Leeham News and Analysis

There's more to real news than a news release.

Outlook 2024: Embraer’s continued recovery

Subscription required

By Bjorn Fehrm

January 8, 2024, © Leeham News: Embraer was hit by a double whammy before and during COVID. The non-closure of the merger of Boeing’s and Embraer’s Commercial Aircraft Divisions and the halving of its E-Jet deliveries during COVID. The year that passed marked the recovery from the extra cost and effort of the non-merger and an increase in E-Jet deliveries and orders.

It was also a progress year for the EVE eVTOL venture, with Embraer finalizing design and starting prototype production. Despite the EVE lagging behind other programs by about a year, the customers believe it’s one the most viable programs. Eve doubles the preorders of the nearest competitors.

The past year will also be seen as the break-trough year for the KC-390, Embraer’s bet to replace the venerable Lockheed-Martin C-130 military airlifter. The customer list went from three to five, with more country air forces in serious negotiations for the KC-390.

Summary:

- The E-Jets are trending back to normal volumes with better margins.

- EVE is the best-selling eVTOL, as operators trust Embraer’s knowledge and support.

- The KC-390 is on its way to capture a big slice of the C-130 Hercules replacement marker.

Air freight growth: one-hit wonder or long-term trend?

Subscription Required

By Judson Rollins

Introduction

January 13, 2022, © Leeham News: COVID-19 has upended the freight world, with air delivery now becoming relatively economical versus the high premium they previously commanded over sea freight. While air freight yields on most trade lanes are 2-3x their pre-pandemic levels, sea freight yields are 8-10x their 2019 levels in lanes like Asia to North America and Asia to Europe.

Sea freight schedule reliability has fallen sharply over the past 18 months driven by a spectrum of port, labor, and container availability issues. Shippers are increasingly frustrated by the large and growing number of “blank sailings,” the industry’s term for canceled departures.

To offer customers backup options – and increase their value capture – ocean freight carriers are starting to buy their own aircraft. Maersk announced its purchase of two Boeing 777Fs in November, while CMA CGM Group said in December that it would order four Airbus A350Fs to complement its existing fleet of five Airbus A330Fs.

As the COVID crisis extends into its third year, will air freight demand prove sustainable at today’s levels? To what extent will capacity increase to match?

Summary

- Sea freight capacity will remain tight for the foreseeable future.

- New-build freighter availability is limited at present.

- Today’s air freight demand spike is unlikely to last beyond mid-decade.

Forecast 2022: Airbus

Subscription Required

By Bjorn Fehrm

Introduction

January 3, 2022, © Leeham News: When the COVID-19 Pandemic started, it was tough to predict its impact on world air travel and how long the downturn would last.

![]() The aircraft OEMs are at the top of a supplier pyramid of hundreds of companies and millions of parts. The prediction of airliner output at the end of this chain is critical for all, but most for suppliers. The suppliers have strained their liquidity to expand the production at the demand of the OEM.

The aircraft OEMs are at the top of a supplier pyramid of hundreds of companies and millions of parts. The prediction of airliner output at the end of this chain is critical for all, but most for suppliers. The suppliers have strained their liquidity to expand the production at the demand of the OEM.

A downturn in deliveries means less money, which forces sensitive suppliers into a liquidity crisis. Brake moderately, and the suppliers can handle it. Brake hard, and they can’t, or brake a bit and then harder, and it’s as bad.

Airbus managed the reductions well, and with an intact supplier chain, 2022 will be about how hard to step on the throttle as the Pandemic isn’t done yet.

Summary

- With a competitive product range and an intact supplier base, 2021 is about the correct level of increase in deliveries, with the Pandemic a bigger worry than the main competition.

- With Airbus’ in perhaps its relative strongest position ever, how much this shifts the market is more a supply issue than anything else.

One A380 departure or two 777-200ER alternatively 787-9?

Subscription Required

By Bjorn Fehrm

Introduction

December 2, 2021, © Leeham News: With the last Airbus A380 rolling of the production line in days, we started looking at why the A380 didn’t sell last week. Now we check its economics for an airline that can fill it. We fly one A380 versus two departures of smaller aircraft on a typical trunk route.

Our analysis takes British Airways as an example and whether it shall use an A380 on Heathrow to LAX at peak traffic or rather two departures with its Boeing 777-200ER or 787-9.

Summary

- When you can fill the A380, it’s surprisingly competitive even against a more modern aircraft like the 787-9.

- This is when we focus on passengers and cost.

- We change the analysis angle next week when we add cargo and look at margins rather than cost.

