Leeham News and Analysis

There's more to real news than a news release.

Boeing 787: Stable Rate, Hike Rate or Cut Rate

Aug. 2, 2016, © Leeham Co.: Boeing officials increasingly downplay the prospect of the 787 production rate increasing to 14/mo by the end of the decade from the current 12/mo, reflecting uncertainty over the strength of the wide-body market in the near-to-medium term.

Dennis Muilenburg, CEO of The Boeing Co., said during the company’s 2Q2016 earnings call July 27 that “we haven’t pinned down a specific decision point [on ramping up to 14/mo] yet because we’re going to keep a close eye on the market. The signals from our customers, we’ve got time to do our due diligence here.

Figure 1. Boeing 787 Orders and Deliveries. Click on image to enlarge.

“Our principle here is to keep wide body supply and demand in balance. And we’re confident in the 787 program across that span of scenarios, and we’re going to continue to work campaigns to fill out to the 14 a month rate step-up, and we’ll evaluate timelines and decisions around that. But you can be very confident that whatever we decide, we’re going to keep supply and demand in balance. We’re going to do it efficiently and productively, and all of this again is enveloped by our expectation of a year-over-year cash growth business.”

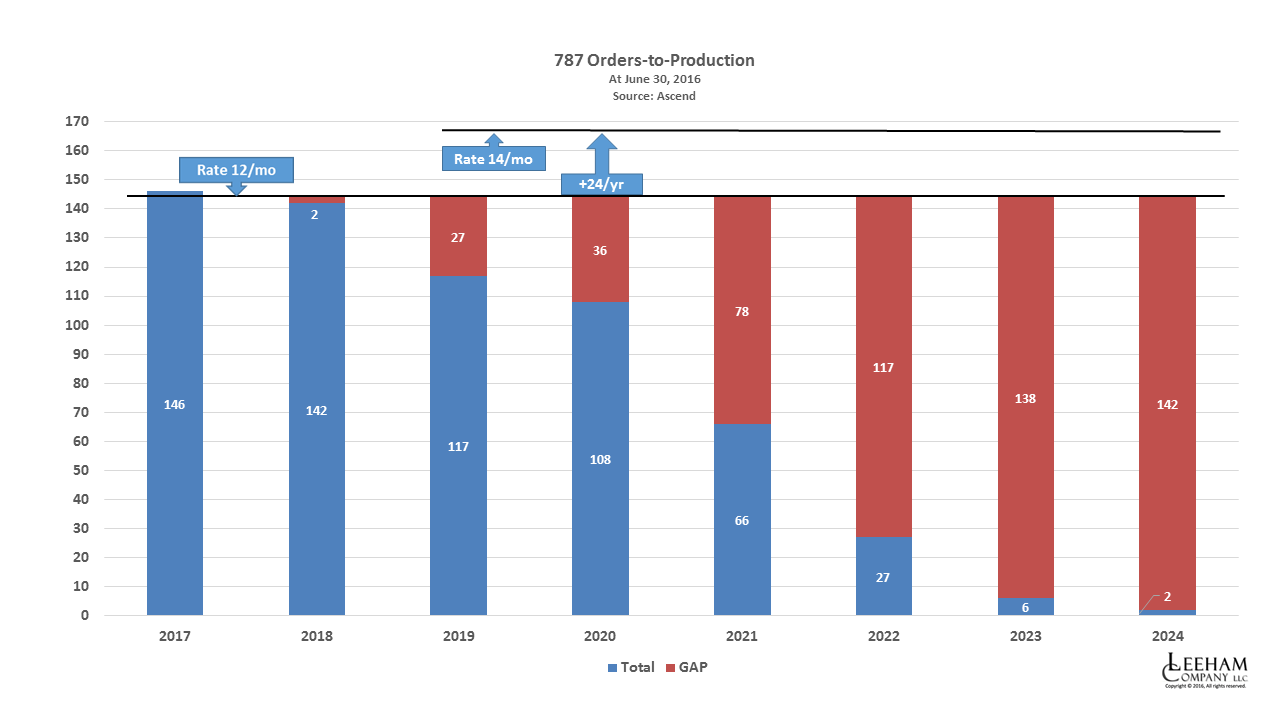

Boeing noted that the program is sold out in 2018 and has some slots available in 2019. At rate 12, the likelihood of these slots being filled may be challenging. Although the number itself isn’t great—27, according to Ascend—finding enough customers for delivery in 2019 could be challenging in the current soft environment, and with competition from a much lower priced Airbus A330, whether a CEO or NEO. The challenge becomes greater the farther out in the future.

