Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Leeham News’ approach to the news

- Leeham News and Comment will be on holiday Dec. 24, 2016, through Jan. 2, 2017, barring major breaking news. Merry Christmas and Happy New Year.

By Scott Hamilton

Dec. 19, 2016, © Leeham Co. Two thousand sixteen is almost over. This will be my last Pontifications of the year.

We approach our job with a little different perspective than the daily newspapers and aviation trades. They have greater resources than we do and have a greater ability to report the news. So LNC tries to bring news with perspective that those outlets don’t.

Analysis, economics, forecasts

We provide analysis of events and of aircraft economics and performance. Not even the trades do the latter. We also make our own forecasts of trends and production rates. Sometimes it takes a few years to be proved right or wrong. So far, we have a good track record of being right.

We’re also not afraid to take on controversy—and be controversial. And we don’t hesitate to call bullshit when we see it.

This gets often us into hot water with the subjects of the controversy.

This is what sets LNC apart.

Cutting production rates

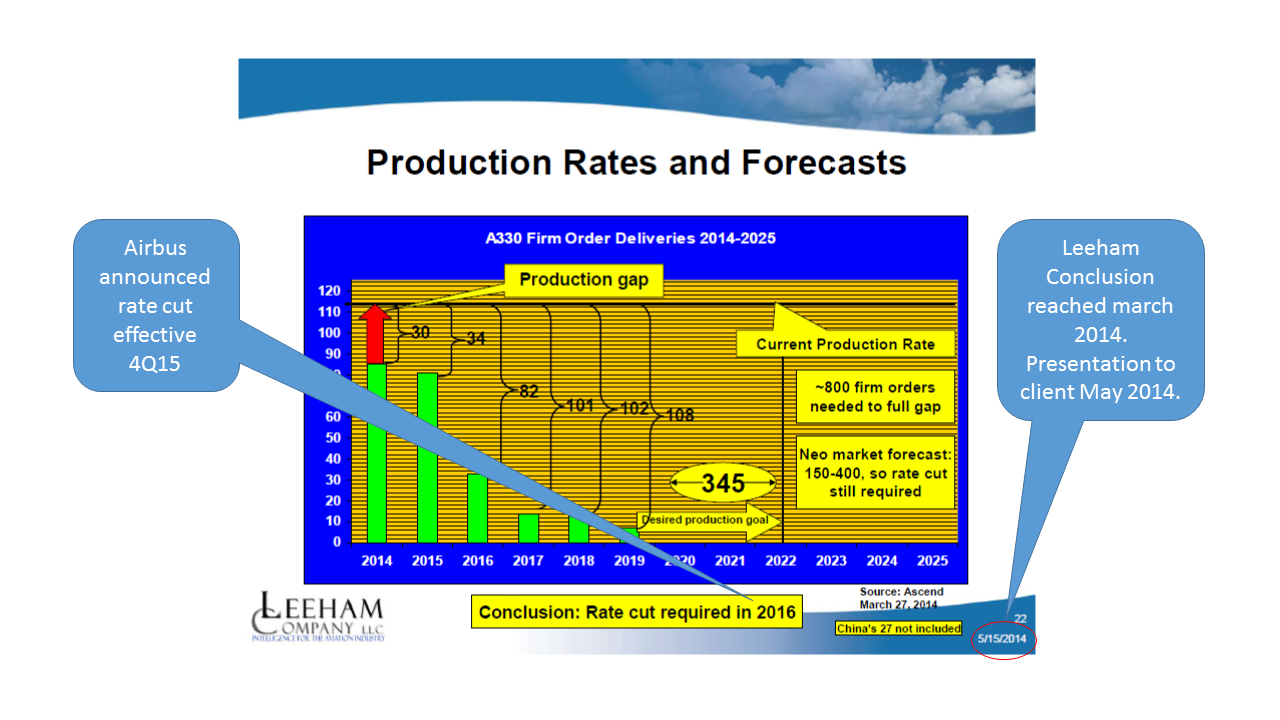

Leeham Co. identified the A330 production gap in March 2014 and predicted a production rate cut for 2016. Click on image to enlarge.

As early as March 2014, we began predicting production rate cuts would be necessary for the Airbus A330 and Boeing 777.

Production rate cuts are sensitive to the companies. It signals weakness in future sales. It means lower revenues and lower cash flow.

