Leeham News and Analysis

There's more to real news than a news release.

Leeham News and Analysis

Leeham News and Analysis

- Does an A220-500 need a new wing and engines? Part 4. July 3, 2025

- GE testing of giant GE9X engine aims for maturity at entry into service June 30, 2025

- Bjorn’s Corner: Air Transport’s route to 2050. Part 28. June 27, 2025

- Parent agency, FAA often at odds as politics outweighs safety June 26, 2025

- Electric Flight and the Ugly Duckling June 25, 2025

Is Long-Haul LCC viable? Part 3

By Bjorn Fehrm

April 11, 2018, © Leeham News: In the second article if Long-Haul LCC is a viable business, we described the cost items which have to be part of a Revenue versus Cost analysis.

In a subsequent article, we used our performance model to develop the typical costs for the aircraft types we study. We now look at these typical costs, discuss their background and relative importance.

The Long-Haul LCC costs

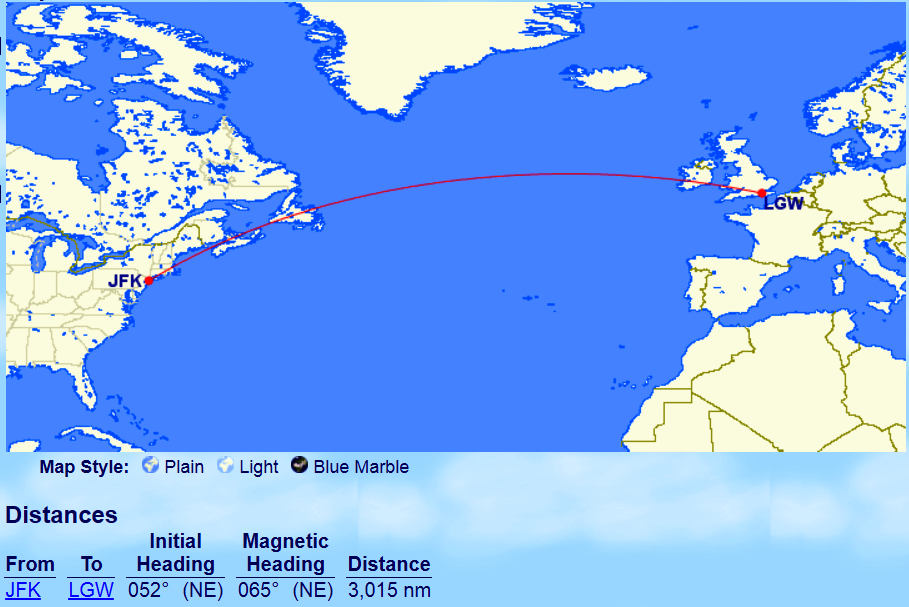

With our performance model, we have developed the typical costs for a modern Narrowbody (Airbus A321LR or Boeing 737 MAX 8) or Widebody (Boeing 787-9 or Airbus A330-900) when flying New York JFK to London Gatwick, Figure 1.

Total costs

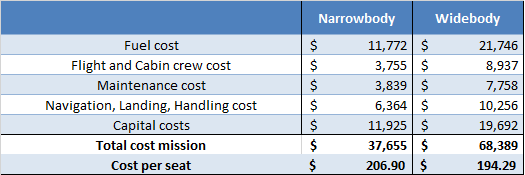

The total operational costs for our Narrowbody or Widebody aircraft for the mission is presented in Figure 2. The fuel is calculated with the present fuel price, which hovers around $2.00 per US Gallon.

These costs are the about the same for each mission over time unless winds change the fuel costs or special pricing from airports can reduce our landing and handling fee costs during the less busy winter months.

The Narrowbody and Widebody costs are the averages of the aircraft under study. This introduces no skew of the costs as these types were close in the per-seat costs for the route. Our mission is to see if we can generate enough revenue on such routes compared with the typical costs and to understand the advantages and disadvantages of using Narrowbody versus Widebody aircraft on the sector. Which of the aircraft is the slightly more economical alternative is not part of our investigation.

Figure 2. Operational costs when flying New York to London. Source: Leeham Co.

On a mission basis, the Widebody aircraft have almost twice the operational costs compared with the Narrowbody on the route. This means we need a sizable passenger traffic to cover the costs of the Widebody aircraft for each departure. If the Narrowbody can handle the range of a route, the mixed use of a Widebody and Narrowbody can be the way to handle different daily and seasonable changes in traffic.

The studied Narrowbodies, with an average seat count of 182 seats, is about half as big as the Widebodies at an average 352 seats. We need aggressive marketing and revenue management to fill the larger Widebody to a high load factor for many periods of the year.

Per-seat costs

If we divide the total costs with the seat count, the total per seat costs are close for both aircraft classes, at around $200 per seat, Figure 2.

The Narrowbody, which has the lower trip cost and by it a lower capacity risk, has a 6.5% higher seat cost.

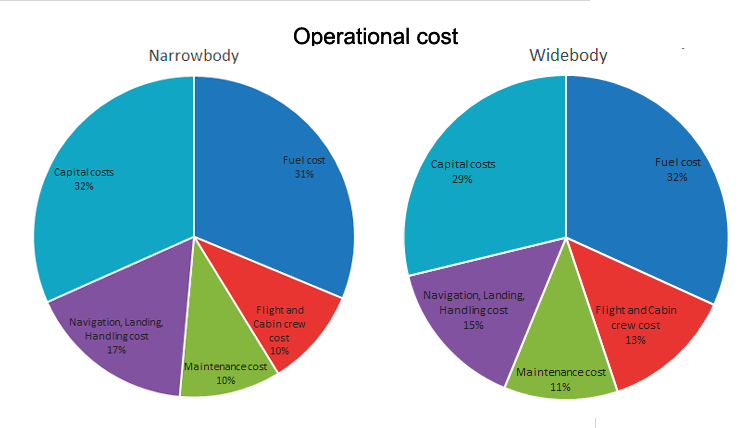

Figure 3 compares the distribution of the cost types between the Narrowbody and Widebody aircraft.

Figure 3. Comparison of the cost distribution between Narrowbody and Widebody aircraft. Source: Leeham Co.

Fuel costs are close between Narrowbody and Widebody, at 31 to 32% of total costs. This was not always the case. The Narrowbody had a higher fuel consumption per seat (and inadequate range for any long-haul flights). The closing up of fuel costs is a development which has come with the A320neo and 737 MAX generation.

