Leeham News and Analysis

There's more to real news than a news release.

Pegasus Airlines, bridging Europe and Asia

By Bjorn Fehrm

April 05, 2017, ©. Leeham Co: Turkey’s Pegasus Airlines has its operations center south of Hungary’s Wizz Air that we wrote about last week. With a hub in Istanbul, the Turkish LCC connects Europe and West Asia/Middle East.

Pegasus is a fraction larger than Wizz Air and had the same dynamic development until last year, when the internal unrest in Turkey threw a spanner in the airline’s growth.

Pegasus is a fraction larger than Wizz Air and had the same dynamic development until last year, when the internal unrest in Turkey threw a spanner in the airline’s growth.

The LCC connecting Europe and Asia

Pegasus started as a Turkish-based charter airline by local investors and Aer Lingus in 1990. ESAS Holdings bought the company 2005 and changed it to an LCC. The development has been rapid since, with the airline today covering 101 destinations in 40 countries, Figure 1.

Figure 1. Pegasus network 2017.03. Source: Pegasus Airlines.

The route network is a mix of Domestic (32) and International destinations (68), which go as far as Delhi, India, and Urumqi, China.

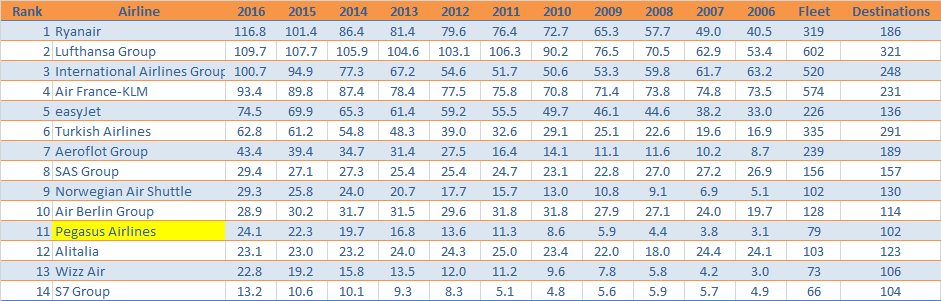

Traffic development has tracked slightly ahead of that of Wizz Air (Figure 2), with operations focusing on geographies further south, straddling Europe and West Asia/Middle East.

Figure 2. Traffic development for Europe’s largest airlines (million Passengers). Source: Wikipedia.

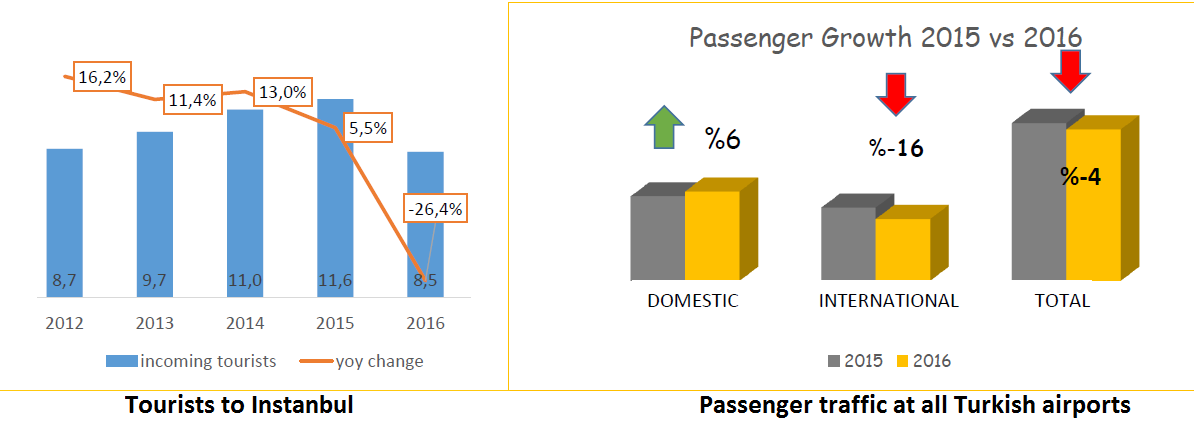

The attempted June 2016 state coup in Turkey brought political unrest. Traffic to Turkey as a tourism destination plunged, Figure 3. The growth in domestic travel fell as well.

Figure 3. Change of travel climate in Turkey during 2016. Source: Pegasus Airlines.

