Leeham News and Analysis

There's more to real news than a news release.

CSeries economy up to 3% better than advertised

Sept. 19, 2017, © Leeham Co., Montreal: The Bombardier CSeries has proved to be 1% to 3% more fuel efficient in service than advertised, the company revealed last week at its Media Day.

The improvements depend on the mission: 1% on shorter routes and 3% on the longer ones.

Better-than-advertised performance had been rumored, and reported, for months but this is the first time Bombardier confirmed the reports.

It also depends on the model. The CS100, a shrink design, is slightly better than advertised; the CS300—the optimized design—is the better performer.

Bombardier’s view of the sector

With Boeing’s redesign of the 737-7 MAX, adding 12 seats and adopting and shrinking the MAX 8 airframe, Bombardier reclassified the 737-7 as a “large single aisle” airplane.

The CS300 used to be compared with the 737-700 and the original 737-7 MAX design. The former carries 130 passengers in standard two-class configuration and the latter two carried 126. The new 7 MAX carries 138.

The reclassification happens to also takes away the comparison between the CS300 and the 7 MAX, at least in BBD’s view—an important distinction in the current trade dispute between Bombardier and Boeing before the US International Trade Commission and Department of Commerce.

Boeing correctly pointed out that even Bombardier compared the CS300 with the 737-700 and 7 MAX (when it was the old design, something Boeing didn’t distinguish in its filings). Boeing correctly pointed out that media (including LNC) did likewise.

Now, with the revised 7 MAX carrying 138 passengers to the CS300’s 130, Bombardier suggests the two airplanes no longer may be compared.

LNC sees this as a distinction without a meaningful difference. The 130-seat CS300 was four seats larger than the 737-700/old 7 MAX. It’s eight seats smaller than the new 7 MAX. But the CS300 is solidly in the 125-150 seat sector most commonly recognized as a dividing point in the 100-150 seat market—as are the 737-700, the old 7 MAX and the new 7 MAX.

In single class, the new 7 MAX can seat 172—but the CS300 can seat 160, both into the +150-sector.

Economics

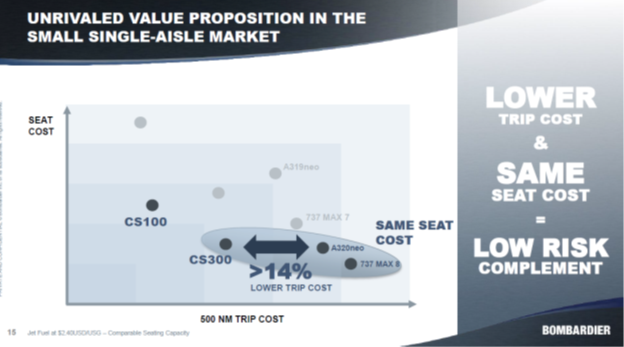

Bombardier claims the same seat-mile cost for the CS300 as the Airbus A320neo and a significantly lower trip cost. It’s presentation at the Media Day suggests a lower seat-mile and trip cost than the new 7 MAX design. (LNC’s analysis preliminarily suggests similar seat costs to each other but the CS300 has a lower trip cost.)

Sweet. Another great twist for Scott to twist the numbers and try and screw Boeing. At this point, Washington State ought to kick his ass out to either Quebec or France.

?????

Cher Scott,

Bienvenue en France ! Le Québec vous invite ! And you, whatever Jimmons you are, the critic is essential for a better world…

He is always welcome in Alaska!

Jimmons: Not at all.

@Steve Jimmons

Sweet — you’re right about that. Yet another in-service improvement for an innovative product from Pratt & Whitney. At this point, Washington State ought to ask Trump to kick Pratt & Whitney out to either Québec or France. How could they do it, how could they do that to Boeing — probably the most export-dependent company in the US.

…actually P&W has been in Quebec for decades… Yes, by all means lets shut down all competition and have as few manufacturers as possible. History shows that competition is the worst thing for innovation and pricing. Tow the party line or shut the hell up, I say. Freedom of speech is only for those who agree with me.

@Steve Jimmons

Boeing can easily bury BBD any time they choose. They can just build something even better and just as important,cheaper to produce.Its up to them, but it seems that they have decided that there’s not enough money in it.

Sweet, Oh yes! Love is like oxygen, willy won’t go, fox on the run, etc.

@Grubbie:

Boeing do find enough money in it.

Boeing Chicago HQ decided that to fight the CSeries program, investment in an army of Boeing lawyers will yield much better RoI than an army of Boeing R&D engineers.

Boeing stockholders probably agreed….

Is it a sign of panic setting in for Boeing in the single aisle market due to the slice of the cake getting smaller for the two big OEM’s?

In the 100-150 seat market the CS100/300, 150-200 seats the C919 and MC21 (CS500?), an 321+ lurking in the works?

Boeing and Airbus have more cake than they can stuff their faces with at the moment.

Taken, but in this business you must look and plan at least 10/15 years ahead and beyond?

If COMAC flood the market in China with the C919 a growth market could be lost to both Boeing and Airbus.

Could the US stop COMAC to sell the C919 for say US$40M in China?

Irkut and BBD.

https://web.archive.org/web/20170310025036/http://www.bombardier.com/en/media/newsList/details.bombardier-aerospace_20130828_irkut.bombardiercom.html

I understand why Quebec but why France?

320Neo was mentioned in the story and obviously linked to Toulouse/France but no attempt by Scott to directly compare 320Neo vs Max.

Anyway, may be Mobile Alabama is a bit more convenient or lower seat mile/trip cost than Toulouse France for relocating Scott…

As someone or other said:’A prophet is not without honor except in his own country…’

Beating the advertised figures sounds pretty good. I’m wondering if the C Series is building up to be an aircraft that airlines cannot afford to ignore. Whatever the economics of operating a 737 or A320neo, it’s just become another 1 to 3% harder to not buy a C Series.

A 3% additional saving sounds like a lot of money over the life time of an aircraft. Is that going to be enough to offset whatever “penalities” Boeing can persuade the US Government to impose?

That would appear to be the main question put forth to Delta, and they seem to think YES. Boeing is scared of this plane. Ten years ago, they hated the fact that Airbus was building the NEO. But at that time, they just couldn’t imagine that Bombardier could come up with something this good. There’s been a leadership vacuum at Boeing since they let Mulally get away. Their stock is only up because of the duopoly, travel has expanded and because Mulally did such a good job engineering and on the business side of the 777.

Hmm interesting. So Delta are effectively saying that the C series is worth it no matter what. That’s quite something.

I agree with your comment on Boeing. Though I think their problem goes back even further, to when the A320 first flew. Boeing didn’t do anything sensible about it then, and its all feeling a bit too late.

That is significant, wonder if Delta will go the sell and lease back route to recover some of the money.

Maybe Delta realize this could be a make or break for the CS and that their long term plan/s will be to operate CS500’s?

So save they will take the punch to save the goose that could be laying the CS500 eggs? And that is exactly what Boeing doesn’t want.

They want to build the MoM and not an NSA now.

@Anton:

“…wonder if Delta will go the sell and lease back route to recover some of the money.”

Not to recover $ but to avoid the case to go further triggering fine/penalty for anyone. It’ll be based on a 3-party agreement between DL, BBD and a foreign lessor and go something like this:

1. DL cancel the entire CS1 order on condition that BBD accept to sell the same order @ the same price to a foreign lessor nominated by DL.

This may wipe off the deal completely and erase the situation where BBD has an onging sales contract to deliver CS1 @ below cost to a U.S. buyer in the U.S. domestic mkt where Boeing operate. The case may be dismissed that way.

2. Foreign lessor order CS1 fm BBD @ the exact same quantity & price as per the now cancelled DL contract and sign CS1 lease contract with DL in parallel.

3. Foreign lessor lease those CS1s back to DL upon delivery @ unbelievably cheap rates as a function of the sales price level per the original DL+BBD CSeries contract.

I’m unaware of any anti-dumping law re leasing below-cost in the U.S. domestic mkt…..

Hello FLX,

Regarding your statement: “I’m unaware of any anti-dumping law re leasing below-cost in the U.S. domestic mkt…..”; the basic US Anti-Dumping statue, 19 USC 1673, states the following.

“For purposes of this section and section 1673d(b)(1) of this title, a reference to the sale of foreign merchandise includes the entering into of any leasing arrangement regarding the merchandise that is equivalent to the sale of the merchandise.”

Criteria for determining whether a lease is “equivalent to the sale of the merchandise” are set forth in 19 USC 1677(19). These criteria include the following.