Airbus sees encouraging signs of wide-body demand recovery

Subscription required

By Scott Hamilton

Oct. 25, 2021, © Leeham News: Airbus sees some “encouraging” signs wide-body demand is recovering from the global COVID-19 pandemic.

Christian Scherer. Source: Airbus.

Passenger demand is nearing-pre-pandemic levels in key areas of the world where single-aisle aircraft are used. Long-haul international demand remains suppressed, however. Some don’t forecast a return to normal for up to two more years. Others forecast a recovery on key routes next year.

Christian Scherer, the chief commercial officer for Airbus, is optimistic.

“I would say that on the wide-body market, you see encouraging signs,” he said during a press gaggle at the IATA AGM Oct. 3-5 in Boston. “Maybe that has to do with the fact that the ecosystem at large is realizing that the best thing they can do in the short- and medium-term, towards that whole global objective of sustainable air transportation is to equip themselves with the most fuel-efficient and therefore eco-friendly airplanes.

“I think that against that backdrop and the opening of more international corridors sees a regained interest on the wide-body side as well. Now it’s lagging the single arch really and there is no scoop here that rates in the long-range airplanes are going to change imminently, but the general sentiment is positive on the wide-bodies as well and that’s really good.”

Is the cargo capacity deciding the airliner variant? Part 3.

Subscription Required

By Bjorn Fehrm

Introduction

October 7, 2021, © Leeham News: In last week’s article, we could see today’s high cargo prices can motivate a 325 seat Airbus A350-900 even though the passenger load on the routes would point to a 240 seat A330-800.

How far does this “paying for a larger aircraft with belly cargo” paradigm go? Today we see if Airbus’ largest aircraft, the A350-1000, can generate the margins of the A350-900 on freight-rich routes. Can an airline that has an A350-900 sized passenger demand for such routes go to an A350-1000 instead?

Summary

- The increased yields for air cargo leads to surprising effects. Oversized passenger models can survive the passenger drought on today’s international routes as long as it’s a route with good freight demand.

Is cargo capacity deciding the airliner variant?

Subscription Required

By Bjorn Fehrm

Introduction

September 23, 2021, © Leeham News: In last week’s article, we put the question: Has the increased cargo pricing started to affect the choice of airliner variant?

We listed recent decisions between the Boeing 787-8 and -9 or Airbus A330-900 and A350-900 where the traffic levels post-pandemic would motivate the smaller variant, but the larger was retained or selected.

It makes you wonder whether the higher cargo capacity of the larger variant compensates for flying a larger cabin at a lower load factor? We make a cost and revenue analysis to find out.

Summary

- Cargo was an additional revenue stream on top of the main source, the passenger traffic.

- The lower traffic levels for international long-haul traffic and the increase in cargo pricing have changed this. Cargo is now as important in the decision of which aircraft to choose as the passenger capacity.

Boeing; 20-year aircraft demand back to pre-pandemic level

By Bjorn Fehrm

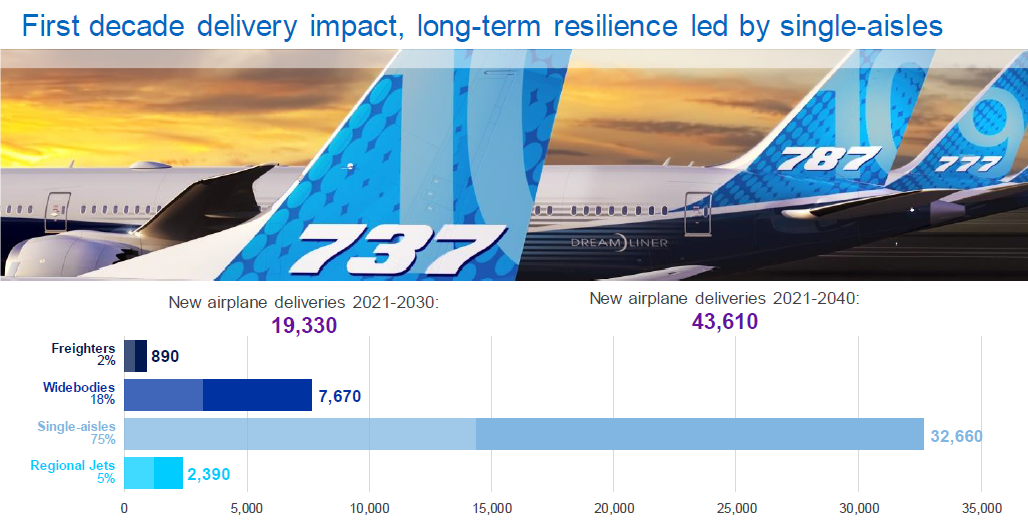

September 14, 2021, ©. Leeham News: Boeing released its yearly commercial aircraft demand forecast today. Over the next 20 years, the demand for single-aisle aircraft is past pre-covid levels at more than 32,000 aircraft, with widebodies down 8% compared to 2019 at 7,500 aircraft, Figure 1.

