Leeham News and Analysis

There's more to real news than a news release.

Delta Airbus deal means Bombardier trade complaint continues

![]() Dec. 13, 2017, © Leeham Co.: Delta Air Lines chose to place its long-awaited order for the re-engined single-aisle airplanes with Airbus for the A321neo, powered by Pratt & Whitney GTF engines, according to an exclusive report from CNN’s Jon Ostrower.

Dec. 13, 2017, © Leeham Co.: Delta Air Lines chose to place its long-awaited order for the re-engined single-aisle airplanes with Airbus for the A321neo, powered by Pratt & Whitney GTF engines, according to an exclusive report from CNN’s Jon Ostrower.

The Delta Board of Directors was expected to decide today, announcing its decision either today or tomorrow at the investors’ day event.

If confirmed, the deal is a major loss for Boeing, which hoped to sell the 737-10 MAX to Delta. A win would have been a huge boost for the MAX 10.

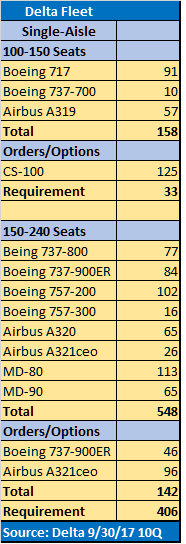

Click on image for a crisp view.

This means there was no deal for Boeing to drop its trade complaint against Bombardier for the Delta C Series order, something that was speculated might have been a quid-pro-quo, but which is unknown (outside the parties, at least) if an offer or demand was ever on the table.

Updated: Delta’s order for 100 plus options for 100 airplanes takes care of about half its future single-aisle fleet requirements.The current order backlog, at Sept. 30, left a need for 406 single-aisles; the neo order covers about half of this. This presents a future opporunity for Boeing to make a new proposal.

At the end of the 9/30 third quarter, Delta had 46 737-900ERs and 96 A321ceos on order, or 142 aircraft. It also has 75+50 Bombardier CS100s under “Commitment.”

At the end of the same period, Delta’s aging fleet is outlined is the chart.

The deal for 100+100 leaves a need for just 28 single-aisle aircraft in the 150-240 seat category. Clearly, the winner of this deal will be in an advantageous position for these.

Related stories:

In Delta Airlines decision matrix for aircraft selection, I’d guess that they weighted the impact of Delta TechOps doing maintenance and repairs on the PW1100G-JM and PW1500G engines, for the North American market, at their technical and operations centre facilities in Atlanta.

Why does the table omit the MD-88 and -90 fleets? The seat capacity groupings seem unusual as well.

Lists are the bane of my existence. This chart has been corrected and text update.

Eager to see the 320/321 mix, and if it is all neo.

(I can’t imagine any need for 319s)

RaflW:

“Eager to see the 320/321 mix”

What do U mean? DL hv been operating 320Ceo since NW merger and 321Ceo for the past 18mths.

That “mix” already exists in DL fleet.

I meant the mix in the order for 100 new frames + 100 options (options are often more opaque, though)

Scott lays out the need, but how DL fills it is of interest, especially since the Cs100 deal is in limbo, how will the MD88s be retired? With 320sneos?

I am hopeful for a large 321neo order to (eventually) replace the 757s.

The mix will be interesting, there is a”huge” gap between the CS100 and 321’s. Still think DAL is dangling a carrot of some sorts to BA?

The 737-800 are brand new by Delta standards. The A320s are older. I doubt much movement here for a long time – my bet would be that they might pick up a few used frames that come off lease somewhere in the world.

I assume there is a promise that all will be built in Alabama? AND maybe an acceleration of the C Series line next door? Airbus needs to accelerate the capacity of US assembly to meet demands of made in US.

Scott,

I dont’t follow your math, how did you arrive with (source is wikipedia):

109 MD-88 + 100 757-200 =209

Already orderd: 92 A321ceos and 43 737-900ER = 135

leaves: a requirement of 74 vs. 100 ordered.

So the story could be that 24 are for 767 replacement, or the or the 62 MD-90s are also on their way out.

How did you arrive at a requirement of 228 frames?

Klaus

The list initially overlooked MD-80s and MD-90s, and this has been corrected and updated. The list is only single-aisles and orders vs in-service is the math.