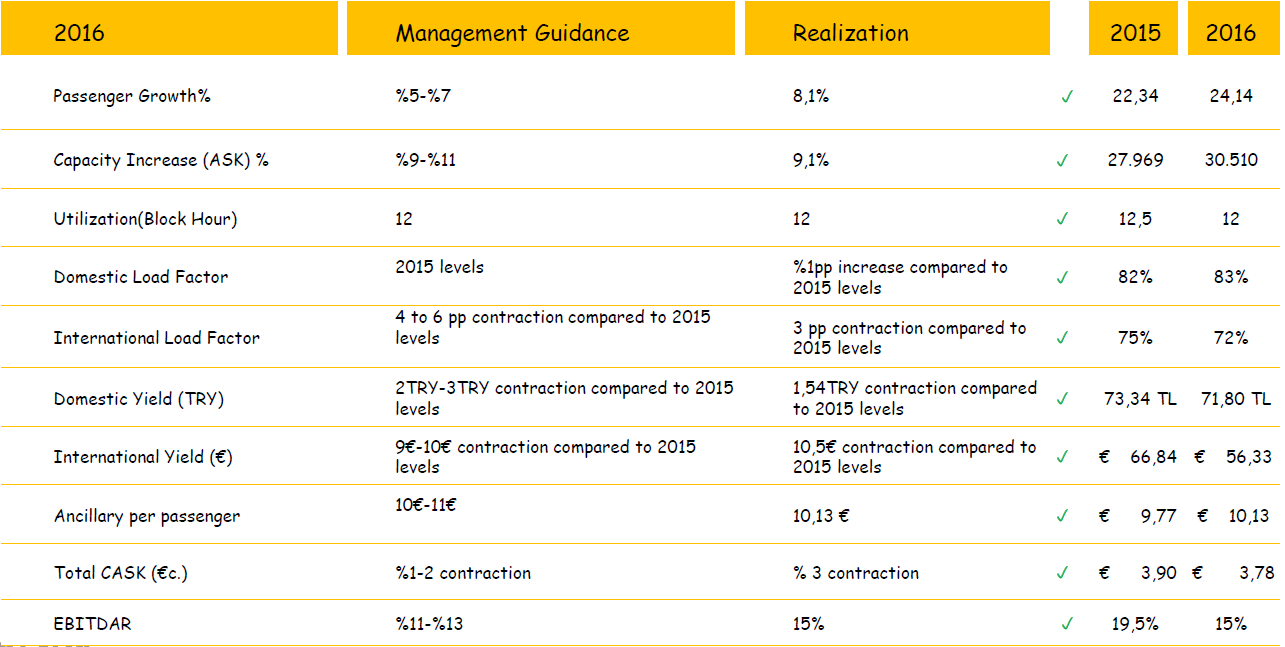

The changed travel climate did not stop Pegasus’ expansion but it hurt its bottom line (EBITDAR), as an expanding fleet could not be filled with international traffic, Figure 4.

Figure 4. Pegasus performance guidance autumn 2016 and actual results. Source: Pegasus Airlines.

In Figure 4, TL and TRY stand for Turkish Lira, which converts to $0.27. For international traffic, Pegasus shows results in Euro as the Turkish Lira has a fluctuating value.

The weakening international traffic is driving Pegasus to sell and lease out older aircraft in their fleet. The airline has also deferred three of five Boeing 737-800 orders for 2017 to 2018 to help with the capacity control.

Pegasus received nine A320neos with LEAP engines during 2016. Average age of the fleet is 5.4 years. The fleet has a planned growth to 100 aircraft by 2020, Figure 5.

Figure 5. Fleet as of March 2017 for Pegasus. Source: Pegasus Airline.

Pegasus is one of the lowest cost LCCs, with CASK ex-fuel at 2.81 Euro cents during 2016. Management is focused on keeping this costs level while increasing a rather low load factor of 82% domestically and a very low international load factor of 72%.