(D)

whether the product subject to the lease is integrated into the operations of the lessee or importer,

(E)

whether in practice there is a likelihood that the lease will be continued or renewed for a significant period of time, and

(F)

other relevant factors, including whether the lease transaction would permit avoidance of antidumping or countervailing duties.

Based on the above cited USC sections, the chance of an airline evading anti-dumping penalties on a particular aircraft model that it had ordered, by instead leasing a similar number of the same aircraft model and operating them in its fleet for 10 to 20 years, is pretty much zero; however, an airline leasing aircraft for a period of several months to cover a period of peak demand, without having had a prior contract to purchase the same model aircraft, would have a pretty good chance of evading any anti-dumping duties in effect for that aircraft type. See below for the full text of the USC sections that I cited above.

Note also that the criteria for anti-dumping penalties in 19 USC 1673 do not require actual sales or actual injury, but only the likelihood of sales or threat of injury.

19 USC 1673

If—

(1)

the administering authority determines that a class or kind of foreign merchandise is being, or is likely to be, sold in the United States at less than its fair value, and

(2)the Commission determines that—

(A)an industry in the United States—

(i)

is materially injured, or

(ii)

is threatened with material injury, or

(B)

the establishment of an industry in the United States is materially retarded,

by reason of imports of that merchandise or by reason of sales (or the likelihood of sales) of that merchandise for importation,

then there shall be imposed upon such merchandise an antidumping duty, in addition to any other duty imposed, in an amount equal to the amount by which the normal value exceeds the export price (or the constructed export price) for the merchandise. For purposes of this section and section 1673d(b)(1) of this title, a reference to the sale of foreign merchandise includes the entering into of any leasing arrangement regarding the merchandise that is equivalent to the sale of the merchandise.

19 USC 1677

(19)EQUIVALENCY OF LEASES TO SALES

In determining whether a lease is equivalent to a sale for purposes of this subtitle, the administering authority shall consider—

(A)

the terms of the lease,

(B)

commercial practice within the industry,

(C)

the circumstances of the transaction,

(D)

whether the product subject to the lease is integrated into the operations of the lessee or importer,

(E)

whether in practice there is a likelihood that the lease will be continued or renewed for a significant period of time, and

(F)

other relevant factors, including whether the lease transaction would permit avoidance of antidumping or countervailing duties.

Just looking approximate list prices in US$, CS300 (85), MAX7 (90), A319NEO (100).

Then add the advantages of a modern fuel efficient aircraft to the CS, no wonder DL wants it.

Yes but how much does it cost to build. My guess is that the C series is much more expensive to build even after the learning curve.

@Matthew:

“..their problem goes back even further, to when the A320 first flew. Boeing didn’t do anything sensible about it then, and its all feeling a bit too late.”

Your comment mentioning 320 actually inspired me to start wondering this question:

Why Airbus has not leveled similar anti-dumping accusation against BBD when CSeries was sold to LH Group(for use by their Swiss brand) nearly 10rys ago?

1. Airbus is a domestic producer based in EU

2. LH Group is an entity based in EU(i.e. Buy in EU domestic mkt)

3. BBD is a foreign producer exporting CSeries into EU mkt.

4. I don’t believe LH Group bought CSeries for much more than DL has. Pricing on LH’s contract would @ least be below cost for those early units delivered due to their launch customer+operator status while DL is nearly a post-launch customer.

5. 319Ceo and later 319Neo are products which compete directly against CS3 by all logical tech metrics. In fact, both LH & LX already operate 319 in their fleets and their CSeries order eventually included CS3.

EU has no anti-dumping laws?

@FLX

In contrast to the hypocrites at Boeing, the management at Airbus seem to acknowledge that all of the players and OEMs in the industry rely on some sort of government support.

Now, it may appear as if Boeing has been dumping 787s all over the place – the EU included. However, Airbus would probably not want to risk instigating a “full-blown trade war” between the EU and the US, based on 787 dumping charges.

Since the 787 developmental programme was a near unmitigated disaster while the programme perpetually missed its production costs targets, by a massive margin, leading to a ridiculously high level of deferred production costs, Airbus has a significant financial leeway on A330neo pricing anyway, and can, therefore, easily tighten the screws on the 787, entirely at their discretion

OV-99:

While I agree fully with the first part.

So far, Boeing continues to sell 787s and the A330NEO languish – not even off the ground yet and maybe we should not to mention rate increase of the 787 (not that I agree but……)

It seems airlines don’ want old outdated aircraft (we will make an exception for the A320 and 7327 or course!)

@TransWorld

1) After the A330neo programme was launched, Airbus seems to have prioritised securing enough A330ceo orders during the transition to A330neo.

2) Since the launch of the 787 in April, 2004, Boeing has sold 1282 787s while Airbus has sold 1248 A330ceo/neo aircraft. Typically, Airbus detractors conveniently seem to ignore A330ceo sales.

3) Before the A330neo enters into service, there is probably little incentive for Airbus to aggressively start selling the A330neo at a significant discount to the 787.

4) The A330neo is obviously not an outdated aircraft. Not only is its RR engine equivalent to the RR engine on the 787, but the A330 itself has been continously upgraded since EIS. There are more than 100 operators of A330 aircraft. The majority of these operators are not like Singapore Airlines and Qatar Airways — airlines that are typically only buying the latest and “newest” aircraft.

5) Just by existing the A330neo is putting immense pricing pressure on the 787.

I have been going on about an A330-200″E”, NEO’s everything and GE engines. Maybe minor updates with 2-4% fuel consumption improvements, de-rated to ~65Klb

Not only for the longer haul LCC’s, but higher density <2000Nm routes. Almost all major domestic destinations in China and India are <1000Nm apart.

In the US the bulk routes between say Chicago and Phoenix, or where ever it is?

In times like now Ryanair could have used it. Think of pilot costs, airport slots, etc. In real terms an 300 seat configured A330-200(E) could be competitive on shorter haul?

Getting 300 people of a twin aisle is quicker than 200 on a SA.

Addendum

I’m quite sure that Boeing is not too pleased having to compete with the new 251 metric tonne MTOW versions. In addition to a serious range hike for the A330-900, it’s going to provide a solid foundation for both an A330-900F freighter and a stretched A330-1000. You ain’t seen nothing yet.

https://targetjobs.co.uk/employer-hubs/airbus/469896-wing-engineering-internship

Thanks, this makes my day (I wont get any of the jobs), was hoping for a 248 MTOW, In my part of the world the 242T, because of hot an high, the 330-300 was pushed for a realistic 5000Nm with full load.

This could be a game changer, think of an A330-800 with 8000+Nm range.

Guess 76Klb engines comes into play?

@FLX,

Airbus do seem to be a lot more easy going on the matter. But then I think they can afford to be – they can clearly sell lots of aircraft without too much difficulty.

And whilst market share is important, I suspect it’s far less important to Airbus (with their European business ethic) than Boeing (where Board members’ personal renumeration depends heavily on share price, share price, and only share price).

I also suspect Airbus see the C series as complimenting their own range; C series is all about economy, and being a little bit more comfortable / practical. That’s taken straight from the pages of Airbus’s book of Good Selling Points. Customers thinking that the C series looks promising are already in the right zone to appreciate Airbus’s offering too.

I often use the phrase “Develop, or die” (I fairly sure I’m not the original author!). You only have to do it a little bit quicker than your competitors. Boeing have not exactly been agile with their development program.

I wouldn’t be surprised if Airbus had a CF A320 replacement design well advanced just in case. The A350 development went like a dream, so they’re likely highly confident that they could have similar success for something smaller. For the moment they don’t need to produce it; Bombardier are small, and the A320neo is still selling quite nicely.

Hello FLX,

Regarding: “EU has no anti-dumping laws?”; the EU does have anti-dumping laws and they are pretty similar to US anti-dumping law. If interested, see the link below for more info.

http://ec.europa.eu/trade/policy/accessing-markets/trade-defence/actions-against-imports-into-the-eu/anti-dumping/

Looks like someone did take much more care in drawing the base graphic than the person making the textual attribution.

in the first graph Advantage never goes beyond 2.8%

in the second graph CS 300 sits slightly above the left arrow and the A320 slightly below its right arrow.

Amusing to see that the base graph was not fudged and

that careful data (reverse)extraction may give rather exact results.

This does seem to suggest that a CS500 would have mighty economics if they have the resources to develop it. I have heard talk of CS700 as well, is this feasible or a stretch too far on the current wing?

Maybe UTC will fund CS500 development to rival the 737 MAX which is exclusively LEAP. Especially since Boeing has decided to get into avionics. This could be by simple purchase of a bond offering in return for the exclusive engine contract.

