Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Embraer counts on Boeing heft for E2 sales boost

By Scott Hamilton

July 22, 2019, © Leeham News: Embraer still appears to be in a bit of a holding pattern following the Paris Air Show in which it announced orders and commitments for only 76 EJets. Two additional orders announced at the show were previously under the Unidentified category.

This seems to be following a pattern set with the Bombardier C Series, in which sales were slow while the market waited for the deal to close in which Airbus acquired 50.01% of the C Series program.

Initial A220 orders

After the transaction closed, effective July 1 last year just before the Farnborough Air Show, Airbus announced at the international event orders from Moxy Airlines and JetBlue for the C Series, renamed the A220, for 60 each.

Bombardier started the negotiations. In the case of JetBlue, Airbus’ last minute majority ownership of the C Series proved to be decisive, LNA was told at the time. A “kicker” for A321neos, wrapping the A220 into the package, proved more than Embraer could overcome for its E195-E2. As the incumbent carrier, with E190-E1s at JetBlue, market intelligence indicated Embraer was favored in the campaign.

Airbus announced a follow-on order with Delta Air Lines by the end of last year, but sales of the A220 are taking off this year.

Airbus announced a follow-on order with Delta Air Lines by the end of last year, but sales of the A220 are taking off this year.

Lessor Air Lease Corp announced an order for 50 at the Paris Air Show. ALC’s endorsement is like the Good Housekeeping Seal of Approval, which in the US has long been a consumer branding gold stamp on products.

Lessor Nordic Aviation Capital committed to 20 A220s at the Paris Air Show.

Air France-KLM Group is poised to order up to 110 A220s as early as this month. A320neos will be wrapped into this deal. (The Group is also said to be planning an order for the Boeing 737 MAX.)

Embraer sales

Ever since the Boeing-Embraer joint venture was announced, sales slowed—just as they did for the already-slow-selling C Series.

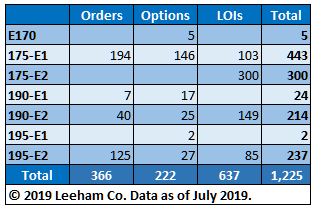

There are only 366 firm orders for all EJet types through mid-July, according to data reviewed by LNA. Fifty-three percent of these are for the E175-E1, principally from US Scope-Clause restricted regional airlines. The E175-E2 does not meet Scope requirements. At the moment, all 300 Letters of Intent for this model are from two US regionals, Skywest Airlines and Trans States Airlines. But these can’t be firmed up for use on behalf of US majors unless Scope is relaxed, an unlikely prospect any time soon.

The US accounts for about half the world’s regional jet market. This leaves the entire E2 family qualified everywhere else. So far, the E195-E2 is the preferred airplane. It accounts for 125 of the 165 firm orders for the E2.

At the pre-Paris Air Show Media Days, John Slattery, president of Embraer Commercial Aviation and CEO-designate of Boeing Brasil-Commercial, said certification of the E195-E2 will spur sales. The first airplane enters service with Brazil’s Azul Airlines in the second half this year.

But certification didn’t boost sales, so far, for the smaller E190-E2. It has only 40 firm orders.

Commitments

However, when Options and Letters of Intent are considered, the picture changes dramatically.

All-in, Embraer has 1,225 orders, options and commitments for the E1 and E2. It’s a matter of speculation how many will be converted to firm orders. It’s assumes most E175-E1 orders and commitments will be converted to the E175-E2 eventually. But in this case, “eventually” depends on Scope relief and with any change appearing to be off the table in current negotiations this year and next, 2023-24 is the next opportunity. Based on today’s pilot aggressiveness in contract negotiations, people are not hopeful about a change then.

This results in some wondering of The Boeing Co. will continue the E175-E2 program after the JV is closed, targeted by year end. Slattery, the CEO-designate of Boeing Brasil, won’t comment in advance of the consummation. In the meantime, he’s pressing ahead to finish the prototype, now in production, with a goal of first flight by year end.

The decision post-closing won’t be his to make. Boeing will own 80% of Boeing Brasil-Commercial and the board of directors will be dominated by Boeing designates. It may well be the E175-E2 becomes the Airbus A330-800 of BBC: a fine airplane with few customers (the A330-800 has only 10 orders so far).

The E195-E2, while not as capable as the A220-300 nor in the same seating class (about 10-15 fewer seats in two-class configuration), doesn’t fill the product gap in Boeing’s 737 line as well as the A220 does in the Airbus A320 line.

But with Boeing’s marketing heft, more expansive global services base, a much larger customer base and the ability to wrap 7-Series orders with the E2—all in the same manner that Airbus can between the A -Series and the A220—Slattery has high hopes that E2 sales will take off once the JV is closed.

