Leeham News and Analysis

There's more to real news than a news release.

Why is Airbus A330-800 not selling?

By Bjorn Fehrm

Introduction

November 02, 2017, © Leeham Co.: Airbus A330neo flew its first test mission two weeks ago. The test aircraft was the bigger A330-900, the neo version of the A330-300. For the present A330, the sales and delivery of A330-300 (the 290-seater) and the A330-200 (the 246-seater) is almost even, 720 versus 650 (including 70 MRTT and Freighters for the -200). But sales of the -300 in recent years far outpaced the -200, for which sales virtually dried up.

For the A330neo version, the A330-800 is not selling at all. Six aircraft are on order for Hawaiian Airlines while 211 are ordered for the A330-900. Why?

A330-900 during its first flight. Source: Airbus.

We decided to use our performance model to understand why the smaller, longer range A330neo has fallen from grace.

Summary:

- The A330-800 flies longer and with lower fuel burn than the A330-900.

- But the differences are not large. And fuel costs are no longer a dominating cost in the overall cost picture.

- For other costs, the types are too similar. The A330-800 doesn’t have any scale advantages over the A330-900; only range, and the A330-900 is flying longer and longer.

Discussion

The A330-300 versus -200.

The A330 was introduced as the A330-300 in 1994, with Air Inter as the first customer. The range for the first 212 tonnes generation was 4,000nm. It could not compete with the Boeing 767-300ER, which flew over 5000nm. The A330-300 could pass the Atlantic, but not much more.

It was the little sister to the long-range A340-300 (with over 7,000nm range and no ETOPS restrictions).

To better compete with Boeing’s 767, Airbus introduced the shorter, longer-range A330-200 1998. It could fly 240 passengers 6,400nm in its initial 230t version.

With the A330-300 limited to medium range routes, the A330-200 had good sales. It flew the missions of the A340 with 50 fewer passengers and at a lower cost. The A330-200 has been popular with the airlines until recent years, Figure 1.

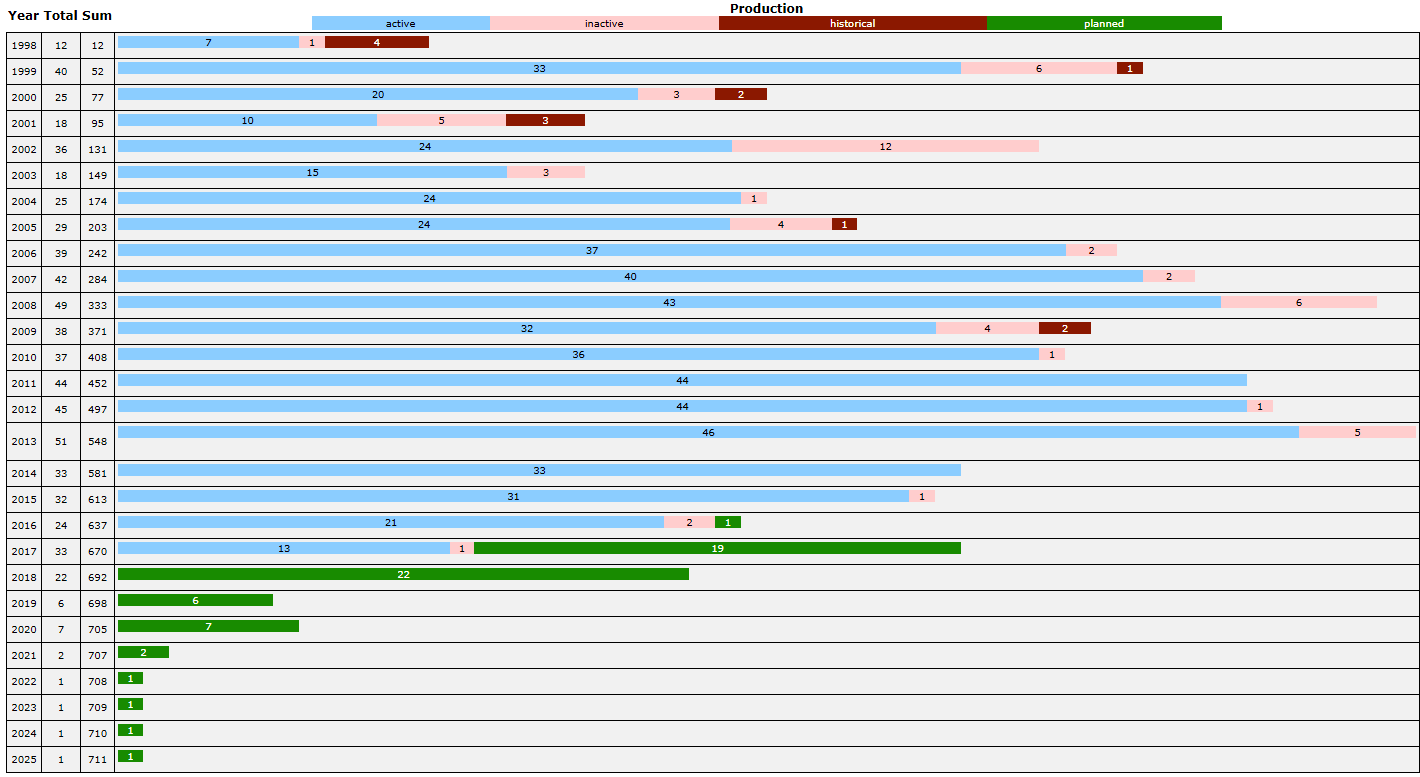

Figure 1. A330-200 production sequence over the years. Source: AeroTransport Data Bank. Click to see better.

