Leeham News and Analysis

There's more to real news than a news release.

Pontifications: OEMs hike list prices

By Scott Hamilton

Feb. 26, 2018, © Leeham Co.: I’m tardy in getting around to this topic, which I do annually, because of an unusually heavy travel schedule this year.

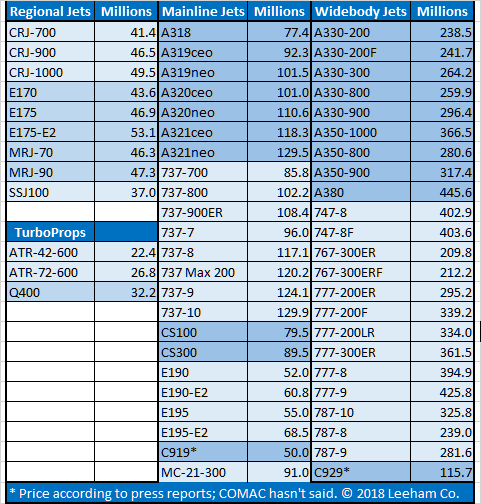

The airframe manufacturers in January adjusted their list prices for airplanes. The prices generally went up 2%-4%, but turboprop maker ATR didn’t adjust this year.

The SADC 2018 conference includes speakers from Airbus, Bombardier, Oliver Wyman, NASA, four states in the Southeast and more. Click here for information and to register.

Meaningless numbers

Of course, list prices are meaningless; no airline or lessor pays list.

In years past, discounts were assumed to be about 45% on average. In recent years, 50% became the norm.

Now, LNC sees deals going to 60%, 65% or even more discounted to list.

It’s not just the big airlines, like United, Delta or British Airways, that are seeing steep discounts.

Small airlines with small orders (a dozen or so) airplanes are seeing deep discounts.

Hawaiian Airlines

Strategic campaigns can command steep discounts for small orders.

Take the Hawaiian Airlines competition between Airbus and Boeing. While it’s apparently not quite done yet—there was some thought it would be completed last week, but it wasn’t—the competition was fierce.

LNC was told Boeing priced its 787-9 below the production cost of the competing Airbus A350-900. We don’t know what the A359 costs to produce, but we do know what we’ve heard about previous selling prices. This suggests to us that Boeing offered the 787-9 to Hawaiian for less than $115m and maybe less than $100m.

The 789’s list price is $281.9; you can do the math.

Wall Street analysts believe Boeing now can make the 787-9 for between $80m and $90m. This still leaves Boeing a reasonable profit margin.

But Boeing’s business plan is evolving to wrap in Boeing Global Services to contracts. Thus, even if Boeing went lower or its costs were higher, profits might come from the aftermarket contract with BGS—assuming this is involved.

The strategic reason to unload at this price is, of course, to kill the A330-800. HA is the only customer for the airplane, though Airbus believes the market will emerge c.2020, as the current fleet of A330-200s it replaces ages. Expansion by ULCC long-haul carriers is another element of the strategy.

Other airplanes

Based on our own market intelligence, Boeing asks $140m for the 787-10; this is a 57% discount to list. Airbus and Boeing are known to have offered the A321neo and 737-10 at discounts of more than 60% to list.

Regional jets OEMs don’t have quite the same ability to discount; these tend to be more in the 50% range, according to market intelligence.

An exception: the Bombardier sale of the CS100 to Delta Air Lines that became the focus of a complaint by Boeing to the US government over price dumping.

Bearing in mind that the list price at the time was just over $70, one price thrown out there by Boeing was $23.4m, a 67% discount to list. This is steep and it’s rare, but it’s not unknown, even by Boeing standards.

On the other hand, if Boeing’s calculation of $19.6m after credits is correct, the discount is 72%, which indeed would be “absurdly low.”

Bombardier and Delta both denied these pricing numbers. Each company provided the contract to the USITC, but this juicy information was redacted from the public filings.

