Leeham News and Analysis

There's more to real news than a news release.

India outlook for Airbus, Boeing: Optimistic at first sight, but what lies beneath?

Special to Leeham News and Comment.

May 30, 2018, © Leeham News: As one of the fastest growing airline markets in the world, India represents a large and growing part of the Airbus and Boeing order books. Although the absolute numbers seem unwieldy at first glance, a closer look at the data show that the country’s aircraft orders may actually make sense given population and consumer trends.

Photo via Google images.

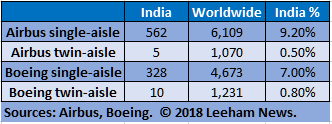

Indian-domiciled airlines operate 562 aircraft of 37 seats or more, with an average age of less than eight years. DGCA rules were recently changed to allow passenger aircraft up to 18 years old to be flown commercially, which points to a relatively low replacement need over the next decade.

Meanwhile, India’s order book comprises 978 aircraft, a 74% increase if no replacements were needed. From a seat capacity perspective, that figure is 73% before replacement demand using assumed operator-specific LOPAs for MAX and neo.

India’s share of Airbus and Boeing backlogs

These orders make up 9.2% of Airbus’s unfilled A320ceo/neo orders and 7% of Boeing’s 737 family backlog. Twin-aisle skyline exposure to India is near all-time lows at both manufacturers.

Figure 1 – Indian carrier unfilled orders, May 2018

India’s GDP averaged 7.6% annual growth from 2004 to last year; most forecasts through 2022 are in line for slightly faster growth. Scheduled seats in India from domestic and foreign operators have increased 11.6% annually since 2004, while ASKs increased 10.1% annually. Even if one looks just at growth since the 2009 financial crisis, seat capacity increased 8.3% annually.

India’s GDP averaged 7.6% annual growth from 2004 to last year; most forecasts through 2022 are in line for slightly faster growth. Scheduled seats in India from domestic and foreign operators have increased 11.6% annually since 2004, while ASKs increased 10.1% annually. Even if one looks just at growth since the 2009 financial crisis, seat capacity increased 8.3% annually.

At 8.3% annual seat growth, India’s current order book – including SpiceJet’s latest 737 MAX order – would be justified within just seven years, even if one assumes zero replacement demand.

When combined with market leader Indigo’s strong profitability and recent turnarounds at SpiceJet and Jet Airways, these numbers paint an optimistic picture of India’s future airline market. However, there is still plenty of reason for concern.

Lacking disposable income

With a population of nearly 1.3 billion and a growth trajectory that has India on course to become the world’s largest country by 2024, one would expect a large enough middle class to support a much larger airline market than India’s. But “middle class” in India often means lacking sufficient disposable income to travel.

The most recent Indian Consumer Economy or ICE360° survey revealed that 86% of Indians never travel. Even the top 1% of Indians average just $173 (11,655 rupees) of annual travel spend. SpiceJet estimates 97% of Indians have never flown. All this begs a question: Even with the rising tide of a growing middle class, will enough Indian consumers be able to afford air travel at profitable yields within the next decade?

Difficult regulatory environment

The country has also long been one of the most difficult regulatory environments for airlines, with a thicket of rules designed to protect state-owned financial laggard Air India. The result has been a long list of failed carriers in India. Air India has long been known as a highly irrational competitor, adding capacity in markets that make little financial sense and offering fares out of line with its cost structure even on routes that might otherwise be viable for others. Future economic growth won’t matter if India’s carriers have to financially slaughter each other just to defend market share in a future downturn.

Mercifully, Narendra Modi’s government has recently undertaken meaningful strides toward liberalization, including a drive to sell 76% of Air India. However, potential buyers are being asked to accept a long list of difficult provisions, including the assumption of $5 billion of debt. Sydney-based consultancy CAPA believes Air India could lose another $2 billion in the next two years – and few industry observers see any realistic prospect of profitability on the horizon. Not surprisingly, no domestic or foreign companies are known to be actively considering a bid under these terms.

