Leeham News and Analysis

There's more to real news than a news release.

Embraer adds range to E190/95 E2s

June 2, 2017, © Leeham Co.: Embraer today announced enhancements to its new E190-E2 and E195-E2 adding range to the 195 and improving hot-and-high and challenging airport performance for the 190.

John Slattery, president and CEO of Embraer Commercial Airplanes, revealed the improvements during its media days at its Melbourne (FL) facilities.

Adding range

The range for the E195-E2 adds 150nm, to a maximum range of 2,600nm. The E190-E2 gains 200nm from Denver and 100nm from London City Airport.

Slattery said that with 50% of the flight testing done, better aerodynamics than forecast proved the airplanes can go farther.

E2 vs CSeries

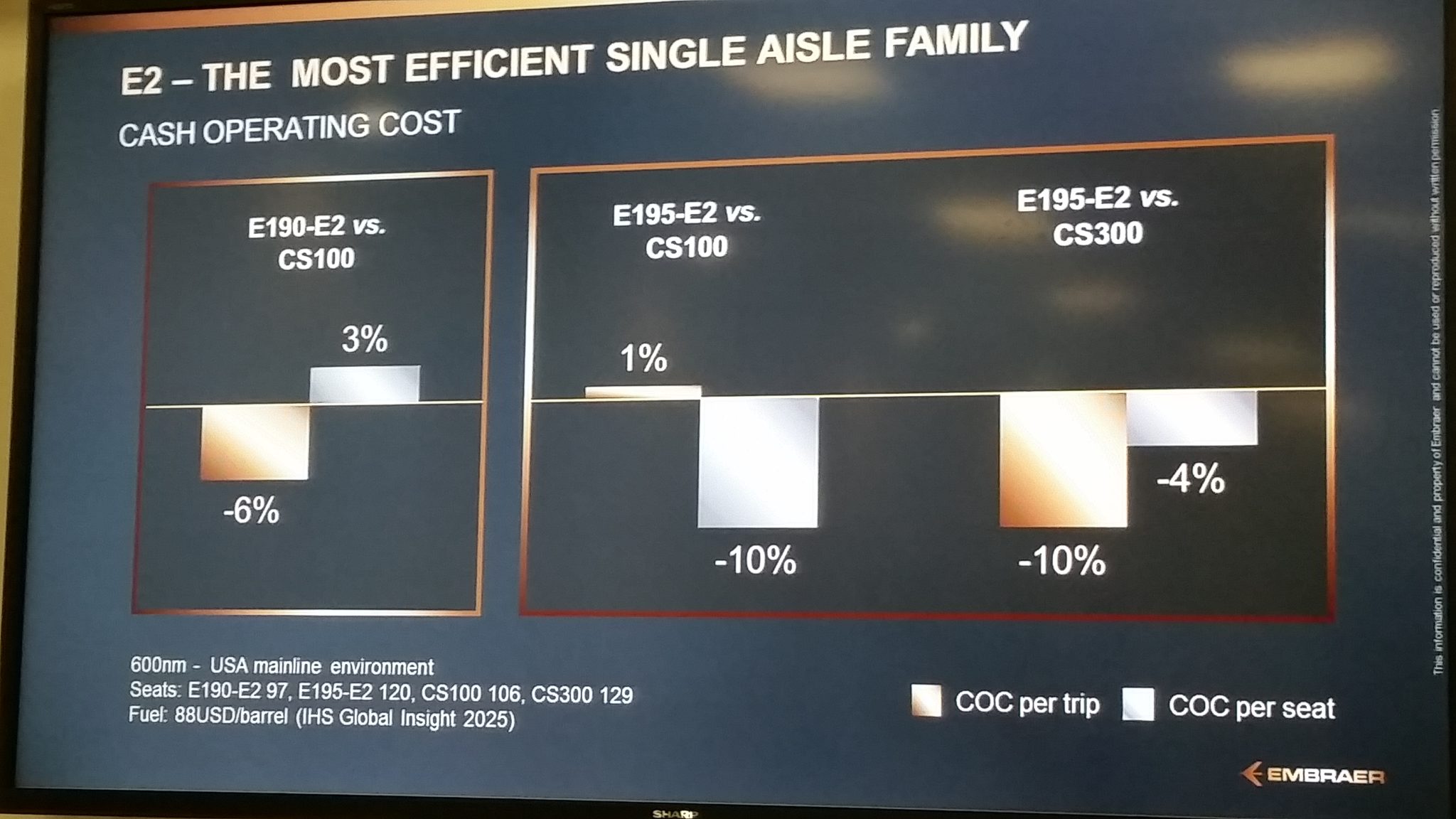

Slattery added the E2 is more efficient on a per-seat and per-trip basis than the larger Bombardier CSeries, with one caveat: the higher crew costs for the CSeries makes the difference.

