Leeham News and Analysis

There's more to real news than a news release.

Sizing up the 777X vs Airbus–and Boeing

It was no surprise that Boeing’s Board of Directors authorized the sales force to begin showing the 777X to customers for sale, as opposed to the concepts. As we’ve reported (and as did others), this move was expected this week. Entry-into-Service (EIS) is slated for late 2019, and will be driven in part by development of the GE9X engine.

The 777X replaces the 777-200LR and 777-300ER, with the 777-9X at nominally 406 passengers giving Boeing a monopoly position similar to that currently enjoyed by the -300ER. The 8X/8LX is 353 passengers.

.

The 777-9X falls just within the Very Large Airplane category of +400 passengers. We believe this will sound the death knell for the struggling 747-8I. The 747-8 nominally carries 467 passengers but Lufthansa, the only operator so far, configures the airplane for 362-386. The 777-9X will likely be far fewer than 406 in Lufthansa’s configuration but plane mile costs should be far superior to the 748. In high density configuration, the 9X will be solidly in VLA territory.

Update, 900am PDT: Boeing dropped five orders for the 747-8F from ailing lessor Dubai Aerospace. The 8F backlog is now down to 33, plus 26 for the 8I.

Looking at your chart, it seems Airbus abandoned the very long range market, as small as it is to Boeing (but the B-77L has out-sold the A-345). They also have no answer to the 400 seat market, and only the A-3510 in the 350 seat market.

FWIW, the A350-1000 sales have been picking up steam. I see Airbus possibly dropping the A358 in favour of the A350-1000.

Its not as if the A358 has racked up sales the past few years anyway.

I hate to pour cold water over everybody’s party but this sound too much like more 747-8i thinking to me.

777-8 will be too heavy to compete against the a350-1000, only works for 777-9 operators who need a small sub-fleet.

777-9 sounds good but what will Airbus do to reply? a350-1000 has been so heavily redesigned that some operators are calling it a different type, what are the odds Airbus could be planning a 400seat/7000mile stretch, which would be a lot cheaper per seat mile than the “9”?

777-8LX sounds great, a perfect a340-500/600 replacement, but, ah, remind me again, just how many a340-500/600s did Airbus sell now??

I think Boeing need to do a clean sheet 400-500 seat twin, the mythical a360, but I can’t see the current management parting with the development cost.

How can you know that, MartinA? Boeing has yet to publicly release any specs on the -8X, -8XL, or -9X.

Boeing won’t build the A-360. IIRC, Boeing still has not worked on the ‘mythical Y-3″. In fact, has anyone heard anything about the Boeing “Y-Series” airplanes in the last few years?

Boeing will still be handicapped by the weight of the legacy hull. From what we have heard about the cost of a new wing, engines, pylons etc I think the cost of project will be 70% of a clean sheet. Safer to go for the clean sheet if you can’t be sure that your updated plane will be better than the new one. A genuine VLA twin would have a better CASM than the a380-800, the market isn’t so big that Airbus would want to compete in the segment while the design would have at least 25 years production life. Another thing, cargo market is down and 50% of belly cargo space is unused, (airinsight) that takes the shine of one of the 777s biggest selling points. A new design could concentrate on passenger capacity over cargo.

A comparable seating arrangement to BA’s presented data for the 777-9x would be about 800 seats on A380 or thereabouts. ( A380 has twice the floor area of the 777-300 ).

Max seating on the A-380 is about 850.

Didn’t a B-742 (El-Al) once take off with 1087 pax, and land with 1090 pax (3 babies born during the flight)? I believe that is still the passenger count record for a commercial airliner.

I think in the end there will only be a 777-9. As for the A350, Boeing can gain a few points in efficiency with the larger wingspan, which is what makes the project viable. The GE engines can add a few points, if they outperform what RR delivers on the A350-1000.

AIRBUS A350 JET ENGINE DILLEMA

Airbus has one “Jonah Airplane and it’s called the A380″. The next Airbus-Jonah will be the A350-800, A350-900 and A350-1000 that is hobbled by the underpowered RR XWB jet engine. The A350-800 and A350-900 is a regional jet incapable of matching the distance of the 787-8, 787-9 and the 787-10. Airbus promised Qatar’s Akbar Al Baker that all A350 models would have 100,000 pounds of thrust and it did not happen. Airbus got Qatar and Emirates to settle for 72,000LBS of thrust which made the A350-800 and A350-900 a regional jet that cannot make long distance routes. Airbus A350-1000 is suppose have 97,000LBS of thrust which will still leaves the plane underpowered. Rolls Royce is using the same triple spool Trent 900 engine the exploded on the Qantas flight for the A350. To this day the over 25 A380 flights had to land at the nearest airport and recently on a Sydney Flight an A380 with a Trent 900 exploded and had a fire and was forced to return to Sydney.

