Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Boeing’s latest forecast raises more doubt than hope

By Judson Rollins

Oct. 12, 2020, © Leeham News: Every year, like clockwork, when Boeing publishes its 20-year Current Market Outlook, there is always another upward revision in forecast demand for new aircraft.

So, when the Chicago-based OEM admits that demand has taken a long-term hit, you know the situation must be dire.

Last week, Boeing belatedly published its annual CMO forecast for global commercial jet production and services. The forecast was quite a comedown as it marked a 2% fall from Boeing’s previous expectations for aircraft demand, with a whopping 10% drop for widebodies and freighters.

Airbus has withheld its 2020 Global Market Forecast while it continues to assess the impact of COVID-19.

Boeing tries to keep upbeat tone despite numbers

The CMO strikes a more optimistic note in its text.

“The current downturn is likely to lead to the replacement of many older passenger airplanes,” the summary reads. “This accelerated replacement cycle will position airlines for the future by improving the efficiency and sustainability of today’s fleet.” Boeing now believes 56% of aircraft to be delivered this decade and 48% through 2039 will be replacements, versus a 20-year forecast of 44% in Boeing’s 2019 CMO. But “replacement” requires new airplanes to be delivered, a distant prospect in many regions – especially considering how many low-time used aircraft have been placed in storage this year.

Overall delivery forecast. Sources: Boeing, LNA analysis

The region-by-region view was almost uniformly negative. Forecasts for developed markets like North America and Europe were decreased by 2% or less, while emerging markets like South America and Africa were slashed by 11%-13%. Only China’s demand forecast was increased from last year, by 6.3% to 8,600 units, and for reasons not explained anywhere in the CMO.

“China’s demographics and urbanization, combined with its ongoing economic transformation,” the CMO’s interactive version says, “are expected to maintain favourable market conditions for air travel over the next two decades.” But has this changed since 2019’s CMO was published? The same paragraph admits “China’s growth rate has slowed in recent years,” a trend almost certainly accelerated by COVID-19.

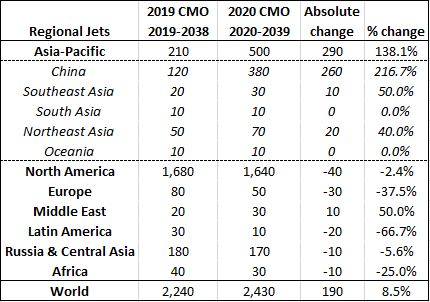

Regional jet deliveries. Sources: Boeing, LNA analysis

Regional jet growth outlook powered by implausible Chinese demand

Boeing appears to draw a boundary on regional jets at approximately 90 seats, classifying the Embraer E170 as a regional jet and E190 as a single-aisle. Its forecast of 2,430 regional jet deliveries over the next 20 years works out to an annualized rate of 122 units/year. Despite Mitsubishi’s withdrawal from the market, this is achievable from a production perspective. Embraer has historically produced up to 100 units per year, although it will need to devote an increasing share to larger E2 variants that Boeing classifies as single-aisles. COMAC and UAC will also start production this decade; LNA believes they will produce no more than 60 aircraft per year combined.

However, a comparison to Boeing’s 2019 CMO highlights forecast modifications which are hard to explain. Somehow, 20-year demand for Chinese RJs increased from 120 to 380 units, a change that more than explains the 8.5% increase from last year’s forecast. It seems difficult to imagine Chinese airlines would waste slots at constrained airports on sub-90-seat aircraft.

Regional jet demand is likely to be particularly light over the next several years, as RJ unit costs are viable only in markets with high unit revenue. Few high-yield markets are likely to return to previous levels this decade given the permanent reduction in business travel predicted by the CEOs of Delta and Southwest, among others.

Single-aisle deliveries. Sources: Boeing, LNA analysis

Single-aisle demand: steady as she goes?

Boeing only reduced its 20-year single-aisle delivery forecast by 150 units or 0.5% from the 2019 CMO. North America demand was exactly flat and Europe was down just 0.7%. Although share shift from legacy carriers to faster-growing low-cost carriers is likely, it beggars belief that 20-year total demand in mature markets would not be materially decreased by a nearly half-decade downturn in passenger travel.

