Leeham News and Analysis

There's more to real news than a news release.

Pontifications: No sale for Boeing in Bombardier complaint

By Scott Hamilton

May 29, 2017, © Leeham Co.: I’m having a really hard time buying into Boeing’s arguments in the complaint about alleged price dumping by Bombardier in its deal with Delta Air Lines.

I say this despite the fact that Boeing lawyers at least four times directly and twice indirectly cited “trade publication” Leeham News and Comment in support of its case. While flattering to be used as an authoritative source, Boeing’s testimony doesn’t support the claim that Bombardier acted improperly, in my view (nor that of AirInsight, which also reviewed the testimony). There are, of course, scads of exhibits and confidential information not available for public review that could, if available for public dissemination, might change opinion.

The thing is, Boeing is known among journalists and analysts for its occasional descent into hyperbole. Or, as one reporter I talked to put it, this is an example of Cirque du Soleil acrobatics. It is with some amusement that I note Cirque du Soleil is, like Bombardier, headquartered in Montreal.

The sky is falling

For starters, Boeing asserted to the ITC that if Bombardier’s price to Delta for 75 CS100s and an option for 50 more—which Boeing calculates in $19.6m, and which Delta and BBD say is “way” low—is allowed to stand, it will start a cascading series of events that will not only put Boeing out of business, but collapse the US aerospace industry.

How many hoops does one have to jump through to reach this conclusion?

Quite a few, it turns out.

Cascading events

Boeing pins its assertions on the allegation of the $19.6m sales price and the ability of Delta to switch the last 25 and all the options to the larger CS300, which competes with the 7 MAX. It also claims the competition to sell airplanes to United Airlines, which BBD lost to Boeing’s 737-700s, drove the price down so low that it created a new benchmark against which all future deals will be measured—not only for the -700 and 7 MAX but also for the rest of the MAX family.

Lost sales to US carriers, Boeing claims, means Boeing will lose market share in the US, depriving Boeing of deposits and revenue to develop new airplanes.

(In its April 27 complaint, Boeing also said this deprivation would make it difficult to provide a return to shareholders.)

All this will eventually lead to Boeing’s collapse and with it, the US aerospace industry, its representatives claimed during testimony. This claim is where I have the most trouble.

Killing the MAX 7

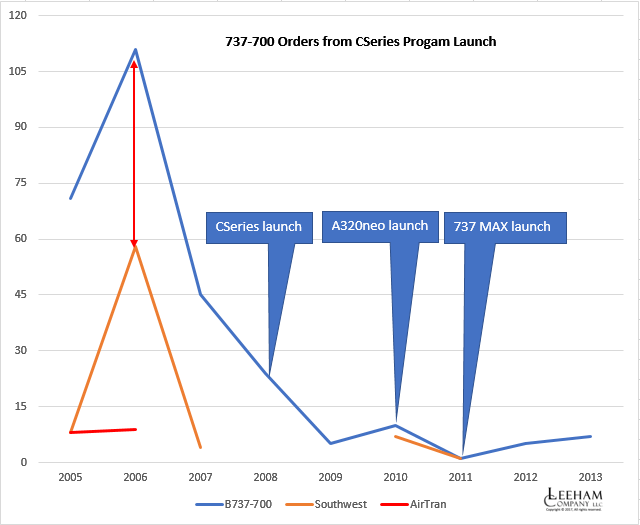

Boeing claims the Delta and United deals make it impossible to sell the MAX 7. The last sale in the US was in 2011, when the program was launched and Southwest Airlines ordered 30. The last major sale was in 2013, when WestJet of Canada ordered 25.

No sales are happening in the US now, all because of the United and Delta deals, Boeing claims.

See our report last week for more detail.

Delta’s representatives at the hearing said Boeing didn’t even offer the MAX 7 (or even the 737-700) because it had no production slots to give Delta on the timeline it needed. Furthermore, Delta said, the used airplanes Boeing did offer—19 Embraer 190s taken in on trade from Boeing’s MAX deal to Air Canada (which includes options for the MAX 7, by the way)—were purchased by Delta.

Although Delta didn’t reveal this purchase price in public testimony, it did say that finding 56 more on the open market (to reach the 75 orders that ultimately went to Bombardier) would cost 40% more than it paid to Boeing.

What does that tell you?

I don’t know the years of manufacturer for those Air Canada E-190s, but its remaining fleet are all 2006-7 build years. According to the appraiser Aviation Specialists in its valuation book, The Guide, in 2016, the current market value of 2006-build airplanes was $13.9m. For 2007, it was $15.1m. Delta’s testimony suggests its purchase price from Boeing may have been between $8.3m and $9m for those used E-190s. If this wasn’t price dumping, it certainly was a fire sale.

Or, if Delta paid CMV (or close to it), another 40% would put the price for the additional E-190s at $19.5m-$21m–a price Boeing hints at in its closing briefs. (See this report here.) I can’t see Delta paying this much for the E-190s from Boeing and certainly not on the open market.

