Leeham News and Analysis

There's more to real news than a news release.

Sizing up engine market share on the A320 family

While competition between Airbus and Boeing snares nearly all the headlines and all the “sex,” competition for engine orders is less sexy and receives less attention.

Part of this is because of the increasing trend toward sole-sourcing. The Boeing 737 has been sole-sourced by CFM International since the creation of what is now called the Classic series: the 737-300/400/500. Pratt & Whitney believed at the time Boeing was upgrading the 737-200 that airplanes were up-gauging and bet its future on the Boeing 757 size. It was one of the classic corporate blunders of all time.

Shut out of the 737, P&W joined with Rolls-Royce and MTU to build the International Aero Engine V2500 for the Airbus A320 family. IAE came to the table late, giving CFM a solid head start on the program with a variant of the CFM 56 that powers the 737 Classic and later the 737 NG.

IAE trails to this day, but has done a remarkable job of coming from behind. CFM tends to be favored on the A319 and A320 while IAE is the preferred engine on the larger A321. IAE offers more thrust and better economics on the A321 while the CFM has better economics for the smaller Airbuses. CFM’s reliability is legendary and tends to be better than the V2500.

The blog PDXlight has done a marvelous job of dissecting the engine market share of the A320 family for the New Engine Option. We asked PDXlight to do the same exclusively for us for the A320ceo family. The results are below the jump.

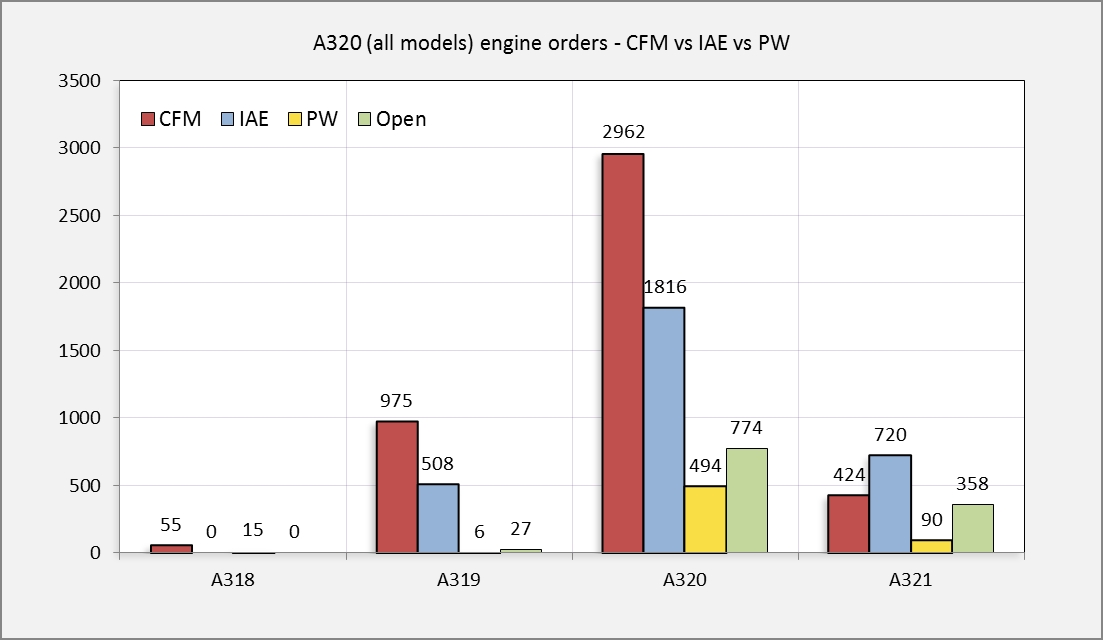

The following chart compares all A320ceo/neo with all engine types (CFM56, CFM LEAP, IAE V2500 and PW GTF).

.