Emerging markets were similarly negative – except, again, for China. An 6.4% pullback in forecast demand for South Asia and 10.6% fall in Latin America, both relatively small markets, was more than offset by an 8.2% or 490-unit increase in the China forecast since the 2019 CMO. Although single-aisle deliveries to China are much more likely to grow than regional jets, nothing has happened since last year that would justify such an increase.

Widebody and freighter demand expected to fall in all regions

The latest CMO reduces widebody demand by 10.3%, with cuts in every region. The Middle East, China, and wider Asia show the largest reductions in absolute terms. However, Middle East widebody demand was reduced by only 11.1% and Southeast Asia by a mere 7.3%. These seem hard to fathom as long-haul “super-connectors” like Emirates, Qatar, and Singapore face growing local competition, increased “overflight” competition driven by the enhanced range of the 787 and A350 – and, above all, a downturn in passenger demand that seems highly likely to extend into the latter half of the 2020s.

Widebody deliveries. Sources: Boeing, LNA analysis

The 10.6% slash in expected new freighters hardly comes as a surprise. Early retirements of hundreds of passenger widebodies, especially 777s and A330s, are likely to provide sufficient freighter conversion feedstock for most of the coming decade.

Demand forecast implies incredible ramp-up in production rates

In an investor note, Morgan Stanley used the CMO forecast data and various market share assumptions to estimate production rates for the current decade. It found that achieving 50% single-aisle market share for Boeing would require a ramp-up to 122 aircraft per month by 2025, a 114% increase from the previous MAX production peak of 57/month.

On the widebody side (including freighters), Boeing would have to produce 29 aircraft per month to achieve 50% market share. Given Boeing’s pre-COVID production of fourteen 787s per month and five 777/777Xs, plus the likely end of 767-300ERF production by mid-decade, such a growth rate seems unachievable.

Source: Morgan Stanley

However, the actual picture may be even worse than Morgan Stanley believes. Before COVID, Boeing’s 737 MAX had an order backlog share of approximately 38% versus Airbus’s 58% when all 100+ seat single-aisles are considered, including the Airbus A220 and Embraer’s larger E2 variants.

The bank’s analysts seem to have built their analysis on an implicit assumption that Boeing and Airbus are the only single-aisle competitors. In reality, Embraer is capable of producing 100 units per year – and E190-E2 and E195-E2 orders will start flowing eventually.

Also, COMAC’s C919 and UAC’s MC-21 should be in production from 2022. (Both claim they’ll enter service next year, but this seems unlikely under current circumstances.) Admittedly, initial production rates will be low, and the two combined have less than 1,200 orders and options. There’s no way to know how quickly each manufacturer will ramp up production, but a maximum of five aircraft per month or 60/year seems reasonable throughout the 2020s.

Boeing’s traffic forecasts have been too conservative – but what does this mean for deliveries?

As Melius Research told investors in a note after the CMO’s release, the air traffic assumptions in the CMO and Airbus’s Global Market Forecast have been consistently conservative over the past 20 years. The firm’s analysis showed that Boeing’s average annual traffic growth assumption in the 2000-2019 CMOs averaged 4.9%, while actual annual growth over the same period was 5.4% – even with 9/11 and the global financial crisis. The latest CMO calls for 4.0% annual growth through 2039.

Melius also claims the regression coefficient between GDP growth and air traffic growth has grown during the past 15 years, due to the rapid expansion of the global middle class. “We believe,” said Melius’s note, “this demographic-based trend will re-emerge post-COVID.”

Notably, the firm did not say whether previous aircraft delivery forecasts have proven accurate.

The CMO’s 20-year fleet estimates, said Melius, assumes aircraft retirement rates in the low 2% range, which is reasonably consistent with historical trend. The wave of retirements happening now is likely to eclipse the 4-5% rate seem in previous downturns, which normally would point to the replacement demand Boeing mentions. However, new entrants may opt to take lower-time used aircraft from desert boneyards if they’re priced competitively enough to offset inferior economics – and supply of such aircraft is stronger than ever.

It’s also possible that some governments will mandate accelerated aircraft retirements as a part of anti-carbon regulations, as the Melius note points out. This would likely be a boon to aircraft manufacturers.

Demand for new aircraft will not stay depressed permanently – this is a certainty. But troubling details in Boeing’s latest forecast make it clear the CMO is an aspirational guide, not one for planning.