Finally, Delta testified that even if Boeing had offered the MAX 7, Delta wouldn’t have bought it because the economics are inferior to the CSeries.

Inferior economics

The Delta order occurred early in 2016, when the MAX 7 was still just a makeover of the 737-700, seating 124 in Delta’s configuration.

A few months later, Boeing revised the design, adding 12 seats. This was announced at the Farnborough Air Show in July. LNC’s analysis shows the Cash Operating Costs (COC) of the original MAX 7 and the revised version to be inferior to the CS300, as is the 737-700. The 737-700 and original MAX 7 COCs are inferior to the smaller CS100. The revised, larger MAX 7, about equals the seat-mile COCs of the CS100, our analysis shows.

The need to revise the design of the MAX 7, adding 12 seats, was indicative that the original design was roundly rejected by the market–having nothing to do with the CSeries, which itself wasn’t selling well because of delays and doubts about Bombardier’s very survival.

It’s dead already

If the economics didn’t already indicate the 737-700 and MAX 7 were already dead, the sales figures should. And this is where Boeing’s case falls apart–and where Bombardier, inexplicably, fails to rest its case. And this is why I have a hard time buying into Boeing’s case.

Neither the 737-700 nor the 737-7 was selling prior to the United and Delta deals. Nor were they selling well during the years the CSeries wasn’t selling. The 737-700 was dead already and the 737-7 was stillborn.

Delta has only 10 737-700s in its fleet, for particularly difficult airports—those with short runways or hot-and-high conditions. Its last order for this sub-type was in 1997 and deliveries were in 2007-2008.

The last order by United for the 737-700, until the aborted one in 2016, was in 1996, by Continental Airlines.

The only other two US airline customers since 2005, when the first iteration of the CSeries program was launched, are Southwest Airlines and AirTran. AirTran eventually merged into Southwest. Southwest later began converting its 737-700 orders into 737-800s.

There have been no orders for the -700 since 2013, save the United deals in 2016 for 65—and these were switched to the 737-800 and the 737-8.

No other US airline ordered the 737-700 or MAX 7, even during times when the CSeries wasn’t offered for sale (2005-2008) or Bombardier’s own problems nearly drove it into bankruptcy (2010-2015) and sales were virtually non-existent.

Revamping the MAX 7

The dearth of sales for the 737-700 and MAX 7 has little to do with the CSeries. American Airlines chose the Airbus A319ceo and neo over the Boeing products in July 2011, when the MAX program (including the MAX 7) was launched. Delta’s position about the 737-700/7 has been recounted in testimony. United didn’t order the MAX 7 with its big MAX orders, preferring the MAX 8/9.

The original, 126-seat MAX 7 simply was unattractive. So, last year Boeing added 12 seats. Although it now complains no orders are forthcoming, there’s a dearth of order worldwide because the industry is on the downward cycle of the bell curve of orders.

Huge backlog and new design

Bombardier’s representatives, and Delta’s, point out that Boeing has a seven-year backlog for the 737. This takes it to 2024-ish.

Boeing testified Bombardier might offer a CS500, a direct competitor to the 737, which BBD says is an “if,” not a “when” (and if it did, probably not for a decade). Accordingly, Boeing fears this is the next step in its demise if the Delta deal remains unchecked.

By then, Boeing (and Airbus) should be well on the way to offering a new, clean-sheet replacement for the 737 (and A320). If Boeing isn’t offering a plane with 15%-25% better economics than today’s MAXes, NEOs and CSeries, then the company has a far bigger problem than the CSeries.

Market share

Boeing complains about losing market share to Bombardier.

Let’s allow this fear, since in the narrow 100-150 seat market this may well come to be true. Boeing officials warned of “commercial momentum” for Bombardier because the Delta deal provides an important endorsement of the CSeries.

This is fine in theory, but in fact, Bombardier hasn’t had a significant sale of the CSeries since the April 2016 Delta transaction.

Let’s also remember this: Bombardier’s ultimate goal, by 2020-21, is to be producing 120 CSeries per year. By then, Boeing should be producing the 737 at this rate every two months. This would give Bombardier a 17% global market share against Boeing (half that if Airbus’s similar A320 rate is included).

This isn’t much of a threat.

The real threats

I’ve pointed out on several occasions, in connection with Boeing’s complaints about Airbus subsidies and now the Bombardier issue, that if Boeing is as concerned about government subsidies as it claims, where is the outrage and where are the complaints to the WTO about China’s government-owned COMAC and development of the C919; and Russia’s support of Irkut and development of the MC-21?

Last week, China and Russia once again announced its joint venture for the wide-body C929. Stories are here and here.

While Boeing is wringing its hands over Bombardier’s CSeries in the 100-150 seat niche, where is the outrage toward China and Russia for single aisle airplanes that are direct competitors to the “heart of the market” 737-800/8 and 737-900ER/9?

Furthermore, the C929 will be a direct attack on the Boeing 787. Where is the outrage for the government monies going to this program?

