Leeham News and Analysis

There's more to real news than a news release.

Pontifications: Casting eyes toward Dubai Air Show

By Scott Hamilton

Aug. 31, 2015, © Leeham Co. September begins tomorrow and we’re only nine weeks away to the 2015 Dubai Air Show.

We’re looking to this event to be the last big opportunity for major airplane orders for this year. While it’s true that Airbus, Boeing and the other ![]() OEMs make a big year-end push to top off the order book, the Dubai show has become increasingly on a par with the Farnborough and Paris air shows, but focused on wide-body orders and program launches.

OEMs make a big year-end push to top off the order book, the Dubai show has become increasingly on a par with the Farnborough and Paris air shows, but focused on wide-body orders and program launches.

Eyes on the Dubai Air Show will be watching for what could be would be this year’s prize catch: whether Emirates Airlines will be ready to place the oft-talked about order for 50-70 Airbus A350-900s or Boeing 787-10s. (Some have floated an even higher number.) The other big item of interest: whether Airbus will launch the A380neo.

Tim Clark, president and COO of Emirates, is adamant there is no linkage between the prospect of an A380neo and the medium twin-aisle order. Clark, of course, is the strongest advocate for re-engining the A380. Qatar Airways CEO Akbar Al-Baker said if the A380neo is launched, he’ll order some. Lufthansa Airlines said Airbus has to do the neo if it’s to regain the lead in seat mile costs over Airbus’ own A350-1000 and the forthcoming Boeing 777-9.

These are the only public declarations of interest I’ve seen.

Airbus might have gained some advantage with the expected launch of the A350-900LR, which adds about 600nm to the range of the airplane at the expense of some passenger seats. The range is now computed to be about 8,500nm. The 787-10 now has a range of less than 6,500nm under Boeing’s new Standard Rule data.

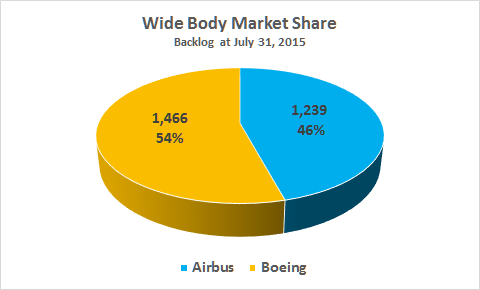

Boeing continues to comfortably lead in the wide-body backlog.

Figure 1. Wide Body Market Share: Sources: Airbus, Boeing, at July 31, 2015.

Boeing’s lead is boosted by its dominance in the freighter market, where it has a backlog of 147 747-8F, 767-300ERFs and 777Fs to a meager 10 A330Fs for Airbus. This is a 94% market share for Boeing. (The Boeing KC-46A and Airbus A330 MRTT are not included.) In terms of passenger aircraft only, Boeing has a 52% market share of the backlog.

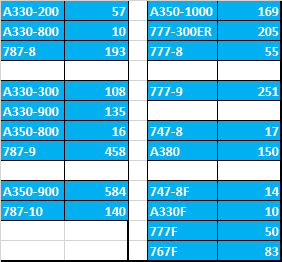

Figure 2 shows the data at July 31, 2015, from the Airbus and Boeing websites:

Figure 2: Backlogs at July 31, 2015. Sources: Airbus and Boeing.

The aircraft are grouped by seating capacity to best show how the aircraft stack up against each other. Airbus does not have a competing offering to the Boeing 777-9.

Figure 2 indicates the bragging rights at stake for the Dubai Air Show.

The aerospace world will be watching.

How come it is concluded Airbus does not have a competing offering to the Boeing 777-9 apparently because the A350-1000 is 10(?)% smaller. Still then the 747-8 is seen as competitive to the A380 while it is at least 20% smaller?

All in all it is clear Boeing has a superior position in the cargo business. Question is if you want to be there. Fedex 767F is a one time nice one, but the business is heavily competing with cheap conversions. Better fuel ecfficiency is low on the cargo operators priority list. Dropping the A380F turned out to be an excellent decision.

@keesje: Good questions.

The 747-8 and A380 are indisputably in the VLA category. In the past we have indeed pointed out that the 748 and A380 are really two different categories within the VLA. Regardless, Boeing always insisted on comparing the two airplanes, including the infamous advertising campaign that got Airbus so exercised. Setting aside this, they are both VLA airplanes.