The forecast for freighters is up at 890 aircraft making a total of 43,600 aircraft until 2040, the level of the 20 years forecasts before the pandemic.

Figure 1. Boeing’s forecast of deliveries of commercial aircraft to 2030 and 2040. Source: Boeing 2021 CMO.

Global airline recovery: LNA’s view shifts from traffic to revenue, but our timeline hasn’t changed

Subscription Required

By Judson Rollins

Introduction

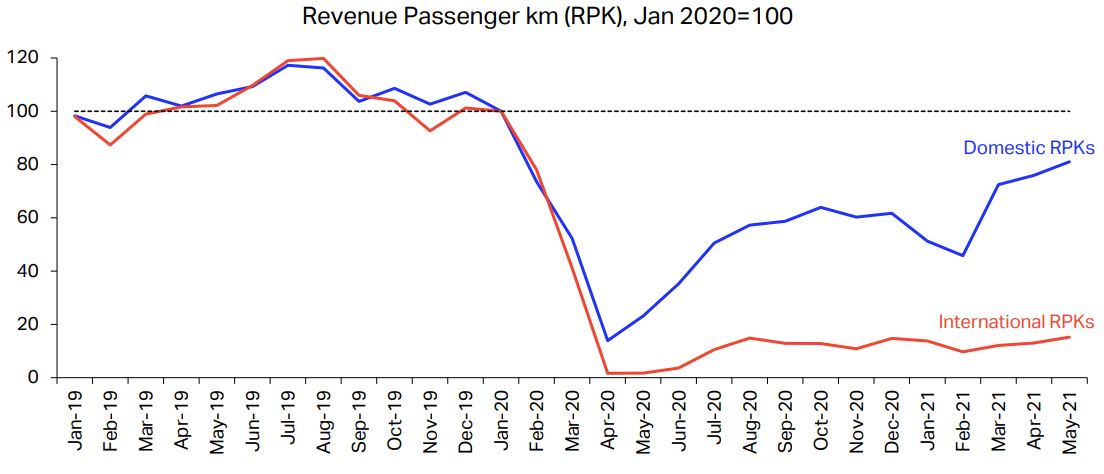

July 19, 2021, © Leeham News: A year ago last week, LNA published what might have seemed an apocalyptic call: global airline passenger traffic would not recover until 2024 at the earliest – and potentially not until 2028.

Early trends and forecast revisions by other parties point to the earlier half of our window. However, one major downside surprise has been an increasingly bifurcated world for airlines as demand returns at widely uneven rates by region and passenger segment.

Air travel is undergoing a “K-shaped recovery” like the global economy, with fairly obvious delineation between winners and losers. The upper leg of the “K” represents countries with large domestic markets, leisure travel, short-haul routes, and low-cost carriers.

The lower leg applies to developing countries, international traffic, business travel, long-haul routes, full-service airlines – and most airline suppliers.

Source: International Air Transport Association.

In hindsight, our prediction probably answered the wrong question, because the key driver of renewed profitability and future investment in commercial aviation isn’t the recovery of airline traffic, but revenue. The many changes to business and long-haul travel make revenue more difficult to forecast, but it will clearly be even slower to return than traffic.

Most industry forecasts don’t call for airline traffic to fully recover until 2024 or 2025, even if large domestic markets recover sooner. That means airline revenue – and profitability – will still be hampered until late this decade.

Summary

- Advanced and developed economies are on widely divergent economic trajectories.

- Global travel recovery statistics are distorted by a couple of large domestic markets.

- Vaccine rollout and documentation issues are likely to keep borders closed for longer.

- Revenue recovery matters more than volume, both to airlines and the aviation supply chain.

Pontifications: The reshaped commercial aviation sector

By Scott Hamilton

July 12, 2021, © Leeham News: With Washington State and the US open for business following nearly 18 months of COVID-pandemic shut-down, there is a lot of optimism in commercial aviation.

In the US, airline passenger traffic headcounts are matching or exceeding pre-pandemic TSA screening numbers. Airlines are placing orders with Airbus, Boeing and even Embraer in slowly increasing frequency.

The supply chain to these three OEMs looks forward to a return to previous production rates.

It’s great to see and even feel this optimism. But the recovery will nevertheless be a slow if steady incline.