The engine specific fuel consumption of these aircraft is close to the engines of the Widebody aircraft. This comes from the new Narrowbody engines having increased the By-Pass Ratio (BPR) over the replaced generation more than the new generation Widebody engines.

The A320 and 737ng engines had BPRs of ~5. The new generation has more than doubled the BPR to between 11 and 12. For the Widebody engines, the BPR went from 5 to between 8 and 9, an increase of 70%.

Capital costs are the second most important cost item for a Long-Haul LCC. The shown costs in Figure 2 and 3 are typical for a smaller fleet of aircraft, rented ( Operationally Leased) from a Leasing company.

Should the airline buy many aircraft in one go (like Norwegian Air Shuttle and many other LCC’s have done) and do a sell and leaseback transaction, the Capital cost part of the pie would have been smaller. We can, therefore, assume our cost level for Capital costs are a worst-case scenario.

Third largest cost item is Navigation, Landing and Handling costs. The Narrowbody has a 2% higher cost fraction, mainly because Navigation fees don’t scale linearly with Maximum Take-Off Weight (MTOW).

Maintenance cost fractions are within 1% of each other. The dominant costs for maintenance are engine related costs. They dominate airframe maintenance costs with a two to one ratio.

The Flight crew for the longer range and more capable Widebody aircraft has a higher salary than the shorter range Narrowbody aircraft. This explains the difference in Crew cost fraction. We researched the crew costs of a Long-Haul LCC ahead of the article series, its about half of the Legacy carrier’s cost.

Total cost for the airline

As explained in the first article, the aircraft operating costs are about 90% of an LCC’s costs. We shall, therefore, add 10% for Sales, General and Admin costs to these figures to get the airline cost for operating the route.

Next article

In the next article, we will take the developed costs and calculate the revenue we need to cover these costs. We will also discuss the ticket and ancillary services pricing strategies we need to cover the costs over the year for the route.

Is the cost per seat based on a 100% load factor

Yes, it’s the total mission cost divided by the seat count. The load factor will come into play when we talk about the revenue of the flight in next article.

Very interesting Bjorn. I have a feeling the NMA has relevance here. i.e. What is the sweet spot where good load factors make you money with biggest narrow body possible or the smallest wide body.

Interested to hear what you have to say on revenue side of things.

Regarding costs — some numbers to add into your model.

LH-LCC going for the niche market — very niche market.

Glesga to the Eastern seaboard + Rust Belt.

Using 2006 vintage A321s at today’s market value.

Add in a $2mill upgrade to bring the interior up to date and pay for a snazzy paint job.

Fuel for 2,800 NM average flight @ 17T’ish = $11K.

Crew at GB rates / 2 plus 6 per flight = $3.5K.

Leasing cost per flight @ 56 flights per month = $12.0K

Made up of two components:

Aircraft — dry lease? — cost per flight = $7.5K

Maintenance cost per flight = $4.5K (seen as high, poss very high)

Charges, fees + Stuff per flight = $5K (again seen as high).

Lower cost airports being used.

Total = $30-32K per flight.

Revenue side with 16 Business / 24 premium economy / 132 economy = 208 economy equivalents.

Target destinations:

New England — Boston + AN Other.

Rust Belt — Detroit, Cleveland, Pittsburgh.

Colonial — Washington, Philadelphia.

Old Canada.

3 / 4 / 5 flights per week using 4 aircraft.

Worth a punt?

Really well laid out. Area I have long been curious about (having seen Freddy Laker and the (assisted? ) failure of the first LCC LH.

I would like to see the seat count in Chart 2.

Puts the per seat number in the right perspective that had me scratching my head until the explanation.

I thought the engines for the narrow bodies couldnt compete because of the pressure ratio mattered on long haul?

I was recently reading about a US 757/767 captain who rode jump seat on a 737 flight from Boston to SanDiego. He was amazed at the length of runway required for takeoff and the stepped climb to get to cruising height, which was often limited compared to what he could do in a 757 .

“faster climb”

If you use 30% more fuel that is easy 🙂

Thats not what I have heard, step climbs are less efficient overall. Sometimes required for ATC reasons.

Then there is the small wing and heavy weight meaning a higher altitude isnt achievable at all. Obviously this is comparing trans continental flights as shorter hops have different charcteristics

There are a lot of variables that matter beyond engines in takeoff and climb performance. Chief among them is the wing- larger wings typically provide more lift which gives better performance. The 757 has a large wing for its size (compare its wing to the similarly sized A321). Coupled with the more powerful engines and the 757 is famous for its great takeoff performance.

dukeofurl: They go as easy on the throttle to extend engine life and lower that very high costs to overhaul.

Add in the computed aspects of climb, weight and best efficiency at what speed.

Its a whole different era!

I remember my first ride on a jet (DC-8). It left the ground the pilot cobbed the throttles and we went up to 35k like a fighter jet (non controlled airspace in those days, no 250 knots under 10k)

My brain is screaming stall, stall, stall (not a prop job could do what it did, even a P-51)

Its not about fun anymore (and rightfully so) but there is a whole lot more to it than cobbing the throttles and climbing like a banshee.

yes I know its the wing that is too small ( CAT D gates), but the 757 still has the same parameters for throttle use.

But limited by wing and engines to lower cruise altitude !

http://www.askthepilot.com/757-v-737/

Hello dukeofurl,

Regarding: “I was recently reading about a US 757/767 captain who rode jump seat on a 737 flight from Boston to SanDiego. He was amazed at the length of runway required for takeoff and the stepped climb to get to cruising height.”

Do you have a link to where you read this? I am curious about what airline is not using step climbs with 757’s and on which routes. Over the last several decades, the airlines I have flown, mostly in the US, uniformly used step climbs to save fuel on routes over 2,000 miles, and usually used them on routes of 1,000 to 2,000 miles, no mater what aircraft model they were using on the route. For instance, for the last 2 years I have been flying Delta about once a month between Atlanta and Salt Lake City, which is about 1,600 sm or 1,400nm, and except for when weather was dictating altitude changes, the general pattern, no mater whether the aircraft being used was a 737, 757, or A321, was direct climb to an initial cruise altitude of approximately 32,000 feet then climb in one or more steps to a final cruise altitude of approximately 37,000 feet. This is done to save fuel, since optimum cruise altitude increases as aircraft weight decreases. Optimum cruise altitude is to a pretty good approximation the highest altitude at which the engines can efficiently develop just enough thrust to maintain the most efficient cruise speed, which will be below the highest altitude that could be reached and maintained at less than optimum cruise speed. I do not doubt that a 757 loaded for a trip between Atlanta and Salt Lake City could reach any given altitude faster than a 737, and could climb directly to a higher altitude than the 737, but on my trips on this route over the last several years, Delta has pretty much always used step climbs and very similar altitudes for both aircraft. The flight tracker on Delta’s seat back screens makes it easy to tack altitude changes.

