Leeham News and Analysis

There's more to real news than a news release.

Farborough Air Show, July 16: Snipe hunts in an era of model improvements

- Upate, 5:30am PDT: The Wall Street Journal has an article that is more or less on point to the theme of this post.

It doesn’t matter what the competition does, it’s always inferior–until you do it yourself.

The continued, and tiring, war of words between Airbus and Boeing throughout the decades is monotonous and self-serving. If you step back, it’s also amusing.

Consider:

- Boeing constantly dissed the Airbus concept of fly-by-wire–until ultimately adopting FBW in its airplanes.

- Airbus dismissed twin-engine ETOPS of the 777 while promoting four-engine safety of its A340–until evolving the A330 into a highly capable ETOPS in its own right.

- Airbus put-down the 777X, saying the only way Boeing could make it economical was by adding seats…which Airbus has now done for the A330-900 to help its economics.

- Boeing ridiculed the idea of a re-engined A320, but then had to follow with a re-engined 737 MAX due to the runaway success of the A320neo.

- Boeing ridicules the A330neo as an old, 1980s airplane–neatly ignoring the fact that the 737 and 747 are 1960s airplanes.

- Airbus still calls the 777/777X/787 a “dog’s breakfast,” though we know some dogs who eat pretty well.

And so it goes.

The fact of the matter is, however, that minor and major makeovers of existing airplanes have long been a fact of life, maximizing investment and keeping research and development costs under control. The Douglas DC-1 was the prototype for the DC-2, which begot the DC-3. The DC-4 (C-54) begot the DC-6, DC-6B and DC-7 series. The Lockheed Contellation was reworked from the original L-049 through the 647/749/1049 (in various versions) and finally the 1649.

Then came the jet age, with vastly more expense, and model upgrades became the norm. The sniping today between Airbus and Boeing goes unabated in an era of historical model improvements.

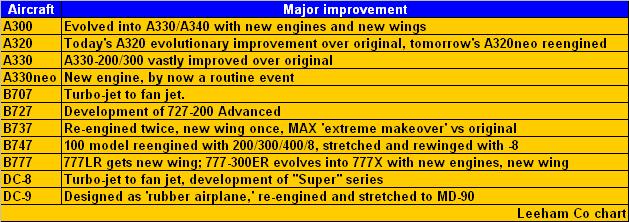

Let’s take a look at just the jet age history.

A short, simplified history of jet age aircraft improvements.

This chart is hardly inclusive but it makes the point: re-engining and re-winging airplanes is common.

Today’s sniping, of course, comes down to derivative vs new. Airbus claims the derivative 777X can’t compete successfully against the new A350-1000. Boeing claims the derivative A330neo, which doesn’t have a new wing to go with the new engine, can’t compete against the new 787.

We have our doubts about the 777-8 being an effective competitor against the A350-1000. The much heavier 777-8, which has to be in order to be the ultra long range airplane that it is, simply is too much airplane for more than about 5% of the world’s routes not covered by the -1000. We believe the 777-8 will be a niche airplane.

The comparisons between the A330neo and the 787-8/9 are more challenging. Based on our pre-neo launch study, using our estimates of specifications for the neo, we concluded the neo would come within 3%-5% of the operating costs of the 787, with a lower price making up the difference. We’ll have to rerun the analysis now that we have definitive data, but Airbus claims the operating costs will match the 787. We shall see.

Boeing claims the 787-10 will be 30% more economical than the A330-900. The 787-10 has a 13 seat advantage over the -900, but we’re skeptical about the Boeing claim. Our re-analysis will tell us if Boeing is correct.

The war of words between Airbus and Boeing is silly, tiresome and unending.

For both Boeing & Airbus, I told them please keep on competing each other. I think this will help introducing better products on the long run for the customers

I see this “war” as something quite childish. I really doubt these car salesman have any effect at all in airline planners. As Leeham themselves they have their propietary models to deface the marketing claims and see if a plane really fits in their business plan. Unless these marketing tactics are aimed at clueless fanboys, it’s a waste of effort.