The 767s are being replaced by A330s and A350s. It’s also a twin-aisle. Not relevant this is discussion.

If this deal is confirmed, I think the “797” will come sooner!

I mean, the decision to launch it…

Well the A320NEO for sure lit a fire under Boeing last time.

You bet!

Even if they do launch it, it is years away from flying. During all that time Airbus will be saying to customers, “wanna try, buy and fly one of our ‘planes?”, whilst Boeing will be saying “look at these marvelous pictures”.

And of course there’s every possibility that Airbus will launch something of their own… And do a C500. And bring the C300 to the wider market.

People going on about slots for 320/1’s. The MAX10’s still needs to fly and get certified, when will they come of the production line?

Soon, very soon (2020 I think)

How much better can the 797 be then an A322? And how soon can it come? Some major 20-30 year decisions have been made. I am not surprised by this one bit. A321 is a superior product to 10 MAX, no question there at all. 8 max can compete with 320, slightly better efficiency and better packaging…maybe higher efficiency in the latest high density config.

To beat a A322 with new CFRP wingbox and wing with a small widebody you need to go up in size and range approx 33%. The body can be of Al-Li friction stirr welded hence almost no rivet joints, the body must probably be a bit like the D8 with trusses thru the mid body to get mass down and a full fly by wire system that is smarter and can optimally use satellite weather information and with everybody having ADB-S out also use ADB-S in fly paths that causes minimum noice at ground and minimum fuel also close to airports. It can have a fuel cell APU that drives a tail duoprop in cruise just to energize the boundary layer and reduce drag. It can maybe be FAA certified with only one pilot in the cockpit as the other one is in Boeings computers flying optimal and per the book. It will not be cheaper aircraft but a much more productive and Boeing can have a steep price increase as you get outside the A322 capabilities.

Well so much for a Boeing preference due to the Seattle Hub!

Not to mention C Series deals.

That should silence more than a few P&W critics as well.

Delta like the engine!

Well that and Airbus can proposes the C500.

That should take care of the other half.

Think AB is waiting for BA to commit to the 797. Then they could go for an CS500/320+/322 which will spell the end of the road for the 737’s?

I think it will all come down to investment cash power!

and, That will only happen if they crank up 320 production, Mobile could actually be an important part of the AB story.

but, but, but FCF!!!

crank up.

A320 : 8/m is ~~ the limit.

That’s a big concern. It could be one of the big drivers for AB to buy into the CS program.

If/when the deal is concluded AB-CS could offer airlines conversions to the CS300 and/or hypothetical CS500 that will take pressure of the A320 production line/s.

Anton:

“…which will spell the end of the road for the 737’s?”

Will make U really really happy if no more 737 is produced…I suppose.

However in reality outside your dreamland, carriers like Southwest, Westjet, AS, UA, FR, Norwegian, Lion Group, etc. will continue to take 737Max deliveries and likely order more for yrs to come….not really because they like 737 more than 320 but because they won’t abandon their huge 737 pilot pools+MRO support regimes that easily.

Agree, I think the MAX8 could still be in production in 20 years from now. But other than that?

If the 763-Revive comes of do they still need an NMA in the short term? Those frames have long lives ~25+ years, sure GE could come up with a “new” engine that could be offered a retrofit for newly build 763’s.

From a Boeing point I would say building an “NSA” of MAX10/757 size with EIS around 2025 should be the priority.

They can’t and won’t take over the whole single aisle market because the 37 isn’t that bad and no airline wants the duopoly to become a monopoly with the pricing power that brings.

Maybe this will encourage B to move on the “97” and a 37 replacement sooner rather than later which we airplane enthusiasts would enjoy.

Whatever happens, stock market investors remain happy (enthralled?) with B which keeps the management in the money.

If no Airline wanted it to become a monopoly, then they would order split fleets to ensure that.

Kind of like saying they don’t want Boeing to have the whole 787 market are so they buy A330s, but they don’t.

Kind of a tofu phrase, it looks like it has substance but their is nothing but air there.

If we could have some kind of data you think backs that up?

This is an ‘America 1st decision by Delta.

The A321Neo will be built in the US and the engines are manufactured by Pratt & Whitney, a 100% owned and operated US company.

