Leeham News and Analysis

There's more to real news than a news release.

Asia-Pacific airline recovery held back by slow vaccination, border closures

Subscription Required

By Judson Rollins

Introduction

July 5, 2021, © Leeham News: The passenger air travel recovery from COVID-19 has been wildly uneven, even between neighboring countries. Most countries with large domestic markets have seen dramatic rebounds in passenger volumes, although yields have been held back by a continued slump in long-haul and business travel.

Aircraft parked at Hong Kong International Airport, with construction on a third runway in the background. Source: Bloomberg.

In the Asia-Pacific region, however, even short-haul international traffic has been disrupted by virus outbreaks, a painfully slow vaccine rollout, and a largely stagnant web of border closures.

Summary

- Much of Asia is well behind global average in the vaccine rollout.

- Domestic markets in China, Australia, and New Zealand are performing strongly.

- Border closures continue to cripple international travel.

- Many Asian countries are likely to stay closed well into 2022.

- Most Asian airlines are reporting slow progress toward capacity restoration.

Europe’s airline recovery: a tale of two continents

Subscription Required

By Judson Rollins

Introduction

June 24, 2021, © Leeham News: The recovery in passenger air travel from COVID-19 has been wildly uneven. A dramatic recovery in passenger volume – although not yield – in many domestic markets has been offset by a continuing sharp slump in international traffic.

The latter has proven particularly crippling to European airlines, most of which have miniscule domestic markets. Intra-EU travel, although generally permitted by member countries, has been slow to recover as business travelers have failed to return in meaningful numbers.

Meanwhile, long-haul travel remains hampered, most recently by an ever-changing landscape of “red zone,” “orange zone,” and “green zone” labels, plus other restrictions placed on arriving travelers.

The bright spot is strong leisure travel demand, which is propelling the continent’s low-cost carriers much closer to recovery than their legacy counterparts. This LCC-versus-legacy split brings into sharp relief the state of European airline traffic.

Source: European Centre for Disease Prevention and Control

Summary

- Vaccine rollout ahead of many developed markets; certificate program launching next week.

- Legacy carrier recovery is dragging out, weighed down by business and long-haul travel woes.

- LCCs performing relatively well, with some on track to fully recover next year.

- Train service unlikely to displace airline demand.

Cheap aluminum widebodies may finally enable long-haul LCC profitability

Subscription Required

By Judson Rollins

Introduction

June 10, 2021, © Leeham News: Residual values and lease rates have plummeted to record lows for previous-generation widebodies like the A330, 767, and 777. Inventories continue to build around the world, and prices appear set to fall even further.

At the same time, business travel ground to a near-halt in most regions. Even in countries where domestic leisure travel rebounded, like the US or China, average fares are down 20%-40%.

Southwest Airlines describes itself as a “low-fare carrier.” With business and premium-cabin traffic expected to take 3-4 years to return and be permanently impaired to some extent, every airline may be a low-fare carrier for years to come.

With higher-density seat configurations, more flexible scheduling – and, most importantly, the lower capital costs of used aircraft – new low-cost carriers (LCCs) could break even on long-haul routes with materially lower revenue than their predecessors.

This confluence of events has created a once-in-a-generation, perhaps once-in-a-lifetime, opportunity for new airlines to achieve a sustainable cost advantage over legacy carriers weighed down by capital-intensive aircraft, expensive crew contracts, and record-high debt service costs.

Summary

- Previous long-haul LCC startups failed due to insufficient capital, overextended operations, fares too low to cover costs.

- Ultra-low lease rates make used A330s cheaper to fly than new-technology aircraft.

- Lower costs, surgical route selection level the long-haul playing field.

- Legacy hub-and-spoke model will be weakened by “overflight” routes.

- Low capital costs mean used airplanes need only be flown when demand warrants.

Widebody availability set to surge; could new entrants take advantage?

Subscription Required

By Judson Rollins

Introduction

June 3, 2021, © Leeham News: Lessors are expected to write down the value of their widebodies as the long-haul travel slump appears set to extend well beyond this year, LNA reported last week.

A tidal wave of excess widebodies has reduced ownership costs to historic lows. Prices will only go lower as lessors finally initiate distressed-asset sales, and lease rates will continue to fall as used widebody inventory grows.

A confluence of factors, topped by the availability of lower-cost used widebodies, could increase the cost advantage of low-cost carriers over legacy competitors – at the same time reduced business travel and lower yields reduce the gap between legacy and LCC unit revenue.

Summary

- Widebody availability is set to increase steadily throughout the decade.

- What airplanes are likely to be most attractive?

- Sustainably lower costs could enable low-cost carriers to overcome a shrunken “revenue gap.”

Widebody write-downs are coming – how much will asset values be affected?