I like Airbus because I’m European and I wish them the best, but that’s it. Boeing makes great airplanes too, and the competition between both has pushed the aeronautic advance faster and further: that’s undeniable.

Well said Deeso. Scott does a great job with the website. Some of the childish back and forth Airbus vs. Boeing cheerleading on the message board isn’t worthy.

The Dassault Mercure is somewhat the predecessor of the A320.

The Mercure was closer to the 737 than to the A320.

DC 9 > MD 80/90 > B 717

an nicely done article that has no equivalent in EN:

http://de.wikipedia.org/wiki/Entwicklungsgeschichte_von_der_Douglas_DC-9_bis_zur_Boeing_717

Is there a link where Boeing claims the 787-10 is 30% more efficient than the A330-900? From memory, Boeing stated such economics against the A330-300.

Boeing has changed its messaging to compare with the A339. From the other day:

Jon Ostrower @jonostrower 4h

Boeing’s Scott Fancher: 787-10 hit firm configuration in April, says jet is 30% more efficient v. A330-900neo, (Airbus: Neo v. 787-9) #FIA14

Well, changing tack is not unheard of*… Boeing also previously (before MAX was launched) claimed that A320neo merely brought the A320 to parity with the 737NG.

https://leehamnews.com/2010/12/10/737ng-vs-a320neo-an-interesting-chess-game/

I’m curious to see what the results of your analysis 787 vs A330neo are going to be, but 30% difference seems outlandish, even for the 787-10. If that were the case, Airbus surely wouldn’t have launched the A330neo.

* Airbus have of course done the same, with Leahy vocally dismissing the possibility of an A330neo during the earnings press conference in January this year.

Life goes on.

“but 30% difference seems outlandish, even for the 787-10. ”

Since Airbus says that the neo is 14% better than the ceo, wouldn’t that also imply that the 787-10 is 44% more efficient than the A330-300?

I guess the trick is NOT to compare the A330-900 against the current 787-9 with about the same seat capacity but instead to use the future 787-10 with EIS about 2018 (https://leehamnews.com/2013/09/24/busy-decade-ahead-for-new-derivative-airplane-eis-dates/). Just like the comparison between current A350 and future 777X with somehow enhanced engines. Don’t mention an A350-1100 with “Advance” engines. This could be “747-8i vs. A380-800 reloaded”.

According to list prices the A330-900 at $275 million is cheaper than the 787-10 at $290 million but more expensive than the 787-9 at $245 million. Maybe efficiency according to Boeing excluding interest rates…

I also still believe an airline can make more profit with an aircraft than without an aircraft.

That’s my recollection too. Seems that the only change in their corporate marketing line is the name of the model from -300 to -900neo. Fair enough that they have not had enough time to study the neo but to repeat the same numbers as for the ceo aircraft is a bit silly.

But then, they did the same thing with the A320neo. Three years ago at Le Bourget they were saying that the A320neo would just bring the aircraft on a par with the 737NG. Of course, the orders at Le Bourget told a different story, and not too long after the MAX was offered in the market before getting a firm ATO.

The dilemma is the same for both companies: Do we modify an existing well proven design or do we launch a brand new effort from scratch?

Sometimes there is no existing model to be able to compete. Like in the case of the 777, Airbus had no direct match. So the A350 had to be the brand new design it is because there was nothing in the portfolio to modify. But the A330 is in a better position to compete with the smaller 787 and therefore it was worth considering a neo version. That was a given for most observers.

But sometimes it is a bit more complicated. What will be the verdict of History on the decision to go for the 737 MAX instead of opting for a brand new design like the NSA would have been. Did Boeing make the right decision at the right time? My own verdict is that it took the right decision at the time it did because it was too late for a new design when it finally, and under duress, took the decision.