If Delta chosen the Boeing 737 Max the engines would have been supplied by CFM which is 50% French owned.

Pratt and Whitney may be a US company, but the GTF is shared with its foreign partners just like CFM:

MTU

Mitsubishi

GKN

Avio (Italian but now owned by GE)

@dukeofurl:

“Pratt and Whitney may be a US company, but the GTF is shared with its foreign partners just like CFM:”

Boeing may be a US company, but the 787 program is risk-shared with its foreign partners…

BBD may be a Canadian company, but the CSeries program is risk-shared with its foreign partners…

The list goes on and on in today’s highly globalized programs and supply chains…

That’s why I firmly believe patriotic chants like we should support Airbus because it’s European or support Boeing because it’s American didn’t make sense over a decade ago and is total nonsense today.

Totally agree!

But it seems not enough people listen to the voices of reason.

I never got the jingoistic angle in the first place but agree

@TransWorld:

“so much for a Boeing preference due to the Seattle Hub!”

I always believe that’s a relatively weak factor for the decision in terms of local consumer preference ever since AS merged with VX and inherited 320 family(and still taking deliveries of leased frames).

It’s a fact that both DL and AS Group hubbed in SEA will operate both 737 and 320 families.

Air France operates more Boeing wide bodies that Airbus twin-aisles. They also have an aging fleet of 32X’s but has place no replacement orders?

@Anton:

“Air France operates….They also have an aging fleet of 32X’s but has place no replacement orders?”

Take a wild guess why…..or actually read more about AF financial performance/status for the past 10~15yrs.

But hey, say bonjour to Joon!

There’s no way to divorce this decision from Boeing’s absurb targeting of the Delta C-Series deal. Heads need to roll at Boeing, starting at the top.

I think your judgement on the reason for Delta’s decision, if confirmed, is correct.

Agreed, but if the short term profits / share price remain good, there’s no immediate pressure from investors for changes at the top. No other measure matters.

And by the time the consequences of all this do start filtering through to the company profit, the root cause might get lost in a flurry of new product launches promising “jam tomorrow”. Again.

Or that Delta is just using Boeing as a ploy for good prices on A321 anyway?

They did that with the A330/350 order.

Not that I don’t think its a great yank on Boeings beard, but it may very well have gone that way, the A321 is simply superior to anything Boeing offers in that category.

Whom will Boeing sue now?

It looks like Delta snookered Boeing into thinking they had a shot once again and then left them high and dry.

Given what’s gone on in recent times, I do wonder if there is someone in Delta experiencing visceral pleasure at the mere thought of making an announcement in the immediate future. We shall see.

That’s quite important; if someone who matters in Delta is so cross with Boeing that they’re positively relishing the prospect of announcing “I’ve bought Airbus products”, how on earth are Boeing’s sales force ever supposed to overcome that? I know that the people who make these kinds of deals are hard headed business practitioners first, humans second, but it’s another hurdle for them to surmount. Selling 737 to Delta was always going to be hard, but right now it seems impossible.

Not a good place to be in; one American company so annoyed with another American company that they’d rather buy European.

No, it’s all the more reason for BA to lean Alaska’s way going forward. Tilden’s reaffirmed Alaska’s “Proudly All Boeing.” (Still working on dumping VA’s leased Airbuses.) Delta’s gonna find it’s name’s mud in Seattle! LOL

Maybe not, BA doing WA state no favors.

“Proudly all Boeing” sounds good in the domestic market, but doesn’t look so great if it turns out that all your competitors are making more money because they’re running a more efficient / comfortable and popular with passengers / re-sellable aircraft.

Whether or not that ends up happening is yet to be measured of course, but on at least 2 of those criteria the 737MAX is probably not ahead of the the Airbus.

@Matthew:

“Proudly all Boeing” sounds good in the domestic market”

Which is a slogan used only by AS which is fine because AS is 99% about domestic mkt.

“…doesn’t look so great if it turns out that all your competitors are making more money because they’re running a more efficient / comfortable and popular with passengers / re-sellable aircraft. Whether or not that ends up happening is yet to be measured of course, ”

Nearly 3 decades of 737 family and 320 family co-existence plus mkt dominance over any other narrowbody family(including CSeries recently) in airline ops worldwide has pretty much proven that it has not turned out as U described.

