Leeham News and Analysis

There's more to real news than a news release.

Pontifications: There are numbers, and there are numbers

By Scott Hamilton

March 7, 2016, © Leeham Co.: The public relations battle between Airbus and Boeing was on full display at the annual conference last week of the International Society of Transport Aircraft Trading (ISTAT) in Phoenix (AZ).

As usual, the respective officials of the two companies used numbers to make the case that their airplanes sold more than the other guy.

A320neo vs 737 MAX

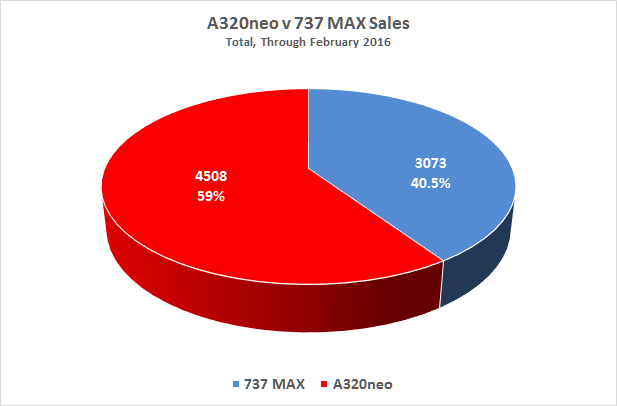

Figure 1. Sources: Airbus, Boeing, Ascend data base. Click on image to enlarge.

Airbus likes to point out that the A320neo has captured 60% of the market since the program was launched in December 2010. (Figure 1.) More precisely, the number is 59.5% through February 29.

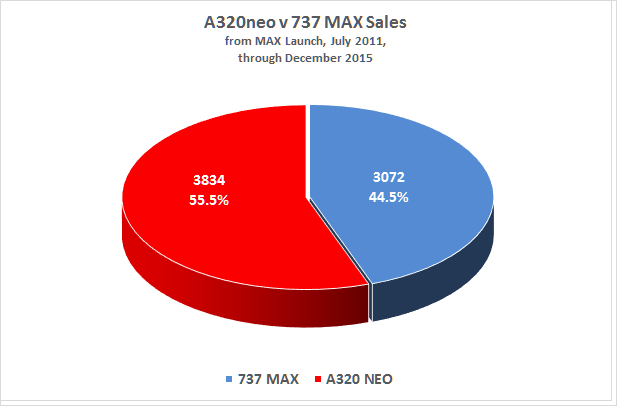

Boeing doesn’t like this number. Officials claims that since the launch of the 737 MAX in July 2011, with the large order from American Airlines, Boeing has captured 50% of the market.

The data simply doesn’t support Boeing’s claim. The data shows the MAX family has captured only 44.5% of the sales since program launch. (Figure 2.)

Figure 2. Sources: Airbus, Boeing, Ascend data base. Click on image to enlarge.

Boeing then falls back on comparing the 737-8 vs the A320neo, since program launch of the former, to make its case—and here, Boeing is correct. Narrowing the comparison to these sub-types only, the 737-8 captured 50.8% of the market. The sole sale, for 100 MAX 200s to Ryanair, is based on the 8 MAX and is included in this figure.

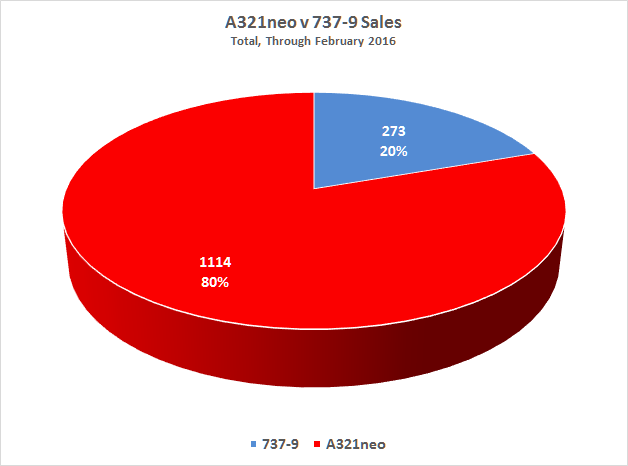

Then there is the 737-9. Boeing likes to ignore the sales comparison vs the A321neo, which is outselling the 9 MAX by a factor of 4:1 since the program launches. (Figure 3.) The A321neo has captured nearly 90% of the sales in each of the last two years.