We looked at the sales history and production rates of both airplanes and concluded rate cuts were inevitable by 2016 for the A330 and 2016 or 2017 for the 777. Airbus cut the A330 rate in 4Q2015. Boeing trimmed the 777 rate the first time in December 2016. Last week, it announced another rate cut effective in August 2017.

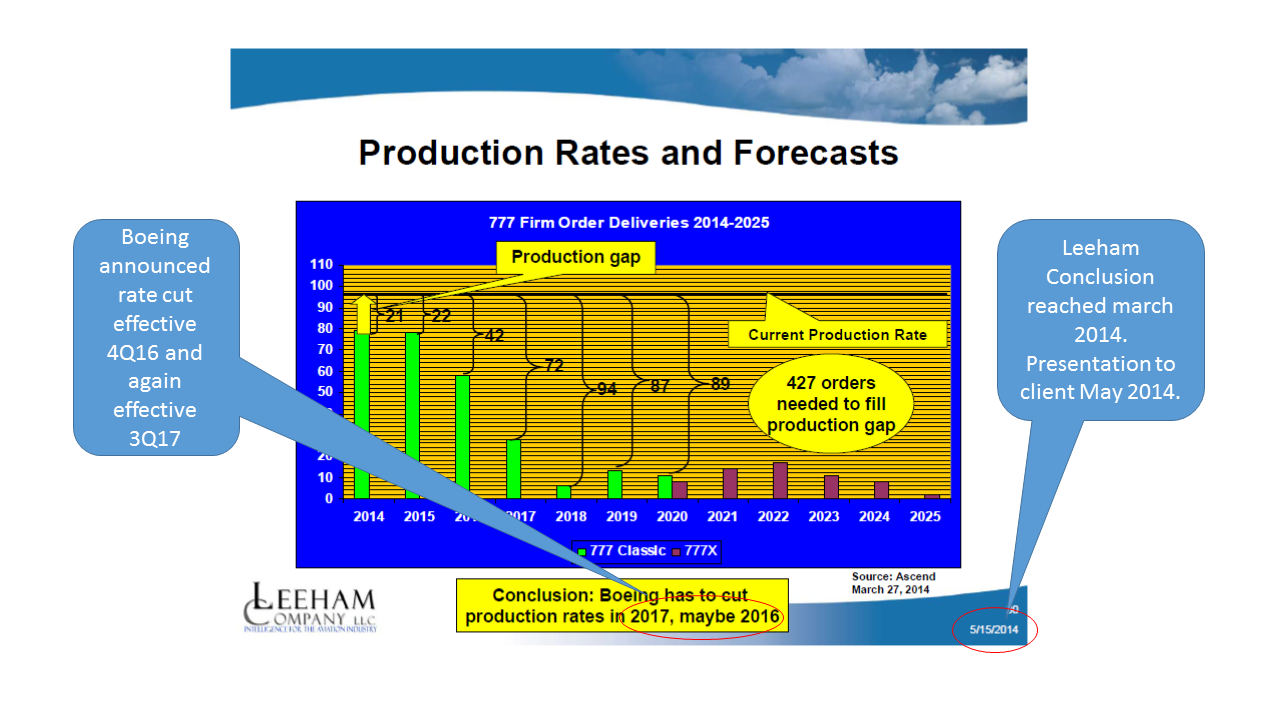

At the same time, Leeham identified the production gap for the Boeing 777 and predicted a rate cut would be necessary in 2016 or 2017. Click on image to enlarge.