For anyone who doesn’t believe me about step climbs being a fuel saving strategy, see the excerpt below from a Wikipedia article on step climbs which may be found at the link after the excerpt.

“Since the early days of jet aircraft and commercial travel, the technique of gradually climbing in cruise altitude as fuel burns off and the aircraft becomes lighter has been widely used by pilots. The altitude that provides the most fuel-efficient cruise at the start of a long flight, when the aircraft is fully loaded with fuel, is not the same as the altitude that provides the best efficiency at the end of the flight, when most of the fuel aboard has been burned. This latter altitude is usually significantly higher than the former. By climbing gradually throughout the cruise phase of a flight, pilots can make the most economical use of their fuel.”

https://en.wikipedia.org/wiki/Step_climb

Wondering if I might have missed a correlation between aircraft type and cruising altitude on Delta flights between Salt Lake City and Atlanta, I looked through a stack of old boarding passes, on which I write notes about routes and altitudes during flights on which I am awake and bored. I found eight boarding passes with complete notes for the whole flight from SLC to ATL , of which 5 flights were on 757-200’s, 3 flights were on 737-900ER’s, and one was on an A321-200. I still can’t see any clear correlation between aircraft type and cruising altitude on this route. All except one flight used step climbs and the flight that did not step climb was on a 737-900ER. On the 757 flight on 10-9-17 that initially leveled off at 27,00 feet, there was some very unusual weather. For part of this flight there were 80 to 90 MPH headwinds at cruising altitudes instead of the usual 80 to 120 MPH tailwinds when flying from SLC to ATL.

See below for my notes on these flights. The flights are sorted from lowest to highest initial cruising altitude.

Date / Flight # / Aircraft Type / Reg # / 1st Cruise Alt. /Final Cruise Alt.

10/09/2017: 147 / 757-232 / N680DA 27,000 37,000

02/26/2018: 147 / A321-211 / N303DN 31,000 35,000

04/02/2017: 147 / 757-251 / N557NW 31,000 37,000

12/27/2017: 147 / 737-932ER / N852DN 33,000 35,000

02/04/2018: 147 / 737-932ER / N860DN 35,000 35,000

04/09/2018: 14 / 737-932ER / N846DN 35,000 37,000

11/26/2016: 14 / 757-251 / N535US 35,000 39,000

05/08/2017: 1121 / 757-251 / N539US 37,000 39,000

Thanks AP, must admit you are a man of above average detail. Just had a look at the 757’s production list and was interesting to see that AA has a large number of 757’s listed as stored.

With Bjorn’s series on LH-LCC’s was thinking someone can still use some of them for a few years, those were real toughies but engines might be an issue?

Flightaware and similar can give you climb characteristics for specific flights/plane types.

Worth looking up?

Just looked up on Flightaware a United 757 from SFO to BOS, the altitude graph on the scales shown was pretty much a straight line up to 10,700 m and then showed the ATC centres as it crossed country

Hello dukeofurl,

I just noticed that you had already posted a link to the article you were referring to.

One element is missing from the calculation and this is aircraft utilisation . The same 737 which does a long haul sector can be integrated into the short network . Revenue of airlines is dependant on how many hours their aircraft is on the air and makes money for them. Aircraft which fly long haul often wait many hours idle in the airport waiting for the departure . They can’t just return back after half an hour ( as many LCC aircraft do) because their arrival time is not convenient departure time from marketing point of view. This means less utilisation . A 737 or A320 who does ,lets say , 10 sectors of 1 hour a day carries potentially 1600 paying passengers per that day. Far more then an A380 who does a 10 hours sector and then just wait idle for his time to return.

It’s “Is Long-Haul LCC viable?” not how financially viable are smaller narrow bodies compared to long haul super twins. Way off topic.

short hops reduce utilization. Doing 10 sectors over the day will not show much more than 6..7 hours of flying time. ( 10 times pax rotation and taxi time already adds up to 10+h.)

A380 tend to go well beyond 10hours ( more like 12..14h/d ) of daily utilization.

Distance traveled is much higher for the long range craft.

Take a look at Icelandair and their 757 operations, it will be the most similar ops to a mix of long haul SA operations. They are pretty successful with long Life on wing for their RB211-535E4’s that can take close to 10 000 cycles on wing making the maintenance cost very good, their 737MAX will be even better with cheaper Engine PBH agreements and cheaper Aircraft Heavy maintenance compared to the 757’s continuing their success.

Iceland is special.

It’s geography is something that can’t be replicated unless Atlantis turns up.

They are a ME3 Aggregator / Distrubutor in miniature.

Balanced approximately on both sides so that they can mix and match aircraft depending on their needs.

Not so much LH and SH.

But short LH and long SH.

Flying pretty long haul with a narrowbody that has reliable Engines is quite economical for them.

This applies as well when you compare 787 with 737NG operations on the same routes, you can do X4-X5 more flights with the best narrowbody Engines on wing than the “Hot Rod Engines ” designed for widebodies.

The core Engine of the 37k RB211-535 is the same size as the 55k RB211-524G, that increase of core flow relative to fan flow and hence lower turbine temperatures makes for the increased Life on wing.

The LAEP-1B might be a bit “Hot Rod” so we will see if it can be as reliable as the CFM56-7B or CFM56-5B’s.

DK:

That assumes the single aisle can be used in the shorter route network.

Its ETOPs configured so all your aircraft would have to be. It would have to be in the right position to do so and return to that position to do the trans Atlantic part.

It might be possible but not a given I would think.

Probably need to address the capability of multi cycles vs long term wear out when using the single aisles engines on a long haul.

I seem to recall that Keflavik was built to handle B52s. Very long runways=great engine life. At one point they held the record for underwing life of a jet engine.

It adds up to 15 hours a day (Ideally). Doable . And 1600 pax (Ideally). Many more than A380. And the cost of the aircraft is quarter or fifth (?) from that of the big bird cost.