A330-200 production had healthy levels until 2016, with about three aircraft per month. The 2017 production is still for 33 units, but it has a larger part of MRTT (Military tanker and utility transport) versions.

The following years the deliveries fall for the A330ceo and should cross over to the A330-800 from 2019. But there are no orders for the A330-800 version. Hawaiian Airlines have six on order, with planned deliveries 2019 and 2020.

A330-800 versus other A330 variants

Why has a variant which commanded 40% of total deliveries fallen to 3% in five years? Of course, the A330-300 and later -900 have increased capabilities. The A330-300 can now cover missions up to 5,600nm or 12 hours. But a 37% fall is not explained by the A330-300 going from 5,000nm to 5,600nm.

To understand more, we ran the A330-200, A330-300, A330-800, and A330-900 over the same 4,500nm mission. This is a typical trans-Atlantic flight, starting in West Europe and flying to the US Midwest.

All aircraft were equipped with our two-class Normalized cabins of A330-200 246 seats, A330-800 250 seats, A330-300 290 seats and A330-900 294 seats.

We used our standard rules of 5% enroute reserves, 30 minutes circling and 200nm alternate.

The A330-200 consumes 51.5t of fuel, the A330-800 44.9t, the A330-300 55.3t and the A330-900 49t. This makes for seat mile fuel differences of A330-200 116.5% (the -800 is datum), A330-300 at 106.1% and finally A330-900 at 91%.

Nine percent higher fuel burn per seat than A330-900 is a lot, but with Jet fuel at $1.75/US Gallon (or $70/Barrell), the higher fuel burn of the -800 cannot be the whole explanation.

Cash Operating Cost differences

When we look at the other costs making up Cash Operating Costs (COC) we find:

- There is no real difference in flight crew cost between the types. As a result, the crew cost differences are small (one cabin attendant) and the larger -300 and -900 divides the costs over more seats. Their per seat cost is 10%-13% lower (the higher value for the higher seat count -900).

- Maintenance costs are essentially the same between the -200/-300 and the -800/-900. The smaller and larger variants have the same Max Take-Off Weights (MTOW) and therefore engines. Again, the per seat differences make the larger variants 10%-13% cheaper to run.

- The same goes for Navigation, Landing and Handling costs. The larger aircraft are around 14% lower in per seat costs.

The similar block costs for everything except fuel means the A330-800 doesn’t have any smaller-scale advantages over A330-900.

The A330-800 aircraft mile fuel advantage is 7%, but with fuel at a low price, the difference is $1700 on a mission COC of $75,000, a 2.3% difference.

Conclusion

As the A330-900 approaches 7,000nm range with the up-and-coming 251t version, the air is getting thin for the A330-800. It doesn’t have any real cost advantages other than fuel cost on a mission basis. With today’s fuel prices, this isn’t worth much.

The A330-900 carries 50 more passengers and has a better residual value. The A330-800 has fallen into the trap of a non-loved variant. The used aircraft market will be difficult. Lessors won’t touch the type.

The variant is for those airlines that need the range (up to 7,800nm in a 251t variant) and that fly the type until it’s time for the scrap-yard.

Thanks Bjorn. Does not look good for the 338 and hence the AB.

However, there could still be niche markets for the 338 out there? Such as long range on thin routes with less pax and more fuel? Or good range in high density (LLC) layout? (As you know I like the 330-200’s)

So what can AB do in the market between a 321+/322 and 339/359. This is where Boeing could have the “797”, 767Revive and 787-8. The 200-250 seat market has potentially strong growth potential during the next 10+ years.

Is the clearer than ever that AB needs a NMA/Mom/330Replacement?

There’s no engine for that MOM.

There are SA engines and that one for B787 and A330.

Typical SA is about 150kN.

B787/A330 are about 250kN.

MOM would need something about 200kN?

I was on the engine desk for an A330-200 operator for several years. I would have like that aircraft a lot better if they’d dropped the idea of thrust reversers. For a surprising amount of the time we flew around with them inop anyway as they were so complicated and unreliable. The effects of ditching them entirely would be;

– Less expensive aeroplane to buy

– Less expensive aeroplane to maintain

– An aircraft with fewer defects, restrictions and better reliability

– More efficient engine installation (fewer aerodynamic duct losses), and better fuel consumption

– Some weight restrictions on particularly short runways, but not relevant to us or most operators I shouldn’t think.

Not all modern jet liners have thrust reversers – they’re optional on the Embraer 145 for instance. I think the A380 only has them on the outboard pair (I stand to be corrected on that).

This might be a relatively easy way to make the A338 more competitive – not sufficient mind you.

Embraer 145 for instance. I think the A380 only has them on the outboard pair (I stand to be corrected on that).

The A380 only has TR on the inboard engines. Reason if I remember correctly is that at some airports, the outboard engines are very close to the edge of the tarmac, or even beyond it, and using thrust reversers on them would lead to lots of dirt etc. being raised and possibly ingested.