The A350 is supposed to be a state of the art airplane however Airbus never orders a new engine when they build a new plane and here is the A350 with an old triple spool engine design stretched beyond it abilities. Airbus has a big problem and when Boeing builds new plane it orders a new engine. When Boeing built the 777 they spent a fortune and had GE build the GE90-115B however this time Boeing and GE had an exclusivity contract for the Boeing-777. Airbus got its start by buying jet engines that Boeing paid to develop and build.

Airbus sent some engineers and executive to GE to talk about buying the G-90 for the A350. GE said no to Airbus and than Airbus asked GE to build them an all new engine just for Airbus. GE said, ‘Why we want to compete with ourselves?” GE is loyal to Boeing and this time Airbus did not get G90-115B or the new GE-9x. Airbus had no choice but to return to Rolls Royce and ask what can do for us? Rolls Royce said we will stretch the Trent 900 and call it the RR XWB engine which is just a redo on an outdated triple spool engine.

What did Boeing do? They called GE and asked them to take the GE G90 to the next level and there building GE-9X with 104,000LBS of thrust. Airbus is not a great company and they have copied Boeing designs for far to long. So the A350-1000 has a bigger problem with an underpowered engine that has not been built yet. The A350-1000 cannot be stretched because it will be underpowered at 97,000LBS of thrust. Airbus’s biggest problem is that Europe lack the Industrial Might to build large jet engines for large jet planes. Even Pratt Whitney said no to Airbus because Americans dislike how Airbus conducts business with heavy subsidized aircraft they dump plane at unfair prices. Airbus needs to play fair or else they will have a problem since 75% of their planes use US built jet engines.

This is why I will never fly on Airbus,

Helga Schmidlap,

It seems to me that your comments are best suited to the likes of YouTube, rather than a serious forum. But wait…..silly me!

We believe this will sound the death knell for the struggling 747-8I.

A380 sales haven’t exactly set the world on fire either, and the 777-9X and A350-1000 will further depress orders.

Boeing apparently has a lot of money to waste so it can design these niche planes like 753, 764er and 778lx that have no future. The whole ULH travel is a dead concept. The cost is too high and the torture of long flights for Y-pax too.

A380 will be just fine. 779 or A3510 is a class and half smaller and the superjumbo will get a stretch and new engines to keep it well ahead in economics.

Interestingly little has been said regarding the recent BA-IAG order for the A350-1000 varient, this order gave Boeing a real bloody nose.

Unusually BA’s decision is not a cautious as one has some to expect & is a real departure from the softly softly appoach to fleet aquisition.

BA-IAG exposure to finer details of the proposed 777X would have been quite detailed, which begs the question what convinced BA to switch long standing loyalties with the imminent 777X launch, something we don’t currently know that the A350-1000 offers that we don’t…

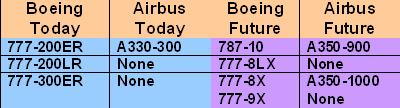

Boeing Today: 777-200ER, 777-200LR, Airbus Today: A330-300.

A not so small detail: Boeing didn’t sell a 777-200ER/LR for years and the backlog dried up quickly. Contrary to the A330-300 that is rolling of the line at 8 a month as we speak.

At this moment there are just 3x 777-200ER and 4x LRs remaining in the backlog and a 787-10/777-8 yet to be launched, EIS not before another 6-7 years.

Meanwhile the A350-900 and -1000 will be entering service in 2-4 years.

Can you see the pain? Boeing is in terms of delivering absent in the 270-330 seat sweetspot of the long haul market since 3-4 years. Reminds me of the A332s in the previous decade. No competition because the 767-400ER was done and the 787 still far away.

Product planing could be better IMO. I think Boeing won’t get away with an easy 787 stretch into the 787-10. They probably will be forced to beef up the 787-10 payload-range; MTOW, wing, engine and MLG. While not hurting the 777-8X..

IMO the table on top suggest something that proves something else when you dig up the numbers behind it.