That is because Boeing was reactive instead of being proactive. Had it launched an NSA earlier it would have caught Airbus by surprise and put it in a quandary: do we proceed with a neo or do we compete directly with Boeing and offer say an A390?

I would say Airbus only needed to be proactive and come out early with a neo to respond to the CSeries challenge. Whereas Boeing had to be bold and come out even earlier with an NSA in order to be able to use the full potential of the GTF engine. Something it will never be able to do with the venerable 737.

The MAX is a short term answer engendered by a short term vision. With the A320 Airbus had a better hand at the opening, and I predict it will retain the upper hand until the 737 dies of old age.

Airbus had a stroke of luck when Boeing decided to make the B787 a longer ranged aircraft. That made it heavy enough to give the A330 a fighting chance. Unfortunately for Boeing Airbus didn’t make the same mistake with the A350, they took aim straight at the B777 market and forced Boeing out of it and into a larger category.

“”But sometimes it is a bit more complicated. What will be the verdict of History on the decision to go for the 737 MAX instead of opting for a brand new design like the NSA would have been. Did Boeing make the right decision at the right time?””

Yes…at the time I believe Boeing made the right decision. Boeing was already busy trying to get the 787 Produced and Flying and, as a result, they were spending a lot of money to do it. In fact, Boeing is still losing money galore on the 787, and I really don’t think this is going to end soon. So…I think Boeing did the best it could have given their financial limitations.

However…had Boeing in 1993 decided to have built a clean-sheet follow-on to the 737 instead of going cheap (or so they thought) with the 737NG, then we wouldn’t even be discussing this today. Back in 1993, Boeing had the money and the manpower to build a clean-sheet replacement for the 737, but they didn’t do it. And this turned out to be a huge tactical mistake that Boeing will pay for until 2030 – and maybe longer. As a result, the A320 NEO has 60% of the market – the sweetspot. The Boeing 737Max will forever be a”Me too” aircraft.

“Back in 1993, Boeing had the money and the manpower to build a clean-sheet replacement for the 737, but they didn’t do it.”

Yes I agree with that statement. But still, at the time there was nothing special that was available in terms of engine. In 2008 there was the GTF engine which was a REAL “leap” forward, and still is.

What I am saying is that the AVAILABLE engine at the time the decision is to be made is a determinant.

But in 2008 Boeing also had fully developed its capacity to manufacture a small CFRP wing like Bombardier did on the CSeries. Imagine an NSA the size of existing 737, or slightly bigger. It would have obliterated the business case of the larger variants of the CSeries: the very promising CS500/700/900 series. And it would also have left the A320neo with less than one third of the market over the long term.

It is true that we cannot entirely blame Boeing for that fatal mistake. Like you I recognize that Boeing was in a bind at the time. All the energy and resources were indeed focused on the 787 which was in a dire strait during the key period of the GTF introduction.

One could say that it was bad luck associated with bad timing. In other words being in the wrong position at the wrong time.

“”But in 2008 Boeing also had fully developed its capacity to manufacture a small CFRP wing like Bombardier did on the CSeries. Imagine an NSA the size of existing 737, or slightly bigger. It would have obliterated the business case of the larger variants of the CSeries: the very promising CS500/700/900 series. And it would also have left the A320neo with less than one third of the market over the long term.””

Maybe. Maybe not. I am not convinced that large scale use of CFRP on smaller planes is practical…yet. While CFRP might save some weight, this could be offset by the increased cost.- and Mitsubishi said as much when discussing an MRJ Composire Wing (And Mitsubishi has the experience to know)

Likewise, we know that the 787-8 can outperform the A330-800, but at what cost? Will the price of the 787-8 ever go down so much that it can economically compete with the A330-800? We just don’t know yet.

However, where the point has been resolved is at the 777-sized airplane and above. At this size plane, CFRP rules.

With a conventional wing the CSeries would be a few thousand pounds heavier. I think Bombardier hit a nice balance with the CSeries by making the more vulnerable fuselage out of Aluminium-Lithium and the rest of the aircraft, including the empennage with CFRP.