The C-series has a payload range advantage, still with a competetive price the ERJ195E2 should be able to compete for airlines not needing the full C-series capability

Southwest needs to start replacing their 500 737-700, the 3 cabin crew core of their fleet.

Already before the crashes, SouthWest deferred most of their small 737-7 for 4 years. Westjet did the same, realistically evaporizing the 737-7 backlog. Proof ? No, because Boeing recently elected to make it invisible on their webside.

With the 737-7 situation being what it is, Boeing better puts energy in having a plan B with Embraer for Southwest. Deny / delay / ignore a bit, and the US build A220-300 has another big US customer. Maybe they are already too late.

https://groups.google.com/group/aviation_innovation/attach/35d4515a510e6/Embraer%20E200-E2%20Boeing%20737-7%20Southwest%20Keesje.jpg?part=0.1&view=1&authuser=0

That E200 would have a longer length to width ratio than any other plane, even the B757-300, or maybe pretty close. I wonder if the cabin would be as comfortable as the five abreast seating… I thinks the A220 is a much better deal. If Boeing made that, I would have to wonder if they would recoup their investment. Kind of a stop gap before an NSA.

The E jets have wider seats, guaranteed no middle seats and more aisle per passenger to hang around than a a220 or A320 😉

https://www.researchgate.net/profile/Jose_Alexandre_Fregnani/publication/312520488/figure/fig2/AS:452057221079041@1484790248092/Double-Bubble-cabin-cross-section-Source-Embraer-2011d.png

not sure I can follow the ‘wider seats’ argument. The link you posted states 18.25in seat width. I guess that picture is for the E Jets.

Isn’t C series 18.5 inches and 19 inches middle seat? http://www.airlinereporter.com/wp-content/uploads/2013/01/Cseriescrosssection.jpg

Based on my experience as a passenger, I would opt for a C Series over a E-Jet anytime. (Well, don’t think airlines will ask me)

Now the Mitac ‘Spacejet’ has the same width as the E1/E2 and 4 across but they dont have the double bubble to have an underfloor cargo hold, thats how they can be Scope compliant as far as takeoff weight.

With the roomer cabin of the A220 above them and the lighter weight SJ below , Boeing Brasil is in a tight spot. Time to bring out the discounts and the deals with the NMA!

But having 3 good planes in the 75 -145 seater market is great.

Wider? Not really. A220 has 18,5″ and 19″ as standard. E2 only 18,25″, and crampy, nartower fuselage.

A220-300 seems like a natural succesor of B737-700 (unless an airline wants specifically a Boeing for “political” reasons) with better capacity and payload than E2-195, and much better then 737-7 (because this doesn’t exist, and probably won’t).

Before MAX fiasco I was seeing that E2 will have very good sales because of Boeing overtake, but now, I’m not so sure, but they still has good possibility to ramp up orders after fusion.

The E2 sales were slow prior to the Boeing deal. My impression on the C-series was that PiPs were to slow and Airlines were rightfully concerned on how long Bombardier could support the type.

The PiPs are incoming.

The issue for E2s is the US market has so many of the airlines that buy used. Leasing companies need to know, if they get the price right, they will have some secondary market.

The E2-195 has potential. For a few more airlines, the E2-190. But with AA, AC, and B6 leaving the type, who will step up to be the volume (100+) buyer?

The profit shark campaign was started over two years ago due to poor sales/backlog. But all articles must simplify.

The E175 remains popular, keeping the line going.

E175 Popular ?

The total E series deliveries last quarter was 11. Eleven planes for both E1 and E2 series.

2018 in full, was better as 67 E175 alone were delivered (plus 1 E170)

The 4Q2018 numbers were 33 , so the drop to 11 for 1Q2019 is massive

I do see sales for the E195 incoming.

It’s cheap, and you can actually replace a lot of CRJs, B737-7 and A318/9 and all E1 jets with. So there is some market for sure.

I just don’t see airlines stepping down from B737-7 to an E2-195.

It’s the other way round: Airlines do step up, that’s why Max 8, 9, 10 and A321neo are selling so well, and Max7 as A319neo don’t sell at all.

Airlines are not longer about the 130 airplane, not even about the 150 pax airplane, they want a 180-200 Pax or even more airplane.

It makes sense. They are just more efficient and demand is exisiting.

It will be intresting to see when Airbus will push for the A220-500, and how the market will react.

It could actually be a killer plane for the smaller Boeing jets (E2-195 and the smaller Max).

Imagine you spent some hours in any wide body and then you jump in an E-Jet and knock your head first followed by the feeling you need to crawl on your knees to find your seat.

Most probably the SJ100 will be on the market next year, then airlines become confident to order SJ90s which are scope compliant and comfortable. Hence much stiffer competion than before (2 years ago E1 vs CRJ, now E2 against SJ and 220). Boeing will stop MOM and urgently needs successors for E2 and 737.