Embraer’s analysis of its economics vs the Bombardier CSeries. Click on image to enlarge. Source: Embraer.

If the crew costs were equal, Slattery said the comparison would be flat.

Slattery ducked a question about his views about the Boeing complaint over alleged price dumping by Bombardier with an order last year by Delta Air Lines.

Slattery previously was critical of Bombardier’s pricing in a competition for United Airlines, in which Embraer competed with BBD and Boeing won.

“I’m going to be very careful about what I say,” Slattery said. “We are not interested in speaking about that campaign explicitly. Our position is, as an independent manufacturer, it’s just our positioning that fair and balanced commercial trade is the way to go.”

Brazil filed a complaint against Canada with the World Trade Organization over government investment in the CSeries. Boeing filed a complaint with the US government over price dumping and the government investment.

E2 vs 737-7, A319neo

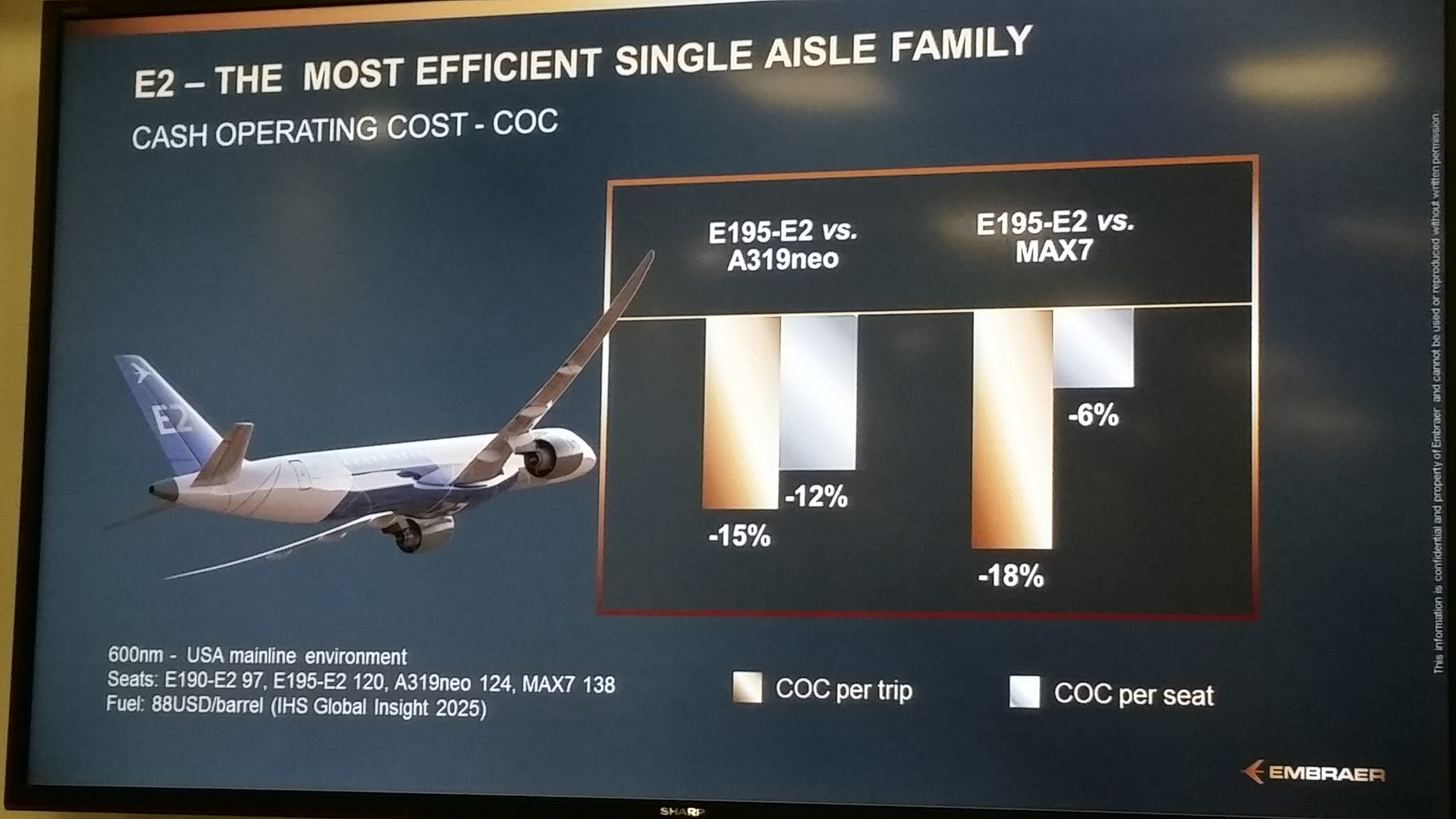

Likewise, Slattery compared the E2 with the Airbus A319neo and the Boeing 737-7 MAX, both larger than the E195-E2.

Embraer E195-E2 vs the Airbus A319neo and Boeing 737-7. Click on image to enlarge. Source: Embraer.

As would be expected, the E2 has better economics than the Airbus and Boeing airplanes, by a wide margin.

But as with the CSeries price dumping question, Slattery dodged a thinly-veiled second attempt at drawing him into the controversy when LNC pointed out that neither the A319neo nor the 737-7 have sold well and asked his view about the market viability of the two airplanes.

“Because of [the earlier question], I’m going to skate very carefully,” Slattery said. “I’m not going to go into that. All I would say is that we spend our time at Embraer trying to develop the best possible solution…. I believe that with the E2 platform, we will have good [market] penetration with incumbent operators and with new operators in North America.

“The economics speak for themselves,” he said.

Does Leeham buy Embraer’s claim of lower total and per seat operating costs? I would be inclined to suspect it is correct vs. the CS100 but have a harder time believing the E195-E2 can compete with the CS300.

We don’t buy any OEM’s claims on their operating costs. So far we have not found one that is not putting the presenting OEM in a good light.

This is the motivation behind our consultancy with our independent aircraft performance model, to be able to take all the OEM information and return a true apples to apples economical comparison.

Nice, Leeham was able to get a confession and go beyond the nice PowerPoint presentation and explain the real difference in cost between the CS100/300 and the E195 which is close to zero. Mr Slattery is validating in some way that the bigger CS100/300 is a good design, mtow,range and efficiency.