If Boeing went to rate 14, this is another 24 airplanes per year that have to be sold. (Figure 1.)

Slowing sales

Figure 2. 787 production rates and gap. Click on image to enlarge.

Looking at the book:bill trend since the 787 entered service in December 2011, Boeing has good reason to be cautious about upping the production rate. The last time Boeing sold more 787s than it delivered was in 2013. The book:bill rate was just 0.73 last year and so far this year, it’s an anemic 0.25. This could change dramatically if Boeing becomes the winner in the long and heated contest for the Emirates Airline wide-body order expected before year end. The 787-9/10 are in competition against the Airbus A350-900 for at least 70 aircraft.

But even if Boeing wins this order, the book:bill rate will be well below the production rate of 144 airplanes a year, absent other orders. In fact, since the 787’s EIS, there has been only one year (2012) once full deliveries ramped up when the book:bill exceeded one. (Figure 2.)

Analyst reaction

Analysts on the 2Q earnings call were quick to note the caution flag raised by Muilenburg and CFO Greg Smith. The following two excerpts from research notes issued after the call are typical.

Credit Suisse wrote:

Realistic commentary on 787 rate and 777 bridge: Although a debate on the prudence of a further rate hike to 14 for 787 rates has been ongoing for a few months, BA spoke to the possibility that it may not happen if the company deems the backlog does not support an increase. While this would extend the deferred recovery by ~six months as per CFO Smith, we view the difference as minimal. However, we think there could be some unit profit impact toward the end of the block due to fewer units absorbing fixed costs, which we think could possibly result in a charge at decision time. BA does not see the decision time regarding the rate for another couple of years. On 777, CEO Muilenburg acknowledged that the current sales pace needs to accelerate even to meet reduced targets of 7 per month in 2017 (80% sold out) and 5.5 per month in 2018 (60% sold out).

JP Morgan wrote:

On the 787, Boeing is reassessing plans to raise production from 12 to 14/mo by the end of the decade to ensure supply and demand are properly aligned, a move that makes sense in our view, given the demand environment, even if there is no need to foreclose the possibility yet. The next question, however, is the sustainability of the 12/month rate into the next decade but this is still several years away.

