Leeham News and Analysis

There's more to real news than a news release.

UBS raises single-aisle production gap concern in lower oil price analysis

Dec. 17, 2014: There is a production gap for single-aisle Airbus and Boeing airplanes that could be exacerbated by the current dramatic drop in oil prices, writes the aerospace analyst for the investment bank UBS in a research note issued today.

Heretofore, focus has been on the production gaps for the Airbus A330ceo and the Boeing 777 Classic, with analyst consensus of those reports we have seen pointing to gaps they believe are insurmountable, and which will demand a rate cut.

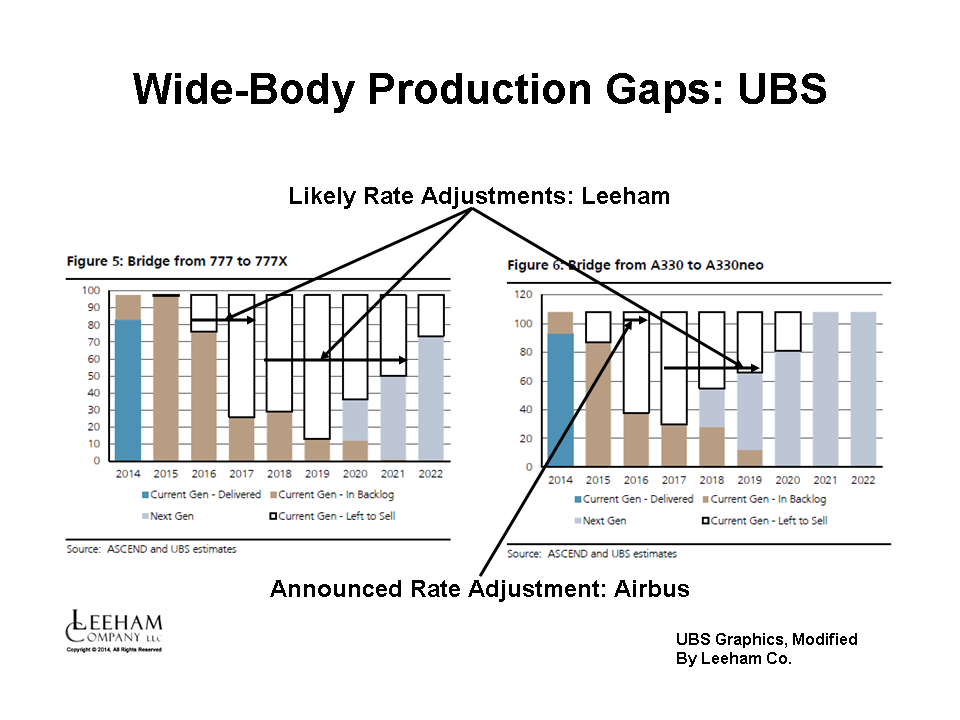

Figure 1. UBS Graphic, modified by Leeham Co. Airbus announced Rate 9 for the A330 and indicated a lower rate. Boeing hasn’t announced any rate reduction for the 777 but analysts suggest the lower rates illustrated (left). Click on image to enlarge.

Airbus has formally announced the rate on the A330 will decline from 10/mo to 9/mo in 4Q2015. At its Global Investors Forum last week, Airbus displayed a graphic that shows a further rate decline. Although officials did not place a number on the rate, our interview with an analyst present said Airbus later indicated a “floor” of 6/mo is anticipated.

Boeing continues to insist it will be able to maintain the current production rates of 8.3/mo for the 777 Classic to the introduction of the 777X in 2020, but analysts predict rate cuts to seven then five and perhaps even four by the time 2020 rolls around.

Figure 2. UBS Graphic, modified by Leeham Co. Click on image to enlarge.

