Leeham News and Analysis

There's more to real news than a news release.

Impact on Boeing’s China deliveries under Trump’s latest tariff tiff will be minimal

By Scott Hamilton

Oct. 23, 2025, © Leeham News: President Donald Trump ratcheted up the trade war with China when he announced on Oct. 12 that a 100% tariff would be levied on imports to the US.

This round was a retaliatory measure against China’s restrictions on exporting rare earth materials to the US and other countries. Rare earth materials are principally sourced from China and are critical to the aerospace industry, among others.

Trump said he also might block deliveries from Boeing to China’s airlines and lessors, as well as key parts, components, and engines. A large portion of China’s current fleet is Boeing aircraft. Blocking spare parts could eventually ground in-service Boeing airplanes due to parts shortages.

US-made engines and a variety of parts and systems for China’s C909 and C919 airliners are also sourced from the US. Airbus aircraft operated by China’s airlines may also have US parts and components that could be blocked if Trump takes this action.

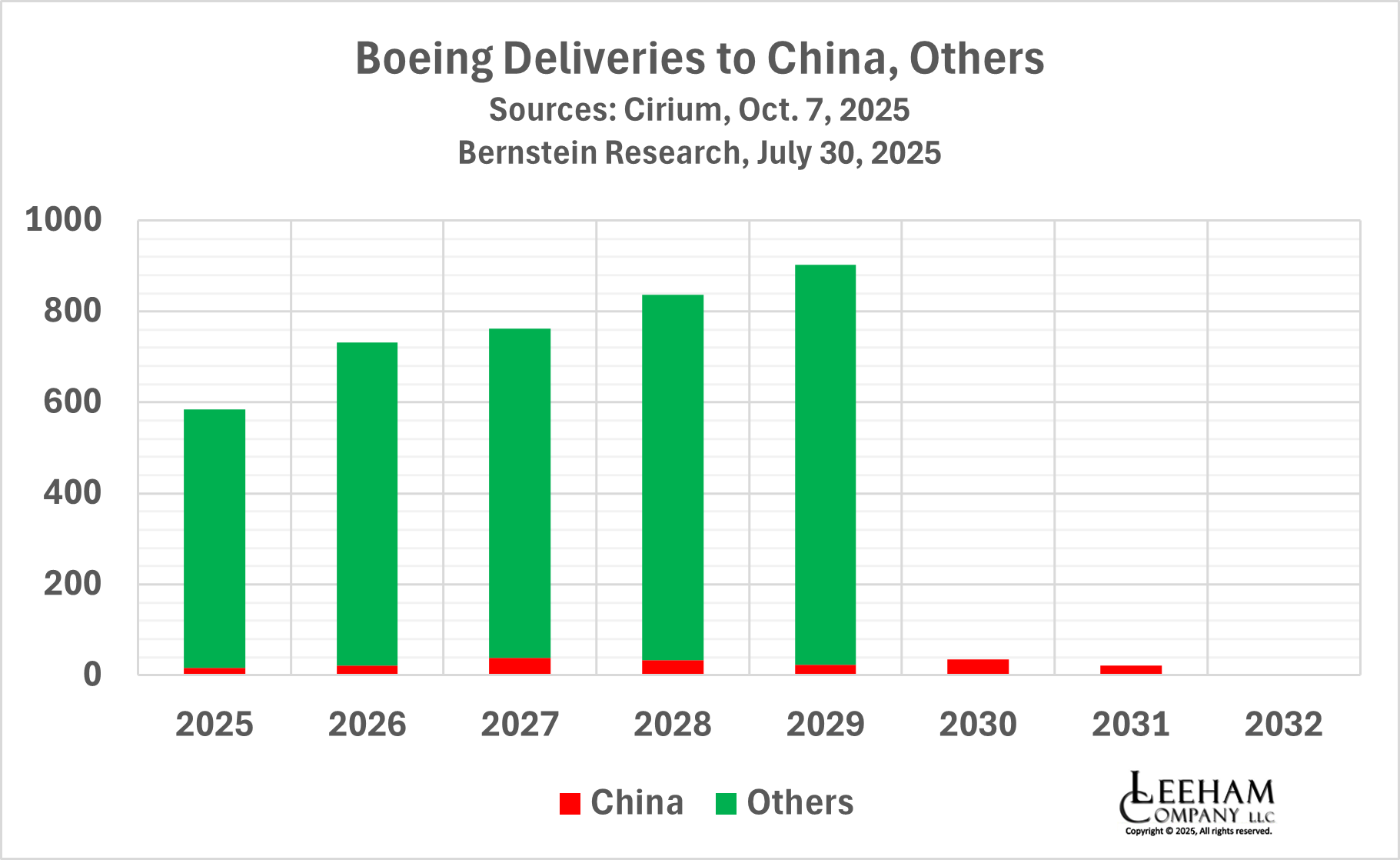

There was initial hand-wringing among some media that blocking deliveries would hurt Boeing. However, when Boeing’s delivery stream to China for the balance of Trump’s current term (which ends on Jan. 20, 2029) is examined, it’s clear that, while annoying, Boeing actually has few airplanes scheduled for delivery.

Deliveries to China represent between 3% and 5% of total deliveries through the balance of Trump’s term.

The China delivery data is from Cirium, as of Oct. 7. The total deliveries through 2029 are estimates from Bernstein Research.

Boeing deliveries to China represent a small single-digit percentage of total deliveries through the remainder of President Trump’s term. Credit: Leeham News.

China, Boeing appear near massive order: report

By Scott Hamilton

Aug. 21, 2025, © Leeham News: Boeing is nearing a massive order for up to 500 aircraft with China, Bloomberg reports. Completing the deal depends on political considerations, as so many of these do between China and the US for Boeing or Europe for Airbus airplanes.

Air China is the primary state airline of China. Boeing 737 MAX. Credit: CNBC.

But it’s significant that negotiations are active and appear nearing a deal if the politics can be worked out between the Chinese government and the Trump Administration. Boeing was frozen out by Beijing in 2017 when President Donald Trump, in his first term, began imposing tariffs on China in 2017.

