Leeham News and Analysis

There's more to real news than a news release.

Single-Aisle backlog market share between the Big Two

The rivalry between Airbus and Boeing intensified in recent weeks with Airbus landing another major order from a previously exclusive Boeing customer, LionAir. Boeing announced another major order just a day later, Ryanair, retaining exclusivity with this customer.

The market share battle between Airbus and Boeing was fierce and prolonged. The introduction of the A320neo family placed more pressure on Boeing, particularly when it became clear Airbus was going to land American Airlines as a major customer for Current Engine Option and the New Engine Option. Boeing, which had been dismissing the neo as a viable option and dithering about whether to proceed with a new design to replace the 737 NG, found its hand forced. Having no other choice, Boeing launched the MAX, a re-engined version of the 737 NG.

With all the recent orders, we’ve done the math and determined market share for the current generation and re-engined types and sub-types. This data is through March 31 and only includes orders that have been listed as firm contracts, not those that have been announced but not yet firmed up.

Sources are Airbus, Boeing and Ascend Worldwide.

First up is the market share within the 737NG and A320 families. Then we begin comparing Airbus to Boeing, followed by the same exercise for the neo and MAX.

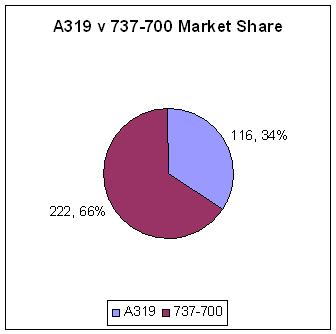

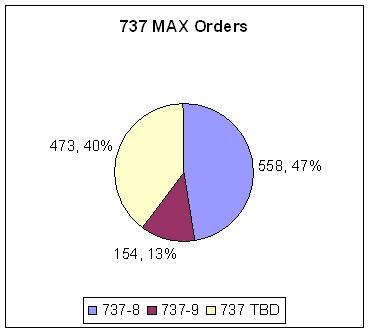

The following chart shows the backlog sub-type market share within the 737NG family.

- Southwest Airlines has 127 of the 222 -700 orders; it has conversion rights to -800s;

- WestJet has 30 of the -700 orders;

- Aviation Capital Group has 22 orders; it typically orders the -700 to take advantage of the lower deposits and progress payments and converts to -800s as it comes time to “cut metal.;

- Chinese carriers have nine of the orders;

- Russian Technologies has 15; and

- Unidentified customers have the rest.

There hasn’t been a -700 order since 2011.

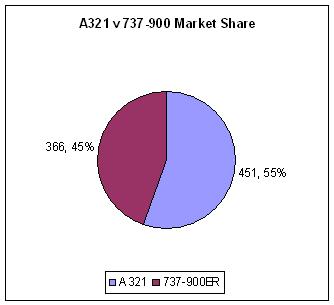

Airbus has a stronger backlog for the A321ceo than Boeing does for the 737-900ER, both in quantity and as a percentage of the family. Given that airlines which analyzed both models tell us the -900ER has a slight advantage over the A321ceo in economics and range, we were a bit surprised at this data. (We hadn’t looked at it for some time.)

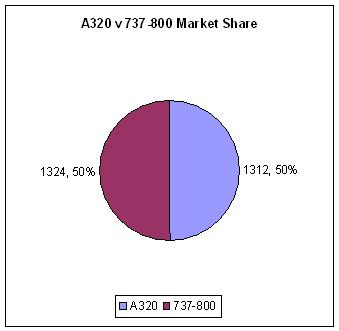

(The following chart shows the A320 market share at 35% and the 737-800 at 34% despite 12 fewer units. This is an Excel rounding issue.) Boeing holds a slight aggregate lead of 1,912 737 NGs to 1,879 A320 Family ceos, or 50.4% to 49.6%.

On the strength of Southwest Airlines’ 737-700 backlog, Boeing has a much greater market share of the 100-149 seat sector.

The A320/737-800 competition is equally divided.

Airbus has a solid market share lead in the A321ceo/737-900ER sector.

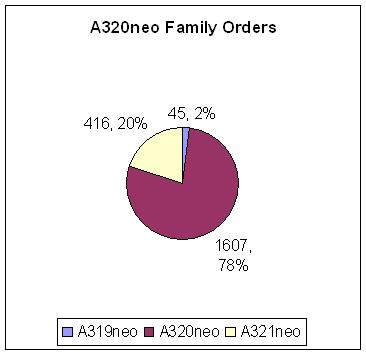

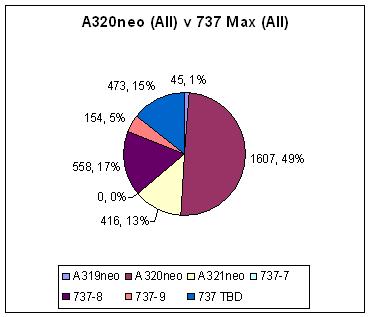

Airbus and Boeing often book orders that are changeable between sub-types. The following chart reflects the firm orders that have been identified. It’s possible that at a later date A320neo orders could be up-gauged to the A321neo and A319neos could be up-gauged to the A320neo or even the A321neo.

