Leeham News and Analysis

There's more to real news than a news release.

New mission focus seen for NMA

Nov. 8, 2017, © Leeham Co.: A revised mission focus for the the prospective Boeing New Midmarket Aircraft (NMA) is seen by a New York research firm.

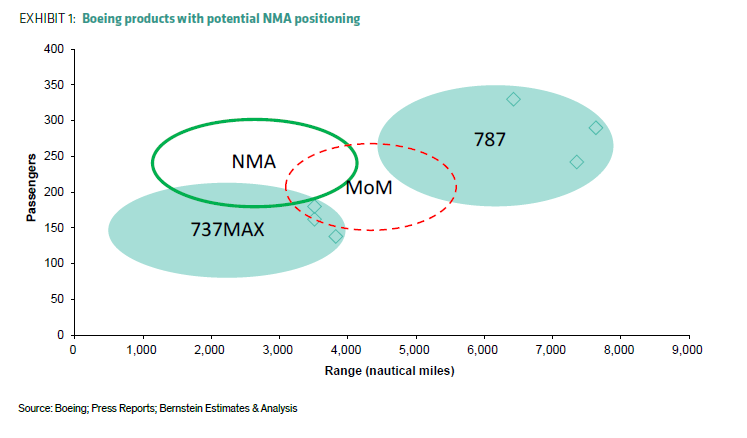

Bernstein Research sees the NMA being redefined as a larger aircraft serving the Airbus A320/Boeing737 market rather than a replacement for the Boeing 757/767 “Middle of the Market” sector.

Bernstein has been cool to the prospect of a 4,500nm-5,000nm airplane. The analyst, Doug Harned, likes the proposed size—220-270 passengers in a 2x3x2 ovoid

Concept of the Boeing 797 New Midmarket Aircraft. Source: fs2000.org.

composite fuselage configuration. But he sees a stronger market serving ranges of 1,000nm to 4,500nm.

So far, there is no market intelligence LNC knows of to support any inference Boeing has refocused the mission statement of the NMA, also known as the Boeing 797, though Harned is firm in his view: “The focus is now on the NMA category, which we see as the right positioning,” he writes in a Nov. 6 research note.

Airlines LNC checked with yesterday reaffirm Boeing’s focus at this time to be 4,500nm-5,000nm.

Recasting the mission

Harned sees limited market demand for the NMA, an issue that’s vexed Boeing and its suppliers.

“The NMA model fits well with fast growing Asian markets and should be able to do many trans-Atlantic routes,” Harned writes. “The range, however, would not be sufficient to do longer, thin, transatlantic routes, say, Newark-Warsaw or Charlotte-Berlin. We see those longer-range routes as better suited to a 787 or A330.

“The reason for the shorter range is that it allows weight to be taken out of the wing and the engines can be optimized more toward a high number of cycles between overhauls (e.g. like a CFM-56 or V2500 rather than a Trent 700). This means that the airplane could operate efficiently on thicker routes of under 2,000 nm, which are common in the Asia-Pacific region.”

Another analyst LNC consulted indicates Boeing is marketing the airplane to low cost carriers who fly, or want to fly, the trans-Atlantic routes.

Taking the pressure off Airbus

A 2027 EIS for the NMA and a 2030 decade for the New Small Airplane replacement for the 737 would take the pressure off Airbus to cobble together a quick response to the launch of the NMA, was many assume will be next year by the Farnborough Air Show (a date Harned still subscribed to).

But it also gives Airbus time for another round of improvements to the A321neo that could eat at the bottom end of the MOM sector and further encroach on what some believe to be a risky business case for the NMA.

This could also give momentum to the idea of restarting the 767-300ER passenger line. See stories from October here and August here. (Wall Street Journal take note: You read it here first.)

I would believe that Boeing will design the 797 in a way to fill the upper end of the current 737 with probably an extended range to get across the Atlantic. I imagine that the smallest version be very close to the capacity of the 737-10. Once the 737 then gets replaced, Boeing can round off the product offering by optimizing the narrowbody to a slightly smaller size.

In 10-15 years the graph above will show the new 737 a bit lower/left while the gap will be filled with the 797. Boeing will ensure cockpit commonality from the new 737 through the 797 up to the 787 having a seamless family serving from thin short routes to thick long ones.

Why not consider a “do nothing” scenario? With no third party aspiring to do a MOM, Airbus and Boeing could simply stick to their current portfolio and maintain a 50:50 (give and take 10) market share.

Not to mention that the EOEMs will keep bleeding on their current new engine programs and couldn’t care less about starting yet another new engine development and industrilaization program.

New 767-300ER with old engines should be banned by the EPA. Seriously, wouldn’t a re-start of the 763ER constitute a total loss of face for the 787, which was touted as a “767 replacement” and “A330 killer”?

Well its not exactly 50/50. Production wise yes, sales wise no.

And the A321 is kicking Boeing really hard.

As Boeing has no analogous product (the -10 falls short) Airbus can sell it at much better margins and make better money.

P&W would heartily disagree with you on a new engine.

They will be first in line with a higher thrust GTF.

And at this point, the 787-8 is going away and the 767 fills a shorter range spot.

787 has no shortage of numbers, make more money on 767s.

CEO gets a big bonus, any problems are the next guys problem.

Focusing on the upper end of the current narrowbody size range and shorter sectors just puts the NMA more firmly in the sights of the A321neo++ (whatever that may turn out to be). With virtually no unamortised R&D on the A320 family, Airbus could afford to price a hugely competitive developed A321 at levels that any all-new aircraft could not hope to compete with.

Such is the price Boeing would have to pay for not having developed a design to truly compete with the A320. And for Airbus, such is the prize for having thought long and carefully about the A320 design in the first place. And for pulling a fancy move with Bombardier.

Other people have also pointed out that the C series frees Airbus up to do a full development of a heavily optimised larger single aisle aircraft. They can do so without having to think whether it could also be scaled down to C300/C500 size. It would indeed be tough to beat.

I wonder who will be quickest to get a CF single aisle A321/2-sized aircraft in the sky? I don’t actually know, but I suspect that setting up the plant to make whole fusealge barrels (like 787’s) is an enormous job. For Airbus, who make their CF A350 out of bonded panels, they could get manufacturing pretty quickly. I wonder if Boeing would switch construction styles?

The issue with carbon is beginning to be made clear. In simple terms, if it comes out of the oven with an issue then the part must be thrown away. In composite world, sometime ago, GKN were honest enough to admit they were regularly throwing away parts because of issues

I think Boeing will give up on barrels. Airbus did a lot better, weight wise, using frames and panels. The A350 fuselage contributes significantly to weight reduction. And they are improving on a daily basis, particularly with thin high strength parts.

It is the thin high strength carbon that intrigues me. The RR Cti fan blade is very thin, meaning significant weight reduction but also improved aerodynamics. I also like the blue colour. Would look good on a NMA

Boeing will follow Airbus. Both will use frames and panels, and the carbon will be thinner and stronger.

A prediction. The next generation whatever will be >65% carbon but also proportionately lighter. Interesting times.

” The issue with carbon is beginning to be made clear. ”

“Ausschuß” is not a new concept introduced with *FRP parts.

If you do statistics on parts tolerances you can even back reason if they were “produced to spec” or “selected to spec”.

But GKN were losing a lot of parts and they admitted it. To lose an entire barrel is something else.

I did read somewhere that GE carbon fans are in part hand made. I think it was Aviation Week. Anybody verify?

Phillip:

Bjorn feels that the two systems are about equal for weight.