As for the TRs on the A330-200/-800: As the -800 has different engines and thus thrust reversers, I doubt this would make a material difference. The points Björn raised seem a lot more significant than TR reliability.

@Chris Lee:

“…if they’d dropped the idea of thrust reversers…This might be a relatively easy way to make the A338 more competitive….”

And also a relatively easy way to lose engine commonality with 339 – the Neo which clearly will see a far higher typical landing weight than any other Neo @ most operators and need those thrust reversers. This is especially the case among operators based in S.E.Asia(And probably those based in snowbelts too) where landing with max payload on a very wet rwy occurs yr round and often with poor rwy surface/drainage conditions even @ top hubs like CGK.

Historically, S.E.Asian operators are among the top mkt prospects in the globe to acquire any 330. I’m not exaggerating as it’s in the fleet of practically every widebody operator there such as PR, Cebu, GA, Lionair, SQ, MH, AirAsiaX(all 3 brands), TG, etc….and that’s excluding large operators based just a bit further north such as CI, BR, CX Group, HX and the Chinese Big4.

For the already tiny global fleet of 338 expected(even if current sales magically triple or quadruple by EIS), losing 100% T7000 commonality with 339 is commercially a no go for the 338. RR may deactivate Thrust Reverser(i.e. no change in production cost) via software tweaks for 338 application but redesign T7000 without TR for production is out of question.

You don’t have to re-design the core engine for installations with & without thrust reversers. The two systems are independent and the core engine can be common.

Nor do aircraft have to be designed to land at maximum take-off weight – there’s a fuel dumping system to cater for a quick return to base.

Thrust reversers reduce the required runway length after a rejected take-off, but I hold that since 90% or more departures won’t be to destinations 7,300 nm away, giving away some emergency stopping distance in order to make the aircraft more competitive is a fair trade.

Bjorn’s point is that operators aren’t buying the aircraft- the reason for this is that the aircraft’s range capabilities, which are of interest to relatively few customers, seem to outweigh the prime directive for any commercial aircraft which is to deliver the best Cost per Air Seat Mile.

Further to my original post, there are another couple of advantages to deleting the thrust reversers;

– Weight

– Engine life limited parts (LLP) cycle limitations – a reverse thrust operation puts the engine through a mini-cycle and is taken into account when the LLPs are lifed. Removing this mini-cycle might provide scope for increasing the life on wing of the engine, reducing overhaul costs.

Once you’re on this track, there’s a virtuous circle to be exploited. A significant reduction in weight could lead to increased life of landing gear for instance. I do recall when they started out on the A330-NEO programme that Airbus would strictly limit this activity – “if you pull on that string, it will never end” being the quote that I remember.

Some real interesting stuff, in mining similar with breaking with engines or electrical motors, cost, wear, safety on large (400T) haul trucks.

At what point for example could it be beneficial to go for 6 wheel bogeys on a 359 to give you more breaking power and less use of thrust reversers?

Just to add a bit of trivia. the KC46 has no thrust reversers.

Seems odd to me but as was the crux of this part, lower cost, lower weight, more reliable, the whole bit.

I don’t know if the A330MRT ala KC47 would have been able to meet specs without using them.

I will also note what we just got was one of those rare views into the real world of why the people that have to work with aircraft like some and don’t like others.

Its things like balky thrust reversers that cause issues.

I know of US mechanics that that did not like the Airbuses. Hard to work on and hard to get parts for.

I have had some of that myself. Trying to get the kind of detailed trouble shooting I need on a European Dryer was impossible.

What I could get out of and is expected on this side is not available on the other. Just remove it and replace it.

And in this case it was not the sensor but I had to build my own data base to fine out, then found I could not even get it out as it was blocked in.

@Transworld

The winner of the first KC-X competition was labeled KC-45 by the USAF. It was the KC-30 offered by Northrop-Grumman and Airbus based on an A330MRTT.

The problem for the winner of the rigged second contest was the capability to take off with the required fuel amount (200,000 lbs) from just about half the available word wide airfields than the former winner.

You don’t need to care about breaking distances in case you can’t get an aircraft airborne save in first place.

With increasing diameter of the fan the thrust reverser gets more and more high tech to get light weight and expensive to repair. They have passed the Landing gear set in maintenance cost. So as the aircraft with the latest CFRP T/R designs the maintenance cost will be significant. Just check the leasing cost of the latest T/R halves to get a feel for future OVH cost.

The difference in number of passangers of this planes doesn’t give the adventages for A338 in all costs

Thx Bjorn for the analysis which confirms what I hv always been suspecting re the tech/econ reasons for the lack of 338 sales.

I also suspect Airbus continue with investing in 338 development & cert mainly because of:

1. Relatively low cost investment due to extremely high level of tech/production commonalities with 339….exactly the underlying reasons for the similar op costs in crew, maintenance support and nav/landing/terminal handling 338 vs 339. Flat chance for Airbus to pour even more $ into 338 upgrades(unless tied to 339) to improve its sales prospect which defeat its current low development+cert cost advantages like some folks are suggesting.

2. The prospect of military /freighter(i.e. 338F) variants to succeed 332F in the future. Unlike a hypothetical 788F, a 338F will be a straightforward carry-over development following the pre-existing 332F template with tons of design reusable fm the 332F(including that bulge fairing in the nose wheel).