So, in our view, is the 777-9, although barely. The VLA category has been defined as starting at 400 seats. The 777-9 is nominally 400 to 425 seats (Boeing specs); in no way, shape or form does the A350-1000 match this size in equivalent seating. Hence, the 777-9 does not have a competitor. The A350-1000’s competitor is the 777-8.

This “VLA size” is arbitrary and artificial.

Though it is not unsurprising that Boeing seems to spend quite a lot of effort on making their definition stick.

The “VLA” 777-9X has a hard standing against the “nonVLA” A350-1000.

This “VLA size” is arbitrary and artificial.

Agreed. A pointless ‘distinction without a difference’ argument if it’s only about how many hapless souls you can stuff in steerage.

Is the general consensus that an A350-1100 won’t happen?

[The performance numbers just not really adding up?]

The performance numbers do add up but only with a new engine, e.g. a RR Advance. Airbus is bringing out the -1000 and the market for a 400 seater is limited. Can Airbus get an ROI for their part of that market? We think this is the real question, not if it can do a competitive derivative in this segment.

@Scott,

Does the Airbus change in seating arrangement to allow more seats bring the A350-1000 closer to the 777-9? I thought that was Airbus’ intention to undercut the appeal of the 777-9?

@Neutron

Yes and Yes.

Tthe a380 has some major problem right now. First it has 52 orders that are in limbo. That include Air France Qantas Amedeo Virgin Atlantic Transaero Air austral and the hong kong airlines order that has went udisclosed. Also the trent xwb and the advance give a 5-6 ton penalty along with the larger fan. Bare in mind that the a380 is already overweight so it is not a viable option. Next we have the trent 1000 but barely able to provide the needed thrust with no growth so it is not so much of a viable option. So a neo is not a good option.

The best thing you can do on the a380 is to make insert a PIP on the existing engine. Engine Alliance have designed in the level of 2.5% reduction. If combine that with winglets and aerodynamic clean up it will cut fuel consumption by 7.5%.

Hi Helen,

you comment has a lot of sensible ideas but you perpetuate some facts that are wrong.

Who says A380 is overweight? The media who proliferates what others have said, not caring to understand what they are pedaling?

Compared to what Airbus once wanted as OEW? Yes, but what other aircraft project is different?

By any other measurement no. There are a couple of OEW quality checks one can do; one being OEWs fraction of MTOW and the other OEW per pax seat. On both measurements the A380 is equal or better than its VLA colleague 747-8i which was certified to an older and therefore “lighter” standard. And better than the next step down, 777-300ER, in fact better than all steps down except for the 777-200LR which has a better OEW/MTOW fraction.

So it is time to stop talking about the A380 as overweight, it does not jive with facts.

Hey bjorn i have a secret to tell you. Just one problem. The 777-300ER is no longer the a380 competitor. The a380 competes with the aa350-1000 and the 777-9X. So that means that the a380 has to go on a diet.

Maybe i was a bit too ofensive about the engine but it will add weight and drag on the aircraft.

Last but not least we should never forget the orderbook. There are many firm orders that will be cancelled or turn in options up to 52.

The A380 is in massive danger. If airbus doesn’t take a decision at Dubai airshow the 2020-2021 EIS is gone. And production will end before the a380neo enters service. So it is now or never.

Tthe a380 has some major problems right now. First it has 52 orders that are in limbo. That include Air France Qantas Amedeo Virgin Atlantic Transaero Air austral and the hong kong airlines order that has went udisclosed. Also the trent xwb and the advance give a 5-6 ton penalty along with the larger fan. Bare in mind that the a380 is already overweight so it is not a viable option. Next we have the trent 1000 but barely able to provide the needed thrust with no growth so it is not so much of a viable option. So a neo is not a good option.

The best thing you can do on the a380 is to make insert a PIP on the existing engine. Engine Alliance have designed in the level of 2.5% reduction. If combine that with winglets and aerodynamic clean up it will cut fuel consumption by 7.5%.

Reposting wrong stuff doesn’t really improve its quality, right?

It seems that UPS and FedEx dropped it for them!

Parturient montes, nascetur ridiculus mus.

So much preparatory ado to present a dragged from the attic still dusty 767 😉

767F — 83 orders

A330F –10 orders

No wonder you’re so peeved.