Therefore, such slogan still look fine(if not great) @ least for some 737 operators.

“on at least 2 of those criteria the 737MAX is probably not ahead of the the Airbus.”

Which 2?

If for the comfort and popularity criteria, they are among the least important factors in a list of probably 500 factors for airline boards to decide which 1 is ahead of which 1 for investing in….

If Jetblue offers pax a 50% cheaper fair from Alaska to X in a A320 (32″ pitch) will they say no because its not a Boeing?

“Delta’s gonna find it’s name’s mud in Seattle! ”

I don’t think Microsoft or the other tech companies care about the Boeing-Airbus fight. They want a solid airline to serve their businesses. Actually, they probably want this Alaska-Delta situation to continue so they have market forces giving them choice and competition.

Ryanair has a fleet of ~410 B738’s and another 180 Boeing’s on order.

If Alaska want to ditch their inherited 321’s an compete with their -900ER’s and MAX9’s good luck to them.

KLM and Transavia operates 737’s only, they also haven’t placed new orders.

Think the LLC’s are giving KLM and AF uphill in the “domestic” market. Don’t know what is happening with Alitalia, but the legacy airline IAG, KLM-AF, LH that could take it over will be the strongest in Europe?

@Anton:

“If Alaska want to ditch their inherited 321’s…”

They probably wanted to before but decided a while ago to keep all deliveries intact. 320 family can’t leave AS fleet until 2024 earliest per AS statement.

“….an compete with their -900ER’s and MAX9’s good luck to them”

Why? Also, what will be the problem for AS to adopt Max10 instead of 321Neo?

Why do you want a MAX10 if you can have a 321N (assuming same price), fleet commonalties however a major consideration.

The MAX10 can work depending on the airport and/or time of the day, but I don’t want to be in fully loaded one if it loses an engine a few seconds after take-off. It happened twice with me in 737-800’s, it was okay but not ideal.

@Anton:

“Why do you want a MAX10 if you can have a 321N..”

Equally good question in reverse. Why do U want a 321Neo if you can have a Max10?

“I don’t want to be in fully loaded one if it loses an engine a few seconds after take-off.”

So U want to be in a fully loaded 321Neo if it loses an engine a few secs after take-off?

Your justification for X over Y is weird because for me, I would neither want to be in a Max10 nor 321Neo in such scenario….they are equal in that perspective…and in so many others.

“It happened twice with me in 737-800’s…”

And I can claim it happened 20x with me in 321Ceo and we can play this game all day long…..pointless but pls, bring it on if U wish.

Because you can hang 33 Klb GTF engines on the A321 wing.

I gesso its forgotten that Alaska had an MD fleet at one time!

Alaska cannot ditch their A321s.

There is a solid lease agreement in place.

They have them for 8 years as I recall.

That gives AK plenty of time to assess and see how they work and fit in.

Yea the PR about All Boeing is nice and catchy and warm and fuzzy.

How do you think Boeing workers feel about Boeing these days let alone suppliers that are getting their contacts beat up to allow Boeing to make more money ( and then spend 18 billion in share buyback?)

@MontanaOsprey:

“Alaska’s “Proudly All Boeing.”

Which will become a lie immediately after 25Apr2018 when all VX flights operated by 320 family will become AS coded flights(not even codeshare) on alaska.com

“Delta’s gonna find it’s name’s mud in Seattle!”

Will be really funny to watch the reaction fm AS pax based in Seattle who really think that way about DL and assumed AS is all-Boeing when they broad an AS flight @ SEA operated by a 320 family after Spring 2018….

People will fly on whatever is low cost, has the right connection etc.

If you believe Delta has slapped Boeing in the face, how would you describe the Emirates Airlines move at the airshow last month when announcing the Boeing order?

Or how do you think Airbus felt in the 80s and 90s trying to sell their products to US based Airlines?

I’m absolutely shocke…….actually, I’m not. Predicted it when you announced the RFP. The pro-Airbus regime is fully in charge, and I’m sure the C-Series complaint was the final nail in the coffin. I don’t know why they had it “in” for the C-Series, which is a beautiful piece of gear, and why Boeing, when they had the chance, didn’t snap it up when Bombardier offered it to them (dummies). Boeing should by now realize that they are fighting an uphill battle at Delta, so submitting any bid with the current culture in place is really wasting their time.