My question is what option/s are there then for airlines in the 200-250 seat medium to long haul.

Maybe that’s why the 339 is also not selling well because airlines realized that and decided to go for Boeing in the entire 200-300 seat segment?

The 330’s fuselage “section” could potentially be the basis for an all new aircraft build with CFRP’s but with benefits of using the same interior that could fast track things?

@Anton:

“…what option/s are there then for airlines in the 200-250 seat medium to long haul.”

Possible options available immediately or shortly=

1. Order 321LR

This thing can carry 200seats(2-class) over 4,000nm(i.e. 8hrs+ sector) per Airbus nominal specs.

2. Order 332

IAG did that recently for Level with plan to add more. Most analysts suspect contract price is dirt cheap and production cost is relatively low anyway.

3. Order 788

IAG also did that for BA last Apr to top-up their 788 fleet. JL did similar in Sep.

4. Order 763ER

If Boeing restart 767pax production line as reported recently. Most analysts suspect contract price will be dirt cheap and I suspect production cost will be even lower than 332. Industry rumors suggest UA is highly interested in the idea.

Possible options available @ least 5~7yrs fm now:

5. Order 322

If Airbus launch this 320 variant that’s larger than 321Neo(almost 753 size) and with a larger wing along with higher MTOW.

6. Order 797/MoM

If Boeing launch this. It’ll essentially hv the same general specs as the 763/764ER or 310/300 EIS over 30yrs ago but of course, with 787 gen tech+efficiency level.

Quite a lot of choices for such a relatively small niche.

Thanks FLX. My concern is for AB around the 332 size. I had my goings on about an A330-200″E”, the CEO with the NEO’s wing, interior etc. Engine pylons an area that will need attention as far as I could make out?

End of the day AB needs something between the 321/22’s and 339/359’s.

FLX – interesting take.

That would mean all new though as there would be the PCF.

Be interesting to see.

Any idea what kind of Containers the A330 uses?

@Anton:

“…the 339 is also not selling well..”

By recent widebody mkt history, sales result is not phenomenal but not bad either @ 200+ achieved only in a bit over 3yrs.

“..airlines realized that and decided to go for Boeing..”

“airlines realized” what?

“..go for Boeing in the entire 200-300 seat segment?”

Is that why airlines continue to order/add more 359 recently(e.g. UA, CX)? Or 359 is a Boeing product?

Forget about Airbus nominal seat count. 359 is a 300 seater in the real world rules for longhaul mission today such as ‘mandatory’ flatbed with direct aisle access for every J seat.

“The 330’s fuselage “section” could potentially be the basis for an all new aircraft build with CFRP’s”

All 330 fuselage section are designed+optimized+tested+certified with largely metallic materials so I don’t know what U are talking about re CFRP. Simply replacing metal with CFRP is by definition a completely diff design “basis”(i.e. no diff than a clean-sheet design in term of development cost+duration) or U end up with an airframe not optimized at all because e.g. U will be applying metallic assumptions on CFRP materials when designing structures.

“but with benefits of using the same interior that could fast track things?”

U must be joking…..especially when Airbus has been doing precisely the opposite re 330Neo: Investing time+$ to give it a cabin interior as diff as possible fm the 330Ceo.

May be Airbus, for reasons unknown to U, somehow prefer to ‘slow track things’ re 330Neo despite delivery is already @ least 0.5yr late for TAP…..

Lots of things here, I meant the 330NEO interior.

What is the viability/plausibility of a “clean sheet” New 330-family based on the 350’s fuselage and interior. New centre section, wing box, wing etc.

The base model to have a length of approximately 58m and seats around 260 pax. Range (tricky?) 6500Nm, RR Advantage engines (again tricky) 65KLb?

Effectively the upper end of Boeing’s MoM while the 322 at the lower end.

These are all just ideas, what matters is what the market wants. One thing is certain, AB needs a new twin aisle with seat capacity between 220 and 260 seats, the Ultra-fans should be available by 2025.

Anton: Wayyy too heavyy

The A330-800 will be the basis for a new A330F and A330MRTTneo. It should have a space in the market for longer range or heavier payload routes but then it bumps into the 787-9 area and cannot compete well. Going the other way of making the A330-800 much lighter to a A330REneo and limit MTOW allowing for massive Engine derate and taking it into 797 territory for 2.5-6hrs jumps 18hrs/day might be a better way. Some redisgned lighter parts can find a home in the A330-900 as well.

As said earlier the lack of airline interest in the A338 probably distract them from the 339 resulting in airlines going for the 787-8/9 combination.

To save 339 sales AB will have to give airlines a viable alternative for replacing 330-200’s, many airlines are operating both -200’s and -300’s.

I don’t buy the A330MRT. Not that many orders out there and the ones there are filled by the A330-CEO

No one is going to want to change that. No advantages of import the way tankers work. New engine and other odds and ends to deal with in very small fleets.

A330-1000 maybe?