As A350 went through a lot of Rev 1/2/3 to get there, I don’t see that anyone knows that the Frame and Plate design is faster.

Out of auto clave is being used in the MC-21.

Boeing will balance experience with the new tech and make a decision as to what looks the right patch down the road.

Airbus had no choice in the A350, they had not put the research that Boeing did into the barrel system.

It worked and worked equally, but going in I don’t’ think anyone would have predicted an even match.

For Boeing I would not predict anything, its a major leap and its got to be the absolute most efficient mfg and in numbers, so it may be all new approach.

I recall that GE’s own videos show a mixture of hand and machine work.

I gather that RR/GKN’s approach to their CTi blades is to maximise the amount of machine layup. I doubt that this is purely to aid mass production; machine layup would be very consistent; that’d help get the yield up.

Blue is a fabulous colour!

There is little reason to build an all composite single aisle. I think AlLi economics are really hard to beat. I honest am not sure if even a composite wing is worthwhile. When you look at the E2 vs Cseries, I am not sure if the a composite wing gets you much advantage in this size class. 100$ AlLi would make more sense IMHO.

@Transworld

I admit I looking for reasons as to why the 787 has lost so much money. I’m also looking to understand why the NMA is 220-270 PAX, just 30 PAX less than the 787-8 and 20 PAX less than the 787-9.

It all seems muddled. The 787-9 (but -9) is Boeings best airplane by far. Why go after your best airplane.

On the subject of thin carbon. In the past whilst carbon is ligher it needed to be fatter to obtain the strength. This may now be history. The RR/GKN fan blade is an example. It is apparently thinner than the equivalent titanium fan blade, allowing the aerodynamics to be improved and therefore propulsive efficiency to be improved.

Thin carbon opens up all sorts of possibilities. For example even longer winglets than we have seen on the A350. Another example, a LPC made of carbon

Thin carbon is the reason why I think Boeing will move to panels and frames for it allows more flexible construction and therefore better yield

My guess is that the 220 is aimed at longer thin routes (up to 5500Nm, the MoM on the graph) and the 270 the NMA on the graph (<4000Nm), for "intercontinental" routes, especially Asia where the 330's are used extensively in this capacity.

AB's "322's" range will be ~1000Nm shy of the 220 seater while none of the current twin aisles (including 789) will come close to 270 seat mile/sector cost on short routes.

I think the real reason is that the 787 isn’t any better than the A330neo, as inadvertently made clear by Willie Walsh. So competition between the 787 and A330neo will be about capital cost. Which is the cheapest to buy. Consequence, the 787 will be subject to severe price pressure.

The NMA will need to deliver on efficiency where the 787 didn’t deliver. Specifically they need to make carbon work for them, for I think we now know carbon didn’t work for the 787, it was all about the engine.

Does mean the A350 is in a class of its own for whilst the Trent XWB is superb it only accounts for 1/2 of the 25% improvement over the 777 classic as confirmed by Cathay and others

I’ve said it before: Boeing need to sort out carbon or they are going to be left behind!

Exactly!

Why not 1 common fuselage/systems with 2 different wing/engine packages?

https://lh3.googleusercontent.com/-XSZq70Ph0nw/WgLiQGz3xnI/AAAAAAAADOs/lnQC79nMhpA9CUBJqwlmIcpOhhyenSKlACLcBGAs/s1600/Boeing%252520MoM%252520NMA%252520NSA%252520A321%252520keesje%252520Airbus%252520Design%252520Engine%252520Wing%252520737_zpscrrkvmms.jpg

your wide aisle idea is never going to fly (haha, get it, _fly_?) because for a mere 4 extra inches they can have a second narrow row rather than 1 wide aisle which is not going to do much to speed turnaround.

the idea of a common fuselage and completely different wingbox/wing/engine set for different missions _might_ be plausible if they can wrap their minds around a modular wing/wingbox concept that can be built to different spans and MTOWs using the same tooling.

but when you think about it, doing a good job requires not just a different wing/wingbox/engine, but also different landing gear, empennage, a full certification regime…

makes you wonder how Embraer can pull off the 175/190/195 with 3 different wings, 2 different engines, presumably different landing gear and still keep the whole think affordable as a RJ.

On the other hand it might reduce R&D per frame and, assuming it doesn’t add significant complexity to parts design, would reduce parts cost per frame, accelerate the mfrg learning curve, reduce maintenance costs etc, all while offering the potential to better sweet spot the product for different markets.

“because for a mere 4 extra inches they can have a second narrow row rather than 1 wide aisle which is not going to do much to speed turnaround.”

Nope, 4 people taking their stuff block 2 narrow aisles, not a single wide one…

I think you are overestimating the real world benefit of a wide aisle in boarding/deplaning.

standard courtesy behaviors (line and turn waiting) will prevent many people from passing the person who is loading their bag in the overhead. a full second aisle (which is what I meant above, not row) provides greater relief than a single wide aisle because now there are two paths available to all the people in the middle.

Your “makes you wonder how Embraer…” comment has got me thinking that if Embraer can make such variations in wings, engines, etc possible in the RJ category, imagine what they could accomplish in the categories of larger narrow-body or wide-body, even, aircraft if they were to move into those.

I and many have always taken the view that the NMA would take away the upper market of the 737/A320. At the upper end the 737/A320 are very poor airplanes and therefore ripe for competition. As we know the market involves 1000s

Having said that I would prefer the NMA to be 200-250 PAX in size, the 757/767 being the standard for me

Agree with this at the moment (seems the MoM/NMA changes every day in my mind).

Bjorn had an ovoid aircraft at 2-3-2 with 230 seats that can take a single LD3 (on section) in one of his posts several months ago. After all scuffling around I also seem to gravitate back to that.

The wing and range a major decision. Don’t say the 797 must be one family wonder but I think wing, engine, etc should initially be optimized for ~230 pax and max range of 5000Nm (typical routes 1000-3000Nm). That looks like the NMA on the graph, so I agree?

The now more talked of 763Revive could fill the market between the single aisles an 787’s during the interim.

How about somebody build a 150-200 pax, dual class, narrow-body, capable of 5000 nm missions. Minimum pitch in business/first class 54 in; 36 in in economy. Seat width 19 in., armrests for each seat. Aisle width of 30 in. That is my idea for a comfortable airplane.

I. A MOM that is significantly more expensive to build than an A330-800 because it would be make in CFRP will be really hard to sell in large numbers.

II. A NMA that would not cannibalize on the “new” 737-10 is impossible to design.

III. Looking at Airbus product development cycles I conclude that they are now planing the next generation single aisle, which will doubtless be on the large end of the spectrum (A321/A322/757/MC-21) especially as the C-Series covers the lower end here. This will certainly feature CFRP wings.

IV. Boeing has to swallow the bitter pill and develop an all new range of single aisle planes, which means not one, but two different models.

V. Will the Boeing management have the funds, the infrastructure, the engineers and the guts to do just that???

As I wrote above, Boeing doesn’t need two singles aisle aircraft. The 797 will cover the upper part with a 2-3-2 layout while the future 737 will have its focus a tad smaller and compete with the CSeries too.

Gundolf: While I don’t say Boeing can do it, if they can, the idea is they can do it with large numbers in mind and a very low cost mfg process and by definition it has to be far lower cost than an A330.

Maybe this will morph into a 767 replacement, the Sonic Cruiser while it kept the tech did that.

I don’t have Leeham data set nor Boeings in the market, what sells for what and the numbers involved.

Without that its just guessing.

Me, I am staying tuned to see what pops up.

Why not do an B767Neo with RR Trent 700 engines if they keep up with promises fuel save burnings? Easy to certify, easy entry into service as the assembly is still working, would fit the needs for many current B767 customers.