International opportunities

The Indian Directorate General of Civil Aviation (DGCA) has also recently scrapped the requirement for new operators to only fly domestically for five years before getting international rights. This “proving period” rule kept the domestic market overcrowded with capacity and yields below viable levels. With this impediment now gone, will previously domestic-only carriers instead overcrowd short-haul international routes? Seat capacity from India to the Middle East and Asia averaged 13% annual growth in the period from 2004 to this year, with a CAGR of >15% over the past three years.

On top of concerns about Indian carrier growth, there is a rising wave of rising foreign capacity into the country. Emirates, Etihad, and Qatar Airways have long built their growth strategies on shuttling the Indian diaspora throughout the Gulf region and beyond. But now a host of low-cost carriers like Air Arabia, Lion Air, and Malindo Air are seeking to grow their respective footprints in India. And AirAsia India could rapidly accelerate its growth via the outsized order book of parent company AirAsia and deep-pocketed local partner Tata Group.

Dubious profitability

If foreign competitors continue to grow over the next decade at rates like those seen in recent years – at the same time that India’s own carriers seek to nearly double their combined fleet – sustained profitability seems like a potentially dubious prospect into the next decade.

Will Airbus’s and Boeing’s future deliveries to India be jeopardized as a result? Time will tell. But investors and suppliers would do well to watch this market closely for signs of what’s to come.

This is the concluding segment to our India series. This installment is provided by an analyst who has worked in multiple parts of the commercial aviation world for well over a decade. LNC is well acquainted with his bona fides and industry perspective, but circumstances require that he remain unidentified for the moment.

Seems the Indian airline market is struggling to take off.

A lot of drag in the whole operation between Government, corruption and no real plane.

https://www.flightglobal.com/news/articles/indian-police-raid-airasia-india-offices-449011/

Police investigation =bribe not big enough.

Operating in India is not easy. There are so many levels of administrative authority which you need to work through that its near impossible if you don’t have a “facilitator” right at the top.

On the technical side I think an B797 type aircraft could do well in the India environment, domestic and Regional/International. So AB better catch a wake-up.

Why not use existing A330s for domestic and some regional routes in India rather than wait 6 years or more for a plane that might be announced this year ( they have been saying that for the last 3 years)

Its 1100 km from Delhi to Mumbai, thats nearly 2 hr flight, very similar times to other shorter widebody domestic flights.

India is shaped like a triangle and hence pretty suitable to Chinese type of high speed trains. It will not be as simple to build as in China as you have private property and a massive administrative system to work through.

The market for Airbus A322 with 250seats doing 1-4hr flights is huge. The physical size of the average indian traveller is still smaller than the average Texan so fitting 250 people into it should go pretty easy. The question is if the A322 will come in different versions like A322Re and A322LR and with Engine choice between a 35k PW1135G and a 43k RR Ultra Fan maybe “The RR Scapa43G”

One in 5 Indians is overweight, would be greater proportion in middle classes. Not so different to Texas after all except its more likely among women.

Agree but then they must get a 2nd access door in front of the wing and go back to the original rear galley and toilets set-up for longer haul routes if you go 220+ seats.

End of the day airlines need an ~250 seat lighter clean sheet twin aisle aircraft with ~50Klb engines and range of around 5000Nm but also good for 1000Nm missions. Good turnaround times and larger aircraft for shorter haul (<3000Nm) routes could be required for India in future.

I think it comes down to cost of purchase/operation, cargo and turn around times. The A322Re is pretty cheap to develop and certify once 35k A320neo engines are certified, the 797 is more expensive and a bit.

The 797 for sure gives you more comfort, more seats, more range, quicker turn arounds and more flexibility but comes at a price of purchace and operations. The A322Re Engines will be relatively cheap, the 797 Engines will be closer to the 777-9 GE9X Engine with its $42 million list price each.