Boeing MAX customers also have switch-rights. Airbus does not list sub-types TBD; Boeing often does and the following chart reflects this.

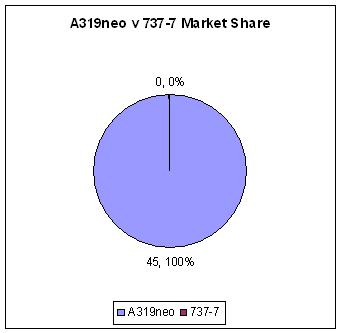

The following chart shows a head-to-head market share between Airbus and Boeing. The 0, 0% represents 737-7, for which no orders have been taken. Southwest ordered the 737-8 and has switch-rights for the 737-7, but when placing the order told us that it wasn’t at that time interested in the smaller model.

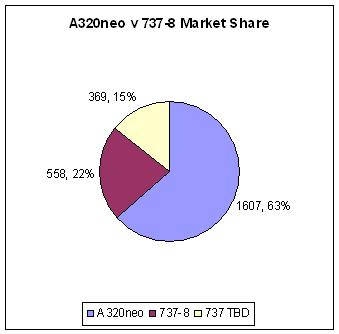

The following charts compare the sub-types between Airbus and Boeing.

For the market shares of the 737-8 and 737-9, we allocated the MAX TBD in the same proportion as the firm orders.

Boeing claims the 737-9 is far superior to the A321neo (not surprisingly). Airbus disputes this (also not surprisingly). The firm orders announced, along with our proportional allocation of the MAX TBD, nonetheless gives Airbus a huge advantage in market share.

The A321CEO/NEO has a strong lead over the B737-9(00)/MAX.

That might be a leading sign that Boeing will launch a new product in exactly that category.

Great insight and review of the sales, one quick request, is colour selection, would it be possible to set one colour for Airbus and one for Boeing (and use different shades), just makes it easier viewing. (eg. A320 is a reddish colour in one, then blue in another etc)

You can thank Microsoft….

Try to use PNG instead of JPG for monochrome pictures. You’ll get smaller pictures with better quality.

A couple of thoughts on this. The 900ER was only released in 2007 and airlines have presumably only been aware of the extent of the improvement since after that date. By all accounts the ER is a big improvement over the previous 900 model in terms of load and field performance.

There is a bigger size difference between the A321 and the A320 than between the 737-900/ER and the 737-800, possibly accounting for a different mix of models sold.

I get the impression that Boeing use the 737-900ER as a negotiating tool with airlines (rather than a discount, why don’t you take a bigger plane?) whereas Airbus prefers to keep the A321 as a premium product and charge accordingly. There’s no right or wrong: each manufacturer is trying to maximize its revenue across the range.

Whatever the reason, the 737 900ER is selling very well now.

How does the construction of the new Airbus plant in Alabama affect this going forward? I remember a few years ago leehamnet had discussed how it would possibly affect the tanker competition, etc. I guess that is a moot point now but I wonder if it would affect other future tanker competitions.

Personally, aside from the aforementioned future tanker competitions, I don’t see it as a big deal anymore. If a US-based carrier wants an Airbus, they will get it regardless of where the plane is built.

In the end, I believe it all comes down to availability, financing and fleet needs.

YMMV

Even though they play up the “Assembled in America” line, I am sure that Airbus is not expecting US based airlines to buy A320 series aircraft based on the Mobile facility being there.

I believe it is truly a long term goal for Airbus to diversify their production locations, reduce costs (US$ is much lower than the €) and to get a bigger footprint or presence in the USA. If a competition for a larger tanker comes out, Airbus will then be able to say they have an existing facility in the USA, rather than stating that they would build one.

That is a benefit of opening and expanding the Mobile facility. I believe the reasons are those as given above but the political and diplomatic benefits must have been evaluated as positives for such a decision.

The 737-900ER can fly further then the A321. Correct. So its the perfect 757 replacement, well.. The A321 can fly the 737-900ER’s maximum payload 1000 NM further. Also correct.

http://i15.photobucket.com/albums/a357/thezeke/range%20payload/f3a7d034.png

Then you can compare boths performance at MTOW (without mentioning the A321 carries 10.000 lbs more payload in that case). Or you can play around with “typical” seatcounts and calculate resulting costs per seat. In other words you can select the right conditions, restrictions to color perceptions, without lying.

The A321 NEO grows the capacity / payload range gab with the 737-9, using the GTF’s and 236 seats option. Also the differences in airfield performance/ required runway length are significant.

Boeing has 154 firm 737-9 orders from 6 customer, of which 100 are for United.