Hi indeed a worrying picture. Boeing can be forgiven for also not knowing what the future will bring. While they state the market proved resilient in th ast (9-11/Sars), 2008, it’s clear we just haven’t seen a worldwide downturn like this before in our industry..

Btw nice to have contributions from down under, demonstrates Leeham’s truly global perspectives.

I don’t buy the big E2’s are Single Aisles not regional. It takes more than a pencil change.

Scope alone in the US truncates that notion.

The A220 beats it soundly in the range and pax areas. Combined with Airbus link in and support, phew.

Airbus clearly goes into the 2020s the big winner.

Its clear its only the E190 and above not the E175

Its Boeings forecast and they are allowed to draw the line where they like – or remove it like they have for the very large widebody category.

The E195-E2 is difficult to categorize, it is a significant stretch over the old E195, they should have names it E200 IMO. It bridges the Regional-NB edge. It has similar capability as the A220-100.

https://upload.wikimedia.org/wikipedia/commons/1/15/CSeries_comparable_aircraft.png

Its bigger capacity , closer match to A220-300

Embraer say at 31in its 132 seats

The Air baltic A220-300 in single class @ 32 in are 145 seats. That was the reason for the stretch to make its numbers compared with its closest competitor.

Duke:

Clearly Boeing can do what it wants, forecast or otherwise.

I (or even we) don’t have to buy it!

Guys, if you discuss capacity, you have to discuss range.

Doesn’t make sense to look at a single factor.

In fact, also the E2 is more a regional aircraft due to it’s range restrictions compared to A320neo / B737max / A220.

The E195 E2 is a 5m stretch over the E190 E2 and has about the same fuel capacity of 13,7t (E190 E2 13,5t).

There must be a serious range restriction, it’s 5m more fuselage, pax and a lot more weight.

The range of 2600 nmi is a more theoretic value, and Embraer didn’t go for a long range wing as it stayed with the old AL material and only changed the design.

Embraer itself calculates with routes of 600 – 1000nmi to show the E2 is superior to the A220-100.

Also the 4 abreast in that narrow fusealage.

The E2 is a regional aircraft, a larger one, but the main focus of this aircraft is to fly routes under 1000nmi.

“”In fact, also the E2 is more a regional aircraft due to it’s range restrictions compared to A320neo / B737max / A220.

The range of 2600 nmi is a more theoretic value,

Also the 4 abreast in that narrow fusealage.””

If you mention 2600 nm range it must be the 195-E2.

The 2600 nm are for maximum cruise speed M 0.82. EMB added different speeds in the payload-range figure. For LRC (long range cruise) the range is 3060 nm with 120 pax, or 3000nm with 122 pax.

The MAX-8 shows only LRC. If using the OEW from ET302 the MAX-8 can reach 3000 nm with 165 pax.

122 pax / 165 pax is nearly equal to 61500 kg / 82190 kg MTOW.

The cross-section of the 195-E2 is newer than the 190-E2. EMB shows the cabin width on the “floor” with 2.52 m, it’s 2.75 m at the armrests. Also the 195-E2 shows an armrest at the windows while there are no armrests on the MAX.

275 / 5 (4 seats + aisle) = 55 cm E195-E2

354 / 7 (6 seats + aisle) = 50,4 cm MAX

195-E2 should be 9 pct more comfortable.

122 seats equals 34,5 inch single class seat pitch on the 195-E2.

165 seats equals 36.2 inch, 5 pct better on the MAX-8.

Better would be a comparison with the MAX-7 if Boeing would show a real payload/range figure instead of hiding it in a combination of payload + OEW.

This report is very welcome – that Boeing should be ‘aspirational’ in all that they do is to be expected, which would include their notable engineering failures, their it is safe to fly report and this what me worry market survey

The account given here is both well written sober and acute

Judson,

None of this is apples to apples

One cannot just go from the 2019-2038 forecast total and compare to 2020-2039 total. Their overlap is only 19 years and you are taking away a low delivery year (2019) while adding a very high delivery year (2039). The result therefore will (almost) always be an increase in total deliveries. In fact, in a world where fleet grows by a constant X% each year (4% over the last 30 years), the expected increase is X%

The fact that it is not, is a reminder of the level of disruption COVID has brought into air travel. In fact, it is quite easy to guestimate Boeing’s view of the disruption. Fleet grows at “Traffic”-“Efficiency” % – i.e. not all traffic growth is represented in fleet growth because of aircraft being used more efficiently over time

