Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Ugly, fundamental changes coming for airline industry

By Scott Hamilton

May 4, 2020, © Leeham News: The global airline industry is on the cusp of a fundamental restructuring that will be painful, and painfully long.

A few airlines already ceased operations.

Several others are on the brink of filing for bankruptcy—among them Lufthansa and Virgin Atlantic, brand names that aren’t normally at the top of an endangered list.

A shake-out in Europe was already underway before the COVID-19 crisis erupted. The inevitable shake-out in Asia hadn’t yet begun.

Fleet rationalization among legacy carriers will occur at rapid-fire speed. And some carriers now have the opportunity to shed unprofitable routes that were maintained for market share.

It’s going to be an ugly process, though.

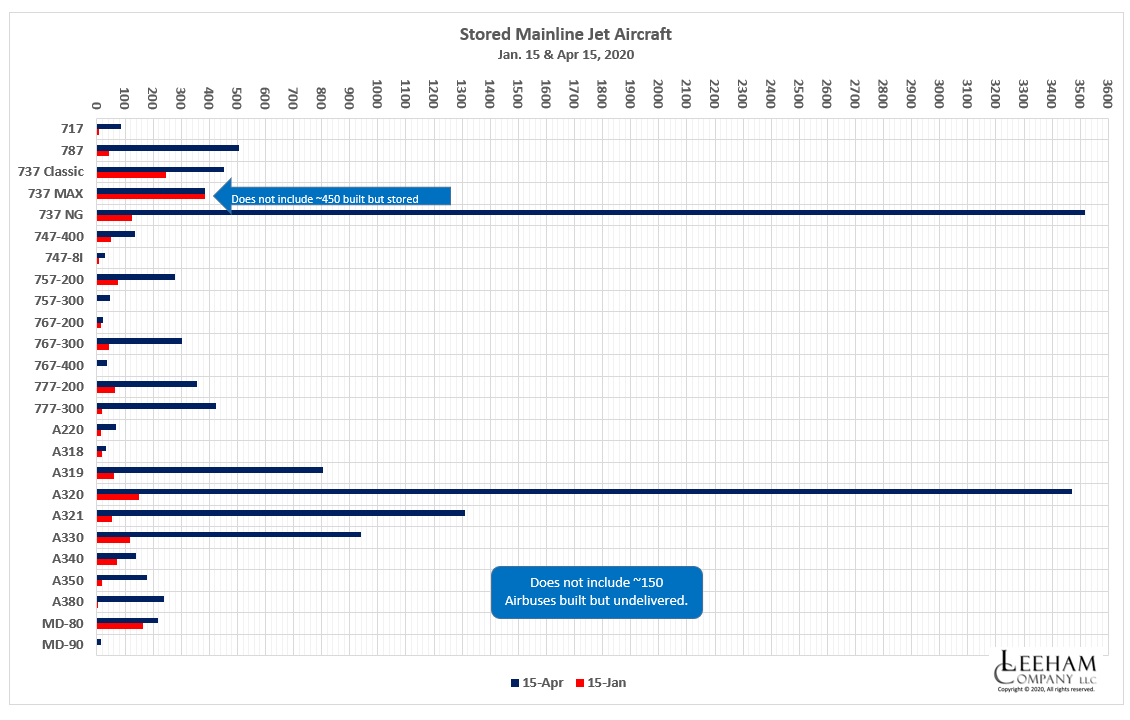

Parked aircraft

There are now more than 16,000 commercial passenger jets classified as stored. This includes nearly 11,000 single-aisle and more than 3,000 twin-aisle aircraft of all descriptions. More than 12,000 of these were parked since March 1, when COVID became a worldwide catastrophe. (About 2,000 aircraft returned to service since then, 35% to China.)

Figure 1.

These figures exclude the nearly 450 737 MAXes and nearly 150 Airbuses that were built but remain undelivered.