It’s a question of mastering the technique and gaining the experience. And that will thrust Bombardier in the major leagues sooner.

The reason Airbus was so nervous about the CSeries is not only because of the GTF engine, but because it is relatively lighter than the A320. There might not be a huge difference, but it is a very significant one nevertheless.

“It is true that we cannot entirely blame Boeing for that fatal mistake. Like you I recognize that Boeing was in a bind at the time. All the energy and resources were indeed focused on the 787 which was in a dire strait during the key period of the GTF introduction.”

Big spending for Boeing started not in the devel. phase but in the “build them anyway and quickfix dumb problems” phase.

Boeings basic ideas was to leverage others for spending ( and gifting ) money for their Dream product.

Such a nice reading (as all the time). Both Boeing and Airbus are good kids they have just competitive mothers that chat and fight about them all the time. Both kids share the same winds and engines therefore are pretty much equal. One have a joy stick the other a yoke. They have the play room painted differently one is gray the other is brown. The only big difference is on their brains (FMC) otherwise it will be so boring in this world. If the fight continue like a Babele tower for seat capacity somenting wrong will happen. It is a war of seats and this is understandable if each seat apparently generate 3 million each year. Soon I will see an aicraft towing a trailer drone for cargo goods to add seats in the cargo area for the Third class. Afterall customer want always to pay nothing to go gambling. I will see an a 380 biplane adding another wing on top for extra lift (and drag) but plane will fly much more hight to thin air despite the “coffin corner” because economy laws prevail on the Phisics ones. This war of architects for a more dense cabin, All the gimmicks of a pretty entrance and cabin is BS.

Soon a smart Howard youngster will suggest an airplane that after reaching cruise altitude will switch off half of its power plans to save fuel. Afterall isn’t the Nextgen navigation project an effort to convert any airliner into a glider after TOD ? What next? Drones, since passenger care more about In flight entertainment system than anything else. Sorry, I drive.

And finally watch this; one day the Airtraffic in America will be by Emirates because if they will not get the “slots” they want they will give back the planes that they have ordered. America is fighting for renew its infrastructures, as you know there isn’t yet an airport that can let two a380 taxing in opposite directions. both childs are growing larger Afterall folding wingtips were studied for the 777 more than twenty years ago.

I cannot imagine a kid with a yoke. That’s for grand-pa! 😉

Your bullet point list left out a few examples.

John Leahy criticized Boeing for building a “plastic plane” in the 787, until Airbus did the same with the A350.

He said the 787s larger windows were a gimmick, until Airbus did the same with the A350.

He criticized the 787 for stuffing the crew rest in the overhead bin, until Airbus did the same with the A350.

He derided 9x seating in the 777, the dreaded “double excuse me seat,” until Airbus did the same with the A350.

“Your bullet point list left out a few examples.”

I can think of even more than your few examples. But his point is clear, and that’s that.

The point is, that every Boeing innovation is BAD, until Airbus copies it. Then suddenly it becomes good.

I don’t see the relevance of your point. The above list also gives examples where Boeing says Airbus innovations are bad until they adopt it too. And I know you can think of other instances of this too.

If you can’t beat them, imitate them! 🙂

fighting externally with words and on each order ,but happy to have a perfect duopoly ;each matching/responding to the other (even in strategic thinking -we will evolve with derivatives and cut program risk /no more moon shots) and enjoying the fruits of the market -much better than the alternative of a third or fourth big player (non regionals). Good for Airbus to keep the Europe brand , tech and workers going ; good for Boeing’s shareholders and its workers and for American Exports. A good equillibrium.

Do you mean that there should be no room for the likes of Bombardier to grow? Why would it be bad to have a third player like say a revived McDonnell or Lockheed?

After all there are three major engine makers. And I am not even counting Safran which has a 50% share in the most successful jet engine in history.

If you have a point I am sorry but I don’t get it.