Not saying the A321Neo isn’t the best choice for Delta, but, given Richard Anderson’s history of digging in on Boeing only to select Airbus, his disdain for Ex-I’m (and the attendant effects on Boeing), it was all too obvious this was going Airbus’ way.

Don’t know how Boeing can dig themselves out of the hole on this one.

The only way is to produce a wonderful 797 and, when Delta begs for discounts, does not grant them and still put them at the end of the shopping queue. These things are cyclical and they will turn around sooner or later.

People seem to forget that DL ordered 100 737-900ERs under Anderson. DL likes dual sourcing. Boeing could well have another opportunity in the future.

Mr. Hamilton,

I remember that, but I think the C-Series debacle has put any Boeing aspirations at Delta in Antarctic ice.

This makes the selection, if true, even more intriguing. Within the last few years DL has ordered nothing but Airbuses, I think at this juncture Boeing will likely treat future RFPs from DL as just a way to get more out of Airbus and be less price competitive. The 739 order was also partly financed as we learned by those 787 deposits. Likewise they seem to be straying from CFM with both CS and A321neos so I’m sure CFM is not too pleased either. I think this entrenched feelings on both sides which ultimately is at odds with DLs fleet strategy, unless they plan to buy used for a long time. Good luck to them in their fight against EK, QR and others, I don’t think the decision will sit well with Trump since the oppposition are major Boeing customers. United now holds the most sway and they haven’t ventured into that spat as much as DL.

Maybe its DAL’s experience with the -900ER’s that contributed to their decision?

@Anton:

“Maybe its DAL’s experience with the -900ER’s that contributed to their decision?”

By the same logic as yours:

May be it’s SilkAir’s experience with the 320Ceo that contributed to their decision to go Max8 as replacement?

May be it’s AC’s experience with the 321Ceo that contributed to their decision to go Max9 as replacement?

As I said, think the MAX8 a better call than the 320N.

@Anton:

“As I said, think the MAX8 a better call than the 320N.”

Still does not explain AC’s case.

That was suspicious, close to dumping prices I guess? A359’s and 321’s would have fitted in with their requirements.

“People seem to forget that DL ordered 100 737-900ERs under Anderson. DL likes dual sourcing. Boeing could well have another opportunity in the future.”

Scott,

Not a clue why the 900 seemed to suit Delta, maybe it was purely pricing.

That said my take is that Delta loves having Boeing as a price foil and they will get taken again down the road.

Boeing doesn’t have anything Delta has to have.

NMA may be a different story but they don’t have it yet.

I personally believe that beyond the fact that the 900ER fits parts of Delta’s network well (and it is a nice ride, to be honest), the biggest reasons why Delta bought the plane are:

1. To get out of buying the 787

2. To dampen the hypocrisy of Richard Anderson’s attack on Boeing and Ex-I’m by saying (which he did, BTW) that “Delta supports American workers….in fact, we have ordered 100 American-made jets”. He made that EXACT ARGUMENT before Congressional hearings on Ex-Im when he was trying his best to kill it. Anyone who doesn’t pay attention will know that, at that time, he had already snipered the 787 (and made disparaging remarks about the -9 and -10, calling them “experimental airplanes), and bought the A330, and ordered the A330NEO (which, by the time he would get it, would be more “experimental” than any 787) and A350 (itself BARELY flying).

Anderson had no intention of buying Boeing products. Ever. And his installed leadership aren’t deviating from that script. It’s looking more and more like they bought the 900ER to get the heat off his (Anderson’s) and Delta’s back while he lobbied to gut Boeing on the Ex-Im issue. And now the C-Series complaint gives them more than enough cover to continue to throw knives at Boeing.

Hopefully, he can make his Mussolini-like outbursts again but better directed at Amtrak employees and its suppliers, and, wait for it, “Make the trains run on time!” LOL

The MAX10 is not better that the 321N, on the other side I think the MAX8 is better that the 320N. Depends on DL’s fleet requirements first?