Re.Tom Bucceri “We believe this will sound the death knell for the struggling

747-8I.”

That’s the av. understatement of all times! The 747-8 is ” a dog’ and should

NEVER have been launched, because it was Boeing’s futile and far to late

an attempt, to come up with an answer to the A380!

Boeing CEO Phil Condit told me as late as Nov.1999,”I will give you my

personal guarantees that Airbus will NEVER launch the A3XX,” after I urged

him to at least assume that Airbus WOULD come up with a more modern

replacement for the 747, to cover the big-airplane market for the next 40-50

years of this century and steel “OUR MARKET away from us!

Airbus launched the A380 in Jan. 2001, two months later and has sold 300+

units so far, the equivalent of about 500 747’s, appr. the same number of

747s sold in the same time period after launch and will remain unchallenged

for decades, just like the 747 was, due to inflation of the development costs!

Rudy, forgive me but you appear to be repeating yourself.

Hey Rudy, give it a rest with the name why don’t you? Enable cookies or get a WordPress account if you feel so strongly about it. You are actually writing more than you otherwise would have.

Rudy it has been my observation too that It seems sometimes like Boeing senior management refuses to read what’s on the wall.

E.g. that airlines wouldn’t wait for the NSA, that the 787-3 was way to heavy for anything, the 747-8i is a 400 seater in apple to apple comparisons, that if the 773ER is 350 seats, the 9i really is ~377 seats not 407, that airlines like JAL and UA do understand and like the A350-1000 specs, the A321 GTF NEO is a real threat, the 787-9 won’t fly in august, etc, etc.

I understand your VLA frustration, having Boeing blood, to see you correctly predicted, warned, were ignored for stupid reasons and see your collegaes hit the wall. Wondering what more you could have done, Been there.. If Boeing had launched the 747-500/600 with GP7000s the situation would have been different.

http://www.flightglobal.com/news/articles/gepw-work-out-details-of-747-x-joint-venture-plan-11869/

keesje,

How about by the end of September. After all, Boeing did say August/September time frame for 787-9 first flight. I think they can do it, based upon the apparent current stability of the 787 production system. I guess we will see. The parts should start arriving at the Everett FAL any day now.

“Not seeing the writing on the wall”

There is more to it. With a historically strong professional background _you can_ to some part influence those other projects This is called FUD, fear uncertainty and doubt.

This doesn’t work so well when your perceived competence sinks in unison with your marketshare.

One more reason why Boeings decline _must at all cost_ be linked to nontechnical advantages of the competition. Thus forex the WTO litigation.