A general business axiom is that for a duopoly to remain stable over time, the two players must not compete to the death and maintain something like parity. If one gains more than 60% of the market, then the other will become too weak to effectively compete and it will become or largely operate like a monopoly and the customers end up the real loser.

A triopoly like the B-L-D works if the costs of development, market size, and profits can support it. The capital intensive, relatively low margin commercial aircraft business probably can’t support it. Your example somewhat proves the point: Lockheed did go bankrupt, Douglas survived by merging with McDonnell, and Boeing survived by eliminating 75% of its workforce. In the A-B-D triopoly, MD became too weak (yeah, blame the management if it makes one feel better) and had to merge with Boeing. One could credit A with saving the industry by stabilizing the duopoly because MD had become too week to compete with B. Kind of like the final shootout in the movie the Good, the Bad, and the Ugly.

Even in engines, Pratt in the last decade or so almost fell out of the commercial business, only now showing promise with the GTF (and surviving the downturn with military contracts). It is increasingly difficult to even have multiple engines on the same aircraft. The 777 is probably the last to offer three engine options and a single engine type will be the norm, not the exception.

Now that the SA market is several thousands of ap’s, as opposed to the historical of hundreds or a thousand, that market will possibly support a third (but probably not a fourth) competitor. I don’t see the duopoly on widebodies changing for decades to come if ever. The capital expenses are so huge, even the duopoly couldn’t survive without government (including military) help.

A strong duopoly is good for everybody, even the airlines and flying public, as long as neither tries to destroy the other, or the two collude to fix prices. I think the healthiest situation for the TA market will be for the A and B to each have a pair of offerings that overlap somewhat but not completely so there is always some market exclusivity for each model and serious competition over most of the range to drive improvement. The 787/350/777/380 mix is pretty close to this.

So let them fight with words, not lethal weapons, and keep enough animosity to prevent them from colluding. I totally see Vaidya’s point.

Lets state the facts

It is nothing wrong the re-ENGINEER a old successful aircraft and make it compete with a newer one of the competition, This was what was done with the B747-400 to attain the B747-8i, which included far, far more than simply re-ENGINING, so to compete with the A380. This was until now not a success, we will know more when

more old B747 will be phased out, serving airports with less facilities and traffic, as where the A380 is operating now.

But it was a success technically, making TIM CLARK to clamor for an A380neo just after 5 years of operation (a quite negative record!!

Another more important reason of the B748i lack of success was the BOEING own wildly successful B777X, which is being even more deeply upgraded from the original B777-300ER. I need not to emphacize the wings and the use of composites.

It was further nothing wrong , at least technically and commercially, to re-ENGINE

the A320, as BOEING had not nothing equivalent available. If the latter was caught sleeping or was surprised that AIRBUS would do that in spite it had good enough result with the Aircraft as it is, is irrelevant. So the A320neo was an success, even if BOEING belatedly come up with a good response.

But it is IMOP a grave misleading issue to sell the idea that was was good for the A320 is good for the A330, joggling the terms re-Engineering and re-Engining!! Using between other arguments that it will be cheaper to built, ignoring the fact that the today’s in both cases list prices are even higher for the A330.

But more because ithe A330neo will have to compete with the both most State of the Art B787 and surprisingly (assuming that the virtues of he A330neo as touted by AiRBUS are real) with their own B359, the only potentially successful aircraft AIRBUS developed in the last 20 years.(the A358 has already committed suicide)

By the way: if we believe above, i.e. that a conventional old heavy aircraft with new engines can be performance competitive with the State of the Art composite ones , we must admit that the “original” A330neo 10 years ago (also called A350 first version) was the right concept and that AIRBUS was terribly wrong to develop the A350XWB, as well as BOEING the B787!!! And by the way, correcting Newton and Einstein in their heretical belief that gravity has a role in issues as here!!

Finally, some airlines signing “Memos of Understanding” (by no means commitments) , morphed to ORDERS by enthusiastic admirers, do so because they expect to buy near term B787 size aircraft and need at least some nominal competitors to maintain BOEING reasonable!!