Over the last 30 years, that would have been Traffic-1.5% and if those trends were to continue, their expected fleet growth should be roughly 2.5% (4% – 1.5%)

The drop in the fleet forecast you outlined is 2.1% plus the expected growth of 2.5% gives of a 4.6% drop in deliveries on an apples-to-apples comparison

This is roughly 2,000 aircraft over 19 years – quite a big chunk – equivalent to all deliveries to several programmes over their life. Doesn’t fare well for new entrants

You also mentioned that Melius Research did not show how Boeing delivery forecasts performed over time. That is also quite easy to check on – looking back at their earliest ones from turn of the century, we see that they are always too optimistic on WB aircraft (by 10-20% almost) while being way to conservative on NBs (40-50% even!). I think internal incentives might play a role – or maybe the lack of appreciation for trends in making smaller aircraft better and more capable

Your math is almost spot-on; Boeing’s expected 2039 fleet is 4.5% or 2,260 aircraft smaller than 2038.

Had Boeing applied its year-over-year growth across all regions in line with their respective traffic growth rates, it would have been defensible. But this latest forecast seemingly boils down to “the world will always get better … because China,” which doesn’t pass the smell test.

CMO is ultimately a marketing brochure, not a planning data source. But a marketing piece so widely read within its industry must be held to a high level of scrutiny.

China’s and Russia’s new entrants will struggle for a variety of reasons unrelated to global demand trends. Any new entrant with superior economics and reliability will still find a place in the world — which makes Mitsubishi’s apparent exit a tragic strategic error, especially if Boeing ultimately proves correct about RJ growth.

Which manufacturers / seat counts did you include in your last-20-years production analysis?

Im thinking Mitsubishi is only a pause, not an exit. Guess who is the lead production of the PW 1200G… its Mitsubishi Aero Engines. The tooling is from Mitsubishi Machine Tools.

The whole project was developed from a government ministry NEDO (New Energy and Industrial Technology Development Organisation) which outlined state support for many different industrial projects. Its a very japanese way of doing things from top down.

Mitsubishi closed all of its US offices and let go of its global sales team, in addition to closing the Montreal engineering center it acquired from Bombardier. Its remaining product, the M90, is uncompetitive with Embraer’s E-Jet. Suspending the program creates uncertainties that will inevitably scare away customers and suppliers. It’s hard to see how they claw their way back when demand recovers.

Duke:

MHI jet and turbine division is a money maker, the jet, all losses.

Being a partner with P&W in Jets is a separate business aspect. They are never going to sell enough MH90/100 or whatever it is this week to make up for the investment even if they owned the GTF.

That GTF program has 3 Japanese partners as well as MTU let alone P&W.

I believe equal in the V2500 program. Have not seen on the GTF, but at best its 20% and probably not that much. So no, that dog don’t hunt.

And if you look at regional jet sales, they pale in comparison to Airbus and Boeing single aisle.

While I thought BBD was nuts to challenge Boeing and Airbus, I admired they did so as they could live in the small pond with Embraer (and maybe MHI) or they could go big.

Mitsubishi elected to go small, then bigger based on a wishful thinking on scope changes. BBD knew they could score big if they succeeded, MHI never was going to score big.

I believe that they will shut the whole thing down.

That will allow Embraer to survive but ironically with the old E1 not the E2 (unless they manage to take weight out of the 175 E2.

Otherwise with two mfgs fighting for a small share is a loosing proposition and MHI is too successful to not see that.

Im surprised you would think the M90 is uncompetitive with the E jets. The interior is the same size ( but with better overhead bin design) and the empty weight is less because of the single circular shape fuselage design . The E190 and its cousin the E195 are now designed for larger passenger capacity with bigger wings and the double bubble underfloor baggage hold.

The covid crisis has upended many development programs including at Boeing. Does anyway really think that Boeing has wiped a NMA type plane completely or has it become a ‘grey’ program for the time being.

“”Does anyway really think that Boeing has wiped a NMA type plane””

Boeing should have done a 767-300ER replacement already but they focused on 777X which seems to be a waste now. Airbus isn’t even interested in an A350-2000. Only 787-9 and A350-900 have the sales. There is still a big gap to narrowbodies and it seems Boeing won’t close it, too expensive and they lost their self-certification business now. Boeing will be busy fixing MAX and QC issues.