After-thought

Our post Feb. 20 that reported Boeing displaced Airbus at Hawaiian Airlines, winning an order for the 787-9 in lieu of the A330-800, caused quite the stir.

LNC has been following the Hawaiian competition for months. We mentioned it in our paywall article Feb. 8, Airbus, Boeing square off with A330neo, 787 in advance of NMA: “HA is running a competition between the 787 and the A350-900, with the intention to cancel the -800, LNC is told.”

We also noted that, “The 787-8, ordered by Legacy American, found that it’s configuration doesn’t work well in the New American business model. Interest in more -8s is said to be limited, but not out of the question.”

The article is now open to all subscribers.

Subsequently, the airline said the A330-800 contract is still in place. I’ll concede I should have written that Hawaiian is “to” cancel the order (future tense), not that it “cancels” (present tense).

For those who read some sort of nexus into the story and the fact I was in Toulouse for the Airbus handover of the first A350-1000 to Qatar Airways, this was happenstance. The tip off came from the US.

In the opposite direction on the scale of actual contract sales prices, it would be entertaining to know instances where sales prices came closer to list prices than anywhere else, naming the airline account saleman of the OEM concerned who got a feather in his hat for bringing home to his employer an unusally fat sales contract ? Because to give away the aircraft at deep discount prices doesn’t honour the salesman, selling at a comfortable margin does, that’s the Job of the Salesman … or have l misunderstood the rules of the “Sporty Game” ?

Salesmen are not stand alone sellers.

They are part of the system, if the boss says get that order, then you dang well better get that order.

Please say salesperson or salespeople; it’s 2018 not 1978.

Dan F:

Sadly I am an old guy and slip on my labels.

I do fully acknowledge this is 2018 and I was in error.

Please don’t assign yourself a gender, that is soooo nineties! 🙂

Your comment eludes my point, you’re explaining why all the giving away, which we all know, whereas l am interested in how/where/who achieved a salesprice beating the record in the opposite direction ?

Huh?

Thanks Scott, are the listed and/or negotiated prices of airliners inclusive or exclusive of engines?

I have read that Airbus aircraft prices are inclusive of the cabin fits while BAC aircraft not.

Was wondering if the 3 B767 that HA sold to UAL fits in somewhere with the 789 deal?

I think you mean when does a salesman know when to walk away. My perception is that we have moved to a market where the big boys have lost that perspective. As it stands Boeing (and by implication Airbus) are determined to win sales at all costs. Given that they collectively own the market this strategy is destined to fail as neither OEM can afford to be shut out.

Assuming no collusion and reflected in the actual level of sales, you could argue that they have shared sales on ‘buggins turn’ where there was tacit acceptance of the realities of the 50/50 market split. This sort of pseudo competition benefits both OEMs parties and brings a degree of stability to the market.

When one or other party wants to change the status quo then the knives are sharpened. We seem to be in that situation at present, Boeing has decided to push 160-170 B787s a year and possibly are concerned about maintaining that order book over the medium term. Airbus want to hang the A330neo spoiler in this market and if they succeed they may even dominate the TA market with A330neo/A350 vs B787/B777x. After years of B77w dominance this is probably psychologically unacceptable for Boeing.

Dear Scott, would you think the 737 Max 9-ER would be about $1.5MM higher than the 9 “list”? And, these list prices are without Buyer Furnished Equipment, correct? Thanks, MO

I don’t know how much money Airbus invested in developing the A330 NEO versions, but Wikipedia claims it was about $2billon US. With 219 orders, one could make the case that the programme as a whole is already in the black. With that in mind, one could argue that Airbus has achieved one of their goals with the A330 NEO, in that they are forcing Boeing to offer their 787’s at extremely low prices.

Obviously, the strategy can cut in both directions.

