, 2020, long-term debt is at $58.46 billion and current debt is at $2.92 billion, amounting to $61.38 billion in total debt. Adjusted for $19.99 billion in cash-equivalents, the company’s net debt is at $41.39 billion.

From Forbes:

Boeing had to offer sharply higher interest rates than past debt issuances – one 10-year tranche yields 5.15%, according to Reuters. If the total offering yields around 5%, that would add about $1.2 billion a year in interest expenses, estimates Robert Stallard, an analyst with Vertical Research Partners. Last year Boeing paid out $722 million in interest and debt expenses.

“Boeing is now arguably owned by the banks,” Stallard wrote in a client note. The offering raises Boeing’s total debt load to $54 billion, a fat 22 times its projected earnings this year before interest, taxes and depreciation, which will take years to be reduced to reasonable levels.

Boeing now has a $1.2 billion annual interest expense bill it has to pay – even if it doesn’t deliver a single aircraft. Put another way – let’s say BA delivers 30 jets a month, for all of 2021 (which is way optimistic, but WTH). 360 jets.

$3.3 million of any earnings made on each aircraft will have to go to debt servicing.

And no, to your point; as long as companies can borrow money, they can keep operating. When the debt load gets too much that lenders finally say ‘enough’ – they can go Ch 11, wipe out the current shareholders and the bond holders become the new owners.

Uber was founded in 2009 and has never made a profit. It’s market cap is $72 Billion. Hasn’t made a buck. 11 years. Billions of losses. $8.5 billion in losses in 2019 alone.

Tesla is worth $420 billion, but just had it’s first profits for 4 straight quarters. 17 years.

There is the very real potential that BA will not make a profit on any of it’s 3 jets, but they can continue to borrow money to stay afloat. If they want to launch a new aircraft, they’ll have to borrow the $15 billion needed to see it through. They had the cash, but…well, you know the story. $43 billion.

If you need further proof, check out AAL. I think they have a debt load now around $49 billion (it was $42, but the gov’t gave them a LOC to access another $7 billion, which they started using)

In 2018, the last year before the 737 max grounding & the virus, this is what they reported:

“Reported a full-year 2018 pre-tax profit of $1.9 billion, or $2.8 billion excluding net special items, and a full-year net profit of $1.4 billion, or $2.1 billion excluding net special items”

There is literally no way they will ever pay back all that money. It would take them 25 years to do so…

I could give you $50 billion today, send you out to buy/lease planes – and you could make a better airline the AAL.

Smoke and mirrors, Rob. Smoke and mirrors…

Frank, you’re bent on presenting the negative case for Boeing, and that’s fine. I look at it somewhat differently, as do their investors.

The $60B in debt is about equal to 1 year of revenue, in a very suppressed year. In a very good year, about 1/2 year revenue. It’s still a high number but also still within bounds of realistic repayment, over time.

Boeing has about $30B in aircraft inventory right now, assuming today’s suppressed prices. Most of that cost is sunken, and is part of the current debt load.

Their bond rating is typical of the current environment. Airbus is two steps higher, after a $15B government bailout. Most airlines are at Boeing’s level or lower.

The US government provided liquidity to the loan market with the expectation that banks would use it to fund businesses in the COVID crisis, which they did. You interpret that as a government-backed junk bond. But then so too is any financing offered by any bank to any aviation business, using that liquidity. It was a net positive as it created opportunity for both lender and borrower.

Boeing also has a very large array of fixed assets, some of which they are selling off now to raise capital, but which can be used also as collateral on debt.

The truth is that Boeing could not raise the equity they have, without making a solid business case for it. Banks don’t give credit because a business is too big to fail. The government perhaps does, but that has not happened with Boeing.

They need to move their products and get costs under control, which they are trying to do. It’s a tough environment right now for sure.

Then in terms of new aircraft development, they eventually need to make an investment, but the initial part of that will be design, the facilities and staff for which they already have available. They will likely need additional funding as they get into the prototyping/build stage. If they have commitments from airlines that will help.

It would all depend on their financial condition at that time. Certainly they could not progress beyond the design stage at present. Nor would the aircraft have a market if they did.

Rob

“The $60B in debt is about equal to 1 year of revenue, in a very suppressed year. In a very good year, about 1/2 year revenue. It’s still a high number but also still within bounds of realistic repayment, over time.”

Your numbers don’t add up. Revenues do not equal profits, nor do they equal free cash flow. In order for Boeing to make $12 billion in profit in 2018, they needed $101 billion in sales. There were $89 billion in expenses.

Since then, they have increased their debt load, which means higher interest payments.

Interest expense ALONE will eat up some $2.5 billion of that (continuing the last qtrs $643 million expense).

Interest Expense for the trailing twelve months (TTM) ended in Sep. 2020 was -242 (Dec. 2019 ) + -262 (Mar. 2020 ) + -553 (Jun. 2020 ) + -643 (Sep. 2020 ) = $-1,700 Mil.

Couple of questions:

Just when do you see BA returning to delivering ~800 jets and getting $60 billion in revenue?

If the CMV of the Max is in the $40–45 million range (LUV is getting theirs for ~$34 million, according to their last 10-Q), how do you calculate BA to have $30 billion in inventory?

If BA were to put every penny they made, using the $101/$12/800 jets model of 2018, it would take 5 years to repay their debt. ~6 years if you factored in interest payments. Without borrowing any new money. Without any additional expenses (like compensation claims related to the grounding from airlines/families). Which is their entire backlog.

You see those numbers happening anytime soon?

I guess that’s why they sold the yacht.

Yes, that is why they sold the yacht, and other properties, and will likely continue to do so.