I hope some blogger would comment above in a respectful manner

.

It has more to do with business than physics. It is true that everything else being equal a lighter plane will be more economical. But there are other factors beside gravity to take into consideration.

For instance a long range aircraft will necessarily have a higher trip cost on shorter distances than an equivalent aircraft designed for shorter routes. And a brand new design will command a stiffer price tag and will be harder to discount than an existing design that is fully amortized.

The A330neo will have state-of-art engines fitted to a relatively “modern” airframe. In other words it’s going to be highly efficient, like the 777X will be made to be. But Boeing cannot offer large discounts on the 787. Douglas never made any money on the airplanes it sold. It’s the same for Boeing with the Dreamliner.

If Boeing has any hope of recouping its investment in the 787 it cannot afford to offer deep discounts anymore. Airbus has much more leverage and can make more attractive offers to prospective customers who would be happy with the capacity/range offered by the A330neo.

That being said, if the oil barrel was to climb to $200 a barrel and stay there permanently, it would be a totally different ball game that Boeing would be sure to win.

Farborough Air Show, July 16: Snipe hunts in an era of model improvements. in response to otontisch: Lets state the facts It is nothing wrong the re-ENGINEER a old successful aircraft and make it compete with a newer one of the competition, This was what was done with the B747-400 to attain the B747-8i, which included far, far more than simply re-ENGINING, so to compete with the A380. This was until now […] It has more to do with business than physics. It is true that everything else being equal a lighter plane will be more economical. But there are other factors beside gravity to take into consideration. OK!! For instance a long range aircraft will necessarily have a higher trip cost on shorter distances than an equivalent aircraft designed for shorter routes. And a brand new design will command a stiffer price tag and will be harder to discount than an existing design that is fully amortized. RESPONSE: Both A330-200/300 nor the B787-8/9 are designed long range, above 8,000 miles. If the route is only 3000, the aircraft will carry excessive empty tank and associate issues weight. I do not know how importante this is, but the related onsequence would be he samein boh cases,. Contrary to Airbus, Boeing has a already designed variant B787-3, much cheaper, 317 Pax, 3050nm, which was already ordered for a Japanese airline, but at this time had not enough taker, and besides, the customer changed it to the B78 —————————————————————————————————————————————————– The A330neo will have state-of-art engines fitted to a relatively “modern” airframe. RESPONSE” Quite relatively! In other words it’s going to be highly efficient, like the 777X will be made to be.——————————————————————————————————————————————— RESPONSE: Here I most strongly disagree. The A330neo upgrade refers nearly only to engines, as it was in case of the A320neo (which had no competitor when launched) whilst the B777X has fundamental changes nearly everywhere, particularly wings,incorporation of a large precentage of composites, etc., . Without this other changes, there is no way the A320 performance will be even near the B787! As said before, AIRBUS tries to hide this incontestable fact behind rhetoric—————————————————————————————————————————————– But Boeing cannot offer large discounts on the 787. Douglas never made any money on the airplanes it sold. It’s the same for Boeing with the Dreamliner’ If Boeing has any hope of recouping its investment in the 787 it cannot afford to offer deep discounts anymore. Airbus has much more leverage and can make more attractive offers to prospective customers who would be happy with the capacity/range offered by the A330neo

You are riding on a lot ( imho false ) assumptions.

( Mostly pronouncements gobled up from Boeing marketing stuff.)

Airbus seems to have a knack for designing airframes that can grow for quite some time with available tech improvements. ( Boeing in contrast has to go to disruptive changes in most models: 737 Classic to NG, 777-300 to -300ER, 744 to 748.)

The laid foundation has enough potential to leverage improvements comparable to a brand new design. As long as that is possible an older frame will stay competitive.

The A330 “Classic” with improvements from recent years was the final A350Mk1 incarnation and sold in big numbers.