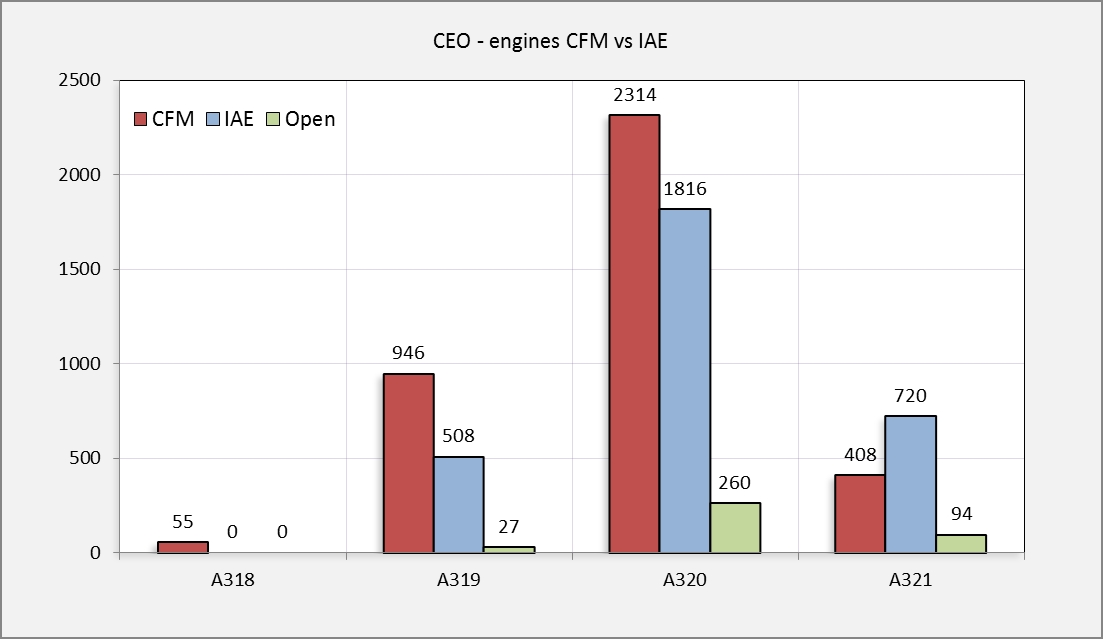

The following chart shows just the CEO engine choices.

.

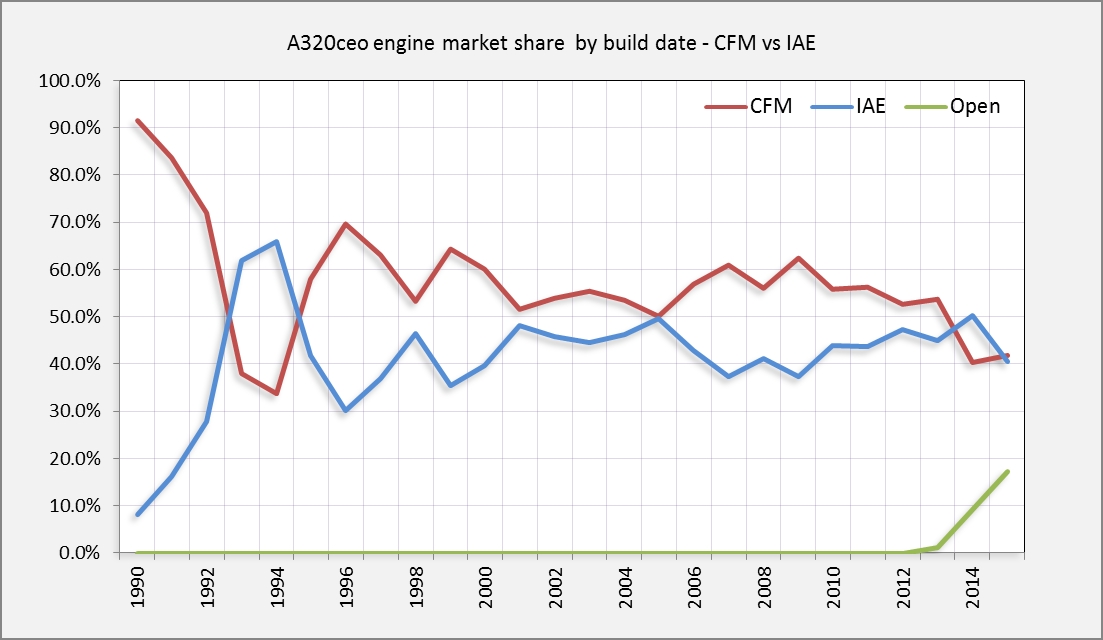

The following chart shows how IAE gained market share vs the CFM 56 to become a significant challenger.

.