The answer, of course, is that there is no way Boeing is going to attack the Chinese projects. China is the largest customer for Boeing in its current backlog.

Boeing’s ties to Russia are extensive, too. Russia is nearly the sole source for titanium, which is used extensively in Boeing aircraft. Boeing for years used Russian engineers on the 787 and 747-8 programs, some of whom came into the US under the H1B visa program that President Trump now criticizes.

In fact, on Friday a Boeing official said the company “welcomes” competition from China. The contradiction is just mind boggling.

According to a Reuters story last week, Boeing is pursuing Bombardier to avoid a repeat of the creation and evolution of Airbus. “Never again,” was the catch phrase, Reuters reported.

“Never again,” except as it relates to China and Russia, it seems.

I still wonder why Boeing didn’t buy BBD Aerospace just before the Canadian government jumped in. The C-Series would have been a great successor to the 737 and the space between the C500 and the 787-8 perfectly justifies an all new MoM.

Because BBD is not for sale and never was.

It WAS for sale. There were representations to both Airbus and Boeing made by the full Bombardier leadership. Boeing and Airbus decided to not join/buy/etc. They figured either: not a threat, will die anyway, we can kill it for cheaper or other. But it WAS offered on a silver platter. But Boeing (and the aerospace industry) doesn’t work in a true clean capitalist manner.

Not true, a minority stake in Cseries was for sale, nothing more.

Well, everything is for sale. Let’s say, in theory, many of the stockholders are in for between 1 to 5 dollars a share including: the Family (other then The Chairman), the street holders, the funds, Quebec and the pension plan. Then Boeing offers $8 a share. Gees, there’s going to be tremendous pressure to take the deal with all the debt the company has. And after it is bought by Airbus for $10 to $12 (who being from Europe understand The Transportation Division) and they make some kind of arrangement to not hold onto The Transportation Division for anywhere between 7 come 11 Billion, then the purchaser whoever they are have a NSA, technology to scale and use in a 757 and 767 replacement, and a manufacturing set-up with suppliers on four continents, for way-way less then what they could do on their own – Especially if McNerney type were in charge. All they have to do is guaranty production stays in certain countries, etc…

the family control 54% of voting share and they never had intention to sell it.

My take on the whole episode is that Boeing are playing games where they don’t care too much about winning but are very keen to make BBD lose. The Cseries is in that position where they desperately need volume. They are near the bottom of the cash flow position and must be hurting. They need 2/3 quite chunky orders to make it look like the programme is on track and all the noise created by this action is pure distraction. Will BBD double down on the C500? It would be a brave undertaking. If they delay too long then Boeing will be selling a NSA soon.

The problem with this approach is that there are a lot of suitors out there who have the muscle to help BBD in some way. Boeing could well find itself forcing BBD into bed with another party, Airbus, Comac, even Irkut where the Cseries suddenly becomes a far bigger thorn in their side with the potential to do far greater damage to the MAX

Narrative is the real purpose of all this nonsense. The average American is not an aircraft nerd who reads such things as leehamnews. They firmly believe that Boeing won at the WTO, instead of a draw (at best) and that all American manufacturers are victims.

Delta will undoubtedly come under pressure to buy American. Opening a European assembly plant could never be contemplated by Boeing.

The survival of the C series depends entirely on whether Boeing or Airbus can be bothered to complete with it.

Choosing when to compare the max7 vs the entire 737 line backlog is how Scott is “confused.”

The conversion of the max7 to a simple max8 shrink made a lot of sense, and the complete family is significant for airbus and Boeing. I still feel Boeing will utilize/contract some of the wing engineering from Russia based on the mc21 project (although Boeing is fairly committed to a different carbon tech than the out of autoclave method they are using).

The Washington state carbon cap and trade impact will probably help finish off Boeing northwest major assembly for new projects in the state, based on what I read today, not some massive cut to the h1b program.

I remember the mooted MC21-400 being mentioned as a good match for Boeing’s mooted MOM/797. With the whole Russia issue surrounding Trump and with Boeing having had long standing relations with Russia and increasingly good relations with Trump, is it possible that Boeing see an opportunity to collaborate with the Russians on the MC21 as a NSA/MOM solution and simply want to kill off any threat from Bombardier?

As for the possibility that Delta would stop buying Boeing as a result, that’s only a small % of the market so surely no way as important as having a profitable strategy for the entire market.

The 400 version has been hinted at/discussed by the Russians many times. Similarly, the PD-14, if it is reliably produced/supported, could force GE to see some competition in any future 797 project, which would be terrific news. I do think some partnership producing a MC-21 variant (or selling/supporting it regionally/geographically) or derivative could be a disruptive option for Boeing.

If in fact it’s a well engineered aircraft I am not sure it’s really the competitive threat to Boeing that they see from BBD, but rather an interesting option (which if pursued might also hamstring the Chinese-Russian projects).

@Sowerbob

S: “The Cseries is in that position where they desperately need volume.”