Figure 3. Sources: Airbus, Boeing, Ascend data base. Click on image to enlarge.

“The heart of the market,” Boeing claims, is the 160 passenger sector filled by the 737-8, where Boeing wins since the MAX program launch.

777 v A350-1000

Boeing, however, isn’t shy about making such a lopsided comparison of the 777-300ER and 777-9 vs the A350-1000. Officials showed this chart at the recent ISTAT and Pacific Northwest Aerospace Alliance conferences:

Figure 4. Source: Boeing.

It’s a classic case of Boeing relying on one argument to make its case (the 777 v A350-1000) and ignoring the same argument when the data works in favor of Airbus.

There are numbers, and there are numbers.

FYI Fig 3 appears to be an erroneous duplicate of Fig 1, rather than the 737-9 data referred to in the text.

@Asad: Fixed.

Airbus sold 3300 A320NEO’s versus Boeing 2700 737-8s.

http://www.pdxlight.com/neomax.htm I’m just fine with anybody constructing statistics for his self concluding the 737-8 is doing better then the A320NEO. E.g. filtering out the 2011 spike.

http://www.pdxlight.com/neo3.png

Maybe adding up CEO/NEO and NG/MAX is better?

Same for the A350-777. Airbus sold 800 XWB’s and has most 777 operators in the pocket. That’s what matters. The 777X is selling slow & many years away.

Now, maybe the 787-10 / 777-300ER / 777-8 combination will beat the h.ll out of the XWB’s in the coming years. And maybe not.

http://i191.photobucket.com/albums/z160/keesje_pics/Boeing%20Airbus%20Widebody%20family%20keesje_zpsh0ffp31i.jpg

Keesje- do your comparison between the A350-1000 and the 777-300ER and you will find that the A350-1000 has been DOA for a number of years. There have been very small dents into the 777-300ER space. Don’t use the fleet life of the -300ER to claim the reason for the slow sales because there have been no major -1000 sales since BA. During that same period the slow selling 777-9X has cleaned the clock of the -1000 (300 to <200) right? People have often said it is driven by slots in production and the current A350-900 orders will be exchanged for A350-1000s, and I will say right because many of those 777-300ERs might upgauge to 777-9Xs. Now we hear Mr. Leahy discussing increasing the size of the A350-1000 to the 1100? ANother reason for the delay in sales because there is the potential of a new shinny object?

Your real problem is not with the 777/787 fight for the A350-900, the real fight is with the A330-900 which has outsold the A350 since its introduction. My belief that Airbus made a miscalculation with the A330NEO is continuing to be proven out by actual orders. Leahy seems to relish in the fact that the A330 is doing so well, but it's not at the expense of the 787. When you have airlines canceling A350 orders for A330NEO, share remains the same. And, if there are 500 low ball sales for the A330NEO, do you really think that those 500 sales are really going to impact the 787? Technology will win and the 787 already has over 400 deliveries. Airlines are using the 787 and it has established a beachhead. But has the A350 established that same beachhead? The A330NEO will impact that opportunity because by the time both programs reach the market the 787 will have 700-800 frames flying. It's nice to see the MH order but those orders are actual backfills for canceled orders and not actual new sales.