I find your theories to be shortsighted, determining that Boeing’ strategy to be a failure before they have even played out. Your comments might be right on about the narrow-body space, but I think that is also playing out the way Boeing wanted. I’m not sure they really had a heart in the segment and wanted to move up and focus on the wide-body space. Looking at the current pool of offerings I think they have made decisions in the space for long term success. I don’t buy they are throwing the 747-8I under the bus because I’m not sure they really carried about the passenger portion, but accepted the offering as a bi-product of the freighter. And they wanted the Air Force One replacement. When that new contract is announced and awarded the passenger variant is gone. Yes they want to keep the lines full but if they had wanted more business they could have dropped price and gotten the business. Why do that and then have a fleet of a/c that were built un-profitability. So the program limps until the goose lays the 3 or 4 golden eggs. Now the rest of the wide-body strategy. Airbus has the A330, which has had new life because Boeing made a major 787-8 program misstep. Nothing says/shows the A330 has the legs to survive past the 787-8 and -9 on auto pilot. Anybody who thinks otherwise is on the Airbus bandwagon and I’m sure anyone really wants to see Airbus carry out such a strategy. Yes there may be a few more major orders but time will catch up and to the desert they will go. Once reality sets in and the A330 comes to an end, Airbus will have three new wide-body programs (A350-900, -1000, and maybe the -800). In some circles the A350-900 and -1000 are almost in different families. Which means what, we really don’t know right now, but time will answer that question. Boeing has the 787-8, -9, and the much talked about and not yet sold-10. That’s a family of a/c a customer can buy to cover a large swatch of their network. Airbus on the other hand has one plane that focuses on replacing the 777-200ER world. A space that is now limited because of their own product nipped and nipped until the A330-300 finally won the space. Boeing, saw it happen, and went to market with two/three options to a competitor’s one/two, so who do you think wins the A330-300 replacement market? Will we see the overweight A350-900 (or a really overweight -800) or one of two/three 787s being the winner in this space? You say bad strategy, I say they saw the end of 777-200ER well before you did and developed a robust plan based on customer feedback. With that issue addressed and a big unwillingness to kill 777-300ER sales before their time, Boeing set it sights on that replacement space. Why did Boeing wait? Easy answer, any new -300ER sales were like printing money and they really needed money to cover that thing called the 787 and what was there to compete against? The company had it current fleet of relative new a/c, the 747-400 and the 777-300ER, or go after the unfinished concept a/c from Airbus or maybe the A380? Boeing made the space, introduced the world to safe 2 engine mini jumbo a/c. No matter what anyone thinks the -300ER did its job very well. It made the industry understand that 2 holes could do what 4 holes had done in the past. The -300ER impacted the A380 sales, and once proven the 747-8I could step aside to the next generation 2 holers. Airbus, said wait, me too, I got the -1000 to go up against the -300ER. What did the industry do? They told Airbus, don’t be stupid and say you have a me too offering. Go back and tell RR you need more power to even begin to have a discussion. The largest customer for the config bought it and then went to Seattle and told Boeing they needed a -300ER replacement. Airbus vote of confidence came in the way of a slap in the face, and the entire industry was doing all it could to get Boeing to continue the development of a more efficient 300ER. Now the industry has the 777-9X and the -8X add on. IAG bought -1000s but used the announcement to say they really wanted the competition’s solution, and by the way the paper plane would fit well with their growth plans. And you say Boeing’s strategy is a failure? See what Boeing has done with the roll out of the 777-9X and the 787-10, compared to the 737 MAX and it tells you where they’re going. They want the profits from the wide-body to drive their long term success. Just keep on watching and you will see where things go. How long did it take Airbus to get the A330/340 program right? How many variants were built, and then compare that to the number of wide-body variants coming out of Boeing over the same time period. You are talking about Boeing’ sweet spot and they will do everything to continue owning this space. Keep watching.

I agree with you Rudy i have been studying the 747 since Lockerbie pray’s for the family’s of the flight 103.

The A380 with it’s Rolls Royce Trent 900 outdated triple spool engines have a tendency to explode. Over 26 A380 flights have had unreported uncontained explosions and engine shut downs forcing the A380 to land at the nearest airport. When it comes to being cheap Airbus is number one and Airbus has a big problem and when Boeing builds a new plane it orders a new engine. When Boeing built the 777 they spent a fortune and had GE build the GE90-115B however this time Boeing and GE had an exclusivity contract for the Boeing-777. Airbus got its start by buying outdated off the rack jet engines that Boeing paid to develop and build.

The A380 is the ultimate inbred mutt or so called dog of plane with it’s cracked wings and hand me down outdated tripled spool jet engines that have exploded and almost killed 450 passengers. The 747-8I is the superior plane where Boeing takes the pride and time to update and makes sure it’s Genex engines are the best. RR Trent 900 triple spool engine desing is 35 years old. How come Airbus puts cheap old outdated engines on its new A350?

Answer because Airbus is cheap and Europe’s Rolls Royce engines lacks quality control and you bet Qantas would never have purchased their A380 fleet because RR and Airbus deliberately withheld information that the problematic RR Trent 900 engines were and still are dangerous. Half the replacement engines from the Airbus assembly line and RR Factory leaked and had defective welds.

So when it comes to planes being dogs it’s the A380 whose bark is the loudest and and some day soon an A380 with its outdated Trent 900 triple spool engine is going to explode again. However the A380 Airbus will run out of luck and kill everyone aboard. However the A380 it’s cracked wings could fail with it’s defective landing gear and kill everyone however I will be snug and safe flying on 747-8I.

Boeing do seem to have been wrong footed by Airbus in the last few years, they should have wiped the A330 with the 787, but the delays and issues have dented that advantage. With the 777X they seem to be killing off (or severely hampering) their own product.

In the past most sites usually stay out of the whole marketing argument, but recently a number (including this one), have been openly questioning Boeings figures (eg seating numbers for the 748).

The launch of the 747-8 seems even a bit bizarre and even more pointless now, it was already been squeezed from below by the more efficient and more capable 77W, I can’t now imagine what a 777X that comes closer to it and capacity and trumps it more in efficiency will do to it.