I think the issue here is one that surfaces frequently in the comments. You insist your analysis is correct based on your own numbers. I don’t attempt to give those numbers because I don’t presume to know the full context. I do have confidence that lenders and investors who do have that context, will have done their diligence, and are not throwing their money away.

You are entitled to your views, but so are the people who have actually built wealth, built companies, and understand them well. They have a more positive view. I don’t think that’s unreasonable.

You’re right but at this point any new order for 777-9s presents some risk that the buyer will back out at the last minute (or go bankrupt entirely) and leave Boeing with a big, unpaid for, White Elephant. At this point all 777-9 customers (except Singapore Airlines, I think) have postponed or cancelled part of their orders. Any 777-9 White Tails will be extremely difficult to remarket whereas Boeing has found it reasonably straight forwards to remarket the 787-9 White Tails which HNA Group backed out of (from memory they went to Biman Bangladesh Airlines, Vistara and Bamboo Airways). No lessors have ordered any 777-9 and I would imagine Sale and Lease Back financing would be difficult – if not impossible – to obtain.

You hit the nail on the head! Boeing needs to inovate to stay competitive. How short are people’s memories? The 787 was a disaster in the begining. It is now a saving grace to the company. All new programs take longer and cost more in the beginning. We are not building legos. Fabricating the world’s longest single piece composite spars and skin are complex in nature. The investment in the composite wing center and Horizontal build line for the x were immense, but I would argue are already a success. Boeing outsourcing to MHI and Alenia was a gable that cost the company big in the beginning. When Boing builds and assembles in Washington, good things happen. There is alot of aerospace knowledge and history in WA for a reason. Avoiding the union to try and save some money is a bad idea. When you talk to a 10-20yr union mechanic, face value is a grumpy redneck, probably wearing camo. Really good at complaining. When the rubber meets the road you have an extremely skilled worker, very likely a generational worker as well.

Full agreement.

But its not innovation that is needed, its engagement that is dedicated to the Company and not themselves.

Management compensation and oversight needs to change, then you can have innovation.

That is why Boeing is treading water on what has been done in the past and has no current future.

The list of failures is not just BAC, its also defense. There is no management bench and the few good players that still can run from one project to another trying to salvage the mess.

Thanks Scott, I agree with this assessment. The market has changed and while there may be some recovery exiting from COVID, it will still emphasize smaller aircraft. So Boeing will do the best it can with the 777X, possibly being more open to the potential freighter market, but won’t cancel after the large investment that’s been made.

One would think so too for the Spacejet. Yet, having an almost developed jet seems not enough. The ramp-up costs for Mitsubishi are certainly a lot higher, but Boeing isn’t in a position where they can afford a lengthy period of burning cash just for the sake of it.

I think Boeing will invest the needed funding, unless it appears that there is no market interest in the 777X. For now that doesn’t seem to be the case. While orders are deferred, airlines have not abandoned their commitments. But obviously it depends on where the market settles post-COVID.

Some of the lessors have said that the need for the 777X is not ended, just deferred. They expect it to have greater viability with more typical production cycle as time goes on, and the travel market recovers. But it may be with reduced numbers, we’ll have to see.

This is more than about a granular decision.

Boeing sabotaged their future with share buy back and dividends.

That is baked into the current management DNA.

The real story is what path Boeing winds up on, Ford under Mulally or belly up per Penn Central?

You can’t run a Pyramid scheme forever. Piper gets paid.

A no decision is still a decision. Invest in the new products needed or go with the old death spiral?

>Boeing sabotaged their future with share buy back and dividends.

This is not so much Boeing as US management theory. Under American management theory the goal is share-holder return. Even if a company is successful now they may make errors in the future and so theory is it is better to give the cash back to the shareholder than leave it in the company. The notion is the shareholder can better decide how to invest those profits than future Boeing management can. And given Boeing management decisions who can say they are wrong. Certainly as an investor I’d be happy having gotten my dividends then.

While I agree its a US in vogue thing, Boeing management went whole hog in on it.

GE is in trouble as well so I understand its done, but it does not have to be done so yes I blame Boeing management. They understand what they are doing and doing it anyway.

Matth:

Its more than a new product or a revamped one.

Boeing failure here was short term outlook that did not come up with a viable new product and abandoned what is a market segment. They had to go bigger to compete on pax numbers as the hull did not on new tech.

Airbus has the much wider slot capable A350 that fits into the hot 777-300 market area as well as a bit above it.

MHI was a bad decision from the start as its a small market and they are not a small market operation. They make small market numbered stuff but its big return (industrial turbines) and government contracts.

End result for both may be the same but the hows and why they got there are much different. Well no thinking they have in common.

I too agree, I think the 777-9 will survive, I’m less sure about the -8. I could well be wrong, but we may see a 777-9 freighter option before we see a -8. Previous logic was for a freighter based on the -8 after the -8 had been certified.

If you may only deliver 600 to 800 777-Xs over the lifetime of the model, why would you make things more complicated, and split that number into different models at this stage where there is so much uncertainty ?

Offer a freighter conversion, and you have a number more frames to sell to keep things ticking over at low rate production until the market recovers. You also provide another reason for customers to buy the passenger aircraft as they’re viable as a p2f conversion if things change.

Would a -9 based freighter be too big ? There are operators of the 747-8F, and the 737 based freighters, and everything between, I think Qatar would probably order a -9 freighter if it was offered.

If it turns out that the market recovers far better than anticipated, you still have room to do the -8.

At some point the world will return to normal, it may take five to ten years or even 15 years, but I think it will recover. A number of 777 ‘classics’ will need replacing around then, and as long as the A350-1000 hasn’t gained too much of a foothold in traditional territory, there will be space for a 777-9.