Well Boeing uses almost all GE engines now (787 aside)

And an NEO still costs and you have to get a return.

A330 not doing so good, seems much less market for 767.

Other than some clean up and latest PIP engines and the winglets, 767 has gone as far as it can.

The MOM/NMA conundrum shows just how difficult it is to find a suitable compromise. Boeing seem to be circling this problem like a wolf does its prey, summoning up the courage to attack but concerned that it is going to be hurt in the process. If the suggestion is that the design coalesces towards a short range high volume competitor this is some way from the original brief. What advantage will it have over existing and upgraded existing offerings?

At twin aisle it may offer quicker turnaround times but suffers substantial weight penalties. And how can they expect to compete on price against a A321 or A322?

I do not envy this decision and believe that a MAX replacement/NSA type offering is more important, single aisle, larger, something to take the fight straight into the heart of A320/1 territory. In simple terms replace the MAX while it is still a cash generator, otherwise it will end up with too many offerings at the end of their life cycles. One could see it as follows:

B757 long dead

B747 near dead

B767 life support

B777 medium term reprieve

B737 MAX shorter term reprieve

B787 maturing

A340 long dead

A330neo shorter term reprieve

A320neo medium term reprieve

A380 go figure

A350 growth

Cseries post launch

I have long agreed that single aisle replacement should be the priority.

Appeal of the NMA if it can be pulled off is an all new market to themselves and Airbus will have no equal.

Boeing will still have no A321 equal let alone a more up revved one.

Wait for tech to get a single aisle that makes a large leap then?

Agreed I would not be the one to make the decision now.

I wool have bit the bullet two 737 generation ago and come out with the latest whiz bang replacement I could and then beat Airbus over the head with it.

But they didn’t and they are in a rough place.

FlightGlobal may have indirectly given an insight into Boeing’s problem. Willie Walsh (IAG) is quoted as saying that an A330ceo (Level 1) burns 6 tonnes more fuel than an identically configured 787-9 when flying from Bacelona to LA (5200nm). I was of the view that it was at least 50% (9 tonnes) more than that, some saying 100% (12 tonnes) more. Therefore 9-12 tonnes fuel burn difference in favour of the 787-9, equating to 15-20% better efficiency. It seems its only 10%.

The A330neo will remove that differential, which is perhaps why the NMA is up toward 787 and not down toward the 737.

I think the 787 will sell at least 2000 and perhaps 2500. The reason being that Airbus can’t produce enough A350s to mount a challenge and the A330neo isn’t better than the 787.

So for me, the NMA should be in the 200-250 PAX range. The range will go up to 5000nm because the wing will be a thin, high aspect ratio wing that will be able, by default, to hold enough fuel for 5000nm and more

Some years ago the proprietor Scott talked numbers in the ~8% fuel delta range ( but for one specific case ).

Those “20% better than current generation” never reached beyond the 767 ( which subtype ? ).

Uwe:

“Those “20% better than current generation” never reached beyond the 767.”

Objectively, should we even expect anything “beyond the 767” at all?

When J.Leahy claimed 359 would deliver 23% lower fuel burn per seat than 772ER back in 2007, he couldn’t possibly expected that 23% gain to reach beyond the 772ER against the 778 launched 6yrs later:

https://web.archive.org/web/20080528042628/http://leeham.net/filelib/Leahy_Final.pdf

On the other hand Boeing claims the 778 will have 4% better economics than the 35K (which I think is unlikely). But around 225 the UF engines could be ready for the 350’s?

Cathay confirmed the numbers in an article in Aviation Week. The A350 according to Cathay is 25% better than the 777 series

@philip:

“Cathay confirmed the numbers in an article in Aviation Week.”

What numbers? Leahy’s claimed 23% lower fuel burn per seat 359 vs 772ER in 2007? That would be a bit weird for CX to confirm as CX has never operated 772ER. If CX referred to their 772, I hv no doubt re their confirmation…the only diff between 772 and 772ER is payload/range performance, not fuel burn and CX do deploy 359 on many short/mid-haul routes used to be flown by their 772.

“The A350 according to Cathay is 25% better than the 777…”

“better” in what metrics? I’m not doubting U but I just want to understand more for my learning.

Efficiency. It takes 25% less fuel to fly an A350 than it does a 777 classic. So Cathay upheld Airbus claims for Airbus have always claimed that the A350 is 25% more efficient than the 777 classic

Be interested to see what Cathay and others think of the 2019 version of the A350, the version where all of the improvements come together.

You seem to have not understood my argument:

Boeing said “20+% over current generation”

but meant 767 which is definitely “not current”

but at least one gen further back.

So they lied.

But they selling aircraft, EK is taking 40 B787-10’s and Azberbaijan seems to be taking another 5 B787-8’s?

@philip:

“FlightGlobal may have indirectly given an insight into Boeing’s problem. Willie Walsh (IAG) is quoted as saying that an A330ceo (Level 1) burns 6 tonnes more fuel than an identically configured 787-9 when flying from Bacelona to LA (5200nm).”

Except that:

1. The article only quoted Walsh said 787.

There was no mention whether it was the 788 or 789 and both are in Norwegian network.

2. Norwegian typically deploy 788 on BCN-LAX

Anyone can easily check that fm from flightaware.com

3. Level only operates 332

Which is logically far easier to duplicate/simulate a similar “config” to 788 than to 789.

“Therefore 9-12 tonnes fuel burn difference in favour of the 787-9, equating to 15-20% better efficiency. It seems its only 10%.”

If the fuel burn diff per seat 332 vs 789 is only 10% as U claim, no operator would invest in a 789.

On sectors below 5,500nm(about 10,000km), I totally buy 10% fuel burn per seat diff 332 vs 788 but NOT 332 vs 789.

“The A330neo will remove that differential..”

Agree partial or even total removal but only for 338 vs 788 for sectors below 5,500nm. Possibly similar story even for 339 vs 789. But then again in high/LCC density cabin config(i.e. near max payload), 339 likely can’t fly sectors anywhere as far as 789 can.

“I think the 787 will sell at least 2000 and perhaps 2500. The reason being that Airbus can’t produce enough A350s to mount a challenge.”

U must hv missed the recent news about 787 & 350 production rate increases planned by Boeing & Airbus. Fm around early 2020, mthly production rate diff between the 2 families will be just 1 per mth.

U are declaring a long term, multi-decades relative sales outlook based on the current/short term diff in production rates between the 2.

“A330neo isn’t better than the 787.”

But functionally close enough and more importantly these days, CapEx for 787 likely “isn’t better than the” 330Neo….and for some airlines/lessors, higher performance/efficiency “isn’t better than the” lower CapEx.

Good point. It is the 787-8 for Level only have A330-200. So I revert to my previous thinking, the 787-9 is 5-8% better than the A330-900, until fact emerge otherwise.

It does though explain why the 787-8 is not selling and the 767 is being revived

Ps. Is the production rate increase of the A350 official or is it LNC prediction. Anybody verify?

It’s not official but the figure was buried on the Airbus website.

… but Iberia have A330-300. Infortunately 6 tonnes, as quoted by Willie Walsh, could represent an average. Dunno, these CEOs should be clearer.

@philip:

“but Iberia have A330-300…”

Which has nothing to do with Level fleet nor with the kind of cabin density used by Level.

IB’s 333 contains 288 seats(2-class) which is an extremely typical FSC density among 333 operators. In LCC/Level-style density, a 333 would be doing 360~380 seats minimum.

“..quoted by Willie Walsh….these CEOs should be clearer.”