At this point, the only good thing Boeing can say about the 747-8 is “at least the other guy isn’t doing much better”

“the other guy isn’t doing much better”

They sold 8 times as much as the 8 i, beat the specs, passengers love it. Sold out for years.

I don’t understand guys bringing hin the 8F, entirely different market.

I thought the A380 was still overweight. If “beat the specs” does not include being overweight, then the 787-8 beat the specs as well, despite engines that were 3% more thirsty then planned.

Airbus has sold 262 A380’s in 12 years, so ROI is still a big open question.

The 747-8 did not beat specs but performed “better than expected” ( going by the known shortfalls : SFC++, weight++ ). That is obviously not the same though what seems to stay in reader minds is “performed better” ( than spec ). ( quite a bit of back and forth pre delivery for the early frames ).

For the A380 it was initially said that overweight was balanced by better than expected performace elsewhere.

Not quite sure what to make of these two links:

http://www.flyafrica.info/forums/showthread.php?12859-Emirates-expects-15h-Endurance-on-A380

http://www.altairproductdesign.com/CaseStudyDetail.aspx?id=10&AspxAutoDetectCookieSupport=1

I seem to remember reading a report on airframe and furnishing weight reduction at Emirates having gained quite a bit of traction.

Most of the links found tend to go to 2006..2008 articles. nothing really “fresh”.

I’m well aware of the 747-8 performance shortfalls. I was making the point that while the A380 might now be considered a good performer, initially it was not entirely to spec, much like the 787-8.

.. initially it was not entirely to spec, much like the 787-8.

Well, to put it bluntly both the 788 and the 748 needed significant MTOW increases to get near spec range and payload while the A380 was assayed by customers to perform to spec from day 1.

In absolute numbers the A380 had less excess weight than the 787-8 though you find articles from before EIS assigning 20..30t flab. Probably just another bashing campaign.

“Probably just another bashing campaign.”

C’mon man, just the facts.

The truth is that the A380 was and still is overweight. It’s great that the airlines still like the performance, because it is performing well, but the facts are the facts.

Obviously, the early 787-8’s were very overweight, but they have been continuously improving. Reportedly, LN-103 meets the original weight specs. But, again, the facts are the facts and the better than promised 20% fuel burn improvement reported by ANA cannot change that.

Any hope for the 748F? Or is that market just too small? Decreasing mega freighters of military nature should leave a spot for the nose loaded 748? You just cant load huge things in a 777F. Airbus has nothing of this kind planned either.

Russia and Ukrain may build some more An-124. A standard 747 can’t carry 777 engines’. Boeing already used An-124 for that task.

The 8f has the benefit of being the only efficient long haul cargo VLA.. When world economies recover they should have a chance IMO.

If the 747-8i gets to be the new plane for US-AF-1, then it could have been worth it.

The 748F nose door just like the 744 has a lower height clearance than the aft side door and high loads have to use the side loading.

To me, historically airfreight has always been the poor relative of the aviation industry with even Fedex still buying used frames.

Most of the blue chip airfreighters have already ordered the 748F, and the remainder will opt for older converted frames.

Sorry, but I dont see much on the horizon for 748 except for AF1 replacement and the procurement process could mitigate against that.

You can load very long items through the nose and you can load about 130t+ of weight on a 748, it is roughly in the neighbourhood of the C5 weight wise but not volume. The 77F can hold about 110t and only things it can load through the side door. Sure the 748 is not an ideal military freighter but it can load thing no other civilian freighter can.

The AN124 will not be built again and more C5s are getting chopped up. A 748 is not as expensive either as a dedicated military VLA.

Two questions.

1. If the the 777-200 and the 787-9 have the same cabin floor length and the same 9 abreast in economy, how can the 777 be bigger?

2. If the several carriers already operate the 777-300ER in 10 abreast, including the largest operator, Emirates, why would they be impressed by a 4 inch increase in width to accommodate 10 abreast? For them the only growth is in the 7 foot stretch. Two rows of economy?

I think the 777X larger version will do well as the 777-300er has been in the fleets of many carriers and its reliability numbers are good. With the A350, this will airbus’ first foray in a mostly composite aircraft and they will have many problems, not perhaps the 5 years worth Boeing had but the delivery dates will be adjusted quite a few times and the 777 has been proven over many years and it still is in demand.

If Being can bring the 787-10 to market soon, the orders will add up quick as they will replace many older A330’s much as did the A330 replace many 767’s, largely due to Boeing’s very late EIS of the 787-8. The production ramp up seems to going well and this will bring delivery dates more agreeable with the airlines.