When I linked to a story about looking at individual planes and the hours in the air, the 747s were doing trans atlantic ( British airways) so that could be some 737s, still way behind the A380s hours for Qantas.

Max hours per sector would still be something like the Silk Air Max 8s doing Singapore -Hiroshima at 6 hours flying time.

When airlines talk about utilization they just really use as a stand in to talk about how many fresh loads of passengers ($$$) they can get a day, with the understanding that higher utilization typically means more passengers. They don’t really care if the plane is in the air or taxiing to the runway (they count that towards utilization)-actual flying time doesn’t matter that much. As long as the plane is not parked sitting empty.

Yes, you charge per flight not nautical mile. Hence some Airlines doing lots of short hop flights have terrible cost per CASK but great Revenue RASK, so the number of cycles makes a difference when comparing cost numbers of different airlines and what a new bean counting CEO could promise the share holders..

According to this Swiss Air is doing up to 10 legs and 17 flight hours on their C-Series.

https://www.skiesmag.com/features/time-departure-c-series-service/

That dog don’t hunt.

Or at least it will need a good trainer.

First you need a LCC with both LH and SH routes.

Plus you have the main transatlantic route generating 14 or 15 hours in the air every day — 98 / 105 hours utilisation a week.

Depends on the route map — not every flight will go to NYC.

Plus 110 hours utilisation is considered good in LCC circles.

Leaves you room for 1 SH flight per day — how do you get back?

Or you push it to 2 SH flights per day and pray for no delays.

Southwest is the ideal airline for such an endeavour . They have huge domestic network which they can extend westward towards Europe and the have the right equipment . (737-7 is going to have 4100 NM range enough for East coast to the heart of Europe.

“Leaves you room for 1 SH flight per day — how do you get back?

Or you push it to 2 SH flights per day and pray for no delays.” Take off from Germany at around 05AM and you reach the East cost very early in the morning having a full day until an evening flight back to Germany. You will need though LCC operation in Europe so your planes won’t get stuck there on the airport waiting.

“…westward towards Europe…”? They must be planning to take “the long way around”! LOL

I am glad non of the rest of us makes mistakes like that!

DK: happens to me all the time.

Probably a 787-8 though, that seems to have the range and pax balance that works.

For someone in Israel , Europe is alway on the west…

A US/Canada operator doing 737MAX flights to UK/Ireland/NorthWestern Europe can cross the Atlantic at around 6-7pm (instead of a red Eye domestic flight) arriving 6-7am in the morning GMT, then a turnaround to do a return flight 7.30-8.30am arriving in US/Canada 7.30-8.30 am local time (same flight speed as the sun over the horizon), hence you can do some domestic flying from 9.30 am until you get to prepare for the 6pm night flight. So how to best use a 737MAX from 9.30 am to 4.30pm?

You can make one sector of up to (lets say) 4 hours flying time along the Eastern coast arriving to a destination that is on the transatlantic range to Europe and operate the return flight ( to Europe ) from there or you can do 2 short ( up to 2 hours ) deeper westward USA and return to start preparing for the flight to Europe. I think we are talking about close to 24 hours utilisation of the equipment.

BOOM! The flexibility the narrow-body offers once the aircraft has done it’s TranAt/TransCon adds to it’s overall value within the fleet.

AerLingus often use their a330s on an early morning ‘sun route’ after landing in Dublin at 5am from the US, returning again fr their journey back to the US. When their a321lrs come next year.. you could see them being used on early morning business-heavy routes, offering proper business class to LHR/CDG/FRA/AMS etc. for those US connecting passengers going onto Europe [so they don’t have to suffer the shock of regular euro-seats [from the Vantage lie flat business they got used to].

I think the a231lr and the like will be the real – opening new low-volume direct routes – the 787 was designed to be. The 787 of today is really an a330 replacement – kinda.

Not sure that AB management fully understand the potential of their A32X NB platform / component set.

New wing on a A321 with a new wingbox will take the nominal range out to 4,500 NM at the same MTOW.

New wing / wingbox / general diet = 2.0T extra fuel or 8/9% increase in range.

New “LH” focused wing with loads of CFD should generate another 5% improvement.

Just a start — any thoughts on a A322 / A323 at 55T OEW and a 50M fuselage should get another 24 passengers out to 5K NM nominal range with appropriate hotel functions for a 10/11 hour flight.

The mood music from AB HQ does not sound great at the moment but the potential is there.

Yeah it’s disappointing to hear as a ‘fanboy’ but AB can move quickly once Boeing show their cards (officially). And a new wing… Bring it on. Needed regardless of a NMA – one ‘wing’ to rule them all – hehe.

On the positive side though, if they can’t get neos out the door at a good rate further updated models will just add to the problem. The new management team need to be more Leahy/Positive when talking though… They come across rather muted and downtrodden… And it’s not coming across well in the media. You’d think things were going badly, when things are booming.

Airbus just blinked and put the A321++, A320+ on hold. They claim too much work to do in production, but it smells that they want a new Engine derivative for the for the A321++ otherwise Airlines will not pay up the extra $millions and the American Engine manufacturers for the neo are not yet cash positive on the neo to dig Another $1-2bn into a 35-37k derivative Engine.

Fergal: The 787 is doing a lot of new routes, its just not the point to point.

Its from a major hub to a miner one (Japan – Boston, Japan – San Jose)

The versatility is its an outstanding A330 replacement a the sales show as well (grin)

Did they blink on the ++?

Article I saw said the + was off but was a bit ambiguous and I couldn’t tell if the ++ was off as well. I would be surprised if Airbus did both with only three or four years in between so I thought it probably inferred that they have privately decided on the ++ alternative. There was also a statement from somebody in AB not long ago saying the A320 platform was about MAXed out and major changes would be needed to get more out of it.

This could indicate a few things. At current rate of sales the 32XNEO’s production sold out for many, the cost of an 321++ (322, CFRP wing, etc?) will be high and only warranted with Ultrafans which is effectively an “all new” aircraft. Could possibly see low cost tweaks of current wing as an in between stage?

Another “or”, the 321LR proves to have better range than expected and could further been improved at low cost?

….or, has AB decided to build an MoM (twin-aisle) of their own?

The maintenence cost difference is very small.

In real Life I think the difference is bigger due to an expected Life on wing for a 737Max is around 15 000cycles and for a GEnX 3000cycles for these routes, so the Power by the hour rates and fully QEC’d spare Engine cost jumps up for the widebody as you need more expensive spare Engines, (like Trent 1000’s). The narrowbody aircraft can also be swapped to do high daily cyclic flying and another 737MAX8 take its place.