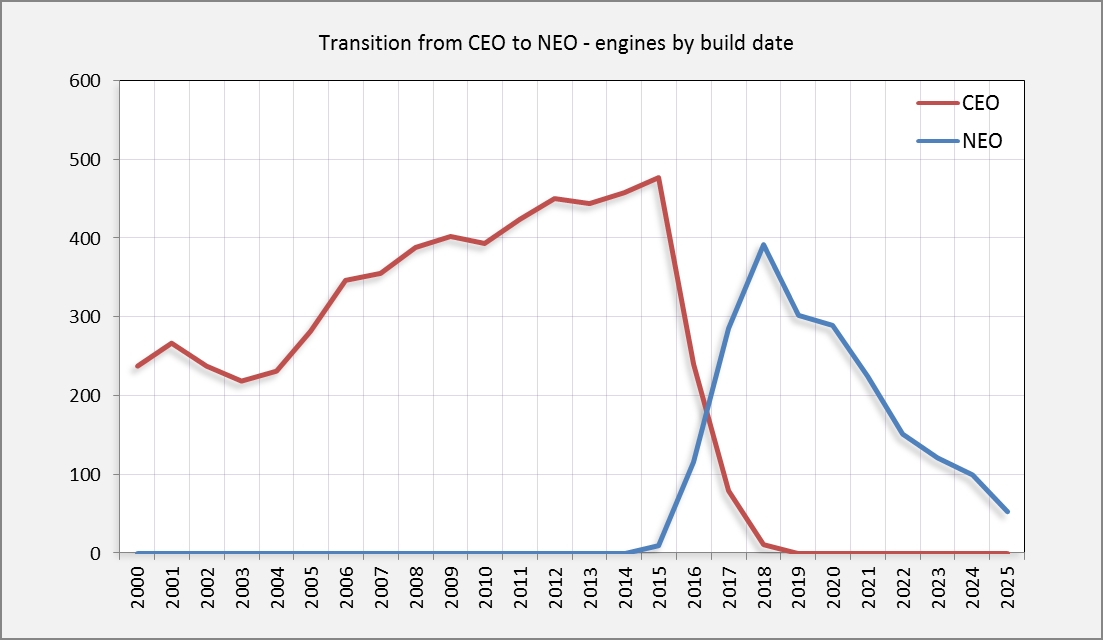

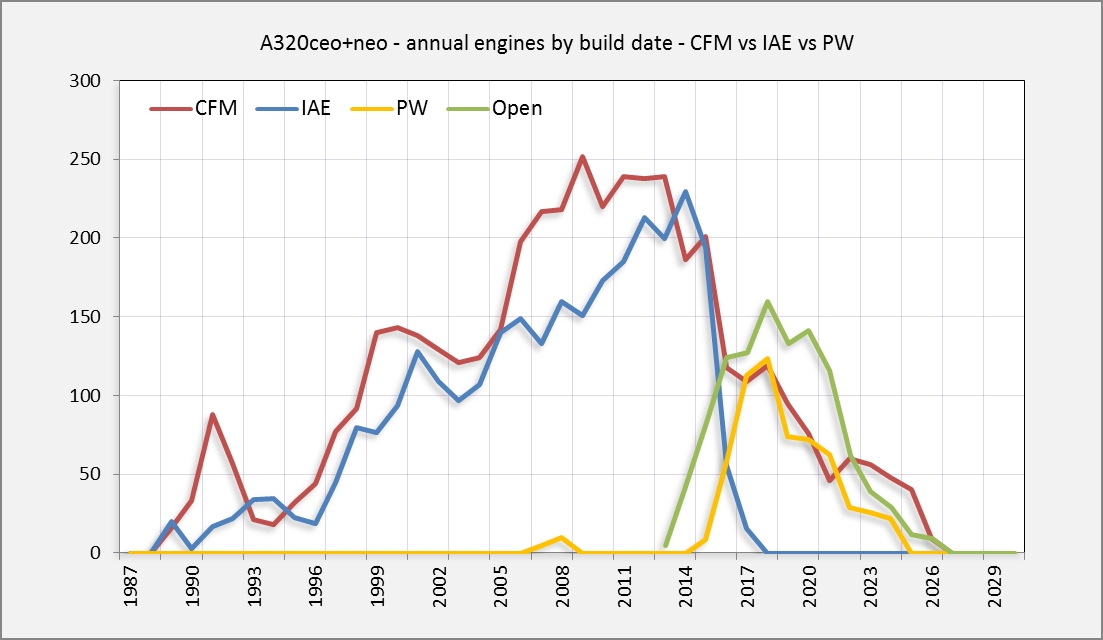

The following chart shows the transition timeline from the A320ceo to the A320neo, both engine types.

.