The 747-8i passenger version now accounts for 38% of total 747-8 orders. This is the biggest piece of the pie it has had since it was launched.

That would be an excellent news if it weren’t due to 747F cancellations.

Reply to Jacobin 777 #2 Re A358

CM, a knowledgable Boeing guy who has commented on this site, said re the A358: Why would A cancel a perfectly good, completely state-of-the art, new plane, and spend billions instead on neoing/re-winging the A330, when that money would be much better spent solving the 358’s problem, which is that it needs a new, optimized wing. I would add that if A does cancel the A358, it will leave B with a near monopoly for years in the entire seqment from 200-290 pax (instead of just 200-250 pax), and result in A’s getting, for its billions spent, a new family planes consisting of only two planes separated by only 36 seats. I think A’s plan is to keep the A358, but wait until they get production of the 359 and -1000 going, and then re-wing it. I think this is B’s plan as well for the 789 and 7810, the idea being particularly for the 7810 to use the new wing to increase payload range to something like the A359’s .

I think A was forced to mothball the A358 because of B’s success in selling -300ERs, and their strategy of PIPing the -300ER until the 777-8X arrives in 2012 (ie 737NG/NSA redux).. They wanted to get the -1000 in the mkt ASAP to soak those sales, before those sales soaked up te -1000.

Initially offered as a optimised frame the -800 variant was changed to a “plain” shrink some time ago. In the same window in time the -1000 model was “uprated” leading to more develtime required for further optimisations like variable thickness frames.

I would not be surprised to see the -800 going back to getting a more bespoke body.

Fuselage and wing optimisations would not cut into the “family” advantages as differentiated structure should have low impact as long as replacable parts stay common.

I agree with most of your observations. Although I think we also have to take into account the A330 line is very efficient, matured and succesfull. Simply scrapping it for the moderately popular/ heavy, long haul A350-800 seems to make little sense.

Repostioning the A330 could also be an option. Optimising it for 240-300 seats short-medium haul up to 5000NMs, clearly below the A350s. A bit like the old A300/310.

Anyway it seems Airbus needs a new smaller, lighter wing for the medium segment. Either for a A322-3 NEO, A330 NG NEO or A350 Light..

http://i191.photobucket.com/albums/z160/keesje_pics/AirbusA330-700Light.jpg

An A-358L, or A-358SR (shorter range for the A market) would be a much better investment than an A-330NG/NEO, which is essentially another rehash of the A-300-B2/4/-600R.

Airbus essentially did offer the A-350 Mk.I, which was really just an A-330NG/NEO as their first attempt at competing with the B-787.

Airbus calls the (current) A-358 “a simple shrink of the A-359”. That means the larger A-359 will absorb most of the design and engineering costs. So, Airbus really is saving money on the A-358 development as it is already money spent on the A-359. The A-358 and A-359 will share many common features, including the wing, landing gear, cockpit, avionics, entertainment system, horizontal tail, and most of the fuselage. The differences between the two models will be few, including the number of frames within the fuselage, and vertical tail. Sinking development and engineering costs into an A-330NG/NEO now would be a doubling of the costs for an airplane in the same class, they will essentially have two 275 seat (3 class) airplanes.

The current A-358 has sold about 95-100 airplanes. It is one of 4 airplanes in this class, the A-332, A-358, B-763ER, and B-789 in, or about to begin production.

The A-332 has sold about 575 airplanes (current back order is about 85)

The A-358 has sold about 100 airplanes (all on back order)

The B-789 has sold about 355 airplanes (all on back order)

I could also add the A-342 (out of production), A-345 (out of production), B-763/ER (ER is still in production with a back order of about 8-10), and B-764ER (still offered, no back log) to this class but that would cloud the numbers.

This class of airplanes has sold very well since the early to mid 1980s, but today there is no room for more than two models to compete against each other. That is because the B-787 and A-350 offer so much more range and much lower operating economics they make the A-330 and older models almost unsellable.

Airbus is already going to ‘update’ the A-330. For what reason, I really don’t know because it will compete mainly with their own product line, possibly taking sales opportunities from the A-358..

Let me be sardonic:

As long as you need two 787 to fly one there is a place for the A330 😉

Similarly the A330 competes well against a potential delivery date beyond the planning horizon of the average airline.