I pushed that concept for over a decade but no one seems to agree 🙂

https://lh3.googleusercontent.com/-0aNG9gitGII/WfHbBs3p-II/AAAAAAAADOQ/L6r85jtyj8ESU0zHCRxWS4tOwFOFchkjACLcBGAs/s1600/A330-1000.jpg

At least I like it Keesje, how much can the 330-3/9 be stretched before tail strike becomes a real issue. It could be a viable alternative to the 78J for shorter range while the 350’s more for longer haul.

Not sure but a 330K could be a base for a freighter when the current 777’s go out of production?

The A330-900 can probably, easily be stretched to the length of the A340-500. That would add about 4 rows of economy seats (32 seats, 11 % higher capacity). If it’s possible to do a slightly longer fuselage, this could very well be an A330-1000 (simple stretch of the A330-900). The engines have the necessary thrust, the A330 has a larger wingspan than the 787-10, and if the MTOW stays the same, there could very well be a business case for a A330-1000.

An 330K will be good optimization of the 330NEO’s capabilities, an 76KLb T7000 should be available.

Again range not a key element (6000NM?), inter Asia and possibly Asia (India/China/ME) to Europe key applications as well as high density Europe to Central US and East coast.

(Seattle to Beijing 4600Nm, Atlanta to Paris 3 800NM, LHR to Delhi 3600Nm).

Keeje:

I believe that was A350 and 777s are for.

Transworld you to pragmatic, we are looking for excuses for the 330NEO’s existence. Think I literally spend maybe 1000+ hours on 330-200’s as pax, won’t like to see it die.

But as for the 747, maybe time to make peace?

Anton: Sorry.

Not sure about the 747? I did say 777?

IMU the design point would hinge around how much stretch is possible without dropping below that “magic range” that initially furnished the swap over from A332 to A333.

I think by now it has become apparent that AB needs something new between a theoretical A322 and the 350.

But are there a big enough market for a 797, 787-8 and AB240New? The 787-9, 339 and 359 covers the 280+ seat longer range requirements.

A seriously reworked 330-200/800, from nose section to wing box, wing (~300 square m, <52m, class D?), range ~6000Nm could be an option. New engine availability with thrust around 50-60 KLb problematic.

Or has the time come for AB to bite the bullet with a clean sheet A330 replacement that is pitched between the 787 and 797, OEW's around 85-90T, 30% less than 787/330's. This will give them the following line-up;

A322, New 240 seat (7000Nm), New 280 seat (6000Nm), (339/33K), 359.

An A330-1000 gets into the same troubles as the A340-600, that empty mass per pax gets too high, the question is if a small stretch is worth the money. Airbus should maybe put the engienering and money into an A322 instead and work on refining the A350-1000 wing further with a future RR Advance certification unless RR charnges $50M/each spare Engine.

Some of these things are mulling around in my head.

A322, will need a new wing. Then AB should not “play”, give it a wing that can handle MTOW for a range of ~5000Nm, it will be cat-D. Thrust 35-40KLb, will the PW1100G handle it or should they wait for the Ultra-fan?

Instead of the 33K I sometimes wondered about a 350-1000 with the 359’s wing, but 6 wheel bogeys, XWB84’s, MTOW ~275T. Range should still be around 6000NM and be very competitive on seat mile cost?

I don’t understand how such an airplane sh0uld commercially work. According to the picture the fuselage has about the same diameter as the lenght of a common fly.

Definitely to small for people.

That looks perfect, 6 wheel bogeys? Maybe drop the MTOW to 354T with 76Klb RR Advantage engines and 6000Nm range, 2-4-2 seating. Keep your 787’s.

An A322 will most likely need 4 wheel bogeys?

I see the 321+ as an updated 321 with mods that could be applied to 320+ which could be a 3-4 row stretch of the 320. The 322 virtually a “new” aircraft?

The 320 can stay as an option (LCC’s) and/or replaced by an CS500

Yes, if they decide to built new A330-1000neo. As long if Airbus will consider it. It’s their choice.

Ho many 787-8 have exactly been ordered for the 787-8 over the last 3 years?

Many airlines use(d) A330-200 to expand their networks. Supported by the aircrafts good cargo capability it opened up tons of routes for many airlines. E.g. to/from China and Middle East.

Since then traffic has grown fast / the dots have been connected, reducing the need for this payload-range combination & hundreds are still around.

https://worldairlinenews.com/2015/04/29/hainan-airlines-starts-chongqing-rome-flights/

Hi Born, before I jump of the cliff or burning candles for the 338. Would really like to see similar comparison between the 788 and 338, guess its not political correct.

Then such a comparison between the 788 and 789 will be very informative.

Hello Bjorn

So on a 4500 Nm fuel burn per trip of the NEO vs the CEO is only 9%?

You compare with the last breed of 242t capable CEO with Pip’ed T700 and short flap fairing is that is that it?

Bonne journée

Stand to be corrected but on sectors less than 3000Nm things are getting real close?

Just looked at some data for ~4500Nm sectors. The 787-8 has 15% higher seat mile fuel burn than a 787-9 and the 787-8 and 330-800 (both ~245 pax) basically the same seat mile fuel consumption. So the 330-800 is not such a dog!

The drive is for increased range but what will be the airport savings be on a 338 variant with say 230T MTOW, reduced MLW and de-rated thrust (67KLb?). Got NO clue what the criteria and/or hurdle numbers are that could change the aircraft’s “airport operating costs”.