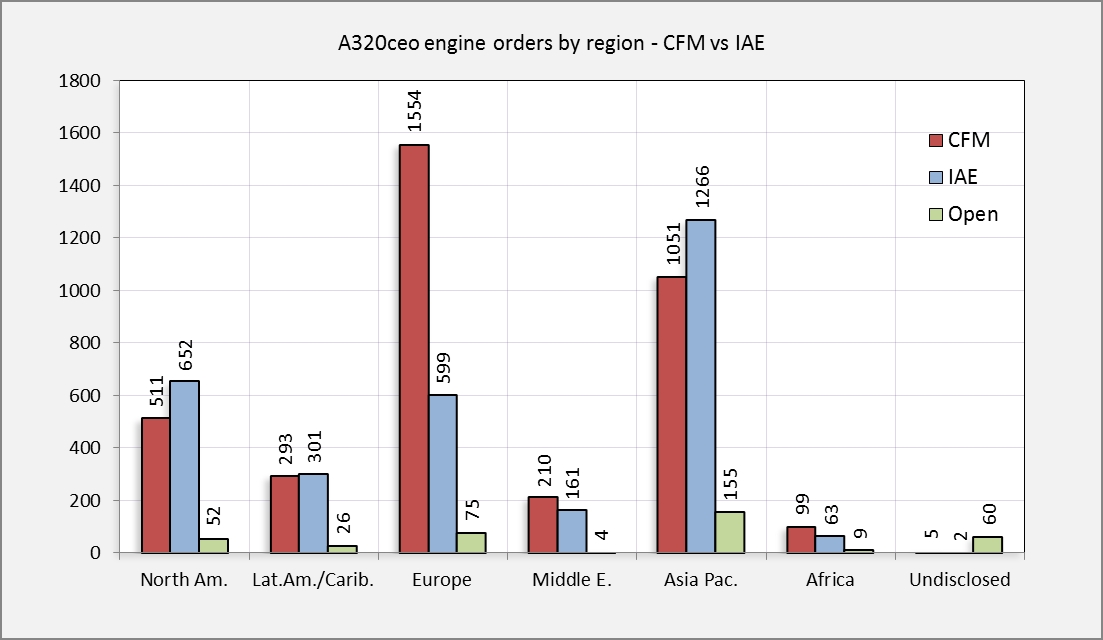

The following chart shows the CEO engine choices by global region.

.

Finally, this chart shows the engine choices for CFM56, V2500, CFM LEAP and PW GTF for future delivery dates.

.

Thanks to PDXLight for this complex analysis.

Very nice

Might be interesting to slip CFM between CFM56 and Leap1A

And to a lesser extend PW between PW600 ans PW1100

I guess the last chart shows aircraft fitted with the respectiv engine types rather than engines. You have to double the numbers in the chart to get the numbers of engines build.

Same is true for the 4th chart.

CFM beat out P & W on several large deals by undercutting the price and offering deals on current engines. Republic for example has ordered LEAP and Purepower. Most think that they will cancel one or the other if all of the conditions and performance guarentees are not met. No one knows for sure how well the LEAP will perform as it is still a paper engine. P & W’s geared engines have over 4,000 hrs of test runs and hundreds of hours of flight time so they are more of a known quantity. The LEAP engine has more stages, burns hotter and relies on exotic blade technology which is high risk. I would not be surprised if the program is delayed or does not match the promised performance specs. If that happens you might see lots of LEAP orders switch and MAX customers go over to NEO. The CSeries may be the big winner as the NEO production line has little extra capacity to absorb additional orders in the near term.

It seems, theoretically, the GTF has the upper hand. What if becomes reality and everyone knows it? CFM will need to go back to the drawing board. Someone else asked what would happen if the GTF proves a rod hot gearbox in front of the engine that isn’t reliable at all. Desperate faces at Airbus, Bombardier, Mitsubishi, Irkut, Embraer, basicly everyone except Boeing. But I agree thousands of good GTF test hours sofar, so that scenario becomes increasingly unlikely.

Anyway, anyone who would have declared that CFM/ mighty GE / RR would be cornered by PW in the biggest market segment, 10 or even 5 years ago, would have been burried under “never”‘s, ” cold day in hell”‘s “arm chair CEO”‘s and “who the hell do you think you are”‘s. Amazing come back by PW.

Personally I think the GTF A321 NEO will have far superior performance in nearly every aspect compared to the 737-9. Having e.g. UA and DL also move over. It could result in Boeing putting a NSA on the table again this decade.

so CFM is GE and Safran, IAE is Rolls and P&W and PW is just P&W?

Yup

CEO engine choices, is that the CEO’s of the airlines??

Current Engine Option

I’d be really interested in knowing what percentage of dreamliner engines are RR and what percentage are GE, the same with the Airbus A350. If someone could point me to an article i’d be very grateful

Wel A350 is 100% RR since there is no alternative engine. With 787 I believe the split is fairly even with GE just slightly ahead.

Pdxlight has started and is maintaining a 787 order/changes/cancelations list.

see: http://www.pdxlight.com/787.htm

A bit more informative than forex the one kept on Wikipedia which only reflects the current status quo.

Currently, 596 Dreamliners have engine selections : GEnx = 744 engines (62.4%) and Trent 1000 = 448 (37.6%). Another 244 Dreamliners did not have an engine selection at the end of March, so there is an open market for 488 TBDs. (i.e. To Be Decided.)

thks for your comments, great help

On the 787 the GE engine currently has better fuel burn over the RR, the PIP2 was certified the other week and it claws back any miss that was still there, RR has about 2% to claw back yet. A C-model followed by the TEN version, RR will actually be in the lead with the TEN version, a 78K thrust model for the 787-10.

Pingback: Odds and Ends: LEAP vs GTF; CSeries flight testing; MRJ FAL | Leeham News and Comment