Bombardier has 350 firm orders and still a very low rate of production that will not reach 120 until 2020 at best. So assuming a progressive increase in the production rate I think we can say that the volume is there. Considering the interest for this airplane, and all the publicity generated by Boeing’s claims, there is a good chance the C Series will get additional orders in the next three years.

S: “They need 2/3 quite chunky orders to make it look like the programme is on track.”

They already have those orders: Air Canada and Delta.

S: “Will BBD double down on the C500? It would be a brave undertaking. If they delay too long then Boeing will be selling a NSA soon.”

My take on this is that because the Canadian government did not lend Bombardier the amount of money that was needed for the CS500 they now have to wait for the completion of the Global 7000 R&D programme in 2018 before launching the CS500. This way the total R&D expenses will remain the same and will not affect Bombardier’s recovery plan over the remaining three or four years, for it is a five-year plan that was devised in 2015.

S: “The problem with this approach is that there are a lot of suitors out there who have the muscle to help BBD in some way.”

Bombardier has already received the help it needed and its recovery plan is on track, if we are the believe the quarterly reports since 2015. In my opinion the success or failure of the recovery plan rests on the success or failure of the C Series and Global 7000. And I have no reason to doubt the success of either one.

As things stand right now they both have a substantial backlog and as soon as the Global 7000 will start to be delivered in 2018 it will contribute substantially to the cashflow, when the C Series will have itself started to make a substantial contribution.

Where Bombardier needs volume is in production rates of the C Series and Global 7000. And according to the recovery plan both will be generating appreciable amounts of cash when the plan expires in 2020.

@ Normand

I agree with you mostly, the reason why the Cseries needs more volume is to establish credibility. Yes they have some orders already but in comparison to all their competitors they have struggled to gain a steady stream of orders. There has been a whiff of desperation about the deals done. If the markets believes that the Cseries will fail it will become a self fulfilling prophecy

If Bombardier’s corporate health is in danger, Boeing might just be using an old business trick. Let’s call it “assisted suicide”. Spending Bombardier’s cash on defending themselves against a clearly frivolous lawsuit might put them under before a judge can get to a ruling. Then, they could generously swoop in and bail out the company and pick up the C Series program for pennies on the dollar.

On the other hand, Boeing’s new corporate mantra might be:

If you can’t innovate, litigate!

I’ll take a contrarian view to that of a CS500 supposedly not being a threat to a New Small Airplane (NSA) from Boeing.

First, a CS500 would be fit rather nicely the 160-189 passenger segment.

2nd, if not launched in the near-term, a CS500 would very likely be outfitted in the mid-term with the same engines as that of the NSA and/or an A32Xneo-Mk2.

3rd, a NSA won’t arrive before the mid to late 2020s and it will require heavy investment. A CS500 along with a CS100/CS300-neo from Bombardier and an A320.5neo-Mk2/A321neo-Mk2 family from Airbus can be done for a fraction of the cost of a new single aisle aircraft from Boeing, while at the same time making the business case for a NSA untenable.

4th, unless the NSA turns out to be a revolutionry platform, I can’t see how it would be able to outcompete a state-of-the art CS500 and mark two versions of the A32Xneo-family.

In fact, if the A320neo would be stretched by 6-7 frames (i.e. A320.5), and along with the A321neo, would be re-winged with composite wings and re-engined With RR UltraFan-type engines, Airbus could conceivably launch a 5-abreast competitor aircraft to the C-series; leading to a situation where a mark two version of the current A320neo would be “pushed” out of the territory that seems to be more favourable for optimised 5-abreast aircraft; namely the 160-189 passenger segment.

For once you say something that makes sense! 🙂

But you confuse me when you say that “Airbus could conceivably launch a 5-abreast competitor aircraft to the C-series,” for I thought there was no market for that category of aircraft. 😉

More seriously, I am in agreement with everything you say here, which gives me some hope that you will fully recover your sanity some day. 🙂

🙂

@Normand Hamel

Clearly, there’s an overlap between a 5-abreast and-6 abreast fuselage (i.e. 737 vs. DC-9/MD-80). The question is at what fuselage length a super-stretched 5-abreast fuselage is starting to lose its advantage over a similar sized, but shorter 6-abreast fuselage.

“The question is at what fuselage length a super-stretched 5-abreast fuselage is starting to lose its advantage.”

Tube or not tube, that is the question!

Where does the sweet spot starts and where does it end.

And this sweet spot is certainly different if you are a five-abreast or a six-abreast. But it likely overlaps at some point. And this is what makes it the more interesting.

That is the reason why I have great difficulty to reconstitute a new family of aircraft, from 110 to 240 passengers, by merging the C Series family with the A320 family. There is clearly an overlap at the centre that I can’t easily get rid of.

I would say Bombardier was both reasonable and bold when it chose the five-abreast configuration. What’s interesting is that the first modern Boeing commercial aircraft design, the so-called Dash 80, was a five-abreast.