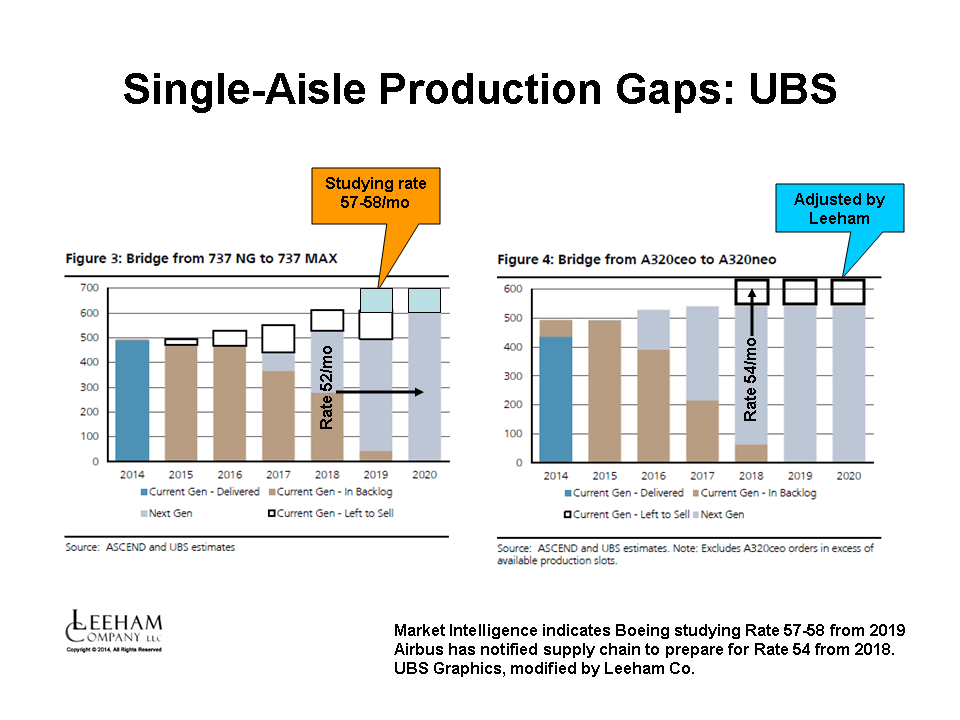

Airbus and Boeing are increasing production rates of the A320 and 737 families in advance of introduction of the neo and MAX, and Boeing further has announced a rate of 52/mo in 2018 (effective in June, according to our Market Intelligence). Boeing is also studying an even higher rate in 2019 of 57-58/mo. Airbus, as we have previously noted, told its supply chain to be prepared to go to rate 54 in 2018.

UBS raises concerns of a production gap for the single-aisle airplanes spurred perhaps by the lower oil prices. The low oil prices, currently $2/gal vs $4/gal a short time ago, means in-service, 10-year old airplanes retain economic viability longer than otherwise when capital costs and the difference in maintenance and other operating expenses are calculated and which offset each other. The UBS slides do not take into account the Rate 9 or 6 for the A330, nor the increased single-aisle rates for the A320 and 737 that our Market Intelligence indicates are coming. We’ve modified the UBS graphics accordingly. The lower rates will narrow the production gaps for the A330 and 777 but higher rates will increase them for the narrow-bodies.

UBS also notes that there is opportunity for carriers to buy late-model, used narrow-bodies to fill near-term capacity needs. We note that Delta Air Lines favors this approach and Southwest Airlines takes advantage of spot opportunities. UBS writes that Air Berlin will phase out 35 late model 737-800s and nine 737-700s. The former have an average age of just 4.8 years and the latter 6.2 years. Delta is already rumored to be a potential buyer of the -800s.

UBS thinks that if fuel prices remain low for 6-12 months, Airbus and Boeing could begin to see deferrals. We believe six months is not long enough, and we remain doubtful that even 12 months would prompt deferrals. But if UBS is correct, it sees Boeing at greater risk because it has a great set of production gaps not only for the 777 but also for the 737.

On the Airbus side, the hike to 54 is what causes this ‘gap’, which gives them the luxury problem of having to sell more neos in 2018 onwards.

Boeing meanwhile has an issue much earlier, just filling the NG slots 2015 through 2019. This is a much bigger problem, and not a luxury one. This is a clear result of Boeing’s policy, from the start of the MAX program, to allow customers to swap pre-existing NG orders to MAX.

This of course allowed them to show better volume on the MAX in the face of the NEO’s gigantic lead. But now we see the impact: production swings from low to high, with depressed cash flows and higher risks in production.