Subscription Required

By Judson Rollins

Introduction

Air New Zealand 777-300ER stored at Victorville, CA (USA). Source: New Zealand Herald.

May 27, 2021, © Leeham News: As central banks pumped liquidity into the global economy over the past 15 months, aviation has attracted a steady stream of investor interest.

However, aircraft transactions have been few and far between apart from growth in sale-leasebacks. An expected wave of lessor consolidation has been limited to one major transaction, the AerCap/GECAS merger announced in March. Even this was likely driven by GECAS parent General Electric’s push to dismantle its finance business, GE Capital.

Fly Leasing, a lessor with just 84 aircraft, sold itself to private equity firm Carlyle Aviation Partners in March. These have been the only lessor mergers or acquisitions to date, despite wide speculation the COVID pandemic would spur many lessors to combine.

A lack of merger activity is likely because aircraft leasing is not a business with large economies of scale.

Widebody aircraft values have fallen 30%-40% since the start of 2020, according to the UK appraiser Ishka. Relatively few of these aircraft have been written down on lessor balance sheets, but more are expected to be so toward the end of this year.

Summary

- Equity investors looking for high returns are finding disappointment so far.

- Asset write-downs are unlikely to have much impact on lessor viability – but could open the door to distressed sales.

- Could a glut of unused widebodies lead to a wave of new airlines?

Global airline recovery is patchy, driven by domestic traffic

Subscription Required

By Judson Rollins

Introduction

May 20, 2021, © Leeham News: Despite widespread hope, the global passenger travel recovery many expected in 2021 has proven elusive to date. Airline industry advocate International Air Transport Association (IATA) said that March global passenger traffic was still down more than two-thirds from 2019.

First-quarter airline earnings in most parts of the world have been lackluster or worse as borders remain closed and business travel continues to be deeply depressed, even within the few countries where vaccine rollouts have made the greatest progress. And jet fuel prices have rebounded to nearly where they were before the pandemic.

Aircraft parked in Alice Springs, Australia. Source: Bloomberg.

Traffic volumes are rapidly growing in the US and Chinese domestic markets, but US carriers are reporting average yields 20%-30% below pre-COVID levels. Chinese carriers don’t provide any visibility into their yields. Forward booking data from IATA shows the domestic-international divergence will only widen in the coming months.

Air cargo continues to cushion the fall in passenger revenue at many airlines, but to nowhere near the extent necessary to fully offset it.

Summary

- International travel continues to weigh on airline earnings globally.

- US carriers are optimistic about the strength of leisure recovery, less so on business.

- Asia and Australasia remain largely isolated due to strict border controls.

- EU internal borders are slowly reopening; vaccinated travelers likely to be admitted soon.

- Cargo provides a revenue offset to some regions, but not all.

2021 fleet trends: small jets get bigger, bigger jets get smaller – and the old makes way for the new

Subscription Required

By Judson Rollins

Introduction

May 13, 2021, © Leeham News: Aviation data provider Cirium said last week that just under 7,850 commercial aircraft were still in storage, down from 8,684 at the beginning of the year and a peak of 16,522 at the apex of the COVID-19 crisis last April.

Although there was an initial spike in aircraft retirements in March and April 2020, the total number has stayed in line with historical norms to date. However, order books for most types have stagnated or even gone backward since the start of the pandemic.

A few trends are becoming clear: larger single-aisles are thriving, larger twin-aisles are disappearing, and sub-100-seat orders are flatlining. Not surprisingly, older-generation aircraft are disappearing at an accelerated rate.

Summary

- Airlines are upgauging their single-aisle orders in anticipation of lower yields and competitive battles.

- Widebody order books continue to struggle; the bigger the airplane, the worse the demand.

- Regional jet and turboprop order backlogs have stagnated.