Burning off the backlog

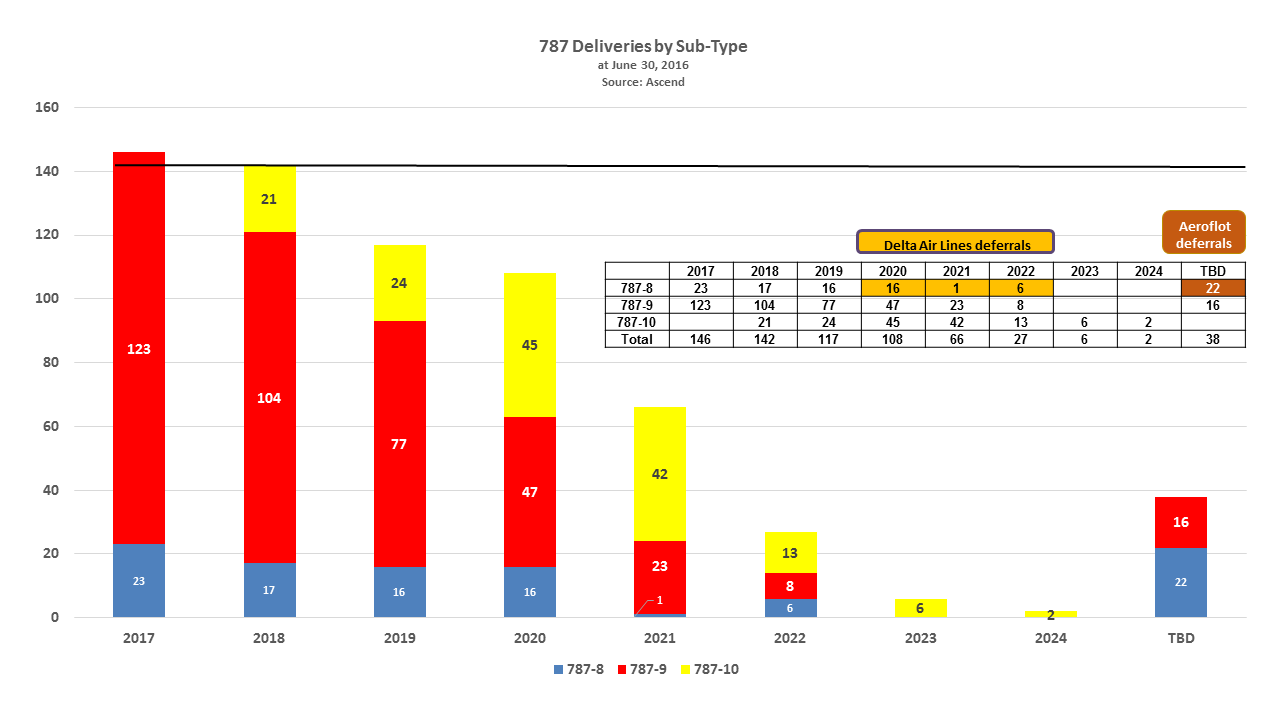

Figure 3. Future 787 deliveries by sub-type. Eighteen Delta Air Lines 787-8s 2020-2022 are questionable. Click on image to enlarge.

With a book:bill history of less than one, Boeing is rapidly burning off the backlog at rate 12. There were just 742 787s in backlog at June 30, according to Boeing’s website. There is an emerging production gap, as one would expect the farther out the future. However, by 2020, Boeing’s production gap really kicks in. (Figure 3.)

Although by the numbers Boeing is scheduled today to deliver 108 787s in 2020, 11 of these are 787-8s ordered by Northwest Airlines, now part of Delta Air Lines. Delta deferred these several times and is known to not want the 787-8s. The others are for Iraqi Airways, hardly a solid order, and Biman, which may also be iffy. This reduces the likely 2020 deliveries to 92 vs 144 production slots. The 2021 and 2022 787-8 deliveries are also for Delta. The 22 TBD 787-8s are those for Aeroflot, which has all but canceled this order.

Stable Rate, Hike Rate or Cut Rate

Boeing’s caution against raising the production rate now becomes clear after looking at the numbers and considering market conditions. These factors clearly argue for maintaining a stable rate of 12/mo.

The question that arises, however, is whether rate 12 is sustainable—or whether the production rate may actually have to be cut in the not-too-distant future.

Boeing sold 1,155 787s through June 30, leaving 145 to be sold in the 1,300 accounting block to achieve program break even. Boeing needs to sell 65 aircraft in 2018-2020 to fill the production gap (81 if one discounts the 16 Delta, Iraqi and Biman 787-8s). The number rises to 260 through 2022 (or more, throwing out Delta, which has a total of 18 787-8s on order).

(It should be noted that there are about 70-80 orders for delivery beyond 2020 that are not in the accounting block, which LNC understands extends only through 2020 at this time.)

Based on history, the raw numbers are achievable. The more important question remains: what will the delivery streams be if these numbers are reached? The streams will dictate what production rates will be in the future.

There are at this early date all sorts of variables and caveats to consider. But it’s also time to start thinking about the What Ifs.

the first graphic is a bit problematic via the quantisation difference ( 12m vs 6m). This does not ring into the book2bill ratio.

Giving year wise average per month numbers could be a fix.

( Deliveries would with ~12.5 overreach 2015 numbers (~11.25) while orders go from 8+ down to ~3)

I think the problems with 787-8 have caused the market to narrow. This raises the question: Why hasn’t Boeing retrofited the -8 with the changes made to the -9 and -10? The -9 and -10 are superb aircraft. Is it that much money?

Would you then have to write off the development costs of the 788?

I mean 788mk 1

Excellent article with clean but informative graphics.

Agreed.

I have had that on my radar for a while now, I did have to laugh, only 744 back ordered!

Reality is that its about when not totals, so they may have to throttle back to rate 8 as time goes by and that’s still good.

Its not going to stop, it has a great future.

After all, all the tooling is paid for, it doesn’t cost them anything to make it (grin)

This debility goes further than being unable to copy a name ?

If Boeing can deliver the 787-10 at a good price it will take over a big chunk of the market as it would be the most efficient Aircraft for many routes, can it survive the cycling most Chinese/ India domestic big city routes will fly it some years from now. But building them cheaper than Airbus A330neo’s can be a challange.

Shame they mucked the program up so bad

It is completely impossible to bring production cost even close to the A330. CFRP is significantly more expensive to purchase and process than aluminum.

I am not only a big fan of CFRP, but we produces violin bows from that stuff every day, but… I think the smart move would have been NOT to make the entire 787 from it, but start with one major part, i.e. the wings. (And of course produce them in-house, as is now the plan with the 777X)

Sometimes it is better to “lend” a good idea than to come up with a new one that might be less good, and the 8-abreast is surely a well chosen sweet-spot.

With such a plane Boeing could have taken on the A330 directly and replace the 767. It would also have been much faster on the market, and at a lower price.

Why would it have been faster on the market?