The big question I have is if the M90 is now a solid aircraft design. If it is, and there are 2 viable capacities, a 100 seat, scope compliant regional might has a future.

E.g. Airbus Canada could absorb it in a JV with MHI. Closing the gap between the ATR’s and A220-100. If it’s a good aircraft, like the A220.

The PW 1200G / Mitsubishi Aero Engines might not play a big role. Those OE’s power the alternative E-jets too.

Great work Judson, kind regards from Honduras.

Interesting item teased out of the Leeham report here is the estimate of 60 combined production of COMAC and UAC.

Call it one months production of single aisle for Airbus or Boeing (not right now of course).

And the capitalist running dog-fighting on the 929 is just beginning!

Caught my eye too. The uncertainty is the chinese have demonstrated over the last 20 years, they’ll plan, pump in hundreds of billions and quietly move mountains, industrially. Made us careful in pooh pooh’ ing them..

They have been stalled in their current aircraft development for almost a decade now. The Comac ARJ21 is a derivative of the MD80/90 produced under license in China, but has a newer wing design done by Antonov. The engine is CF34-10 from GE, which really is derivative of the CFM56, which was specially developed for the E195. Everyone but China has done the heavy lifting there.

The larger Comac C919 ‘seems to be’ based closely on the A320 and has GE leap engines. Even so, its years behind the original schedule . The main Chinese airlines only have a handful of firm orders each with the rest options so doesnt seem they expect much. Likely for some time will be only used within China.

Have to agree with Duke, and more so.

Aircraft are not smart phones. Nor are jet engines. Both are huge tech capability in multiple fields and last 20 years or more.

China has failed miserably and do not even have Certification’s for the 919 let alone the ARJ21. Without that alone you are not selling any to other than China (and give some to Zimbabwe and Venezuela )

But you also are not going to sell without a world wide support organization and you have to be customer service oriented (better or worse for Boeing)

With China as the customer, its about prestige and appearance not service. Russian has the same issue.

The Superjet might have been a good offering, but its badly done (breakdowns) and poorly supported and no one can tolerate that in an age of 98% reliability on departures.

China nor Russian sells any jet engine into the world market (let alone aircraft)

Airbus was an anomaly of state supported industry (Japan no longer is a shipbuilding center is it? low cost market, not high tech) .

But Airbus was given a charter and then left alone on design. Their first effort was no all that successful (I flew an A300 early on and while I had not idea on the economics it was clear it was a well built aircrat)

Boeing afforded them a rare opportunity (Lockheed and Douglass has limited product lines) and Airbus took advantage of it and succeed with two engine ETOPs that were allowed in Asia and eventually became allowed across the world.

And no, I was not the least bit happy when I found we were going from Taiwan to the Philippines with only two engines!

So, with the 929, what could possibly go wrong?

Like the Superjet, the MC21 looks like a nice offering. I don’t see it coming close to succeeding in world sales and it at least will have Certification.

Which is a major reason China joined with Russian, China has not path to certification .

But they are fooling themselves. It won’t matter. It will be way late, way behind because its focus on China as a customer.

Airbus knew they might get some sales from the partners, but they knew success was scattered all over the world and the parts that came together had some experience in that.

I think that Covid-19 will have a very long economic impact tail which is still difficult to forecast. It seems that too many commentators blithely assume that society will eventually return to pre-Covid travel patterns and levels. I am not so sure, even with the eventual arrival of a vaccine. The pumping of money into the economy at virtually zero interest rates for as long as has been going on demonstrates we are in a new era.

Underlying the preoccupation with (or under the cover of) Covid-19 is the acceleration of trends that reduce jobs, on the one hand and, on the other hand, the acceleration of remote meeting and business processes. I have been a bit surprised at how effective video conferencing has been. Weekly video meetings of dozens of geographically dispersed managers has dramatically improved our organization-wide communication and productivity at virtually no cost.

As regards the possibility (or not) of a long-term economic impact from CoViD, it should be remembered that “The Roaring 20s” occurred just after the 1918 Spanish Flu…and WW I. Sometimes things pan out differently to what one might expect.