I thought Walsh was pretty clear in that he wasn’t talking about anything re IB.

I think Boeing moving might be driven by things Boeing knows but will never communicates

1. MAX sells on availability, commonality & price, 737 is over.

2. Downplay Airbus CSeries publicly, not in the boardroom

3. At best the MoM will have break even at 1000(?) ac

4. A shrink MoM ain’t good enough for huge 170-210 seat/1500NM segment.

A move back from NMA to NSA isn’t unexpected at all. Something a little bigger, better and lighter than the A320 should be possible. The A320 is eighties material. If Boeing bites this bullet it will be a survival 5-7 years for the MAX situation though..

Agreed, the whole thing could morph into a couple different possible directions or stay on path. That’s why its best to see what happens, we don’t have the info Boeing does.

I suspect the honesty is at the BCA level and the board and CEO continue sing the kum bey yas (however you spell that!)

Spelling is Kumbaya.

https://en.wikipedia.org/wiki/Kumbaya

I like your drawing of common NSA/NMA fuselage. different wings and engines for a far different TOGW, but I have a different conception of NSA — which should not be small, should come first ASAP, with NMA deferred, if ever

The NSA, should be renamed DSH for domestic short haul. It should carry 250 passengers in comfortable single class (as in Southwest Airlines 737 MAX 8 with 175 passengers) — and have growth to 300 passengers. It should have 2 aisles and 7 abreast elliptical as in Boeing 797 studies and Bjorn’s drawing, or 8 abreast as in the MIT / Aurora / NASA D8 configured for extra body lift (also applicable to 7 abreast) which is more elliptical with a different nose. The NMA fuselage would be about the same capacity and same shape as DSH

This DSH should be a really light weight airplane designed for 2000 nm range and .72 mach cruise, carrying only passenger baggage . The fuselage should be composite, likewise wings, wing box, tail. High bypass 15-20 engines will be available for service in 2025. This DSH should beat the 737-8 MAX by 30-40% in fuel burned per seat mile under 2000 NM where over 95% of domestic traffic flies.

The 250 passenger (2 class), 5000 nm. .85 mach cruise NMA could be designed concurrently and would have much higher TOGW, more than twice the fuel capacity, thicker skin, heavier frames, more wing area and span, larger tail, heavier landing gear, and larger engines with somewhat lower bypass ratio. There w0uld be high commonality in systems and same flight deck etc

The DSH would be a very popular airplane in domestic markets of N.America, W. Europe, China, and India — I’d guess a market of 10,000, There will be plenty of other 150-200 passenger (single class) airplanes by 2025 and beyond which can fly the domestic traffic over 2000 to 3000 nm : improved A320neo, improved 737-8MAX, MS-21, C919 and, best of all, CS300 / 500 and new ones in this class by 203o.

Global domestic fleets w0uld be mixes of airplanes from 100 to 300 passengers with ranges from 2000 nm (or less) to 3000-3500 nm: improved 737-8MAX and improved A320neo, C919, MS-21 and best of all, improved CS300/500 and all-new post 2030 models.

My DSH thinking is driven by the need to greatly reduce global fossil fuel burned and CO2 generated — with unmatched economics. Climate change driven by human activities is here, it will get much worse, the public will become very concerned, aggressive action must be taken to lower emissions — not just level them off at say 1.5 Billion tons of CO2 per year (air transport CO2 emissions are currently 750 million tons a year and growing).

By 2025 I believe any NMA would be a low priority airplane for any airline fleet, but if it goes ahead, it could have much commonality with the DSH. I don’t think Airbus will build an NMA to counter Boeing; they would happily build a DSH and bury them.

Plus less pilots needed, until single pilot aircraft, which may take longer than predicted.

This NMA/MoM thing is actually good fun for someone that has nothing to loose, maybe a synopsis of aircraft and potential aircraft available.

321LR, not enough range, wing limits.

322New, 220 seats, de-planening problems shorter routes, needs new wing, range not enough?

338, heavy, expensive, 256 pax

339, to big.

MAX10, no show,

788, heavy, expensive, right 240 pax,

763ER, old, to many pax,

789, big, expensive.

AB Modification options.

A322, CAT-D wing, stretch to accomm 2nd door in front of wing and more amenities for longer haul, current 321NEO seat count (206).

Boeing options.

787-8, lighter, new wing, UF’s, 5000-6000Nm.

Build an 757-200 size NSA, Cfrp’s, UF’s, etc.

A new 220-240 seat narrow twin aisle for Boeing or 240-250 seat new 2-4-2 (ovoid) twin aisle AB (6000Nm) replacing the 332/8’s the best long term options, stretch variant 280 seats 4500-5000Nm.

AB could actually gain more if they build a MoM-Bus as it will compete with the 787-8, 797 while the 797 could take away sales from the 787’s?

“A321 not enough range.”

“A330 to beefy.”

I’d expect a competitor to place his new product by defining a demandarea such that the potentially competing products are just outside the parameter.

And defend that to the last breath.

“NMA new focus” imho means Boeing feeling cold water lapping at their feet.

…or they realized that an NSA has much lower risk and better returns. The economics of a MoM/NMA could be marginal.

They’ve still got the 767-300ER. If it works, don’t fix it. Airbus has the A338, which in seating, is an A321 and a half. While antiquated, Boeing has the 767, which is an A321 and 3/8ths. What Boeing doesn’t have is the A321 exactly, so why not leapfrog it with an A321 and an 1/8th, or an A321 and a 1/4, at similar ranges. Is that a 757-250 at 165′, a 2-2-2 at 165′, or a larger 2-3-2 at 170′? What ever the best design, they have to commit to a new fuselage, so they can’t mess it up.

Anton: “AB Modification options.

A322, CAT-D wing, stretch to accomm 2nd door in front of wing and more amenities for longer haul, current 321NEO seat count (206).”

Scott: “But it also gives Airbus time for another round of improvements to the A321neo that could eat at the bottom end of the MOM sector and further encroach on what some believe to be a risky business case for the NMA.”

I think it isn’t rocket science to get a picture of what Airbus could do, calculate how much it would costs, time to market and how the specs for such an aircraft could look.

If Airbus takes aim at this segment, significant development could go in optimizing cruising speed (wings, cockpit), range (getting out ATC’s, wing) and a stretch to create space / lower unit costs.

Apart from the fuselage/systems it would probably not be a A32x anymore.

https://lh3.googleusercontent.com/-YckgYMk2UT4/WefZgFfVq_I/AAAAAAAADOA/KMkNbbEqJlIBKx_4eBuQpO83oWAH-USwQCLcBGAs/s1600/A360-900.jpg

I have been toying with this in my head and try to read through lines.

AB seems to have been working on wing related matters lately, several months ago mention of modular carbon wingbox etc. Isn’t the following a most likely scenario what is going at AB re the future of their narrow bodies, as every body knows the biggest market by volume.

1)A322, NSA, new CFRP fuselage, UF or similar engines, (200-210 seats), 4500-5000Nm (wing 1), wait for Boeing 797 launch to trigger.

2)Ramp-up CS production, launch CS5, 155 seats, 2500Nm,

3)Launch 321 replacement, “322” fuselage, wing 2, 3000Nm, 190 seats.

4)Launch 320 replacement, “322” fuselage with wing 2, 3500Nm, 165 seats.

Think that’s why Boeing is c….p..g itself to launch a small twin aisle? In 10 years from now (2027) ~2400 A32X and 1800 737NG’s will be between 15 and 20 years old.

Airbus, “your one stop narrow body shop”!