Range should still be around 6000Nm which is more than enough for most applications, especially in the East which is a major 330-200 stronghold which AB should endeavour not to lose.

Where did you get the data?

@Geo:

“Where did you get the data?”

And we get dead silence fm Anton re your question….despite probably 33% of all replies/comments here are fm him.

I assume your query included data which lead to Anton’s claims such as:

“787-8 and 330-800 (both ~245 pax) basically the same seat mile fuel consumption.”

I wouldn’t worry too much about his data. He probably even failed to realize official load per pax+bag assumptions are diff between Boeing and Airbus which obviously affect fuel burn per seat even if Boeing & Airbus produce exactly the same aircraft type.

Please see attached link.

https://en.wikipedia.org/wiki/Fuel_economy_in_aircraft

@Anton:

There are so many inconsistencies(not surprising due to mixing diff source references and calculation assumptions together) and even basic errors among data found in yr weblink that I don’t even know fm where to start to explain the problems with your source(often typical with wiki) and with using it to do any aircraft type comparison.

For yr benefit, I give U 4 obvious examples which U should hv noticed b4 sharing it here:

1. How can 1st flight for 339/338 be 2016/2017 when it was/is not even built yet?

2. Data for this pair of 330Neo are @ best just estimates @ this stage whereas data for other types look like actual op data(e.g. real airline seat counts).

3. Just notionally, any reasonable observer would hv detected data are not comparable with each other when a 380 with 544seats burn MORE fuel per seat than a 772ER with 301seats over the same 6,000nm sector.

4. Even more funny is that U get 2 fuel burn per seat figures for the same 772ER with the same 301seats over the same 6,000nm sector.

So I noticed, understand a bit more of why LCC’s land where they do.

https://a4e.eu/wp-content/uploads/2015/02/AvEc-Airport-Charge-Analysis-v1.5.pdf

Never saw that wiki.

https://en.wikipedia.org/wiki/Fuel_economy_in_aircraft

While many assumptions have to be made, that can all be discussed some-one did his best to be objective & provide insights. Respect.

@Anton:

“787-8 and 330-800 (both ~245 pax) basically the same seat mile fuel consumption.”

I hv a little doubt about that especially when no data source is cited by U. Fm what I hv read so far, the 788 is @ least a little bit more fuel efficient per seat than 338.

“..what will be the airport savings be on a 338 variant with say 230T MTOW…”

Wouldn’t it be depending on which airport and its landing fee structure? But a bigger question for U to think thru before yr question is:

Wouldn’t whatever savings for a 338 variant @ 230t MTOW be the same for a 339 variant also @ 230t MTOW?(In fact, whatever aircraft type @ 230t MTOW)

“…reduced MLW..”

Which I hv never heard of as a basis to calculate landing fee @ any airport. Pls educate me on this new airport charge scheme…

“…and de-rated thrust”

Which again has nothing to do with calculating landing/airport fee. The only benefits fm a de-rated engine are typically only:

a) Lower acquisition cost(i.e. manufacturer willing to sell @ lower price than for the highest rated version)

b) A bit lower maintenance cost due to less wear & tear @ artificially reduced engine ‘redline’.

“Range should still be around 6000Nm.”

Which is practically what the 333 @ 242t MTOW already offers for only 2% higher fuel burn per seat than 338 according to Bjorn’s model explained in his story.

“…which is more than enough for most applications.”

Probably true for many 330 operators and the reason why they chose the easy way by simply ordering more 333 instead of the hard way of ordering a de-rated 338 to maximize RoI such as:

a) Acquisition cost=

333 cheaper for Airbus+RR to build/customer to buy than any 338.

b) Seat rev$ opportunity+flexibility per Bjorn’s cabin config model=

No more than 250pax on a 338 but 333 can carry either 250pax, 290pax or any number in-between.

c) Max available belly cargo space after deducting crew rest compartment pretty much mandatory for any mission beyond 4,500nm(let alone 6,000nm)=

LD3 x23 for 338 vs x28 for 333.

“especially in the East”

Where below deck belly cargo traffic has been growing as fast as or faster than above deck pax traffic for widebody operators thx to unique geog unlike N.America and Europe where long-range cargo transport by rail/highway is practical.

“which is a major 330-200 stronghold”

But still absolutely pale against the 333 fleet size this region already has and still continuing to order(but no new 332 ordered for yrs).

“which AB should endeavour not to lose.”

And has been @ least partially successful in retaining thru many 330 operators there upgauging fm 332 to 333 over the past 10yrs.

Overall, a de-rated 338 sounds like a solution looking for a problem….

FLX you mentioned a week or so that thrust de-rating is done do lower airport charges and has no impact on fuel consumption, has things changed.

See landing fees are based on aircraft’s MGLW and parking fees on MGTOW, could find nothing on thrust.

@Anton:

“…you mentioned…that thrust de-rating is done do lower airport charges….has things changed.”

Nothing has changed including U continue to mis-interpret others’ comments/explanations or take them out of context. The followings are the summary of what i said in whole re thrust de-rating of engine:

1. Lower landing fee comes fm lower MTOW(or de-rated MTOW).

2. With a lower MTOW & reduced performance requirement, no need for the original max thrust level.

3. Engine can be de-rated in such case.

“See landing fees are based on aircraft’s MGLW and parking fees on MGTOW…”

“See” where?