@Bryce

The roaring Twenties are here already, stock market Fed printing and pumping, billionaires a lot richer

But the poor getting a great deal poorer and about to more so

So Roaring Twenties and Great Depression all at once

Caveat- In the ‘west’ only : Asia and Africa will do a lot better, as they have done better with the bug

“In reality, Embraer is capable of producing 100 units per year – and E190-E2 and E195-E2 orders will start flowing eventually.”

During the heady ‘good’ times of the past few years, pre-covid – when airlines were using free cash flow to purchase shares in the great stock buyback, it has kind of fallen through the cracks. What would lead you to believe that the ‘too big for regional carriers and too small for mainline fleets’ E2 line would all of a sudden start to pick up orders?

Boeing walked away from the program (yes, they haven’t been stellar in their decision making, as of late) so they must have seen something in it that they didn’t like.

I think ~100 seats, 2 cabin crew members and a quiet, efficient, affordable jet has proven its value. Competitors are paused (MHI), local (ARJ) or more expensive (CS100). There is a significant replacement market. Hundreds of aging E190s, Fokkers, 717s, MD80 around.

I Agree with Judson Embraer will be alright. The government will keep them Embraer afloat if they are smart, in a few years strong product lines; EJets, KC390s, Bizzjets & Tucano’s will be rolling of lines.

Boeing walking away from the program might prove another thorough decision based on wrong assumptions. E.g. no one else will step in.

The US was the heart and soul of that market and with scope in place, the E2 is not going anywhere.

World wide sales are not where the money is, nice supplement but not the numbers the US has.

Keep in mind that the 717 and MD80 had range. Different market even if the seating is close.

That is where the A220-200/300 fit in so well. Large enough to replace a 717, far more economical and updated with the range desired.

The E2 does not have that flexibility so its whatever market there is for the E1 in the US and some E2 world wide.

Not being in Embraers position of what they can do, no idea what they will do. The could try to take weigh tout of the 175 E2. Fair amount of it in a smaller aircraft though.

The 190-E2 and 195-E2 will have a place. Not all airlines need range and A220 production rate is low. But it depends on the price and EMB could be in the back seat, same as BBD was against the E1.

More then 700 non scope compliant E190/195s operating around the world.

And we now know what the EU can do per WTO

https://www.wionews.com/business-economy/eu-wins-tariff-clearance-on-4-billion-of-us-imports-in-boeing-case-335072

EU could put 50% tax on the MAX, that would force European airlines to cancel MAX orders and the tariff wouldn’t even be used.

I think we need AP Roberts on that.

What the US does is more driven by the nut behind the wheel, EU follows all those funny rules (and like emissions looking for all the gaps to shoot through – that is said with some humor ala the Emissions aspects)

According to reporting from Reuters, this ends the WTO case brought in 2004. It’s basically a stalemate, the WTO upheld both its rulings allowing tariffs on both sides, due to subsidy activity on both sides.

The current position of both the US and EU is that they are now compliant, having dropped their subsidies, and the WTO has no further jurisdiction because their rulings cannot exceed the scope of compliance, as mandated in their charter.

So that leaves the issue outside of the WTO’s power to resolve, meaning that it will require negotiation between the US and EU to settle the outcome. Both have signaled they want settlement, so we will see how serious they are. There’s a good chance that the US will to negotiate will significantly improve after the election.

At present each side believes they have right to apply tariffs, but also denies the other side’s right to apply tariffs. So we can hope that will provide sufficient incentive to negotiate.

Given the current crisis in aviation, the whole thing seems a bit ridiculous in hindsight. It’s time to move on and stop trying to penalize each other. Work it out like adults, and focus on the bigger problems that we all share.

“An 18.9% pullback in forecast demand for South Asia and 10.6% fall in Latin America, both relatively small markets, was more than offset by an 8.2% or 490-unit increase in the China forecast since the 2019 CMO.”

. . . the table indicates South Asia is down by 6.4% not 18.9%

Good catch — now corrected. Thanks!

More then 700 non scope compliant E190/195s operating around the world. In Europe they kept lines open during the past 6 months. In the recovery they’ll play an important role. US and China East Coast, Europe that a good part of the global market, all <1500NM.

“it beggars belief that 20-year total demand in mature markets would not be materially decreased by a nearly half-decade downturn in passenger travel.”

you are presenting the Leeham News forecast as a fait accompli . . . it is not certain that it is a half decade downturn