Fastners !

has everybody forgotten so soon, sure it wasnt the only issue

Removing any single issue would have done nothing for the timeline. though Boeing was rather active in linking select external hickups to “explain” inside delays.

CFRP per weight is more expensive than AL. But AL is machined in a subtractive process ( from billet to CNC machined rib forex ) oftentimes 90% or more of raw material goes to the shavings box.

CFRP is an additive process. you trim the edges, make some cutouts. 90% of raw material goes on the plane.

Obviously applied processes and machinery are rather different. New stuff has to be learned.

All that does not explain the massive miscalculation ( if it ever was calculated and not just a childish footstamping “but I want to” target.) over the complete process chain.

Definitely not limited to FAL transit times.

( initially every three days a finished frame going over ?5+1 contingency? stations for a transit of ~15days. Where is Boeing today?)

@Happyday: Take a look at Intel. They do Tic-Toc in their product development. One step is they shrink the structures (i.e. they change the production), the next step is they change the design.

The decision to change everything at once was what led to all the problems with the 787:

Body made from CFRP barrels – a world premiere

Wings made from CFRP – never done on an airliner before

AL-Li Battery – another world premiere

Mostly electronic systems – a first for airliners

Outsourcing most components and even big portions of the development – never tried before on an airliner

They should have done maximum half of these and the whole project would have sailed a much cleaner line. I think they should 1) have used the 767 facilities and upgrade them to more automatic production (similar to Airbus) for the body. 2) They should have built their own production of CFRP wings. 3) The full electronic systems and Al-Li battery should have tried extensively on an otherwise proven plane, for example on the 777. If successfull Boeing could have offered that as an alternative version resp. as an upgrade. 4) The CFRP barrel body could have been tried on a later project like for example a MOM plane, where only the CFRP body could make a very long and light single aisle feasible.

In difference to Intel, Boeing did not only do Tic and Toc in one go, but also Tac and Tec. This was a terrible strategic decision that might cost Boeing everything.

If they had done it the pedestrian way as you advise ( good advice!) they would never have been able to create that druglike rush that cut Airbus short and filled their orderbook to overflowing.

But Boeing outcompeted Airbus with a fully fledged mirage.

Everything else follows from there.

Sales success on overstatements and project foundering on underperformance are intrinsically joined.

@Uwe: The big joke on all this is that Boeing at the time was possibly feeling very prudent after the SonicCruiser folly. They probably did not understand they were betting the company on a project that was just as crasy and only superficially more reasonable.

Their thinking was not deep enough to comprehend that pushing over “risk” to suppliers (must have appeared such a beautiful idea at board meetings) means that their own product would be at risk in the end (Battery, stabilizers, fasteners,…) and that all the trouble would bite them in their own back.

I get really annoyed when people talk about the Sonic Cruiser as a folly.

You do not understand how an aircraft does (or should, sans the A380 ego thing) to be built.

Boeing goes to the dcustomers and asks them, what do you want.

They did so, fast was the answer.

Boeing designs modern fast.

Ok, here it is, this is what it will cost. Well we really don’t want to pay that for that. Huh?

Well what we meant was we want something that is economical. Hmmm. Ok, how about this? Yea that looks interesting, flesh it out and let us know what it will cost.

Boeing then took the salient features of the Sonic Cruiser (composite and more electric) and used that as the basis of the 787.

If you go back in history, the 777 started out as a 3 engine design and morphed into the killer twin it is now. The original version did not have the range the current one does.

The reality is that things evolve, Eddison did not “invent” the electric light bulb, his assistants spent enormous amount of time testing all sorts of materials to make it work.

You can call the first material a failure if you want, what it was, was a learning experience and each one refined what worked, what didn’t what characteristics needed to have form what was working and what was not.

Boeing did not pull the 707 out of a hat, they took all they had learned form the B-47 and B-52 (which in turn came from B-29) and applied it to a passenger jet.

There was an early version that did not pass muster, not what was needed vs what was coming, so they re-grouped and re-did and it was very successful.

A300 was not a failure though not a huge success either, it set the stage for the far more successful A330.

@TransWorld: Well, that’s not the way I work. What I do is I try to find out what my customers might need and buy in the future (not what they SAY they will need or buy) and see if we can provide that and make a profit on the way. Next step is I check if we have all the required recources and know how, if we can master the technologies, if our suppliers can reliably contribute and then make a master plan. Next is we try to shoot some holes into the plan and see if it still holds water if a few things go wrong. If it still looks good, then I approach my customers and show them what we could make and what it will cost. If they like it plus we can be sure we will be a step ahead of the competition, then we have a go and I will try to collect some orders.

Would you say that is what Boeing did?

Gundolf: We may be saying the same thing from different angles.