Very nice concept. Seems like the logical route. New taller landing gear I assume.

what seems to be ignored in this discussion is the possibility of amortizing some of the 787 costs by building a 797 based on the 787 tooling (fuselage and cockpit mandrels/ovens) but with tailored layups for the different mission (which is one of the great strengths of composites, easy tailoring) and shorter fuselage.

call it 787-7 length with a lighter wingbox and something similar to the -3 wing in span, no-bleed versions of the 747-8 engines, lighter landing gear..

I think it would be very hard to make it light / cheap and competitive. It’s would have to be aimed at 280 seats/5000NM segment, leaving the 737 to fight on for another 12 yrs..

https://lh3.googleusercontent.com/-VXRYcwhkbt8/WVt97-eU9TI/AAAAAAAABKc/JqX3I85vYU4WBDfF4oalN1_wQ_aNEVDRwCLcBGAs/s1600/787%2BNMA%2Bvariants%2B6.jpg

Agreed, but could take half the time and cost to develop. With cash and time in the pocket development of an NSA could basically start first and the 787-7 triggered to be ready when the UF engines are ready?

The 763ER Revive is buying time until the UF’s arrive.

Using the 787 as a basis for the 797 is not that easy, it shall be much lighter but take many more cycles. The present 787 is Heavy and have a fat cross section as a MoM, I guess Boeing is looking at making a 797 from half as many CFRP layers in most structures and a pair of brand new wings with 37-45k Engines. If instead Boeing makes a 4500nm A330 cross section 797 with 2-4-2 seating and Twin LD3’s using robots producing carbon fiber structures AI will sweat. Boeing can stuff it with 787 systems and software. It will be the final A330 replacement for routes between 1-7hrs. It becomes bigger than an A322 and AI will hesitate doing yet another A330 competing version, still they could do it with the same new Engines and stuff it with A350 boxes. AI will try first with the A322 with 797 Engines, then depending on Boeings price for the least capabile 797 decide if they should do its own version.

Aye, and sure call it the 787-3 neo 😀

These are deliciously confusing. Boeing has definitely the advantage in the 240-290 seat market, AB will need something new, panel beating the 330 is not going to work.

If Boeing’s doesn’t do something in the upper end of the single aisle market they are toast there, but which is the right decision.

200-220 seat NSA or 220-240 seat NMA/MoM?

Whatever the decision, if the 322 is just a band aid 321 AB is losing the plot.

Fuselage skin layup is largely based on impact resistance not structural needs

That’s why the A350 nose is Al and carbon Fans have metal leading edges

I would have thought so too, the skins , Al or fibre are very thin to start with. The wing is the place to save weight for a smaller plane and with less fuel load a smaller lighter engine

I mentioned something along these lines a few times, comments about lack of commonality with 789.

But keep it simple, shrink the 789, new wingbox, wing (25% smaller), UF’s and you could still have a range of 6000Nm with 240-250 pax. Think of cockpit and cabin similarities, from production to the operational side.

Not a real MoM, cost to develop $5B?, but good bang for your buck and not introducing a new type to airlines fleets.

Hate to say it with my AB cap on but a 787-“7” and -9 could really go a long way. An 787-“97” with the -7’s wing, wing box, engines could be a serious machine for 1000-4500Nm routes along the lines of the NMA’s definition in the graph.

Just for the record, the graph has some administrative oversights taking the 737MAX to ~75 seats for example, or is that Boeing buying the E-jet program?

“Just for the record, the graph has some administrative oversights taking the 737MAX to ~75 seats for example,”

See the little low contrast diamonds ? Those are the real products 🙂

But this is what they call a real aircraft.

https://cdn.airplane-pictures.net/images/uploaded-images/2017/10/1/970588as.jpg

“same mandrels, bespoke layup. .. which is one of the great strengths of composites, easy tailoring.”

neither mandrel formers with embedded stringer pockets nor barrels as such lend themselves to leveraging that flexibility.

Are there comparisons around between AlLi and CFRP centric fuselage sections?

Once again Doug Harned demonstrates his knowledge, or lack thereof.

Does he want his 7-a-breast design powered by pixie-dust to keep competitive with the fuel burn of a stretched A322? Does he want it designed for free so they can keep non-recurring costs down to a competitive level?

Or what about the concerns about an orphan? You can’t exactly shrink it without being even more uncompetitive on a fuel burn basis – and if you stretch it you will have either insufficient range or have released a baseline that is too heavy == uncompetitive. Unless of course you make a separate wing. I suppose you could try to make do with ACTs, but the ovoid fuselage would leave a correspondingly smaller cargo area to make do with already, never mind adding fuel tanks to that.

Basically every charge he levelled against the CSeries would actually apply to this MoM – only it’d be far more expensive and have a much smaller target market! Ironically most of the reasons he gave for the CSeries line being shuttered didn’t apply!

How does an A332 compete against an A321neo at 2,500nm to 3,000nm, like for Hawaiian? I would like to see the economic analysis of that.

Randy Tinseth doesnt blog anymore, now we know why. Boeing has found different channels to getting its angle on the competition out there plus some speculative ‘well never build this but keep them guessing anyway’ stuff for good measure

Isn’t this just a modern A300? Or is it a bit shorter on range?

It seems that this Doug Harned – cited twice – has his own head, not related to reality.

It is fun to read and even more fun to read the discussion, but I do not believe his articles has any relation to the real life situation – I doubt his knowledge of Boeing or Airbus intentions, and to me his logic is to be polite “peculiar”

….have…

See Uwes comments in the last post. Brain the size of a house and years of experience in this field.

Who?

Doug Harned?

Never designed, analysed, built or maintained an aircraft component in his life.

Hes a ‘sell side’ financial analyst. That means its about marketing the employers company so that institutional investors will put their share orders on a target company through their trading desk.

Some wags have called sell side analysts as ‘high priced travel agents’ who arrange meetings between the buyers of stocks and the target companies management.

‘Buy side analysts’ are more interested in getting the fundamentals and their predictions right. Bernstein doesnt market themselves as buy side research.

A wasted and undignified career

What we wrote first was having United on-the-record with looking to put new 767-300ERs into its mix. People love sourcing.

And Puget Sound Business Journal was the first to specifically name United.

How would Boeing even build for a realistic price for the 15% margin overall they insist now is required?

Its on a very low production rate around 2 per month ( incl KC-46) and still made by traditional methods with lots of rivets. They wouldnt have invested in more automated methods.

United has its 3 class Polaris version of the 763 with only 183 seats or 2 class at 214. Compare with 2 class 737-900 with 179 seats. The newer 737-10 would be even better.

A look at Delta who fly A330-200s and they seat 234 in 2 class. It would be starkers to buy new build 763s when you can get end of line new build 332s with a slightly bigger capacity.

Hello dukeofurl,

The capacity of 179 seats you cite for the737-900 is for what in the US would be a legacy carrier domestic two or three class configuration, while the seating capacities you cite for 767’s and A330’s are for what in the US would be legacy carrier international three class configurations. In an apple to apples comparison, the seating capacity of a 767 or A330 in US domestic configuration is (soon to be was) much higher than for a 737-900, and neither 737-900’s or current A321’s have the payload/range or cabin space for a three class legacy carrier international configuration at anything close to an international range capability.

Some specific examples for Delta Airlines follow. All of the data listed are from the Delta Airlines public fleet page at the following link, except for the info on the two domestic 767-300’s still flying.

https://www.delta.com/content/www/en_US/about-delta/corporate-information/aircraft-fleet.html

737-900ER Domestic: 180 seats (20 first at 37 inch pitch, 21 Delta Comfort at 34 inch pitch, 139 Main Cabin at 30 to 31 inch pitch). Range 2,870 miles.