Yes, there’s an overlap, but we also do have to take into account; i) that a 5-abreast fuselage is not able to accommodate LD3-45 containers in the hold; ii) that a long 5-abreast fuselage with no cargo container capability will take longer to load/unload than a shorter 6-abreast fuselage with cargo container capability; iii) that some customers prefer cargo container capabilty, some don’t (for same-sized aircraft); that a base model design range of 3500nm-plus is perhaps not that desirable for a 5-abreast aircraft.

Therefore, I would argue that a mark two version of the A320neo — having composite wings and UltraFan-type engines) — should consist of two models — a three frame stretch, 198-seat A320-800 (Space-Flex version) and a nine frame stretch, two-class 180-seat A320-900 (Space-Flex version). In contrast, the A321 is a 13-frame stretch of the A320.

With a design range well in excess of 3500nm for the A320-800 and A320-900, an all new Airbus 5-abreast family could be optimised with a design range of 3000nm for the base version, but where the larger, stretched member of the family would have reduced range (2500nm) and a single class capacity of about 180 seats, or so. The largest member would have an excess cargo capacity in the hold, so the aircraft could be designed having a smaller take-off, fuel volume limited, but very high aspect ratio wing (i.e. wing smaller in area (and lighter) than the wing on the CSeries, but not in span), and with one or two optional auxiliary fuel tanks in the hold.

Finally, Bombardier clearly saw an “opening” and took it — all hail to them. 🙂

Addendum

The A320-800 (Space-Flex version), as described, is a single class configuration of 198-seats.

“The answer, of course, is that there is no way Boeing is going to attack the Chinese projects. ” Not directly, no. But indirectly? Sure.

Scott is right to point out that BBD is never going to make a huge dent in Boeing sales. But he is quite wrong to argue that this is the relevant fact.

Bombardier/COMAC/Irkut are dangerous to Boeing and Airbus NOT because they are going to outsell the incumbents. They are dangerous because they are already forcing the price of aircraft ever-downward, putting the industry in a commodity spiral.

If Boeing cannot consistently charge enough money for an airplane to make solid profits, then there will be no replacement for the 737 – because you cannot justify a higher sticker price to make back the investment dollars in an era of low fuel prices and lots of competition: see the 787 and its near-$30 billion in the hole.

Indeed, right now plenty of airlines are doing the math and ordering CEOs and NGs instead of NEOs and MAXes – adding $10 or $20 million to the sticker price for a shiny new 737 replacement airplane is going to be very hard to justify with $40-$50 fuel.

The Duopoly worked. For years Boeing and Airbus talked a good competitive game, but they both made money. Those days appear to be over, which is great for passengers, but not for the airframers.

So why didn’t Boeing just leave Bombardier to it, instead of grinding the price into the ground and ruining it for everyone? Also threw 500 787s out of the door for bargain prices when they were selling like hot cakes, making a huge loss.

Is a CEO 320 or NG 737 ever more efficient than a NEO or Max on extremely short legs, on account of its lighter weight?

If “efficiency” is defined as cost per mile (including capital cost), then old airplanes are already more efficient than new ones.

This is the underlying problem OEMs are facing. With cheap fuel, 10-15 year-old 737s and A320s have better economics than brand new MAXes and NEOs.

Because Boeing reckoned they could drive a stake through Bombardier’s heart if they could just cripple CSeries sales. They did it with United and 737-700s.

The capacity problem that means airlines always end up with very low margins is about to hit the airframer business.

I think you hit the nail on the head there iWe. Boeing has finally discovered just how bad a position they are in due to their overall strategy of the last 10, or even 20, years.

You said it yourself, Boeing is trying to cripple Bombardier, not the other way around. To that end, they somehow managed to pull off a sale of 737-700s to United, who were supposedly looking for something smaller. One can assume that the cost of that sale, and the general lack of other orders in this category, is leading them to try a spurious claim of dumping by one of their competitors instead of actually being competitive themselves.

The very fact that Bombardier is still struggling to get orders for the C-Series should be enough to prevent this case from going to far. Or one should say that in a logical world, that would be the case.

If Boeing didn’t totally mess-up the development of the 787, it would have plenty of money…and time to develop new aircraft. The deferred production cost of 33 billion has and will have many insidious effects on future development. Deferred production cost is normal…if kept under control and in the 787 case it completely went out of control. For an aircraft like the 787, a normal deferred production would be in the 5-10 billion range. And we also know that Boeing have to paid large compensations to airlines due to repeated delays in the program. We also know that the R&D cost was several billion above prediction. Meaning, that with the mismanagement of the 787, Boeing lost the opportunity to develop several aircraft such as a true replacement to the 737 and a MOM aircraft.

@Sowerbob

S: “The reason why the Cseries needs more volume is to establish credibility.”

If Bombardier was still missing some credibility Boeing has since given Bombardier all the credibility it needed, and then some.

S: “In comparison to all their competitors they have struggled to gain a steady stream of orders.”

If Bombardier had competitors I was not aware of it. For it is the only aircraft manufacturer to offer a family of aircraft in the 100-150 segment. More seriously, it is totally unrealistic to expect Bombardier to receive at this stage the same amount of orders as A&B are receiving today, fifty and thirty years later respectively.