For 18″ seats at long range, the A338 could have a place. If it is cheaper to fly 200 seats on an A338 than an A359 at 5,500 or 6,000 nm, then the A338 is the most economical small seating option at long range. Unless a 788 with 8 abreast economy has better economics. The production cost would be more for the 788?

What’s the runway performance of the A338 versus A339? Does that make a difference at Maui?

I think the a330-mrtt will eventually – and maybe soon – be an a330-800 derived aircraft, making an already worthy derivative even better.

If AB didn’t do the 800 – they’d limit themselves going forward in terms of platform flexibility.

I don’t think the 800 will be flying with airlines – but better to have it designed and developed and ‘ready’ along with the 900s development, than have to ramp-up R&D at some future point. Doesn’t matter hugely to AB as it’s the same production lines/equipment… and who knows what the future holds and what will be required in the future.

List price for the -800 is 254.8 against 290.6 Mio $ for the -900. If the same discounts apply for both models, there will still be quite a difference between the two in net pricing. I would think that the price difference is significantly larger than the difference in production cost. So if I was on Airbus sales team I would surely not push the -800 to much.

On the other hand, if an airline has serious doubts about getting all the -900 filled, they would certainly consider getting a few -800s in their fleet. Or if you have to replace some 767s that are hardly filled…

Airbus needs the -800 anyway (tanker, freighter,..), and when slots become available and no other 767 replacement comes up over the next couple years, I would expect that it will still sell.

In case the A330 production will not be booked that well, maybe Airbus has still some leeway in the pricing for the -800 they will then use in contest with the 789 say in 3-5 years?

Those list prices are correct but seems AB doesn’t want to sell NEO’s?

The list price of the 359 is $311M and the 787-9 $264M, why should you buy a 339 at $291M?

At these list prices the 787-9’s are the cheapest seats you buy, no wonder they are selling (~$920K/seat) while the AB’s ~$1M per seat.

Airbus’ and Boeings list prices can’t be compared directly. Airbus’ list prices includes fully furnished cabins, while Boeings prices only includes a barebones aircraft.

Both OEMs gives significant discounts.

Thanks Meg, now things start to add up.

@Anton:

Yes, they “start to add up” only if U believe cabin furnishings are worth $27m per 789 when one whole CS1 airliner is only $19.6m for DL to buy according to Boeing….

Even if a 789 including cabin is listed @ the same price as a 339, which 1 will U insist for a steeper discount % @ yr local Airbus or Boeing dealership?

@Meg:

“Airbus’ list prices includes fully furnished cabins, while Boeings prices only includes a barebones aircraft.”

1st of all, how do U know? I can make the same argument in reverse….

2ndly, “includes fully furnished cabins”, so a 359 cost only 6.9% more than a 339?……Come on.

“Both OEMs gives significant discounts.”

That’t true and basically commercial aerospace 101 level knowledge.

What’s lesser known is that a higher than reasonable list price is a good platform to ‘pump-up’ total transaction value in trade deals reported by general media worldwide. This delivers a significantly higher PR value in diplomatic/political arenas for consumption by the relevant public/citizens/voters….

Think its the price of the Tent7000’s that’s killing the 330NEO’s. RR wants to recover their costs on a projected small volume of sales?

Trent7000 “list price” $38M each while the T700’s $23M.

Anton, production cost of the 338 is certainly a lot lower than the 789 and the price of the RR7000 identical or at least very close to the 1000 of the 787.

Airlines know that, so maybe they just wait until Airbus feels to pressure to discount the 338 further once the pile of existing orders is shrinking?

@Gundolf:

“..List price for the -800 is 254.8 against 290.6 Mio $ for the -900….price difference is significantly larger than the difference in production cost.”

Totally agreed and normal for commercial aerospace industry i.e. pricing is rarely cost+ but rather based on value to customer/buyer.

“…if an airline has serious doubts about getting all the -900 filled…”

With 200+ frames on the firm backlog, airlines/lessors interested in 330Neo seem to hv little or no doubt re such scenario. At the minimum, they seem to be ok with filling only 250pax, equal to max capacity on a 338, on a 290 seat bird….

“…they would certainly consider getting a few -800s in their fleet.”

But aside fm HA(In which their CEO is clearly doubting 338 in the media last wk) and certainly considerations hv been done, why none is getting any? It’s rhetorical question in which I think Bjorn has done an excellent job answering…..

“Or if you have to replace some 767s that are hardly filled…”

In such scenario, U likely don’t hv a viable mkt/route for a widebody in the 1st place and replacing 763ER with an even larger 338 doesn’t seem logical if the goal is to reverse the load factor situation.

“Airbus needs the -800….and when slots become available…”

What are U talking about? There’s no shortage of near term 330Neo production slot and the 338 and 339 share the same output capacity. The shortage is in customers committing to take those slots.

By far the largest customer for 330Neo is AirAsiaX. Do U know that their delivery schedule stretches all the way to @ least 2025/26?….meaning AirAsiaX will take an avg of well below nine 339 per yr when the 330 assembly line is now geared for 84 per yr.

“…no other 767 replacement comes up over the next couple years, I would expect that it will still sell.”