With the A380 out of the way Emirates is going to need something as large as possible to replace it’s existing A380s as they retire. There are still a number of point to point destinations where A380s work as it’s easy to fill them, I don’t see a problem filling a 777-9, and indeed, in some cases even the 777-9 is too small.

I do see certification taking longer than Boeing or the FAA thought prior to the MAX fiasco.

I only caught a few minutes of Patrick Ky of EASA on the MAX at a press conference on TV a month or more ago, it sounded very interesting, but I haven’t been able to find the full video anywhere. I wonder if anyone else saw that press conference, and has a link to the full video ?

I’m really interested in the full context of what he said as it would certainly have implications for 777-X certification.

600-800?

Boeing would sign that any day.

Airbus would sign that all day long for its A330neo.

Look at the backlog.

Cathay won’t take it. They are hit hard by the protests and then the lockdown, have A350 and a lot B77W. Why would they need 21 B779. They would be more happy to have more replacement for their A333 fleet, and the B78T would be ideal.

Etihad is out. They won’t take any, 6 doesn’t make any sense.

Lufthansa would like to reduce but is one of the few carriers who will take them. BA will take them, due to Heathrow.

SIA will take them.

Emirates will proplably delay delivery and slow it down, their model is at the limit now and they would enjoy more B789.

I can’t see 60 at Qatar. Over 80 A350s, 60 B787, the existing B77W and on top 60 B789? They would need massiv growth to fill them.

So overall, Boeing must be happy if they have about 200 – 250 firm oders.

Most airlines would be happy to switch their B777x orders for B787.

Boeing is now at A380 numbers order wise.

Sash,

I was thinking 600-800 over the next 20 to 25 years, certainly not in the short to medium term (as long as it’s viable over the short term).

I agree Cathay is problematic, will probably end up converted to 787-10s. Qatar, agree also no way 60 777-X.

I do think over time Emirates will take enough 777-9 to persuade Boeing to keep going. Emirates model will have to evolve in some areas as they were able, pre-COVID to fill A380s into a number of airports, some of which (LHR being one) that were slot constrained. On the slot constrained routes, there’s just no substitute for an A380, even a 777-9 is just not big enough.

Of course at some point over the next 20 years, Airbus might NEO the 350, and that would take another chunk out of the possible 777-X orders.

Jak,

they said that about the A380 too. Emirates will take enough to keep it alive and get an A380neo.

Airbus is already talking about an A350neo, and I’m pretty sure it comes with a stretch for the A35KK or whatever it’s named.

The bet is that goes with the RR Ultrafan, available in the 2nd half of the decade.

This is the trouble with delays, as seen with the A380 – it was to heavy, to large, and didn’t offer better costs or technology to make up for it, as it’s delay borught it close to the technolgy shift.

The A380 would have been much better if it would have had the B787 engine, though the 87 was delayed.

If the B777x comes in 2022, and Airbus is deploying it’s A350neo with the RR Ultrafan arround 2027/28 – the A350 is 15 years then –

Boeing has a problem.

It’s to early to do a re-engine of the B777x, they basically just did one. Airbus will boost the performance of the A350 also.

And Boeing will need to re-engine the B787, which will be 18 years then.

I think on thick routes, we will see the A380 survive. But that will be less routes than we expect.

I don’t have any further information, but it sounded like Ky put the onus on Boeing to deliver 777X safety analyses and certification documents. I think he feels that if Boeing does this, then EASA will process those documents in a timely manner that won’t delay the certification. So that echoes Dickson’s position last December that the best way for Boeing to expedite certification is to be forthcoming with documentation.

That sounded reasonable to me. I think EASA will have more of a partnering role in verifying certification and raising any issues with the FAA. And I think FAA will also be looking at the amended type changes (especially controls) in greater detail. And finally I think Calhoun knows this, and is allowing extra time for the certification process to satisfy all the stakeholders.

Jak:

The reason the 777-200 was chosen as a freighter platform was its loading and range ability. It has the -300 wing.

While a 777x (8 maybe) might work for FedEx (UPS seems set with the 747-8F) that is package and a small part of freight.

The 777-200F is likely to be the long term freighter option.

F comes after a successful PAX run, 747-8F shows its supplemental and not a mainstay.

The 200F/8F and the 747-400F (fuel burn not as big a deal now) cover that market solidly.

FedEx now uses the 200F in a combination of long range high value flight and to start replacing the MD-11F in slots.

Also in play but a huge unknown is Wide Body recovery and the lack of belly space vs the freight market.

UPS runs the 767 on International routes (that is not the norm but they have shown it works)

In that larger size the 747-400/8F are far more flexible due to the nose loading.

747F production will end in the next 18 months or so. The airframe sub contractors have moved on, Boeing just bought enough assemblies to tide them over. That just leaves the 777F and 767F in production. The reduced hours that freighters fly compared to passenger jets means they will be flying long into future. I dont see Amazon buying new planes as their busines model requires near end of life planes and pilots with blemishes on their records

To Your Attention

”

GECAS Cargo announced an agreement with Kalitta Air for three Boeing 777-300ERSF aircraft. With this agreement, Kalitta will be the first operator of the new passenger-to-freighter type, adding to their already sizable all-cargo fleet when these aircraft deliver in 2023. ”

This conversion is to be done by IAI.

How successful the 777-300 conversion to F is depends on who Kalita is going to lease it to. DHL or ?

You can’t just order a new 767 or 777F. Production is so low rate you are in line with FedEX and UPS.

So yes it has to be Pax to F conversions.

Both UPS and FedEx use their F types heavily as they do international with them (FedEx and the 777 and UPS the 767)

Rob,

I only caught a few minutes of Ky’s statement, but the bit I was interested in was where he appeared to say regarding the 737-MAX, that Boeing, and the FAA were only going to deal with MCAS, and that it was the other regulators that convinced them that there were a number of issues to be satisfactorily addressed.