A321-200 Domestic: 192 seats (20 First at 37 inch pitch, 29 Delta Comfort at 34 inch pitch, 143 Main Cabin at 30 to 31 inch pitch. Range 2,565 miles.

767-300 Domestic: 261 seats (30 First at 37 to 38 inch pitch, 35 Delta Comfort at 34 inch pitch, 196 Main Cabin at 31 to 32 inch pitch). Range 3,515 miles. There are 2 still flying, N140LL and N1402A (which so far today has flown from Detroit to Raleigh-Durham and from Raleigh-Durham to Pittsburgh)

767-300ER International type 76L: 211 seats (36 Delta One at 77 to 81 inches pitch, 32 Delta Comfort at 35 inches pitch, 143 Main Cabin at 31 to 32 inches pitch). Range 6,408 miles.

A330-200 International: 234 seats (34 Delta One at 80 inch pitch, 32 Delta Comfort at 35 inch pitch, 168 Main Cabin at 31 to 32 inch pitch). Range 6,536 miles.

A330-300 International: 293 seats (34 Delta One at 80 inch pitch, 40 Delta Comfort at 35 inch pitch, 219 Main Cabin at 31 to 32 inch pitch. Range 5,343 miles.

As an aside, while wondering what Delta would use to replace 767-300’s on a morning Atlanta to Salt Lake City flight that I sometimes fly (the rest of the day is mostly 737-900’s and 757’s) I noticed that this flight is now being flown by an A330-300. How many passengers are going to pay extra $$$ for the lie flat seats on the A330 on a 1590 mile flight? Would not a domestic seating configuration be more profitable on this flight? On the routes I fly in the US, it seems obvious to me that the US big three have an aching need for something bigger than 737’s or A321’s, and much smaller than 6,000 mile range 300 passenger wide body aircraft with lie flat seats, for major hub to major hub flights at busy times of the day when there are enough passengers to fill a 737 or A320 every 30 minutes or less.

In Australia both Qantas and Virgin Australia fly a330-200’s on flights as little as one hour with fully lie flat business seating.

eg Sydney to Melbourne <500 miles

It seems to work fine for them

Maybe I was wrong above about the US Big 3 not wanting aircraft with international lie flat seating on Domestic routes. The following quotes are from an e-mail that I got today from Delta. See also the press release at the link after the quotes.

“Delta introduces industry-leading Medallion Member Unlimited Complimentary Upgrades for domestic Delta One.

Delta is launching its Delta One experience on key long-haul domestic routes, starting April 1, 2018, with select flights between the following markets:

◦Boston and Los Angeles

◦New York-JFK and San Diego, Seattle

◦New York-JFK and Las Vegas, starting May 1, 2018

Delta One will also become the premium offering April 1, 2018, on the following routes with one scheduled daily flight each:

◦Atlanta and Honolulu

◦Minneapolis and Honolulu

Delta One will be offered during strategic flight times on select routes as the airline works to customize the service offering to align with times when customers are seeking the Delta One experience, which includes flat-bed seats, elevated amenities and a refined dining experience. First Class service may be available on alternate flights on the route.”

“Delta already offers the Delta One experience on all flights on the following routes:

•New York-JFK and Los Angeles, San Francisco

•Boston and San Francisco

•Washington-Reagan and Los Angeles”

http://news.delta.com/delta-one-service-amenities-take-flight-select-long-haul-domestic-markets?mkcpgn=em_mktg_TNUP_CL_171120_AA008449_A01A_P0_CTA

I often see it said here that airlines don’t care about passenger comfort, my experience, and the above link both suggest to me that the US Big 3 are very aware of passenger comfort issues, but willing to provide more comfortable seats only to those passengers willing to pay for them, with cabin space being allocated to produce maximum income. Pay a little more, get a seat a little bigger, pay insanely more, get an insanely huge seat, not willing to pay more – bring a shoe horn to help you get into your seat. Personally, I usually cough up the extra $ for first class on domestic US flights longer than 2 hours if the upgrade situation doesn’t seem to be playing out well for me, but I wouldn’t cough up extra $$$$$ for lie flat (i.e. Delta One) seats on 2 to 5 hour domestic flights, so if Delta were to do away with domestic first class on such flights, I would probably have to switch my domestic allegiances to an airline that would let me slum along in plain old fashioned domestic first class.

The differences between the front and back is getting bigger and bigger.

Personally I feel airlines could offer a higher percentage of floor space to E+ which generally means one seat/row less than economy. Its most of the time fully booked.

Hello Anton,

Regarding E+, the airlines that I am familiar with, the US Big 3 (pretty much the only one that fly anywhere near the small US towns that I have lived in for the last ten years), have been spending lots of money installing E+ throughout their fleets over the last several years.

When I am flying US domestic on Delta every plane is usually almost full in every section, but from playing the upgrade game I know that this doesn’t mean that everyone in premium seats paid more for them. I believe that the airlines are very, very aware of how many premium seats they gave away to people who don’t pay extra for them, and how much of a markup they were able to get for the ones that they able to charge extra for. According to the article at the link below, Delta is proud of the fact that the percentage of First Class seats that they are giving away as upgrades is down from 85% to about 50%.

“Delta’s chief executive has been vocal about the airline’s efforts to sell more premium-class seats instead of giving them away for free through upgrades.

Delta used to sell about 15 percent of its first-class seats and now between 50 and 60 percent is sold, Delta’s CEO Ed Bastian told reporters last month.

“Any business where you give the majority of your best product away, it doesn’t work,” he said a month earlier at a conference.”

https://www.cnbc.com/2017/11/20/delta-will-offer-free-business-class-upgrades-for-us-travel.htm

Here, maybe, is the correct link for the article that I referenced above in which the Delta CEO was quoted as being happy about now giving away only about half of Delta’s First Class seats as upgrades.

https://www.cnbc.com/2017/11/20/delta-will-offer-free-business-class-upgrades-for-us-travel.html

Design a twin aisle 3,000nm aircraft with a CFRP wing, what does that look like? Bigger than an A321. 40 to 42m wingspan, possibly folding to 36m. Can use the current engines at 35K, so that saves time and money. At 100t MTOW, single axle main gear for simplicity and economic savings. 2-2-2 or 2-3-2 seating. Short fuselage model with field performance for Midway or other 6,000′ runways.

Probably 20-25% higher empty weight for the same number of seats. Who’s wants to pay the fuel for that?

Might United be looking at the almost ancient 767-300er because Boeing has told them that the MOM/NMA design has changed, and not to expect a more direct 767 replacement?

I agree with that. The crucial market is the A321 plus 20% more capability. A say, 170′, 2-3-2, 5,000nm aircraft is more like a A321 plus 50% capability. Maybe not the best move.

Now and then you read about tail strikes on the 321, not sure how much you can stretch before it becomes a real issue. The 752 was 3m longer than the 321 but it was a long legged stallion.

My personal view is that the 321 could be improved with an updated wing etc. but stretching, higher MTOW than the 321LR could have snowball effects from new (folding) wing, 4 wheel bogeys, engine requirements, etc. maybe this is better left for an A322NSA than doing a MAX10 on the 321?

Make hay with the 321 while you can, a Boeing MoM will hurt the 322 and a Boeing NSA could kill the 322.

Even 737 have tail strikes. Considering the numbers of both main single aisles in service its bound to happen

What I am trying to get to is that the 321 is still OK, but not sure what will if you stretch it 3-4m.