Anyway, its present rate of production would not be able to take it. That is why I feel very confortable for Bombardier with a backlog of 350. If Bombardier were to get a few more big orders like they have received last year one would hope that the new customers would not be in a hurry to get their aircraft.

So please, everybody out there, stop comparing Bombardier to A&B. I am sure they feel honoured, but to make such comparisons is totally disconnected from reality, and history as well. Look at what happened to Douglas when they introduced the DC-9. To make a long story short, its success was such that it created chaos in Long Beach.

So if Bombardier were to receive the same kind of orders as A&B are receiving today, or even Douglas then, it would just create chaos in Mirabel. They have given themselves five years to recover financial stability and everyone should display concomitant indulgence.

“If the markets believes that the Cseries will fail it will become a self fulfilling prophecy.”

Again, Boeing has removed any doubt about this.

@ Normand, you last comment I truly agree with, it will survive in some guise for some business combination. The balance however I must take some issue with. The orders are okay but they have picked up two large orders recently at what are reportedly very low prices. You may argue that these are necessary to get the project moving. I was in no way suggesting that they should expect orders similar to A or B but it is a fact that BBD are into this programme for a whole lot of cash and the outflows are unlikely to stop for a good few years. The order backlog is better than it was but not stellar. The C500 is the big one but as it stands I fear that there is insufficient confidence (or cash) to add yet more red ink to the bottom line. Your comparison with the DC-9 is scary, the success of that aircraft came at massive financial damage to Douglas, something from which they never really recovered. For BBD to get well they need volume to work down the learning curve and prices that reflect the quality of the aircraft. That is a tough ask

Spot on Normand.

At some stage the Grim Reaper will appear at Boeings door asking for the $33 billion of 787 deferred costs and maybe some of its other deferred costs.

How many corporations could get away with these numbers and survive?

When’s the last time United, American, Delta, Soutwest, Alaska took delivery of 737-700 or even an A320? The 737-8/9 and A321 seem to be a better value.

But if the smaller market for 150 seats and three flight attendants saves enough money over flying 175 to 200 seat aircraft with 50 empty seats….

I still think Southwest may take hundreds of MAX 7 for smaller markets. I don’t think the CS and the cost of another aircraft type is worth it for them. Also, another model for 150 seats in mixed class should be looked at, with a five foot stretch over the MAX 7. United and Alaska could have a good combo with MAX 7.5 and MAX 9. American could convert their MAX 8 orders to MAX 7.5 and use the A321 for the next step up in capacity.

@Sowerbob

S: “The orders are okay but they have picked up two large orders recently at what are reportedly very low prices.”

We have to make a difference here between profit and cashflow. The first C Series deliveries will restore the cashflow, which was bleeding like crazy during the development of both the C Series and Global 7000; not to mention the Learjet 85, which itself put BBD in the red for 3B.

Bombardier may only have about a dozen deliveries so far, most likely at a loss, but it is all welcomed cash that can be used to pay employees and outstanding bills. And next year the Global 7000 will start to be delivered to customers, and this is all gravy because the Global is sold with much higher margins than the C Series. Bill Gates doesn’t really care for the price, he just wants the best. So not only will the cashflow increase substantially with the Global 7000 but the profits will almost be immediate.

The focus is on the recovery plan, and so far it is tracking well. And when we will have reached the deadline in 2020 Bombardier will be a much healthier and stronger company. And its margins on the C Series are likely to have increased by then because the manufacturing costs will inevitably go down, and I expect them to go down fast because of all the advanced technologies involved. The focus should really be 2020 and beyond. It’s the same for Boeing, but for completely different reasons.

S: “The C500 is the big one but as it stands I fear that there is insufficient confidence (or cash) to add yet more red ink to the bottom line.”

I am of the opinion that Bombardier can do the CS500 when the Global 7000 R&D will have been completed in 2018. This way they can retain their expertise while maintaining the R&D expenditures at a relatively constant level. In other words additional red ink will not necessarily be required. Therefore the “bleeding” should remain constant if the CS500 follows the Global 7000.

S: “Your comparison with the DC-9 is scary, the success of that aircraft came at massive financial damage to Douglas, something from which they never really recovered.”

The C Series situation is totally different. The DC-9 was not a standardized aircraft and each batch was highly customized. The C Series on the other hand is a highly standardized aircraft which is extremely economical to manufacture. Remember that despite being twice as big as the CRJ it takes half as many people to build a C Series.

Besides, the way Douglas was managed then and the way Bombardier is managed today is very different. Alain Bellemare and the team he has put in place are all very experienced individuals who are extremely competent. Even in the days of Pierre Beaudoin the company was much better managed than when Donald Douglas Jr was leading the company.

S: “For BBD to get well they need volume to work down the learning curve and prices that reflect the quality of the aircraft.”