767F — $40mil/each

A330F –$90mil/each

( well my estimate 😉

767 passenger demand ~ zero

A330 passenger demand ~= significant.

Most of the interestreductions in the A330F resulted in PAX airframes being ordered.

Actually we see the same tactics as in the 777-9x case

defines its own class “Twin VLA” “MOM” and present it as best of breed in its class ( of one ).

You are forgetting the soon to be launched 767MOM! (grin)

You are forgetting …

Actually not.

First it was MOMmmmmmmm?

Now it is Heureka: 767! ( yawn )

Whatever happened to dismissing a plane because it only had one customer ?

A380 has only one big customer looking forward, so its a ‘market’flop’ but the 767F is in the same situation and its a success ?

Of course any business gets its customers wherever it can find them

You confuse life-tine orders with future orders.

Dismissing A380 because only having EK as major customer seems to have vaporized late 2013, after 777X launch.

Hardly. EK, but also EY, QR, NK, SQ, and LH have ordered 777X’s. Yes, 150!! of those are EK. Who’s ordered an A380 other than EK in that timeframe?

Sorry – NH

And CX for SQ. Getting old sucks. 🙁

Anyway, the point stands, my crap memory notwithstanding.

Ouch. NK ordering 777Xs? How would they configure that… 10 abreast 28 inch pitch all the way w/o recline? 😐

My conclusion is that the 779 is in a class of its own because it is basically a 747 in the form of a twin jet while the A35K is a twin jet made to compete against the likes of the 77W.

I’m still puzzled why the 767 still gets a bad rap. Its plane that is proven, still flies in both passenger and freighter theaters. I guess because it’s old you have to abandon it forever.

I am confused as to why cargo operators would consider fuel efficiency as “low”on their priority list?

Lastly, I strongly believe that if Airbus knew that they could back into the cargo market with the A380F, they would. Dropping the program was not something that they wanted. It was revenue that was lost when FedEx and UPS dropped those orders to order other models.

I think Leeham wrote some times that cargo operators have a much lower plane utilisation than most passenger airlines. If you fly less, you have to pay the capital cost with less flying hours. The capital cost become more importantly in relative terms then.

Fed-Ex flies many of their planes twice a day, fuel consumption is not a major factor as compared with a passenger version of a freighter flying 6 to 10 flights daily. A retired person does not need a fuel efficient car if his driving is limited to 10 to 20 miles daily.

That’s true. Thank you.

FedEx and UPS dropped it when it was clear Airbus was going to be years late and possibly not at all (behind the scenes stuff)

FedEx actually dropped it before the drop dead date, unknown what they worked out but UPS waited until it was past its expiration date and dropped it and got their money back.

FedEx probably got parts for the Airbus fleet, UPS? Maybe did not care so much.

For sake of not rewriting history, Airbus onesided delayed the A380F until after 2014 to focus on A380. Which was unacceptable to Fedex and UPS and they cancelled.

I believe FedEx canceled before that delay and technically were in violation of purchase. They could see hand writing on the wall that not only delayed but never to be.

Probably worked it out with Airbus

UPS waited until official.

Excellent opportunity to start the Bombardier CS500! With a large purchase from Iran. Otherwise, can you already think it’s time for the big American groups (AA, Delta, United) to launch, too, low-cost subsidiaries (as Air Canada for Rouge, Lufthansa for Germanwings, Air France for Transavia ), with a regional component, by buying CSeries? And do it in Dubai, on the ground of their (new) competitors?

Not in Dubai (which is, as noted in the main article, mainly focussed on widebodies).

Farnborough2016 is the place for a CS500 launch – if the executives at Bombardier have (a) the guts to go for it, (b) the means to finance it and (c) the ability to price it competitive against A320/B737-8.

Aspect (b) is a little tricky, as quantifying risk is difficult. Having a family with a model larger than CS300 could result in more CS300 orders and push up prices (c), improving overall company position.

It would be a terrible shame if the (expensive) lessons learnt within Bombardier during the gestation of the CS100 were not fully exploited but were instead lost due to undue conservatism or inability to access finance. Long term, not going with a CS500 would probably bury Bombardier as the emergence of further competitors (Irkut and Comac) surely won’t allow them another chance.

Slightly off topic here, but much has been made of the ME3’s geographic advantage allowing them to onestop pretty much any location in the Europe, Asia, Africa and Austral-Asia and how they are using that geographic advantage to build their non-Oil economy.