I really want to see the whole statement to understand exactly what he said, and in what context.

On the face of it, that looks like all the regulators will not take anything for granted with the 777-X (or any other new aircraft), and that I suspect, inevitably means that it will take longer to certify than Boeing or the FAA originally had in mind.

I also saw some mention elsewhere of a possible problem with 777-X certification. It was a Q & A, and when asked if the issue wouldn’t just be dealt with through software, the answer seemed to indicate that might be problematic. Again, I’d like to see the whole text, and preferably a couple of trusted sources. I’ll need to do more research.

Can you shed any light on this ?

JakDak, I was quoting Ky from the press conference announcing that EASA would recertify the MAX. In that context, he was asked about 777X certification, and as I reported, he said that it was really up to Boeing as far as any delays were concerned. He didn’t seem to think a delay was inevitable.

I haven’t seen any of the other remarks you cited, so am not sure. I’ve never heard Ky speak critically of the FAA, nor Dickson of EASA, I think they are both too professional for that kind of behavior (I won’t use the more indicative “classy”, to avoid another uproar).

With regard to 777X technical issues, I’ve seen speculation in some forums that it has the same pitch augmentation problems as the MAX, due to the large engines. Not sure if that is true, but since the 777X is FBW, it really shouldn’t pose a problem, anymore than it does for Airbus.

Also some talk of the tail being undersized, but that too may be based on people’s mistaken notions about the MAX, which were disproven.

We do know the 777X just completed a 10 hour circumferential test flight of the US, flying at different speeds and altitudes. So it seems unlikely that it has significant control issues.

Thanks Rob,

I don’t think, the few minutes of the Ky press conference that I saw was the one you mention.

I too was surprised at what I heard, I don’t think it was a direct criticism of Dickson, or the FAA, it appeared to be a matter of fact statement, a documentary of the path to certification. That’s why I’d like to see the whole press conference.

I agree both Dickson, and Ky are very professional. I’m also sure that it’s a difficult task to balance economic, and political realities.

Again my argument for an international, non-political, non-partisan flight safety, and regulatory agency with no economic mandate.

The tail being undersized was what I’d heard, but still can’t find a reputable source. I’d find it strange if it was the case, modifying the 777 to a 777-X, I don’t see how you’d get something like the tail wrongly sized.

Surely not a re-run of the 707 tail fin height issue, the -X tail fin I believe is taller than the original 777? Puzzling.

JakDak, the discussion within & between regulators, of their positions and certification processes, is confidential. So that generates a lot of speculation in the public and media. There is actually far more speculative reporting than factual, just because of the dearth of information.

Some of the speculation then persists even after the facts are available. A good example recently in the FAA public comments, a person with concerns about the MAX, offered to share his Internet story links with the FAA, if they didn’t believe him.

That was both a bit comical and a bit sobering. The Internet quite willingly fills in with opinion, when the facts are not yet known or require effort to discern. For a person steeped in that environment long enough, the opinion can become elevated over the facts. The extreme case of this is the conspiracy theory, where the person no longer trusts the facts at all, only the opinion.

So we should be careful about jumping on the speculative bandwagon. It requires more discipline to either search for (or wait for) the facts, but that’s the most beneficial in the end.

With the regulators, I consider the path over time, which has been one of convergence and agreement. Individuals within the agencies may have dissenting opinions, but overall there is consensus. That is what we expect to see, when as in science, there is a factual process. Divergence only occurs where opinion is given precedence.

That’s also why I think CAAC will certify the MAX eventually, unless their government forbids it for political reasons.

After knowing that the self-certification business was lost on Dec 12, 2019, MAX production stopped. 777X production should have stopped too.

Are Qatar’s and Emirate’s configuration very different to Lufthansa’s?

Would the already produced 777-9 be too expensive for a freighter conversion?

If LH2 really picks up, a big fuselage is good to have.

But till then maybe Methanol will be carried and transformed to H2 during flight.

Leon:

Self cert had nothign to do with the stop on MAX. It was 450 non delivered and them scrambling to fix the mess. The MAX production is resumed at much lower rates.

Boeing can build anything it wants, it just can’t self certify the MAX and I don’t know for sure what happens on the 777X as it is not certified yet.

In a couple of days we may see a sea change going to occur and different management on Jan 20th on.

This is a case of where political has an impact as a lot may shift on Nov 3, a huge amount in play involved for the FAA future.

The probability that the 777X will be an economical success for Boeing is very small now. It would require a recovery of air travel that exceeds the capabilities of the 787 and A350, both in airport slots and availability. If I try to put a number to it I would hazard maybe 20%. Still, there is a chance, and there is little damage done by running the production on low figures for the coming years. The investments are all made if as long as making the X is not cash negative, I expect the line to remain open.

I agree with you, but if Boeing is only making ~2 777-9s a month, then they will be bleeding a lot of cash. Boeing just built a ~ 1.5 Billion factory for the 777X’s wings which will have to be paid off.

Also agree but keep in mind, Boeing has lost 20 billion still on the 787 and its not affected how they operate.

They are on a slippery slope.

Cash bleed I think is done for now, something the size of a Meteor Crater.

They simply write stuff off but where they go with not buying off shareholders and themselves with one modern product?

Right, but now the factory is built and the development and testing paid for. So if Boeing doesn’t sell enough of the 777X to completely recoup those cost, then at least they recoup/cover a part of it. If they stop production entirely, they lose the entire investment.

Of course, there is a minimum quantity that have to be produced to cover the monthly cost for the operation, maybe at 1/month. If you fall below that, it would probably be better to close the production down, as we have seen on the 747-8 and the A380. But I don’t expect the 777X will face that badly.