@Anton:

“MAX10 is not better that the 321N…

…MAX8 is better that the 320N”

Pls define “better”. More importantly, for every operator on earth or for some?

Horses for courses.

Blaming the CSeries blocking could be a kind of comforting. But it’s hard to find a MAX-10 USP for Delta. Or any other carrier. Reality is kicking in again.

Lost in Scott’s flowing prose previously was what I thought was a very pertinent comment. The efficiency of the NEO vs the MAX was too close to call using the LEAP. Factor in the GTF and things change.

To me the big win is with P&W. By all accounts it will be the engine of choice going forward offering better efficiency and critically more scope for future gains.

I see AB gaining massively due to this with the MAX fatally flawed by, yes you guessed it, it’s short undercarriage which limits it to the LEAP. A less efficient version at that.

Apparently there are 2nd generation PW-GTF’s for the NEO’s in the pipeline that will have improved reliability and around 2% better fuel economy, it all adds up.

@Anton:

“Apparently…it all adds up.”

And apparently, only the Neo program will get it(because it’s sacred Airbus) but none of the other programs also using PW1000G will get it. May be E2Jet will also get it too because U like EJets.

Also apparently, there’s nothing similar in the pipeline fm the LEAP family because CFM decided to just sit on their hands and do nothing to counter PW1000G.

@FLX

Actually, all other P&W programs can avail of it.

https://www.flightglobal.com/news/articles/pratt-plans-performance-upgrade-for-a320neo-engine-396062/

Available to all.

RE. LEAP improvements.

CFM have a much tougher time finding efficiency improvements due to their design relying more on the extreme optimisation of materials and current design.

The GTF is a paradigm shift in architecture, one which the LEAP is ill-equipped to counter in performance – but *may* beat in reliability.

The A321 has sufficient ground clearance in order to put 35,000 lbs thrust, Rolls Royce UltraFan engines, with a fan diameter of 90″ and a bypass ratio of 15;:1, on a next generation A321neo, from the middle of the next decade. TSFC should be around 15 percent lower than the current Leap-1A and the PW-1100G engines.

The fact of the matter is that the 737MAX is just about maxed out. I’ve hard time seeing that sans a complete re-design, the MAX being able to be outfitted with UltraFan-type engines that have bypass ratios significantly increased over that of the current crop of engines.

unlikely that you are going to see 15% sfc gains from the Ultrafan over the GTF, as the UF is not architecturally much different. the

PW, during that same time period will improve their core (which is currently pretty low stress & tech compared to LEAP) with low risk/high reward tech insertions, have 10 years of in service experience with the gearbox to refine performance and reliability…

PW is putting a lot of money into their next gen gearbox (4:1 ratio) which will be optimized for larger diameter fans…

Well, I said the current crop of engines. Of course, Pratt will improve their GTFs over time. However, the Ultrafan engine will have at least a 70:1 overall pressure ratio vs. 50:1 for the PW-1100G, a bypass ratio of 15:1 vs. 12:1 for the PW-1100G, and a gear speed reduction of 4:1 vs. 3:1. A response from P&W would essentially require a new engine.

I think you are optimistic in your projections regarding UF.

even the very largest most modern engines coming out over the next few years (GE9x) are only at ~60 pressure ratio, and the smaller the engine, the harder it is to increase pressure ratios due to higher % pressure losses due leakage and aero efficiency (blade tip gap and interstage seal tolerances can only get so small, airfoil shape manufacturing tolerances are more critical on the smaller compressor and turbine blades of the smaller engines, small defects have greater impact).

at the 30-40k thrust bracket, even achieving 60pr is going to be very difficult.

PW already has their 4:1 gearbox in test, so if they do their job correctly, strapping the 4:1 hub and a larger diameter fan on the same core should be relatively easy (certainly easier than doing it all from scratch as RR must do, remember, PW already sells the PW800 on the same core with a 1:1 fan…) and strategic tech insertions in the core can raise PR and TIT significantly

I think BBD feels they can extract a similar gain from aero cleanup of the CS, vs the very mature A320. Any $ they invest will not yield an advantage over E2 so why spend the $. Aero improvements are a better investment for them, while 3% will give A320 an advantage over 8 Max that they cannot replicate unless LEAP does something similar.