The flight crew for the 737’s will be more available and they can finish their weekly schedule with a pair of long haul flights taking turns dozing off at Cruise altitude per EASA/FAA rules.

And better inventory costs if you’re already a narrowbody operator. You hardly need any new inventory for the long haul in that case, whereas you need plenty if you opt to take on a widebody. Particularly engines.

Bjorn’s analysis is not flattering to the widebody – the entrepreneur can move passengers at the same cost for far less risk if he/she operates the service with a narrowbody.

Interesting point gonna be how the “comfort” will be feel by passengers traveling TATL on a narrowbody.

With the same seat pitch — and 9-abreast on a 787 — the comfort really isn’t all that much different. Comparing 787 and A321LR, for example, the former will have the new interior and some more humidity, but the latter will have somewhat wider seats.

And as has been noted many times here in the past, most pax choose on price and have no idea what kind of aircraft they will be flying on.

Yes. The plane that gets there on time is the one they prefer.

It will be a DC-8 recall for some but with todays seats and herringbone arrangements it can be done ok, not as nice as in a widebody but you do as good you can with the space you got and your asking ticket prices reflect that.

Not so easy to swap a/c long haul when it involves ETOPS.

As well as the other fit in factors like timing. crews etc.

I think AK has made all the US-Hawaii capable part of the fleet ETOPs so they can plug in any one of them.

I wish Bjorn, or someone “in industry” here, would comment on ETOPS cost. I understand it’s quite costly re: airline qualification, adequate qualified crews, ETOPS qualified a/c maintenance, and a/c history records/tracking. There’s little direct, internet, “open source” info on this topic. (Maybe understandable, based on sensitive, proprietary nature of much of the information?)

It appears that you, MO, like many enthusiasts think ETOPS is something very complicated and barely achievable due to cost.

I have been flying ETOPS for 29 years. Transatlantic. It is just a set of rules which cover equipment requirements, maintenance requirements (recordkeeping mostly) and crew initial training and procedures. Nothing really complicated, and in todays (EASA) environment that requires a lot of record keeping anyway. For simplification in the fleet I operate, both the ETOPS and non-ETOPS aircraft are under the same maintenance program.

That would make sense, the alternative of a ETOPS sub fleet can cause problems.

https://onemileatatime.boardingarea.com/2015/09/11/oops-american-accidentally-flies-wrong-plane-to-hawaii/

Claes:

“The flight crew for the 737’s will be more available and they can finish their weekly schedule with a pair of long haul flights taking turns dozing off at Cruise altitude per EASA/FAA rules.”

I really don´t get this…

Many crews fly irregular hours from early morning flights to late arrivals with some downtime in between, other days stand-by in the morning and fly afternoon/evening.

Doing that for some time and move from hotel to hotel gives you fatigue especially as years go by, often your significant other is also in the airline business putting on additional strain. In some countries pilots are the #2 occupation to divorce.

So being offered a trans Atlantic flight were you are allowed to put in a few hours legal sleep behind the Wheel while your buddy do the monitoring can be relaxing and put you in a good mode when finally done with your block of work.

I remember years ago World Airways used the same 747 crew flying to Europe and do the return flight as well.

Claes, in short, what you write is bollocks with FTL rules and controlled rest. No one is “standy in the morning and then flying in the evening”, at least not on the European side.

The rules for EASA is here, https://understandingeasa2016ftl.files.wordpress.com/2014/04/easa-combined-ftl.pdf

Good points, I think this is the type of thinking BA has in mind with the 797.

Interesting numbers — as an outsider I had no figures for the “Navigation, landing, handling” or NLH costs.

Couple of elements still to be included — cabin segmentation in a LH-LCC environment.

Are all the seats you mention the same class?

Or are they a mix of styles and pitches with different revenue ratios?

Using an A321 as an example:

Business @ 24” x 48” pitch / RR of 2.5 or even 3.

PE @ 18” x 40” pitch / RR of 1.5 or 1.75.

Economy @ 18” x 32” / RR of 1.

Poverty spec @ 18” x 32” carryon only / RR of 0.85 or 0.9.

182 seats then can be arranged to generate revenue equivalent to 200 economy seats.

Also what range of routes are you looking at?

3,999 NM = 50T of OEW and therefore a choice.

4,001 NM = 125T of OEW only.

This is why I think the MoM’ster at 5K NM or better still 6K NM range nominal is important — the aviation industry only currently has two has two hammers in its tool kit.

Not a very flexible tool kit.

Finally what about reality?

What you can get today for service tomorrow?

A330 – 200 or A321 economics for the here and now?

Not only do narrowbody aircraft have less efficient engine, their lift-over-drag ratio is worse. This is due to physical reasons (Reynolds-Factor), and partly design reasons stemming from the short/medium range heritage.

The gap is about ~10% (read: NB have 10% worse LoD than WB).

Because of the number of aisles? Or the fuselage diameter? Or fuselage length? Or wing size? Please do provide some more details for those of us who are not aerodynamicists.

In the end, though, the fuel burn per seat doesn’t appear to be all that different, though.

given that I regularly see round trips east coast to Barcelona for ~$350 they must be making bank on ancillaries and demand based variable pricing.

That would be part of it (or maybe the ROI).

Be interesting to see if that gets added in and a good point and not a clue how much.

Love all this techno stuff. I just need more gin on my flights. How is that factored in per seat/passenger 😉

A factor that will no doubt come into play in a future corner on the revenue side is freight – widebody has much more scope to generate revenue in the belly.

Only if they can sell it to the less likely destinations.

Another one to add to the questions worth fining out the answers on.

Maximum range numbers we see published and most people here would think about are for passengers and their baggage only.

How much freight business will LCCs realistically do?

If they start taking major business away from legacy carriers, there will be a lot of freight that needs to get moved.

Almost none. The rule used to be that pax pays 7 times better per lb than cargo.

Interesting. Why were so many knocking the A380 for having relatively little cargo space below?

Yes, cargo is icing in the cake, but since you need to fill and Aircraft +63% of seats to break even everything above is your profit, hence you want to load up cargo when you are not 100% full with pax.

If the A380 only had 2 Main Landing Gears of Convair B-36 size that would open up space from one Landing gear bay to cargo space. Now many early A380 operators are redoing their passanger cabins for +$30M each and add more seats, 7-10 years from now they are ready for a A380neo or redo the cabins one more time on their old A380’s.