Are we seeing another Airbus widebody program looking for the right market niche? Were it not for the A330 program, all of the Airbus widebody programs will have performed less than. Sorry but there has been little of anything that has lived up to the hype of Mr. Leahy claims in the widebody world. Heck the 777-9X may catch the A380 for the VLA market leadership poosition while the internaly teams are looking at another NEO concept. Let's say the A380 is dead. A340 ,4 is better than 2, and what happened to the 340-600, 500? Dead. The A350 being killed by the A330, and in 10 years will we be reading that the program failed because of poor internal strategy? And then there's the, let's go to China and give them a widebody training approach through A330R sales. Leahy is selling to China to continue his share dominance, and the rest of the world will have much to thank him for over the long term. I know Boeing is going over shortly but in both cases that is the worst strategy the west has ever done. In the name of market growth we sell and give technology and innovation away with little real gain. 20 years from now when both companies are fighting to hold position we'll look back on these days and say, "thanks for helping to make the western world a third teer aerospace supplier." Pontificate on that Scott!!!!

” The A350 being killed by the A330, […]”

And I thought the horror-movie with the parallel-universe I watched at weekend was only fantasy. Now I recognize there’s more behind it than I could imagine 🙂

Back to reality: If anything, the A330neo will have a hard time in about 10 years. It’s only an interim solution IMO. No urgent need for Airbus to move in that size-class and a good way to catch some 787-sales, but the A330neo has only a comparatively small program life.

Historically it is rare for there ever to have been such a distinction between orders and deliveries. I believe that there is a real concern by the whole industry of severe contraction of the market going forward. When I say contraction I mean that orders for all OEMs will be cancelled due to the market fundamentals changing. The smallest of global change in terms of the cost of capital or borrowing costs is going to bring a halt to the order spree and swing airline management back to extending the lives of their fleets back to established norms (20-25 years).

With all those recently completed A320/b737/A330/b777 floating around and a low fuel paradigm we should be looking at a very different environment for all, couple that with a likely contraction in economic activity in Asia and the Middle East and the froth disappears very quickly.

The order backlogs will help for a while but 60+ for NB and 10+ for WB monthly production may start looking hubristic to say the least in a couple of years time. This is the biggest and most sustained boom in commercial aircraft ever and I don’t see it continuing forever.

I see the Boeing/ Airbus spats as almost faux competition at present with both having champions and also rans. It is not each other that should be their main concern, instead short/medium term economic and long-term environmental issues are the matters they should be focusing on. Why do we have the basic concept in short haul not changing in 50 years?? There are fundamentally more efficient and environmentally less damaging options that are readily available.

Typical Boeing [edited].

Typical [edited] tactics by Boeing, you would never find Airbus playing these kind of games with numbers.

You can’t be serious. Airbus always plays with numbers just like Boeing.

Announcing new sales six years down the road and compiling surrealistic backlogs all amount to meaningless dogfighting about theoretical market shares and really such leads nowhere except to exasperating us market observers … what makes sense is yearly aircraft deliveries, which we may predict forward based on announced or estimated ramp-up/down figures. What we see is that unless we have a bubble building up, Airbus is moving onto a sustainable 60+ NEO family deliveries/month whereas Boeing should think twice before incrementing the present pace, possibly the best move would instead be to begin slowing down the NG/MAX throughput pace somewhat, or else soon they will end up with having to manage a severe over-production. This is brutally the correct description of the respective narrow-body situations and trends, accounting for the fact that Boeing’s product is in all practical respects ‘obsolete’ (the MAX Series included) whereas Airbus’ range is not. Airlines are fully aware of this distinction and the behaviour of their Asset Strategists will integrate this fact. About Randy I’d say there isn’t a blinder man than he who does not want to see …

@FT

In terms of NB, the core market, yes Boeing must be at substantially greater short-term risk but just to see your direct competitor falter first is not really a reason to rejoice when you can see the market constrict around you if you are Airbus.

How solid are these order books?

while the market is quite big to accept both A & B products, there is no doubt that A succeed to grape most of the single aisle market but it is quite hard for B to accept the reality.

Just like the reality that the A350-900ULR is winning more and more costumers.

Due to Boeing’s small pitches the 777-X8 is 25 seats ahead and so not in the same class as the A350-900 . . .

So the 777-8X was counted for the “4X” advantage but the A350-900 not.