Even if Boeing committed to launch 797 yesterday, all 767 operators clearly understood 1st delivery won’t occur until 2024 @ the earliest. This is not some new discovery but a common industry knowledge since BEFORE 338 was launched in Jul2014.

So why they did not ordered 338 to replace 767 for the past 3.5yrs but suddenly decide they should “over the next couple years”? Objectively, 330Neo is not such an unknown+high development risk type(not even a heavily upgraded variant unlike 77X..) in which airline must take a wait & see attitude b4 ordering.

“…maybe Airbus has still some leeway in the pricing for the -800 they will then use in contest with the 789 say in 3-5 years?”

1st of all, putting 338 in the same sales contest against 789 is akin to putting 788 in the same sales contest against 359……not really comparable in size and lift capability.

2ndly, even if such contest makes sense, why wait 3~5yrs? If Airbus has the so-called “leeway in the pricing”(I don’t doubt that since the basic 330 platform R&D investment must hv been fully amortized nearly a decade ago), they would hv used it in sales campaign against 787 since Jul2014.

Some may argue T7000 cost may go down in a few yrs along with pricing. However, 787 would enjoy similar advantage since T1000 is extremely similar to T7000(except bleedair system) but has been in production for 6yrs longer.

After all of that, with what must an airline operating a mixed fleet of 330-200/300’s replace their 330-200’s with?

Trouble is the 800 is too much airplane now. It would probably be okay if the freight market was ok, the extra non pax MLW would have value, but that doesn’t look like happening. Still you have to expect some deals to be in the pipe somewhere, it still is costing AB money to build and certify.

On a 4500Nm sector it seems to have very similar sector fuel burn as the 787-8, and the pax get 2-4-2.

True in many aspects. Why buy a 4×4, you can do 99.9% with a 2×4.

I have been in this too many times, its that 50m that you can’t cross that spoils a perfect trip and cost you dearly at the end of the day.

Would love to be a fly on the wall on Boeing sales people training/briefings, they surely good at it.

AB should sharpen up on this, pilots and engineers should be identified to do the selling, accountants and lawyers to sort out the paper work.

If a guy in a pin striped suit and Rolex try to sell me a 400T haul truck he has a hope as big as snowball in hell.

If the A330-900 is increasing in range should not the A330-800 follow suit?

Same wing.

Back in 2014 LNR did analysis of 338 and 339

Worth looking at it again

https://leehamnews.com/2014/07/14/airbus-a330-800-and-900neo-first-analysis/

https://leehamnews.com/2014/09/06/final-a330neo-analysis-cabin-improvements-gives-the-a330neo-gains-over-todays-a330/

https://leehamnews.com/2014/07/17/airbus-a330-800-and-900neo-first-analysis-part-3-performance/

Thanks, good to re-cap. Seat-mile costs very much a function of airline layouts.

The 2-2-2 in business not bad, don’t know why airlines pushing 1-2-1’s on medium haul (<12 hours). 2-3-2's in E+ most likely better returns on floor space?

On the 787's and 350's Y's, millions must have gone into the research for going 3-3-3. But 2-5-2 in my eyes not a bad option. Only one "real" middle seat, you can borrow some inches from the 2×2 on the side to add an inch or two to the middle seat of the 2-5-2.

If they fill the plane effectively you can land up with a real world 2-4-2 in many instances. With 3-3-3 its often messy, especially traveling with a family.

Bjorn,

I thought the range for the 251t A330-800 would be around 8200nm. That is significantly different than the 7800nm mentioned. So which one is it?

If it is indeed 8200nm, that might change things a bit. That would be the ultimate aircraft for ultra-long and thin missions and at an attractive price.

There will be nothing like it and I for one remain very intrigued by this “niche” plane.

Airbus is building it so they probably expect sales of more than 6.

My thoughts as well as any increase in 900 should be reflected in the 800 or more.

I think some airlines should have to orders A330-800neo. There are only Hawaiian Air who already orders A330-800neo. I think they should have orders more A330-800neo or A330-900neo. UA or AA hasn’t orders A330neo yet. What about JetBlue? They haven’t decide to orders A330neo yet.

Just a few notes comparing the 787’s and 330/NEO’s

Lets see what the fuel burn of the NEO’s are after the test flying.

The only reason the 787’s having better projected seat mile cost then the NEO’s is because airlines are cramping pax into the 787’s uncomfortable 3-3-3. Fly the 787’s at 2-4-2 in Economy at it could be a different picture.

Fly the 338 in 3-3-3 (16.5″ seats) as AirAsiaX does with their 330’s and see which of the 338 or 787-8 have the best seat mile cost.

I will pay with a smile 10-15% more for me and the family in the back of a 330 than flying in a 787 at the back.

Trump Boeing’s best salesman? Big Boeing order from China but no 330NEO’s!

They did order 350’s recently but the 787-9 (and lack of 350-800) are starting to hurt badly. Someone at AB must start to wake-up!

See link.

http://c.newsnow.co.uk/A/909971995?-303:3665:3

“Chinese airlines” operates operate around A330’s, non of them has placed an order for the NEO so far?

No, they didn’t orders A330neo yet. They haven’t talks with Airbus yet. I think they should orders A330neo for Chinese airlines. That’s important.

I see something similar happening for the B777-X. Not this drammatic because the -8 is selling, but roughtly a fifth of the bigger -9.