The A380neo might be a stretch as well to make it 80.00m long and new RR Ultrafans with a new more slender carbon wing and suitable pylons. Airbus schedule is more or less determined by Emirates, they cannot fit the showers into their new 777-9’s making for new A380’s as time goes by and the move to DWC Al Maktoum International Airport is decided that would require “The mother of all TAX FREE shops” to have pax transfer there instead of somewhere else (like Qatar). If Emirates decides that 100 new neo’s are better than redoing the cabin on 102ea old A380’s it might happen after Enders is gone and Tim Clark makes his last mega order.

Thanks Bjorn. The the real life question is load factor, its likely easier to fill a single aisle which will expose the airline to lower risk. If you can get a “bumper” route and fill the wide-body you can make money but will most likely have to fly from and into Tier-1 airports with related higher landing fees, etc. to do it. The single aisles maybe better for Tier-2 airports?

While it’s cutting back to summer only going forward, this comment made me think of Norwegian’s 737 Boston to Cork service. Apparently, the bookings are strong for the summer season. Strong enough, that they’ll probably add New York to Cork service, also. So maybe even “Tier 3”, on one end at least! LOL

And having seen the Tour and charter operations snap up 787s there has to be a return involved (they did get good deals as they were early orders).

Another question/variable is oil/fuel price. The current tensions in the world has made the oil price/market nervous.

Nothing new there, it all goes up the same and the LCCs LH have newer fleets versus the older mixed fleets of the majors.

Hi Transworld, you to fast today.

The majors however have the ability to ride the storm and “bully” the LCC’s by offering full or near full service economy seats at prices that is effectively not much above that of LCC’s when you add all up.

Try to bully Ryanair for flights in EU. Not so easy anymore. I agree when the LCC are small and poor, but the ones building up a good pile of money and are over a certian size it gets hard. Just see what SWA had to fight before it grew to todays size.

Your numbers can’t be correct:

Fuel: Your figures don’t match with your previous numbers for new-generation aircrafts divided by pax, by a great margin (A321 2.2t/h, A339 5.4t/h, A351 6.8t/h).

Crew: How can the crew cost be higher per seat on a larger aircraft? The opposite would seem to make more sense.

Capital: Since when is a widebody cheaper than a narrowbody per seat? Well, it is not.

I don’t get it.

Fuel

The fuel burns in tonnes per hour are the figures you mention for the A321LR, a tad lower for the MAX 8, 789 and 339.

Crew

I have researched the cost and done the numbers. And I know how you must staff you aircraft for the route. Please do them and come back and tell me what is wrong?

Capital

Give me some numbers before you issue such blank statements. I know the leasing market for these aircraft. The costs are market conform, but as said a bit on the high side for a large fleet LCC. The difference between the aircraft types are real.

Then your previous statements must be faulty. I don’t know very much at all, I just noticed that your numbers are mismatched with other claims that you’ve made. But if you want, I will provide the numbers, no problem. I just don’t understand why, you provided them in the first place. And really, your calculations are obviously wrong in this case, an argument about that really seems to be redundant.

One would think economy of scale would help flight crew costs, but apparently the cost structure holds the reverse to be true.

Theoretically the per passenger cost would be smaller for a larger plane, $2,000/200p = $10/p vs $2,000/400p = $5/p

In reality, $5,000/400p = $12.5/p

Is the per passenger flight crew cost higher on a 500 seat A380 than a 100 seat E190, for a similar 2 hour flight. Are A380 pay rates more than five times higher.

More crew required on larger aircraft — and with higher salaries.

OT, but interesting. I’ve read on a blog recently that BA’s brought its 87-8 afterbody fabrication/construction totally in line with that of the 87-9 and 10. So, maybe, slowly but surely, they’re continuing to “ride down the cost curve”, and will make the 87-8 great again? (I.e. Make it a relevant, competitive product that they can sell in today’s market.)

Must mean the hybrid laminar flow control over the tail fin is now on the 788.

https://www.flightglobal.com/news/articles/farnborough-aero-secrets-of-boeings-new-dreamliner-401784/

Dont think they will need the extra flap settings on the wing though. That seems to leave only the ‘old’ 788 cockpit design where they used titanium. Some other structural parts seem to have changed from Ti to Composite

Thanks for the link, very interesting.

The seat count looks a little low for LCC on an A321? JetBlue for instance takes 200 passengers at a combination of 32inch and 38 inches. I accept it might be a little less than long haul in that configuration. By contrast Norwegian takes 340 seats at similar average pitch in its 787-9’s.

As long as you don’t need to go over 3500 nautical miles or so, the A321LR looks to be the perfect low-cost longish haul plane. Stick a new wing on it and it will be unbeatable across the piece, I suspect.

JetBlue removes six rows of economy seats and replaces them with 5 rows of economy plus seats.

6 x 32” becomes 5 x 38” plus shrapnel.

That gets you 30 “business class” seats.

The other 12 come from the two rows after exits which have a longer pitch to suit the de-planing regulations.

That sizing is closer to premium economy to my mind.

Means that 206 seats @ 32” pitch becomes 200.

Not sure what the uplift is on the new posher seats?

1.25 = extra 1.5 economy equivalents

1.5 = extra 7.5 economy equivalents

Plus the windfall of the exit seats.

Business class should be 4 abreast @ at least 40” pitch.

The example I used above had business at 48” pitch.

AerLingus will have something like 12 Vantage business [same as Jetblues Mint] and about 170 economy in their LRs. TAP has similar type seat count – see it here: https://goo.gl/images/pkrn5N

I’d imagine JetBlue et al would have a similar layout.

So for more traditional full service carriers these would be the numbers. For LCC you’d be around the 210/220 if they have a PE/Comfort or Business-ish class.

Also… The ‘coming soon’ Vantage Solo – may allow for the same # of business seats in a smaller space. http://www.thompsonaero.com/seating-range/vantagesolo/

I can see this being popular if executed well – which they tend to do. The vantage is a very popular business seat.

It comes down to how you do seat counts and make that tricky apples to apples comparison. Based on a slightly denser configuration on A321 and B789 planes, it looks like the narrow body would come out ahead on a seat basis using Bjorn’s figures.

In terms of how close we now are in efficiency between wide-body and narrow, when you factor in the newer-newness of the longhaul aircraft and LH optimized wings etc. vs. the older SH wings of the narrowbodies – you can kinda foresee a re-winged a320/321 ++ [or whatever they call it] as being quite the achiever, even with current engines and a PIP.