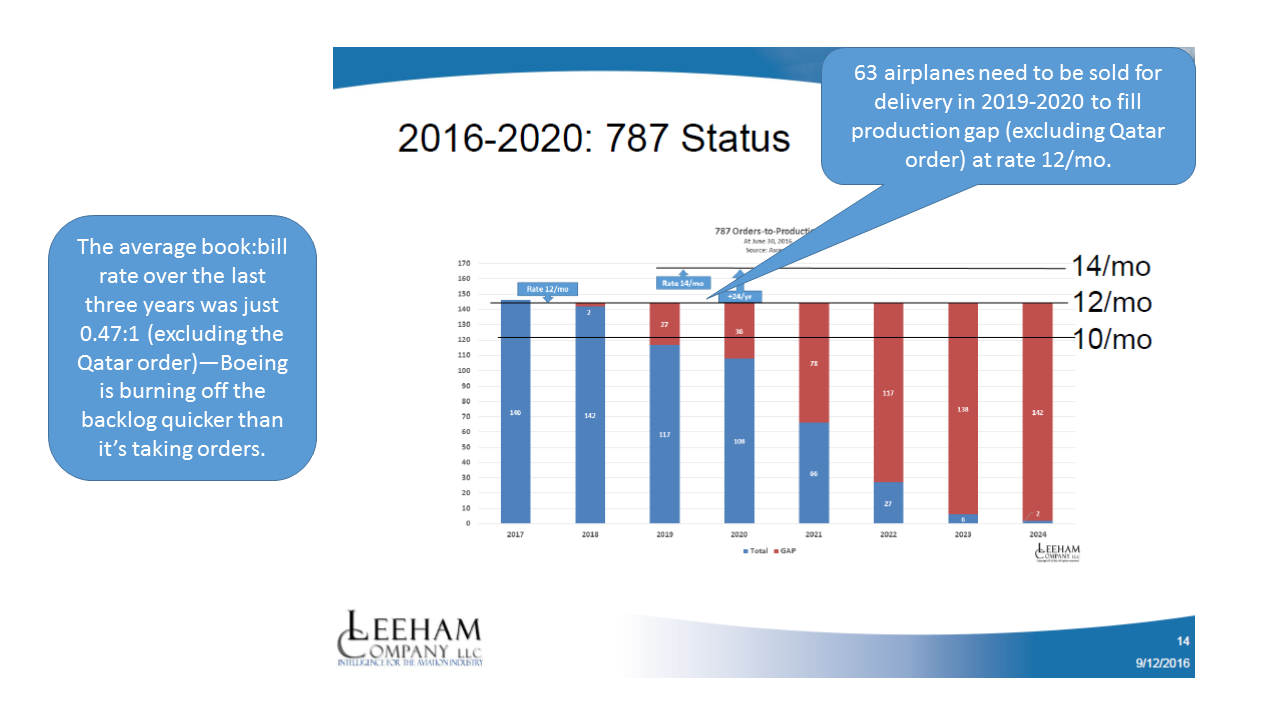

787 rate cut possible

Using the same methodology, we see a potential production rate cut for the 787 in 2019 or 2020 from 12 to 10/mo. There is a production gap of 27 and 36 airplanes respectively (before taking into account the Qatar Airways orders this year). Over the last three years, the book:bill sales for the 787 was only 0.47:1 (before Qatar). This isn’t enough to sustain rate 12.

Reflecting this weak sales demand for the 787, Boeing recently decided not to extend the accounting block from 1,300 to 1,600. This is a necessary move to help recover the $27bn in deferred production costs for the program. (Add $3bn in deferred tooling costs.)

Boeing is burning off its 787 backlog faster than it’s making sales. A production rate cut in 2020 seems possible. Click on image to enlarge.