I bet Airbus will move as soon as Enders leaves Airbus with Udvar Hazy influencig the design making it a profit machine for both Airbus, lease companies and the operators.

From an AB perspective I am concerned that a similar situation could develop as 787 vs 330NEO if they stay out of the NMA/MoM race, availability of an engine better than that for the 797.

A new CFRP wing for an 322(Re) that could be used on a updated 321LR could be important priorities for AB in the India and other markets.

Yes, it needs a new wing no matter their Engine selections. Still Boeing will not ship 797’s Before 2027 and Airbus might be able to certify a rewinged A322Re around 2023, a A322LR will take maybe 2 more years and with an Engine delay you are close to the 797 certification date. The 797 is designed for robotic assembly/fabrications of Composites as Boeing is quite dependet on suppliers getting their equipment producing what the 3D Catina models specify, that can cause delays as well. If Boeing goes for a single source PW1050G Engine it is a risk as well. We will see by Farnborough.

The shape of a service area has nothing to do with it.

It could be a parallelogram for all it matters.

What matters is population density, proximity, enough free income to travel and the excess funds (or a taxable population)

India is missing key ingredients (Money and excess funds, aka a reasonably well off middle class).

This misses the other key ingredient. The ability to run and manage something as incredibly dangerous as a high speed rail system when they can’t even build and operate adequate airports which is relatively low tech enterprise.

@TransWorld

Good points about the Indian economy and problematic management of large projects.

Off topic, my girlfriend asked why I’m on a “forum” with TransWorld?

@everyone

I think we might have to focus on fertility rate in India to get a better understanding of the middle class not expanding like other countries.

Comparing (historic) fertility rates and economic growth of Japan, South Korea, China (I could insert any other Asian country where the middle class greatly expanded) suggests the middle class starts to expand after the fertility rate drops below 2. The same can be said for many western european countries, though WWII and the babyboom mess up the data a bit.

In 2015 India had a fertility rate of 2,40 which is a number China was at in 1990 (China had 2,43 to be exact).

IMHO this seems to suggest when it comes to middle class growth India is around 25 years behind China (this is fluid and definitely not a hard number).

Variable costs being highly unpredictable and about 8 airlines all operating in cut throat environments with slot restricted airports + bureaucratic nonsense

all year round doesn’t present a scenario where the market will mature as it possibly could. Instead if 4 airlines at the most, with A321 Neo’s/737 max 10 to scoop up demand left over by 4 airlines, all domestic operations, it would do wonders. I’ve heard 2 more private airlines are on the way in the Indian market.

Will be interesting to see what Qatar’s plans are for the proposed new airline in India. Seems X-number of 787-8’s will eventually shift to AirItaly.

But they also have 30 B789’s on order with deliveries staring 2019.

With these the US East and West coast destination could be reached from Delhi and Mumbai for example if the 789’s are used by the “Qatar India Airline”.

Yesterday was closing date for offers for Air India, no offers received. Could we see more airlines perish in India with survival of only a few “strong” ones?

…or “Qatar India” could feed into AirItaly for example serving destinations in the US and Europe?

Longest distance Chennai to Milan (~4100Nm) which brings me back to the 797 as good concept aircraft for India. Time not such a big issue as it appears the non-domestic market is lagging the growth rate of the domestic market.

Your news is only concentrating on aircraft orders but not addressing core issues. If these aircraft start coming on scheduled delivery dates, where they will be parked? Indian aviation needs massive infrastructure upgradation in terms of airports. It’s time that every airport in district capital must be upgraded to server wide body aircrafts and should have night landing facilities. The biggest threat to growth of civil aviation in India is DGCA. One must start questioning their ad hoc rules. The fact is they don’t even draft CAR but exactly copy from CAA UK. You can verify from both sites. There is lot more, but I am stopping here.