Leeham News and Analysis

There's more to real news than a news release.

Is Norwegian in trouble?

By Bjorn Fehrm

July 11, 2017, © Leeham Co.: In our review of Norwegian Air Shuttle (Norwegian) the 8 of February, we pointed out the company’s ambitious fleet expansion plans with a rather weak balance sheet. We followed up with a second article the 15th of February where we analyzed the risky fleet plans further.

Last week, the longtime Norwegian CFO, Frode Foss, departed. It sent shock waves through analysts and the stock tanked 8% in a day.

The departure of a CFO is many times the pre-warning of troubled times. Foss was with Norwegian for 15 years. It was not a planned departure and Foss has no successor. The post is run by the Investor Relations manager in the interim.

Norwegian’s trouble

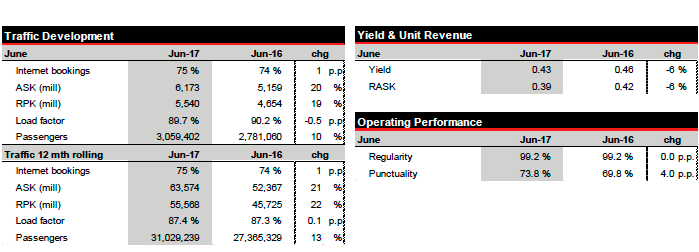

Analysts ask why Foss left. Norwegian’s assurance, that Foss wanted to do something else after 15 years with the company, appears unconvincing. Several speculate the June traffic data reveal (Figure 1) could be behind the departure. It’s not likely.

Figure 1. Norwegian June 2017 traffic data. Source: Norwegian.

Foss has been through ups and downs with Norwegian CEO, Bjorn Kjos, for 15 years. A dip in yields by 6% Year-on-Year would not trigger a CFO departure. There must be more behind.

What has deteriorated in recent months is the fleet expansion plan. Norwegian ordered 100 Boeing 737 MAXes and 100 Airbus A320neos in 2012. Of these, Norwegian has the need for the 737 MAX. The A320neos are leased out by the group’s leasing company to other airlines.

The problem is, the A320neos have the Pratt & Whitney GTF engine. Customers try to push out deliveries of these aircraft to mid-2018, when the engine will have its final fixes for today’s problems. Norwegian thus has six A320neo this year which are difficult to place, with a further 13 arriving next year (Figure 2).

Figure 2. Norwegians fleet expansion plans. Source: ATDB. For the interactive graph, with pop-up labels, press here!

To take delivery of GTF-based A320neos during 2017 is not a good idea for a lessor. When the engine runs trouble-free, the impressive fuel performance (clearly better than advertised) is what the market will remember. This is what a current operator tells us. But right now, the engine is a challenge to operations.

Therefore, it will be difficult to place Norwegian’s A320neos with reasonable lease rates for at least the next 12 months. Each A320neo that cannot be placed costs parking fees, and has no lease payments to cover the financial costs of the purchase.

Each aircraft which is not operating with a lease customer costs Norwegian ~$0.4m per month. With six aircraft scheduled for 2017 and 13 for 2018, the deficits on the leasing arm could quickly reach $20m-$30m, with no easy short-term fix. This compares to a yearly profit for Norwegian of $50m in the last 12 months.

The load on the company’s financial credibility comes when seven out of nine Boeing 787-9s for 2017 shall be financed, on top of six 737 MAXes and six A320neos (Figure 2). For a company in perceived difficulties, the capital costs rise quickly. Not what you want as a finance chief of an LCC, where margins are razor thin.

Foss’ departure

It’s easy to imagine Foss was against the risky 200-unit narrow body order from Boeing and Airbus. Events have shown the Airbus part (except for 30 A321LRs) was not needed. The perceived risk has happened and Foss, who is renowned for his careful financial planning, probably decided he’d had enough.

He didn’t feel like staying and sorting out the mess.

Was also wondering about airlines with very big orders/growth-plans such a SpiceJet, Lion, AirAsia etc?

Why would an LCC engage in the leasing business in the first place? Isn’t that a completely different business with very high financial requirements?

The CEO and founder, Bjorn Kjos, is on record saying that for the last several years, the profits made in the aviation industry are made by the lessors, and therefore I suppose he fancies morphing Norwegian into a lessor, basically. He is a rather astute risk-taker, obviously, considering Norwegian’s rapid expansion.