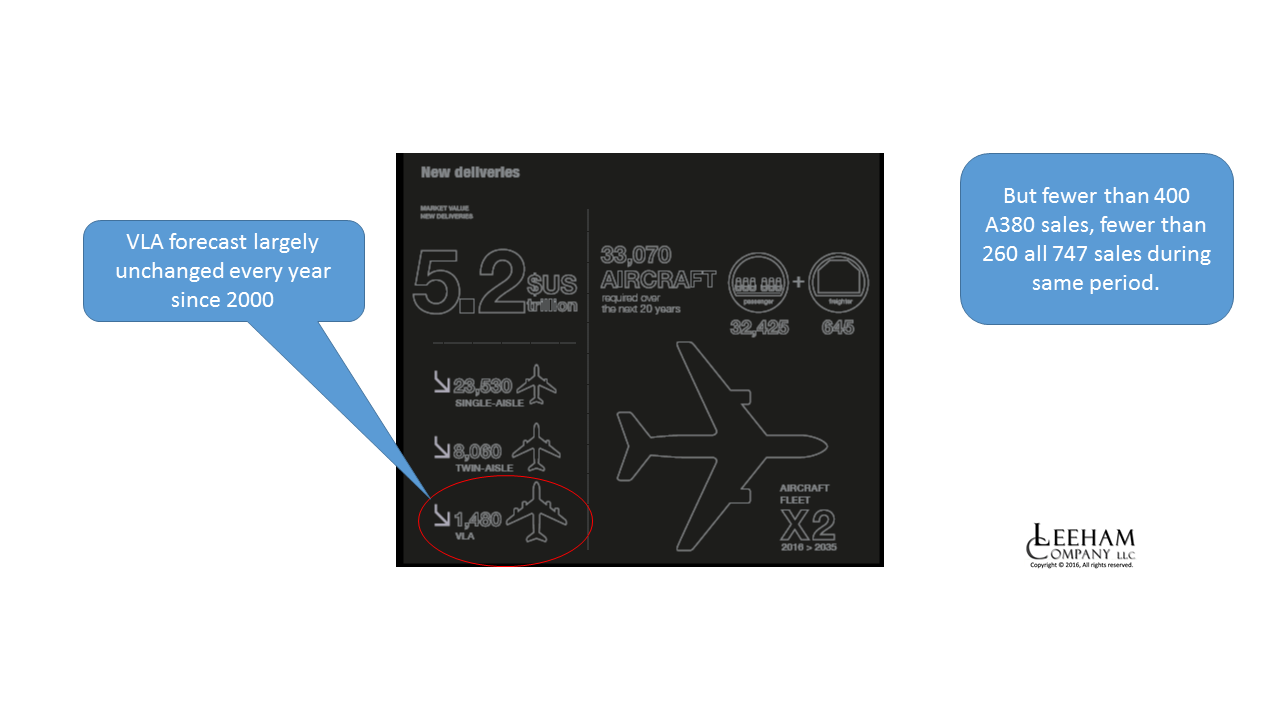

A380 forecast

The debate over the demand of the Very Large Aircraft (VLA) sector was a hot one. Airbus stubbornly sticks to its 20-year forecast that there will be a demand of 1,200-1,700 VLA-Passenger and VLA-Freighter aircraft (depending on the year of the forecast). Boeing’s forecast has been in a steady decline.

Airbus today pegs the 20-year demand at 1,400. Boeing is down to less than 600.

We’ve criticized the Airbus forecast for its relatively unchanging view since 2000, when the A380 program was launched. It’s simply unrealistic in the face of the development of the 787, the A350 and the 777X—all of which serve to further fragment global routes that were already being fragmented by the A330 and 777-300ER.

Airbus hasn’t significantly changed its 20 year forecast for Very Large Aircraft since 2000, despite the development of the Boeing 787 and 777X and Airbus’ own A350. Click on image to enlarge.

Since 2000, Airbus and Boeing sold about 600 A380s, 747Fs, 747-400s and 747-8Is. This is less than half, over 16 years, of the original 20 year forecast by Airbus. Sales of the VLAs dried up in recent years. Yet Airbus sticks with its optimistic (and unrealistic) forecast.

Airbus’ 319 A380 sales to date compare with total program sales of 650 it forecast, according to the lawsuit between Rolls-Royce and Pratt & Whitney that was filed several years ago. Airbus figured it would capture half the VLA market. It’s capturing almost all of it today.