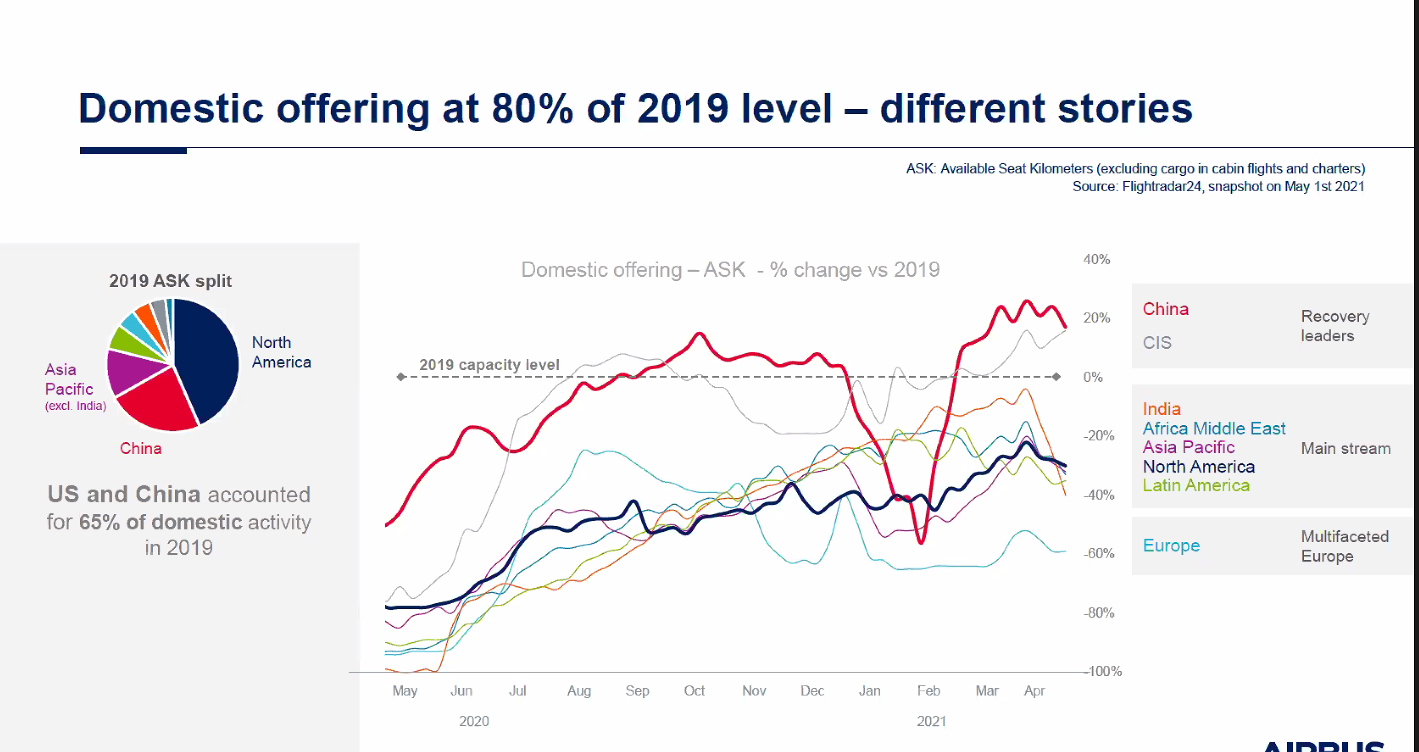

HOTR: Airbus’ view on recovery from COVID; why Southwest stayed with MAX 7

By the Leeham News staff

May 11, 2021, © Leeham News: Domestic traffic throughout the world is returning to 2019 levels, but at different rates, according to an Airbus analysis.

Robert Lange, Head of Business Analysis and Market Forecast, said today that the fragmented cross-border travel regulations and uneven vaccinations continue to inhibit passenger traffic recovery from the COVID-19 pandemic.

Pontifications: A330-300 could be great deal ahead

May 10, 2021, © Leeham News: The COVID-19 pandemic prompted airlines to ground more than 8,000 aircraft at the peak.

By Scott Hamilton

Among widebodies, no aircraft was hit harder than the Airbus A330ceo.

Traffic within China, the US and Asia recovers with narrowbody airplanes. European short- and medium-haul traffic is not recovering as quickly due to continued boarder closings. International traffic, for the same reason, remains awful.

But in chaos some see opportunities.

Jep Thornton, managing partner of the boutique lessor Aerolease, last week said the A330-300 could be a great trading opportunity.

At April 1, there were 267 -300s and 286 A330-200s (of all types) in storage, according to data reviewed by LNA.

China’s air travel “recovery:” volume improving, but revenue still elusive

Subscription Required

By Judson Rollins

Introduction

May 6, 2021, © Leeham News: In a media briefing this week, the International Air Transport Association (IATA) showed a deep contrast between the airline landscapes in the US and China versus the rest of the world.

The two countries together delivered 55% of the world’s domestic passenger traffic in March, with Chinese domestic capacity approaching 100% of pre-pandemic levels. China’s three largest carriers – Air China, China Eastern Airlines, and China Southern Airlines – are matching their US peers by deploying A350s and 787s on domestic routes, as most international routes to/from China remain closed.

However, first-quarter data continued to paint an ugly picture as unit revenue, or revenue per available seat-kilometer (RASK), was down at every publicly-traded carrier. Some of this was due to reduced load factors in January and February, but a key driver is the ongoing sale of “all you can fly” passes on most Chinese airlines.

Summary

- Domestic load factors have picked up, but international traffic near non-existent.

- First quarter financial reports show unit revenue fell below even last year’s abysmal levels.

- “Airpass” promotions continue, but it’s unclear how long they will go on.

- Fleet utilization during COVID: widebodies down but not out.