Back to each mfg of a 777x does not return 300 million.

You have to pay for the whole thing still.

In reality you add to the program costs until you break even point is reached.

So yes, you keep going deeper in the hole for that period.

1 a month is a limp along process that looses money when you need at lest 4 a month.

Airbus ran into that with the A380, they lost money, just not as much but also if kept going losses worse as no new orders.

Overhead has gone up as 777X and 767 have to pay for all of Everett now.

Oh for sure. Boeing is in a really difficult position here. They can’t afford to cancel the 777X program yet it’s unlikely to ever bring them positive cashflow.

Its the other way round actually. The cash flow will be positive soon enough, even with small numbers, as the development, factory, certification, tooling is all paid for. So as long as the sales price fetches more than the net production cost (materials, labor, energy, heating, cleaning,…) you have a positive cash flow. The difference between production cost and sales price is the gross profit, which should cover the investments, taxes, interests, etc. After that is all paid you have a profit. In the case of the 777X, Boeing might never see a profit though it may turn cash-flow positive with something like 2 monthly deliveries.

“”The cash flow will be positive soon enough, even with small numbers””

Depends how high the Pre-Delivery-Payments are.

If PDP are 50% Boeing might have burned that already.

It seems Boeing hasn’t learned too many lessons from the 747-8. All the signs are there — plain as day — but it’s less traumatic to cling to fantasy and pretend that increased demand is just around the corner.

There is such a thing as “throwing good money after bad”.

Yes, “throwing good money after bad” is spot on!

another motto is perfect for the certification process

“once bitten twice shy”

FAA will probably double check every single design detail…

that will take a long long time.

If certification requires any modification on already assembled frames, that will not be cheap….

and cash will keep burning…..

New deffered costs coming???

Bryce:

Laugh of the day. I have not seen Boeing management has ever learned anything about their failures.

Honestly, I can’t say I’m at all surprised at this situation that Boeing has gotten themselves into. It was fairly clear from the beginning that the 777-X was going to have very, very limited appeal at best.

The 777-8X never had a future beyond a few token sales to the ME3 and presumably as a freighter.

Supersizing the already large 77W limits the 777-9’s market appeal at the best of times. Optimizing the aircraft further so that it can fly a full payload from AUH/DOH/DXB to the West Coast of the US on a 50 degree + day reduces it even more. That’s optimization is fine for operating those missions, but for shorter missions (which are a much higher %age of the Long Haul market) such as AMS/CDG/LHR/ to IAD/BOS/JFK the extra weight that the aircraft are carrying around makes them less efficient than say a 787-10 which is appropriately optimized for that kind of mission. By focusing the aircraft’s performance for such missions, Boeing essentially built an aircraft for the ME3 that was never going to be particularly competitive in the fleets of “regular” carriers.

In a post-COVID world, most operators who are evaluating replacements for their 77W fleets aren’t going to want the risk of having to sell an extra ~50 seats per flight as compared to existing 77Ws. Depending on your outlook on the demand for business travel, this could be even worse: a COVID induced collapse in the business travel market means that existing 77Ws are eventually going to get refitted with more Economy seating and less Business seating to properly match demand. In this situation (who’s probability is hard to say at this point, but it’s not looking good) airlines looking at a 777-9 would be having to judge if they could justify selling ~80+ Economy seats per flight as compared to a 77W of today. Justifying the purchase of an 777-9 becomes much harder than as compared to a 787-10 or A359 (or even an A350-100 I would think).

Unlike the A350-1000, the 777-9 doesn’t have a successful smaller sibling from which it can gain fleet synergies with. Although I am skeptical of the A350-1000’s future success (although much less so than that of the 777-9), I recognize that, thanks to the A359, it doesn’t really need to sell that well. If Airbus builds/delivers 6-7 -1000s per year then the A350 program will still be fine. If Boeing can only build/deliver 6-7 777-9s per year then the 777 program will be deep into the red.

The 777X won’t lose as much money as the A380 program did, but this is going to be very painful.

An excellent comment.

Tailoring the B777x to Emirates demands might have been too much for other airlines.

There’s an often-overlooked point on yields: If you add seats it’s not only you lower seat-mile cost and gain effects of scale. You usually also gain lower yields due to higher supply.

That’s why the additional +40 or so seats from A35K and B779 don’t matter that much, though they offer great CASM. You have to fill them often for a good yield to realize the advantage.

Look at the US flag carriers. They only operate small numbers of the B77W, with United being a late customer and AA only operating 20, thus both have huge B772 fleets. None of them has orders for A35K – Delta has converted theirs – and none has ordered A380, B748 or B777x.

They have huge orders for B787 (or Delta A339), AA propably going on the B787 as only WB, and A359.

Out of all the WBs available, A359 and B789 seem to have made the race.

In case you really have demand for a VLA, you either fly them twice – or you just raise the prices, and take the $$.

Exactly – when talking about matching aircraft capacity to demand, most people are always forgetting that airlines are perfectly happy to leave the lowest yielding traffic behind and enjoy higher load factors + stronger yields.

Depending on how bad the effects of COVID is on long term demand, I expect to see a substantial portion of 77Ws get replaced by A359/787-9 sized aircraft.

Boeing pretty much has to keep the 777-X program going – otherwise it effectively cedes the bigger twin engine market to Airbus. I don’t think it will be the roaring success that Boeing had originally hoped, but if traffic picks up by the middle of the decade it will find its place in the market.

Yes, that is also the position being taken by some lessors, and I think by Boeing as well. It will have a place, but probably not as large as once imagined.