Boeing had input from customers that something fast and new was desired. Boeing may have floated it, the customers may have.

Regardless it got interest, a lot of interest.

As an aside, one of the big air cargo operations (Polar or Cargolux) participated heavily in the A380F design. When it came down to brass tacks they were not interested. You would think they would have figured out it did not work for them early.

When the Sonic Cruiser was fleshed out and the costs of production (purchase or correctly) as well as operation were clear, it fell flat on its face commitment wise.

What they did find was the customers liked the overall composites and more electric, just not the speed.

I don’t know what you do, but aircraft are not computers or smart phones, you can’t morph changes quickly let alone afford them not to sell in the first place.

You have to come out with something that sells now, but also in the future.

You can’t go to the board with “I think they will like this” they need commitments (behind the scenes seldom public)

Regardless I have no issue with Saying the Sonic Cruiser did not fly when offered, I do have a problem that it was a bust.

Somewhere in the process both sides got their wires crossed up.

But like most aircraft, it was an iterative process (and granted a major shift) that came out with the current.

Meanwhile Airbus is going to be at 10 A350 / month late 2018 and was thinking going up to 13 / month. In addition to 7 A330, 1 A380 and 14 787 + 5.5 777 + 0.5 747, we have about 40 widebodies per month to be absorbed by the market.

What if the fuel price remains low ?

@birdy

I don’t think it is fuel price driven, at any rate not directly. There are 3 fundamentals at work that have been driving sales in recent years

1 fuel prices – being high favouring more fuel efficient designs, the received wisdom is that they will go north over time but of course the urgency to replace has reduced.

2 zero interest rates – the world is run on funny money as central banks need to borrow cheaply given govt debt and do not know how to create even more growth from a moribund and vastly indebted environment.

3 anticipated global demand – the growth in the need for new aircraft due to more passengers flying.

Of these the fuel price is the shorter term issue as it may rise or fall for any number of reasons, the eventual rise in interest rates is a medium term issue and the anticipation of global demand is a longer term issue.

Given the enormous boom in orders in recent years some sort of slow down was always on the cards. I feel that lessors are running slightly scared of the potential medium term future and that there will be a shake out.

At current fuel prices the decision by British Airways seems prescient as they can extend out their 744s to their full life. In fact all those elegant 343s and less elegant 346s suddenly have a new lease of life.

40 WB aircraft a month seems way off what the market needs IMHO and therefore the battle for orders is going to become a bloodbath for the OEMs. How low can prices go?

There is a small but fatal assumption made by you:

airlines order widebodies without looking at narrowbodies.

In my opinion no airlines cares about the number of the aisles as long as boarding works. One, one and a half, two, three

For the 787 with the loss of the -8 the seat count for the 787 starts around 280 seats. Medium range routes with low density 787-8 seat count could be served by an A321LR.

So true. The in seat entertainment matters more to passengers, who are mostly in blocks of 3 seats, twin or single aisles. It reminds me of the old battle in cars, front or rear wheel drive- who cares any more.

bastardized conceptions.

Either some kind of 4WD was done or the basic one axle driven concept was engulfed in little helper appliances.

( using brakes, difflocks, steering overlay, whatnot.)

You see the same in the petrol vs diesel wars. Todays engines have from two directions reached similar pressure ratios for similar efficiency by applying design elements of the competing technology.

And is Airbus going to have to throttle back. Someone just deferred A350 deliveries. Too much of that and……

Once Emirates and Turkish announce their large orders, most of this nit picking about orders will largely be forgotten…

Why would anyone think orders would suddenly dissappear. ..

Just look at the current order book..So many unposted orders..

I guess everyone forgot about china eastern (15),a slew of new -9 orders from Chinese carriers..will they ever post hainans -9 order?

When Boeing finally does decide to post them, im sure , the backlog won’t look so bleak after all.

When Boeing finally does decide to post them, I’m sure , the backlog won’t look so bleak after all.

Or as may happen just a re badge of “undisclosed customer” bookings.

Oh well, Turkish might not annouce anything big so soon now.

Airport hassles are bad enough without having the security more real than just a queue.

TC: What you want is steady sustained orders. I don’t think its a crisis per se, but they may have to throttle back to maintain a steady flow.