The CS500 (4 or 5 more rows) can be done with the same wing. Leeham even had an analysis of it (paywalled) some time ago. A CS700 would need a new wing, new landing gear, would be reeeaaaallllyyyy long for 5-abreast and seems more like the dream of enthusiasts.

The MD90 stretched the original DC-9 to 46.5m overall length, while the Cseries

is 35m and 38.7m long.

I think there is a way to go before it gets too loooooong . Bombardier have history of going longer it the market is there.

Thats Boeings real worry, a 180 seater Cseries. Even if they only sold under 500 of the really long ones

@Sowerbob:

“…heard talk of CS700 as well, is this feasible or a stretch too far..”

Assuming yr hypothetical CS7 must be preceded by a hypothetical CS5, that will make the CSeries a family of 4.

Recent civil aerospace history has shown that for any family of 4 fm the same tech generation, 1 member would always lose out in the mkt:

318Ceo was a sales loser among the 320Ceo family of 4.

736 was a sales loser among the 737NG family of 4.

Max7 is still a sales loser among the Max family of 4.

Heck, even a 3 members family appear to be risky biz:

764ER was a sales loser among the 767 family of 3(Not counting sub-variants like 763 vs 763ER)

358(assuming this bird still exist in Airbus production plan) is a clear sales loser among the 350 family of 3.

788 is becoming a sales loser among the 787 family of 3.

May be it’s just bad karma for the CSeries if BBD ever try to develop a CS7….

The CS500 would be a less range but much lighter and more efficient than the 737-800 on shorter routes with quick turn-arounds thans to 3+2 seating. Like a modern DC-9 from the 2000’s. The question is if they can produce it cheaper than the aluminum 737-8 and charge the same with less capability but lower operating costs due to lower mass, cross section and lower fuel burn per pax. It might suit China better than the US that need full payload trans Continental range. 2265nm BOS-LAX, vs 1210nm Shenyang to Guangzhou or 1744nm Shenyang to Lhasa. So a single class 200pax 1500-1800nm + reserves CS500 with a 25-33% lower seat mile cost would find buyers.

With the latest revisions CS300 now has 3400 NM of range, so as far as I can see, even with no extra tankage, the CS500 will still be a trans con capable plane. As long as the wings have the margin for MTOW increase and the gear can be upgraded easily, I suspect around 2950 NM without a PIP from P&W. with a PIP 3100 NM is again in the picture. That is a helluva plane.

All this seat cost and trip cost is BS. Big time.

What counts for an airline is profit, not cost.

If cost goes up, but revenue grows even more, the airline will gladly take that cost delta.

Repeat:

Cost is BS.

Profit is king.

I can draw this on a board, if necessary, to make it easier to understand.

Er since Profit = revenue-cost……how can cost be BS. If your COST>then REVENUE you have a LOSS and THAT is NO BS.

Mark is correct. You make profit by having revenues higher than costs. And since few pax will pay more to fly a specific aircraft, you increase your profitability by reducing your costs.

The trip costs is relevant when comparing different sizes of aircraft: if you cannot fill the larger aircraft, you are still paying the trip cost for each flight.

No. The only way for an airline to make a profit is to control its costs. These are the only factors on which it can exercise control. It can not control the selling price: it is the market that decides. You’re not an accountant or a business executive, obviously …

The taxiway to Hell is paved with wannabe airlines that didn’t realise you can never sell enough seats below cost to make a profit – ergo, costs count: and when all that revenue accrues you’ll have even more profit.

@Paulo A Franke:

“If cost goes up, but revenue grows even more..”

This worked in an earlier era, pre-dereg(e.g. U.S. mkt before 1978), when effective fare floor existed(i.e. fares could go up but could not really go down) due to:

1. Artificially restricted competition in the mkt

2. High entry barriers party erected+enforced by regulators

3. Geographically very costly to promote any low fares & sell+distribute tickets because no http://www.???.com nor google.

That was an era when airlines could compete by charging more in return for giving us even more because there was no option/incentive in the reverse direction.

But the reality today facing airline CEOs is that increasingly tough competition anywhere worldwide, especially fm the ULCC gang and consumers armed with smartphones, ensure avg Rev$ per pax don’t grow much if at all and for the longterm.

In contrast, airline CEOs hv much more control over op cost and that’s the only part of the profit equation that they can realistically tweak. This is why vendors talking nonstop only about how much cost they can help airlines to save if buying their birds.

I wonder how much of the improvement is thanks to the PW engines and how much is due to the airframe itself. If it’s the engines, then presuambly that is osmething that will also benefit the Embraer E2 and the Airbus 320neo. If it’s the airframe, then it makes for a bigger advantage for Bombardier.

Could someone explain why the Pratt GTF engines on the A320 series are having issues but not the Bombardier C series jets?

Three reasons can explain this in my view:

1. The first A320neos have been operated in a harsh environment.

2. On the C Series the engine is mounted differently onto the aircraft, which makes it less prone to some of the problems we see on the Neo.

3. The C Series engine has been designed and tested first, and because of that it may be more robust, for it was presumably over-engineered to play it safe.

the way that airbus chooses to hang the engine on the pylon.

BBD has a “fan and core” mount, where A just has a core mount, which means that the fan weight is farther from direct support resulting in greater opportunity for the shaft to bow.

P&W should probably have put some more study into the static load effects of the core only mount, but likewise, airbus could have opted for the more robust mount…

Interesting Bilbo, hopefully AB will address this IF a new/updated wing on the A32X series ever happen.

@bilbo:

“P&W should probably have put some more study into the static load effects of the core only mount, but likewise, airbus could have opted for the more robust mount…”

I strongly suspect P&W already done all they could re engine mount design for PW1100G+320Neo integration within design parameters set by Airbus. Also, no way Airbus willingly still opted for a less robust mount without good reasons….these guys are pros and hv been dealing with 320 engine pylons+mounts for @ least 3 decades and know very well which part of the design could be revised within realistic time+$investment limits. It’s probable that to copy CSeries engine mount architecture(i.e. fan+core), 320Neo team might hv to substantially redesign many wing internal supporting structures for the area immediately adjacent to the engine pylon possibly with even more ripple on effects(e.g. recalculating many load paths) for the rest of the wing structure further out – making the entire Neo venture far more costly+time consuming than originally projected.

These new-gen giant turbofans for narrowbodies are amazingly fuel efficient but also much heavier than their predecessors(For 32o application, PW1100G is @ least 21% heavier than IAE V2500). Original 320 wing structural+engine mount design foundation done 3 decades ago likely never accounted for such level of weights & forces fm the pylon….

This leads to a far more simple reason why PW1000G hv far more integration issues with 320 than with CSeries:

Often easier /less design issues when pairing a new engine design with a clean sheet airframe design developing concurrently than with an existing airframe design.

Like the CSeries, MRJ also does not share the same engine mount design issue as the 320Neo.

Any idea what mount is used on the Embraer’s E2?

With Airbus certificating PW1100G and Leap-1A nose-to-tail on A319neo MSN 6464 only (not also using MSN 6620 as I believe originally planned), is it true that the PW engine/pylon combo was fitted first, before replacement with Leap for initial flight-test – and what drove that sequence? The PW engine/pylon is to be (re?)fitted in a few months’ time for cert flying next year.

Perhaps A319neo/PW eis is far enough out to provide time to do both on one machine (reducing flight-test costs…)? Or did something delay A319neo/PW testing, and Airbus fit the Leap because MSN 6464 was already kitted out to flight-test?

That’s interesting to here, things happens in the real world.

The PW1100G has much bigger fan of 81″ (frontal area-drag) than the CS’s PW1500G’s (73″).

Wonder if AB ever considered this engine for the 319? Thrust goes to 24KLb that will be good enough for the 319?

Its a somewhat different engine and it has a different mounting system that minimized the rotor bow issue.

So, the 737-700 or the -7 has a MTOW of 177K

C300 is 149K

How can those two compare at all?

C300 is lighter, has to carry less fuel to carry fuel.

Is there a figure that reflects this in fuel use?

Fuel burn per pax mile?

It seems that overall the C300 would have a 5 to 8% cost advantage in carrying passengers?

Lowe landing fees, lower tire costs, lower break costs all should have a value.

That’s maximum weight and also reflects the larger fuel capacity of the 737. What you should really compare is OEW, which measures the empty aircraft. In this case 737-700 is 83,000 lbs while the CS300 is 81,750 lbs — not a huge difference.

thysi: Thank you, now my brain hurts again.

C series made out of the latest greatest whiz bang lite stuff, 1 seat narrowed and is less than 3000 lb difference vs the old tech 737.

Put jet engines on a DC-3 and the heck with the rest of this stuff?