Think the 322 needs a major rework to happen and probably best left to an NSA with its own dedicated wing, undercarriage etc along the lines of the 757.

Now that the MoM/NMA are under discussion again, there is an obvious market in the US and Transatlantic but the big one Asia.

From my bit of experience I found these oaks don’t always show great patience during de-planing and their fondness of duty free result that boarding could become a bit hetic due to substantial volumes of hand luggage.

From an AB perspective they should therefore not overcook the length of a single aisle.

@Anton:

“321 is still OK, but not sure what will if you stretch it 3-4m.”

Such a 321(a.k.a. 322) would exceed the length of 752 by about 1.8~2.8m and without taller landing gears, its belly would still sit significantly closer to the ground than 752.

“..their fondness of duty free result that boarding could become a bit hetic”

Though would be irrelevant for flights within EU or U.S. domestic…2 large existing mkts for 321Neo/Max10 or 321Ceo/739ER earlier.

“From an AB perspective they should therefore not overcook the length of a single aisle.”

Clearly and despite taller+beefier landing gears than 321, Boeing did “overcooked” the 757 platform for the 753. Relative deliveries of 757 pax variants:

752=913 frames

753=55 frames

The 753 is only 53cm shorter than a 763ER.

@Anton:

“The 752 was 3m longer than the 321 but it was a long legged stallion.”

And it’s also 1 of the key tech reasons, aside fm diff design era, why @ similar seat count, 752 is structurally way heavier than any 321….4 wheels boogie is quite a diff ball game than 2 wheels boogie on a narrowbody.

“a Boeing MoM will hurt the 322 and a Boeing NSA could kill the 322.”

Though the exact opposite can easily be claimed by anyone i.e. 322 “will hurt the” MoM/797 and “could kill the” NSA….”Make hay” or no hay regardless.

Luckily, all 3 are hypothetical @ this stage likely with no more than a conceptual specs+3D model sitting on the desktop screen/hard drive of a designer/engineer @ Toulouse and Everett.

Think the flip in aerodynamic’s from single aisle is at ~220 seats if I can recall Bjorn’s post correctly, can’t recall the exact change from 2-3-2 to 2-4-2 but was somewhere around 260 seats?

Just in my simplistic way of thinking to go from 3-3 to 2-3-2 you add 18″+18″ for one extra seat, adding 18″ aisle for two 18″ seats will therefore make more sense for me, the following cabin widths for comparison.

320/146″, 767/186′(+40″), 330/204″(+58″), 787/216′(+70″).

If you knock off 1/2″ from each of the 330 seats to 17.5″ the cabin will be around 200″.

If you use the 737MAX8’s cabin width to length ratio as ideal a 200″ cabin 2-4-2 will have a fuselage length of ~56.8m (the 330-200/800=58.8).

So there it is. The next twin aisle, 200″ wide ovoid cabin, (2-4-2), ~57m long, pax ~240. Wing and engines depending on range/MTOW.

This shows that the 330-200’s fuselage is actually not far off the mark from a size perspective.

@Anton:

“This shows that the 330-200’s fuselage is actually not far off the mark from a size perspective.”

Only if the key design perimeter to determine optimal fuselage diameter is cross sectional seat count+aisle layout.

330 fuselage diameter is a direct design legacy fm 300. I’m not sure if U are aware that when Airbus determined fuselage diameter for 300 in the late 60s, the most important criteria used was not really how many seats across the minimum cabin diameter. It was chosen for the smallest possible diameter that can fit 2 LD3s side-by-side in the belly. It was a very logical Airbus design decision @ that time when LD3 was just invented(actually, it was the 1st ever containerized cargo system for pax airplane) and based purely on 747 fuselage specs. Naturally for better sales, LD3 compatibility was a design priority for the 300.

If U look @ the 300’s cross section, total area above and below main deck are almost equal….a very diff distribution fm the widebody cross section for all Boeings and even Airbus’ own 350. This is the primary reason why till today on the 330Neo, we still see the concave/attic effect on the cabin sidewall….outer edge of the window seat armrest cannot be pushed all the way to align closer with the max available cabin floor diameter and therefore by definition, some 330 cabin floor area are not utilized/wasted as seat space.

If designing a clean-sheet widebody with 8abreast today and LD3 space efficiency is not important(e.g. for route types now flown by 757/767 and soon 321LR), fuselage diameter will be smaller than 330.

This looks to me like a trial balloon being floated on behalf of Boeing by people who serve them.

Boeing spread FUD (Fear Uncertainty Doubt)? Who would have thunk it.

After having a bad nights sleep about this lot at least a few things dawned on me, the biggest the skewness in airframe types between larger single aisles and twin aisles relative to market size. The following if you leave the C919 and MC21 out for the moment.

Twin aisles (including freighters in production).

Boeing, 747, 767, 777, 787 (now talk of 797),

Airbus, 330, 350, 380.

“Larger” single aisles.

Boeing, 737’s (50 years old),

Airbus, 320’s (30 years old)

“Smaller” single aisles.

CS, E-jets, SUJ100, CRJ’s, ARJ21.

Something is horribly wrong here?

Which made me think that Boeing could have had two airframes in mind for their NSA. 2-3 (CS-MD) size and wider 3-3 (320/MC21).

That’s maybe why they are so unhappy with the CS amongst other things?

The larger was likely to be 160-220, now maybe 140-200 resulting in the 797 not to start at 240 but 220 (797-7?).

@Anton:

My gut feeling tells me it is beyond “Something is horribly wrong here” when someone is “having a bad nights sleep about this”…..

Never realized the C919 had 350-“like” winglets?

http://c.newsnow.co.uk/A/909955894?-303:3665:0

Literally they are looking at the 757

A shrink to compete with optimized/ stretched aircraft in core market (180 seats)/ 1200NM) with same engine technology is risky.

@Keesje:

A shrink(e.g. 333->332) to compete with optimized/ stretched aircraft(e.g. 763ER) in core market(220-250seats) with same engine technology(Except the RR option, the other 2 engine family options are common across 763ER and 332) seemed to worked well last time in Airbus favor….

Unless a shrink is always risky for manufacturer X but not Y?

Is the MoM/NMA market big enough to warrant a 2/3 aircraft family?

Shouldn’t the design optimization be for something really middle of the market that can be stretched or shrinked if demand warrants it.

250 pax, 5000Nm range, 50 KLb engines (basically 788, 338 size but 30% lighter, etc). Up and down sizing could then be 220pax/6000Nm and 280 pax/4000Nm.

The main market high density short-medium haul routes.

For some reason you left the unique payload-range capability that made the A330-200 successful.

@keesje:

“..you left the unique payload-range capability that made the A330-200 successful.”

And the relatively “unique payload-range capability” is somehow exclusive to the 332 and can never be repeated again by Airbus or Boeing in future programs especially cleansheet programs?

I think U were the one who originally “left the unique payload-range capability” as a factor per your shrink is risky comment….I’m aware of that factor all along.

Unique payload range for an 180 seat aircraft? Anything is possible but I don’t see a lot of demand..

@Keesje:

“Unique payload range for an 180 seat aircraft?”

Unique payload range possible only for a 250 seat aircraft which happens to be a 332?

And why 180 seats anyway? Why not 200 seats or even 190 seats?

We can play this game all day long…..bring it on.

Its week-end, relax.

But a thought for you, a single aisle has a seat/width ratio of ~0.85. you can calculate the others but you will sea that an 2-3-2 is note the greatest of layouts for air frame economics, seat/aisle ~0.78.

See AB says there was a 25% increase during the last 6 years of passengers carried by wide bodies on short haul routes.