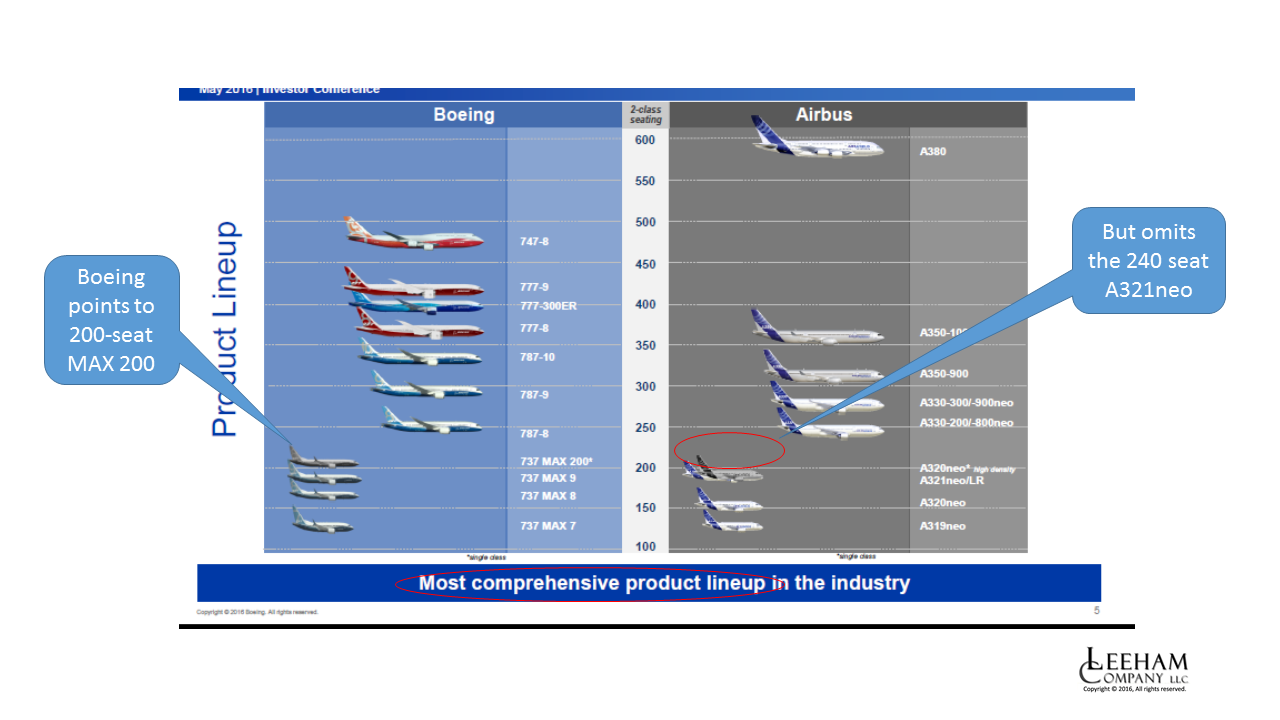

Playing with data

Airbus isn’t the only one to play with data. Boeing is notorious for doing so.

Boeing disappeared the 240-seat Airbus A321neo, leaving the impression Airbus has a product gap that doesn’t exist. Click on image to enlarge.

As far back as 2010, we pointed out that assumptions used by Airbus claiming an advantage for the A330 (this before the neo) over the 787 were skewed.

LNC on many occasions challenged Boeing’s public presentations in which it compared its airplane data vs Airbus. Invariably, the Boeing data was pumped to look better than Airbus.

Look at this example, taken from Boeing’s May investors’ day, during which officials touted the most comprehensive product line in the industry.

Boeing completely omitted the A321 240-capacity version while including the 737 MAX 200, including instead the 168-seat A321LR international configuration.

This left a capacity gap for Airbus that doesn’t exist, while touting a smaller gap in Boeing’s own product line.

New candor and new questions

The ascension of Dennis Muilenburg as CEO of The Boeing Co. brought more candor than existed under former CEO Jim McNerney. The appointment of Kevin McAllister as CEO of Boeing Commercial Airplanes is new enough that no indication of his candor can be assessed yet.

Perhaps the New Year will answer the questions of McAllister’s direction.

Happy holidays and come back refreshed for more analyses and reports in 2017 for us

Keep on doing the good work. Being independent is much harder then consistent communicating what a certain target group wants to hear & won’t get you a job at Frontiers. But contrary to Frontiers, it’s read in Chicago & Toulouse 😉

Happy holiday.

Personally I think Airbus’ forecast for over 400 seats is pretty spot on. It’s just that 400 seats includes a different mix than before. Old VLA description now includes a lot of 777s and even some 330s. Floor space might be a better method, but in the end a lot ddepends on the World’s economic performance. A curious example of what can happen when markets aren’t impoverished happened a few weeks ago in Australia. The cheap GM small car, Daewoo Cruze, is being replaced by the Opel Astra. It appears Holden (GM) lost a lot of market share by going for the cheapest. So I see airplane sizes in some way dependant on seat sizes and wealth of pax. On current trends I guess the 779 is about a 450 seater and only time will tell if that stays the same or changes.

all size types grow over time.

( The current 2016 VW Polo has grown to 1974 Passat proportions, 2 classes above the 1975 Polo. )

That too goes for the VLA monicker.

I’d question that the 777X by going a handful of seats over 400 suddenly is “core” VLA country.

The question is what is a VLA according to forecast by Airbus?

On the other side airlines doesn’t bother much about aircraft type rating set up by Boeing or Airbus. The choose the aircraft according to what suits them best.

Air France 777 “Caribbean” has nearly 470 seats and all 747-8i have around 360 seats.

The A380 orders stalled due to the lack of a neo-version. The oil price is to low to make the more expensive neo profitable but no airline wants such a big aircraft without latest engine technology.

mainly trying to say LA, VLA, 250-300 seat, 300-350 seat etc etc are now redundent concepts.

VLA is 400 seats and above with Boeing and Airbus.