That is why the production increase makes a lot of sense. Also bringing in improvements for the second half of the decade will delay the drop off imho. so by all means cheap improvements are definitely a Good Thing (TM) for Airbus.

Apropos: the majority of A330 deliveries has shifted from the -200 to the -300 model (currently ~ 2 -300 : 1 -200 : 1/3 -200F , ~110 for the year )

Apropos freighter: ~1/3rd of 777 deliveries are freighters while 777-300ER ( 2/3rds ) and A330-300 are about 1 : 1 . other 777 subtypes are 1..2 per year.

Hmmm…..

The current (2013) list prices:

A-330-200 = $216.1M USD

A-330-300 = $239.4M USD

A-330-200F = $219.1M USD

http://www.airbus.com/presscentre/corporate-information/key-documents/?eID=dam_frontend_push&docID=14849

B-787-8 = $206.8M USD

B-787-9 = $243.6M USD

B-767-300ERF = $185.4M USD

B-777-200LRF = $295.7M USD

http://www.boeing.com/boeing/commercial/prices/index.page

These are list prices for 2013. We all know airlines do not pay these prices. But, based on list prices, the B-788 costs less than the A-332, and the B-789 is just about $4M more than the A-333. The B-767F and B-777F have the A-330F price bracketed, just as they do on payload and cubes.

Wasn’t the inital list price for 787 models about 2/3rd of its A330 equivalent?

We do know that 787 production is currently very expensive and will stay

well above originally planned levels.

Thus going by list prices customer utility isn’t all that much apart.

Definitely not in “revolutionary” dimensions.

New “optionless” 787 customers won’t get their purchase before ~2020.

“We do know that 787 production is currently very expensive and will stay well above originally planned levels.”

What’s the basis for this assertion, especially the second part?

The reality is that the 787-8 unit cost has been steadily decreasing almost exactly like Boeing predicted back in 2011. Last year, there was roughly a 50% cost reduction from LN-8 to LN-75 which put 787 production on a 21% learning curve. Currently the cost reduction is about 60% between LN-8 to LN-100 which puts 787 production on a 25% learning curve. Of course, these fitted curves are idealized models but the fact that units LN-76 to LN-100 improved the learning curve is a great sign.

Boeing’s 2011 prediction of a 25% learning curve was criticized by industry analysts as being overly optimistic, considering the 777 program historically showed a learning curve of about 18%. Apparently, Boeing knew something that the analysts did not.

I think the reason it got better after LN-75 to LN-100 is because those frames no longer required any rework. The question, in terms of being able to predict break-even, is whether or not the learning curve will continue to be at 25%. There will probably not be any more major learning experiences, of the magnitude of eliminating rework, but the recent rate increase to 7/month and the subsequent rate increase to 10/month scheduled for later this year can potentially keep the 787 production system on the 25% track.

If the 787 stays on the current learning curve, the program can break even way sooner than the more skeptical analyses predict.

Mike,

Boeing’s 2011 predictions are miles away from their original planning.

What today is assembled on 3 lines was originally planned to pop off

a single line. Just snapping LEGO’s together at 10 per month 2 years after EIS or thereabouts.

With significant extra work per plane caused by change incorporation fast gains

can obviously be expected from reducing that rework part.

But this gain is from “exorbitantly expensive” to “still very high”. The whole projection is definitely still above original planning ( 2004..2006 ) and will stay there.

( Then my guess is that not only product comparisons are bolstered by creative

math )

Uwe,

According to the list prices, Airbus is asking more for the A330-200 than Boeing is asking for the 787-8. Given this fact, how is the cost of 787-8 “exorbitantly expensive” or “still very high”? Especially since LN-100 reportedly cost ~$160M to build, which is already much less than the list price. Yes, I know that airlines almost never pay the list price, but that goes for both Airbus and Boeing.

As far as the production rate goes, it should be up at 10/month by the end of 2013, which is about 2 years after EIS which was late 2011.

1 line, or 3 lines, who cares. It all comes down to unit cost, which, like I said above, is lower than the list price and is deceasing according to plan. If you are indeed so sure that the unit cost is “definitely” high, and will stay that way, why not support your assertion with some numbers.

Mike, we were talking about production cost to Boeing.

In capitalism for sales price the first order determinant is customer utility and not cost.

for production ( i.e. the sales price is as high as the customer is willing to pay )

Production cost then determines your profits ( or losses ).

I would assume that list prices are a tentative positioning in the market.