In regards to volume you need to know that in 2020 they will be at 120 a year on the C Series, which is close to the maximum attainable in Phase 1. Phase 2, if required, would double that but would not add anything in terms of productivity. This means that in 2020 Bombardier will be where it needs to be. And right now they have everything they need to get where they want to be. You just have to be patient and give them time to get there.

@ Normand

I know where your heart lies and for a whole host of reasons I hope you are proven correct. I think there will be a few bumps in the road but good luck.

@Grubbie

If I understand your question, the answer is no. For the difference in weight increases is more than compensated for by the increase in efficiency of the new engines. This was the main idea behind the NEO and MAX. These are fundamentals and should not vary much except for future PIPs.

On the other hand what iWe says is a transitory phenomenon that can vary widely over time. To illustrate what I say lets take the extreme case of an oil barrel at 150$. In such a case the value of the C Series for example would go up dramatically in relation to the A320 and 737, because it is so much more economical to operate than both.

Actually the C Series business case rests on fuel prices. At 100$ a barrel it becomes a very interesting proposition, and at 150$ it would be more difficult to stay in business and continue thriving without such an efficient aircraft. Especially if fuel prices were to remain that high for a prolonged period of time and became the new normal.

Capital cost (acquisition price + interest rate), fuel prices, and overall aircraft efficiency (operating costs) are variables that are all part of a big equation that can help buyers to properly evaluate a potential acquisition.

Right now new efficient airplanes like the 787, A350, C Series and 777X are all having difficulties taking in new orders because fuel prices are stubbornly remaining low. But the 737 MAX and A320neo are long established players that can ride this comfortably while remaining attractive for buyers because of their relatively low acquisition cost.

Personally I don’t expect to see fuel prices going up appreciably, and for a sustained period of time, in the foreseeable future. And if I am correct there will be some casualties for sure, along with a few NDE.

@OV-099

Statement 1- “A base model design range of 3500nm-plus is perhaps not that desirable for a 5-abreast aircraft.”

Statement 2- “An all new Airbus 5-abreast family could be optimised with a design range of 3000nm for the base version, but where the larger, stretched member of the family would have reduced range (2500nm) and a single class capacity of about 180 seats, or so.”

There is so little difference between 3,000nm and 3,500nm that I almost saw a contradiction in what you were saying. But I have no real issue with that, for anything above 3,000nm will do with me. On the other hand when you suggest that the stretched Airbus five-abreast should have a reduced 2500nm range I interpret this to also mean that Bombardier should design the CS500 with a 2400nm range, as suggested by LNC. Well, I think you and Bjorn Fehrm are seriously mistaken! 🙂

I am of the opinion, and I feel quite lonely in my camp, that the CS500 should have the same range as the A320 and 737. All the A&B variants have more or less the same range, which is around 3,500nm, depending on what reference you take in terms of passenger weight, and also which evolution: CEO or NEO; NG or MAX. There must be a reason for this, don’t you think?

My reasoning is based on two things: history and actuality. Let’s start with history. Trident, Caravelle and Mercure, what do they have in common? You guessed right, their limited range, but also their limited success.

Now, why did Airbus make the A320 with the same range as the 737? Or put differently, why is it that the Airbus did not content itself with a 2,500nm aircraft? You guessed right again, because airlines would have gone to the longer-ranged 737. And what do you think is going to happen to the CS500 if its range is limited to 2,400nm? You are absolutely right, it won’t go very far! 😉

Perhaps, like many other people, you view the CS500 as a complement to the A320 and 737. But I would rather view it as a replacement. And how can the CS500 possibly be a replacement for the 737 and A320 if it has an inferior range? It is simply impossible.

“I interpret this to also mean that Bombardier should design the CS500 with a 2400nm range, as suggested by LNC. Well, I think you and Bjorn Fehrm are seriously mistaken!”

Not at all.

The design range of a CS500 “neo”, outfitted with UltraFan type engines, should quite easily exceed 3500nm. Bombardier should obviously try getting as much out of the CSeries design as possible.

What I’m talking about, however, is about a 5-abreast aircraft that would be designed to be significantly lighter than the CSeries. One major design objective would be long and slender wings* — possibly including laminar flow.

Since a mark two version of the A32Xneo would have more range capability that anybody would ever really need, an Airbus 5-abreast family should IMJ be optimised closer to the single aisle “sweet spot. More than 90 percent, apparently, of all narrowbody flights in the world are below 1500nm.

A significantly lighter 2500nm-capable 5-abreast aircraft, therefore, would not have to carry around the extra structure and heavier airframe that is required for an aircraft designed to transport 180 passengers over 3500nm-plus route sectors. Thus, a state-of-the-art CS500 would risk being squeezed from above by an A320-800 (as described above) and from below (range-wise), by a significantly lighter 180-seat Airbus 5-abreast competitor.

http://www.airbusgroup.com/int/en/news-media/corporate-magazine/Forum-89/Wings-of-the-future.html

“More than 90 percent, apparently, of all narrowbody flights in the world are below 1500nm.”

So if I understand your reasoning, what you are trying to say is that Boeing and Airbus were quite stupid to give the 737 and A320 such an unwarranted range.