Talking DC3, think you will appreciate it, this is a real beauty. Carried out a number of surveys for us, had privilege to fly in this bird.

May you have seen it, carried out many surveys in the Northern America’s.

http://www.spectrem.co.za/

I don’t know … the difference does seem too small. But as far as I understand things, OEW is the actual weight of the airframe + engines.

@Transworld:

“the -7 has a MTOW of 177K…C300 is 149K…How can those two compare at all?”

Easy. By manipulating/omitting those figures in your anti-dumping case document submission to the Trump administration where anyone involved in the ruling decision probably has no idea what is MTOW.

Nex anti-dumping case submission by Boeing will probably be about how MRJ90 sold @ below cost to Skywest hurting Max10 sales campaign @ DL & AA in the U.S . domestic mkt purely on the basis of both types having single aisle inside the cabin and therefore comparable products….

The Q400 max capacity is a claimed 90 at 28″ pitch. There are talks of a stretch. +3 Rows will make it 102 seats.

So banned from the USA, threatening the existence of Boeing and the US economy?!

Considering two cylinders that roughly represent a 6 abreast and 5 abreast solution for 150 seats. The six abreast cylinder is 152″ wide by 115′ long. The 5 abreast cylinder is 132″ side by 130′ long.

The six abreast solution has 33% more frontal area and 2% more surface area. From a drag perspective, clearly proportion matters.

Great article, I wish a comparison between A380 & B747-8I usage and utilization can be made for the same carrier in future.

Seat numbers are a very poor way of comparing something as complex as an airliner, even if they were the same. On the other hand,maybe Boeing has a bit of a point, the C series should be much more expensive than the 7 max. Perhaps Boeing might be doing BBD a massive favour in highlighting how much better their product is and handing them a billion extra $, by forcing them to abandon unnecessarily suicidal prices. Surely it’s better to renegotiate the price than hand the money to the lawyers and US government?

@Grubbie

“My guess is that the C series is much more expensive to build even after the learning curve.”

Well, my own “guess” is that the C Series will be cheap to build at high volumes.

First of all the labour costs in Canada are relatively low compared to Boeing and Airbus. And the new Final Assembly building in Mirabel is a state-of-the-art facility that should work extremely well once it will have been supplemented with the Secondary Assembly building.

Phase 1 of the construction project was meant to give Bombardier the capacity to produce 120 aircraft a year, but they now think the new facility can produce at least 140 a year, and possibly as many as 150. Phase 2 would double that to 300.

It’s the same thing in Ireland where the wing assembly takes place in a state-of-the-art facility that can manufacture wings in great quantities and very efficiently.

As for the fuselage they are not there yet because the Chinese supplier is not up to the task (to be polite). In the meantime a large portion of the work is done in Belfast and this indeed adds to the manufacturing costs of the C Series.

The aft fuselage and the pressure dome are made of composite material and both of them are manufactured in Montréal (Saint-Laurent). So is the cockpit. The Saint-Laurent facility is highly automated, and like Mirabel it makes extensive use of robots.

The composite empennage, which includes both the vertical and horizontal stabilizers, is made in Italy in the same facility where the 787 empennage is made. There should little difference between the two except for size.

That being said, three problems remain to be solved before Bombardier can produce the C Series cheaply:

1. The C Series production rate has to be increased to 140-150 aircraft a year.

2. They need to solve the fuselage production problems they have with China.

3. Phase 1 of the construction project in Mirabel has to be completed; this includes a new Secondary Assembly building, a new store and a new paint shop.

The CS’s looks and probably are very good aircraft, but if I was a lessor I would start ordering 190/195E2’s?

@Anton:

“…if I was a lessor I would start ordering 190/195E2’s?”

Then why U or more lessors hv not been doing that? After all, E2Jet has been for sale for 4yrs.

190/195 portion of the E2Jet program has sold 75 frames to 2 lessors while CSeries program has sold 80 frames to 4 lessors. Pretty neck-to-neck in terms of attractiveness to lessors @ this point just by sales data.

Think there are a lot of lessors watching the outcome of this, the US pilot restriction story another Boeing invention?

@Anton:

“Think there are a lot of lessors watching the outcome of this…”

Think U may be nice enough to answer the question I posted for U earlier….

“the US pilot restriction story another Boeing invention?”

Which is totally irrelevant to the U.S. mkt prospects for the CSeries or 190/195E2 regardless of invention by Boeing or not.

The ‘true’ story talks about a long running clause within Big3’s pilot union contracts specifying an aircraft’s MTOW must be below certain limit if flying of that aircraft(typically a RJ) for the Big3 is outsourced to a 3rd party operator(e.g. SkyWest). That MTOW limit is so low that even the MRJ90 and 175E2 hv exceeded that limit….let alone the far heavier CS1/3 or 190/195E2. Big3 hv been trying to negotiate with unions for yrs to raise that limit slightly to also cover MRJ90/175E2 so out-sourced flying by regional partners can continue with more efficient new gen RJs.

Good idea to get yr story straight 1st before speculating any company inventing any story…

Apologies, start losing track, still squeezing in some work stuff (for a Canadian company!!).

On the E2’s I believe their purchase price (per seat) and seat OC ‘s will be very competitive. The 2-2 seating (~18.x “) are very nice.

I am aware of some kind of restrictions on weight/size. Didn’t know it was restricted to the big 3’s pilots Union.

Who gains from this and, what will happen to for example the E-1xxE2 sales in the US if it gets lifted?

That’s why it’s expensive to build, low volume and a lack of money to invest in plant.

What if BBD breaks out the price of engines and plane into two separate deals, and moves all the discount onto the engine package. Since the engines are US made, can you “dump” US made engines into the US market? BBD can also charge an integration fee for engines as a service performed onsite at Mirabel. Boeing does not make engines so good luck complaining to the ITC on dumping of US built engines into the US market.

Most likely, but only if mounted on a Boeing?

“Since the engines are US made, can you “dump” US made engines into the US market?”

The C Series engines are actually made in Canada.

@Normand Hamel:

“The C Series engines are actually made in Canada.”

Not true.

P&W(More precisely P&W Canada) does hv large ops to build/assemble aero engines in Canada. However, all are for helicopters, turboprops and private jets applications….I don’t think CSeries belong to any of these categories.

Where is the MC21’s PW1400G’s “made”. Irkut is working on their own GTF, the PD14, up to 34Klb.

@Anton:

“Irkut is working on their own GTF, the PD14…”

None of the above is true…..no idea why folks here enjoy spreading mis-information/news due to being busy @ work or whatever other reasons/agenda….

1. Irkut hv never done engine development. They’re an airframer.

2. PD14 is under development by Aviadvigatel which has always been an engine developer+manufacturer.

3. PD14 does not include any geared fan architecture.

4. A derivative of PD14 for a potential future engine program, the PD18R, is planned to use geared fan architecture to be paired with a PD14 core. However, PD18R is no more than an early concept /’paper engine’ @ this stage.

Given how long it took P&W to develop+certify PW1000G family and RR still not yet achieved cert for any UltraFan-based engine, I est. it’s gonna take Aviadvigatel @ least 5~7yrs to achieve cert for PD18R even if they somehow decide to officially launch development tomorrow by taking some R&D staff resources away fm the still ongoing PD14 effort.

I am aware of that.

@Anton:

“I am aware of that.”

Yet U still chose to spread incorrect info……

Amazing.

For those interested in the PD14 engine FOR the MC21 see link.

http://www.ainonline.com/aviation-news/air-transport/2017-04-18/russia-commits-full-scale-production-engine-mc-21

GTF made all over the world, but Bbd engines assembled in Canada. There really is no “home” market for the Cseries. By value it would be the US.

” it is establishing a global network of assembly sites that include: Middletown, Connecticut;

North Berwick, Maine;

West Palm Beach, Florida;

Mirabel, Canada;

a facility managed by Pratt & Whitney’s collaborator, MTU in Germany; and a facility managed by Pratt & Whitney’s collaborator MHIAEL in Japan. ”

http://www.pw.utc.com/News/Story/20170803-1200

Hello Mark,

Regarding your suggestion that: “BBD can also charge an integration fee for engines as a service performed onsite at Mirabel”; I believe that such a scheme to evade antidumping penalties by having the customer in an antidumping case supply the manufacturer in the case with subassembly components, for which the manufacturer then charges an assembly or processing service fee, instead selling a fully processed or assembled product directly to the customer, is not likely to succeed, due to recent US Supreme Court precedent in a similar case. For those not familiar with the US courts, the Supreme Court is the top US court; its decisions are final and cannot be appealed.