The A350 XWB is a decidedly different product: Initially aiming for the 777

playing field from below designed to grow with improvements to cover the full 777 range ( after a couple of years ). One might think the A350-800 was just a decoy to obscure this.

Sorry!!

As you respond my previous post asking for comments stating that I drew my wisdom from BOEING. this phrase being your only “argument”, and in turn qualify the most successful changes by Boeing, as the achievements in the past resulting in the B747-400, B777-300 and B737NG as “disruptive”, I do not see any reason to continue this conversation.

Well, you not only see Vaidya’s point, but you make me see it very clearly as well. Thanks for your answer which turns out to be a beautiful post on its own.

That being said, I remain skeptical deep down inside. Business administration is a very young science and there is a possibility that what has been observed so far has more to do with History than science.

There is no undeniable basis for the argument. It is what they teach to MBAs and it is based more on observation of market forces than a deep understanding of those forces. The workings of business, like like those of finance, remain mysterious and hard to predict.

When Fred Smith of Federal Express was in business school he earned a “C” for his paper where he first exposed his new ideas for transporting goods. That does not necessarily mean that his teacher was stupid. It only means that it did not fit the preconceived notions of business schools at the time.

I believe the duopoly thing is similar. United States used to define the way the economy works. There was little competition outside the US. But slowly the economy, which used to be essentially American, is becoming global. If China is successful in developing its aerospace industry it will not necessarily be to the detriment of Airbus or Boeing. I mean not to the point that one of the Big Two will have to disappear.

And if Bombardier believed the duopoly thing was real and insurmountable it would not invest billions of dollars to commercialize an airplane that is designed to take on Airbus and Boeing. Just about everyone in BBD’s top management holds an MBA along with an engineering degree. I am sure they all know this “law of the duopoly”. Are they all reckless or just plain foolish?

They are not reckless anymore than they are foolish. And they don’t expect to replace one of the Big Two even if they were to become completely successful. BBD dominate business aviation and compete directly with Grumman and Dassault. That did not deter Embraer from entering the market. And it has been quite successful. The only difference is that there are now more players to share an ever growing pie.

It will be the same with large commercial aircraft and engines. There will be more players to share an ever growing pie. If two players can share a market of 25,000+ aircraft in means there is room for a third player.

It is fascinating to watch the permanent face-off between the Big Two. And it should be even more interesting to follow a third player like COMAC or Bombardier make its way into the major leagues. And thrive with the other two. That is when the Big Two will become the Big Three.

Yes and don’t forget that Boeing executive Nicole Piasecki said “I think the A320neo is going to be obsolete by the end of the decade” in March of 2011 to Reuters.

Normand,

“Bus Admin is a young science…”. The duopoly theory is more Micro-Economics than business which has developed over a couple of centuries (Adam Smith). Businesses don’t necessary follow economic theory and sometimes they beat the theory (Fed Ex vs. USPS and UPS), but most of the time they fail when they do (Airborne). “US defined how economy works…” The US had the market and the technology to develop a successful commercial airplane business (with government help), but the model in Europe followed a very similar trend – several different aircraft makers that eventually consolidated into the Airbus consortium (also with government help). Europe didn’t have the huge transcontinental market like the US to foster the industry.

I do think there is room in the 10K+ SA marketto support three contenders, but probably not four. Since there are now several companies trying to be #3 there will be a fierce battle for it, and hopefully one will emerge as a strong competitor. BBD vs. COMAC will be an interesting battle. Meanwhile, A and B’s customer base will assure they will both be dominant players for at least a couple of decades. But the trend of the big two of ceding the low end market to new competitors (first <100, then <125, now <150) will continue as they avoid the heart of the dogfight. BBD managers are neither reckless nor foolish – they are competing,but it is a gamble and gambling IS more business than economics. They are also and they are striking at the low payload/range end where A and B offerings are most vunerable.