If Airbus launches an A350-8000 having a 319-plus (metric) tonnes MTOW, at Farnbourough, I’d not be surprised if they’d also choose to offer a 319-plus tonne ULR version of the A350-1000, as well.

777 10 abreast for 15 hours. I think the airlines will do a reality check.

Yes, I’d not be surprised if Emirates would choose to cancel their 35 777-8s on order — for this specific reason — and instead order a similar number of A350-1000ULRs (35), between 50 and 70 A350-8000s and a few A350-900LRs for immediate lift, as well. They would probably retain most of their 777-9s that’s on order, though.

I’m not so sure EK would cancel. I bet they got a deal and a half. Then many of the pax that will use these 777Xs are workers with no say on who they fly. I wouldn’t be surprised if EK got various A350 types for paying pax, who are starting to sit up and take notice when price differences for different economy seating is only equal to a day’s pay.

The Boeing graphic is a cunning one because it mixes the near term availability of the 777-300ER with the long term availability of the 777X and the A350-1000. I also like the way the gray band at the bottom of the chart makes the A350 sales look even smaller.

No doubt Airbus could come up with a similar (2x?) chart for the A330 and A350-900 versus the 787.

Having said that, there is a message for Airbus: there is a sizeable market for larger than A350-900 aircraft and Boeing are capturing about two thirds of it on a yearly basis. There is a case for an A350-8000 and/or improved engines on the A350-1000

AFAIK, Emirates is planning to take 15 777Xs per year from 2020 through 2029. As you indicate it’s pretty meaningless, therefore, to compare a large chunk of the 777X order book that are set for deliveries post 2025 with the entire A350-1000 order book – most of which will have been delivered long before 2025. A 319-plus (metric) tonnes MTOW version of the A350-1000 – together with an A350-8000 – would IMJ constitute a significant competitive threat to the 777X programme.

Many viewers / stock owners looking at this graph see 800 77x orders. .

Its cumulative.. in reality their are 300 77X on order.

Boeing again is aiming at perceptions. In my opinion they risk damaging long term Brand credibility with people that matter by communicating like this.

It’s interesting to listen to Randy — in the link below — when he’s being questioned by a colleague about the Boeing seat width “standard”, he starts to veer into non-relevant talking points such as how the curved ceiling improves “the feeling of spaciousness”, and items such as ambient lighting and expansive windows, storage bins, improved air quality etc. Apparently, 17-17,2 inch wide seats on ULR flights is not an issue — according to Randy & Co.

http://www.boeingblogs.com/randy/archives/2016/03/mail_bag.html

Hes a natural salesman, always push your features and advantages…storage bins…air quality…

I can see how a two hour flight is not pleasant but doable in a 17″ seat. Longer flights, I would look for an A330.

To be fair he did a salesman’s job but at the very end of the piece he effectively conceded the point. what exactly did you expect him to say?

I enjoy his interviews, soft though the questioning naturally is.

“There are three kinds of lies: lies, damned lies, and statistics.”

(attributed to Mark Twain).

I know Scott thinks I am wacky, but I do think the numbers are valid for a competitive 737MAX in the A320/737-800/8 segment if you lump the -8 and -9 together.

As Boeing clearly does not have an A321 competitor its that or add a third slot in an in- between category (Call it Cat II) and Boeing gets 100% of Cat II and Airbus gets 100% of CATIII.

CATIII having both much larger numbers and a ROI advantage is by far the better spot to be in.

Larger backlog overall also produces more buffer for Airbus to gracefully get through a slump than Boeing.

No matter how Boeing slew the numbers, its in a unenviable position in the Single Aisle market.

Airbus has all the options from a str4echted A320 to new wings and matching anything Boeing comes up with at much higher cost.

Boeing mistake was two 737 generations ago and not bringing in at least a modern airframe and skipping the current 700/800/900 generation completely.

@TransWorld: In sofar as Boeing views the 737-900ER/9 as a competitor to the A321, I’m not sure how you think you can overrule Boeing on a whim.