See Air Italy will “get” 30 B787′,s. Interesting Qatar operates 30 B788’s and have 30 B789’s on order, some twist to this tail coming keeping in mind the airline Qatar wants to start in India?

http://c.newsnow.co.uk/A/925847367?-303:3665:3

Qatar might have some problems due to its relations to its neighbors after The Donalds visit and the information he spread, hence they have to readjust its fleet and doing the redjustment thru affiliates in India and Iataly might be a good solution if executed right. New aircrafts are due in rapid succession and the combined new and old fleets need to find a profitable home.

The 338 could find itself a niche as a smaller wide body aircraft with long range as the 788 “fades away” while the NMA wont have the range?

Prices for the C919 and 929 looks production cost like?

Do the proportions of the list prices mean anything? I see it is about 15% to 20% more for an A321 than an A320, or a 738 than a 737, or a 7810 than a 789, or an A339 than an A338.

Question is, what is the actual production cost increase to build the bigger model? Is it more like 10%? The manufacturers have to try to get maximum profit out of the bigger models, but at the same time, if they fill one slot for an airline, they get more profit off the bigger model even if it is built at production cost plus another 1M profit. So, an interesting game of pricing.

typically the only significant manufacturing cost delta would be materials, especially on an aircraft with so much automation in the manufacturing process. labor cost increases would be minimal, even in the interior install which is likely the most manual labor intensive delta between a -9 and a -10

so, what is the material cost of 20′ of fuselage, wires and air conditioning ducts?

Likely its a fraction of the actual extra cost the manufactures charges. Car companies, cell phone companies all play the same game

exactly, the development, labor and infrastructure cost delta between a ford fiesta and an F-150 is less within 10%, the materials cost delta is something like 30-50% (most of the expensive systems parts are common or cost roughly the same) but ford sells a fiesta for $16-21k retail and the cheapest F-150 is $30-70k

A win for Boeing at Hawaiian would be a huge win and perhaps another catalyst for the stock.

Speaking of stock, I just remembered about a year ago Scott was promoting an investment SELL thesis by Buckingham Research Group when the stock price was around $168! Today for the record it closed at over $363!

https://leehamnews.com/2017/02/13/analyst-puts-sell-boeing-stock-unusally-bearish-report/

LNR says that it was ‘extraordinarily bearish ‘ and of course those predictions from Buckingham about rate reductions and declining orders were wrong. ( their clients cant be happy!)

The Hawaiian order is a tiny number and far exceeded by the 67 or so 787 dropped orders in the last 4 years. Last week Qantas let an single 787 option lapse, not because they are unhappy, just maybe over-committed and didnt want to firm up a future option.

Trump “does a number”and saves US taxpayers $1.4 billion on the price of air force one.To bad he wasn’t on site to take on an assault rifle single handed and unarmed.

except the original bid (per the AF, not trump’s mouthpiece) was $4B and the new one is $3.9B. by “nearest 10’th of a Billion” rounding rules, he might have only reduced the cost by $1.

Boeing will make it up in cost overruns/missed requirements upcharges.

The $100million is probably something to do with using the totally unwanted planes left laying around in the desert,if it was ever going to be that much in the first place.Alsorts of talk about degrading specifications.

Handshake deal. With both Trump and Boeing,I’d want it in writing.

@Grubbie: Trump and the shooting aren’t germaine here. @Bilbo, the snide Trump mouthpiece isn’t warranted.

A reminder to everyone: “Political” comments on issues that don’t involve politics (such as ExIm Bank, typically) aren’t on topic. I don’t want this becoming a political forum.

Hamilton

apologies Scott, “mouthpiece” was not intended to be snide, I was actually trying to not be snide as mouthpiece is a relatively standard way of referring to a politician’s spokesman.

was merely intending to point out that the claimed $1.4 billion savings was not backed by actual fact.

I think Aircraft purchases with deliveries into the future has index Formulas for both Aircraft and Engines that takes into accout Aircraft grade titanium alloy and aluminum alloy prices, CFRP prepreg prices, labor rates and currency changes as well as Current List Prices “CLP” increases. So one way or Another has the yearly price list increases an effect of final sales price for deliveries into the future.