Engines I think follow the same model: There are two strong (GE and RR) players, and in third are a variety of weaker players/partners (PW, Safran, BMW…). I doubt GE or RR will develop a major derivative for a market projected to be less than 1000 engines. IMO we will see exclusives on models that don’t project to sell more than 500/ap’s. The bet on the 777-200/-200ER/-300 (570/ap’s) split across 3 engine makers didn’t work out well for any of them but worst for PW. The 300ER/200LR with a GE exclusivity that has ~550 ap’s worked out for GE, but it’s success was far from assured initially.

On the 330neo if it sold over 1000 ap’s two engine makers may make money, but if it is much less than 500 then it may be difficult for even one to make money. The dilemma for the GE and RR here is that they both are cannibalizing their own sales on the 787; RR has roughly 40% of the 787 so they may gain more sales on the 330neo than they will lose on the 787.

Of course, if RR can truly build an engine that is so much superior to its engine of 10 years ago (that missed its initial targets BTW), that totally offsets the advantage of the new airframe (I’m skeptical), then there will be no choice but to do a 787neo engine near the end of the decade (a GE/PW GTF?)…

@GT62

I am glad to hear that you are open to the idea that there is room for a third player in commercial aviation.

I don’t expect in my lifetime to see a situation like we have right now in business aviation with Bombardier, Grumman, Dassault, Embraer and Cessna. But with the continuous extension and expansion of commercial aviation across the globe and sustained growth over a prolong period of time, there should indeed be an opportunity there for a viable third player.

For the engine side of the business, I take objection to your statement that P&W is a weaker player. It is true that it practically vanished from the commercial scene in recent years, but it remains a very strong company. Much stronger than Rolls-Royce as a matter of fact.

RR is on its own. By that I mean it is not part of larger entity like GE and P&W are. The strength of GE for example is that it is directly supported by GE Capital, which is an extremely powerful player in commercial aviation.

As for Pratt & Whitney it is part of United Technology, which is very well positioned right now in commercial aviation manufacturing. Especially since its acquisition of Goodyear. It also has a strong military base, which is no longer the case for RR.

But on top of all this P&W has recently developed the most promising engine concept in years. It has already taken a strong lead with the GTF. And the advantage of the technology behind it is that it is scalable. The bigger the engine is the more efficient the principle becomes. It is therefore almost a certainty that P&W will soon start to make interesting propositions for the widebody market.

Recently RR sold its rights to P&W in the IAE consortium. This indicates to me that P&W is stronger financially than RR is. That being said RR remains a force in commercial engine that P&W is only aspiring to become again. But that day is fast approaching, while RR remains vulnerable financially.

As we entered the 21st Century the world economy was changing rapidly. The US economy still remains the strongest while other economies are developing at a frightening pace.

Brazil has almost 200 millions citizens now. The well developed Europe counts over 700 millions people. While China and India are each well past the billion. There are only two manufacturers right now to answer this increasing demand for air transportation.

That explains why the order books of Boeing and Airbus hold such impressive figures. Thousands of airplanes, year after year. It has continued unabated even after one of the greatest economic debacle since 1929. All that is telling me that time is ripe for a third force to enter commercial aviation.

That is exactly what the engine makers would need: a larger variety of platforms to bolt their engines on. And it would also be an opportunity for the airlines to recover some of the leverage they lost when MD and Lockheed vanished from their radar screens. They actually can already see one or two dots pupping up over the horizon…

Cheers!

Normand

I do agree with your comments on PW. At the moment it is a very weak player in commercial engines, but has survived on the military side and yes the GTF may switch its position in comming years. And it greatly benefits as part of UTAS.

I see less commercial platforms in the future, not more. I think you will see 4-6 TA platforms: 787/A330, A350/777. The wild cards are if/what happens if there are one or two offerings in either <250R pax and 400+ pax markets that are not derrivatives of the other four. The A380 will go unconstested for now and may be replaced by a very large twin down the road. There will only one or two engine offerings on each platform. SA's there may be 3-4 at most.