It would be very strange if the acquisition cost of the CS-100/300 was close to the EMB 195 since Bombardier invested in the project something like three times more, considering the use of wings made of composites and Al-Li fuselage. If the energy efficiency of the E-190/195 is similar to the CS-100/300, Bombardier will find itself in a delicate situation.

Ah, the canadian turkey would be truly “done”–take it out of the oven! LZoL

Most likely same cost per seat for a flight within the E-195E2 fully loaded range. The CS-100/300 take more pax further and then the numbers diverge as the E-195E2 need to offload pax as flight distance increase. Some Airlines will use both, the E-195E2 for cheaper shorter range hopping with fewer pax and the CS-100/-300 for longer range flights. The CS-300 will be a good base for a long range biz-jet as well.

@Caerthal:

“..would be very strange if the acquisition cost of the CS-100/300 was close to the EMB 195.”

Avg contract price for a significantly ‘de-rated’ CS1(But with options to reactivate/restore max capabilities @ extra cost anytime after delivery like in DL’s contract) is probably close to a 195E2 sold @ near its max capabilities.

On the other hand, no way the avg contract price for a CS3, even a de-rated one, would be close to a 195E2….

It would indeed be “very strange” to those unfamiliar with this industry in how the same aircraft type can be sold @ various contract prices due to different contracted capabilities specified…..sometimes even by the same customer. It’s not just about powerful customer driving a hard bargain to get ultra-low prices for airplanes….

“If the energy efficiency of the E-190/195 is similar to the CS-100/300, Bombardier will find itself in a delicate situation.”

I think you missed 3 key points there in your assertion:

1. “Energy” efficiency or total op cost efficiency?

When Slattery mentioned ‘E2 is more efficient’, he most likely referred to the total op cost per seat or per trip…not purely “energy”/fuel efficiency. If Slattery talked purely about fuel burn E2Jet vs CSeries, the crew cost factor would be irrelevant and he didn’t need to mention it as a caveat…but he did.

Total op cost is NOT just crew+fuel cost. Assuming Slattery referred to the CS3 vs 195E2 when he admitted total op cost for CSeries and E2Jet would be equal when their crew cost are the same, he’s indirectly implying CS3 has @ least slightly BETTER fuel burn than 195E2 because for example:

a) CS3 has significantly higher MTOW(about 11%) than 195E2 and most airports charge landing fee by MTOW.

b) Landing fee is part of total op cost.

c) If a CS3 spend more on landing fee, it must spend less on fuel than 195E2 in order to remain equal in terms of total op cost.