A few thousand of these aircraft probably won’t return to service. Aging Boeing 757s, 767s, 777-200s and 747-400s are down for the count. The same is true for Airbus A340s, the oldest A330s and even some A380s, the oldest of which are just 12 years of age.

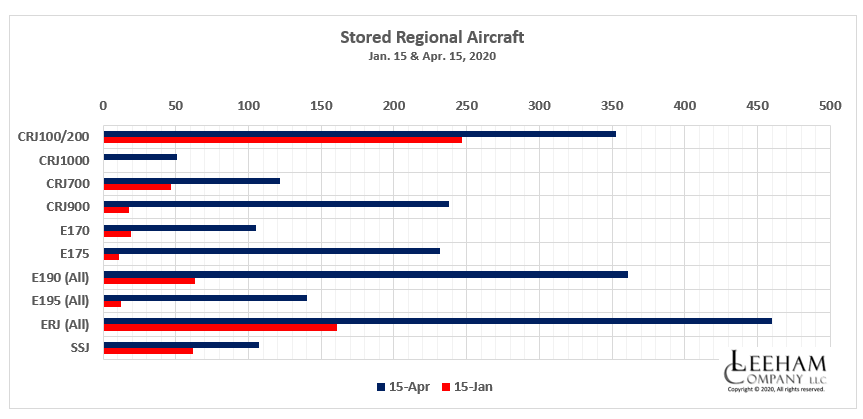

Older Airbus A320 (all) and 737 NGs are probably done. Bombardier CRJ 200s are gone, as are Embraer 145s and the smallest, oldest E1 Jets.

Figure 2.

With these retirements goes marginal routes across the globe.

No bonanza for Airbus and Boeing

These accelerated retirements won’t mean a bonanza of new orders for Airbus and Boeing. The down-sized route systems see to this.

But it could mean the fear of canceled and deferred orders may be mitigated. As airlines rebuild, they’ll take deliveries of airplanes on order.

And, in a counter-intuitive scenario, now that credit markets are reopening to the industry, taking delivery of new orders could be cash-positive for airlines

Many carriers will finance their planes instead of paying cash for them. Depending on a lot of factors, few of which can be identified with certainty today, financing might be over invoice price, resulting in a net cash gain.

Airlines (and lessors) typically pay 30% of the airplane’s cost before delivery. This is sunk money. Whether financing, or sale/leasbacks, are done over invoice cost, the transactions still means cash for the customer.

Regional Jets

In a podcast Friday organized by Aviation Week, Embraer Commercial Aviation CEO John Slattery suggested regional jets will be among the first to return to service. Demand initially will be thin, supporting smaller rather than larger aircraft, he said.

In a follow-up with LNA, Slattery amplified his comment.

“Seventy-six…enhance the product offering flown by the major airlines to insure stability for the major airlines and their work force (by having the right capacity that complements and contributes to the larger mainline aircraft in the systems),” he wrote LNA in an email.

American, Delta and United airlines are limited in the number of RJs that can be flown in proportion to mainline jets. Slattery isn’t suggesting there will be disproportionately more smaller jets as airlines resume service.

“Our view is that during this crisis, the airlines will not seek to add more regional aircraft units allowed under Scope (as happened post 9-11), but to work towards better optimization of the types of airplanes, currently available, that are flown by regional partners. Given the depth of this crisis, nothing can be off the table for majors to insure their immediate survival as well as creating a sustainable structure post CV-19. It is important that the airlines create greater flexibility in their toolkit and diversification of risk, to allow them to be position to react to events such as this pandemic. Quickly being able to have the right aircraft (capacity and customer experience) at the gate has never been more important.”

US carriers already were moving away from 50-seat RJs, as Figure 2 shows. Slattery believes another look is warranted.