And to make matters worse they gave the same range to each member of their respective families. What a bunch of idiots these guys were!

OV, you are falling in the same trap in which de Havilland, Sud-Aviation and Dassault fell into. Like them you have a short-ranged vision. 🙂

Aircraft design is a compromise between competing factors and constraints. When Airbus, for example, designed the A320 they didn’t have a single aisle platform. In order to compete properly with the 737, it was obvious that a 6-abreast platform with built in growth capability was needed. What growth capability means was that the wing box had to be big enough to handle a significant increase in MTOW for a stretched version – and not for the stretch itself.

Single aisle aircraft are rarely used near their maximum performance capabilities (particularly for range, but also payload). Thus, airlines are much more interested in deploying aircraft on a variety of routes and missions in their networks versus consistently operating them at

maximum capability. Cast in this light, the A320-200 wasn’t designed with excessive range. In fact, the design range (pax + bags) for the A320-200 (minus sharklets) is about 3300nm, but it doesn’t take into account additional cargo, headwinds and fuel reserves for diversions. So, the effective range is less than 3000nm.

Now, Airbus has the luxury in already having a highly succesful single aisle family. Bombardier, on the other hand, doesn’t have that. Airbus also have an added luxury of being able to increase in size and capacity, members of their existing single aisle platform (i.e. A320-800X/900X, A322X, A323X), without too much difficulty.

Thus, by upgauging the A320neo series (Mk2 versions), Airbus will be able to develop a 100-seat to 180-seat 5-abreast family of aircraft that will not overlap with their existing single aisle platform (e.g. A315X, A316X, A318X).

However, the design for the A315X, A316X and A317X would incorporate all of the latest technologies available. In addition to a lower design range that leads to lower MTOW, lower OEW etc., fuel consumption per seat should, at least, be 10 percent lower than similar sized members of the CSeries family. IMJ, that would change the game quite significantly. Instead of having a one size fits all — with respect to one single aisle aircraft family — operators would be forced to look at having 2 optimised single aisle families (i.e. 100-seat to 250-seat-plus).

“Thus, a state-of-the-art CS500 would risk being squeezed from above by an A320-800 and from below, by a significantly lighter 180-seat Airbus 5-abreast competitor.”

The reality is that if the CS500 comes out with a range of 2,400nm, as Bjorn predicts, it will be squeezed between a rock (737) and a hard place (A320). To be more economical than the 737 and A320 would not be enough for the CS500. It also needs to offer the same performances. And that includes the range.

You seem to have misunderstood the whole thing. 😉

2500nm would be the design range for a 180-seat A317X (i.e. 3000nm for an A316X). I’ve not been saying that the CS-500 should be designed having a 2500nm range capability. In fact, Bombardier should IMO go all out and design the CS500 with about the same range as that of the 737-8MAX and the A320neo. What I have been implying, though, is that the CSeries could be at risk of being squeezed between a 5-abreast A315X,A316X,A317X family and mark two versions of the current A32Xneo family.

“You seem to have misunderstood the whole thing.”

This is indeed quite possible, because I don’t understand the majority of your posts. Perhaps it would help if I read them, but I have no time for that. 🙂

Joking aside, I have to admit that I was indeed automatically transferring anything you said about your baby Airbus to my baby Bombardier.

I previously said that I felt lonely in my camp about the CS500 range and I am glad to see that I am now in good company.

Cheers!

Normand

“The design range of a CS500 “neo”, outfitted with UltraFan type engines, should quite easily exceed 3500nm. Bombardier should obviously try getting as much out of the CSeries design as possible.”

Do I see a contradiction here? 😉 Obviously you don’t want to admit it, but deep down inside YOU KNOW that 3,500nm is the way to go. 🙂

“Obviously you don’t want to admit it, but deep down inside YOU KNOW that 3,500nm is the way to og.”

Again; 35000nm for a CS-500 — yes; 3500nm for an A317X — no.

A 3500nm range for the CS500 is EVENTUALLY the way to go. The first step is a quick and dirty stretch trading range for seats.

There are plenty of 737’s and 320’s in fleets that can take care of the extremes on range, but they are also penalized by carrying around tons of extra weight they don’t need for sub 2500nm, (the meatiest part of the narrow body route networks).

Sure, at $100+/bbl oil, the CSeries has a huge advantage with trip costs, but at $50/bbl, fuel is still a very significant proportion of airline expenses, and the savings of a CS500 would not be insignificant.

Airlines have spent, and are spending, hundreds of thousands of dollars, to millions per plane, outfitting them with various styles of winglets to squeeze a couple of percentage better efficiency out of their aircraft.

A 2500nm CS500 should be able to handily best a 738max or 320neo over that range.

Yes a 2,400nm range CS500, as expected by LNC, would be acceptable as a quick-to-market interim solution. This would give the Bombardier engineers more time to develop an optimized version of the CS500 that could also benefit from further developments of the GTF engine, and perhaps later on the Rolls-Royce UltraFan.