Airbus took a very different approach with the NEO. From the start of the program the policy was ‘no neos without ceos’. This seems to have relaxed a bit since the ceo production is sold out.

Which customers so far have switched to the MAX from the 737NG?

I have not seen much news about this.

In Spring 2011 we advised Airbus to introduce A321F CEO feeder dedicated airfreighters (we called them F21QR ceo) to absorb the CEO —> NEO phase-over production gap, estimating an immediate market requirement for this type to aroud 150 units. If listened to, the 2015-16 A321F or F21QR CEO buffer slots would have been about rightly timed. Airbus chewed upon the suggestion, but decided there wasn’t a problem … looks like they’re gonna bite their nails ?

As for the B737NG slots that need to be sold before the B737MAX takes over full production see: http://aeroturbopower.blogspot.de/2014/12/a320ceo-and-b737ng-backlogs.html

What’s changed?These b737’s were never going to be scrapped or parted out were they?either I’m missing something,or these city types are not as smart as I thought they were.rising interest rates are what they should be thinking about.

The Air Berlin continuous asset roll-over (degressive) financial depreciation model rendering an asset (financially) “obsolete” after 5-8 years in service is a source for trim condition perfectly serviceable aircraft … and Air Berlin are not alone. The general problem in Aviation is nobody wants to pay taxes !?

Looking at the graph it strikes me that possible development delays need a bit of thought.anything like 747-8,787,a350,c-series will be horrible in narrow bodies.a320neo seems to be clear.i find it hard to believe cfm are going be very late,and in any case Boeing have a bit more time ,not being first.A&B are going to have to think about this very hard when replacing current planes.

The more I look at this, the more it reads like UBS trying to highlight Boeing’s NG\MAX issue, without treading too much on Boeing toes.

For example: in the footnote to their chart for Airbus, they note that the chart does not include ceo orders where the level of orders is beyond the production rate. So basically they have not included all the Airbus backlog.

These gabs have been there before for Boeing. The idle 747 line before the 747-8 entered service. 6 yrs of 0 deliveries.

http://en.wikipedia.org/wiki/Boeing_747-8#Orders_and_deliveries

The 767 had 1 per month, for 7 years. Not so long ago.

Last week, stock traders were panicking when Airbus suggests production of A330s might, temporary, slip from record 10 to maybe 7. Stock fell 15% while Airbus announced one of its most successful years ever.

I don’t know. The market apparently wants to be fooled with good news only. Boeing knows and keeps quiet. UBS & Bernstein are careful not to mess up.. (e.g. silence on MAX’ 450 “Unidentified Customer(s), a bubble?).

Maybe some find gaps useful to clean up the factory, off load resources, such as expensive labor. Move the best/cheapest to new lines.

747 across all models data is here:

http://en.wikipedia.org/wiki/Boeing_747#Orders_and_deliveries

Thus for the 747 you get 1 year with zero deliveries.

… and the -8 today is about where the previous model was in production rate when it was discontinued 😉

i.e. the 747-8 development extended production by ~4 years.

1. Whatever the price of Fuel an airplane that uses 20% less of it is more economical than its competitor.

2. The cure for low prices is low prices. When the Frackers get squezed out of the market becuase of marginal returns (which is what the Saudis are trying to achieve by not reducing their output) the price will go back up.

3. The cure for high prices is high prices. When the price goes back up high enough the Frackers will come back in to the market.

My gut feeling is we are looking at two years of lower oil prices.

You have players in this like Ryanair who at least previously would sell a 737 when the warranty was up (5 years).

Lion Air has massive single aisle orders from both A and B as does Norwegian

and Indigo from Airbus (those are the ones that come to immediate mind).

So things change and where do all those go?

It will be interesting to see if the production increases go away.

As time passes, that only increases the risk that routine deferrals become conversions” into the 777X, said Richard Aboulafia, an analyst at Teal Group.

“Going head to head with the A350″ gives customers leverage,” he said. “Convert, or we defect.”

http://www.reuters.com/article/2014/12/19/boeing-air-france-klm-777-deferral-idUSL1N0U32D620141219