“It makes sense to look at the older 50 seaters (and the fact that many of them are slated to exit as part of the fleet drawdowns announced) along with the need for a baseline regional aircraft that plays a crucial role in maintaining service to [smaller] markets. By allowing some small adjustments on weight to allow an E175-E1 sized aircraft (even if slightly less the 76 seats) to fill current 50 seater scope slots, airlines can maintain the correct capacity flex to meet the market demands. This doesn’t change the ratio of regional to mainline pilots.

“Absent any adjustments on utilizing existing aircraft slots, there are still ways for the airlines to use existing aircraft in fleet in different ways [C550] that will allow for new, in production, aircraft to be introduced in their place and solidify their product and market position.”

Embraer last year floated a concept of turning used E-170s into a 50-seast configuration. It gained no traction at the time.

But—a new threat?

While COVID should cull the weak carriers across the globe, the plethora of retired aircraft, most with long useful life left, and cheap oil may actually spur entrepreneurs to create new low cost and ultra-low cost airlines to compete with the legacy carriers that downsize.

In the US, David Neeleman planned Breeze Airlines, initially using used Embraer E190s and new Airbus A220-300s to serve small- and medium-sized cities across the country. Andrew Levy, formerly of Allegiant and United airlines, planned a new LCC/ULCC to be based in Houston (TX).

With American, Delta, United and even Southwest airlines planning smaller operations, will Breeze and Levy’s carriers have greater opportunities? Will similar concepts start-up in the US, Europe and even Asia? Used airplanes will be cheap and plentiful. And there will be plenty of out-of-work pilots, flight attendants, mechanics and others looking for jobs.

It’s something to think about.

I see airlines as commodity operations so, in general, tend to agree with the ‘new scenario’ sentiment and, in terms of supply timing, I can’t see there ever being a better or more likely time for new airlines. Basically, so much capacity has been shed that there are more or less fully formed airlines (pick your size, any size batch of matched aircraft and the teams of people already operating them etc.) ready to go, I’m guessing desperately wanting to go, all at short notice.

But, in the large markets:

China – I don’t now, but my guess is the CPC don’t want large new airlines

Japan – doesn’t seem ripe for large new airlines

Rest of Asia – already dominated by young airlines

Russia – Putin

Europe – EU wants short haul to be replaced by trains (being enforced in French bailout to Air France). Lots of legacies and national prestige but the relatively healthy Ryanair and Easyjet (and some smaller) are already there and ready to take over any short haul routes dropped but still available. No huge opportunities outside EU.

Latin America – Brazil already dominated by young airlines. No other particularly large markets or large legacy carriers.

Africa – too emerging to show a dramatic shift

North America – big enough, open enough, largey no rail alternative, so yes, possible.

I also suspect a factor in government bailouts is airlines wanting governments to have enough skin in the game that they choose to hinder new entrants to protect their investments.

I agree, there’s never been a better time to start a new airline but not until 2021 when a vaccine has been found for CV-19.

All of the current Airlines in the world are hurting badly and bleeding Money like never before. This time next year they will be even weaker that allows a new start-up to come in with a fresh balance sheet and no blood on its books to attack markets with limited resistance. Between now and next year, the restrictions on flights will drive prices up and Airlines will struggle to make them profitable which opens the door to new entrants.

RJ’s may be an interesting option in the current period (for a short period of time), but once the CV-19 restrictions are lifted its going to be a rush to get your hands on larger aircraft as soon as you possibly can to reduce costs and improve revenues.

In the end, 2020 will be a transition period, 2021 will be the year that defines new Airlines taking market share from traditional market players operating today.

We don’t know how travel rules will be as Covid-19 reduces in many countries, EASA is working on new rules due mid May for comments (testing requirements with vaccine-e-card and pax seating denisty in terminals and on-board I assume) to open up air traffic in the EU.

Lots of pent up demand and prices might climb pretty quick for available seats, like biz class pricing for available economy class seats.

There are women flying biz-jets to open countries like Sweden to go to hairdressers and party…

Claes: Where there are women there are men.