I am surprised that a similar tack has not sprung up in the western hemisphere. there are several nations/territories that would be able to onestop all of the western hemisphere using narrowbodies (as exemplified by honduras, puerto rico and panama on this Great Circle map using 737-9 range http://goo.gl/VpZvgJ ). you would think someone would spot this economic opportunity (particularly Puerto Rico is attractive given it’s US territory status and ability to serve parts of western Europe and Africa to boot)

Copa does exactly what you suggest out of Panama City. They also aggressively code-share with foreign airlines, allowing carriers like KLM and Air France to use PTY as a sort of virtual hub for parts of Central and South America.

Again slightly off topic. The VLA credentials of the 779x are dependent on 10 across. The tighter seating on flights is now reaching the wider media as more and more 9 across 787 and 10 across 777 start reaching European operators. I have picked up widely consumed feeds (radio and print) on the topic. I see this as the tip of an appreciably large iceberg going forward.

Wouldn’t it be better to just discuss the square footage (metres) available to airlines on a specific aircraft together with the recommended j/y layout as a better way of understanding a model’s size and capability

@Sowerbob:

around 70% of 777 customers choose 10 abreast. The figure for the 787 @9 abreast is probably similar.

LNC’s Bjorn Fehrm looks as SF in doing LOPAs to standardize our analysis on apples-to-apples comparisons.

“around 70% of 777 customers choose 10 abreast”

🙂 Part of the Boeing/AA/EK/AF media campaign.

“more than 70% of 777 aircraft fly 9 abreast today”. Also correct, and todays reality/ benchmark.

“The figure for the 787 @9 abreast is probably similar.”

– I count 30 787 airline operators as of now. Out of that, I’m only aware of JAL using a 787 fleet . ANA is mixed with early deliveries being 8 abreast. So just over 93% of the 787 operators are 9 abreast (taking ANA as 8 abreast). This is only going to grow.

Sometimes it seems 787-9 abreast and 777-10 abreast defenders try to generalize, play down, confuse and redirect the topic.

It seems the airlines are increasingly under pressure. If they see a structural drop of passenger satisfaction for 787 9 abreast and 777-10 abreast and see passengers actively avoiding them, it’s a boardroom topic.

They can’t admit until they have a “solution”. See British Airways. There are more but they don’t have the “solution” yet.

https://www.youtube.com/watch?v=aUsyhMg_YTQ

What do you Al Baker thinks?

Isn’t the 777X a bit wider than the 777 to allow for 10-abreast seating without the discomfort?

@Arcanum: A thumbnail (left-to-right, that is) width per seat wider.

Although Airbus has said they will not do the A380 NEO for one customer, the reality is that if they do it all, it will be funded by one customer – Emirates who are the only ones who would initially commit to it in large enough quantities to be interesting. Airbus would need to find $3 billion of headroom in Emirates business to pay for the NEO programme. But that business does not have to all come from the A380. Rolls Royce would have to find a somewhat smaller headroom in the business it does with Emirates. Hence the following may not be quite as clear cut as Tim Clark makes it out to be:

no linkage between the prospect of an A380neo and the medium twin-aisle order.

The price to NEO the A380 will also be paid by Rolls-Royce. For RR the A380 would not be the last aircraft to put this engine on but the first one. So Airbus has different sources to finance the A380NEO.

Also Airbus has to pay a price to keep the A380 on top of the list.

Don’t you think that Mr Clark doth protest too much. He would not be the negotiator he is without the linkage of a tasty discount on 359s as a quid pro quo against a commitment to the NEO. There again he has to keep his powder dry to hammer the discount vis a vis 781 as well. I am betting on 359s due to the hot and high issues discussed a couple of months ago.

The NEO decision is going to the wire on the basis that it HAS to happen and it CAN’T happen in equal measure. My money is on a launch simply because the alternative is too painful to those at the top in Toulouse.

” I am betting on 359s due to the hot and high issues discussed a couple of months ago.”

May I ask what you think of the – 10’s that Ethiad bought?They’re the same machines operating in the same climate.

Maybe Etihad aren’t using their planes on the same routes Emirates is planning.

Its a bet, no more. More based on the comments made by Mr Clark at the time and the view that it gives them options for use on some of the thinner longer routes that the 9x wont work for. No doubt it is a close call either way.