Exactly. I think CFM has a lot up their sleeve that they are just waiting to roll out in the face of any GTF update.

I’m pretty sure they’ve already got a GTF design of their own waiting for the right time to introduce it. I think they know that the LEAP is more than enough and has plenty in store to handle PW at this point.

Another bone I think is that Delta is probably using CFM and GE as proxies in their battle with Boeing, so going with the GTF is just another way to continue their little sand fight with Boeing. Aren’t Virgin’s 787s RR-powered?

Delta Tech Services has been experience brand new P&W engines before like PW2000/PW4000 and know it can be a huge volume of work. Most PW1100G engines are on a PWA power by the hour constract and will be sent to Atlanta to be fixed and upgraded en masse.

@Sowerbob:

“…big win is with P&W. By all accounts it will be the engine of choice going forward…”

Apparently, QR is not among those “accounts” U mentioned re “engine of choice going forward”….

“offering better efficiency and critically more scope for future gains.”

I agree but on the other hand, it’s also that engine choice which will take longer to mature in terms of reliability+durability+maintenance intensity, ….ironically, none of those issues is related to the Fan gear system – the star feature of the PW1000G.

“I see AB gaining massively due to this…”

In contrast, I continue to see 320Neo family has a structural advantage in mkt share primarily due to 2 choices of engine manufacturer/design rather than certain inherent tech advantage of PW1000G platform vs LEAP platform.

“..the MAX fatally flawed by, yes you guessed it, it’s short undercarriage which limits it to the LEAP.”

No, I didn’t guessed it because Max is limited to the LEAP not because of ground clearance. It is because:

1. PW did offered a PW1000G version optimized for Max but Boeing turned it down and rather to continue the faithful marriage between CFM and 737.

2. There’s no inherent tech barrier to design+produce a PW1000G variant @ 69.4in or similar fan diameter as a LEAP-B1. PW1200G/1700G are already produced in 56in fan diameter.

” A less efficient version at that.”

Yes, in terms of SFC. No, in terms of weight. In shorthaul missions, lighter weight is generally as great a contributor to overall fuel efficiency gain as lower SFC .

@FLX

Let’s wait and see. As I see it the neo gives choice and with a LEAP equipped aircraft that is hitting performance targets initially missed by a considerable margin on the MAX. The improvements for the MAX variant are likely to feed back into the NEO variant maintaining the status quo advantage if the user opts for the LEAP. It also offers the GTF that promises even greater development potential into the future. So it is hedged both ways with greater efficiency on both applications. I do not see how this is beneficial in any way for the MAX.

My view is that Boeing needed MAX on time, and they achieved that brilliantly but were forced to go with what they knew to achieve that. It does however give a competitive edge to the neo. If smaller, lighter fans were the way to go I get the feeling Airbus would have gone that route somehow or perhaps their undercarriage is too long in your view.

A32Xneo backlog is approaching 6000 units. I’d not be surprised if Airbus would hike up production to 80 per month in 3-4 years time.

Looks like the deal with Pratt & Whitney as engine MRO provider was weighted quite heavily, as well.

http://news.delta.com/delta-selects-airbus-a321neo-narrowbody-fleet-renewal

I don’t understand why people think the planes need to be built in Mobile? There is no tarriff on Airbus planes. They can build these in China if they want.

@Mark: The don’t “need” to be built in Mobile. They just will be.

At Sept 2107 there were 1440 A319’s in operations, The most noticeable US operators are AA (125), UAL (64), DAL (57) and Spirit. The CS300 have comparable seat capacity and range of the A319.

If the CS-aircraft remain blacklisted in the US it can create a sticky situation as the CS3 is a near perfect 319 replacement.

The 319NEO has become an orphan, AB is running out of capacity to deliver to build more 320’s (?), so US airlines could be forced to look at MAX7/8’s as replacements.

The E195E2 could potentially serve 319 routes but have range and cargo restrictions. Assuming the AB-BBD CS ventures continues I can see hard push to market the CS300 to take pressure of A320 production.

If you consider that the A319 takes up the same full production slot as an A321, then yes, why not sell CS300 and even CS500 and ship those hugely profitable 321s!!!

If there are delays with deliveries of the CS100’s to DAL was wondering if they are considering to change the entire order and options to CS300’s?