Yes, we seem to like them… Still will be interesting on the new procedures from EASA and how dense they will allow pax after passing quick-test in security.

It might be different procedures for families that can fill a row in one cabin section with removed rows fwd and aft and strangers that might have 2-4 empty seats between them and a zick zack seating pattern. Row n have seat A and F occupied and row n+1 seat C and D with the aile in between. Aircraft HEPA filters might need replacement with N95 filters if air recircualtion cannot be fullt shut down with all exhaust air getting dumped over borad making the Air Cycle Machines work a bit harder.

This also means a bright future for long range SA frames.

As they are a lot easier to fill than WB

dear Scott, you should not bury “aging 757” they might find a new life….

and 321LR are obviously on the sweet spot…

just another unrelated question: Following BOEING Q1 figures, shall we have -as usual- analyst comments?

usually, they come very quickly after Q1 publication!

these should be especially interresting now!

we should be able to sort the smart analysts and the clever guys from the bad…

757/767 and A321/A330’s if removed from pax service at depressed residual values should be popular for cargo conversion. The old 777-300 might also be picked up for cargo conversion as a combination of good cargo fares, cheap fuel, goverment money and lots of these airframes parked with owners short of cash is a perfect storm for cargo conversions.

At the moment BILD headline “Lufthansa Bankrupt” is more of a tantrum and extortion move.

https://www.austrianaviation.net/detail/darum-droht-spohr-mit-einer-insolvenz/

A definitive NO now will be an upcoming contigency in the near future. .. For any airline around that is more or less grounded.

The Covid crisis is so deep that it’s keeping alive some carriers that might otherwise have failed.

Right now, no lessor or financier wants their aircraft back, because there’s nowhere to put it. Norwegian is an example of a carrier that, because the rest of the industry is in crisis, is being given a heck of a lot more leeway than it would have gotten had it failed if the industry had been even remotely OK.

Secondly, the crisis is so deep that its given countries license to prop up their carriers. With the US throwing 10s of bns of dollars at the industry, and France the same, and apparently Germany too, who is going stop the Italians from rescuing Alitalia for the umpteenth time. A bunch of subscale, perennially failing national-virility symbols are going to survive this because their countries won’t let them fail. The ones that will fail will be private carriers without political cover.

So, yes, a bunch of capacity is about to leave the business, but nowhere near as much, or as fast, as probably we need it to, given the above tendencies.

Gordon Bethune was just on CNBC, and although he did not suggest this, the CNBC guys asked him if there was any possibility of Airline Travel being nationalized sometime in the near future. It would seem next to impossible for airlines to make money and carry passengers safely till there is an effective vaccine.

911 showed various restrictions can be implemented and air travel can thrive.. Its surprising how much of a ticket price in plenty of countries is for items other than the actual in air part of the flight.

Makes me wonder, if ticket prices are actually higher, or lower, than they usually are.

faith in an ‘effective vaccine’ coming any time soon, one year two years, seems to be widespread among those who should know better, as here

it is an assumption which is lazy when making any arguments about the future

even if anything approaching an effective vaccine is invented, it is possible/probable it will be seasonal only

better, when predicting the future, not to factor in a one stop shop solution ‘all these problems will go away once the miracle cure is here’

this is magic thinking a cargo cult pennies from heaven, money for Bill Gates only

The major media outlets love to champion any sort of effective vaccine, and do so without a hard look at history and facts. They know the viewer will glom onto these stories and not switch to another TV channel, myself included.,…

It’s amazing how militant pilot unions are, reality doesn’t seem to have sunk in. Some BA pilots are talking about industrial action! Scope rules have got to go, new entrants will probably break it anyway.

People Middle aged and upwards can’t safely fly until we at least understand exactly how covid19 is transmitted.

“t’s amazing how militant pilot unions are, ”

it is amazing how greedy and militant management has been in the past. “Home to roost” comes to mind.