When you get to rate 8, you don’t need Everett as Charleston can do that (and Everett can’t do the 10)

Boeing has only three products that work right now: the 737 MAX 8, the 787-9/10 and the 777-9X . The 737 is, or was until recently, selling like crazy. We don’t know how long this bonanza is going to last though. Perhaps not long enough for Boeing to compensate for the losses incurred on the 787. This situation is unfolding over a period of many years when all kinds of things could happen. And there are already signs that we may be entering into a bear market for commercial aviation. This could not happen at a more inappropriate time for Boeing. Perhaps less so for Airbus. For sure if it happens it’s going to kill the A380; but Boeing is now facing a much more serious threat; and I am not talking about the end of the 747 here, but about the end of the 737, which in my opinion might be coming faster than Boeing needs to survive in this negative-growth period for the 787. Like if this situation was not difficult enough, the 777 is arriving at a slump period of its own at the very moment the other two leading products will likely be facing strong headwinds.

WARNING: The road ahead might be slippery and rocks might be falling. Only an avalanche might save Boeing, but that would have to be an avalanche of new orders.

Are you really sure about 777-9X?

The first 777-9X will not be delivered next year.

Boeing will not make any money before 2030.

Way to go.

“Boeing has only three products that work right now: the 737 MAX 8, the 787-9/10 and the 777-9X ”

I looked up 777-9 sales, it has been “relaxed” over the last 2 years.

https://en.m.wikipedia.org/wiki/Boeing_777X#Orders

The 777 situation is the exact opposite of what it is for the 737. The latter sells in great numbers, but has no future; while the former doesn’t sell so well right now, but should have a great future. If it was not for the 777, the 737 would slowly kill Boeing.

You are forgetting , its the engines that airlines worry about, not when the wing or fuselage was made or whether it comes out of an oven or a riveting machine.

Normand: You roll the 787-9 and 10 into one, and then cut out the 737 to a single (there is the 7X and possible -10)

Is the A320 series one product or two?

Boeing has the 777-200, 300, F as well as the 777-8 and 9 (8 being an adjunct like the 737-900/9 as it will not stand alone.

In reality Boeing has the 737-7x , 737-8 and the 737-9.

If people would look past the Boeing rhetoric, the 737-9 is NOT an A321 competitor, but it is a nice adjunct to the 737 line and doing nicely from that standpoint (low cost to develop )

Both A and B will be affected by a downturn. There is a bubble and like all bubbles it took longer to burst than I thought it would, inertia is an interesting thing.

Only a high production rate could bring the 787 into positive cash flow territory. But this would only be possible if the number of new orders was high enough. What we want to know is the minimum rate of production needed to make the 787 profitable. We already know that Boeing needs an exceptionally large block of orders to absorb its deficit, but this block is likely to melt away fast if new orders don’t come in to replenish it. This may force Boeing to write-off a huge amount of money on the Dreamliner programme if the trend doesn’t change.

We do know that the 787 @12/month is currently manufactured at slightly above ( conventional bookkeeping ) cost. i.e. deferred cost stay constant. This for obvious reasons is not an acceptable state.

Gains from scaling are more or less done

Gains from learning / optimizing should still be available in modest amounts.

Gains from leaning on the supply side are wide open.

( easy, cheap, beancounter accessible “duh, obvious” and will be overused resulting in some rather unpleasant breakdowns in the future frustrating the objectives B should follow longrange. “Supersaver” Ignatio Lopez nearly killed VW at the time.)

Normand:

At issues is the excess build capacity. Charleston alone can do Rate 8, and is the only place to do the -10

That would be a good opportunity to the do the MOM in Everett though.

Have to see if Boeing is still pulling shenanigans or has realized scattering you plant all over the US is not a good idea.

Wherever they do the MOM, if they do it it will become a classic case study for MIT and Stanford students as an example of the kind of decisions that can be made which can ultimately bring a company down.

The pacific N.W. is at risk (what % per year not well estimated I believe) of a great earthquake and sea wave which will take (a lot of) years to recover from. Diversification away from there may be justifiable for that reason alone.

Ok, diversification is nice.

Lets see, all 737 goes down, all 767, all 777.

1/4 way diversified does not cut it.

That does not include the fact that Boeing management clearly stated that they were opening up Charleston production because of the Union, not diversification.

Japan has the same issue and without Japan 767 and 777 production comes to a screeching halt.

Diversification costs and as we have seen, it has added a huge amount to the 787 program.

@MHalblaub

“Are you really sure about 777-9X?”

– Yes I am sure about the 777-9X. Perhaps I should say that I believe in it, for it hasn’t flown yet. I must admit though that it is a little ambitious without being a clean-sheet design; i.e., it’s going to be expensive to develop without bringing all the benefits of a brand new design. But it is a very potent aircraft, of which Airbus has no equivalent just yet. The jury is still out on this though. What I am less sure of is the gestation period that will give a new lease on life to this baby. The amount of risk involved with this upgrade is almost as high as it was with the 787. And most of the risk involves the wings. Until now Boeing was outsourcing its wings, but decided this time to in-source it. That is where all the risk is, because Boeing is starting from scratch and the task is huge. I believe it is the largest composite wing ever made. It would have been less of a challenge if Boeing had hone its skills on the smaller NSA first. So, no I am not so sure after all.