First 777-300ER didnt go into service till early 2004 and most of the deliveries have been in the last 10 years, so too early to fill most of the replacement market ( which is around 1000, when you include the sibling heavy weight planes).

For those flights of 10 hours plus, time zones, preferred boarding times isnt solved by increased frequency. It isnt as easy as the short range mass market of around 2 hrs or less.

I don’t buy that the A321 takes over significant wide body missions.

Narrow thin ones possibly, but the long ones as noted turn around and flights get to be non viable and pax numbers make a difference.

Frequency can work to a smaller aircraft advantage but you don’t get frequency on an 8-10 hour flight.

It seems that Airbus got lucky (this time) by delaying to give a green light to the A350-1100/2000. Maybe it’ll make sense in 3-5 years, with new engines, but for now the demand simply isn’t there.

Agreed.

Timing is important as are strategic decisions.

Reality is Airbus has made more better ones than Boeing management .

I refer to Boeing management as I have been accused of being anti Boeing.

I am not, never have been. Boeing as a company was a proud contributer to the United States at one point.

Boeing Management has brought a fine company to an all time low that goes back to the perilous days of their founding when they could have gone belly up like so many other firms.

Boeing has not failed, its management of the last 15 years has failed in all aspects (including defense)

They shared the specification of such an aircraft to the many A350 operators, including the ones with 777X orders. That didn’t help & most 777-300ER are relative young indeed.

“Prediction is difficult- particularly when it involves the future.”

— Mark Twain

But it is still interesting that both air-framer’s have been caught out building aircraft that are too large. The need to post “DON’T BET AGAINST THE SMALLER MORE CAPABLE AIRCRAFT” in their design centres.

In the next decade we will see range improvements on the 787/350 to the point where they can pair any two markets. We will see a 5000nm+ larger single aisle and a 4000nm+ A220. If Embraer or Mitsubishi ever get their act together we’ll see a transcontinental “regional” sized jet get some traction.

One of my points as well. Boeing vacated the 777-300 space and with a product that is viable only because its larger capacity.

Airbus has a core A350-900 that has been stretched and can shrink (not successfully but it is there if it fits a need)

777-8 was never a stand alone viable product sans a larger 777-9 fleet.

It reminds me of Ford and the monster car the Mustang became and left the large numbers build behind in the hope you could make money on fewer higher priced.

Someone always fills in behind you and gets that larger market.

Boeing didn’t vacate the B77W space.

Airbus attacked it.

It’s the airlines going for B789 and A359 instead of larger options.

Most of the B77W are to young to be replaced and Boeing has sold out this market. The A35k doesn’t have a significant amount of orders, there are not even 200 in the books.

Boeing had to stretch the B777x to make it competetive and build a new wing. Their main customers from the Gulf requested it.

The B779 is an airplane tailored to the needs of Emirates and Qatar.

Sash:

When attacked you can do one of three things

1. Stay and fight (tough part)

2. Run (easier)

3. Surrender (not a great option but ….)

Boeing rather than doing an all new aircraft that would compete with the A350 vacated (ran) . The Chicken management decision base on shareholder profits not long term Boeing good.

Boeing had a great position on the 777-300 market area, and they left it. That was a risk and it may well prove to be another failure, break even at best.

TW,

the 777-9 is only 2.13m longer (2 rows) than the 777-300, the 777-8 is 5.32m longer than the 777-200. The 777-8 escaped the A350-900, the A350-1000 can fight against the 777-9 since even Bjorn said that per seat costs on the 777-9 are not better.

With 2 rows longer Boeing can disguise the higher OEW of the 777-9.

The future. Looking into the future, there is a lot of technology that will come online in aerospace. The big question is What, and When? We’ve been reading about electric and alternate fuels; the Ultra Fan is near, new materials are being used, and the blended wing may fly. I don’t see either BA or AB, doing these type of “Moonshots,” in the near term; but I do see them thinking in ten years the NSA could be quite a different airplane then what we have now. The type of big changes just waiting for the economy to pick up could be NMA, A322, B757 replacement, and / or A220-500. Intuitively, Mark Twain, Jr.

10 years entry into service is basically now in terms of technology maturity. So tube and wing, ultra-fan, PIPs on the GTF. More automation on existing materials, both carbon and aluminum. More 3-D printed parts such as brackets etc. More electro/hydraulic actuators. Next generation high lift devices possibly avoiding a central hydraulic system. Full digital twins for faster, lower error design.

But no new configuration such as blended wing or trussed wing. No new higher efficiency core for the GTF (unless they are further along than they let on). No radically new materials or build systems. And especially no new fuels or electric propulsion. Those are all at least 15-20 years away from an EIS perspective.

787 Production in Charleston:

I would like to note that the subscription only part about Charleston capacity is nothing new.

Its been out since the beginning that they had excess capacity and the building was under utilized.

they can do at least 10 a month there if not 14.

Under utilised ? They seemed to struggle even with all the space they had as quality problems meant planes were pulled out of the building for rework ( no space inside the FAL building)

The average time per plane on the assembly line was around 22 days while Everett could do it in 16 . Its been shown already to be wishful thinking that the build time will decrease and now they want to speed up the monthly out put .

Knowing Boeings habit of making a wrong decision for the wrong reasons a hurricane could come and cause major damage as well.

The difference is that space has nothign to do with quality. Boeing deliberately made Charleston bigger than needed for a single line as part of the long term plan.

That is why there never was a decision on 787, as soon as they could the 787 was moving to Charleston (long term at rate 10)

You have a green workforce at best, the area is not noted for its high education levels let alone the pride established by 100 years in Everett or the legacy of a multi generational work force.

Not all of this is just Charleston. Boeing quality at Everett has also gone down hill (MAX with FOD, KC-46 and all its issue)

Charleston is just worst as its the core of the aircraft done wrong but that is Boeing management MO, lower costs no matter what the consequences.