The case that I believe makes such a scheme unlikely to succeed was United States vs. Eurodif. Eurodif is a French company that operates a uranium enrichment plant that services US power reactors. Eurodif claimed that transactions in which US companies purchased unenriched uranium, which they then shipped to Eurodif to be enriched under uranium enrichment service contracts, were exempt from the antidumping duties that had been imposed on enriched uranium from the Eurodif plant. The US Court of International Trade and Federal Appeals Court ruled in favor of Eurodif; however, the US Supreme Court ruled unanimously in January 2009 that the transactions in question were subject to US antidumping duties. Following are some excerpts from the Supreme Court’s ruling in the case, and a link to the full ruling. Not all Supreme Court rulings are unanimous, and very few contain the word “absurd”.

“SUPREME COURT OF THE UNITED STATES Nos. 07–1059 and 07–1078

07–1059 UNITED STATES, PETITIONER v. EURODIF S. A. ET AL.

07–1078 USEC INC., ET AL., PETITIONERS v. EURODIF S. A. ET AL.

ON WRITS OF CERTIORARI TO THE UNITED STATES COURT OF APPEALS FOR THE FEDERAL CIRCUIT

[January 26, 2009]

JUSTICE SOUTER delivered the opinion of the Court.

Section 731 of the Tariff Act of 1930 calls for “antidumping” duties on “foreign merchandise” sold in the United States at “less than its fair value,” 19 U. S. C. §1673, but does not touch international sales of services. These cases test the application of this antidumping provision to imports of low enriched uranium (LEU), a highly processed derivative of natural uranium used as nuclear fuel, when domestic utilities contract to obtain LEU for cash plus unenriched uranium delivered to a foreign enricher. Although the parties’ contracts call these transactions sales of uranium enrichment services, the Commerce Department treats them as sales of “foreign merchandise” subject to the antidumping provision. The issue is whether the Commerce Department’s way of seeing the transactions as sales of goods rather than services reflects a permissible interpretation and application of §1673. We hold that it does.” ……

“These are good analytical grounds to show that SWU transactions are reasonably placed within the ambit of sale of goods, and the Department’s reliance on them is reinforced by practical reasons aimed at preserving the effectiveness of antidumping duties. There is no dispute that LEU sold under an EUP contract at less than fair value must be subjected to antidumping duties under §1673, there being a clear sale of goods when a domestic utility pays a single sale price in cash for the feed uranium and enrichment components represented by LEU. If foreign enrichers set this price below the fair value of LEU, the domestic enrichment industry is obviously open to material injury, the very threat the antidumping statute was meant to counter, see H. R. Rep. No. 1, at 23. But the same injury would occur if a SWU contract were untouchable. Under a SWU contract, the domestic utility pays cash to a third party for unenriched uranium and provides this along with additional cash in exchange for LEU; any EUP contract could be structured as a SWU contract simply by splitting the transaction in two, one contract to buy unenriched uranium and another to enrich it. And the restructuring would not stop with uranium; contracts for imported pasta would be replaced by separate contracts for wheat and wheat processing services, sweater imports would give way to separate contracts for wool and knitting services, and antidumping duties would primarily chastise the uncreative. The Commerce Department’s attempt to foreclose this absurd result by treating SWU transactions as sales of goods is eminently reasonable.

III

Where a domestic buyer’s cash and an untracked, fungible commodity are exchanged with a foreign contractor for a substantially transformed version of the same commodity, the Commerce Department may reasonably treat the transaction as the sale of a good under §1673. We therefore reverse the judgment of the Federal Circuit and remand the cases for further proceedings consistent with this opinion.

It is so ordered.”

Here is a link to the full opinion.

https://www.supremecourt.gov/opinions/08pdf/07-1059.pdf

In the first paragraph of my post above “instead selling a fully processed or assembled”should have been “instead of selling a fully processed or assembled”.

Who is going to be the winners and losers here.

Some Boeing lawyer that gets a fat bonus and share options for saving the company?

Another winner most likely Embrear, the E’s are not bad aircraft, but that’s not the way it should earn its place.

People in Canada, US and Ireland losing their jobs and US airlines not able to fly aircraft that is the best in their class?

Life certainly is not fair.

Think we’ve seen it. You in beautiful Alaska and I am in “my” African bush.

Life is good!

Live and let live my motto, especially in a case like this.

@Anton:

“Another winner most likely Embrear”

Another mysterious claim by U.

Pls kindly explain how EMB can directly benefit fm whatever outcome fm this BBD+DL vs Boeing trade dispute. I can only see everyone, including EMB, exporting jets to the U.S. domestic mkt fm now on hv far less pricing flexibility in doing deals.

Production cost of the E-195E2 most likely significantly less than the CS100.

The list prices that I could get get is 195E2 <US70M and that for the CS100 ~US$85M.

http://www.ainonline.com/aviation-news/air-transport/2017-03-07/embraer-rolls-out-first-e195-e2-brazils-largest-aircraft

@Anton:

“Production cost of the E-195E2 most likely significantly less than the CS100.”

Assuming your claim is true(I’m not doubting), that cost differential would logically remain unchanged with or without a BBD+DL vs Boeing trade dispute case.

So how can EMB suddenly be declared as “Another winner” only because BBD/DL lost a legal case against Boeing? That lost makes the deal costly due to penalty but does not change the CSeries sales data.

Furthermore if U’re saying 190/195E2 should win against CS1/3 because of its relatively lower production cost, why sales data do not reflect that expectation? Most importantly, EMB ‘should win’ does not equal to EMB is “Another winner” as U claimed.

Dasault win

That one crossed my mind, but the SU35 is well adapted to icy conditions.

Boeing, the lawyers, and Embraer will win.

I really can’t see boeing getting much out of this.

@AS:

“…Embraer will win.”

Pls kindly explain how.

If the CS100/300 is effectively “banned” from the US what 100 seat aircraft will airlines resort to?

@Anton:

“If the CS100/300 is effectively “banned” from the US….”

How they can be “banned”?

Assuming U’re talking about BBD no longer able to sell CS1 @ below-cost due to this trade dispute case/outcome, the same will be true for all importers such as EMB. Same rules apply to all foreign vendors in the U.S. mkt.

I beg U pls don’t tell me EMB doesn’t need the ability to sell 190/195E2 @ below-cost like BBD because their cost is already lower than CSeries. It’ll only further expose how little U know about how sales work in this industry for ALL players mkting any newly developed design and EMB is not immune to that.

Just try to think in terms of my little alternative universe where EMB won the DL contract to acquire 195E2 instead of CS1 also in that competition. That contract would still likely included below-cost pricing. Boeing would still dragged EMB into a trade dispute battle in which below-cost 195E2 is hurting 73G sales in U.S. mkt. So how could I declare BBD a winner in such case?

“Banned/Black listed” whatever you want to call it. Duties could be imposed on all 100-150 seat commercial aircraft from Canada that will make effective purchase price high.

Wonder if duties will also apply for sparse when in service for example?

You can buy them but it is going to cost you!

@Anton:

“Duties could be imposed on all 100-150 seat commercial aircraft from Canada..”

A scenario that exists only in your strange dream which does not hv a shred of reference/connection to how U.S. anti-dumping trade rules+penalty system work in reality. No wonder U incorrectly assumed EMB will be a winner fm this trade dispute.

A foreign producer is found guilty in a deal because that deal involves selling a product in U.S. mkt @ a unit price that is below its unit cost which hurt U.S. producer selling similar/same product. As a result, a fine is imposed for each unit of sale within that deal. Furthermore, the fine is equivalent to the diff between unit price stated on contract and unit cost determined by Trade authority which effectively makes the unit price on contract+fine=unit cost.

That’s it and that’s the extent of such penalty where its only objective is to return effective unit price to unit cost in any sales transaction by foreign producer. Foreign producer is absolutely allowed to sell @ a price=cost in U.S. mkt. If Boeing price for same/similar product still can’t match that price in U.S. mkt, tough luck for Boeing. U.S. anti-dumping law is not designed to enforce pricing by foreign producer to match pricing set by domestic producer.

After BBD/DL paid the fine re dumping in this case, no U.S. authority will impose any fine on whatever BBD will sell again to whomever in the U.S. Nor will they impose any fine on whatever DL will buy again fm whomever in Canada as long as those deals do not involve selling @ below-cost.

Applying a blanket ‘blacklist’ to all products fm Canada/BBD on all transactions/deals, even if all those deals are compliant with U.S. anti-dumping rules, describe more about a trade war between 2 nations which is well beyond U.S. anti-dumping law jurisdiction. It’s possible the current DL/BBD vs Boeing anti-dumping case can trigger that but penalty due to dumping can only be applied towards specific contract(e.g. DL+BBD’s contract) that’s violating anti-dumping rules.