Lufthansa 747-8 has 509 seats and 488 seats . A long way from 360 seats

Korean has 368 and Air China about the same.

@Uwe

I understand the issue you make as my old (Mk2) golf was considerably smaller than the Polo I bought for my daughter last year. I don think however it works in the context of aircraft flying today for a couple of reasons.

First the growth in seat width which occurred with A300 following through to A330 and from the B767 through to the B777 seems to have gone abruptly into reverse. The B787 was to have offered a fine environment at 8 across but (ANA excepted) has gone to 9 and the B777 has gone from 9 to 10. I think we all suspect that a large number of A330 at 9/A350 at 10 will become even more constrained going forward. The A380 may be seen as the high water mark of passenger comfort which will be fondly remembered in the grim years ahead.

Second the nature of the industry is to get rid of any space that is not productive meaning galleys/ toilets will become increasingly constrained. For bean counters this is a no brainer and we can expect a fight to the bottom in terms of economy seating. My view is that wider industry is fighting against corporate parsimony and making flying in economy so nasty that all executive travel veers back to premium economy or business. I am seeing this with my team who are not happy bunnies sitting at the back any more. they are not prima donnas or very precious about things but even they are feeling the pinch.

On that basis a VLA encompasses a wider range of aircraft than before.

On that depressing note, festive greetings to all

“I guess the 779 is about a 450 seater”

Very few 779s will at the time of delivery be configured with more than 400 seats. The 779 is the smallest stretch of any aircraft derivative ever.

Expect 779s to have similar number of seats as 773s, plus one more row of economy seats and one more row of business seats, or two more rows of economy seats. This doesn’t make the 779 fit the VLA definition.

Merry Christmas Scott. Lets hope for a fresh and fruitful beginning to 2017.

Scott: What determines whether a 787 order makes it onto your chart?

If I’m counting correctly, there are 614 deliveries on your chart for the full 2017-2024 period. Boeing had 721 firm Dreamliner orders on its O/D page as of the end of November, with 11 set for delivery in December. That leaves a discrepancy of nearly 100 frames. The Qatar Airways order explains part of that — are you excluding all of the other orders firmed up in the second half of the year as well? (I suppose there may be a very small number of 787s scheduled to deliver in 2025 or even later.)

Happy holidays!

The Ascend data base delivery stream, Adam. It sometimes takes a while for firm orders to show up, especially from non-US, non-public carriers. That said, it’s highly unlikely that an airline will take delivery of all 30 (in Qatar’s case) over a two year period, and typically some much smaller number. This is why I update the data at least twice a year.

There are also 74 Unidentified 787 customers. This plus Qatar equals 104 right there.

Thanks, Scott.

My point was just that the Qatar order only accounts for a third of the missing firm orders. If there are 90 firm orders not in the Ascend database yet, and they are evenly spread over the 2019-2024 period (just for argument’s sake), then the actual order gap is more like 33 aircraft in the 2019-2020 period. Even if Boeing just keeps going at the current pace, with 70-80 orders a year, it should be able to stay at rate 12 at least through 2021 or 2022. By then, the 777X will be ramping up, which will give Boeing slack to reduce production if need be without hurting cash flow too much.

Obviously, a negative economic shock could upend that calculus. The 787 line isn’t in good position anymore to withstand a year of no orders combined with deferral requests. (Clearly, there are advantages to having a long, overbooked backlog!) But in the normal course of events, I think it’s early to raise the alarm about 787 production rates.

@ADA: You can’t look at the backlog in isolation; you have to look at the order stream as well.

Boeing dismissed all “alarms” about the 747-8 and 777 production gaps and rates for two years–and analysts and we were right all along. Don’t be so quick to dismiss the concern about the 787 production gap. I’m already aware of some institutional investors in Boeing who think the 787 rate will have to come down to eight (8!) by 2020. I’m hardly that gloomy.

Scott,

I give you great credit for calling some of the other production gaps in the past few years well ahead of time.

That said, I think there’s a big difference between the 747-8/A380/777 on the one hand and the 787 on the other. The 747-8 and A380 never found meaningful customer acceptance. The 777 is an aging model that is in the midst of being superseded by the 787, 777X, and A350. (Maybe even the A330neo, to some extent.)

By contrast, the 787 is still relatively new and best in class. I think it’s far more likely that the past three years represent a temporary dip in orders than the beginning of a terminal decline. Airlines that decided to invest in heavy checks on aging 767s in 2015 or 2016 based on low fuel prices will still need to replace them a few years down the road. And the early 777-200s/200ERs will start to come up for replacement in significant numbers after 2020.