President Biden, who took office in 2021, not only kept the Trump tariffs in place, economic and industrial sanctions were imposed when China covertly aligned itself with Russia following its 2022 invasion of Ukraine. When Trump was reelected in 2024, one of his first actions the following year was to impose more tariffs on China.

Even if the Boeing deal doesn’t successfully conclude soon, the very fact that serious negotiations and a near-deal validate LNA’s thesis since

Related Articles

- Here’s why China needs Boeing as much as Boeing needs China July 7, 2021

- China still needs Boeing as much as Boeing needs China July 11, 2022

- China still needs Boeing as much as Boeing needs China despite interminable limbo Oct. 31, 2022

- China banks on C919, but numbers say it still needs Boeing Sept. 2, 2024

LNA’s analysis over the years concluded that China’s home-grown COMAC C919 could not fill the gap for the domestic demand for new airliners in the coming years created with the 2019 21-month grounding of the Boeing 737 MAX. China was the first to ground the aircraft after two fatal crashes of the MAX five months apart in 2018 and 2019. It was the last to un-ground the MAX after the Federal Aviation Administration recertified the airplane in November 2021.

Boeing wants to remarket China’s airplanes. It’s costly and time consuming.

- China has 130 Boeing airplanes that are identified in the Boeing backlog. On last week’s earnings call, officials said China accounts for 10% of its backlog of 6,319 aircraft as of March 31. This means there are about 500 Chinese-destined aircraft in the “Unidentified” backlog.

- Reconfiguring airplanes would cost millions of dollars. Backlogs to order materials and complete the work could be as much as two years. Engineering that may be required and regulatory review also could take a year or two.

Subscription Required

By Scott Hamilton

Reconfiguring aircraft interiors is a costly and time-consuming challenge. Aftermarket company ATS is one of those engaged in this sector. It explains the process here. Credit: ATS.

April 28, 2025, © Leeham News: China used to be Boeing’s most important single collective customer. By the end of 2016, this country’s airlines and lessors accounted for between 25% and 33% of Boeing’s annual deliveries, depending on the year.

Boeing was losing ground to Airbus there. The European rival aggressively sought to partner with China. In 2008, the company opened an A320 family final assembly line in Tianjin. This followed a long courtship in which Airbus boosted its supply chain and engineering in China. Airbus establishing an A330 finishing center in China in 2017.