I took it from AF Roberts response;

From Subject Received Size Categories

Leeham News and Comment [New comment] Pontifications: Next steps in Boeing-Bombardier trade complaint Tue 3:37 53 KB

@Anton:

“I took it from AF Roberts response…Tue 3:37 53 KB”

I hv no idea what U are talking about nor referring to.

Basically, I think U are confusing:

A) Fine/penalty due to dumping by 1 foreign producer in specific sales contract(s)/transaction(s).

vs

B) Trade tariff/duty erected against all products imported fm specific foreign nation(s)/producer(s).

A) and B) are not the same thing for anyone who has basic knowledge in int’l trade or history/trend of global trade protectionism vs liberalization.

In essence:

A) only ensure foreign producers do not set price below their cost.

B) completely ignore cost and only ensure foreign producers are effectively setting price @ or higher than the price of domestic producers.

Many nations hv A). Most used to hv B) but no longer since the advent of WTO because WTO membership rules outlawed B) @ least in theory.

@FLX

All the C Series engines have been made in Canada, except for the first few units, which were made in the USA. However the design of the engine was done in the USA, if that’s what you meant.

To be more specific, the PW1500G is a Pratt & Whitney engine that is currently assembled by Pratt & Whitney of Canada.

As for the other GTF variants, my understanding is that all of them are made in Canada as well, except for the A320 variant (PW1100G).

But apparently the A320 engine might also be made in Canada eventually, in order to supplement production of existing PW1100G facilities located in the USA and Germany.

The PW1100G would fill the gap left by the delayed MRJ programme, which uses the PW1200G. And this would rather be convenient because the PW1100G production has fallen behind.

All this could change in the future though, as the situation continues to evolve.

The plot thickens, 350 with Zodiac cabin supply problems, PW1100G’s for the A320NEO’s made in the US with problems.

Wonder if AB could claim damages?

Nope here is the list of P&W Canada products:

http://www.pwc.ca/en/engines/turbofans

The P&W 800 uses the Cseries core, and its possible the core is exported to the USA for Cseries engine production, but the engine is not made in Canada.

@Mark from Toronto:

“Nope here is the list of P&W Canada products…the engine is not made in Canada.”

That’s my understanding too re no PW1000G family assembled in Canada also based on info fm the the same P&W Canada official website.

So I hv no idea what Normand Hamel is talking about.

GTF assembly locations;

Connecticut, Florida, Maine, Montreal Canada, Germany, Japan

http://www.pw.utc.com/News/Story/20170803-1200

@Normand Hamel:

Apparently, U are correct and product range info on P&W Canada website may not be conclusive(don’t know why though).

PW1000G(Most likely the PW1500G variant) is also assembled @ Mirabel:

http://www.assemblymag.com/articles/92405-pratt-whitney-rethinks-jet-engine-assembly

A 3m stretch and the CS500 is the size of the A320, another 2m stretch and the CS700 is the size of the 737-8. The fundamental value is there to be harvested by some investors. Just a matter of time, and who will prime the pump.

Someone made a comment about the number of aircraft types in an aircraft family, 2 is generally good, with 3 one of them fall of the bus. If you 3 it must include wing, landing gear etc changes.

Maybe the CS300 should have been slightly longer, by 2 or 3 rows, and that is it for the current wing, etc? Bigger than that they start walking into a Hornets nest.

Since Airbus changed the wingtip on the a330neo, the CS could get a blended tip or split tip. Plus, a slightly longer span before it hits the 36m limit.

Thanks Ted, just hoped they don’t run into engine clearance issues if a bigger fan sized engines is required from the current 73″?

The GTF’s plays a big role in its fuel efficiency but it could be “funny” if they offer a LEAP1-B (69″) with 28Klb thrust for a CS500, especially where FOD could be a problem and create engine compatibility for current MAX operators.

@Anton:

“…could be “funny” if they offer a LEAP1-B (69″) with 28Klb thrust for a CS500.”

Sorry, I don’t see any humor in such idea except it’s “funny” that U’ve completely forgot the exclusive propulsion agreement between BBD and P&W re CSeries program in exchange for the enormous risk-sharing to develop the PW1500G variant.

Then again, U may still believe engine designs these days are still commodities that can be easily+cheaply swap around for use across diff airframe designs with no potential integration issues like the good days when the same basic CF6 can be used on 747, A300, D10, etc. with little to no major design modifications….

I thought the very diff experiences in airframe+engine integration re 320Neo vs CSeries in recent yrs already shown everyone a lesson on the level of complexity involved these days even within the same engine family by the same engine manufacturer….

Will the 73″ inch fan PW1500G have enough thrust for a stretched CS300?

How much a bigger fanned engine can the CS’s take before ground clearance becomes and issue?

I was not aware of the BBD-PW arrangement.

@Ted:

“the CS could get a blended tip or split tip”

But CSeries already use a wingtip device which visually appears very similar to the type used on 330Ceo/744.

Both “blended tip or split tip” are not some novel wingtip treatment concepts which existed long b4 CSeries program launch(Actual industrialization came a few yrs later though such as for 737Max). Pretty sure BBD already considered these wingtip alternatives along with others b4 selecting the current wing tip config as the most optimal.

I bet that state of the art today is worth a percentage point or two over when the CS tip was chosen. Embraer switched to a flat cant on the E2. Why would Airbus put a blended transition to the cant on the A330 if there wasn’t an efficiency improvement over a creased transition?

CS 100 is a hot rod special for small airports.

My old guy type of aircraft, had some very good memories of <800Nm flights on 747SP's with <50 pax on what was really ferry flights to a long haul route.

@Grubbie:

“CS 100 is a hot rod special for small airports.”

Basically, when a design is certified to land @ LCY thru such steep approach angle, take off again fm such short rwy and then still being capable(admittedly in a special, low cabin density/payload longhaul config: https://leehamnews.com/2017/02/23/cseries-trans-atlantic-capability/ ) to cruise nonstop against the N.Atlantic headwind to land in EWR/JFK, that design can operate into/fm any commercial airport on earth with a paved rwy 99.9% of us will care to visit:

And the above is the biggest diff between CSeries and 190/195E2 aside fm their production costs. Comparing 190/195E2 against CS1/3 is a bit like comparing Max10 against 321LR. Their look & size are similar but they are not the same kind of animal.

CS3 is essentially a mini 321LR with slightly discounted long-range performance……clearly beyond the capability of a 195E2 even when paired with a super-duper turbofan design surely will be dreamt up soon by Anton…..

The E195E2 was never intended for Transatlantic, its biggest application most likely <2 flights, but still have the legs to fly from NY to Ecuador if you want to.

@Anton:

“The E195E2 was never intended for Transatlantic..”

And therefore possibly, CS3 was never intended/expected to be built/marketed for 195E2 level production cost/selling price range?

This is despite U were trying to compare their production costs /selling prices earlier and using those advantages to declare 195E2 is a “winner” over CS3…..

So what is/was the intention with the CS’s?

@Anton:

“So what is/was the intention with the CS’s?”

So what is/was the intention with the E2Jet?

My perception on the genesis of the CS300 was incorrect, I always thought it was a stretched CS100 not realizing it was the base model and the CS1 a shrink.

The CS5 should therefore be good working within wing, under carriage etc limits. Not sure what the PW1500G thrust growth limits are.

If the range is reduced by 500Nm to ~2800Nm you probably don’t need much increase in MTOW or thrust.

@Anton:

U somehow know what will be better for the program as per here:

“Maybe the CS300 should have been slightly longer”

yet U don’t know what are the basis of the program such as:

“I was not aware of the BBD-PW arrangement.”

Amazing.

I knew about the PW1500G agreement for the CS100 and 300 but not that it extended to any future models?

I am not a lawyer for any of the two companies.

@Anton:

“..knew about the PW1500G agreement…not that it extended to any future models?”

No way this is a perpetual exclusivity agreement but will last a very very long time for P&W to recoup investment if we look @ similar contemporaries.

LEAP-1B is a good parallel to demonstrate the level of investment required because it’s not cheap for CFM to scale-down the basic LEAP architecture into such a small package only for 737 application(In contrast, LEAP-1A and -1C share tons of commonalities). How many LEAP-1B sold? 7,600+ based on total Max sales of 3,800+. So let’s be extremely generous and say PW1500G only need 3,000 units to break-even partially because it shares many commonalities with PW1900G(190/195E2 application). It means BBD must sell/deliver 1,500 CSeries with PW1,500G for the venture to pay-off for P&W. What is the total sales for CSeries today? 360. How long do U think it’ll take BBD to sell/deliver 1,140 more? Given BBD planned only 30 deliveries this yr and ultimate rate is planned @ 120/yr, I’d say @ least 10yrs. So PW1500G exclusivity will last until 2027 earliest(This is optimistic as CFM56 exclusivity for 737 Classic lasted 14~15yrs… and then renewed for NG). But if a CS5 won’t be certified well b4 2027, it won’t be a CSeries anymore but a CSeries NG/Max/Neo or whatever U want to call it with substantially diff engine tech than today’s along with astronomical new investment$ requirement fm both BBD+P&W.