I don’t mean to exclude the possibility of an order gap at some point, based on fluctuations in demand. (The 787 backlog could disappear in a hurry if Trump offends China to the point that they start canceling Boeing orders out of spite and a decline in trade sparks a global recession.) But while a production cut could plausibly come as early as 2019 or 2020, I would put the most likely case closer to the middle of the decade as things currently stand.

Best,

Adam

Ada:

Is there such a thing as a Positive Economic Shock?

ALW:

I don’t have all the data and figures, but in what I have seen over the years, a sustained wide body rate of 8 is more like reality. 777 was an anomaly the last few years and it was a peak and its falling back to normal.

Maybe 9 0r 10, but certainly not 12 and not even going to 14 now.

Is there some new information around on how Boeing manages on cost? ( or do we have to wait for the 2016 numbers ~4weeks away. Hmm. )

“The ascension of Dennis Muilenburg as CEO of The Boeing Co. brought more candor than existed under former CEO Jim McNerney.”

Seriously?

December 12th – raise dividend 30% and announce new round of stock buybacks.

http://boeing.mediaroom.com/2016-12-12-Boeing-Board-Raises-Dividend-Renews-Share-Repurchase-Authorization

December 18th – lower the boom on the “forgotten man” right before Christmas.

http://www.seattletimes.com/business/boeing-aerospace/boeing-cuts/

Does this strike you as candor (honesty/sincerity)?

I wonder if Airbus will produce the A330-800NEO.

With the TransAsia Airway’s bankruptcy it looks as though Hawaiian is the only customer.

https://en.wikipedia.org/wiki/Airbus_A330neo

@Kristoff: It was interesting that in Hawaiian’s investor day presentation a few weeks ago, the company presented all of its capex guidance with the A330neo excluded. It does make you wonder… http://cms.ipressroom.com.s3.amazonaws.com/249/files/201611/Investor+Day+2016_FINAL_posted.pdf (see slide 98)

No, I stated a couple of titles back that the 800 NEO is a dead duck.

For what they want Hawaiian would be better off with a 787, seem stuck on the A330 though.

Its one of those Airlines that they seem bound and determined on an Airbus (so far) despite the fact that each time Airbus has killed the very aircraft they wanted to start with (A350-800)

I tend to agree with the sentiments re the A338 but can’t help thinking that with the B788 effectively gone there is a gap in the market. No one is offering anything at the bottom end of the WB market. I am guessing this is a reflection that concedes the better economics of NB and their progressive domination of a lot of medium haul traffic. I have noticed the gradual replacement of B767/A330 on a number of these length routes

Scott:

You really missed a two major items on what differentiates you from other sites.

That is the fact that not only do you continue to provide free access to a lot of your material, you offer an open discussion forum/site for that for enthusiasts to comment on and or bring in current news.

THANK YOU !!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!!

This is a quote from Av Week

“Germany also is purchasing the C-130J in conjunction with France because the A400M is seen as too large for some missions.”

most interesting.

LNC in 2016 first sourced the MC-21 wall-to-wall interior trim, so we have (finally !) a clear vision of the competitive picture for the Feeder line-up :

– MAX (139.2″ = 2 x 59″ + 20″ aisle + wall-panel clearances 2 x 0.6″) vs

– NEO (145.4″ = 2 x 62.5″ + 19″ aisle + wall-panel clearances 2 x 0.7″) vs

– MC-21 (150.0″ = 2 x 63.5″ + 20″ aisle + wall-panel clearances 2 x 0.6″ ) vs

– C919 (153.5″ = 2 x 65″ + 22.3″ aisle + wall-panel clearances 2 x 0.6″)

and let’s add on the Canadian Outsider : C Series regional jet :

– C Series (128.7″ = 43″ double + 63.5″ triple + 21″ aisle + w.p.c. 2 x 0.6″)

That leaves us here AvGeeks with a prospective 2017 full of lively comments …

Thank You LNC !!

ERRATUM

Cancel and delete above :

– MC-21 (150.0″ = 2 x 63.5″ + 20″ aisle + wall-panel clearances 2 x 0.6″ )

and replace by :

– MC-21 (150.0″ = 2 x 63.8″ + 21″ aisle + wall-panel clearances 2 x 0.7″ )