“”Charleston is just worst as its the core of the aircraft done wrong but that is Boeing management MO, lower costs no matter what the consequences.””

In the six month April to September Boeing delivered 20 787. At rate 10 they must reworking 40 tails, 2/3 of the production.

If they couldn’t deliver 10 in October then the production is still not fixed.

Only ten years ago the same people said bigger is better.

The mantra was airports don’t have many slots left.

Airports should not restrict planes, right.

I’m sure every airline would prefer a 96t OEW, 248 pax, 7700nm range WB over the 777-9, eight days a week.

Since when did it become fashionable to manufacture significant quantities of airframes *before* certification has been achieved?

Do other aircraft/engine OEMs do the same?

If you believed when you started development, that certification was a certainty, why wouldn’t you start building production aircraft as soon as possible ?

If you’ve designed, built, and tested the aircraft correctly, you’d have nothing to fear from certification. However, if you take shortcuts, or get something spectacularly wrong, then going ahead, and building aircraft before certification is risky.

From what I remember the A350 got EASA certification towards the end of Sept 2014, FAA cert not long after that. One A350 was delivered to Qatar in 2014, but I don’t know how many Airbus had actually built by the end of 2014, but they had only delivered another 14 by the end of 2015. So it looks like Airbus hadn’t built a couple of dozen before certification.

Like you, I’d be interested to see data on certification dates of recent aircraft, and number of production aircraft built in advance of cert date.

I certainly don’t think that Airbus did this type of “pre-certification manufacturing” for either the A350 or the A330neo. I also don’t think they did this for the A320neo or the A380.

Any idea if Embraer does this? Or (the old) Bombardier?

Scott, could you please give us some clarity on the 2-dozen built 777X number? I have only seen 4 that are flightworthy, and those are still in the test fleet, which is about the normal number for a certification program.

Are the 2-dozen already built just non-engined, non-flightworthy airframes? Sorry if that’s a dumb question, just trying to make sense of the numbers.

I can’t speak to their flight status, but there are 777Xs all over KPAE parked. Some in colors, some in green.

Thanks Scott. I found seven 777X tail numbers registered thus far. So perhaps those are airframes awaiting completion. None of them have flown.

I think they need production certified engines which are coming soon if not being delivered.

“”If you believed when you started development, that certification was a certainty””

Muilenburg believed that everything was streamlined to allow Jedi-mind-tricking-self-certs till Dec 12, 2019, then he stopped MAX production, but he did not stop 777X production.

As if the 777X were treated different LOL

Even Clark asked about the 777X software. I can imagine that Emirates will only take 777X if Boeing signed that there is no new software. If it turns out that there is new software Emirates gets $100m for every 777-9.

Same as the SW deal, if sim training is needed, $1m discount for every MAX.

Calhoun can’t stop 777X production yet because of his bonus.

We will have fun to talk about 777X certification for years.

What used to be prototypes are now more or less zero series products. ( That is if you do your homework and have all your “moonies” tested elsewhere. )

In the sense that a “prototype” is not a finished product, but will be fixed from test findings for series manufacture.

Where today’s “Zero Series” are regular production samples that are used for certification. ( ideally proven when those “Zero Series” items are being sold off to customers afterwards.)

When I estimated the OEW of the 777-8 and 777-9 years ago + the investment required and specifications the new wing, that already raised some flags.

That an aircraft is a bit heavier than it’s competitor that is often compensated by extra capability. If that capability is marginal and the “a bit heavier” is 30t I start feeling uncomfortable.

Looking at wing/ engine specs a future 777-10x is clearly bakes into the design. Problem is they left open 300-350 seats/8000Nm territory to the real heavy 777-8 and payload range limited 787-10.

And it’s not they weren’t warned.

Remember the airbus credo: “A full A350-1000 weighs less than an empty 777-9”.

Food for thought.

It is food for thought.

But I remember an article that Bjorn wrote where the 777-X, and A350 were compared, and it was surprising that both aircraft were closely matched when you got down to cost per seat.

In the end the airlines would buy what works for them at the time, or what they thought would work for them at some point in the future … and then COVID happened, and is still happening, so it’s going to be an interesting ride.

Yes its close, and if they could sell it a -10 is a bit of a plus on top.

But is it too big and the A350 ranges in lower sizes for a wider market and that market was good with the 777-300 variants.

In its heyday the 747 for any given period was not selling in those numbers, it had a head start of many years and was the only player in that size and range for most of it.

“”an article that Bjorn wrote where the 777-X, and A350 were compared, and it was surprising that both aircraft were closely matched when you got down to cost per seat.””

Do you mean the one where Bjorn wanted to compare apples with apples, then I already have a laugh.

When comparing per seat, Bjorn must have compared 777X narrow seats with A350 wider seats, giving the A350 an over 3% disadvantage from the start.

What are Bjorn’s tainted per seat numbers good for when every airline is using own seat, lavatory and galley configurations.

According to Boeing’s payload-range curve the 777-300ER can’t reach 8500nm and according to Boeing’s own data the 777-9 has less range than the 777-300ER. All A330neo and A350 can reach 9500nm.

Boeing even didn’t offer the 777-9 for Quantas’ Project Sunrise, must be because the 777-9 can’t compete, but Bjorn said they are same.

I wonder how much MTOW can be reduced on the A350-1000 to make capabilities same because then A350 wings need to lift less weight per sq ft than 777-9 wings.

The comparison was between A350-1000@2016 real numbers vs 777-9x@EIS promises.

We’ve seen that the A35K is not a static target.

@Bryce

Regulatory Capture?