Realistically, a reasonably affordable CS5 development project for BBD must continue to use only PW1500G and must hit mkt before 2025 to avoid being obsolete. Fm BBD and CSeries customer perspective, they almost certainly will prefer PW1500G exclusivity to continue for CS5 to maximize commonality across the whole family. A CS5 with LEAP will be a bit like an orphan product to sell/lease and support in the mkt.

“I am not a lawyer for any of the two companies.”

So U are a BBD engineer/product planner because of the following?

“the CS300 should have been slightly longer, by 2 or 3 rows…”

What is the envisaged/proposed stretch of the CS5 relative to the CS3?

Again if have to make myself clear on an earlier post by someone that said that if you have more than 2 aircraft in a family one is generally a “flop”.

The example of the 767-200/300/400 was used were the -400 was not a great success story.

BBD could have avoided a 3rd member by making the CS300 say 2 rows longer (+10 seats).

Then you would have had the CS100 at 108 seats and CS300 at 140 seats in the same layout, this just a comment/observation and not criticism of the CS300.

@Anton:

“…someone that said that if you have more than 2 aircraft in a family one is generally a “flop”.”

U’re mis-quoting my comment. I said if 4 in a family, 1 is usually a ‘flop’ but if 3 in a family, it’s “risky biz” which does not mean always include a ‘flop’. 737 Classic is a good example of a family of 3 in which no variant has sold less than 389 units…not bad for the global narrowbody mkt scale 2~3 decades ago when there were 3 competing manufacturers.

“BBD could have avoided a 3rd member by making the CS300 say 2 rows longer.”

But BBD is exactly avoiding a 3rd member in the CSeries family @ least for now. In fact, most industry analysts commonly expected BBD won’t launch a CS5 until 2020 or thereafter due to lack of financial health in the near term.

“…making the CS300 say 2 rows longer” is 1 way but not the only way to avoid a 3 member family…..especially when I hv not yet heard anyone except U saying CS3 is 10seats too small to be more successful in sales.

Size, performance capability and op cost per seat of the current CS3 are practically matching 319Neo & Max7 already. More than 2,700 units of their predecessors, the 319Ceo & 73G, hv been sold(including BBJ/ACJ variants). Assuming 75% of this quantity(a bit optimistic) will be replaced thru upgauging to 320Neo/Max8/C919/MC21, that will still leave a same-size replacement mkt of 675units. Given poor sales for both 319Neo & Max7(About 100 total for both) across 7yrs since their launch and 195E2 not really in the same capability league, most of those 675units will naturally go to CS3. Therefore, it’s not unreasonable to expect 500 more CS3 will be sold simply for replacement need…..not bad at all for 1 variant and BBD will be more than happy about such sales outcome particularly if it’ll be realized within about 4~5yrs. And we’ve not even accounted for CS3 to be sold purely for growth(mostly LCC mkt segment).

Really hope the CS’s do well, see it as the perfect A319 and 737-700 replacement.

LCC’s in general don’t like to mix things its seems, EasyJet and Jetblue are big A319 users and could be potential CS300 customers. Boeing will have to disappear from the earth before Southwest replace Boeing with anything else.

Can see WizzAir having application for an CS100 for the type of destinations it serves in Eastern Europe and the East block.

After having a look again at the DL fleet I coming to some conclusions (which most likely are incorrect). A319 and A320’s are getting older but real need is for the replacements of MD88/MD93’s (~180) equivalent aircraft

DL operates these with 150 and 160 seats, they have 2-3 (5 abreast), range 2000-2500Nm. Wont the CS500 (~150-160 seats) be a perfect replacement? But will BBD be able to produce at the required rate?

Maybe Boeing’s big drive with this case is not to save the MAX7 but to stop the development of the CS500?

The CS300 could be a replacement for the A319 and 717-200’s.

No wonder DL is saying it is prepared to buck-up in the CS100 case, it could potentially operate a large fleet of CS1/3/5’s, and Boeing knows that.

Airbus has a huge production backlog, also seems DL is focusing on the A321’s.

@FLX

Since Boeing stretched the 777-9 about three rows, the 737-7 and 737-10 two rows, I think that is a smart move. Add floor space and revenue to match increased capability. Every row is worth a million more in profit every year unless the seats are blocked at maximum performance.

When the CS has the money, offer two more choices and harvest the capability gains. Let airlines have lots of choices for varying degrees of more cabin size for less range and runway performance.

Yes, very well, apart from the industrial logic of the after-sales service and the training of the pilots, by bolting a section of 3 meters and then another of 2 meters, what are the net costs more advantageous that an airline would get? Can anyone make an inventory of the positive benefits of …? Or, what about a company like Ryanair with CS100, 300, 500 and 700 in its fleet? It is this type of analytical look that is lacking in my opinion in this kind of forum.

The big 3 operates 245 A319’s between them, don’t think Boeing wants to share those replacements with a third party.

But I can see things also being in rooms with big wooden tables; “We have spend Y on the MAX7, we want our RTI, sort it out”.

End of the day Boeing still needs to get the 777X of the ground, which in a 10 years accounting basis is not going to feed the piggy bank.

787, Good for cash flow but not a good investment from a share holders RTI perspective.

Wonder how much US company pension fund money vests in Boeing? Once you have that is not good for high risk business, but you can’t stop that, just try to manage it, as its big money.

@Anton:

“…big 3 operates 245 A319’s between them, don’t think Boeing wants to share those replacements with….”

Based on the current narrowbody upgauging replacement trend @ the Big3 and the actual sales logs achieved for Neo/Max across 7yrs, most of those 319Ceos in Big3 fleets will be replaced by neither 319Neo nor Max7. This directly imply BBD has nothing in its product line that can share with Boeing’s line as replacements for those 319s.

“…with a third party.”

So U are saying Boeing is ok to share with the 2nd party(i.e. Airbus) but not the 3rd party(i.e. BBD)?

I didn’t know Boeing like Airbus that much….

United had a serious look at the CS300, then Boeing basically gave B737-700’s away for”free” to them.

AA has a fleet of 125 A319’s and 45 A320. The order for 100 MAX8’s a likely replacement of the A320’s and older 737-800’s.

Two of American Eagles subsidiaries combined operates 120 E175’s and another two ~120 CRJ900’s.

The CS100/300’s could be and ideal aircraft for AA between the MAX8’s and 75 seaters of American Eagle?

American Eagle seems to focus on the <100 seat market, so 100-150 seat aircraft replacement needed for AA? Has Boeing achieved what they wanted…..

…will AA go MAX7 and Eagle gets larger 190/195E2's? A real blow for BBD will be is if Eagle replaces CRJ900's with 175E2's, and the ultimate blow if CRJ200/700's is replace in part by 175E2' and by ERJ145XR's.

@Anton:

“United had a serious look at the CS300, Boeing basically gave B737-700’s away for”free” to them.”

If U believe the top mgmt team @ UA who studied CS3 and then decided on 73G earlier was the same team which is running things now such as ditching that earlier 73G order and upgauging fm a bunch of Max9 into Max10 recently, I think U’ve some serious catch-up readings to do re UA developments over the past 2yrs.

“AA has a fleet of 125 A319’s and 45 A320. The order for 100 MAX8’s a likely replacement of the A320’s and older 737-800’s.”

Max8 to replace some older 320Ceos is likely because of fleet age(avg 16yrs old).

Max8 to replace 738 is VERY unlikely also because of fleet age(avg below 8yrs old).

In contrast:

Max8 to replace M80/90 is EXTREMELY likely again because of fleet age(avg over 22yrs old) and AA still has 53 frames in fleet.

Max8 to replace+upguage some older 319Ceos is again likely because of fleet age(avg 13.4yrs old).

I believe AA has not decided on how to replace younger 319Ceos yet.

AA operates 49 “oldish” A320’s and 50 B787-800’s that is between 16 and 18 years old.

49+50 is MIGHTY close to 100 (MAX8 order indirectly?).

The MD82/83 are being phased out and will be retired by 2019 . This is mainly replaced by 737-800NG’s, there is still an outstanding order for 6.

When received those AA will have 254 B737-800’s that is newer than 8 years.

All MAX8’s should be received by end 2019.