They really have achieved a lot.

The 321’s wing is not ideal for longer missions. Think AB’s “problem” is that the market for 3500+Nm is not that big and “niche” to some extent.

For an 322 or 321+LR to be competitive with an 797-type aircraft in future it will need an 30 degree sweep (?) and 40m high aspect ratio wing? This will cost “big” money that could put you a long way towards developing a clean sheet MoM or FSA.

Should read, …market for 3500+NM SINGLE AISLES is not that big…

New wing , in carbon , wont really be “big money” if they use their new partner Bombardier’s design and their factory to make it.

I think Airbus did the design and calculation than asked LH, AF/KLM what they would pay for them with present neo engines. Seems they did not swallow it and when Airbus showed LH the PW1135G on it they most likley responded that they had problems keeping 27k PW1100G’s in the air right now and could see the troubles a PW1135G had to go thru before meeting LH expectations.

I agree it is a good opening for RR to make a 37-40k engine for an A322 and A321++ and reuse its core with anonther fan and gear ratio for the 797 50-55k engine that can run hotter as it will do longer range flying on average. That would get LH attention espcially coupled with a license to do MRO of its engine at N3 engine services for most of the EU operators.

Last people you would ask is existing ‘mainline’ and widebody transatlantic carriers. They dont want to give competition opening

Silkair is doing 6 hr flights with Max8s now from Singapore to Hiroshima in Japan.

Asia is where a bigger A321+ would make its real mark

I’m amazed by the crew cost figures as well,maybe narrowbody crews will start to ask for more money as the distances increase?

Franco,German,Canadian,etc MPA is interesting. New A321 wing fitted to A320 would do great things for range and provide an opportunity to fling some money at Airbus.

IAG/Norwegian deal also very interesting. Apparently Norwegian have been selling off some of their new aircraft.How does this work?In a buyers market,what stops an airline from selling off new aircraft at a profit instead of paying a penalty for cancelling an order?How does Boeing stop an airline from buying Airbus anyway ,having displaced them?Would this be legal?

Well, I think you’re really talking about a seller’s market—given AB and BA have a/c order backlogs in the thousands! And, as I recall at least Norwegian and LionAir have both “over ordered” in the hundreds of a/c, leaving themselves “backdoors” of a/c leasing companies and/or affiliates to offload their “over orders”.

Yes grubbie, 4.61% IAG share purchase not a big amount but a foothold in norwegian, norwegian share prices soared after the news was aired!

I can see IAG being able to help with maintenance costs as they have a facility at cwl for 787’s, but a full takeover, mmmmm not sure on that one.

Some of the articles today strongly intimate Willie wants it “all” in the IAG stable!

“The A320 and 737ng engines had BPRs of ~5. The new generation has more than doubled the BPR to between 11 and 12. For the Widebody engines, the BPR went from 5 to between 8 and 9, an increase of 70%.”

So basically the A340 was ahead of its time? I’d love to see how the fuel burn of an A340neo with four 30k GTFs or LEAPs (using the smaller A330neo wing) compares to an A330neo with two 70k Trent 7000s, or a 787 with two 70k GEnx.

I asked about that some time back, was told the overall pressure ratio mattered too for long haul. So even a GTF engine had the wrong characteristics.

From the historical context the A340 when first announced was ‘supposed’ to get an earlier version of the GTF from Pratt. Development issues put paid to that and GE stepped in with a ‘long range’ version of the CFM, the 5C with a bigger fan. But as the CFM dated back to the 1970s it didnt have the advantages it needed against the GE90

Leap engines BPR range from 9 for Boeings version to 11 for the A and C versions

In reality Boeings version is significantly different to the other two with changes to allow competitive efficiency despite a significant lower BPR ( along with lower max thrust)

https://leehamnews.com/2012/05/17/more-on-the-changes-to-the-cfm-leap-1b/

This story indicates the smaller diameter core is at the heart of the Leap-1B

Of course bringing a GTF to the big fans could be another leap on BPR

But bigger BPR brings more drag and its Pressure ration they seem to be increasing

Interesting article on British Airways eyeing Norwegian.

http://c.newsnow.co.uk/A/933044227?-303:3665:3

See they talking about possibly changing ETOPS from 330min to 140min for 787’s with T1000 engines. Don’t know what engines Norwegian for example are using?

http://c.newsnow.co.uk/A/933183379?-303:3665

Wonder how an A350-1000 will do as a long haul LCC aircraft if you can fill the seats and pay the price?

Calculated that you can get ~430 seats fitted at;

1)E+, 2-4-2, 40-42″ pitch, 100 pax,

2)Y, 3-3-3, 30-32″, 330 pax,

3)Exit limit 440.

http://bloga350.blogspot.fr/2015/02/airbus-announces-18-additional-seats.html

Airbus where looking at improving the 3-4-3 offering to equal the 16.8 inch seating on the 777 classic. As far as I know nobody is interested. That should have great CASM for an LCC. Interestingly the lack of orders tells us that pax do notice and pay for better seating at some point, or else EK would have taken the A359 instead of the 787-10.

The 7double7 — Classic — was developed and delivered as a 9 abreast aircraft up the back. That was the situation for 15 plus years until BA decided that a windfall of 4” was enough to transform it into a 10 abreast up the back in its new NG models.

A case of deja vu all over again.

The B787 was launched at a roomy 8 abreast only to be transformed later on into a sardine class 9 abreast later on — ruining a very capable plane in the process as 8-10 hour flight at this density is a form of torture that the Medieval period could only dream about.

Consequently when will it all stop?

Does the Global airline industry only believe what BA tell them?

17.2” wide seat is horrible.

16.8” wide seat is an abomination.

Where next — the 16.5” wide seat — charter airways special?

Is it not time for some sort of industry or governmental regulation?

Or will we need to wait until there is a statistically noticeable hit to passenger health?

Hello Fat Bloke,

My personal memory about airline seat widths goes back to the 1960’s. In Douglas and Boeing jet aircraft from the 1960’s to the present, the standard seat width in economy has always been around 17 inches. See the vintage seat map fro a United DC-8-52 at the link below. Seat width in economy is 16.4 inches for middle seats and 16.8 inches for window and aisle seats. Seat pitch is economy is a no longer seen 38 inches, perhaps to allow room to place the bodies of those who have succumbed to the health effects of what you classify as horrible and abdominal seat widths.

https://frequentlyflying.boardingarea.com/vintage-airline-seat-map-united-airlines-dc-8-52/

See the seat map below for a current day Delta MD-88.