In China, doing business there meant providing “benefit” to its new and growing industries. “Benefit” was a loosely defined term that generally meant transferring technology, helping create a supply chain and ordering parts and components made in China. For some, it meant providing kickbacks. (This is not suggesting Airbus engaged in kickbacks, but corruption is a matter of public record. Such was suggested to me when I was doing business in China between 1989 and 1993.)

It had been a long struggle. When Airbus was establishing its presence there selling airplanes, some officials said they didn’t need any air buses—passengers boarded by jet bridges. Over time, Airbus began to surpass Boeing’s orders in China and today is the leader.

Boeing recognized it needed to do more in China. It floated the idea of establishing a 737 final assembly line in China, but its touch-labor union, the IAM 751 exercised its veto contract clause to stop the idea. Instead, Boeing opened a 737 completion center in China in 2018.

Completion centers paint the airplanes and install the interiors. A few 737s were at Boeing’s completion center when President Trump started the tariff war with China; the airplanes returned to the United States.

How good is the C919? Part 2.

Subscription required

By Bjorn Fehrm

March 27, 2025, © Leeham News: The COMAC C919 is finding its first customers outside China, which gives us reason to examine it and estimate how efficient it would be operating a typical mission compared to its Western competitors.

We will compare the C919ER version with a 3,000nm maximum range to “its look-a-like”, the A320neo, which served as the C919 design template.

Figure 1. The C919ER is analyzed using the Leeham Aircraft Performance and Cost Model (APCM). Source: Leeham Co.

Summary:

- The C919 consumes more fuel as the airframe is larger for the same seating capacity as the A320neo.

- Due to a lack of airframe maturity, the maintenance costs will also be higher.

- The big unknown will be the capital costs as the pricing or leasing strategy of a state-owned COMAC is hard to predict.

The back story to a Chinese lessor sale of 737 MAX orders

Subscription Required

By Scott Hamilton

Aug. 28, 2023, © Leeham News: The order in February by Air India for 190 737 MAXes involves a backstory involving China that until now hasn’t been told. A subsequent sale by a Chinese lessor of all 737 MAX orders to a Middle Eastern lessor further reduces Boeing’s exposure to China.![]()

The Air India was finalized at the June Paris Air Show. When Boeing announced its second quarter financial results the following month, the MAX inventory accumulated during the 21 month grounding of the type was reduced by 55 aircraft. These 55 MAXes were part of the inventory of 140 737s that were built for Chinese airlines and lessors.

Subsequently, the Chinese lessor CALC announced a deal to sell its entire MAX backlog of 54 to the Emirates lessor, DAE. Purchase rights to some 50 more MAXes were also transferred to DAE. This transaction left CALC with no 737s on its order books.

In its 2022 annual report, the most recent CALC financial statements available, the lessor wrote, “As at 31 December 2022, CALC had 226 aircraft on its orderbook, including 131 Airbus, 66 Boeing and 29 COMAC aircraft.”

UPDATED: Boeing posts quarterly loss; increases Commercial production rates

By Bryan Corliss

July 26, 2023, (c) Leeham News — The Boeing Co. on Wednesday reported a quarterly loss of $99 million, due in part to spending tied to production rate increases in its Commercial Airplanes division.

![]() Boeing said that rates on its 737 line in Renton are increasing to 38 a month. The 787 program has increased rates to four a month, with a plan to increase that to five a month by the end of this year.

Boeing said that rates on its 737 line in Renton are increasing to 38 a month. The 787 program has increased rates to four a month, with a plan to increase that to five a month by the end of this year.

Boeing is working with suppliers to get rates up to 50 a month on the 737 line sometime in 2025-26. CEO Dave Calhoun said during Wednesday earning call that demand is there for even higher rates.

“I’d love to get to 60 and the market is there for it,” he said. “The industry is short of airplanes by a relatively large margin.”

However, Boeing and its suppliers need to stabilize production at currently projected rates before considering going beyond what’s already been announced, the CEO said. “We’re going to work hard on stability.”

For this year, Boeing said it expects to deliver between 400 and 450 737s, along with 70 to 80 787s.