…and that brings us back to the A319’s that has largely not been accounted for. AA is also phasing out 20 E190’s by 2019 that is not on American Eagles “books”. Then there is also the 22 A359 orders that seems to hang in the air.

An order for say 100 CS300’s will most likely be the best for AA’s routes, but 100MAX7’s will give fleet commonalities with the MAX8’s.

You correct, my knowledge of UA is very limited, maybe because I never flew with them. Of the US airlines I have flown with AA, DL, Jetblue and Southwestern

Now that I am getting into it. The North American Free Trade Association. Good reading, see link.

https://ustr.gov/sites/default/files/files/Press/Releases/NAFTAObjectives.pdf

While things on the BBD subject have a bit of a political flavor, the next Presidential elections are juts over 2 years away. See below link to a warm up.

https://en.wikipedia.org/wiki/United_States_presidential_election,_2020

@Mark from Toronto

The link you provide is for the list of Pratt & Whitney of Canada engines, but the PW1500G is not a Pratt & Whitney of Canada engine, as I have explained in a previous post.

The PW800 engine was supposed to be manufactured alongside the PW1500G engine in the new facility that was inaugurated in 2011. However the PW800 was put on hold before entering production because the Citation Columbus it was supposed to equip was cancelled.

Therefore in the first few years of production the new facility was only used to assemble the PW1000G family of engines, except for the PW1100G variant.

The engines for the MRJ (PW1200G), E-Jet E2 (PW1900G) and MC-21 (PW1400G) are assembled in Canada in the same facility as the PW1500G for the C Series.

It is only recently that the PW800 engine was added to the production line for the Gulfstream G500/G600, instead of the Columbus.

As far as I know, only eight (8) C Series engines were assembled in the United States, and those engines were used strictly for testing.

However, the Airbus A320neo engine (PW1100G) is indeed assembled in the United States, and in Germany as well.

http://www.pwc.ca/en/about/mirabel-aerospace-centre

Keeping in mind while P&W is the lead on this, they have a very close relationship with MTU as well as several Japanese turbine mfgs (V2500 program)

Almost as close as CFM group if not as much though not a separate entity.

Risk sharing has to be involved at least with MTU and probably the Japanese.

Which means that Aerospace has become more than ever an international business. If you have the opportunity please explain this to Boeing, for they don’t seam to understand. And while you are at it tell them also that competition is good for the industry, including Boeing itself. 🙂

TW you are right. The GTF involved Pratt, MTU, Avio (used to be Fiat Aero) and the Japanese consortium.

The certification for the GTF does state IAE as the engine OEM. It hasnt included Rolls Royce for some time

Do technically the GTF is an IAE product.

Why not sell for production cost.

Because Boeing drove down the price. Why not sell it for more than a max 7/1(if it was available),because it’s a better product?Can Bbd cancel the deal if DOC rules against it? This might be the way to go, then they can just write the whole thing off as a very successful sales tool.

@Daveo:

“Why not sell for production cost.”

Because of this stubborn economic reality known as learning curve in aerospace manufacturing.

If I(i.e. buyer) ask U(i.e. producer) to complete a 1,000 pieces puzzle U hv never seen before and U agree to charge me $1 per hour to do it, I’ll hv to pay U $24 total since this will probably take U a day to complete due to tons of trial & error. If I ask U to repeat the same for 99 more times, it’ll likely only take you 1 hour to compete that same puzzle when U finish it the 100th time and I’ll only hv to pay $1 for that. For me(buyer) it’s still the same puzzle but the price diff is 2,400% between the 1st and the 100th unit completed. Now imagine there’s another guy(i.e. new producer) offering to do a 2nd puzzle no one has seen before also with 1,000 pieces but look a bit nicer than the 1st puzzle. He also has to charge me $1 per hr to do it. It’ll likely cost me $24 when he is done for the 1st time. So when all I need is to see the completion of a 1,000 pieces puzzle again, do U think I’ll pay U just $1 to see the 1st puzzle again or pay $24 to the new guy for the nicer 2nd puzzle? The answer is obvious….the new guy has no chance unless he’s willing to charge me only $1 also like U – sell @ well below his production cost.

Constructing a modern jetliner meeting tough cert+performance std is the equivalent to completing a 10,000,000 pieces puzzle.

Finally, L.B. Thompson gives us the official Boeing position. Trump.

Loren completely misstates the entire selling airplanes below production cost thing. At this point in sales, of course this happens. Just ask Boeing about the 787 (a point Loren completely ignores, and so will Commerce).

Scary stuff though, isn’t it?

Out of control,megalomaniac and paranoid. And that’s just Boeing.

Boeing is afraid, very afraid. They know that both the C-series and the A32Xneo-series can be re-engined (C-series) and re-re-engined (A32Xneo) with fully optimised, large diameter RR UltaFan engines — 10 to 15 percent more efficient than the current engines on the C-series, the MAX and the A32Xneo. The MAX obviously won’t be able to accommodate these engines.

Interestingly, a re-winged A32X (composite wings) could with the addition of UltraFan engines and a further upgraded fuselage, icorporating aluminum-magnesium-scandium alloys, enable mark two versions of both the A318 and A319 to be competitive with the CS-100 and CS-300 (i.e. we’re talking about significant weight-savings for the A318 and A319).

–

http://www.aerospacemanufacturinganddesign.com/article/the-future-of-aircraft-metals-appears-february-2016/

OV-099:

“….a re-winged A32X (composite wings) could….”

And as U & I clearly understand, won’t be a relatively cheap+quick exercise in terms of development & re-cert efforts even if Airbus manage to grand-father the cockpit rating commonalities….

“…with the addition of UltraFan engines and a further upgraded fuselage, icorporating aluminum-magnesium-scandium alloys, enable mark two versions of both the A318 and A319 to be competitive with the CS-100 and CS-300.”

1st of all, a 319 with UltraFan or similarly not-yet-seen production engine won’t be “mark two” version of the 319. It’ll be a Mk III due to predecessors 319Ceo and 319Neo. By the time 319Neo EIS nex yr, 22yrs elapsed between 319Ceo and 319Neo and Airbus didn’t even touched the basic wing structure+fuselage in that transition. Even if we assume Airbus+RR can somehow accelerate 319 Mark III development in half the time as before and ignore the fact that the 319Neo will then only hv 10yrs RoI(i.e. Airbus basically abandoning 319Neo), are we expecting earliest EIS for 319 Mark III in 2028/29?

2ndly, U made it sound like UltraFan(or similarly efficient future engine designs by CFM or P&W in the same thrust class) and new metallic alloys for fuselage construction will be exclusive/accessible only to a hypothetical 318/319NeoNeo(i.e. mark two versions of both the A318 and A319) and somehow inaccessible for other types such as CSeries…… Frankly, when a 318 is already a no show and 319Neo being such a poor seller in the 320Neo family game plan, new fuselage material is not gonna be much of a justification to revive a 318 to create a 318NeoNeo.

Most importantly, a 320 with yet another new engine design, a completely new/clean-sheet wing design(e.g. geometry+structures when using CFRP will be very diff fm current 320Neo’s), new alloy for fuselage construction(Require re-cert @ the minimum even if no structural redesigns) and then integrate all that(i.e. the infamous ripple-on effects re design changes required) into a new package per your idea – is such a bird truly still a 320 anymore? Same or just a bit more costly for Airbus to invest in a cleansheet narrowbody design instead?

Was looking a bit at the single aisle Transatlantic route option “story”. The “box” what in airlines can work in is relatively small.

The “practical” range of an A321LR (depending on pax) is possibly not much more than 3200Nm?. If you can add 500Nm to that it can make a big difference. Not so much the destinations in the US that can be reached but departure points in Europe. Ireland is a good departure point but then pax must first get there, maybe not the fastest or cheapest way.

But on the other side, what will the seat mile cost be of an 321LR be with 160 seats compared to that of an “old” 330-200 with 310 seats (like Level), or 787-8 with 290 seats (789 ~340 seats) like Norwegian (actually with generous pitch for an LCC)?

With the wide bodies you can fly basically fly from any destination in Europe to any in the US. Was thinking of something like Budapest to Florida (4600Nm).

@Grubbie

Scary? Not really. The good doctor sounds more and more like a dotard. 😉

Totally of the post. Turkish Airlines just ordered 40 B787-9 what looks like a total replacement of their A330-200/300 fleet.

Firstly it must come as a blow to Airbus but secondly wonder at what price?

Turkey is not an EU state but part of the EFTA states, the European equivalent of NAFTA.

Just shows how complicated these things are. It’s not all about the up front price, geopolitical factors and in particular technology transfer is specifically mentioned.