Seat width in economy is 16.8 to 17.5inches.

https://www.delta.com/content/www/en_US/traveling-with-us/airports-and-aircraft/Aircraft/mcdonnell-douglas-md-88.html

As everyone who reads comments here probably knows, the economy seat width on Boeing 700 series aircraft, of which more than 10,000 have been produced and used widely throughout the world since the late 1950’s is, and always has been, between 17 and 18 inches, the same or a little bigger than it was on contemporary Douglas products. For instance, see the current day Delta 737-900ER seat map at the link below. The seat width in economy is 17.3 inches.

https://www.delta.com/content/www/en_US/traveling-with-us/airports-and-aircraft/Aircraft/boeing-737-900er-739.html

Why do people never howl on this website about unacceptable seat widths on Douglas aircraft the same way they do about Boeing aircraft? Perhaps because Airbus chose not to mention Douglas aircraft in their marketing campaign alleging that a fraction of inch of extra seat width makes a significant difference?

You propose to have governments pass regulations to require that airlines no longer use the same seat widths that they have been using since the 1960’s, about which there was little complaint before a new manufacturer whose products had a fraction of a inch of more seat width started a marketing campaign promoting this difference? Should governments also pass regulations outlawing small economy cars because people cannot be trusted to buy a bigger car if they feel that they need more seat width per passenger? The biggest BMW, Mercedes or Ford models almost always sell far fewer units than the smaller or medium size models, as in the airline industry, apparently many car buyers seem to prefer a lower price and better fuel economy over the largest possible seat width.

Thanks again. Check the B747 that started out largely as a 9 abreast but by the mid 1970s were all 10 abreast. Much the same seat widths as you mention.

Cant remember any squeals of anguish about the Queen of the skies all those years

My B747 memory is 8 years to short to remember the 9 abreast plans of 1970.

For me it was always 3-4-3 up the back.

However you live and learn.

The links below show 3 more seat maps for Dc-9 or MD-80 series aircraft with economy seat widths of about 17 inches.

https://www.seatguru.com/airlines/Allegiant_Air/Allegiant_Air_MD-80.php

https://www.seatmaestro.com/airplanes-seat-maps/northwest-airlines-mcdonnell-douglas-dc9-30/

http://www.seatexpert.com/seatmap/241/Delta_Air_Lines_DC9-50/

I was surprised to notice that Delta’s current seat maps for its 717 and MD-90 aircraft, unlike the above seat maps and its current MD-88 seat map, show 18 inch economy seat widths. See below.

https://www.delta.com/content/www/en_US/traveling-with-us/airports-and-aircraft/Aircraft/boeing-717.html

https://www.delta.com/content/www/en_US/traveling-with-us/airports-and-aircraft/Aircraft/mcdonnell-douglas-md-90.html

Did Delta shrink the armrests, figure out a new way to measure seat width, or change over from legacy inches to new improved and more compact slimline inches? Maybe this was always possible, but in the days before the seat width marketing war 17 inch seat width with a wider aisle sounded like a better idea? I fly pretty regularly on Delta 717’s and MD-88’s on short flights for which I don’t bother to pay more for first class, and I haven’t noticed any difference in economy seat widths on these aircraft, but then I also don’t notice in difference in seat width in economy in A320’s an 737’s, so it might just be the case that my butt isn’t sensitive enough to detect fractional inch differences in seat width. I definitely do notice a difference between economy and first class seat widths, which is typically about 2 inches on DC-9’s and MD-80’s, and 3 inches on 737’s and A320’s.

Interesting feedback — historical angle based on DC and BA going to 6 abreast in the late 50’s.

My point is about incrementalism or coin clipping.

Starting with something that is acceptable and then reducing that standard in small amounts to lesson the outcry or consumer resistance.

My main point relates to the 7double7 where airlines are now converting the classic model to mimic the layout of the NG version. They are significantly degrading the passenger comfort level of existing planes and we are supposed to accept that on the basis that “competitive” forces will sort it out in the end.

Well not really — we have been through this in other areas in the past and it has taken sustained collective action in both political and civic arenas to make change happen.

BA selling the B787 at 8 abreast all the while nodding and winking to those in the know that 9 abreast was waiting in the wings was shameful as it was deceitful.

BA now selling the 7double7 NG as a 10 abreast aeroplane on the basis of an extra 4” of cabin width is just another step downwards in a race to the bottom that now has the owners of the previous generation copying this move on the basis that it would make them uneconomic if they did not — 4” or no 4”.

Such behaviour is unacceptable — to your 1950’s question the world has moved on and if we are to continue to live in the past then why not the 1850’s or the 1750’s?

I’m sure the chimney sweeping industry provided plenty of justification to support the use of children in their industry?

Or the cotton growing industry put up huge resistance at every possible level to justify the need of chattel slavery to produce a harvest economic to them.

However back to the 1950’s — automobile design has changed for the better and government standards have played a big part in that. Cars now are much more spacious and much safer now in the face of many competing parameters.

If Big Auto can do it then so can Big Aero.

It might mean less share buybacks and more R+D spend but it is well within the wit of man to increase the structural efficiency of aircraft by 11% over 25 years rather than decrease it by 11% over the same 25 years.

At some point the camel will collapse — it always has.

Not a case of if, just a case of when?

Another data point — NAS doing Auld Reekie to Upstate NY in a B737 M8.

Interesting on a number of fronts …

Revenue = 186 x Economy seats only.

Very limited ability to upsell any of them.

That is 15% less revenue than is possible from a similar A321.

Or 20% plus less potential revenue than a mixed class A321.

Maybe MO’L has a point after all.

Seat pitch = 31 rows on a B737 / 8 fuselage pointing to a pitch of 29” for the vast majority of the seats.

Tight squeeze on a 1 to 2 hour RY flight.

Borderline human rights abuse for an 8 hour Atlantic crossing.

NAS economics — UBER economics for aeroplanes?

Valuable informations about long haul flights and costs and other concerning issues .You made it more enticing by including quality pics of flight seatings. Really you made great efforts on it. With the help of pictures the information became more understandable for anyone and will surely help them to decide . But, if you can then i would like you to write something in depth about Ethiopian Airlines and ethiopian airlines accra airport office as well including including other services and benefits offered.