“Boeing will not make any money before 2030.”

– I assume you mean that Boeing will not make any money on the 777-9X before 2030. But I take the larger view that Boeing will not make any money in 2030, period. Because they might no longer be in business by then. Okay, I am exaggerating a bit, like I alway do. What I would like to emphasis is the fact that Boeing will be strapped for cash for an extended period of time. I expect this to start to happen at the turn of the next decade. And like you suggest this situation may last until the 777 becomes cash flow positive again.

The size of the wings is likely the reason in was done in Seattle, too big to fly around the world, and Boeing hasnt barged anything to Seattle since the early days of the 747.

Remember they don’t have a tip.

folded span is 65m. subtract wingbox width,

divide by two and you are below 30m.

The slightly upgauged Beluga XL has no issues moving a pair of outfitted nonfolding A350 wings. ( up from one for the existing 600ST Beluga.

The reason they make the wings is that they finally understood that making the wings and the body is what makes you a plane maker. Outsourcing both does not only give the profit for both away to your suppliers but also a good part of the technology and control over pretty much everything. Do you think they want to repeat the 787 desaster with the 777?

But even if they don’t posess so much strategic intelligence – if they have asked Mitsubishi for an offer to make those wings they will have found out that the 777X would not be profitable ever.

It all depends on trade agreements and lobbying in the end. The cat next door knows you dont want to be flying in a Chinese made aircraft. Its not really a technology giveaway they need to worry about, though that doeent help. Its that the Chinese will eventually be able to export US technology back to the US and use dumping to guarantee you cant compete without transitioning to Communism.

“dukeofurl

August 2, 2016

The size of the wings is likely the reason in was done in Seattle, too big to fly around the world, and Boeing hasnt barged anything to Seattle since the early days of the 747.”

Significant parts of the 767 are barged from Japan, center fuselage amongst them.

They are doing the wings in house so as to develop their internal capabilities. Does anyone know how much of the tech and knowledge Mitsubishi has gained with the 87 wing is shared w/Boeing per contract or otherwise? It’s the 87 wings they “should” have done in house to be the world leader in this.

Like Normand I’m a big fan of the 779. I only wish they had launched it sooner (before the 300ER was so clearly threatened by the 350-1000) which would have limited the production gap between the 300ER and the 77-9.

They are building half a clean sheet aircraft with the 77x which is probably prudent, but risky because while (supposedly) 4″ wider inside than 77 it is still a tight 10 abreast aircraft’ more like a good 9-1/2 (kid seats anyone).

It seems to this aircraft fan-person that once they get it ramped up they should straightaway start the development of a new (presumably composite) fuselage and wing box to go with the great new wing. Give it an internal width of 20′-4″ to have a real 10 abreast aircraft. Make it in say 72 and 80 meter lengths (maybe even put the cockpit in a 747 hump so the whole main deck can be used for passengers and an extended upper deck added later) and you would have a real category killer and probably stop Airbus from building a super twin of their own which would kill the “current” 77-9 and 10. Just a fan-person dream! but maybe.

The question is, would the 777-X have created a production gap sooner?

Hey TW

I am thinking that the large WB market has been more moribund and for longer than anyone imagined. The production gap on the existing B773 and the lack of recent significant orders on the A351 and B779 may just suggest that in a time of uncertainty none of these aircraft is worth risking from an airlines perspective (Emirates excepted).

It seems we are destined to be flying only A359 and B789 (maybe the odd A330neo) until matters resolve themselves

Rate 14 has to happen or the nightmare is prolonged for the Dreamliner, the pain deaded by yet more forward charges taken on the programme.

The 787 will have to be improved, time does not standstill. Ploughing money into research for a loss making programme only adds to the bottom line. Let’s call a spade a spade. Till it goes past its accounting block, the 787 is a loss maker.

Running two production lines requires a high output to make the whole thing financially viable. 12 aircraft/month from two production lines? Really? How many 350 are Airbus proposing from one line as a comparison?

Hindsight et al but if only Boeing had the 787 do what they said it would do WHEN they said it would do it?

How many 350 are Airbus proposing from one line as a comparison?

Airbus FAL line isn’t really a hard line setup like B uses.

It is “widened” per station ( following demand ) i.e. they replicate select stations for work flow in parallel.