Perhaps because EK fleet strategy ≠ EY fleet strategy? Just compare their aircraft mix and use.

Tim Clark himself said that the 787-10 has insufficient thrust. So it is very likely true for his case regardless of what others are doing.

(Something of note: EY topped off their A350 order by adding A350 regionals around about the same time they ordered the 787-10.)

I suppose even RR are not seeing that as a gift but as an investment. ( GE seems to have walked that path years ago )

ergo: “Power by the Hour” will get a mark up while airframe prices could stay/not rise as much.

That fits todays most popular model “deferred cost” and “pay as you go”.

The risk of doing the A380 Neo is amplified by a slow down in the world economy. There is ample evidence of airliners struggling financially being force to cancel or deffer deliveries.

The timing is bad for Airbus and the decision to undertake such an expensive project would be a tough one.

I don’t why everybody believe that the a380neo can be built at least now. First rolls royce reduced profitability doesn’t let her participate in over risky products like the a380neo. Secondly there is absolutely no demand outside emirates and qatar. Actually customers look to cancel orders on the aircraft and replace it with the 777-9X. So i find ridiculous or even stupid for someone to believe that the a380neo makes sence. I do not understand why we are talking it about for two years now.

Just for curiosity’s sake, who is looking to cancel A380 orders and replace them with 777-9Xs?

As for beliefs, I believe the A380 NEO is more a go than a no.

Qantas.http://www.ausbt.com.au/qantas-flags-boeing-777x-as-potential-a380-replacement

this from the comment section:

“This is a click bait article. Gareth Evans outlined possibilities for A380 replacements including the Boeing 787-9, Boeing 777X and Airbus A350, he didn’t specifically denote the Boeing 777X as the future replacement. We will have to wait and see what develops in the near future but until it’s confirmed then it’s just speculation.”

Does the orignal source fit your referenced article?

Uwe: the original story source as linked in the http://www.ausbt.com.au/qantas-flags-boeing-777x-as-potential-a380-replacement article says exactly the same thing, Gareth Evans called out the 777X as a potential replacement for the A380s at end -of-life which is say mid-2020s, which is significant because a lot of people felt QF should have bought the 777-300ER instead of the A380, so QF citing the latest of the 777 family holds some significance which was lost among some of the idiots commenting on that article.

Dear Scott,

What is the exact story the A450-900LR? The plane described here with a range of 8500 sounds more like an 787-9 competitor as opposed to ULH 777-8 competitor.

Range appears to be a lot nearer to the 777-8x than 787-9

couple of hundred nm less versus 1k nm more.

Capacity wise the 359-900 is nearer the 787-10 and the 777-8x than the 787-9, isn’t it?

A versus B bespoke metrics make a comparison more difficult

and for a nice aggravation B metrics are currently in “flow”.

The key parameters are availability (A359LR 2018 vs 777-8 2022) and the size and therefore trip fuel burn which equates to load factor and yield risk. The 777-8 is one size larger.

Do we assume 777 10 abreast for 8000NM. That would become interesting.

Boeing will need to develop a nursery aboard to take care of blood clots, Massage parlor to nurse those jammed muscles and a brig to keep rioting pax at ripping the plane apart.

Is the A330-800 really going to get made? It seems odd to think that Airbus will go through with development for such a small demand. Even as a variant, it will have costs in addition to the -900, and I would think Airbus would want one of three things to happen:

+ Convert the few -800 orders to -900s.

+ Move the few -800 orders to -200s (unlikely that airlines would want the older tech/lower performance, but Airbus could cut them a terrific deal)

+ Convert some of the 57 A330-200 backlog to -800s?

I assume you mean A350-800?

The table in the main article shows 10 A330-800s. Per Airbus’ own web site “The A330-800neo retains the current-production A330-200’s fuselage length.”

But there are only 10 orders. This seems like an offering that to me will not prove commercially viable.

I believe Airbus is doing all in their power to not make the A350-800 without losing, or disappointing a customer.

Aeroflot will stay with its A350-800 order. This is the easiest way to get rid off this order and to receive some hard currency. The Russian market is in big trouble.

And a true blow to Boeing and interesting assement of the A380 picture

http://www.businessinsider.com/r-boeing-sticks-with-747-production-plans-despite-sales-drought-2015-9