Scott:

I certainly cannot dictate to Boeing on something I consider more than a whim (it started that way in a jab at Keejse, but the more I thought about it the more ??? I though should be asked)

Your column questions Boeings stats, and has called them to task in a lot of other areas that are equally valid.

I am questioning Boeings statements in regards to where the 737-900/9 sits. The numbers compared to the A321 are so skewed out of bounds that it needs a fresh look to explain it.

Either Boeing is failing by Biblical proportions and the 737-900/9 is a piece of junk (which I do not think it is) or its a DIRECT competitor in Boeing mind only and is factually only the NEAREST competitor Boeing has.

Again, at what point do you break out a different category (or sub category) from the “direct or nearest competitor” ?

Logic of the numbers say the 737 -900/9 is not a direct competitor to the A321. The sales and production numbers are way outside of whack for that to be true.

Whether is an adjunct to the 737-800/8 or a separate category or sub category between the 737-800/8 and A321 is certainly an open item.

Sometimes the King really does not have cloths on.

Transworld,

it is hard to deny Boeing’s success with the 737NG, but maybe they were comfortable with where they stood for too long.

The NEO / 737-900ER/9 relative weakness was written on the wall undeniably, in 2006-2008 already.

http://www.airliners.net/aviation-forums/general_aviation/read.main/4907469/

http://www.airliners.net/aviation-forums/tech_ops/read.main/245698/

Some people will conclude the 787 debacle sucked all energy out of Boeing 2006-2010. Maybe they are right, or 51% right..

I think the energy was sucked out of Boeing before that as they demonstrably proved they were not interested in coming out with any new aircraft for a time.

When Mullaly pulled them in with the smoke and mirrors of outsourcing and production scattered all over the globe it made things worse (there is never a free lunch and I do think he was desperate and also underestimated the consequently by huge margins, in no way do I think he expected it to go so badly)

But with the timeline of the 800-900 series, they should have done something well before the 787 came to fruition and the 800-900 series should never have seen the light of day.

And not that its not a good aircraft, it just is boxed in future and that is showing up most severely in regards to the competition between the 737-900/9 and the A321.

Scott:

All over the Internet I see comparisons for the XWB and 777 or the XWB and the 787. Which of the two is correct and why? Thank you.

@Rotate: A350-900 competes with the 787-10 and 777-200LR/ER. A350-1000 competes with the 777-300ER and the 777-8. The prospective A350-1100 will compete with the 777-9.

The A350-800 competes with the 787-9, should it ever be built.

Here is a simple overview. I think some further changes in the wide body segment are not unlikely. I feel in between the 787-9 and 777-9X Boeing has a competitive gap.

http://i191.photobucket.com/albums/z160/keesje_pics/Airbus%20Boeing%20A350-8000%20keesje_zpseeyxrxez.jpg

@Keesje: The 777-8 is the same size as the A350-1000; yours is in the wrong place.

Hi Scott, maybe you are right, maybe not. The A350-1000 is 4 meters longer then the 777-8; 777-8 length: 69.5 m, A350-1000 length: 73.78 m.

Lets assume the 777 has 17 inch narrow 10 abreast in the back and the A350-1000 the wider 18 inch 9 abreast.

Looking at big twins like the 777-300ER, you can see almost all of them are 3-4 class. E.g. Cathay that ordered both the A350-1000 and 777-9, or BA, AA, ANA. Most of the cabin is used for First, Business and Economy Plus. In those classes there won’t be much difference between 777 and A350. (1-2-1, 2-2-2, 2-4-2.

http://www.seatguru.com/airlines/Cathay_Pacific_Airways/Cathay_Pacific_Airways_Boeing_777-300ER_A.php

In economy class 10 abreast versus 9 abreast makes a seatcount difference, but only for the 17, 18 rows seats in the cabin, adding as many seats.

Because the A350-1000 is 4 meters longer than the 777-8, it can theoretically more then compensate with ~4 rows /36 seats.

Cabin length works better then cabin width in 3-4 class configurations.