Well they can’t all transition to being lease companies, someone has to fly the things and carry passengers. If there’s too many lessors, the money will be with the airlines…

Agreed on the nutty orders by not just Norwegian but Air Asia, Lion, etc.

Boeing and Airbus taking those orders are equally to blame.

Can’t Norwegian seek compensation from Airbus or PW for the faulty engines?

Why did they take delivery of them in the first place?

Just read of more trouble for Indigo with the P&W’s.

See link.

http://c.newsnow.co.uk/A/893550256?-303:3665:3

I thought airlines were too eager when ordering A320’s with the GTF. A radical engine design with no proven track record, just empty promises from P&W. Buyer beware.

Radical ?

Better fuel consumption. And that is proving true. In a year’s time it will be sorted and the clients have many years of lower fuel consumption.

The wonder is that the testing did not show up the flaws.

It seems the transition from hand built to industrialization had more flaws than they though.

GE had that occur on the GenX. A new coating process on the shaft led to failures in (fortunately ) very short order.

You have to assume Pratt simply has not done this in so long they have lost the art of how to.

None of the problems are inherently fatal so the basic work is fine. Some details not so much.

It will be an amazing engine when it gets through the gestation.

Every engine these days has parts shared with partners, eg Avio did the gearbox, MTU does the high pressure compressor and the low pressure turbine. The risk is shared but so are the problems

Is the fuel burn between the PW and the new LEAP engine enough of a difference to warrant using it ?? There have been red flags going up on this engine for some time now …

In the long run, the difference is very much worth it. That’s why customers are not switching away en masse.

The principal behind the GTF is sound. You get better power efficiency (faster turbine) and better propulsive efficiency (slower fan), almost for free.

Not having a GTF and trying to achieve the same overall improvement with higher pressure ratios and higher temperatures is hard.

I suspect that there is nothing definitive yet in the public domain about which engine is going to be better, but despite the problems the PW GTF has some loyalty.

This: You can’t just turn around and change an engine type.

There are hundreds if not thousands line up ahead of you that get their first.

CFM is still ramping up to full output and regardless you can just crank out another 1000 or so.

The customers are stuck with what they ordered. They can change future orders.

The good news is none of the issue are more than small items and it will be good once they get them back fitted.

Spread this out among all costumers of the GTF, and you are you are talking about a lot of pain and a lot of cash. No doubt the thought of adding all this up has occurred to LN. Who pays? Historically these problems are quite normal, the ramp up isn’t.

Probably not going to happen, but this could create the sort of situation Delta’s C-suite folks love: an opportunistic moment!

They already operate the A320 (exNWA, some are being retired but most just got a significant refit), and have gone fairly big into the A321ceo. They have and can move up plenty of pilots and crews.

Delta could take the GTF on a ‘test drive’ by taking a dozen or 15 of them off Norwegian for maybe 5 years on easy terms, and see if they like them.

Wouldn’t hurt that it’d also be a poke on the nose to Boeing who are screwing around with DL’s C100 plans.

I will point out Delta suckered Boeing into a bid on the Twin aisle replacement and when was all said and done it was just a stalking horse.

Delta intended to take A330NEO and A350 all along, they brought Boeing in purely to drive the price down.

The Norwegian Q2 earnings slump does not seem to be in any way related to the A320NEO woes. Based on the 10th paragraph of the Reuters article, The 787 appears to be the culprit as it is noted that: “A larger share of leased aircraft in the fleet, and a larger share of 787 aircraft, lead to increased unit costs,” the company said, referring to its acquisition of more Boeing 787 Dreamliners.

http://www.reuters.com/article/norweg-air-shut-results-idUSL8N1K40HZ

I am no accountant, but it seems to me that would be an expected expense.

The A320 not so much.

I am not aware of the term “expected expense” in accountancy. Budgeted expense perhaps? Either way, Norwegian seems to be singling out the 787 as a prominent contributor to the loss and not so much the A320.

The real “fun” starts when Lion Air et al “craters”. Have they yet even issued recent CPA-audited numbers? BA and AB, check your order books from same! LOL

Norwegian Managmet is not in position

to manage this Order they are in fincial problems because they don’t send received Deposit back,

They don’t respecting Industry rules.