- Deliveries up at BCA

- China: Boeing hopes for delivery restart

- 777-X production to restart in 2023

- Calhoun ‘intent on proving’ trans-sonic truss

- BDS continues to struggle

Boeing, GE optimistic for return to normalcy with China

By Scott Hamilton

Larry Culp, CEO of GE Aerospace. Credit: GE.

June 20, 2023, © Leeham News: Relations between the US and China remained strained, beginning with the Trump Administration’s trade war initiated in 2017—which continues under the Biden Administration.

The strain has been exacerbated by China’s tilt toward Russia during the Russian-Ukraine war. Except for a brief meeting at this year’s G7 meeting between President Xi and President Biden, there has been little in the way of top-level diplomatic contact until this week. Secretary of State Antony Blinken met with Xi this week, leading to optimism by Boeing and GE Aerospace that relations between the US and China may be thawing.

During executive media briefings surrounding this week’s Paris Air Show, Boeing Commercial Airplanes CEO Stan Deal and GE Aerospace CEO Larry Culp gave their outlooks about the near-term future.

Embraer reports first-quarter losses but says production will increase

Subscription required

By Bryan Corliss

May 5, 2023 © Leeham News – Embraer on Thursday reported a loss in what typically is a slow quarter for the Brazilian jet-maker.

![]() However, executives talked up plans for production ramp-ups and ongoing sales campaigns as they pointed toward growth in future quarters.

However, executives talked up plans for production ramp-ups and ongoing sales campaigns as they pointed toward growth in future quarters.

“We are on track and we are going to get there,” CEO Francisco Gomes Neto said.

- Deliveries up year-over-year

- Supply chain ‘still challenging’

- 11 active campaigns involving 200 jets

MRO companies report double-digit growth in RBC survey

Subscription Required

By Bryan Corliss

April 12, 2023, © Leeham News: – MRO operators foresee double-digit growth in the rest of 2023 – as long as they can get the spare parts they need.

![]() That’s the finding from RBC Capital Market’s latest quarterly survey of commercial aerospace MRO companies.

That’s the finding from RBC Capital Market’s latest quarterly survey of commercial aerospace MRO companies.

“The outlook remains robust,” RBC analyst Ken Herbert wrote, in a report sent to clients this week. Based on the survey results, RBC projected overall MRO sales and parts purchases increased 18% in the first quarter, with the strongest growth in Asia and Europe.

Much of that was driven by the engine market, where demand is up 20%, he wrote.

However, “spare part availability and material lead times, followed by ongoing labor shortages, remain the key risks to the 2023 outlook,” Herbert wrote.

The survey gathered responses from about 40 global MRO companies, parts distributors and OEMs in early April.

- Engines powering confidence

- Six-month outlook ‘bullish’ for spare parts

- Supply chain, labor remain key risks

Pontifications: Airbus grows in China while Boeing remains on the sidelines

By Scott Hamilton

April 11, 2023, © Leeham News: Airbus last week firmed up an order for 150 A320neos and 10 A350-900s with China. The deal was announced last year.

Additionally, Airbus and the Chinese government agreed to add to the A320 family assembly site in Tianjin, increasing the capacity of the plant. This will be another step in Airbus’ goal to achieve a production rate of 75 per month by 2026 for the A320 family.

And that’s not all. Airbus and the China National Aviation Fuel Group (CNAF) signed a Memorandum of Understanding to increase the development of Sustainable Aviation Fuel.

Meanwhile, Boeing remains essentially frozen out of China. Deliveries of the 737 MAX remain stalled. Although China Southern Airlines outlined expected deliveries this year and through the next few years, we’ve seen this sort of thing before. Until an official announcement comes from Beijing authorizing deliveries, or some of the stored airplanes are delivered, words are just words.

That said, there are some solid indications we’re seeing that Boeing deliveries to China may well resume in the not-too-distant future, but on a glacial pace. The financial viability of some airlines within China, while opaque to outsiders, is monitored by the CAAC, China’s regulator. Some airlines are deemed too financially risky now to accept delivery of any new aircraft, whether the OEM is Boeing or Airbus.

While Boeing’s 140 MAXes originally ordered by China remained in a Twilight Zone of sorts, delivery of some Airbus A320neos also has been blocked. Generally, though, Airbus continues to tender airplanes and win orders while Boeing sits on the sidelines.