‘we at least understand exactly how c19 etc’

it might be safer, pardon the pun, to say that it is entirely possible c19 is to be followed by c20 and this viral event is only just getting going, and that ‘exact understanding’ is not going to be possible for a good long while

the max crisis is hard enough to understand exactly, how many more times complex difficult and yes deadly is c19?

Yet exactly is already foreseen for the bug?

look at this bug thing structurally, after all this is what this website seeks to do for the industry

otherwise all predictions and arguments have failed because the main event is not being treated objectively

Me? If I could predict the future I would be rich.

All we really know is its going to be a long drug out mess.

Wide available testing is one key. We don’t have it. Maryland is guarding a shipment they got with the National Guard. What a mess.

Vaccine is the long term key and the rest is a patchwork that limps along to get to the we can really operate point.

We’re not flying until….1)vaccine and/or 2)someway, somehow we have antibodies against the corona virus. Its really as simple as that.

And antibody testing is challenging. If the test’s specificity is 95% (pretty typical) you could have up to 5% false positives. If you’re checking for 50%, 55% is not so much different, but if the actual positives are only 1%, you could see a test result of 6%, with the vast majority of them being fast positives.

Not really. A very small number of people are flying now and everyone accepted the much higher risk of catching the flu or DVT up until now.

For me to fly, I would have to be fairly sure covid19 isn’t transmitted by aerosol,I could manage the risk otherwise.

“”Airlines (and lessors) typically pay 30% of the airplane’s cost before delivery.””

If this is the deposit customers paid for MAX orders, up to 30% is much. If all MAX orders would be cancelled how could Boeing pay it back.

In Germany the Covid situation looks pretty good, in June it will be even better. I would fly now to a safe country same as Germany but there are not many. So it will take little bit longer till other countries get better too.

Antibody blood tests will be fast soon and more medical improvements won’t take long. I can’t believe that this crisis will be deep for a long time. Sure, we might wear masks on bord but if I need to fly I do it. In July the situation should be pretty good. If we only could reduce the amount of careless people.

Even if Germany is in good shape.

Even if a potential vacation country is in good shape.

Even if the airlines can manage the distancing.

Even if there are flights operating.

Will your destination country allow you in? Will you need to do a 14-day quarantine on your arrival there — or on your return to Germany?

At the moment I am not expecting any significant international flying until sometime late in 2020. And that may well change yet. This will be a massive hit on the airlines, and indeed the survival of the fittest (or survival of the most heavily subsidized).

The observation about raising cash by financing above invoice price is reminiscent of something that some state-owned Chinese airlines, among others, used to do years ago that was known as “equity stripping” among western financiers. In such cases, book value of course reflected the financed amount. However, some of those chickens have since come home to roost. Chinese airplanes tend to be disposed of earlier in their operating lives than those in many other countries (typically after about 20 years). For such over-financed airplanes, that can of course result in the market-based disposition price being well below book value, thus resulting in a book loss upon resale. Since those airplanes are state assets, this can invite PRC government scrutiny, especially in this subsequent era when possible corruption by government officials is a hot topic. The downside can be pretty steep for those involved, even though, as the old saying goes, “it seemed like a good idea at the time”.

Key is being able to run an airline.

Organizations tend to ossify, as WestJet appears to have (it also changed its market focus).

People’s Express made strategic errors, as did America Wes.t (With its 747 route, costly, didn’t understand international flying – did they ask PW executives who had experience with overseas operations? Many costs even as small as getting crews to a decent hotel economically – I was part of looking at that one time, one European country had very expensive taxis and no really good bus service (which needs to be quick, hence some airlines/airports in Canada-US had their own service for flight crews). Curfews increase impact of delays. ETC.

Back in the 70s there were only to profitable US majors – Northwurst and Delta. NW had frugal but smart thinking maintenance, and good flight ops. Delta had employees who’d give you stickers if you toured their shops, and management who didn’t bother with a capital budget: “we have money for great ideas.”, employees knew they had to justify their requests..