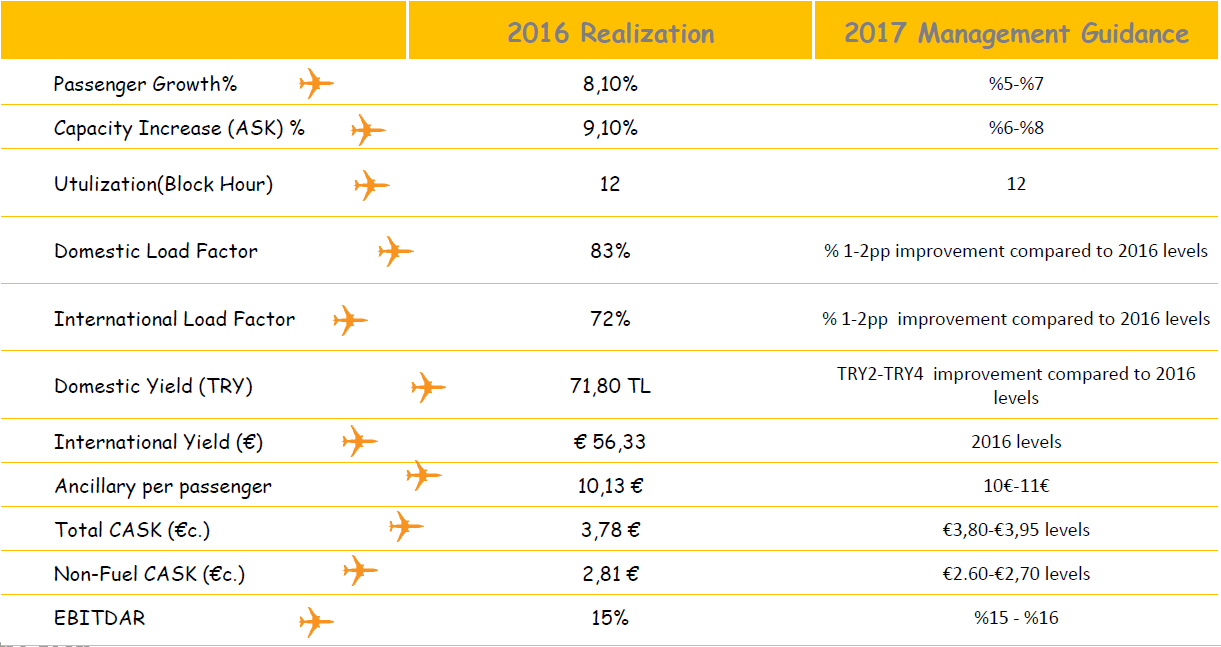

The low load factors for an LCC is the result of the recent decline in traffic paired with the expanding fleet, Figure 4 and 6.

Figure 6. 2016 operational results and plans for 2017. Source: Pegasus Airlines.

The decline of results for 2016 has shrunk the cash reserves to around $200m, Figure 7. The increased asset and debt from 2015 (+~80%) is the result of the A320neo aircraft that arrived during 2016.

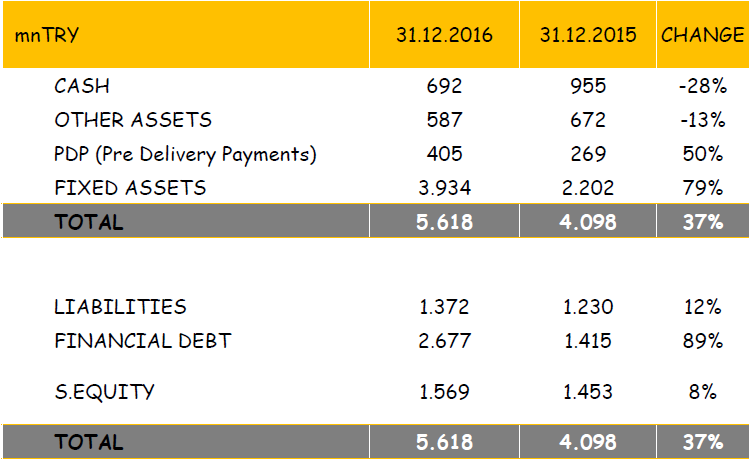

Figure 7. Pegasus Airline’s balance sheet. Source: Pegasus Airline.

Shareholder equity at 28% is higher than Norwegian Air Shuttle (20%) but considerably lower than Wizz Air (52%), EasyJet (49%) and Ryanair (45%).

They might want to rethink that logo on their planes, it looks like “flypigs”

Thank you for such a fine article, Bjorn. Two quick questions. One, do you know how management was able to avoid a severei revenue downturn after the coup? (I would have thought revenue would have been down at least 10 to 15%–year over year–post-coup.) Second, any comment on how Airbus looks to have won the Pegasus fleet “battle” going forward over the next five years?