( and some stations also flexibly share flow from the A330 line and the A350 line. )

It is actually very probable that the 787 will never be profitable, as long as Airbus is around. From all we know the A350 is cheaper to produce although it is bigger, and the A330NEO is much, much cheaper and offers almost the same performance. This is the reason why orders for the 787 have slumped in 2014 when the A330NEO was introduced.

Assuming a bearish market for the next couple years you will find the production rate of the 787 between 5 and 8 a month and one of the lines closed.

Ebbuk: No Rate 14 does not have to happen. If not its the way the world goes.

Boeing is not going to deliver 5 or 6 white tails a month (can’t afford to)

They can write off the whole 787 program (Bjorn, can they with their accounting method?)

IF Rate 8 as I predict is what keeps white tails off the tarmac, that is what they will do.

It will hurt them, but not as bad as the alternative.

The commonality between 787 models has been raised by LNC before

“The -9/10 are about 90% common, but—depending on who’s doing the talking—the -8 may only be about 40% common to the -9.”

leehamnews.com/2016/03/21/pontifications-787-8-no-longer-favored-boeing/

Boeing has given a higher figure -95% -for the two larger versions.

“Scott Fancher, vice president and general manager of Boeing Airplane Development, put the total at 95 percent in a recent Aviation Week report.”

having the same takeoff weight is probably the key here.

The difference for the 787-8 seems staggering if its the lower number, as you would expect it to be in the region of 85-90%

Previously its been noted that the 787 cockpit windows assembly was changed from titanium to aluminium , with a reduced parts count.

So Im considering if the commonality is based on an absolute part count, which over emphasizes small differences , ie bolts may be one size larger but the sub-assembly is otherwise identical, rather a completely different part?

We would need a super computer to do all that. Enough to make your head hurt.

I think we have to go with the essence of Leeham, the -8 is an orphan and will stop being offered when the backlog is done.

If demand is there down the road it might be a variation of the -9, not sure that is economically possible.

@TransWorld

“You roll the 787-9 and 10 into one, and then cut out the 737 to a single (there is the 7X and possible -10).”

– The 787-9/10 are like a single model to me and I believe they have a great future ahead, despite their troubled past, which can be blamed mainly on the -8. As for the 737 it has only one interesting variant, which is the MAX 8. I do not consider the -7 and -10 as viable products. For one thing, try to imagine an A321LR without cargo containers! With the -10 we only get a bulk cargo, and an extra-long one that will require an army of specially trained rats to retrieve luggages. Very few airlines will want to carry this many passengers, that far, without the possibility to carry cargo along with it. It could be a good aircraft though for low-cost vacationers. But Boeing will never retrieve its investment.

“Is the A320 series one product or two?”

– The A320 is one product and the A321 is another. The latter (neo+LR) has no equivalent at Boeing, while the former has a stiff rival with the MAX 8. And the latter will quickly become an orphan, unless the 7.5, 9 and 10 become successful. They better be, otherwise it will be a lot of money and time wasted. In my not so humble opinion the 737 is kaput, and if the 737 is kaput then Boeing has a very good chance to be kaput as well. There is a lot at stake here and important decisions are about to be made.

“Both A and B will be affected by a downturn. There is a bubble and like all bubbles it took longer to burst than I thought it would.”

– As for the downturn, that’s what it is, a downturn. The bubble is not about to burst because there has never been a bubble. We were until recently into a growing market. It looks like it wants to slow down a bit, but it hasn’t reach its potential yet and things should pick up again as soon as the world economy gets going again. But don’t hold your breath.

I will argue that the A320 and A321 are the same aircraft different revs.

I believe that Airbus wanted to have more “models” so rather than having an A320-200 and 300 (and then variations of those as time went on) they went with two ids for the same model and only difference is one is starched.

As for the market, its been jacked up by low interest rates and high fuel prices, high fuel is gone and it will go back to historical norms, ie. there will be peaks and valleys and its going into a valley and its going to be a deep one.

“I will argue that the A320 and A321 are the same aircraft different revs.”

Of course they are; the same way that say a CS500 would be the same aircraft as a CS100. But we are still talking about entirely different beasts here. For the difference between an A320 and an A321 is big enough to easily squeeze an A320.5 in between. And the latter is what the A320 should have been all along. Theoretically we could say that the A318 and A321 are the same aircraft, but even if they belong to the same family they differ so much as to be considered two different models of aircraft. The 787-8 is very different than the 787-9/10, and the Comet 4 was also a very different aircraft than the Comet 1, yet they can respectively be treated as the same aircraft. This sounds like an academic discussion to me.

Pingback: Pontifications: A good week for Boeing wide-bodies - Leeham News and Comment