Airbus has 416 firm A321NEO orders from 20 customer, of which 130 are for AA.

http://www.pdxlight.com/neomax.htm

Is this analysis really worthwhile? With the market the way it is, it seems that what you can sell is purely limited by what you can build. Both Airbus and Boeing are running at 100% capacity. If there are open slots, there always ways to fill them (see last Friday’s sale of 18 A320s to Mandala airlines with delivery completed by end next year). So it seems more a matter of profit margins than volume. And margins we can only guess…

And for those who see the Mandala sale as a proof of Airbus weakness or strength: we will never know. They were either sold at rock bottom price because of open slots needing to be filled, or at record prices for the highest bidder because someone else deferred delivery and the slots opened up, or anything in between.

And I agree with the comments on the colours: the combination of default colours with a low image quality makes it very hard to read.

The most interesting factor is not so much the Airbus/Boeing rivalry, but the capacity P&W has to challenge GE (and indirectly Boeing) & transform the equation. P&W market share within the Airbus segment of the SA market is the factor to follow.

I think all three of Keesje, NdB and Mermoz have it right.

The A321 has bigger capacity, but flies farther than the A321 at some conditions. But both A and B are slot restricted, so it is a matter of margin, which is much more difficult to assess (by an outsider, i.e. any of us).

And the PW1000 is sure the thing to follow, especially once in service and with data on reliability/service cost. And once the first PIP is in place (couple of years after EIS I’d guess). CFM has a large user base in the MAX and GECAS power behind them, so they can fight fiercely.

For what it is worth, I think the CFM share on the NEO will not be all that large, definitely smaller than 50%, perhaps as low as 25-30%. I just do not see what it can offer (for the MAX it can be smaller/lower weight and with higher wing integration to counter some of the difference, but on the NEO?). GE are always very good with materials, and have state-of.the-art compressors (not a traditional strong point with PW, hence lots of MTU content historically), but it is enough?

not sure I agree with you re CFM vs GTF on the neo – currently LEAP has 30% of orders and GTF has 28% AND the GTF comes a year earlier or so. That suggests that the GE (AND Safran) materials/core AND the all important performance guarantees are pretty equivalent to the GTF package – http://www.pdxlight.com/neomax.htm

As regards to NG vs ceo (not mneja’s post, but on the original analysis)- you would expect the NG to have more orders – they have to produce the thing for a year (or more) longer than the ceo.

Aren’t they jsut around the corner from you? You can go have a chat with them.

=:-))

Difficult, the boss is away dancing with apes 😉

What I missed in this post for completeness is an overlay of CEO/NG backlog over the “must sell” available production volume.

Both airframers expect to change over to the new product in ~~~~2 years after EIS.

This gives a minimum number of available frames (still depending on production ramp up.. Obviously more CEO and NG frames could be build later on).

Will Boeing intermesh NG and MAX production on the same line or do a dedicated setup for the new type?

It’s my understanding that Boeing has been planning for awhile now to open up a third line in Renton for the MAX. They would use that new line to start, and then add MAX capacity by successively switching the 2 existing lines to MAX production as NG production tapers off.

I see that Turkish AL has just ordered 70 Max, so the 65% market share is more or less reflected internally in this Airline, which has ordered 100Neo.

I’ve said it before and I’ll say it again: the 737MAX is a DOG. I concur with BOEING’S OWN BEST CUSTOMER, RYAN AIR: IT IS RUBBISH.

Note to Boeing: this is what happens when you take a 50 YEAR OLD AIRFRAME and ADD TOUCH UP PAINT.

It doesn’t have the seat cost/mile, doesn’t have the commonality, doesn’t have a modern flight deck (I mean, come on, LIGHTS??? IN AN ERA OF LARGE FORMAT DISPLAYS??? HELLO! THE 1960s CALLED, THEY NEED THEIR VACUUM TUBES BACK!). Airbus cockpits are clean, common, modern, and are comfortable. Boeing’s cockpit in the 737, meanwhile, is a throwback to a different era.

Doesn’t help that many of the older hands are retiring and the new hands are being left with BLUEPRINTS and PAPER records. This old timer remembers when the offices were newer, fresher, cleaner, and young workers worked on the latest technology. Today’s graduates must be crestfallen when they enter the dingy, dark, dank, offices and pull out musty, yellowing, unintelligible notes and blueprints from the 60s. What’s a slide rule? If I was a new grad today, I WOULD LEARN FRENCH OR GERMAN and APPLY AT AIRBUS!

I admire what the 737 did for air travel, I really do, and the NG is bulletproof reliable. No doubt about that. But this old dog has essentially run out of tricks, and it’s time to be put to pasture. Remember and honor the legacy, and do what’s right. Make a new airplane.

Johan is a first-time poster. Johan, I draw your attention to Reader Comment rules. Your post is more toward the emotional side than factual discussion of issues. Please tone it down for future comments.

Hamilton

Pingback: Boeing’s Strategy for its Commercial Airplanes (BCA) division | The Talkative Man