2. Despite 3x higher program investment, customers unwilling to pay more for CSeries because it returns the same fuel burn as the E2Jet?

If that’s the only econ justification/logic for R&D investment/fleet acquisition, no 787/330Neo would exist because Max9/321Neo would return slightly better fuel burn per seat.

Nominal max payload /range:

195E2 = 16.2t /2,600nm(Latest updated)

CS3= 18.7t /3,300nm (i.e. 15% heavier /35% further than 195E2)

Essentially, CS3 can do all missions(e.g. BOS->PHX) that can be done by 195E2 but not vice versa(e.g. BOS->SFO). Similar story CS1 vs 190E2.

3. Poorer RoI(Return on Investment) for CSeries than E2Jet program?

True if we focus only on today and ignore the followings in the past and for the future:

a) Unlike the CSeries, E2Jet is a derivative fm the 18yrs old E1Jet platform. Unless BBD goes bust and per typical industry practice, we can expect the CSeries platform to remain in production & contribute RoI long after the last EJet platform future derivative(E3?) is delivered and EMB already invested in the next cleansheet platform as replacement by that time.

b) E1Jet platform was once also an expensive clean-sheet design when development began in 1999. CSeries costs 3x more to invest than E2Jet but U’ve forgotten to account for how much EMB had already invested in E1Jet that makes today’s E2Jet possible.

c) E2Jet is based on a platform scaled for RJ ops such as 2-2 abreast cabin diameter but not really scaled for mainline ops. E.g., despite having maximum seat count far lower than 319Neo/Max7, the 195E2 fuselage is already much longer than a 320Neo/Max8 and approaching that of a Max9. I suspect the 195E2 is already close to or @ the ultimate fuselage length limit of the EJet platform. Any further stretch to raise seat count in order to dig deeper into mainline territory will likely run into rotation tail-strike issues not easy to resolve. This isn’t the case for the CSeries which was designed as a mainline platform fm day1 with relatively easy fuselage stretch opportunities build-in.

@FLX

De-rating the CSeries will reduce production costs on little or nothing. I know the pricing issue is complex, but ultimately the BBD should expect return on investment. BBD has made choices that make the marginal cost of producing CSeries much higher than competitors – that’s why government support is so critical;

Energy Efficiency: I cite this question precisely because the BBD presented this as a great advantage of its product, while the EMB response seems to challenge this premise;

EMB tends to present its comparison broadly (CASM and Trip Costs), obviously other non-fuel costs will be considered;

The family of E1 jets started its commercial operation in 2014, so they are 13 instead of 18 years. Its cost of development was USD 1 billion, which was considered to be a very low cost. Such an investment has already been amortized, since more than 1300 units have already been delivered;

There will be no capacity increase. The 195 E2 has the largest possible size. Already CSeries could have bigger versions, but in the meantime BBD will not be able to compete in a market big enough to justify the huge investment made.

Personally, I understand that BBD made serious mistakes already in the design of the aircraft. Too heavy and sophisticated for the regional segment and too small for the contemporary single-aisle market.

“Too small for contemporary single aisle market” ??

There are 150 B717’s still flying,

450 MD88/90s still flying.

60 A318s & 1450 A319s

180 F70/100s still flying

190 Bae 146s

All up thats 2500 or so planes covered by the Cseries market.

Please note the word “contemporary.” How much A-319 and 737-7 are being sold?

Just because those members are the orphans of their larger family members doesnt mean a new design that is optimised for that segment wont succeed.

What do you think will happen for those airlines passengers that currently have 100-150 seats- they catch the train?

Sure the top end will migrate to the larger planes but that will happen too for the 80-100 seaters.

Have you got any idea why the crew cost is higher for a C series?

Larger airplane.

@dukeofurl

BBD and EMB made distinct bets, but both believed that their products could complement larger single-aisle jets, breaking with a doctrine advocating an extreme fleet simplification (a la Southwest).

BBD would have an advantage in a context where oil would cost more than 100 USD / bpp and with extreme environmental pressure to control emissions, which would lead to stagnation in air traffic. But very few people working in the energy sector (like me) believe that oil will rise to a level well above 60 USD / bpp in the next 5 years.

I repeat, BBD’s best bet is to develop the CS-500. In the current position, the company is in a precarious position.