FDA not independent

https://www.statnews.com/2020/11/03/should-fda-be-independent/

I think it’s not inconceivable that a non-independent body could be seduced/coerced by a powerful pharma lobby…it wouldn’t be the first example of conflicted interests 😉

On the subject — more articles pointing out that T-cell response appears to be more important than B-cell / antibody response in the case of CoViD, and also pointing out the shortcomings of having vaccines that only use a single spike protein to illicit an immune response:

https://news.berkeley.edu/2020/09/09/for-an-effective-covid-vaccine-look-beyond-antibodies-to-t-cells/

https://www.bmj.com/content/370/bmj.m3563/rr-6

@Bryce

Thank you for these links

The Stat article was more concerned about the FDA being overruled by the Department of Health than corrupted by pharma ; but look at the FAA – I think there’s a lot more money to be made out of drugs than planes – so same difference : everybody is in a rush, come what may

From the bmj article « It is high time for joined up solid scientific rationale to overthrow mainstream narratives based on an alternative “science” controlled by industry interests/politics »

Mr Hellerstein’s arguments are in the same direction

Again just to add clarity, the vaccines in Phase 3 clinical trials do provide T-cell responses in addition to anti-body responses.

Further as the antibody responses are around 90% after the first shot and rise to 100% after the 30 day booster, the T-cell response is fully present after the first shot.

So the dependence of the immune system on T-cell responses also favors the use of a vaccine, doesn’t detract from it.

The FDA has resisted pressure from the Trump administration to accelerate. They use independent advisory boards (similar to JATR for the FAA) to help assure they are following the best science. So the claim of undue influence also lacks merit.

The premise that a vaccine is somehow a mistake or not beneficial, is being dismantled with each new wave of information. It’s very likely to be found both safe and effective. But we need to let the trials complete and fully analyze the data before jumping to conclusions.

One unfortunate advantage of the recent surge in cases, is that it has the effect of accelerating the trials. Hundreds of people have to become infected to get a statistically representative sample. It’s not ethical to infect them, and that would alter the results, so has to occur naturally.

Another issue is that people who volunteer for the trials tend to be knowledgeable about the virus, and so tend to get infected at a lower rate. The people who would become infected quickest, dismiss the virus and wouldn’t volunteer.

The turnout of volunteers was quite large, so they were able to choose people with high exposure professions (healthcare, bartenders, etc). Good to see so many people recognize the benefits and want to help. Many said they knew people with severe illness or death.

@Rob

Unverified assertions as usual – provide links to show detail reports

FDA part of the Department of Health, takes orders

Is using fastest track régime EUA – many are against this, within FDA & without

Much internal dissent – read the links before replying

There is as yet no premise concerning something which does not yet exist, a vaccine

@Gerrard White

When you have a court full of people who don’t know what they’re doing, it’s very easy for a Rasputin to come along and exert undue influence in a particular direction. You can fill in for yourself who the court/Rasputin are in this particular analogy 😉

As regards the minks: yes, there was animal-to-human transmission on a mink farm in NL a few weeks ago but, in that case, there was no mutation made known, and only the minks on the farm were culled — not the country’s whole population. The fact that Denmark is now culling the country’s entire population of (15 million) minks indicates that the authorities have had a nasty wake-up call. In the following link, note the sentence:

“genomic analysis of Danish human cases of coronavirus indicates half of the 783 human cases of coronavirus in the northern part of the country are related to mink”.

https://www.nationalgeographic.com/animals/2020/11/denmark-mink-culling/

Do you think anyone in the airline industry follows any news regarding vaccines / immunity, or is the industry just clinging to a default fantasy that an all-encompassing silver bullet will soon be announced?

@Bryce

I think the rush to get a vaccine out is to be compared with the rush to get the max out : band aid the thing later if too many people start to complain

The studies you have linked to and others too insist on two things, amongst many others, which are of relevance – vaccines take a long time properly to be developed as effective, coronas are really tough to vaccine against, and… ok mutations in this bug are being discovered in increasing numbers, the version doing the rounds in Europe at the moment is The Spanish Corona, and the logistics of the mrna vaccines are horribly complex and expensive

Your new link points to deeper underlying currents and spread – if anyone did a random check on sheep, pigs etc what would they find ? Maybe this virus is much, much, more widespread than naively hoped

I assume that the sentence you quote means that more than half of the 783 human cases were related to mink in that the same mutation as found in the mink had spread to humans – rather than the other way round – so that the virus initially had spread from human to mink, established a foothold, then improved itself by a mutation which allowed better travel between species

As with the researchers in Central Africa, what you really really do not want is for this virus to be come so adept and agile as to switch between species, and to build up a reserve in ‘reservoir’ species hard to get at, or to get into your pork and beef factories

As for airtravel -It’s not only the complexity of developing a vaccine, certification systems what’s the word for secure certification so you can know that the person in from a very long way away has not bribed his document ? – it is to take into consideration mutation, to widespread testing of animals, domestic ind ag and wild – all this to be subject to universally approved standards implementation and inspection with a tolerance of failure very very close to zero

That’s a lot more money and much more effort than the aviation industry is worth – a great opportunity to close it down, plan out a new business model and open doors in 2025

I would have thought, from the links to the various crises in European airlines you have been posting, that the walking wounded would be glad of a rest and a chance to jettison a model that has’nt been working for some many years now

@Gerrard White

Where the aviation industry is concerned, you’ve laid your finger on a number of sore points:

(1) There are plenty of Greenies in Europe that would love to see the aviation industry go into the dust…after all, they’ve been brainwashed by Greta into believing that it is the root of all evil. For example, Greenpeace are suing the Dutch government over its financial support of KLM, arguing that such support indirectly flies in the face of various environmental laws.