This would indicate that the A330 as a package ( capabilities + availability )

has slightly higher value than the 787.

On manufacturing cost:

3 times the originally planned production arrangement needed would indicate that the original workforce/workplace arrangement was completely insufficient. You can’t tell me that the required expansion could be cost neutral. Neither in infrastructure investment nor on workforce / manhours requirements.

The 787 will stay more expensive to produce than planned for in the exceptionally sucessfull sales campaign and its pricing.

787 production has been running since 2007/8. Getting to ten a month end of this year is a 5..6 years interval.

How many carriers canceled their B-787 orders just to turn around and order the A-332?

That is an interesting question.

We know that about 200 787 purchases were canceled during

a period that saw 2..4 times that many A330 sales.

We also know that the initial 3/5 of the current 787 order book were sold at an average of $85m at a time the A330 probably sold for nearly twice as much.

Then, most 787 customers are on a “tranquilizing” compensation drip. Not canceling does not incurr losess beyond the fubared business model. .. and maybe eventually the horse will learn to sing.

So it looks like a lot of customers either went for only the A330 or took to A330 while keeping their extremely cheap but unavailable 787 purchases for later at no increased hurt.

It still stands: after the 787 has turned into a known entity like the A330 sales don’t reflect the touted advantages. List prices seem to actually give a measure of relative utility.

Use the list prices only as a guide and assume discounts.

For the A330-300 v 787-9 capital costs, Airbus assumes a $900,000 lease rate for the A333 and $1.2m for the 789 when assigning ownership costs and calculating economics. Using a 1% lease rate (which may or may not be reality–flag carriers like Lufthansa would be less), this infers a $90m and $120m sales price respectively. Compare this with the list prices and you get your discounts. We wrote about this on AirInsight around May or June of 2012.

Uwe,

We are talking production cost, as in unit cost. Cost of additional engineering, facilities, and tooling are indeed program costs, but are not typically considered part of the unit cost. Obviously, the 787 program is way, way deeper in the hole than Boeing originally planned, and it is well known that Boeing will have to sell many more units than planned for the program to break even. None of this changes the fact that Boeing now has the 787 unit cost well under control, and the production system has been stabilized.

I only brought up list price to illustrate that the current 787-8 unit cost of ~$160M is not out of line.

You said 2 years from EIS to 10/month, now you are changing what you are saying to support your own opinion. When the program was delayed, everything got delayed by the same amount. Boeing wisely chose not to ramp up the production rate until the design was stabilized.

Production of the A380 was slowed for the first 3 years after EIS relative to the original plan. This after the EIS itself was delayed. Obviously, Boeing has fared a lot worse with the 787 schedule, but it is a matter of degree.

It’s 2022, not 3012.

Philippine carriers will eventually be looking to expand their long-haul fleets to cater to the budget conscious Filipino-traveller. Low cost carrier Cebu Pacific’s first A330 just rolled off the assembly line with a whopping 436 seats!

Once the ban on Philippine carriers flying to the US and EU is lifted, they will be in the market for an aircraft that can handle a long-haul Manila to Europe segment at the lowest possible cost per seat mile. No airline has yet been able to successfully maintain a long-haul budget route between Europe and Asia.

Air Asia X pulled out their A340 services citing that it was not economically viable and previous to that Oasis Hong Kong and their Boeing 747-400’s failed. But Cebu Pacific will be looking to make another attempt at cracking this market successfully.

So the only question that remains is as the carrier seeks to expand its long-haul fleet, which aircraft will have the ability to provide the best economics on the Europe-Asia sector for a budget carrier? A350, B787, B777X? With the improved economics and fuel efficiency of the modern aircraft models, it is quite possible that a long-haul budget carrier might yet fly viably.

More Information on the needs of Cebu Pacific and Philippine Airlines here:

Cebu Pacific

http://www.philippineflightnetwork.com/2013/05/first-glimpse-of-cebu-pacifics-brand.html

Philippine Airlines

http://www.philippineflightnetwork.com/2013/05/the-exciting-flight-path-of-philippine.html

On the Air Force One talk, would the US invest in a platform that has a strong possibility of it being one of the last frames?

It’s great if you buy a huge fleet of them ( a la KC-135), but on a 2-3 aircraft fleet would that make upkeep increasingly difficult and expensive? One of the reasons for the change of aircraft, rather than it using it’s flying hours, especially if based on a relatively small fleet of 748’s.

Pingback: Aviación y turismo