So then why don’t they do something about it? An322 and 330-800 is not the answer, or is this a cat and mouse game as usual.

If Boeing waits a little longer Airbus will simply launch a payload-range sub series of the A321 and quickly score a thousands orders. Like 7 years ago with the NSA/NEO.

https://lh3.googleusercontent.com/-w0yvq58-h2M/WVuATjJFU0I/AAAAAAAABK4/RKFBEiw4WT83RjRqZa3UdwaP8kURPFHOQCLcBGAs/s1600/Airbus%2BBoeing%2BA322%2BMoM%2BConcept%2Bkeesje%2B737%2BMAX%2BA320NEO.jpg

Sometimes it seems Boeing believes nothing happens, if they take their time, lay out their options, discuss with all their customers, are happy with where they stand, take no hasty decisions, try to fully understand the market, build their business case, focus on efficiencies, the usual crap.

Are your words cynisism or sarcasm!

I agree they do need to get on with something. Airbus is increasing production and now have access to a new workforce educated in carbon. Add Russia/China into the mix, Boeings problems are mounting. Currently 55/45 in favour of Airbus. This could become 40/60, then 35/65 in favour of Airbus….

As LNC says, Boeing is invincible. If it goes wrong, the US tax payer will cough up, but it won’t be a subsidy and certainly not dumping!

Asia an China is deemed to be the market of the future. COMAC Jv looking at the 929. Maybe Boeing and AB can see from this what the East want and where the sweet spots are that’s missing from their line-ups.

https://www.flightglobal.com/news/articles/uac-and-comac-christen-widebody-family-as-cr-929-441648/

Hello Phillip,

According to the Reuters story out of Paris at the link below, dated 11-8-17, year to date sales (minus cancelations) of commercial aircraft are 288 for Airbus and 538 for Boeing.

https://www.reuters.com/article/us-airbus-boeing-orders/airbus-trails-boeing-in-orders-heading-into-dubai-showdown-idUSKBN1D82W8?il=0

By my high school math 538 divided by (288 + 538) is to three significant figures 0.651, which means that Boeing has accounted for about 65% of combined Airbus and Boeing sales year to date. This is also the year to date market share stated in the article. From 2010 to year to date I calculate a 52% to 48% split in favor of Airbus (7867 for Airbus vs. 7221 for Boeing) based on the sales data in the Wikipedia article at the link below. In what year do you predict this year’s trend in favor of Boeing will reverse and start the death spiral that you predict?

https://en.wikipedia.org/wiki/Competition_between_Airbus_and_Boeing

Airbus sales have been held back by production. They are still held back by production. Everytime Airbus announce an increase in production the slots get dold very quickly. Airbus have a backlog of 9 years. Customers can’t wait 9 years for an airplane, so they buy Boeing.

Lets see if Airbus announce further production increases. I think it will happen

More like a thousand tail strikes.

A322 with new tech LR wing @ 55T OEW approx / 48.5M length takes the A320 component set out its current limit.

105T MTOW means 240 32”x18” seats fully loaded to 4K NM’s and then some.

The fuselage stretch would be low tech / low risk.

The wing would offer a chance to bring sweat the CFD and deliver a industry leading design — start of a family of new tech wings for the AB single aisle family. A chance to show BBD — and the world — what they can do.

That would be the gradualist strategy.

The money shot would be the 325 and 328 models to aim for the heart of the MoM gap — make big in roads into the MoM range gap.

A328 = 75T OEW / 58.5M length using an A320 Heavy Duty component set as in new wing box and wing plus a strengthened centre fuselage — Super 60 @ nearly sixty years on.

150T plus MTOW means 300 32”x18” seats out to 5K NMs on a capacity of 50T of fuel / 40T plus usage.

A325 = 54.5M LR version aiming for longer range on the same MTOW.

Works NW Europe — eg Glesga — out to LA / HK and beyond.

The ME3 get worried as their aggregator/ distributor model starts to fail as more thin LR routes offering point to point become viable.

The engine element of the equation starts to get exciting.

100K lbs total thrust would be the ballpark figure.

Just a case of 2 — new tech don’t exist — or 4 where the new tech engines are commodity and their is competition.

Remember the A340 Mk2 was a huge missed opportunity.

The base question is what can 75T of OEW generate in the market?

How much real estate and how much opportunity / range?

High volume base — SA or low volume base — TA?

What offers the better value proposition?

Boeing are in a strong financial position, MAX and 787 production going well. B777-9 EIS 2020/21?

The question is can BA launch an NSA (210 seats) using 35KlB engines (MTOW 100T) and 250 seat NMA with 45Klb engines (MTOW 125T) in a relative short time of each other. Or will it be an 230 seat twin aisle with 40KLb engines? Lots of head scratching, no wonder its not launched yet.

The magic could be a new engine family that is used for both along the lines of the PW15/1900’s (73″) and PW11/1400 (81″ fans).

An EMB/BA partnership could work on a smaller (2-3?) NSA.

This will make my grey hair stand up straight under my Airbus cap, but it will be exciting for aviation and the airline business.

NSA is imminent

The next generation of jets may look like this thing: https://youtu.be/ohig71bwRUE

Forget the batteries. The point is to use many small electric powered fans to suck up non laminar flow. E.g. at the rear of a fuselage. Drag reduction could overweight the efficiency loss of power conversion to electricity.

BTW. the jet in the video has no empannage.

Building an old style NSA is not recommendable.

If Boeing goes for a 2-3-2 cross section for the NMA, they might consider specifying a wider container making better use of belly available space, maximizing cargo revenue potential. It could retain interchangebility with the widely used AKH / LD3-45 family of containers.

https://lh3.googleusercontent.com/-xLTg0IhbaHM/WgLinjG-zQI/AAAAAAAADPE/i7VKHyBMtu0Ix_OkpQxEw3ZozLL5rJDAgCLcBGAs/s1600/Extendable%252520AKH%252520LD3-45%252520Container%252520MoM%252520A320%252520NMA%252520Luggage%252520Cargo_zpsmcpdadpl.jpg

Keesje I can recall a wide aisle single aisle drawing (Greenliner) you posted a while ago with 2 aisles in the front.

Currently the 320 “uses” approximately 6×18″ + 20″ = 128″ of its cabin (of 146″). I know it will take a major cabin rework but is it not plausible for a “322 cabin” to have twin aisles in the front? Possibly 2 arrangements, one for shorter haul high density and the other for longer haul with flat beds.

1-1-1 (3 x 24″ =66″ for flat beds plus 2 x 29″ aisles), or you could go,

2-1-2 (5 x 18″ =90″), this will leave you with 38″ for 2 x 19″ aisles.

Hand luggage can still go in the side bins bin (but they will have to be smaller), ventilation, lighting, etc will have to be provided for the middle row, head room over the aisles the obvious hurdle.

Depends on requirements and layouts this could give you a twin aisles in the front of the wing with a single aisles at the back, even based on the A320/1 fuselage?

Just did a calc (incorrectly assuming a sphere for the fuselage, to have the same frontal and surface area as an 767 the 320’s cabin width could be widened by 12″ to ~158″ and 7″ inches to get to an A330 equivalent, if I am correct?

If Boeing goes 2-3-2 for the 797 it will have to be ovoid?

For the 1-1-1 should have been 3 x 24″ =72 with 2 x 27″ aisles.

What airbus needs to do;

1. Delete A319, replace with CS

2. Add morr Al-Li and bigger composite wings on A320 and A321 and A332 or whatever that’s is called

3. Change existing nose on A320/322 to CS series nose which is more aerodynamic

Done- all covered

Done

What are you going to keep the same?